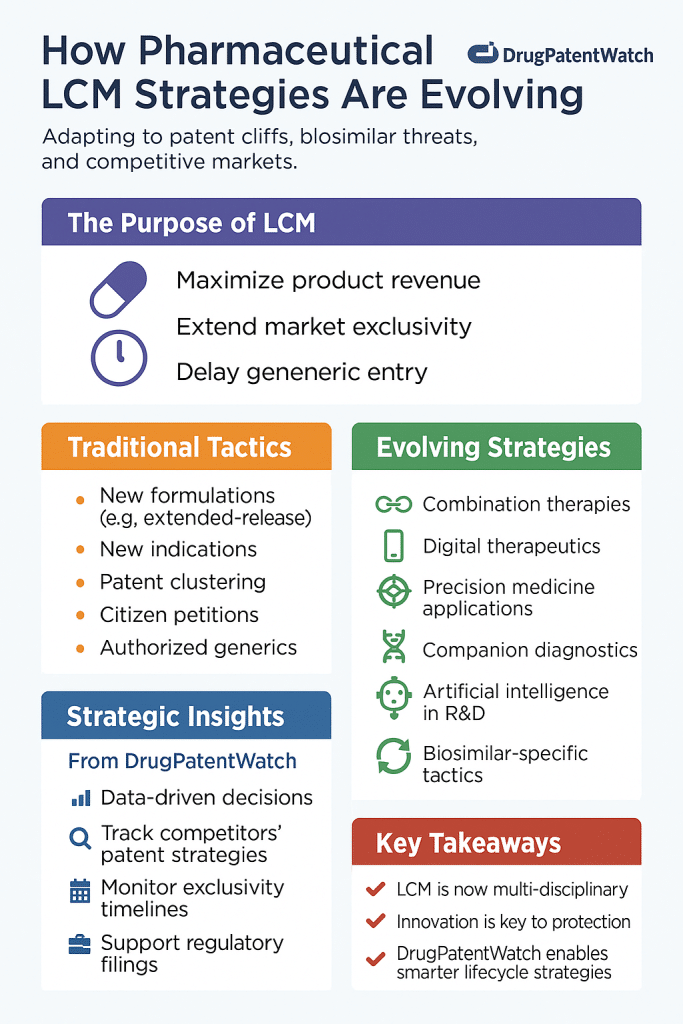

Executive Summary: The Economics of Loss of Exclusivity

In the pharmaceutical sector, the transition from patent exclusivity to generic or biosimilar competition acts as the primary determinant of asset valuation. It functions not merely as a legal milestone but as a fundamental restructuring of market economics, shifting a product from monopolistic pricing power to near-perfect competition. For small-molecule drugs, this transition—colloquially termed the “patent cliff”—typically precipitates a revenue collapse of 90% or more within months of multi-source generic entry. However, the emergence of biologics, complex generics, and sophisticated defensive legal strategies has transformed this binary event into a prolonged, multi-variable erosion curve.

The industry currently faces a period of unprecedented capital exposure. Between 2026 and 2030, blockbuster assets generating over $236 billion in annual revenue—including Keytruda, Eliquis, and Opdivo—will face loss of exclusivity (LOE).1 This “Super-Cliff” represents a massive liquidity event for payers and a strategic crisis for originators. Navigating this period requires a granular understanding of the regulatory mechanisms of the Hatch-Waxman Act and the Biologics Price Competition and Innovation Act (BPCIA), the litigation tactics employed to extend effective patent life, and the commercial leverage exerted by Pharmacy Benefit Managers (PBMs).

The forecasting of generic entry is no longer a simple exercise of tracking patent expiration dates in public registries. It has evolved into a discipline of predictive intelligence, requiring the synthesis of litigation docket analysis, supply chain geopolitics, and regulatory signaling. This report provides an exhaustive analysis of these dynamics, moving beyond surface-level timelines to examine the structural forces that dictate the speed and depth of market share erosion. It integrates legal analysis, economic modeling, and competitive intelligence frameworks to support decision-making for originators, challengers, and institutional investors.

We examine the intricate machinery of the 30-month stay, the fragile nature of 180-day exclusivity, and the emerging threat of “induced infringement” liability that threatens the Section viii “skinny label” pathway. Furthermore, we analyze the divergence between the small-molecule “cliff” and the biologic “slope,” driven by the opaque arbitrage of PBM rebate walls.

“Between 2025 and 2030, blockbuster drugs representing an estimated $236 billion in global revenue are set to lose their patent protection, unleashing a flood of low-cost generic competition.” 3

The Regulatory Architecture of Market Entry

The timing of generic entry is rarely determined by the statutory expiration of a single patent. Instead, it results from a complex interaction between regulatory exclusivity periods, patent litigation stays, and the adjudication of intellectual property rights. Understanding the statutory machinery is the prerequisite for accurate forecasting.

Hatch-Waxman Mechanics: The Paragraph IV Trigger

The Drug Price Competition and Patent Term Restoration Act of 1984, known as the Hatch-Waxman Act, established the modern Abbreviated New Drug Application (ANDA) pathway. It created a framework where generic manufacturers could rely on the safety and efficacy data of the reference listed drug (RLD) in exchange for proving bioequivalence.4 This compromise eliminated the need for redundant clinical trials, dramatically lowering the barrier to entry for generic competitors.

The critical mechanism for early entry—and the primary signal for competitive intelligence—is the Paragraph IV (PIV) certification. When filing an ANDA, a generic applicant must certify against patents listed in the FDA’s Approved Drug Products with Therapeutic Equivalence Evaluations (the “Orange Book”).

The statute provides four certification options:

Paragraph I: No patent information has been filed.

Paragraph II: The patent has expired.

Paragraph III: The generic will not launch until the patent expires.

Paragraph IV: The patent is invalid, unenforceable, or will not be infringed by the generic product.4

A PIV certification is an aggressive move. It asserts that the listed patent is invalid or irrelevant to the generic product. This certification acts as the starting gun for the litigation process.

The 30-Month Stay as a Financial Instrument

Filing an ANDA with a PIV certification is considered an “artificial act of infringement” under 35 U.S.C. § 271(e)(2). This legal fiction allows the originator to sue before the generic product has even entered the stream of commerce. If the New Drug Application (NDA) holder initiates litigation within 45 days of receiving the PIV notice, the FDA is statutorily barred from approving the generic application for 30 months, or until a district court decision is reached, whichever is earlier.4

Strategically, the 30-month stay functions as a guaranteed extension of exclusivity during the litigation window. For a blockbuster drug generating $10 million daily, a 30-month delay preserves approximately $900 million in revenue, regardless of the ultimate validity of the patents in question. This incentivizes originators to list marginal patents in the Orange Book to trigger stays, a practice recently scrutinized by the Federal Trade Commission (FTC).8

The 30-month period was originally conceived as a reasonable duration for patent litigation. In practice, it sets a floor for the timeline of generic entry. For analysts using platforms like DrugPatentWatch, the filing of a PIV certification marks the beginning of a specific countdown. If the 30-month stay expires without a court verdict, the generic manufacturer may launch “at risk”—a decision laden with immense financial liability if the patent is later upheld.

Strategic Implication: Originators must maintain a “picket fence” of secondary patents (formulation, polymorph, method of use) to ensure that at least one patent extends beyond the five-year New Chemical Entity (NCE) exclusivity period, thereby enabling the triggering of a 30-month stay. Without this, the generic could launch immediately upon NCE expiry.

180-Day Exclusivity: The Challenger’s Prize and Forfeiture

To incentivize generic manufacturers to challenge weak patents and incur the costs of litigation, the Hatch-Waxman Act grants 180 days of market exclusivity to the “first applicant” to submit a substantially complete ANDA with a PIV certification.5 During this six-month window, the FDA cannot approve any other generic version of the same drug product.

This period is the primary profit engine for the generic industry. Being the first filer allows a generic to price its product just below the brand—often at a 10-20% discount rather than the 80-90% discount seen in a multi-player market—capturing hundreds of millions of dollars in margin before the price collapses.

However, this exclusivity is fragile and subject to complex forfeiture provisions introduced by the Medicare Prescription Drug, Improvement, and Modernization Act (MMA). These rules were designed to prevent “parking” exclusivity—a tactic where a first filer settles with the brand and delays launch, thereby blocking all subsequent generics from entering the market.

Forfeiture Triggers and Scenarios

Forfeiture of 180-day exclusivity is self-executing but requires a triggering event. The most critical trigger is “Failure to Market.” A first applicant forfeits exclusivity if they fail to market the drug by the later of two dates:

75 days after a final court decision (from which no appeal can be taken) finding the patent invalid or not infringed.

30 months after the submission of the ANDA.10

This “later of” language creates a strategic paradox. If litigation drags on beyond 30 months (which is common), the forfeiture clock does not start until a court decision occurs. However, if a subsequent applicant (a generic who filed later) receives a tentative approval and obtains a court judgment of invalidity, they can trigger the forfeiture of the first applicant’s exclusivity if the first applicant does not launch within 75 days.

FDA Guidance on Forfeiture: Recent FDA guidance clarifies that forfeiture is not discretionary. If the statutory conditions are met, exclusivity is lost. This creates a “use it or lose it” dynamic. Competitive intelligence teams must closely monitor the tentative approval status of subsequent filers. A tentative approval signals that a competitor is scientifically ready to launch and is merely waiting for the exclusivity blockage to clear. If a subsequent filer forces a judgment, the first filer must launch immediately or forfeit their prize.12

Table 1: 180-Day Exclusivity Dynamics and Valuation Impact

Scenario

Market Impact

Revenue Implication for Generic

Standard Launch

First filer enjoys 6 months of duopoly with Brand.

Peak profitability; captures ~40-50% market share at high margin.

Shared Exclusivity

Multiple generics filed PIV on the same day.

Exclusivity is shared; prices erode faster (to ~50% of brand).

Authorized Generic (AG) Launch

Brand launches its own generic during the 180 days.

First filer revenue drops by 40-52% due to immediate price competition.

Forfeiture

First filer loses exclusivity; market opens to all approved generics.

Immediate price collapse to commodity levels (<20% of brand price).

Sources: 13

The BPCIA and the “Patent Dance”

For biologics, the Biologics Price Competition and Innovation Act (BPCIA) creates a distinct pathway. Unlike the rigid notification system of Hatch-Waxman, the BPCIA establishes a flexible, albeit convoluted, information exchange process known as the “patent dance”.16

The Choreography:

Discovery: Within 20 days of the FDA accepting an abbreviated Biologics License Application (aBLA), the biosimilar applicant provides the reference product sponsor (RPS) with its application and manufacturing information.18 This disclosure is confidential and allows the innovator to evaluate potential infringement.

Patent List Exchange: The RPS provides a list of patents it believes are infringed. The applicant responds with detailed invalidity or non-infringement contentions.

Litigation Phases: The process is designed to resolve disputes in two waves—an immediate phase for agreed-upon patents and a second phase triggered by the Notice of Commercial Marketing (must be provided 180 days before commercial launch).19

Strategic Divergence: To Dance or Not to Dance?

Crucially, the Supreme Court ruled in Sandoz v. Amgen that the patent dance is not mandatory. A biosimilar applicant can choose to opt out of the disclosure process.

Opting In: Provides the applicant with information on which patents the brand intends to assert, potentially narrowing the scope of litigation. It also prevents the brand from bringing a declaratory judgment action on certain patents immediately.

Opting Out: Exposes the biosimilar applicant to an immediate declaratory judgment action on all patents. This clears the path to market faster by forcing the litigation to a head but carries higher upfront legal costs and risk.16

For originators, the BPCIA provides 12 years of data exclusivity (compared to 5 for small molecules), creating a longer baseline monopoly. The lack of an Orange Book equivalent for biologics (though the “Purple Book” is evolving) makes patent thicketing easier, as there is no requirement to delist invalid patents or limit the number of asserted claims initially, leading to the dense “Type I” and “Type II” thickets seen in cases like Humira and Enbrel.21

Intellectual Property Warfare: Thickets, Skinny Labels, and Inducement

As the patent cliff approaches, the legal strategy shifts from prosecution to litigation. The battleground in 2025 and 2026 is defined by two emerging trends: the assault on “skinny labeling” and the fortification of patent thickets.

Skinny Labeling Under Siege: The GSK v. Teva and Amarin Precedents

“Skinny labeling,” enabled by Section viii of the Hatch-Waxman Act, allows a generic manufacturer to seek approval for a drug for unpatented indications while “carving out” patented uses from the label. Historically, this has been a safe harbor, allowing generics to enter the market even if the brand holds valid method-of-use patents for newer indications.23

However, the Federal Circuit’s decision in GSK v. Teva (Coreg) and the subsequent Amarin v. Hikma (Vascepa) litigation have introduced significant liability risks via the doctrine of induced infringement.25

The Legal Shift: In GSK v. Teva, the court reinstated a $235 million jury verdict against Teva. The court found that even though Teva had carved out the patented congestive heart failure indication from its label, its marketing materials—including press releases describing the product as an “AB rated generic equivalent” and the clinical reality that the unpatented and patented conditions were intertwined—were sufficient to induce physicians to infringe the patent.23

This precedent suggests that a skinny label alone is no longer a shield if the generic company’s broader commercial behavior “encourages” the infringing use.

The Supreme Court Intervention:

In January 2026, the Supreme Court granted certiorari in Hikma v. Amarin. The central question is whether a generic manufacturer can be liable for inducement based on:

Describing the product as a “generic version” of the brand in investor relations materials and press releases.

Citing public sales data that implies the product will be used for the patented indication (since the patented use constituted the majority of the brand’s sales).28

Strategic Implication: If the Supreme Court upholds the broad inducement theory, the Section viii pathway will become perilous. Generics may be forced to delay launch until all method-of-use patents expire, effectively granting brands extended exclusivity for old drugs simply by obtaining patents on new uses. Competitive intelligence teams must now analyze not just patent expirations, but the labeling strategies and marketing communications of generic challengers. A generic launching with a skinny label is now a target for massive damages litigation.30

Patent Thickets: Type I vs. Type II

Originators employ “patent thickets”—dense webs of overlapping patents—to delay generic entry. To forecast entry effectively, analysts must distinguish between two types of thickets.

Type I (Innovation-Driven): These thickets consist of a large number of non-overlapping or inventive patents that cover different, legitimate aspects of a biologic (e.g., specific cell lines, purification methods, assays). These are defensible and reflect the complexity of the “process is the product” doctrine in biologics.21

Type II (Strategic Duplication): These consist of overlapping, arguably non-inventive patents (e.g., minor dosage variations, multiple patents on the same formulation with slight tweaks) designed solely to increase the cost and duration of litigation.21

Case Study: Enbrel vs. Humira The Enbrel case demonstrated the power of a Type I/II hybrid defense. Amgen successfully defended its thicket in court, pushing biosimilar entry out to 2029, nearly 30 years after the drug’s initial approval. The court upheld patents covering the fusion protein’s structure and manufacturing, validating the strategy of layering protection.21

Conversely, regarding Humira, AbbVie amassed over 100 patents. While they settled to allow entry in 2023, the sheer volume of patents forced biosimilar competitors to settle rather than risk litigation. The cost of clearing the thicket became the barrier to entry, rather than the validity of any single patent.21

Regulatory Counter-Measures: The FTC has taken an aggressive stance in 2024-2025 against “improper” Orange Book listings, specifically targeting device patents on inhalers and autoinjectors that create Type II thickets. This pressure forced companies like Teva to voluntarily delist hundreds of patents, dismantling the thickets for asthma products and clearing the path for generics.8

The Economics of Erosion: Modeling the Fall

The trajectory of revenue loss after LOE differs radically between small molecules and biologics. Accurate forecasting requires distinguishing between the “Cliff” and the “Slope.”

The Small Molecule Cliff: Competitor Count is King

For traditional generics, price erosion is a function of the number of competitors. FDA and HHS data demonstrate a consistent, mathematically predictable pattern.

Table 2: Generic Price Erosion by Number of Competitors

Number of Generic Competitors

Price as % of Brand (AMP)

Market Share Dynamics

1 (First Filer)

70% – 90%

First filer captures ~40-50% volume share rapidly; price remains high due to 180-day exclusivity.

Commoditization. Prices approach marginal cost of goods sold (COGS).

Sources: 33

The Mechanism of Collapse: Small molecule erosion is driven by automatic substitution laws at the state level. Once a generic is rated “AB” (therapeutically equivalent) in the Orange Book, pharmacists must substitute it for the brand unless the prescriber explicitly writes “Dispense as Written” (DAW). PBMs reinforce this by placing the brand on a non-preferred tier (Tier 3 or excluded), creating a hard stop for patient access.36

Authorized Generics (AGs) as Spoilers: An often-overlooked variable is the Authorized Generic. Brands frequently launch their own AG (either directly or through a partner) precisely when the first independent generic launches. This AG does not rely on the ANDA pathway but on the brand’s original NDA. The entry of an AG during the 180-day exclusivity period effectively splits the market, reducing the first-filer’s revenues by 40% to 52%.14 For financial models, the presence of an AG agreement in a settlement is a key negative variable for generic revenue forecasts.

The Biosimilar Slope: Institutional Friction

Biosimilars do not follow the cliff trajectory. Due to higher development costs ($100M+ vs. $2-5M for generics) and manufacturing complexity, the number of entrants is naturally lower.38 Furthermore, most biosimilars are not deemed “interchangeable” (automatically substitutable) without specific FDA designation, meaning physicians must actively prescribe the biosimilar.

Erosion Factors for Biologics:

Rebate Walls: PBMs often contract with the originator to maintain the brand as the preferred product in exchange for massive rebates (often >50% of the Wholesale Acquisition Cost). This blocks biosimilars even if their list price is lower. The PBM makes more money retaining a percentage of the high brand rebate than they would from a lower-priced biosimilar.9

ASP + 6% Incentive: In the “Buy-and-Bill” model (clinics/hospitals), provider reimbursement is often based on the Average Sales Price (ASP) plus a 6% markup. Higher-priced brands yield higher absolute dollar margins for clinics, disincentivizing the switch to lower-cost biosimilars.41

Net Price vs. List Price: While list prices for biosimilars may only be 15-30% lower than the brand, the net price erosion (after rebates) is often 50-70%. However, this savings is accrued by the Payer/PBM, not necessarily the patient.42

Forecast for 2025-2026: Data from Humira (adalimumab) biosimilar entry in 2023-2024 shows a “scalloped” erosion curve. Market share did not shift immediately. Instead, erosion occurred in steps coinciding with PBM formulary contracting cycles (typically January 1st and July 1st). By 2025, biosimilars had captured ~20-30% of the volume, a far cry from the 90% seen in small molecules.40 This indicates that biologic LOE models must account for a 2-3 year ramp to peak erosion, rather than the 6-month crash of small molecules.

Supply Chain Geopolitics: The Hidden Variable

External forces beyond the patent system are increasingly influencing the reliability and cost of generic entry. The pharmaceutical supply chain’s dependence on China has transformed from a logistical detail into a primary geopolitical risk factor.

The China API Chokehold

As of 2025, China produces approximately 40-45% of the Key Starting Materials (KSMs) and Active Pharmaceutical Ingredients (APIs) for the global generic market.44 China’s dominance is even more pronounced in the Asia-Pacific Contract Development and Manufacturing Organization (CDMO) market, where it holds a 37.68% share.44

Strategic Vulnerability: While India is the world’s largest exporter of finished generic formulations, its industry is structurally dependent on Chinese upstream chemistry. Indian manufacturers rely on China for approximately 70% of their KSMs.45 There is no immediate alternative capacity that can match China’s scale and cost efficiency.

Legislative Threats: The BIOSECURE Act

The introduction of the BIOSECURE Act in the U.S. represents a significant disruption. The Act aims to prohibit U.S. companies from contracting with “biotechnology companies of concern” linked to foreign adversaries.

Impact on Generics: If major Chinese API suppliers or CDMOs are targeted, U.S. generic manufacturers would be forced to switch suppliers. Qualifying a new API supplier is a regulatory process that takes 12-18 months.

Cost Inflation: Shifting supply chains away from China to Europe or domestic U.S. manufacturing (onshoring) would fundamentally alter the cost structure of generics. The “race to the bottom” pricing model relies on cheap Chinese inputs.

Erosion Floor: Geopolitical decoupling could artificially inflate the floor price of generics. Instead of prices dropping to 10% of the brand, they might stabilize at 30-40% due to higher COGS, reducing the economic benefit of patent expirations for payers.46

Strategic Case Studies: The Playbook in Action

Analyzing recent blockbuster LOE events reveals three distinct archetypes of market entry that serve as templates for forecasting the 2026-2030 period.

1. The Volume-Limited Ramp: Revlimid (Lenalidomide)

Bristol Myers Squibb (BMS) executed a masterclass in soft-landing a patent cliff. Facing patent challenges from Natco, Teva, and Dr. Reddy’s, BMS settled the litigation by allowing them to launch in 2022, but with strict volume limitations.47

Mechanism: The settlement restricted generics to a mid-single-digit percentage of the total market volume initially, gradually increasing each year until full open entry in January 2026.

Result: BMS retained the vast majority of revenue for four additional years. The price remained high because the artificial scarcity prevented the “commoditization” phase of the erosion curve.

Lesson: Settlements creating “oligopolies by contract” can preserve value better than risking an all-or-nothing trial. This model is likely to be replicated for other high-value oncology assets.49

2. The Formulation Fortress: Eliquis (Apixaban)

BMS and Pfizer successfully delayed generic entry for Eliquis until April 2028 through a combination of Patent Term Extension (PTE) and formulation patents.50

Strategy: The composition of matter patent (‘208) was extended to 2026 via PTE. However, the partners also asserted follow-on patents (‘945) covering the specific crystalline form of apixaban, which extend to 2031.

Litigation Outcome: By winning on the formulation patents in district court, the partners secured a litigation settlement that delays entry to 2028—six years beyond the original 20-year patent term.51

Revenue Impact: This extension protects an estimated $50 billion in revenue between 2022 and 2028, demonstrating the massive ROI of formulation patent enforcement.51

3. The Subcutaneous Pivot: Keytruda (Pembrolizumab) & Opdivo (Nivolumab)

Facing a 2028 patent cliff for their IV formulations, Merck and BMS are aggressively developing subcutaneous (Sub-Q) versions to “product hop” the market.

Strategy: By converting patients to a more convenient Sub-Q form (protected by new device and formulation patents expiring in the late 2030s) before the IV biosimilars launch, they aim to move the market standard.

FDA Action: The approval of Keytruda Qlex (pembrolizumab + hyaluronidase) in late 2025 provides a bridge. If Merck can switch 50% of patients to the Sub-Q version by 2028, the revenue impact of IV biosimilars is effectively halved. The biosimilars will be competing for the “legacy” IV market, while the high-value patients remain on the patent-protected Sub-Q product.53

In this high-stakes environment, passive monitoring of expiration dates is insufficient. Firms must employ predictive intelligence infrastructures that synthesize legal, regulatory, and commercial data.

Utilizing Intelligence Platforms

Advanced tools like DrugPatentWatch have become essential for analyzing the patent landscape. Rather than simply tracking expiration dates, these platforms allow analysts to:

Monitor Patent Litigation Dockets: Identify PIV challenges the moment they are filed, often before they are public knowledge via company press releases. This provides an early warning of a generic challenge.55

Analyze Orange Book Data: Decode “Use Codes” and exclusivity flags (e.g., NCE, ODE, PED) to calculate the true effective patent life, accounting for pediatric extensions and 30-month stays. Simply reading the expiration date of the primary patent leads to errors of 3-5 years in forecasting.57

Track Tentative Approvals: A surge in tentative approvals for a specific molecule indicates a crowded, high-erosion launch is imminent. It signals that the FDA scientific review is complete, and competitors are merely waiting for the legal gate to open.12

Decoding the Signals

Citizen Petitions: Brands often file Citizen Petitions under Section 505(q) of the FD&C Act to raise safety concerns about generic bioequivalence just before approval. While the FDA rarely denies ANDAs based on these, they can cause administrative delays. A spike in Citizen Petitions is a leading indicator of a hostile defense strategy.60

Settlement Timing: While specific terms are confidential, tracking the timing of settlements (e.g., dismissal with prejudice) via litigation ledgers helps forecast entry dates. If a settlement occurs early in the 30-month stay, it often suggests a “volume-limited” or delayed entry deal (like Revlimid). If it occurs on the eve of trial, it may indicate a “walk-away” or a more favorable term for the generic.56

The 2026-2030 Super-Cliff: Sector-Wide Exposure

The pharmaceutical industry is approaching a period of unprecedented revenue exposure. Between 2026 and 2030, over $236 billion in revenue is at risk.2 This “Super-Cliff” will redefine the competitive hierarchy of the industry.

Second-Order Insight: The concentration of LOEs in 2028 (Keytruda, Opdivo, Eliquis) will trigger a massive liquidity event for payers. The budget freed up by the genericization of these massive products will be substantial. Paradoxically, this may increase spending capacity for next-generation modalities (Cell & Gene Therapy, ADCs) as PBMs and insurers have more headroom in their budgets. However, for the originators (Merck, BMS), the “earnings hole” will likely drive aggressive M&A activity in 2026-2027 to backfill revenue, potentially inflating valuations for mid-cap biotech targets.66

Conclusion

The prediction of market dynamics after patent loss has evolved from a simple calendar exercise into a multi-dimensional strategic discipline. The era of the simple “patent cliff” is ending, replaced by complex erosion slopes defined by litigation settlements, biosimilar adoption barriers, and supply chain geopolitics.

For the next five years, the industry will be defined by the tension between the “Super-Cliff” of 2028 and the defensive fortifications of Sub-Q switching and patent thickets. Success for originators lies in the successful execution of these delays to bridge the gap to new launches. Success for payers and generics depends on navigating the legal minefield of induced infringement and breaking the PBM rebate walls that prevent price competition from translating into actual savings.

Understanding these dynamics requires a shift from reactive observation to predictive modeling. The companies that can accurately forecast the effective patent life—accounting for the 30-month stay, the 180-day forfeiture risks, and the PBM rebate dynamics—will possess an asymmetric advantage in capital allocation and strategic planning.

Key Takeaways

The 2028 Super-Cliff is Imminent: The simultaneous LOE of Keytruda, Opdivo, and Eliquis represents the largest concentration of revenue risk in pharma history ($236B+), necessitating aggressive M&A and lifecycle management strategies in 2026-2027.

Skinny Labeling is a Liability: The Supreme Court’s review of Hikma v. Amarin could fundamentally alter generic entry strategies; a ruling against Hikma would effectively extend market exclusivity for multi-indication drugs until the last method-of-use patent expires, killing the Section viii pathway.

Biosimilar Erosion is “Scalloped”: Unlike the 90% crash of small molecules, biosimilars erode in steps (20-30% initially), dictated by PBM contracting cycles and rebate walls.

Volume-Limited Settlements are the New Standard: The Revlimid model—allowing early but capped generic entry—is the dominant strategy for managing “soft landings” for blockbusters, preserving value for originators while guaranteeing access for generics.

Supply Chain Fragility: The reliance on Chinese KSMs (40-45% of supply) is a critical vulnerability. Geopolitical decoupling (BIOSECURE Act) could artificially inflate the floor price of generics, reducing the economic benefit of patent expirations.

Intelligence Must Be Active: Tools like DrugPatentWatch are mandatory for identifying Orange Book delisting opportunities, monitoring the real-time status of PIV litigation, and predicting 180-day forfeiture events.

FAQ

Q1: How does a “Citizen Petition” impact generic entry timelines?

A: Brands often file Citizen Petitions under Section 505(q) of the FD&C Act, asking the FDA to impose stricter testing requirements on pending generics (e.g., demanding new bioequivalence studies). While the FDA must respond within 150 days and rarely denies an ANDA solely based on a petition, the administrative burden can delay final approval by months. The FDA now reports “sham” petitions to the FTC, but they remain a common delaying tactic used to buy time.

Q2: What is the difference between “Interchangeability” and “Biosimilarity,” and why does it matter for revenue forecasting?

A: All approved biosimilars are “highly similar” and clinically equivalent. However, only those with an “Interchangeability” designation (requiring additional switching studies) can be substituted by a pharmacist without the prescriber’s permission (depending on state law). Without interchangeability, sales depend on convincing physicians to change prescribing habits, resulting in a much slower adoption curve. Legislation is proposed to streamline this, but for now, it remains a key differentiator in erosion speed.

Q3: Can a generic launch “at risk” before a patent case is fully resolved?

A: Yes. If the 30-month stay expires and the FDA grants approval before the district court issues a verdict, the generic can launch “at risk.” However, if they later lose the patent case, they are liable for 3x the brand’s lost profits (treble damages), which can bankrupt a generic company. Consequently, “at risk” launches are rare and usually limited to cases where the patent is viewed as extremely weak or the generic company has a very high risk tolerance.

Q4: How do “Authorized Generics” (AGs) affect the 180-day exclusivity period?

A: An Authorized Generic is the brand’s own product sold under a generic label. The brand can launch an AG during the first-filer’s 180-day exclusivity period. This cuts the first-filer’s market share roughly in half and reduces their profits by 40-50%, acting as a punitive measure to discourage PIV challenges. It is a key variable in valuing the 180-day prize.

Q5: Why would a PBM prefer a higher-priced biologic over a cheaper biosimilar?

A: PBMs generate revenue through rebates (a percentage of the list price paid back by the manufacturer). A brand drug with a $10,000 list price and a 40% rebate ($4,000) generates more revenue for the PBM than a biosimilar with a $6,000 list price and a 10% rebate ($600). Unless the plan sponsor demands a “lowest net cost” model, the PBM has a financial incentive to block the biosimilar to maximize their own rebate retention.

Sixteenth Annual Report on Delays in Approvals of Applications Related to Citizen Petitions and Petitions for Stay of Agency Action – FDA, accessed January 22, 2026, https://www.fda.gov/media/184951/download

Our search for a reliable patent intelligence solution ended with DrugPatentWatch, accessed January 22, 2026, https://www.drugpatentwatch.com/