The Inevitable Horizon: Understanding Loss of Exclusivity (LOE)

The pharmaceutical landscape is characterized by cycles of innovation, market exclusivity, and eventual competition. Within this dynamic environment, Loss of Exclusivity (LOE) stands as a predictable, yet profoundly challenging, milestone in a drug’s lifecycle. Far from being a sudden, unforeseen disaster, LOE represents the point at which an innovator pharmaceutical manufacturer relinquishes its exclusive legal rights to develop, sell, and market a specific drug formulation. This pivotal transition opens the market to generic competition, fostering a delicate balance between incentivizing groundbreaking innovation and ensuring broader public access to more affordable medicines.1

For a limited period, typically between 10 to 15 years, a pharmaceutical company that formulates a new prescription drug is granted a legal patent, providing the exclusive rights to its development, sale, and marketing.1 This period of market protection is designed to allow companies to recoup the substantial investments made in research and development (R&D), which can be considerable, with some companies reinvesting as much as 18.6% of their total sales back into R&D in 2014.3 However, once these protections expire, the market transforms, inviting new entrants and a new set of strategic imperatives for the original patent holder.

Strategic Lifecycle Management: Maximizing Asset Valuation Amid Loss of Exclusivity

Loss of Exclusivity (LOE) is the most significant structural risk to pharmaceutical enterprise value. For a multi-billion-dollar blockbuster, the transition from a protected monopoly to a commoditized market can erase 90% of trailing twelve-month revenue within three quarters. Effective management of this transition requires a shift from commercial execution to intellectual property (IP) defense and portfolio pivot strategies at least seven years before the primary patent expires. This guide provides a technical roadmap for navigating the ‘patent cliff’ by integrating legal, regulatory, and commercial levers to preserve long-term cash flows.

Key Takeaways: The LOE Landscape

LOE planning must begin during Phase II development to ensure secondary patent filings have sufficient time for prosecution and enforcement.

The valuation of a pharmaceutical company is tied to the ‘terminal value’ of its key assets; extending this value by even 18 months can add billions to a firm’s market capitalization.

Small molecule drugs face a ‘cliff’ (rapid erosion), while biologics face a ‘slope’ (gradual erosion) due to manufacturing complexity and pharmacy benefit manager (PBM) contracting.

Investment Strategy: The Analyst’s View

Institutional investors prioritize the ‘Pipeline Coverage Ratio’—the ability of new launches to offset revenue lost to LOE. Analysts look for ‘thicketing’ density and the success rate of Paragraph IV challenges as lead indicators of a company’s future dividend health.

Pillar 1: The Architecture of the Patent Thicket

A single patent on an active pharmaceutical ingredient (API) is an insufficient defense. Senior IP strategists build ‘patent thickets’—a dense web of overlapping legal protections designed to multiply the cost and duration of litigation for generic or biosimilar challengers. This ‘defense-in-depth’ strategy ensures that even if a challenger successfully invalidates the primary composition-of-matter (CoM) patent, they remain blocked by dozens of secondary filings.

IP Asset Valuation: The Humira Precedent

AbbVie’s management of Humira (adalimumab) is the benchmark for biologic thicketing. The company filed over 250 patent applications, with roughly 90% occurring after the drug received FDA approval. This strategy created a ‘patent wall’ that delayed U.S. biosimilar entry until 2023, nearly two decades after launch. For analysts, the valuation of the Humira IP estate was not based on the 2016 expiry of its core patent, but on the ‘settlement value’ of the secondary patents—method of treatment, formulation, and manufacturing process—which forced competitors into licensing deals that preserved AbbVie’s monopoly for an additional seven years.

The Hierarchy of Patent Protection

Composition of Matter (CoM): The core molecular structure. This is the hardest to challenge but the first to expire.

Formulation and Dosage: Patents covering specific delivery mechanisms, such as extended-release matrices or stabilized liquid formulations for biologics.

Method of Use (MoU): Strategic filings for specific indications. If a drug is approved for rheumatoid arthritis and later for Crohn’s disease, the Crohn’s patent may extend protection for that specific patient volume.

Manufacturing Processes: In biologics, the ‘process is the product.’ Patents on proprietary cell lines or purification techniques are increasingly used to block biosimilars that cannot replicate the exact manufacturing environment.

Pillar 2: Navigating the Hatch-Waxman and BPCIA Frameworks

The legal pathway for generic entry differs based on the molecular weight of the drug. Understanding these frameworks is essential for timing the market entry of competitors and the subsequent price erosion.

Small Molecules and the Paragraph IV Filing

Under the Hatch-Waxman Act, a generic manufacturer seeking to launch before patent expiry files an Abbreviated New Drug Application (ANDA) with a Paragraph IV certification. This filing asserts that the brand’s patents are invalid or not infringed. The moment a brand manufacturer receives a ‘Notice Letter’ of a Paragraph IV filing, they have 45 days to sue. Filing this suit triggers an automatic 30-month stay of FDA approval for the generic, a critical window that allows the brand to transition patients to a next-generation product.

Biologics and the ‘Patent Dance’

The Biologics Price Competition and Innovation Act (BPCIA) governs the entry of biosimilars. Unlike the Orange Book for small molecules, which is a public registry, the BPCIA involves a ‘patent dance’—a private exchange of confidential IP and manufacturing information between the brand (Reference Product Sponsor) and the biosimilar applicant. This process is designed to narrow the scope of litigation before a product reaches the market. Biologics also enjoy 12 years of regulatory data exclusivity, which runs parallel to patent protection and provides a guaranteed floor for asset valuation regardless of patent strength.

Key Takeaways: Regulatory Strategy

The 30-month stay is a statutory gift to brand companies; it is often used to execute ‘Product Hopping’ (switching patients to a new formulation).

For generics, being ‘First-to-File’ is the goal, as it grants 180 days of market exclusivity, allowing the generic to capture high margins before the market becomes fully commoditized.

Biosimilar competition is slower because PBMs require significant rebates to switch patients, often resulting in the brand maintaining 40-60% volume even after LOE.

Investment Strategy: Litigation Risk Assessment

Analysts must track the ‘Markman Hearing’ outcomes in Hatch-Waxman cases. A favorable claim construction for the brand company can signal a multi-year extension of the revenue tail, whereas an unfavorable ruling often precedes a ‘settlement with entry’—a deal where the generic agrees to enter the market a few months before patent expiry in exchange for dropped litigation.

Defining LOE: Patents vs. Exclusivity

To fully grasp the mechanics of LOE, it is essential to distinguish between two primary forms of market protection: patents and exclusivities. While often discussed interchangeably, these mechanisms operate under different statutes and offer distinct layers of protection for pharmaceutical products.2

Patents are property rights granted by the United States Patent and Trademark Office (USPTO). They can be issued at any point during a drug’s development and typically confer protection for 20 years from the patent application filing date.2 Patents are broad in scope, covering not only the new molecular entity itself but also the intricate processes used to manufacture the drug, its specific methods of use, and even new formulations.3 The effective patent life can sometimes be shorter than 20 years due to the extensive time required for product development and regulatory review.4 However, patent protection can also be extended beyond this standard term, particularly if there were delays in the patent processing at the USPTO or during the product review by the FDA.3 All patents on branded pharmaceutical products are meticulously registered and listed in an addendum to the FDA-published Orange Book.3 During the patent’s life, other manufacturers are legally prohibited from selling generic alternatives without risking substantial legal penalties.3

In contrast, exclusivity refers to specific statutory delays and prohibitions on the approval of competitor drugs. These protections attach upon the approval of a drug by the FDA or upon the approval of certain supplements.2 Unlike patents, exclusivity periods are fixed durations set by statute and are not tied to the patent filing date. For example, Orphan Drug Exclusivity (ODE) provides 7 years of protection for drugs treating rare diseases, while New Chemical Entity (NCE) Exclusivity grants 5 years. New Clinical Investigation Exclusivity offers 3 years, and Pediatric Exclusivity (PED) uniquely adds 6 months to existing patents and exclusivities.2 It is crucial to understand that patents and exclusivities may not always run concurrently, nor do they necessarily cover the same aspects of a drug product.2

The interplay of these distinct but complementary protections creates a formidable “solid fence” against generic competition for a defined period.5 This multi-layered intellectual property framework is designed to provide innovator companies with the necessary market exclusivity to recoup their R&D investments and generate profits, which are then often reinvested into future drug therapies.3 However, once these protections expire, the market dynamics fundamentally shift, allowing generic manufacturers to enter and compete freely.1

A notable example of a drug that has undergone LOE is Truvada, an HIV medication.1 The journey of such drugs often involves a strategy known as “evergreening,” where pharmaceutical companies apply for subsequent patents related to a single medicine. This practice, which can include patents on isomers, metabolites, prodrugs, new formulations, or fixed-dose combinations, aims to extend patent protection for as long as possible, thereby delaying generic competition.3 For instance, evergreening efforts might have extended patent protection for TDF/FTC until 2024 and TDF/FTC/EFV until 2026, had generic companies not developed TDX and the EPO not rejected the patent on TDF/FTC.5 In Europe, original drug manufacturers benefit from an 8-year data exclusivity period plus 2 years of market exclusivity from the approval date, meaning generic manufacturers can apply for approval after 8 years and launch after 10 years, assuming patent expiry.5 This complex interplay underscores the strategic importance of understanding every facet of intellectual property protection.

Type of Exclusivity

Duration

Brief Description/Purpose

Orphan Drug Exclusivity (ODE)

7 years

Granted for drugs treating rare diseases or conditions.

New Chemical Entity (NCE) Exclusivity

5 years

Applies to drugs containing no active moiety previously approved by FDA.

GAIN Exclusivity

5 years (added)

Added to certain exclusivities for Qualified Infectious Disease Products (QIDP).

New Clinical Investigation Exclusivity

3 years

Granted for new clinical investigations (other than NCE) essential for approval.

Pediatric Exclusivity (PED)

6 months (added)

Added to existing patents/exclusivities for conducting pediatric studies.

Patent Challenge (PC)

180 days

For Abbreviated New Drug Applications (ANDAs) only, granted to the first generic applicant to successfully challenge a patent.

Competitive Generic Therapy (CGT)

180 days

For ANDAs only, granted for drugs with inadequate generic competition.

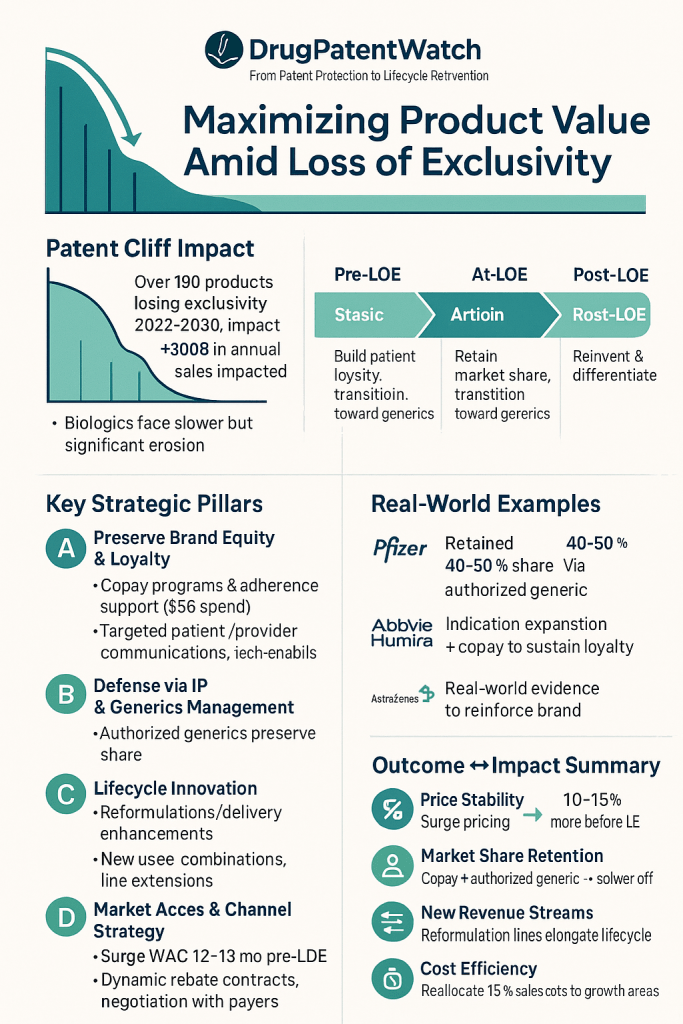

The “Patent Cliff” Phenomenon: A Looming Financial Challenge

The term “patent cliff” vividly describes the sharp, often dramatic, decline in revenue that a pharmaceutical company experiences when patent protection for its blockbuster products expires.9 This phenomenon is not new; it was particularly pronounced between 2010 and 2015, when numerous high-revenue drugs like Lipitor and Plavix lost their exclusivity, leading to significant financial turbulence for their manufacturers.10

However, the pharmaceutical industry is currently bracing for an “unprecedented wave” of patent expirations, a patent cliff of even greater magnitude. Over 190 products are projected to lose exclusivity between 2022 and 2030, placing an estimated $300 billion in sales at risk between 2023 and 2028 alone.11 The products slated for LOE through 2030 collectively represent a staggering $183.5 billion in annual sales.13 This financial exposure is not merely a forecast; it is a critical challenge demanding comprehensive strategic responses from pharmaceutical companies.

A significant aspect of the current patent cliff that differentiates it from previous waves is the higher proportion of biologics facing LOE.13 Historically, patent expirations primarily impacted small molecule medicines, which typically face rapid and deep sales erosion upon generic entry. However, biosimilars, the generic equivalents of biologics, generally gain market share more slowly compared to generic competition for small molecules.13 This distinct dynamic suggests that while the initial revenue drop for biologics might be less precipitous, the period of sustained erosion could be more prolonged and drawn out. This necessitates a more nuanced and adaptive LOE strategy tailored to the specific characteristics of the drug type, moving beyond a one-size-fits-all approach. For companies, this means understanding that the “cliff” for biologics might look more like a gradual slope, requiring different long-term strategic investments and patient retention efforts than the rapid decline seen with small molecules.

Blockbuster drugs, which have historically fueled the pharmaceutical industry’s growth, are at the forefront of this challenge. AbbVie’s Humira, one of the most profitable drugs in history, has already faced patent expiration, with its revenue projections indicating a steady decline after generating over $18 billion in U.S. sales in 2022.9 Similarly, Merck’s Keytruda, a blockbuster cancer immunotherapy, faces patent expiration in 2028, creating significant financial exposure for the company, with analysts projecting a 19% decline in sales from an estimated $33.7 billion in 2028 to $27.4 billion in 2029.12 Novartis’s heart failure drug Entresto, which generated $7.8 billion in the prior year, is set to lose market exclusivity in July 2025, prompting the company to initiate proactive defense efforts as early as September 2022.14 These examples underscore the immense financial stakes involved and the proactive measures companies are taking to mitigate the impact.

Historical Context and Future Projections of Revenue at Risk

Looking back, the 2016 patent cliff was projected to erode $100 billion in brand-name sales, a substantial figure at the time.13 The early 2010s witnessed the expiration of patents on numerous blockbuster medications, including Lipitor and Plavix, which led to significant revenue reductions for their original manufacturers.10 Pfizer’s Lipitor, for instance, experienced a dramatic decline, with its revenue dropping to less than 10% of its peak sales after losing its patent protection.10 These historical precedents serve as stark reminders of the profound financial consequences of LOE.

The current and future outlook paints an even more challenging picture. Projections indicate that over $200 billion in annual revenue is at risk through 2030 due to patent expirations.9 In the Indian market alone, approximately $500 million in pharmaceutical sales are at risk from LOE between 2019 and 2028, with a significant portion, around $210 million, at risk in 2019 and 2020.16 These figures highlight the global scale and localized intensity of the patent cliff.

From an industry perspective, the sentiment is clear: “The patent cliff is exactly that: a cliff”.14 This statement encapsulates the dramatic and rapid nature of the revenue drop, emphasizing the urgent need for pharmaceutical companies to develop robust strategies. However, this challenge also presents a unique opportunity. While the “patent cliff” is undeniably a threat, it can also be viewed as an “invitation to innovate”.11 The pressure of LOE can compel pharmaceutical companies to accelerate their R&D efforts, diversify their portfolios, and explore novel value-creation avenues, such as new indications or formulations, that might otherwise be deprioritized. This market-driven evolutionary pressure, if embraced, has the potential to lead to long-term competitive advantage, transforming a period of potential loss into one of strategic growth and resilience.

The Profound Impact of LOE: Beyond Revenue Decline

Entering the post-Loss of Exclusivity (LOE) phase is often described as a “complete game changer” for pharmaceutical companies.17 The strategies and approaches that propelled a product to blockbuster status during its exclusive period are no longer sufficient to sustain its value. This transition necessitates significant adjustments across the entire organization, extending far beyond mere financial considerations.

Financial Ramifications: Sales, Profitability, and Cash Flow Erosion

The most immediate and palpable consequences of LOE are financial. Upon patent expiration, a significant drop in demand for the branded drug is almost inevitable. This occurs because generic competitors can quickly enter the market, offering bioequivalent medicines at a fraction of the cost.1 The impact can be severe, with branded drugs often losing up to 80% of their revenue within the first year of facing generic or biosimilar competition.9 Some drugs have even witnessed a staggering 73% loss of market share within just two weeks of LOE.1

This surge of lower-cost generic alternatives directly erodes the innovator company’s profitability. As more competition enters the market, the customer base for the branded drug shrinks, leading to a decrease in overall profit.1 Generic drugs are typically manufactured at a lower cost and subsequently sold at significantly reduced prices compared to the original drug.1 This intense price competition inevitably leads to a reduction in the innovator company’s cash flow, as lower sales volumes of branded drugs translate directly into less generated cash.1

The extent of price erosion post-LOE can be dramatic. For instance, prices for generic drugs can decline by as much as 20% in markets with approximately three competitors. This reduction deepens further, dropping by 70% to 80% relative to the pre-generic entry price in markets with ten or more competitors after three years.18 In some international markets, the price disparity is even more pronounced. In the UK, generics are commonly priced at only 5-10% of the original drug’s price before patent expiration, while in the Netherlands, the cost of some generics can be as low as 2% of the originator drug price, leading to substantial healthcare savings.19 Studies consistently show that prices decline by about 15-40% with 3-5 generic sellers and by 60-90% with 10 or more.18 These statistics underscore the immense pressure on innovator companies to adapt their financial models.

Market Share Dynamics: The Rise of Generic Competition

The entry of generic drugs fundamentally reshapes market share dynamics. While generics represent a substantial portion of prescriptions—for example, 91% of all prescriptions in the United States in 2022 were filled as generic drugs—they account for a much smaller percentage of the overall drug costs, approximately 22% in the US.18 This disparity highlights the critical role generics play in driving cost savings across healthcare systems.19

However, the pace and extent of generic market penetration vary significantly across different countries and therapeutic areas. For example, average generic penetration up to three years after first entry reached 55% in the UK, but only 10-25% in France, Italy, and Spain.19 In China, originator drugs remarkably maintained over 70% market share eight quarters after the first generic entry. This slower adoption of generics in certain markets can be attributed to factors such as physician and patient skepticism, a lack of mandatory substitution policies, and past regulatory weaknesses.19 This varied market response indicates that the impact of LOE is highly nuanced and context-dependent, not a uniform “cliff.” Companies must conduct granular market analysis to understand specific regional and therapeutic area dynamics, rather than applying a generic, one-size-fits-all LOE strategy.

Despite these variations, the general trend remains clear: when a drug goes off-patent, its market share is likely to dwindle quickly due to the influx of new market entrants.1 This reality necessitates a strategic pivot for innovator companies, focusing on how to retain value and relevance in a newly competitive landscape.

Metric

Typical Impact/Range

Timeframe

Context/Conditions

Revenue Decline (Branded Drug)

Up to 80%

Within first year of generic/biosimilar competition

General

Market Share Loss (Branded Drug)

73%

Within two weeks of LOE

Specific example (unnamed drug) 1

Market Share Retention (Originator Drug)

Over 70%

Eight quarters after first generic entry

In China, due to factors like skepticism 19

Price Reduction (Generic Drugs)

20%

With ~3 competitors

General 18

Price Reduction (Generic Drugs)

70-80%

After 3 years, with 10+ competitors

General 18

Price Reduction (Generic Drugs)

5-10% of original price

Before patent expiration

In UK 19

Price Reduction (Generic Omeprazole/Simvastatin)

2% of originator price

Post-patent expiry

In Netherlands, due to quarterly auctions 19

Price Decline (Originator Drugs)

38-48% (physician-admin), 25% (oral)

Post-patent expiration

General 12

Price Decline (with 3-5 sellers)

15-40%

General

Various studies 18

Price Decline (with 10+ sellers)

60-90%

General

Various studies 18

Operational Shifts: Adapting to a New Landscape

The financial and market share shifts triggered by LOE exert immense operational pressure on pharmaceutical companies. The existing organizational structure and strategic priorities that served the brand during its exclusive period must undergo a fundamental transformation.

One significant shift occurs in marketing focus. Where efforts previously centered on communicating product features and driving market expansion, they must now pivot towards building brand trust, emphasizing real-world evidence, and offering additional services or innovative pricing messages.17 This transition acknowledges that post-LOE, the value proposition of the original brand shifts from exclusive efficacy to a more holistic patient experience and perceived reliability. The brand is no longer just the chemical compound; it is the entire ecosystem of support, trust, and potentially superior quality that generic alternatives may not easily replicate. This implies that investments in brand equity, patient support programs, and robust real-world evidence generation become even more critical, as they emerge as the new differentiators in a price-competitive market.

Similarly, sales teams must reorient their objectives. Their focus shifts from aggressive market expansion to diligently maintaining high volume levels and preventing patient migration to generics.17 This requires a different skillset and a more patient-centric approach, emphasizing adherence and long-term relationships rather than initial prescription uptake.

Beyond these functional adjustments, LOE necessitates broader organizational changes. Companies may need to establish entirely new processes, acquire relevant skills and capabilities that were not previously central to their operations, and even review headcounts and the composition of their teams.17 The imperative to drive cost reduction and protect the bottom line becomes paramount.17 This isn’t merely about cutting expenses; it’s about fundamentally re-evaluating the entire operational model, from optimizing manufacturing efficiency through continuous manufacturing technologies to streamlining supply chain management and re-allocating R&D investments. The ripple effect is a pervasive drive towards lean operations and a sharper focus on return on investment for all remaining brand-related activities, ensuring that every dollar spent contributes directly to value retention in the post-exclusivity era.

Proactive Defense: Strategies Before LOE

The most effective way to navigate the pharmaceutical patent cliff is not to react to it, but to anticipate and proactively prepare for it. Companies that act decisively and strategically before LOE can position themselves not merely to weather the impending storm, but to emerge stronger and more resilient on the other side.13 This proactive stance is not a luxury; it is a strategic imperative, with planning ideally commencing at least two years before the anticipated LOE date.20 Delaying these efforts can significantly diminish their potential impact.22

Comprehensive Market Analysis and Strategic Planning

The foundational step in any successful LOE strategy is a thorough and comprehensive assessment of the market landscape.13 This deep dive provides the critical insights necessary to develop an effective late-lifecycle strategy specifically tailored to the product’s unique characteristics and prevailing market conditions.13

Assessing Competitive Landscape and Forecasting Impact

A crucial component of this analysis involves asking penetrating questions about the future. How will the market evolve after LOE? What will be the likely impact on revenue and volume? When exactly can generic players be expected to respond and enter the market? 13 Answering these questions requires a meticulous understanding of the existing patent landscape, including identifying any patent vulnerabilities, potential design-around solutions that generic manufacturers might employ, and prior art that could invalidate existing patents.23 It means assessing the strengths and weaknesses of the innovator’s own intellectual property portfolio.

Equally vital is a deep understanding of patient needs and prescriber behaviors. What factors truly drive prescribing decisions for this particular drug? Are there specific unmet needs that the innovator product addresses more effectively or uniquely than potential generic alternatives? 13 This granular understanding of the market and its stakeholders is indispensable for developing strategies that can maintain loyalty and preference even in the face of generic competition.

Based on this comprehensive assessment, effective LOE management demands the creation of a detailed, multi-year timeline. This timeline should meticulously map out all key milestones and decision points in the years, months, and even days leading up to patent expiration.13 Such a roadmap ensures that all strategic actions are coordinated and executed with precision, minimizing surprises and maximizing the impact of each defensive maneuver.

Maximizing Current Drug Value and Pricing Optimization

Even as LOE approaches, a disciplined approach to pricing remains critical for maximizing the value extracted from the innovation during the pre-LOE period.13 This involves a nuanced understanding of how the product’s innovation translates into tangible value drivers for customers. These drivers might include superior efficacy, a more favorable side effect profile, enhanced convenience for patients, or broader cost savings within the healthcare system.13 By clearly articulating and demonstrating this value, companies can justify their pricing strategy and prepare the market for the impending shift.

Value-Based Pricing and Strategic Price Adjustments

One common tactic observed in the pre-LOE period is “surge pricing.” This involves adopting systematic price increases, often multiple times a year, in the 12 to 18 months leading up to patent expiry, with the aim of maximizing earnings before generic entry.24 For example, one major pharmaceutical company gradually increased the wholesale acquisition cost (WAC) of its nerve pain medication starting three years before LOE, anticipating the looming revenue cliff.24 Similarly, another company raised the price of its multiple myeloma drug by over 50% between 2016.24 However, this strategy requires careful management, as historical analysis suggests that price increases greater than 9% can negatively impact revenues and profits.24 This suggests that pre-LOE pricing isn’t solely about immediate revenue maximization; it also serves as a strategic signal to the market and potential generic entrants. A carefully managed, aggressive but not excessive, price increase might signal strong brand value and a robust defense strategy, potentially influencing generic pricing decisions or market entry timing. Conversely, a poorly managed surge could alienate payers and patients, inadvertently accelerating the switch to generics.

Beyond direct price increases, dynamic rebate strategies are crucial for aligning with the evolving motivations of Pharmacy Benefit Managers (PBMs) and other payers. As LOE nears, payers often adopt a “generic first” approach, seeking to funnel patients towards generics as quickly as possible. This dynamic creates an opportunity for manufacturers to offer heavy rebates on line extensions or next-generation brands, incentivizing payers to facilitate patient switching to these newer, still-exclusive products.24

Furthermore, implementing innovative contracts with pharmacies, distributors, and wholesalers can significantly expand market reach and preference for the branded product. Strategies such as volume discounts, bundled product offerings, and service discounts are commonly employed to incentivize these channels to stock and dispense preferred brands, thereby inhibiting generic substitution to some extent.24 Value-based arrangements tied to patient outcomes or strategic price reductions can also make the branded product more competitive against anticipated generic pricing, demonstrating its continued value beyond just the molecule.13

In the high-stakes environment leading up to LOE, vigorously protecting intellectual property is paramount. Companies must pursue all reasonable avenues to safeguard their innovations, including filing for additional patents and aggressively defending existing ones against challenges.13

Evergreening and Patent Litigation

“Evergreening” is a common and sophisticated practice employed by pharmaceutical companies to extend patent protection for as long as possible.4 This involves applying for subsequent patents related to a single medicine, covering aspects such as isomers, metabolites, prodrugs, new drug formulations (e.g., extended-release versions), or fixed-dose combinations.3 Patents can also be filed on manufacturing processes or delivery methods.4 These tactics create a complex web of patents that generic manufacturers must navigate, effectively delaying their market entry.4

Alongside evergreening, aggressive patent litigation is a key defensive strategy.13 Innovator companies often vigorously defend their existing patents against challenges from generic manufacturers. While generic companies may challenge remaining patents in court (e.g., through Paragraph IV certifications), a risky but potentially faster route to market entry if successful, the innovator’s defense can significantly delay generic competition.4 AbbVie’s successful patent defense of Humira (adalimumab) stands as a prime example, demonstrating that it is possible to protect sales even as rival biosimilars seek to enter the market.13 Similarly, Novartis proactively filed a citizen petition to the FDA, requesting that the regulator not approve drug applications referencing Entresto and specific patents related to it, showcasing a preemptive legal maneuver.14 The success of IP defense directly impacts the commercial runway. Strong IP protection provides the crucial time and space for commercial teams to implement patient loyalty programs, explore new formulations, or prepare for an authorized generic launch. Without robust IP, commercial strategies become reactive and significantly less effective. This underscores the critical need for tight integration between legal and commercial teams in LOE planning, with IP strategy informing and enabling commercial decisions.

Beyond the traditional patent term extensions, various regulatory exclusivities offer additional, fixed periods of market protection.2 These are distinct from patents but contribute significantly to the overall period of market exclusivity.

One particularly valuable regulatory incentive is Pediatric Exclusivity (PED). This provision grants pharmaceutical companies an additional six months of market exclusivity if they conduct pediatric studies in accordance with FDA requirements.2 The benefits of PED are multi-faceted: it can lead to increased revenue, with estimates suggesting an average value of $50 million to $100 million per drug.25 It also enhances market share and bolsters the company’s reputation by demonstrating a commitment to developing safe and effective medications for children.6 Uniquely, Pediatric Exclusivity attaches to all existing patents and exclusivities on

all drug products held by the sponsor for that active moiety at the time of its grant.2 This means a single pediatric study can extend the market protection across an entire portfolio of related products.

To maximize the benefits of PED, companies must conduct high-quality pediatric studies, ensure impeccable data quality and integrity, thoroughly understand FDA review processes and timelines, and prepare effective submissions and responses to FDA queries.25 The relatively short six-month period of Pediatric Exclusivity, while financially beneficial, serves a larger strategic purpose. It acts as a crucial “bridge,” providing a strategic window for companies to finalize and implement their broader post-LOE strategies, such as launching an authorized generic or transitioning to an over-the-counter (OTC) formulation, without immediate, full-scale generic competition. It is a tactical delay that buys crucial time for a more comprehensive transition, rather than a standalone, long-term profit driver.

Other significant regulatory exclusivities include New Chemical Entity (NCE) Exclusivity, which grants 5 years of protection for drugs containing a new active moiety.2 Orphan Drug Exclusivity (ODE) provides 7 years for drugs treating rare diseases.2 The GAIN Exclusivity adds 5 years to certain exclusivities for qualified infectious disease products (QIDPs).2 Additionally, there are 180-day exclusivities for Abbreviated New Drug Applications (ANDAs) related to Patent Challenges and Competitive Generic Therapy.2 These various forms of exclusivity underscore the intricate regulatory landscape that pharmaceutical companies must expertly navigate to extend product value.

Lifecycle Management (New Formulations, Indications, Combination Therapies)

Differentiate from generics, prolong life cycle, create new IP, expand market 3

Ongoing

Targeted Marketing & Real-World Evidence (RWE)

Communicate differentiated value, support use in specific populations, justify value 13

Ongoing

Transition to Over-the-Counter (if viable)

Maintain/grow volume, acquire new customers, protect long-term revenue 20

Ongoing

Build Resilient Business Models (Diversification, Partnerships)

Reduce reliance on single drugs, explore new areas, foster innovation 15

Sustaining Momentum: Strategies During and After LOE

Loss of Exclusivity is not the end of a pharmaceutical product’s journey; rather, it is a significant milestone that, much like a market launch, demands strategic planning and meticulous management to ensure optimal returns on investment.16 The period during and after LOE calls for a fundamental shift in strategy, moving from a position of monopoly to one of competitive differentiation and value retention.

Lifecycle Management Through Innovation

A cornerstone strategy for sustaining product value post-LOE is continuous lifecycle management driven by innovation. This involves extending the product’s commercial life by developing variations of the originator product and securing new patents for these advancements.3 This requires a sustained commitment to focused research and development, even for mature products.17

New Formulations and Delivery Systems

One of the most effective ways to differentiate a branded product from generic competitors after LOE is through the development of improved formulations or novel delivery systems. These innovations can provide additional patent protection, creating new barriers to entry for generics, and offer meaningful clinical advantages that justify continued preference for the branded product.13

Consider the possibilities: extended-release formulations that require less frequent dosing, significantly enhancing patient convenience and adherence.3 Or perhaps alternative administration routes, such as injectables, transdermals, or inhalables, which might cater to specific patient needs or improve drug bioavailability.26 Formulations with improved stability, reduced side effects, or pediatric-specific adaptations addressing unmet needs in younger populations also fall into this category.3 These activities, coupled with rigorous clinical trials to generate new data on the improved product, can further differentiate it from generic alternatives, prolong its commercial life cycle, and create unique selling propositions that resonate with prescribers and patients.17 This approach highlights that lifecycle management is not merely about adding years to a patent; it is about the continuous evolution of the product’s value proposition, effectively creating a “new” product from an old one to meet evolving patient needs and expand into new markets. This necessitates agile R&D and market access teams capable of rapidly identifying and capitalizing on these evolutionary pathways.

Exploring New Indications and Combination Therapies

Another powerful avenue for extending product value is the exploration of new indications. This refers to the discovery of new evidence suggesting additional medical applications for an existing drug or procedure.27 For pharmaceutical companies, this represents a highly attractive proposition, as investors often view new indications as a bullish indicator, anticipating new revenue streams at a relatively low cost.27 Repurposing existing drugs for new uses can significantly reduce research and development (R&D) costs compared to developing entirely new drugs, as the existing safety data often streamlines the development process. While obtaining final FDA approval for repurposed drugs still involves substantial costs, the reduced risk compared to de novo drug development makes it a compelling investment.27 The FDA actively supports this approach, frequently approving previously approved drugs for new uses and broader patient populations.30

Beyond single-drug repurposing, the development of combination therapies offers another strategic pathway. This involves combining two or more compounds with different mechanisms of action, an approach that has shown promise in increasing the success rate of drug repositioning efforts.28 Such combinations can be part of a broader strategy to enhance patient access to therapies, with pricing models designed to reflect their combined value to patients and the healthcare system.31 This highlights that lifecycle management is a continuous process of evolution, not just extension. It’s about reinventing the product to meet evolving patient needs, expand into new markets, and create new intellectual property, effectively creating a “new” product from an old one.

Preserving Brand Equity and Patient Loyalty

Even as generic competition floods the market, preserving brand equity and fostering patient loyalty become paramount for slowing brand erosion and sustaining sales momentum. This requires a strategic shift in focus from traditional marketing and sales activities aimed at maximizing pre-LOE sales to a new set of efforts centered on patient acquisition and, critically, retention.20

Patient Support and Loyalty Programs (e.g., Copay Cards)

Patient support programs (PSPs) are indispensable tools for maintaining market share post-LOE.13 Pharmaceutical companies invest approximately $5 billion annually in these programs, which are designed to help patients access, afford, and adhere to their medications.32 These programs can encompass a range of services, including financial assistance, adherence support, and enhanced services that generic competitors cannot easily replicate.13

A particularly effective tactic is the strategic use of copay cards. Innovator companies can transition patients to copay card programs three to six months before LOE. This helps drive affordability and reduces patient out-of-pocket (OOP) expenses to levels equivalent to or even lower than generics, thereby helping to maintain sales volume and mitigate profit erosion.21 Additionally, enrollment programs, such as mail-order services, can be established to collect patient information, facilitating targeted interactions like refill notices and reminding patients of the branded product’s continued availability even after generics have launched.22

Despite the significant investment, a major challenge lies in the awareness gap: only 3% of patients utilize PSPs, and a staggering 59% have little to no knowledge of these valuable resources. Even 42% of prescribers are unfamiliar with these programs.32 Bridging this awareness gap is critical for PSPs to fulfill their purpose. This requires a dual approach: leveraging technology to empower patients and providers with accessible solutions (e.g., online scheduling, secure messaging, telehealth) and strengthening the human touch through expert guidance and personal support to navigate challenges.32 The significant investment in and focus on PSPs and loyalty efforts after LOE, despite generic entry, highlights that price is not the

only driver for patients. The low utilization of PSPs, despite high investment, points to a critical awareness and accessibility gap. The deeper observation is that patient loyalty, cultivated through support, convenience, and perceived value, becomes a vital “moat” against generic erosion. This means that post-LOE marketing must shift from being purely product-centric to genuinely patient-centric, focusing on the entire patient journey and leveraging technology to make support seamless, thereby converting existing brand affinity into sustained adherence and sales volume.

Targeted Marketing and Communication Post-LOE

In the post-LOE environment, commercial teams must refine their communication strategies to effectively convey the differentiated value that the branded product continues to offer across various customer segments.13 This communication is crucial for building a lasting perception of value that can help maintain loyalty even after generic entry.13

A powerful tool in this regard is the generation and dissemination of real-world evidence (RWE). RWE, derived from real-world data (RWD) collected outside traditional clinical trials (e.g., electronic health records, medical claims, patient registries) 29, can demonstrate the product’s value in everyday clinical practice. This evidence can support the branded drug’s continued use in specific patient populations or clinical scenarios where generics might be perceived as less suitable, thereby justifying its premium position.13 RWE, while used across the drug lifecycle, takes on new strategic significance post-LOE. In a market flooded with cheaper generics, RWE provides the

evidence to justify continued preference for the branded drug by demonstrating superior real-world outcomes, safety profiles, or cost-effectiveness in specific patient populations. This implies that RWE is not just for regulatory approval but becomes a crucial commercial tool for value-based pricing and negotiation with payers, effectively shifting the competitive battleground from patent protection to demonstrable real-world value.

Strategic Market Entry: Authorized Generics and OTC Formulations

As generic alternatives become inevitable, innovator companies can strategically participate in the generic market themselves, turning a potential threat into a controlled opportunity. This involves profiting directly from patients who migrate to generic alternatives by offering their own generic version.22

The Authorized Generic Model

The authorized generic (AG) model involves the innovator company manufacturing a generic version of its own branded drug or partnering with another party to do so.20 While seemingly counterintuitive, as it introduces internal competition, this strategy offers significant benefits. It allows the innovator company to retain a higher portion of the product’s value with relatively low implementation costs.20 Furthermore, it helps protect market share by capturing a segment of the generic market, enables the implementation of price segmentation strategies across branded and generic offerings, utilizes existing production capacity more efficiently, and maintains quality control over the generic versions of their products.26 Speed to market is paramount for the success of an AG, as it allows the company to capture market share quickly and lock in contracts with distributors and wholesalers.22 Pfizer’s post-patent success with Lipitor, which included launching an authorized generic through a partnership with Watson Pharmaceuticals, serves as a compelling example of this strategy in action.26 The launch of an authorized generic, while appearing to cannibalize the innovator’s own branded drug, is in fact a strategy of

controlled cannibalization. The underlying understanding is that if generic entry is inevitable, the innovator company can proactively capture a segment of the generic market by leveraging its existing manufacturing, distribution, and regulatory expertise. This allows them to maintain some control over pricing and market share, mitigating the full impact of external generic competition, rather than ceding the entire market to competitors. It is a pragmatic acceptance of market realities to salvage value.

Transitioning to Over-the-Counter (OTC)

For certain products, transitioning to an Over-the-Counter (OTC) formulation presents another viable strategy to maintain and even grow volume post-LOE.20 This approach can significantly decelerate value erosion, help retain current customers, attract new ones, and protect the branded product’s long-term revenue stream.22 A key advantage of an OTC strategy is gaining access to a broader base of potential patients, as it removes many of the reimbursement hurdles associated with prescription drugs.22

However, the viability of an OTC transition hinges on whether the existing prescription product, or a modified version thereof, can satisfy the FDA’s strict OTC approval criteria. These considerations include the ease of symptom identification by consumers, the product’s safety profile, its potential for misuse or abuse, the complexity of the dosing regimen, and the patients’ ability to self-manage their condition.22 If these criteria can be met, a two-pronged strategy involving both the prescription product and an OTC version may be highly appropriate. If not, doubling down on the existing prescription strategy or exploring other LOE tactics might be more prudent.22

The Power of Data: Transforming Insights into Market Domination

In an increasingly competitive pharmaceutical landscape, the ability to transform raw data into actionable intelligence has become a cornerstone of innovation, particularly for navigating the complexities of Loss of Exclusivity (LOE).33 Data analytics plays a pivotal role in reducing uncertainties throughout the drug development lifecycle, streamlining operations, and significantly increasing overall efficiency.35

Leveraging Real-World Evidence (RWE) for Post-LOE Value

Real-world evidence (RWE) is emerging as a game-changer in the post-LOE environment. It is derived from real-world data (RWD), which encompasses health-related information routinely collected from diverse sources outside traditional randomized clinical trials. Examples of RWD include electronic health records (EHRs), medical claims data, patient registries, and data gathered from digital health technologies and wearable devices.29 RWE, then, is the clinical evidence about the usage and potential benefits or risks of a medical product, generated through the analysis of this RWD.29

RWE serves as a crucial complement to traditional clinical trial data, offering invaluable insights into treatment effectiveness, safety, and healthcare outcomes as they unfold in real-world settings.33 The FDA has a long-standing history of utilizing RWD and RWE for post-market safety surveillance of approved drugs and is increasingly open to its use for supporting effectiveness claims and broader regulatory decisions.34

RWE in Regulatory Submissions and Payer Negotiations

The applications of RWE extend significantly into regulatory and commercial realms. For instance, RWE can provide compelling support for regulatory submissions seeking new drug indications or modifications to existing labeling. It also plays a vital role in monitoring the long-term safety and effectiveness of medicines after approval, moving beyond the controlled environment of clinical trials.29

Furthermore, RWE profoundly influences payer decisions. It helps payers evaluate coverage and reimbursement policies, supports the implementation of outcome-based pricing models, and provides physicians with data highly relevant to their specific patient populations.29 This capability to demonstrate a drug’s value proposition through real-world outcomes can be instrumental in negotiating favorable formulary positions post-LOE.13 By leveraging RWE, pharmaceutical companies can shift the conversation from mere efficacy to demonstrable value in everyday clinical practice, a powerful differentiator when facing generic price competition.

However, leveraging RWE is not without its challenges. Data fragmentation, where information is scattered across myriad siloed sources, presents a significant hurdle. Issues of data quality and completeness, as well as complex regulatory and privacy constraints (e.g., HIPAA, GDPR), also require careful navigation.33 Despite these complexities, building a robust data ecosystem that integrates diverse RWD sources and employs advanced analytics, while prioritizing regulatory compliance, is essential for unlocking the full potential of RWE.

Advanced Data Analytics and Predictive Modeling

The sheer volume of data generated in the pharmaceutical industry, from clinical trials to patient outcomes, necessitates sophisticated data analytics tools. These tools are adept at transforming complex datasets into actionable insights, enabling companies to make more accurate predictions and streamline their operations.35

Optimizing Commercial Strategies with Data

Predictive analytics, a subset of data mining techniques that analyze historical data to forecast future outcomes, is revolutionizing how pharmaceutical companies approach LOE. It helps forecast drug efficacy and potential side effects, predict clinical trial outcomes, thereby reducing R&D costs, and significantly accelerating time to market for new drugs.36 For instance, machine learning algorithms can be used to predict adverse drug reactions by examining previous clinical trial data and patient electronic health records.36 Beyond drug development, predictive analytics can optimize manufacturing processes and supply chain management by accurately forecasting demand spikes and identifying potential disruptions, as exemplified by Pfizer’s use of AI and predictive analytics to drastically reduce the timeline for bringing the COVID-19 vaccine to market and ensure efficient global distribution.36

In the commercial sphere, predictive analytics can identify high-value target segments, allowing for optimized promotional efforts and maximized return on investment.37 It provides granular visibility into key performance indicators such as prescription volume, market share, sales growth rates, and patient adherence rates.35 This enables a proactive, data-driven LOE strategy. By anticipating market shifts, competitive entries, and patient behaviors, companies can pre-emptively adjust pricing, launch patient programs, or initiate authorized generic production with greater precision, thereby minimizing the “cliff” effect. This transforms LOE from a reactive threat into a manageable, data-informed transition.

Furthermore, data analytics plays a crucial role in cost reduction by identifying unnecessary expenses and streamlining processes, leading to substantial operational savings.35 It also enhances drug safety by facilitating the early detection of potential risks, allowing for proactive preventive measures.35 The ability to break down data silos and integrate disparate data sources is critical for effective analytics, enabling a holistic view of the market and operational landscape.36

The Role of Patent Intelligence Platforms (e.g., DrugPatentWatch)

Navigating the intricate landscape of pharmaceutical patents and competition demands specialized tools. Patent intelligence platforms, such as DrugPatentWatch, provide deep, centralized knowledge on pharmaceutical drugs, encompassing patents, suppliers, generics, formulations, and more.38 These platforms integrate vast amounts of data from authoritative sources like the US Food and Drug Administration (FDA) and the United States Patent and Trademark Office (USPTO), as well as international government bodies.38

Identifying Opportunities and Monitoring Competition

DrugPatentWatch serves as an indispensable tool for branded pharmaceutical companies engaged in global business intelligence and forecasting.38 It allows users to accurately predict branded drug patent expiration dates, identify potential generic suppliers, and proactively manage inventory to prevent overstocking of off-patent drugs.38 The platform’s comprehensive database provides critical competitive intelligence, including data on patent litigation, tentative approvals, clinical trials, Paragraph IV challenges (where a generic manufacturer asserts a patent is invalid or not infringed), and information on top patent holders.38 This allows companies to assess the past successes of patent challengers and gain insights into the research paths of their competitors.38

For generic manufacturers, such platforms are equally vital. They help identify profitable generic drug opportunities by enabling a thorough understanding of the patent landscape and the assessment of patent vulnerabilities, such as prior art that might invalidate a patent, overly broad claims that could be challenged, or potential design-around solutions that avoid infringement.23 The platforms also facilitate the evaluation of market opportunities, considering factors like current annual sales of the branded product, historical price erosion patterns for similar generic market entries, patient population size, and the reimbursement landscape.23 This allows for the identification of first-time generic entrants and the anticipation of future formulary budget requirements.38 The sheer volume and complexity of patent information, including evergreening tactics and Paragraph IV challenges, make manual tracking nearly impossible. These platforms serve as a

strategic compass, providing real-time competitive intelligence that allows companies to not only monitor threats but also identify new opportunities, such as underserved markets or patent vulnerabilities for generic entry. This enables more informed portfolio management, R&D decisions, and market entry timing, transforming a potential blind spot into a source of competitive advantage.

DrugPatentWatch offers various features to support these analyses, including searching by pharmacology, patent expiration year, approval date, finished product suppliers, dosage, and even by DMF holder or pharmaceutical class.39 It also provides email alerts and data export capabilities, ensuring that users can keep their data and stay informed of critical market shifts.38

“The pharmaceutical industry is facing an unprecedented wave of patent expirations, with more than 190 products set to lose exclusivity between 2022 and 2030, putting over $300 billion in sales at risk between 2023 and 2028.” 13

Case Studies in Resilience: Learning from Industry Leaders

Examining how leading pharmaceutical companies have navigated the patent cliff provides invaluable lessons and demonstrates that Loss of Exclusivity (LOE) does not have to spell doom for branded drug revenue streams.20 These real-world examples illustrate the effectiveness of various strategic approaches and the importance of adaptability.

Success Stories in Navigating the Patent Cliff

Several companies have showcased remarkable resilience in the face of LOE, transforming a period of potential decline into one of sustained value.

AbbVie’s Humira (adalimumab) stands as a monumental case study. Despite being one of the most profitable drugs in history and facing the inevitable onslaught of biosimilar competition, AbbVie successfully protected its sales through a robust and aggressive patent defense strategy.9 This multi-layered legal approach, involving numerous patents covering various aspects of the drug, effectively delayed the widespread entry of biosimilars for an extended period, allowing AbbVie to maintain significant market share and revenue. This case powerfully highlights the critical role and potential power of a strong intellectual property strategy in mitigating the immediate impact of LOE.

Pfizer’s Lipitor (atorvastatin), a former blockbuster cholesterol-lowering drug, faced a dramatic revenue drop after losing its patent. However, Pfizer implemented a multi-pronged approach to value extraction. This included strategic cost reductions across its operations to maintain profitability even with lower prices. Simultaneously, the company launched patient assistance programs aimed at preserving brand loyalty, recognizing that some patients might prefer the original brand due to familiarity or perceived quality. Crucially, Pfizer also launched an authorized generic version of Lipitor through a partnership with Watson Pharmaceuticals.10 This allowed Pfizer to directly participate in the generic market, capturing a portion of the sales that would otherwise have gone entirely to external generic manufacturers. This comprehensive strategy demonstrates the effectiveness of combining cost control, patient engagement, and a direct stake in the generic market.

Merck’s Keytruda (pembrolizumab), a leading cancer immunotherapy, is a forward-looking example. Facing patent expiration in 2028, which poses significant financial exposure with projected sales declines 12, Merck is proactively positioning new assets like WINREVAIR as key pillars in its future growth strategy.15 This exemplifies a proactive pipeline diversification approach, where the company invests heavily in developing and bringing to market next-generation therapies to offset the anticipated revenue loss from an expiring blockbuster. Robert Davis, Chairman of the Board, President, and Chief Executive Officer of Merck, emphasized this strategy, stating, “We are positioned for long-term leadership in oncology as we continue to diversify and deepen our pipeline. In immunology, HIV, and ophthalmology, we have opportunities to bring forward first-in-class and/or best-in-class blockbuster medicines”.15 This strategic focus on continuous innovation and pipeline replenishment is essential for long-term success in the face of recurring patent cliffs.

It is also worth noting that not all originator drugs experience immediate and catastrophic market share loss. Some have managed to maintain over 70% market share eight quarters after the first generic entry.19 This demonstrates that with effective, tailored measures, a significant loss is not always inevitable, and the impact of LOE can indeed vary depending on the brand and category of the drug.1 The variety of successful LOE strategies observed across these case studies, from robust IP defense to multi-pronged commercial approaches and pipeline diversification, underscores a crucial point: there is no single “silver bullet” solution. The most effective LOE strategy is a

customized portfolio of tactics, meticulously tailored to the specific drug, its market dynamics (e.g., small molecule vs. biologic), the competitive landscape, and the company’s internal capabilities. This necessitates a diagnostic approach to LOE planning, identifying the most potent levers for each product.

Lessons Learned from Challenging Transitions

While success stories offer inspiration, challenging transitions provide equally valuable lessons, highlighting common pitfalls and the critical need for adaptability.

One overarching lesson is the imperative for profound adaptation: “What got you to this point, will not take you further”.17 Companies must be prepared to make fundamental adjustments in their strategies and operations in the face of new competition.17 This includes re-evaluating internal processes, acquiring new skills and capabilities, and even restructuring teams and headcounts.17 The need for “adjustments in the face of new competition,” “establishing new processes,” and “reviewing headcounts and the composition of your teams” highlights that LOE is not just a commercial or legal challenge, but an

organizational one. The deeper understanding is that successful navigation of the patent cliff is a strong indicator of a pharmaceutical company’s overall organizational agility and adaptability. Companies that can quickly pivot marketing, sales, R&D, and even internal structures are better positioned to sustain value. This implies that investments in organizational flexibility and cross-functional collaboration are critical long-term assets.

The impact of LOE is not uniform; it varies significantly depending on the brand and the category of the drug.1 For instance, while small molecule drugs often face rapid market share erosion, biologics may experience a slower decline due to the complexities and higher costs associated with biosimilar development and market entry.13 This variability underscores the need for highly customized LOE strategies rather than generic approaches.

Perhaps the most critical lesson is the absolute importance of early and proactive planning. Proactive planning is paramount to safeguard medicines from the patent cliff.1 Delaying LOE efforts can significantly diminish their impact, making it far more challenging to mitigate revenue loss and maintain market presence.22 The window for effective intervention shrinks rapidly as LOE approaches, emphasizing that strategic foresight is a company’s most valuable asset in this challenging phase.

Finally, many drugs approaching LOE today are specialized therapies, often targeting smaller patient populations or rare diseases.10 These specialized markets present unique complexities, requiring highly tailored approaches to maintain market presence and value. The strategies that work for a mass-market blockbuster may not be effective for a niche orphan drug, necessitating a deeper understanding of the specific market dynamics and patient needs.

The Future of Pharmaceutical Value Maximization

The pharmaceutical industry stands at a critical juncture, facing an unprecedented wave of patent expirations that threaten billions in revenue. Yet, this challenging period is not merely a threat; it is, fundamentally, an “invitation to innovate”.11 Rather than viewing Loss of Exclusivity (LOE) as a terminal event, leading companies are reframing it as an opportunity to become stronger, faster, and more future-ready.11 The future of pharmaceutical value maximization hinges on a proactive, multi-faceted approach that transcends traditional product lifecycles and embraces continuous evolution.

Embracing Innovation as a Continuous Strategy

The imperative for innovation in the post-LOE era extends far beyond the discovery of new molecular entities. It encompasses a continuous commitment to improving existing products and exploring novel applications. This includes developing new formulations, optimizing delivery mechanisms, exploring combination therapies, and identifying new indications for established drugs.17 This approach highlights that lifecycle management is not merely about extending a product’s patent life; it is about the continuous evolution of its value proposition. It is about reinventing the product to meet evolving patient needs, expand into new markets, and create new intellectual property, effectively creating a “new” product from an old one.

The revenue generated during a drug’s period of exclusivity is critical for fueling this ongoing innovation. A substantial portion of profits is typically reinvested into research and development, which is essential for discovering and developing future drug therapies.3 This creates a virtuous cycle where current commercial success directly enables future scientific breakthroughs and pipeline replenishment. To accelerate this cycle and access diverse expertise, strategic partnerships and collaborations are becoming increasingly vital. These alliances can help identify novel applications for existing compounds, facilitate the development of improved formulations or delivery systems, generate new intellectual property through collaborative research, and provide access to specialized expertise and research capabilities that might not exist in-house.26

Building Resilient Business Models

The recurring nature and increasing scale of the patent cliff necessitate a fundamental shift towards building inherently resilient business models. This goes beyond managing individual drug LOEs; it is about cultivating a robust corporate structure that can withstand and thrive amidst market shifts.

A key component of this resilience is diversification. Companies must strategically diversify their pipelines, exploring new therapeutic areas or market segments to reduce over-reliance on single blockbuster drugs.15 This often involves a strategic re-allocation of R&D resources and a greater emphasis on mergers and acquisitions or partnerships for pipeline replenishment, ensuring a continuous stream of innovative therapies to offset inevitable revenue losses and maintain sustained growth. This creates a “portfolio resilience” imperative, where the focus moves from individual product survival to the health of the entire portfolio.

Furthermore, value-aligned pricing will be crucial. As generic competition drives down prices, innovator companies must explore innovative pricing models, such as value-based pricing and risk-sharing agreements. These models allow companies to maintain price points by emphasizing the distinctive attributes of their products, such as enhanced efficacy, superior safety profiles, or greater patient convenience, directly linking cost to proven outcomes.17 This shifts the competitive battleground from price alone to demonstrable real-world value.

Finally, embracing digital transformation is no longer optional but a necessity. Leveraging digital solutions and rethinking traditional workflows can significantly maximize a company’s chances of success.11 This includes the widespread adoption of data analytics for promotion optimization, precise patient targeting, and stringent cost control.37 The future of pharmaceutical companies will depend on their ability to integrate technology, data, and patient services into a holistic offering that extends beyond the chemical compound itself. This creates an “ecosystem-centric value creation model,” where value is derived not just from the drug, but from the surrounding services, data insights, and demonstrable real-world outcomes, forming a competitive barrier that generics cannot easily replicate.

The overarching message is clear: LOE is not the end. It is the beginning of a smarter, stronger, and more resilient operational paradigm.13 History shows that many brands have successfully managed sales declines and maintained profitability for five or more years post-LOE.21 By proactively embracing innovation, building diversified portfolios, and leveraging the power of data, pharmaceutical companies can transform the patent cliff from a looming threat into a catalyst for sustained growth and market leadership.

Key Takeaways

LOE is Inevitable but Manageable: Loss of Exclusivity (LOE) is a predictable phase in a drug’s lifecycle, marking the expiration of patent and exclusivity protections. While it leads to significant revenue erosion and market share loss due to generic competition, it is not an insurmountable challenge if approached strategically.

Proactive Planning is Paramount: The most effective LOE strategies begin years in advance (ideally two years pre-LOE), involving comprehensive market analysis, strategic pricing adjustments, and robust intellectual property defense. Delaying these efforts significantly diminishes their impact.

Beyond the Molecule: Value from Innovation and Service: Sustaining product value post-LOE requires continuous lifecycle management through innovation, including new formulations, delivery systems, and exploring new indications or combination therapies. Additionally, preserving brand equity and patient loyalty through patient support programs and targeted communication becomes critical differentiators.

Strategic Market Participation: Innovator companies can mitigate losses by strategically participating in the generic market through authorized generics or by transitioning products to over-the-counter (OTC) formulations, allowing them to retain a portion of the market value.

Data as a Strategic Asset: Leveraging real-world evidence (RWE) for regulatory submissions and payer negotiations, coupled with advanced data analytics and predictive modeling, enables companies to make data-driven decisions, optimize commercial strategies, and identify new opportunities in a competitive landscape. Patent intelligence platforms like DrugPatentWatch are essential tools for competitive intelligence and forecasting.

Organizational Agility and Diversification: Successful navigation of the patent cliff requires organizational agility, the ability to adapt operational models, and a commitment to pipeline diversification. This builds resilient business models that can withstand future LOE events and ensure long-term growth.

FAQs

1. What is the fundamental difference between a drug patent and market exclusivity?

While both patents and market exclusivities grant periods of protection, they originate from different legal frameworks and have distinct characteristics. A drug patent is a property right granted by the United States Patent and Trademark Office (USPTO), typically lasting 20 years from the filing date, and can cover the drug molecule, manufacturing processes, or new formulations.2 It can be issued or expire at any time, regardless of the drug’s approval status.2 Market exclusivity, on the other hand, refers to statutory delays or prohibitions on the approval of competitor drugs granted by the FDA, attaching upon the approval of a drug or certain supplements.2 These periods are fixed (e.g., 5 years for New Chemical Entity, 7 years for Orphan Drug, 6 months for Pediatric Exclusivity) and are designed to balance innovation with public access.2 They may or may not run concurrently with patents.2

2. How significant is the “patent cliff” currently impacting the pharmaceutical industry?

The current “patent cliff” is substantial and represents an unprecedented challenge. Over 190 pharmaceutical products are projected to lose exclusivity between 2022 and 2030, putting more than $300 billion in sales at risk between 2023 and 2028.11 This is a significant increase compared to previous patent cliffs, such as the 2016 period which eroded $100 billion in brand-name sales.13 The impact is particularly complex now due to a higher proportion of biologics facing LOE, as biosimilars typically gain market share more slowly than small molecule generics, altering the dynamics of revenue erosion.13

3. Can a branded drug company truly maintain profitability after its patent expires, or is it an inevitable decline?

While a significant decline in sales and profitability is common, it is not always an inevitable or permanent alteration of brand profitability.1 Many brands have successfully managed sales declines and maintained profitability for 5+ years post-LOE.21 This is achieved through strategic measures such as launching authorized generics, transitioning to over-the-counter (OTC) formulations, implementing patient support and loyalty programs, continuous lifecycle management through new formulations or indications, and leveraging real-world evidence to demonstrate continued value.13 The key lies in proactive planning and agile adaptation to the new competitive landscape.

4. How do patient support programs (PSPs) help a branded drug after Loss of Exclusivity?

Patient support programs (PSPs) are crucial for maintaining market share and patient loyalty after LOE, even when generic alternatives are available at lower costs. These programs, which receive significant investment from pharmaceutical companies (around $5 billion annually), offer financial assistance, adherence support, and enhanced services that generic competitors often cannot easily replicate.13 By reducing out-of-pocket expenses (e.g., through copay cards) and providing ongoing support, PSPs help maintain sales volume and reduce the velocity of profit erosion by fostering continued patient preference for the branded product.21 However, their effectiveness hinges on bridging the significant awareness gap, as many patients and even prescribers are currently unfamiliar with these valuable resources.32

5. What role do data analytics and platforms like DrugPatentWatch play in mitigating LOE impact?

Data analytics and patent intelligence platforms are indispensable tools for mitigating the impact of LOE. Advanced data analytics, including predictive modeling, helps pharmaceutical companies forecast market shifts, optimize R&D costs, streamline supply chains, and identify high-value target segments for marketing efforts.35 This allows for proactive, data-driven LOE strategies. Platforms like DrugPatentWatch provide comprehensive, centralized intelligence on drug patents, generic entries, litigation, and market opportunities.38 They enable companies to predict patent expirations, identify generic suppliers, assess competitive threats, and uncover new value opportunities, transforming complex data into actionable insights for strategic decision-making.23