A deep-dive for pharma/biotech IP teams, R&D leads, and institutional investors on PBM market power, formulary mechanics, IP asset valuation, regulatory risk, and structural reform.

The PBM Market at a Glance: Scale, Concentration, and Why It Matters Now

Three companies — CVS Caremark, Express Scripts (now part of Cigna’s Evernorth health services division), and OptumRx (a subsidiary of UnitedHealth Group’s Optum) — control roughly 80% of all U.S. prescription drug claims processing. To put that in dollar terms: the U.S. prescription drug market exceeded $600 billion in total spending in 2024, meaning the Big Three exercise significant formulary influence over the coverage decisions affecting that entire market.

The PBM industry did not begin this concentrated. It arrived at near-oligopoly status through four decades of mergers, acquisitions, and what the Federal Trade Commission now formally describes as anticompetitive vertical integration. The FTC’s July 2024 interim staff report concluded that the largest PBMs have used their market power to inflate drug costs, steer patients toward affiliated pharmacies, and squeeze independent dispensers on reimbursement rates.

What makes 2025 structurally different from prior years is the simultaneous convergence of federal litigation (the FTC’s insulin-pricing lawsuit against all three Big Three PBMs), landmark state legislation (Arkansas banning PBM ownership of in-state pharmacies, effective 2026), and bipartisan congressional proposals (the Patients Before Monopolies Act) that would mandate structural separation between PBM and pharmacy assets. These are not regulatory abstractions. For pharma manufacturers, biosimilar developers, independent pharmacy operators, and plan sponsors, each of these pressures translates directly into formulary access risk, reimbursement rate volatility, and contract renegotiation exposure.

Key Takeaways — Section 1

The Big Three PBMs control approximately 80% of U.S. prescription claims processing, concentrating formulary leverage in three corporate structures.

2025 marks the first year all three simultaneously face federal antitrust litigation, landmark state structural reform, and active federal legislative proposals targeting their integrated business models.

For pharma IP teams and institutional investors, PBM regulatory risk is no longer a distant policy question — it is a near-term variable in drug pricing models, biosimilar access timelines, and specialty pharmacy revenue projections.

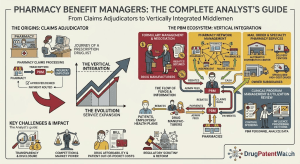

Origins: Claims Adjudication and the Pre-Digital Formulary Era (1960s-1989)

The Insurance-Driven Mandate for a Third Party

PBMs emerged not from pharmaceutical innovation but from an insurance industry problem. When commercial health insurers began adding outpatient prescription drug coverage to group health plans in the 1960s, they immediately encountered an administrative burden for which they had no internal infrastructure: pharmacies filed paper claims, eligibility verification was manual, and the volume of transactions made real-time benefit adjudication functionally impossible.

Third-party administrators stepped in to handle claims processing on behalf of insurers and self-insured employers. These early entities had a narrow mandate: receive a claim, verify patient eligibility against a benefit schedule, calculate the patient cost-sharing obligation, and remit payment to the dispensing pharmacy. Formulary management, as the term is understood today, did not exist. Coverage was largely open, and the administrative entity’s value was entirely operational.

The Plastic Card and the Electronic Claims Revolution

The 1970s saw PBMs take on the fiscal intermediary role more formally, adjudicating drug claims electronically and managing pharmacy payments. The introduction of the plastic drug benefit identification card was the first consumer-facing technology change: instead of submitting paper receipts for reimbursement, the patient presented a card at the pharmacy counter, and the transaction was processed in real time against the plan’s benefit file. The operational efficiency gain was significant — error rates dropped and payment cycles shortened from weeks to days.

The 1980s brought online, real-time electronic drug claims processing, which was the technological prerequisite for everything that followed. Once PBMs could receive, adjudicate, and store a prescription transaction in milliseconds, they accumulated claims data at scale. That data, covering prescribing patterns, drug utilization rates, therapeutic category trends, and patient adherence metrics, became the raw material for formulary construction, drug utilization review (DUR) programs, and, eventually, manufacturer rebate negotiations. The administrative function had grown a data infrastructure.

Early Formulary Construction and the Seeds of Market Power

The formulation of closed or preferred drug lists — what became the modern formulary — gained traction in the late 1980s as employers and insurers sought to manage rising drug costs by differentiating reimbursement levels across therapeutic equivalents. A drug placed on a preferred tier carried a lower patient copay; a non-preferred drug cost the patient more out of pocket. Manufacturers quickly recognized that formulary tier placement drove prescription volume, and the implicit negotiation between PBMs and manufacturers over what price concession would secure preferred placement was already underway before the term ‘rebate’ became standard industry language.

This is where the structural conflict first appeared, even if it went largely unrecognized at the time. The entity negotiating with manufacturers on behalf of payers — the PBM — had begun to accumulate discretion over which drugs patients would realistically use. That discretion had monetary value. The full commercialization of that value would take another decade.

Key Takeaways — Section 2

PBMs originated as pure administrative intermediaries, created to solve an insurance claims-processing problem in the 1960s.

Real-time electronic claims processing in the 1980s generated the prescription data infrastructure that enabled formulary management and eventually manufacturer rebate negotiations.

The formulary tier system gave PBMs discretionary control over therapeutic category market share before the industry had fully conceptualized that control as a negotiating asset.

The Consolidation Engine: M&A Timelines and the Birth of the Big Three

The Manufacturer Acquisition Wave and the FTC’s Response

The 1990s opened with a wave of pharmaceutical manufacturer acquisitions of PBMs. Merck acquired Medco Containment Services in 1993 for $6.6 billion, Smith Kline Beecham acquired Diversified Pharmaceutical Services, and Eli Lilly acquired PCS Health Systems. The strategic logic was straightforward: owning the formulary manager gave manufacturers a channel to preference their own drugs. The FTC identified the conflict immediately and ordered divestitures. Merck eventually spun off Medco; the others sold their PBM assets as well.

The FTC’s divestiture orders established a regulatory precedent — manufacturer-PBM co-ownership raises per se conflict-of-interest concerns — that the agency would not revisit with the same urgency when the integration ran in the other direction (PBMs merging with insurers and pharmacies) until the 2020s. The 1990s divestitures left a group of mid-sized independent PBMs that consolidated among themselves throughout the 2000s, steadily building the market concentration that the Big Three represent today.

The Consolidation Timeline: 2000-2019

The mergers that created the current oligopoly followed a two-phase pattern. Phase one, roughly 2000-2012, consolidated independent PBMs into the three dominant entities. Express Scripts acquired AdvancePCS in 2004. Caremark and RxAmerica merged in 2004. Express Scripts then acquired WellPoint’s NextRx unit and, most consequentially, Medco Health Solutions in 2012 — a $29.1 billion deal that the FTC reviewed for eight months before closing the investigation without challenging the transaction.

Phase two, 2015-2019, was vertical integration proper: PBMs merging upward into health insurers and downward into pharmacies and specialty pharmacy operators. OptumRx acquired Catamaran Corporation in 2015 for approximately $12.8 billion, consolidating pharmacy claims and specialty pharmacy operations. CVS Health acquired Aetna in 2018 for $69 billion, creating a structure in which a retail pharmacy chain, a PBM, a Medicare Part D plan sponsor, and a commercial insurer all sat under one corporate parent. That same year, Cigna completed its $67 billion acquisition of Express Scripts, pairing the second-largest U.S. commercial insurer with the country’s largest stand-alone PBM at the time.

Market Concentration Metrics

The American Medical Association’s 2024 analysis of PBM market concentration calculated a Herfindahl-Hirschman Index (HHI) for the commercial PBM market that exceeded 3,000 — a threshold the DOJ and FTC Merger Guidelines classify as highly concentrated. For context, markets above 2,500 HHI are presumptively anticompetitive under merger review standards. The PBM market has been operating at or above that threshold since approximately 2013.

Key Takeaways — Section 3

The FTC’s 1990s divestiture orders addressed manufacturer-PBM co-ownership but left insurer-PBM vertical integration largely unchallenged for two decades.

The Express Scripts/Medco merger in 2012 ($29.1 billion) and the CVS/Aetna and Cigna/Express Scripts deals in 2018 ($69 billion and $67 billion, respectively) were the structural events that locked in the current oligopoly.

The commercial PBM market operates at an HHI above 3,000, placing it firmly in the highly concentrated category by federal antitrust standards.

Vertical Integration Mechanics: How the Big Three Built Their Empires

CVS Health / Caremark / Aetna: IP and Asset Valuation

CVS Health’s vertical integration began in earnest in 2007 when CVS Corporation merged with Caremark Rx in a transaction valued at approximately $26.5 billion. The merger combined the largest U.S. retail pharmacy chain with the second-largest PBM, creating the first entity with meaningful ownership of both the formulary management function and the primary dispensing channel.

The strategic asset in the Caremark acquisition was not a patent portfolio in the conventional pharma sense, but rather a proprietary formulary management system, specialty pharmacy infrastructure (including Specialty Pharmacy Networks and the Accordant chronic disease management programs), and a mail-order fulfillment network that generated high-margin prescription volume outside retail pharmacy economics. Caremark’s specialty pharmacy revenue, which carries gross margins substantially above retail dispensing, represented the bulk of the acquisition’s IP-equivalent value.

The 2018 Aetna acquisition at $69 billion completed the integration stack. Aetna brought 22 million medical plan members, a Medicare Advantage footprint that CVS could cross-leverage with its pharmacy benefit administration, and a Part D plan sponsor license. The combined entity now controlled the member relationship at the insurance level, the formulary at the PBM level, and the point-of-dispensing at the retail and specialty pharmacy level. Any drug that a CVS/Aetna member took through a CVS retail pharmacy or CVS Specialty, adjudicated through Caremark, and covered by an Aetna plan, generated revenue at four distinct points for a single corporate entity.

The IP valuation relevant to pharma manufacturers and analysts is the formulary position itself. CVS Caremark’s 2025 formulary exclusion list, which the company publishes annually, excluded over 500 drug products from its standard formulary. Exclusion from a Caremark formulary affects access for its approximately 105 million covered members. The negotiating leverage that exclusion list represents is, functionally, the core asset of the integrated enterprise — more operationally significant than any individual patent or manufacturing facility.

Cigna / Express Scripts: IP and Asset Valuation

Cigna’s $67 billion acquisition of Express Scripts closed in December 2018, folding the largest stand-alone PBM into a combined entity now branded as Evernorth Health Services. Express Scripts, at acquisition, was processing over 1.4 billion adjusted prescription claims annually and had the largest rebate aggregation operation in the country through its affiliated GPO structures.

The intellectual property value in Express Scripts that justified the acquisition premium was concentrated in three areas. First, the formulary and rebate contracting systems — proprietary algorithms, manufacturer contract templates, and therapeutic category tiering logic developed over decades that could not be easily replicated. Second, the specialty pharmacy network, including Accredo Health Group, which Express Scripts acquired in 2012, focusing on high-touch dispensing for oncology, inflammatory, and rare disease therapies where margins are substantially higher than traditional retail. Third, the home delivery infrastructure — Express Scripts operated one of the largest mail-order pharmacy networks in the country, with manufacturing-scale fulfillment operations whose volume economics created durable cost advantages.

Post-merger, Cigna/Evernorth restructured its PBM operations to sell services to third-party health plans as well as Cigna’s own insurance business, positioning Evernorth as a healthcare services entity rather than a captive PBM. This rebranding is strategically significant for manufacturers: it means Evernorth now competes for PBM contracts with entities that may be Cigna’s commercial rivals, creating a complex web of client-competitor relationships.

The 2025 Evernorth formulary exclusion list runs to over 460 products. The specialty pharmacy component, Accredo, generates revenue from manufacturers through both dispensing fees and data licensing arrangements — a secondary IP monetization stream that blurs the line between service provider and market intelligence vendor.

UnitedHealth Group / OptumRx: IP and Asset Valuation

OptumRx occupies a distinct structural position among the Big Three because it has always been a captive PBM within a larger health services conglomerate, rather than a standalone PBM that was acquired by an insurer. UnitedHealth Group built Optum as a separate reporting segment encompassing pharmacy benefits, health analytics, and physician group management, meaning OptumRx’s financial results are intertwined with Optum’s broader data and technology revenue.

OptumRx’s aggressive acquisition strategy from 2015 onward — Catamaran for $12.8 billion, Helios PBM assets, and Diplomat Pharmacy in 2019 — expanded its specialty pharmacy and home infusion capabilities. The Diplomat acquisition added a large specialty dispensing footprint focused on rare disease and oncology, drug classes where per-prescription revenue can exceed $10,000 per fill and where the manufacturer’s limited distribution network (LDN) strategies intersect directly with PBM specialty pharmacy relationships.

The IP-equivalent value at OptumRx is most accurately understood through Optum Insight, the data analytics subsidiary that sits alongside OptumRx in the Optum umbrella. Optum Insight holds claims data on over 200 million individuals, which it licenses to pharmaceutical manufacturers for real-world evidence (RWE) generation, market access analytics, and post-market safety surveillance. This means that UnitedHealth Group captures value not only by processing claims and dispensing drugs, but by selling analytical derivatives of those claims back to the manufacturers whose formulary placement and rebate negotiations the same entity controls.

Investment Strategy Note — Big Three Asset Valuation

For institutional investors modeling PBM-affiliated equities, the conventional metrics — earnings per adjusted script, mail-order penetration rate, specialty pharmacy revenue growth — understate the regulatory-embedded risk now attached to these assets. The FTC’s active litigation and the Arkansas structural reform model introduce optionality-destroying risk to the integrated asset base. CVS Health’s equity has traded with elevated volatility since the FTC filed its insulin-pricing lawsuit in 2024. Any federal legislation mandating pharmacy-PBM separation would require asset divestitures that would crystallize losses against the goodwill recorded on the Caremark and Aetna acquisitions, where combined goodwill on CVS Health’s balance sheet exceeded $70 billion as of 2024. Investors should model divestiture scenarios as a tail risk, not a low-probability event.

Key Takeaways — Section 4

The core IP-equivalent asset of each Big Three PBM is its formulary position and rebate contracting system, not a conventional patent portfolio.

CVS Health’s vertical integration created four-point revenue capture on a single prescription transaction: insurance, PBM, retail pharmacy, and specialty pharmacy.

UnitedHealth Group/OptumRx monetizes claims data as a secondary IP stream, selling analytical products back to the same manufacturers whose formulary positioning it controls.

Investors should model forced divestiture as a tail risk, given the goodwill exposure embedded in CVS Health, Cigna, and UnitedHealth Group balance sheets.

The Formulary as a Competitive Weapon: Drug Coverage, Rebate Architecture, and List Price Inflation

How Rebate Mechanics Drive List Price Behavior

The pharmaceutical rebate, as practiced in the U.S. market, is a post-sale payment from a brand manufacturer to the PBM, calculated as a percentage of the drug’s wholesale acquisition cost (WAC). Because the rebate is WAC-indexed, a manufacturer seeking to maintain its net realized price (the price it keeps after paying the rebate) has a structural incentive to raise WAC while simultaneously agreeing to a higher rebate percentage. The PBM, in turn, receives a larger absolute dollar rebate on a higher-WAC drug.

This dynamic is not speculative — it is the mechanism the FTC cited in its 2024 lawsuit against the Big Three over insulin pricing. The agency alleged that the PBMs’ rebate negotiation practices created incentives for manufacturers to escalate WAC-listed insulin prices even as the net price paid to manufacturers declined. The patient, however, pays cost-sharing calculated against WAC at the point of sale, not against the net price. A patient in a high-deductible health plan (HDHP) or with coinsurance cost-sharing tied to list price effectively subsidizes the rebate that the PBM retains.

Formulary Exclusions as Negotiating Leverage

The annual formulary exclusion list is the most powerful tool in the PBM’s formulary management arsenal. When CVS Caremark, Express Scripts, or OptumRx excludes a branded drug from its standard formulary, covered members who need that drug must either pay full out-of-pocket price or seek a medical exception. For most therapeutic categories, this effectively removes the excluded product from the realistic prescribing landscape for that PBM’s covered population.

Manufacturers understand this. The implicit negotiation — often explicit in rebate contract terms — is that a manufacturer must meet the PBM’s rebate threshold or risk exclusion. A drug excluded from all three Big Three formularies simultaneously is essentially non-reimbursed for 80% of the commercially insured U.S. population. That is a market access problem no amount of sales force activity or physician detailing can solve.

The FTC’s interim staff report documented that the Big Three’s formulary exclusion practices have accelerated since 2017. The number of drugs excluded from standard formularies by at least one of the three major PBMs has grown from approximately 100 in 2014 to over 500 in 2025. The therapeutic categories most affected include immunosuppressants, GLP-1 agonists for diabetes and obesity, respiratory biologics, and multiple sclerosis agents — precisely the categories where manufacturers have the highest revenue concentration and where biosimilar or therapeutic alternative competition is either pending or already available.

Therapeutic Category Deep Dive: Humira and the Adalimumab Formulary Wars

AbbVie’s adalimumab (Humira) is the most instructive case study in PBM formulary dynamics as applied to a major branded biologic facing biosimilar competition. Humira’s U.S. patent protection, though the core compound patent expired in 2016, was extended through a thicket of device, formulation, and method-of-use patents — a classic evergreening strategy that kept biosimilar competitors off the U.S. market until January 2023, seven years after European biosimilar entry. AbbVie’s intellectual property strategy on Humira will be discussed in detail in Section 10; the formulary dimension is equally consequential.

By 2023, nine adalimumab biosimilars had received FDA approval. The Big Three PBMs faced a choice: exclude AbbVie’s Humira in favor of lower-cost biosimilars, or continue covering Humira while accepting biosimilar competition on their formularies. The formularies they announced for 2024 and 2025 were more complex than either binary. CVS Caremark excluded Humira from its standard commercial formulary in favor of biosimilars, including its own private-label biosimilar Cordavis Hyrimoz (a co-branded version of Sandoz’s Hyrimoz). Express Scripts took a different approach, maintaining Humira on formulary while excluding certain biosimilars. OptumRx negotiated its own set of preferred biosimilar arrangements.

The result is that formulary position for adalimumab is now fragmented across three major PBMs, with patient access to any specific adalimumab product depending on which PBM administers their benefit. For manufacturers, this is the new normal: formulary competition at the biosimilar level means that regulatory approval is no longer sufficient to secure commercially meaningful access.

Key Takeaways — Section 5

The WAC-indexed rebate structure creates an incentive for manufacturers to raise list prices while agreeing to higher rebate percentages, with patient out-of-pocket costs tracking list prices rather than net prices.

Formulary exclusion lists have grown from roughly 100 products in 2014 to over 500 in 2025, covering the highest-revenue branded and biologic drug categories.

The adalimumab (Humira) biosimilar formulary landscape illustrates that regulatory approval now precedes a separate and equally competitive formulary access battle.

Spread Pricing: The Hidden Revenue Mechanism That Payers Rarely See

Spread pricing is the practice by which a PBM charges a health plan or employer a higher reimbursement rate for a dispensed drug than the PBM actually pays the dispensing pharmacy, retaining the difference — the ‘spread’ — as undisclosed profit. It is distinct from rebates, which are disclosed as a line item (even if the disclosure is incomplete), and it is distinct from administrative fees, which are explicitly contracted.

In Medicaid managed care programs, where PBMs are often contracted to manage pharmacy benefits for managed care organizations (MCOs), spread pricing became the subject of multiple state audits between 2018 and 2023. An Ohio state audit of its Medicaid managed care program found that PBMs charged MCOs approximately $224 million more for generic drugs over two years than they paid the dispensing pharmacies. Similar analyses in Kentucky, Arkansas, and New York documented spread pricing at scale in both generic and brand drug categories.

The commercial employer market is harder to audit because contracts are private, disclosure requirements are minimal, and employers often lack the claims data sophistication to identify spread. A 2022 analysis by the Pharmacy Benefit Management Institute estimated that spread pricing extracted $1 billion to $3 billion annually from commercial plan sponsors in the U.S. market, though industry representatives dispute both the methodology and the magnitude.

The legislative response at the state level has included spread pricing bans in Medicaid programs in Kentucky, Ohio, West Virginia, and Arkansas, among others. Federal legislation to extend a spread pricing ban to all PBM contracts, including commercial plans, has been proposed but not enacted as of Q1 2026. The Pharmacy Benefit Manager Transparency Act, introduced in multiple congressional sessions, would require PBMs to disclose pharmacy reimbursement rates and the spread retained on each transaction.

For PBM parent company equity analysis, spread pricing regulatory risk is asymmetrically concentrated in government program revenue. If federal legislation extends spread pricing prohibitions to commercial plans, the revenue impact on CVS Caremark, Evernorth, and OptumRx could be material. Analysts should model a 10-15% reduction in PBM segment operating margins as a bear-case scenario for any federal spread pricing ban scenario that includes commercial markets.

Biosimilar Formulary Strategy: The 2024-2025 Exclusion Data and the Private-Label Gambit

Big Three 2025 Formulary Exclusions: Biosimilar-Specific Analysis

The 2025 formulary exclusion lists published by the Big Three contain a specific biosimilar-related pattern that warrants dedicated analysis. CVS Caremark excluded multiple adalimumab biosimilars not affiliated with its Cordavis private-label arrangement, effectively creating a preferred formulary tier for its own co-branded product. Express Scripts’ 2025 list excluded several adalimumab biosimilars while maintaining Humira on formulary at a negotiated net price, reflecting a different commercial calculus. OptumRx’s exclusions concentrated on biosimilar TNF inhibitors more broadly, consolidating preferred volume into a smaller number of contracted products.

The Stelara (ustekinumab) biosimilar landscape in 2025 presents a parallel dynamic. Johnson & Johnson’s Stelara lost its core U.S. patent protection in September 2023, triggering an authorized generic entry deal and multiple biosimilar entrants. The Big Three’s formulary decisions on ustekinumab biosimilars will determine which products gain meaningful market share. Early 2025 formulary exclusion data showed at least one of the three excluding reference Stelara in favor of biosimilar alternatives — the mirror image of the Humira strategy — suggesting that PBM formulary decisions on biosimilars are product-specific commercial negotiations, not systematic policies on biosimilar promotion.

The Private-Label Biosimilar as a Vertical Integration Endpoint

CVS Health’s Cordavis subsidiary, established in 2023 to develop and commercialize private-label biosimilars under co-branding arrangements with biosimilar manufacturers, represents the logical endpoint of formulary integration. Cordavis sources biosimilars from manufacturers (the initial product was a co-branded version of Sandoz’s adalimumab biosimilar Hyrimoz), relabels them under the Cordavis brand, and then preferences them on CVS Caremark formularies.

The conflict of interest is structural and explicit: CVS Caremark simultaneously owns the formulary that determines market access and the product entity that competes for preferred formulary position on that formulary. The manufacturers of competing adalimumab biosimilars — Boehringer Ingelheim, Samsung Bioepis, Pfizer, Coherus, and others — are negotiating for formulary access against an entity that already has a preferred contractual relationship with the PBM because the PBM is, in effect, its own competitor.

For biosimilar developers assessing market access strategy, the Cordavis model establishes a new competitive dynamic that extends beyond price and clinical data. Manufacturers now need to account for PBM-sponsored private-label competition when projecting biosimilar market share. IQVIA data from Q3 and Q4 2024 showed Cordavis Hyrimoz capturing approximately 12% of formulary-preferred adalimumab volume on CVS Caremark’s commercial book — meaningful share achieved without traditional pharmaceutical market access investment.

For investors in biosimilar developers, the private-label PBM model compresses the available market access runway for non-affiliated biosimilars on Big Three formularies. Companies pursuing adalimumab, ustekinumab, bevacizumab, or trastuzumab biosimilars without a preferred PBM co-branding arrangement should factor in an access discount of 20-35% on addressable commercial lives when building revenue models. Regional and alternative PBMs represent the path to formulary access for non-preferred biosimilars, but those entities collectively cover a smaller commercially insured population.

Key Takeaways — Section 7

The Big Three’s 2025 formulary exclusion strategies for adalimumab and ustekinumab biosimilars vary by product, reflecting commercial negotiations rather than uniform biosimilar promotion policy.

CVS Health’s Cordavis subsidiary creates a direct conflict: the PBM owns the formulary and a competing biosimilar product simultaneously.

Biosimilar developers without Big Three private-label co-branding arrangements should model a material formulary access discount on commercial lives in their revenue projections.

Patient Steering: How Pharmacy Networks Function as Competitive Moats

Pharmacy network design is the mechanism by which vertically integrated PBMs translate formulary control into dispensing channel control. When a PBM designates its affiliated pharmacy — whether CVS retail, Accredo specialty, or OptumRx mail-order — as the preferred or exclusive in-network option for a drug category, plan members face cost differential incentives to shift their prescriptions to that channel. The differential is typically $10-$25 per fill in copay savings for preferred pharmacy use, which is sufficient to redirect most chronic medication patients.

The competitive consequence for independent pharmacies is direct. A 2023 study published in JAMA Health Forum documented that independent pharmacy closures in markets with high PBM market penetration correlated with increased PBM affiliated pharmacy volume in those same markets. The National Community Pharmacists Association (NCPA) has tracked over 2,500 independent pharmacy closures between 2020 and 2024, attributing a significant portion to below-cost reimbursement rates from Big Three PBMs and systematic steering to affiliated channels.

The specialty pharmacy segment is where patient steering has the largest financial impact. A specialty drug fill — defined by most PBMs as a drug with a monthly cost above $600 and requiring clinical management support — generates dispensing margin four to six times higher than a retail generic fill. When CVS Caremark directs a specialty drug claim to CVS Specialty rather than an independent specialty pharmacy, the margin retained within the CVS Health corporate entity is substantially larger than the administrative fee CVS Caremark would otherwise earn for claims processing alone.

The FTC’s interim staff report on PBMs documented that the Big Three systematically reimburse their affiliated specialty pharmacies at rates above what they pay competing independent specialty pharmacies for identical drugs, documenting in some cases reimbursement differentials exceeding 20% for the same drug and dosage form. That differential is a direct transfer of value from unaffiliated pharmacies to affiliated ones, enabled by the PBM’s information asymmetry over reimbursement rates.

The 340B Intersection: Where Vertical Integration Meets Federal Drug Pricing

The 340B Drug Pricing Program, administered by the Health Resources and Services Administration (HRSA), requires pharmaceutical manufacturers to sell drugs at a ceiling price of approximately 23.1% below average manufacturer price (AMP) to covered entity hospitals and clinics serving low-income patients. The program’s intersection with PBM vertical integration creates a separate set of conflicts worth dedicated analysis.

When a 340B covered entity contracts with a vertically integrated PBM to administer its pharmacy benefit, and that PBM also owns a pharmacy that the covered entity uses as a contract pharmacy, the 340B discount captured by the covered entity is potentially shared with or offset by fees paid to the PBM’s affiliated pharmacy. Multiple manufacturers, including AstraZeneca, Eli Lilly, Sanofi, and Novo Nordisk, unilaterally restricted 340B contract pharmacy arrangements between 2020 and 2022, citing what they characterized as diversion and duplicate discounts enabled by the PBM-contract pharmacy relationship.

HRSA sued several manufacturers over these restrictions, and the litigation wound through the federal courts between 2021 and 2024 without a definitive resolution of manufacturers’ ability to limit contract pharmacy arrangements. For pharma IP and government affairs teams, the 340B conflict is a proxy for a broader question: when PBM vertical integration extends into federally subsidized purchasing channels, the conflict of interest is no longer merely commercial — it implicates federal program integrity.

Manufacturer IP Strategy Under PBM Pressure: Evergreening, Lifecycle Management, and Formulary Defense

The Evergreening Toolkit and Its Formulary Interaction

Pharmaceutical manufacturers pursue lifecycle management strategies — commonly called evergreening — to extend the effective commercial exclusivity of branded drugs beyond the expiration of the primary compound patent. The standard toolkit includes: filing secondary patents on drug delivery devices (autoinjectors, prefilled syringes), formulation patents (concentration, excipient composition), method-of-use patents (new indications, dosing regimens), and process patents (crystalline form, manufacturing method). AbbVie’s Humira patent portfolio, which the Institute for Clinical and Economic Review (ICER) and researchers at the University of Illinois documented as comprising over 160 patents, is the most cited example of this strategy executed at scale.

For brand manufacturers seeking to maintain formulary position against biosimilar entry, the IP strategy and the formulary defense strategy are interdependent. Extending the data exclusivity or patent protection period on a biologic through legitimate lifecycle management — adding an FDA-approved new indication, for example — extends the period during which the manufacturer can negotiate rebates from a position of formulary necessity rather than formulary competition. A biologic with no biosimilar competitor on formulary faces a different rebate negotiation than one with eight competing biosimilars.

The Authorized Generic and Biosimilar Entry Interplay

Manufacturers facing biosimilar entry have used authorized generic (AG) strategies — licensing the reference biologic to a biosimilar manufacturer or generic company at a pre-negotiated royalty in exchange for the AG manufacturer delaying independent biosimilar launch — in conjunction with formulary access agreements. Johnson & Johnson’s arrangement around Stelara ahead of ustekinumab biosimilar entry included an authorized generic component that gave certain formulary-preferred distributors access to the reference biologic at a substantially discounted price, complicating the formulary economics for non-authorized biosimilar entrants.

For pharma IP teams, the interaction between patent term, authorized generic strategy, and PBM formulary mechanics is now a core element of launch planning for any biologic facing loss of exclusivity (LOE). The question is not simply when a patent expires but when formulary dynamics will shift against the reference product, and whether an authorized generic or co-branding arrangement with a PBM can extend meaningful commercial life beyond the formal IP exclusivity window.

Small Molecule Evergreening and Paragraph IV Dynamics

In small molecule generics, the Paragraph IV Hatch-Waxman filing mechanism creates a well-understood 180-day exclusivity window for the first successful generic challenger. PBM formulary strategy intersects with this dynamic in two ways. First, PBMs increasingly negotiate ‘exclusivity agreements’ with first-filer generic manufacturers during the 180-day window, agreeing to preferred formulary placement for the generic in exchange for pricing below WAC that is passed to the plan as savings. This compresses the first-filer’s exclusivity profit window but ensures formulary access that might otherwise require direct manufacturer-to-PBM negotiation.

Second, the Paragraph IV filing landscape provides PBMs with forward visibility into generic entry timelines — through public Orange Book patent certification data — that enables them to pre-negotiate formulary exclusion of the branded drug before generic entry, effectively pre-empting the manufacturer’s ability to negotiate a brand protection rebate once a generic competitor arrives. DrugPatentWatch data on Paragraph IV filings is routinely used by PBM formulary analytics teams for precisely this planning purpose.

Investment Strategy Note — IP Lifecycle and Formulary Timing

For institutional investors analyzing branded pharmaceutical equities approaching patent expiration, the traditional LOE model (revenue cliff at first generic entry, 80-90% erosion over 18 months) understates the role of PBM formulary timing in accelerating that erosion. When a PBM pre-negotiates formulary exclusion of the branded drug contingent on generic launch, the erosion curve steepens in the first 60-90 days post-launch rather than the traditional 6-12 month ramp. Investors should weight PBM formulary strategy disclosure — which is rarely detailed in manufacturer IR materials — as a key variable in LOE modeling.

Key Takeaways — Section 10

Evergreening strategies — secondary patents on devices, formulations, methods of use — extend the period during which a manufacturer can negotiate formulary position from strength rather than in competition with biosimilars.

Authorized generic arrangements and PBM co-branding deals for biosimilars are now legitimate tools in biologic LOE planning, extending commercial relevance beyond formal IP exclusivity.

Paragraph IV filing data, publicly available through the FDA Orange Book, gives PBM formulary teams early intelligence on generic entry timelines that manufacturers should be actively monitoring.

Regulatory and Litigation Landscape: FTC, DOJ, State AGs, and the Arkansas Model

The FTC Investigation: 2022 Through the 2024 Lawsuit

The FTC launched a formal investigation into the six largest PBMs’ business practices in June 2022, issuing compulsory orders to CVS Caremark, Express Scripts, OptumRx, Humana Pharmacy Solutions, Prime Therapeutics, and MedImpact. The investigation covered rebate negotiations, formulary design, pharmacy reimbursement, and the treatment of competing pharmacies within network contracts.

The FTC released an interim staff report in July 2024 that found the Big Three’s rebate and formulary practices had contributed to higher drug costs for patients, particularly in insulin, and had systematically disadvantaged independent pharmacies through below-cost reimbursement and patient steering. The report stopped short of formal findings but explicitly described the integrated PBM structures as enabling ‘a new and troubling form of market power.’

In September 2024, the FTC filed a formal lawsuit against CVS Caremark, Express Scripts, and OptumRx, alleging that their rebate negotiation practices for insulin — Eli Lilly’s Humalog and Novo Nordisk’s NovoLog being the principal products cited — constituted unfair methods of competition under Section 5 of the FTC Act. The complaint alleged that by requiring manufacturers to pay escalating rebates as a condition of formulary access, the PBMs forced manufacturers to raise WAC-listed prices, resulting in higher patient cost-sharing. The lawsuit did not proceed to injunctive relief or consent order before the administration change in January 2025, and the new FTC leadership’s approach to the litigation remains an active area of uncertainty as of Q1 2026.

State-Level Action: The Arkansas Model

Arkansas enacted HB 1150 in April 2025, signed by Governor Sarah Huckabee Sanders, prohibiting pharmacy benefit managers from obtaining or holding pharmacy permits in the state. The law takes effect in 2026, meaning CVS Caremark’s affiliated CVS retail pharmacies, and any OptumRx-affiliated pharmacy operations in Arkansas, must divest or restructure their state pharmacy permits. The Arkansas model is widely described as the most aggressive structural remedy enacted by any state, going further than transparency requirements or spread pricing bans by prohibiting co-ownership at the entity level.

The NCPA and the American Pharmacy Association (APA) applauded the legislation as a template for other states. By April 2025, attorneys general from 38 states and territories had sent a joint letter to Congress urging federal legislation modeled on the Arkansas approach. The legal vulnerability of the Arkansas law is ERISA preemption: self-insured employer benefit plans governed by ERISA may argue that the state law impermissibly regulates the terms of an employee benefit plan, a federal preemption argument that has successfully challenged multiple state PBM regulations in prior litigation.

The Patients Before Monopolies Act

The Patients Before Monopolies Act was introduced in the Senate by Senators Elizabeth Warren (D-MA) and Josh Hawley (R-MO), and in the House by Representatives Diana Harshbarger (R-TN) and Jake Auchincloss (D-MA), marking one of the few genuinely bipartisan legislative proposals in pharma policy. The bill prohibits any corporation from owning or operating both a PBM and a pharmacy, requiring structural separation within a transition period following enactment.

If enacted in its current form, the Patients Before Monopolies Act would require CVS Health to divest either its Caremark PBM operations or its pharmacy assets (retail, specialty, and mail-order). UnitedHealth Group would need to separate OptumRx from Optum Specialty Pharmacy and associated dispensing entities. Cigna/Evernorth’s Accredo specialty pharmacy would need to be separated from Express Scripts. The capital market implications are significant and are addressed in Section 14.

DOJ Task Force on Vertical Integration

The Department of Justice formed a dedicated task force on vertical integration in healthcare in May 2024, explicitly including PBM vertical integration in its mandate. The task force has not yet produced public enforcement actions specific to PBMs as of Q1 2026, but its establishment signals that the DOJ views the structural questions around PBM integration as within its antitrust enforcement authority, separate from and parallel to the FTC’s consumer protection approach.

Key Takeaways — Section 11

The FTC’s 2024 insulin-pricing lawsuit against the Big Three is the most significant antitrust enforcement action against PBMs in the agency’s history, though its resolution remains uncertain under the current administration.

Arkansas HB 1150 is the first U.S. law prohibiting co-ownership of a PBM and pharmacies at the state level, effective 2026, with 38 state AGs urging Congress to enact a federal equivalent.

The Patients Before Monopolies Act, if enacted, would require structural divestiture of pharmacy assets from the Big Three, a capital markets event with no modern U.S. healthcare precedent.

The ERISA Preemption Problem: Why State Reforms Keep Running Into a Federal Wall

ERISA, the Employee Retirement Income Security Act of 1974, preempts state laws that ‘relate to’ employee benefit plans. Since the Supreme Court’s 1995 decision in New York State Conference of Blue Cross & Blue Shield Plans v. Travelers Insurance Co. and subsequent cases, the scope of ERISA preemption as applied to state insurance regulation has been actively contested. For state PBM laws, ERISA preemption creates a structural limitation: a state can regulate PBM practices for state-regulated insurance plans (Medicaid managed care, fully-insured commercial plans), but cannot directly regulate the pharmacy benefit for self-insured ERISA plans, which cover approximately 60% of the commercially insured population.

The practical consequence is that the most aggressive state PBM reforms — spread pricing bans, formulary transparency mandates, any-willing-provider requirements, and network adequacy standards — have limited reach. A PBM operating under a contract with a large self-insured employer is largely beyond the reach of state regulatory authority. Federal legislation, whether the Patients Before Monopolies Act or a broader PBM transparency statute, is the only mechanism that reaches self-insured employer plans.

The Arkansas pharmacy permit law is structurally different from contract regulation: it regulates who can hold a pharmacy permit in the state, not the terms of the benefit contract. Whether that distinction survives ERISA preemption challenge is untested as of Q1 2026. PBM parent companies have retained outside counsel on Arkansas ERISA preemption arguments, and legal observers expect a federal district court challenge before the 2026 effective date.

Alternative PBM Models: Pass-Through Pricing, GPO Disruption, and Market Challengers

The Pass-Through PBM Model

The ‘alternative PBM’ category encompasses a range of business models that share a common claim: full pass-through of manufacturer rebates to plan sponsors, transparent pharmacy reimbursement equal to actual ingredient cost plus a disclosed dispensing fee, and no spread pricing. Companies in this segment include Capital Rx, SmithRx, Rightway, and Navitus Health Solutions, among others.

The pass-through model remunerates the PBM through a flat per-member-per-month (PMPM) administrative fee rather than through rebate retention and spread. For employer plan sponsors with sophisticated procurement teams, this model offers clearer cost accountability and more direct alignment between PBM incentives and plan cost management. For manufacturers, pass-through PBMs are a potentially friendlier formulary environment — formulary decisions are based on net cost rather than gross rebate potential — though pass-through PBMs’ smaller covered populations limit the commercial scale of their formulary decisions.

Market share for alternative PBMs remains below 10% of total U.S. prescription claims as of 2025, constrained by the Big Three’s advantages in pharmacy network breadth, specialty pharmacy infrastructure, and mail-order dispensing economics. The alternative PBM growth trajectory has been real but incremental, largely driven by self-insured mid-market employers seeking transparency after auditing their incumbent PBM contracts.

Mark Cuban’s Cost Plus Drugs: Disrupting the Retail Dispensing Layer

Mark Cuban’s Cost Plus Drugs (formally Cost Plus Drugs Company, PBC) bypasses the PBM and traditional pharmacy supply chain entirely, selling generic drugs directly to consumers at cost-plus-15% margins. As of Q1 2025, Cost Plus Drugs listed over 2,500 generic medications, with prices on many drugs running 80-90% below retail chain pharmacy prices. The platform is not a PBM and does not adjudicate insurance claims; it is a cash-pay direct dispensary.

The competitive relevance of Cost Plus Drugs to PBM analysis is not as a direct PBM substitute but as a price transparency signal. When Cost Plus Drugs lists metformin at $4 per 90-day supply and a plan member’s cost-sharing through a Big Three PBM is $35 for the same drug, the pricing opacity that enables PBM spread pricing becomes visible to the plan sponsor and the patient simultaneously. This transparency pressure is an indirect regulatory force that is contributing to employer demand for pass-through PBM contracts.

Key Takeaways — Section 13

Pass-through PBMs remove rebate retention and spread pricing from the PBM revenue model, replacing them with transparent PMPM administrative fees, but hold less than 10% combined market share as of 2025.

Cost Plus Drugs functions as a price transparency disruptor rather than a PBM competitor, creating visible reference prices that accelerate employer dissatisfaction with traditional PBM contract opacity.

Alternative PBM growth is real but constrained by the Big Three’s scale advantages in specialty pharmacy, mail-order dispensing, and manufacturer rebate negotiating leverage.

Investment Strategy for Institutional Analysts

Equity Exposure: Big Three PBM Parent Companies

CVS Health, Cigna Group (parent of Evernorth/Express Scripts), and UnitedHealth Group each carry PBM-related regulatory risk that is not fully reflected in current consensus earnings models. The key variables to monitor and model are:

The FTC insulin litigation resolution: A consent decree or injunctive relief requiring changes to rebate negotiation practices would structurally reduce PBM revenue per script in brand drug categories. Model a 5-10% reduction in PBM segment operating income as a compliance cost floor.

Federal PBM legislation passage probability: The Patients Before Monopolies Act and similar structural separation proposals have bipartisan Senate co-sponsorship, which is unusual in current legislative dynamics. A 25-35% passage probability over a two-year window is a reasonable analyst assumption, given the pace of state-level action and AG coalition activity. Passage would trigger divestitures at all three Big Three parent companies; goodwill impairments would follow.

Biosimilar private-label revenue contribution: CVS Health’s Cordavis subsidiary is an undermodeled revenue contributor in most sell-side analyses. As biosimilar competition expands across TNF inhibitors, anti-VEGF biologics, and oncology supportive care, Cordavis-format co-branded private label products could generate incremental PBM segment revenue of $500 million to $1.5 billion annually by 2027, partly offsetting regulatory headwinds.

Fixed Income: PBM Parent Company Credit

The goodwill concentration risk in CVS Health’s balance sheet — over $70 billion in goodwill related to the Caremark and Aetna acquisitions — is the primary credit risk factor for institutional fixed income investors. A divestiture scenario would require write-downs that would pressure CVS Health’s leverage ratios and potentially breach credit agreement financial maintenance covenants. Credit analysts should model divestiture-triggered impairment in a structural separation scenario and assess covenant headroom at current leverage levels.

Manufacturer Strategy: IP and Market Access Alignment

For pharmaceutical and biotech companies, the PBM landscape requires treating formulary access as an intellectual property-equivalent asset that depreciates with contract renegotiation cycles. Brand protection strategies should be designed in parallel with formulary defense strategies: the patent term extension or new indication approval that extends exclusivity should also extend the period during which the manufacturer can negotiate formulary necessity rather than formulary competition.

Manufacturers with late-stage biologics should model PBM private-label biosimilar competition at LOE as a baseline scenario, not an edge case. The Cordavis model is scalable, and if the economics on adalimumab prove out, other PBMs or pharmacy chains may pursue similar structures for bevacizumab, trastuzumab, ustekinumab, and etanercept.

Independent Pharmacy and Specialty Pharmacy Operators

For private equity and strategic investors in independent pharmacy or specialty pharmacy, the regulatory environment in 2025-2026 is more favorable than at any point in the past 15 years, given the momentum behind structural PBM reform. A federal pharmacy-PBM separation mandate would redirect specialty pharmacy volume away from Accredo, CVS Specialty, and OptumRx Specialty, creating market access opportunity for non-affiliated specialty pharmacies. That opportunity is contingent on legislative outcomes that remain uncertain; investors should weight this as an upside optionality position rather than a base-case assumption.

Structural Reform Scenarios and Their Market Impact

Scenario A: Status Quo with Incremental Transparency Requirements

Congress enacts transparency legislation requiring PBMs to disclose rebate amounts to plan sponsors, report pharmacy reimbursement data to federal agencies, and ban spread pricing in Medicaid. No structural separation requirement. This scenario preserves the Big Three’s integrated business models while adding compliance cost and reducing some opacity-dependent revenue. PBM segment operating margins compress by 3-6% over three years. Manufacturer rebate negotiations continue in the current format but with greater plan sponsor ability to audit retained rebates. Market impact: mildly negative for Big Three parent companies, neutral to slightly positive for manufacturers and pass-through PBMs.

Scenario B: Federal Pharmacy-PBM Structural Separation

The Patients Before Monopolies Act or equivalent legislation passes, requiring divestiture of PBM and pharmacy assets within 36 months of enactment. CVS Health must separate Caremark from CVS retail, CVS Specialty, and Aetna’s pharmacy operations or structure them as genuinely independent entities. Cigna must separate Accredo from Evernorth. UnitedHealth must separate OptumRx Specialty from OptumRx. Market impact: highly disruptive to Big Three parent company equity. PBM segment valuations decline as integrated synergies are eliminated. Independent pharmacy and specialty pharmacy operators gain formulary negotiating position. Biosimilar developers without PBM private-label arrangements gain market access. The manufacturing sector benefits from a rebate negotiation environment less dominated by integrated structural advantage.

Scenario C: Continued Regulatory Fragmentation

Federal legislation stalls. States continue enacting PBM reforms of varying scope, with ERISA preemption limiting effectiveness for self-insured populations. FTC litigation settles without structural remedies. The Big Three continue their current integration trajectory, with Cordavis-format private label biosimilars expanding to additional therapeutic categories. Market impact: secular margin compression for non-affiliated biosimilar developers, continued independent pharmacy closures, and growing employer dissatisfaction driving incremental share to pass-through PBM alternatives. The long-run competitive dynamic favors the Big Three’s scale but concentrates systemic risk in three corporate structures.

Key Takeaways — Section 15

The most likely near-term outcome (Scenario A) is incremental transparency legislation without structural separation, moderately negative for PBM parent company margins and neutral to positive for manufacturers.

The structurally disruptive scenario (Scenario B) has real legislative momentum in 2025-2026 and warrants serious probability weighting in institutional investment models for CVS Health, Cigna, and UnitedHealth Group.

Manufacturers, biosimilar developers, and independent pharmacy operators all have material upside exposure in a structural separation scenario that institutional models currently underweight.

Conclusion

Pharmacy benefit managers have traveled a long way from the administrative claims processors that insurance companies first contracted in the 1960s. They are now the most consequential non-government actors in U.S. drug pricing, wielding formulary design, specialty pharmacy ownership, mail-order dispensing, and insurer affiliation as interconnected tools of market control. The three largest PBMs control 80% of prescription claims processing, operate private-label biosimilar subsidiaries, and retain portions of manufacturer rebates that payers and patients rarely see itemized.

The structural conflicts of interest embedded in this model have produced regulatory pressure at a scale and with a bipartisan character that has no precedent in PBM history. The Arkansas law, the FTC lawsuit, the 38-state AG coalition, and the Patients Before Monopolies Act are not isolated events. They reflect a policy consensus, still developing and still contested, that the current integrated structure is producing drug prices and access conditions that benefit the integrating entities more than the patients and employers the PBM system was originally created to serve.

For pharma and biotech IP teams, R&D executives, and institutional investors, the practical imperatives follow from this analysis. IP lifecycle management and formulary access strategy must be developed in parallel, not sequentially. Biosimilar market access models must account for PBM private-label competition at LOE. Manufacturer government affairs functions must engage the Patients Before Monopolies Act debate with a clear-eyed assessment of what structural PBM reform would mean for their own formulary relationships. Institutional equity and credit analysts must build regulatory disruption scenarios into PBM parent company models with probability weights that reflect the actual legislative momentum, not the comfortable assumption that the status quo persists.

Sources for this analysis include: FTC staff reports on PBM practices (2024), AMA PBM market concentration analysis (2024), NCPA pharmacy closure data (2024), Congressional Budget Office analyses of PBM regulation, DrugPatentWatch patent database, IQVIA market data, and primary legislative texts for the Patients Before Monopolies Act and Arkansas HB 1150.

")