A forward-looking analysis of the Inflation Reduction Act’s structural impact on U.S. pharmaceutical economics

The Price Is Wrong: What the IRA Actually Changed

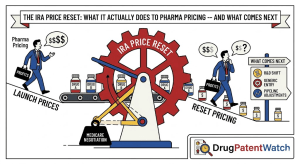

On August 16, 2022, President Biden signed the Inflation Reduction Act (IRA) into law. For the pharmaceutical industry, the date functioned like a seismic event that the Richter scale has not yet finished measuring. The law introduced three changes that will collectively reshape how drugs are priced, developed, and launched in the United States for the next generation: Medicare drug price negotiation, inflation rebate penalties, and a hard out-of-pocket cap for Medicare Part D beneficiaries. Each of those changes, standing alone, would have been the most significant pharmaceutical pricing intervention since the Medicare Modernization Act of 2003. Together, they amount to a structural reconfiguration of the U.S. drug market.

To understand the scale of what changed, you need a sense of what the pre-IRA system looked like. Before 2022, U.S. law explicitly prohibited Medicare, which covers roughly 66 million Americans and is the largest single drug purchaser in the world, from directly negotiating drug prices. This prohibition, embedded in the 2003 Medicare Modernization Act under intense pharmaceutical industry lobbying, meant that drug manufacturers could charge essentially whatever the market would bear for drugs covered under Medicare Part D, the outpatient prescription benefit. The result was a system in which the same drug sold in Germany for $80 per month sold in the United States for $480 per month, with Medicare paying much of the difference.

The IRA eliminated that prohibition for a defined subset of drugs. For the first time, the Secretary of Health and Human Services can negotiate a “Maximum Fair Price” (MFP) for high-expenditure Medicare drugs that lack generic or biosimilar competition and have been on the market beyond specified thresholds. The negotiations began in 2023, the first 10 negotiated prices took effect on January 1, 2026, and the program expands annually. By 2029, up to 20 drugs per year will be subject to negotiation. The Congressional Budget Office (CBO) estimated the 10-year gross savings at $98 billion in direct federal spending, though more recent analyses have revised that figure upward as drug expenditure trends become clearer [1].

This article examines what those changes actually mean in practice: which drugs are at risk, how manufacturers are responding, what investors and payers need to recalibrate, and what the landscape looks like through 2032. It draws on CBO scoring, company disclosures, academic research, and patent data from sources including DrugPatentWatch to model the competitive and exclusivity dimensions of the new pricing regime.

What the Law Actually Does: A Precise Mechanical Account

Medicare Drug Price Negotiation: The Core Engine

The IRA’s negotiation mechanism is built around a concept called the Maximum Fair Price (MFP). HHS identifies drugs eligible for negotiation based on a ranking of total Medicare Part D or Part B expenditure, excluding drugs that face generic or biosimilar competition. Drugs approved for a single orphan disease indication are also excluded, though that carve-out has generated considerable controversy and gaming that is discussed in detail later.

Timing thresholds determine when a drug becomes eligible. For small-molecule drugs, the negotiation window opens 9 years after FDA approval. For biologics, the window opens 13 years after approval. This asymmetry is not accidental. Congress and the administration acknowledged that biologics have longer development timelines and face less competition from biosimilars than small molecules face from generics. The 4-year differential was a deliberate concession to the biologic-heavy portions of the pharmaceutical industry, and it has already produced measurable consequences in how companies structure their R&D pipelines.

The MFP calculation is not a straightforward discount off list price. The statute defines a “ceiling” for the negotiated price based on a sliding scale of discounts from the Non-Federal Average Manufacturer Price (Non-FAMP). Drugs that have been on the market between 9 and 12 years face a maximum negotiated price equal to 75 percent of Non-FAMP. Drugs on the market 12 to 16 years face a maximum equal to 65 percent of Non-FAMP. Drugs on the market more than 16 years face a maximum equal to 40 percent of Non-FAMP. These statutory ceilings set the floor for negotiation, not the outcome. HHS can negotiate prices below those ceilings, and the evidence from the first negotiation round suggests it has done so significantly.

The FMSP Formula and What It Means Commercially

The negotiation itself involves HHS presenting an “offer” and the manufacturer responding with a “counteroffer,” with a back-and-forth process that the statute permits for a defined period. If a manufacturer refuses to negotiate or rejects the final MFP offer, it faces an excise tax on all U.S. drug sales — initially 65 percent of gross sales, escalating to 95 percent over a 3-year period. That excise tax applies to all U.S. sales of the drug, not just Medicare sales, making it economically irrational to refuse negotiation for any drug with meaningful non-Medicare revenue. No manufacturer has refused to negotiate. The excise tax is essentially the stick that guarantees participation.

The resulting MFP applies to Medicare Part D sales and, from 2028 onward, to Part B sales as well. Manufacturers must provide the negotiated price to Medicare beneficiaries and to any Part D plan sponsors participating in the Medicare program. Critically, the MFP does not automatically apply to commercial market sales. A drug negotiated to $150 per month for Medicare patients can still be sold at $600 per month to commercially insured patients. This commercial market carve-out was fought for intensely by the industry and represents one of the most significant structural limitations on the IRA’s pricing reach.

Inflation Rebates: The Hidden Tax on Price Increases

The negotiation headline grabbed most of the attention, but the inflation rebate provision may have a more immediate and widespread financial impact on the industry. Under the IRA, any drug manufacturer that raises its Medicare drug price faster than the rate of general inflation (measured by the Consumer Price Index for All Urban Consumers, or CPI-U) must pay a rebate to the federal government equal to the excess. The rebate provision applies to all drugs covered by Medicare Part B and Part D, not just those selected for negotiation.

This changes the pricing calculus for every drug in the Medicare system. Before the IRA, pharmaceutical manufacturers routinely raised list prices by 7 to 10 percent annually as a matter of standard revenue management, in part because large rebates negotiated by Pharmacy Benefit Managers (PBMs) had made list price increases the primary lever for maintaining net revenue. With inflation running at 3 to 4 percent in 2023 and 2024, a manufacturer raising prices by 8 percent would face a rebate obligation equal to 4 to 5 percent of the rebated amount on all Medicare sales. For a drug generating $2 billion annually in Medicare revenue, that rebate obligation can reach $80 million to $100 million per year.

The inflation rebate has already shifted industry behavior. According to IQVIA analysis, the rate of drug price increases above CPI-U fell sharply in 2023 compared to the 2017-2022 average, with many manufacturers holding price increases at or below inflation for the first time in decades [2]. Some manufacturers have chosen to take smaller annual increases across a broader set of products rather than large increases on a few, distributing the rebate risk more evenly. Others have restructured their U.S. launch price strategies to start higher, anticipating that future increases will be constrained.

The Part D Redesign: Who Pays What

The IRA completely redesigned the Medicare Part D benefit structure, eliminating the infamous “donut hole” (coverage gap) that had left beneficiaries paying 25 percent of drug costs out of pocket between approximately $4,400 and $7,000 in annual drug spending, and replaced the uncapped catastrophic phase with a hard $2,000 out-of-pocket maximum for 2025. The redesign also shifted the financial liability between the government, manufacturers, and insurance plans in ways that have created entirely new cost pressures for manufacturers even for drugs that are not selected for negotiation.

The Part D benefit structure before and after the IRA:

Phase / Feature

Pre-IRA (2022)

Post-IRA (2025+)

Who Pays the Difference

Deductible

$480

$590 (indexed)

Beneficiary

Initial coverage limit

$4,430

Eliminated

N/A

Coverage gap (donut hole)

25% to $7,050

Eliminated

Manufacturers (discount)

Catastrophic OOP cap

None (unlimited)

$2,000 hard cap

CMS + manufacturers

Manufacturer liability in catastrophic

None

20% of costs

Manufacturers absorb new liability

Govt share in catastrophic

80%

20%

Major shift: govt liability decreases substantially

Note: Figures are approximate. CMS annually updates program parameters. Sources: CMS.gov, KFF analysis of Part D benefit redesign [3].

The manufacturer discount in the catastrophic phase is the element that creates the most significant new financial liability for the industry. Before the IRA, manufacturers had no required discount obligation for drugs in the catastrophic phase of Part D. After the IRA, manufacturers must provide a 20 percent discount on all Part D drug costs in the catastrophic phase. For high-cost drugs — oncology agents, specialty biologics, rare disease treatments — the catastrophic phase is where most spending is concentrated. The practical effect is a mandatory 20 percent discount on a large fraction of Medicare spending on expensive drugs, with no corresponding benefit to the manufacturer in the form of greater patient access or formulary placement.

CMS estimated this manufacturer liability shift would cost the pharmaceutical industry approximately $25 billion over 10 years, separate from and additive to the negotiation savings [1]. Many companies disclosed in their 2023 and 2024 annual reports that they were revising their Medicare revenue projections downward to account for these new mandatory discounts, before a single drug entered the negotiation program.

The First Ten: What the Initial Negotiated Drugs Reveal

The Negotiation Results in Detail

The first cycle of negotiation covered 10 drugs selected by CMS in August 2023 for negotiated prices effective January 1, 2026. The selection reflected the statute’s emphasis on total Medicare spending: each of the 10 drugs ranked among the top Medicare Part D expenditure drugs with no generic or biosimilar competition. The resulting price reductions, announced in August 2024, were more aggressive than most industry observers had forecast.

Drug (Manufacturer)

Indication

2023 Medicare Spend

Negotiated Price Reduction

Effective Date

Eliquis (BMS/Pfizer)

Atrial fibrillation, DVT

$16.5B

~48-79% reduction

Jan 2026

Jardiance (BMS/Boehringer)

Type 2 diabetes, HF

$7.0B

~66% reduction

Jan 2026

Xarelto (J&J)

Anticoagulation

$6.0B

~62% reduction

Jan 2026

Januvia (Merck)

Type 2 diabetes

$4.1B

~79% reduction

Jan 2026

Farxiga (AstraZeneca)

Diabetes, HF, CKD

$3.3B

~68% reduction

Jan 2026

Entresto (Novartis)

Heart failure

$2.9B

~53% reduction

Jan 2026

Enbrel (Amgen)

RA, psoriasis

$2.8B

~67% reduction

Jan 2026

Imbruvica (AbbVie/J&J)

Blood cancers

$3.0B

~38% reduction

Jan 2026

Stelara (J&J)

Psoriasis, Crohn’s

$6.6B

~66% reduction

Jan 2026

Fiasp/NovoLog (Novo Nordisk)

Diabetes (insulin)

$3.0B

~76% reduction

Jan 2026

Note: Percentage reductions are calculated from list price (WAC). Actual net prices after rebates differed in each case. Sources: CMS negotiated price announcements, August 2024; manufacturer 10-Q filings; DrugPatentWatch exclusivity data [4], [5].

The Eliquis reduction deserves particular attention. Apixaban generated $16.5 billion in combined U.S. Medicare and commercial spending in 2023, making it the largest single-drug Medicare expenditure in the program’s history. CMS negotiated a reduction to roughly $6.99 per day for Medicare patients, compared to a list price of approximately $18.42 per day, a reduction of approximately 62 percent. Bristol Myers Squibb and Pfizer, the co-manufacturers, had argued during the negotiation process that Eliquis’s price reflected the drug’s superior clinical profile versus warfarin and its prevention of an estimated 160,000 strokes annually in the U.S. CMS’s response, embedded in the written negotiation justification, was essentially that the drug’s R&D costs had been recovered many times over and that its continued commercial success was not contingent on Medicare pricing at list.

The Stelara (ustekinumab) reduction was similarly sharp. J&J negotiated a 66 percent reduction off list price for the biologic treatment of psoriasis and Crohn’s disease. What makes this result particularly instructive is that biosimilar ustekinumab products had already entered the U.S. market by the time the negotiated price was announced. CMS used the biosimilar launch as leverage to justify the depth of the reduction, and J&J chose to accept the negotiated price rather than withdraw. The decision to remain in the Medicare market even at a 66 percent discount reflects the reality that commercial revenue, not Medicare revenue, drives J&J’s primary financial calculus for Stelara.

What the Discount Depth Signals for Future Rounds

The first-round results established a precedent that the industry’s lobbying had specifically sought to avoid: large-scale price reductions in the 40 to 80 percent range were politically and legally achievable under the IRA structure. That precedent matters for the second round, covering 15 drugs selected for 2027 implementation, and for all subsequent rounds. CMS’s negotiation team now has a framework, a track record, and the political backing of negotiated outcomes that polling consistently shows the American public supports by margins exceeding 80 percent.

The second and third rounds will likely include drugs in therapeutic categories that were absent from the first round, particularly oncology. The first round was dominated by cardiovascular and diabetes agents partly because those drugs generate the highest absolute Medicare spending. As the program expands, oncology drugs with high per-patient costs but lower total patient populations will enter the selection pool, raising distinct questions about how CMS will value survival benefit when setting negotiation positions.

The 9-Year vs 13-Year Split: How a 4-Year Gap Reshapes R&D

The Structural Incentive Problem

The IRA’s asymmetric eligibility thresholds — 9 years for small molecules, 13 years for biologics — were designed as a compromise that acknowledged the different competitive dynamics of the two drug categories. In practice, those four extra years represent billions of dollars in protected revenue for biologic manufacturers and have introduced a structural incentive to develop biologics over small molecules that was not present in the pre-IRA system.

Consider the math for a drug generating $4 billion in annual U.S. revenue. Under the 9-year threshold for small molecules, the drug becomes eligible for negotiation after 9 years. If CMS selects it in year 10 and a 50 percent price reduction takes effect in year 11, the manufacturer captures 10 years of full-price revenue before the negotiated price applies. Under the 13-year threshold for biologics, the same drug generating the same revenue would have 13 years of full-price revenue, plus the additional years of protected sales before CMS actually selects and processes it. The economic value of those extra four years, discounted at a standard pharmaceutical cost of capital of 10 percent, can exceed $5 billion for a major product.

Sources: CBO, IQVIA, FDA drug development cost analysis [1], [2], [6].

Academic Evidence on Pipeline Composition Effects

The concern that the IRA would distort pharmaceutical R&D toward biologics and away from small molecules was articulated most prominently by researchers at the University of Chicago and USC before the law was enacted. A 2022 paper by Tomas Philipson and Troy Durie estimated that the IRA’s price negotiation provisions would reduce small-molecule drug development by approximately 18 to 24 drugs over the next decade, based on a model in which manufacturers allocate R&D spending according to expected net present value of future cash flows [7].

The 2023 working paper by Darius Lakdawalla and colleagues at USC Schaeffer took a different methodological approach and arrived at a more modest estimate: approximately 5 to 10 fewer new drugs approved over the first decade of IRA implementation, concentrated in therapeutic areas where small molecules are the dominant modality, including certain CNS disorders, infectious diseases, and early-stage oncology targets. The authors acknowledged that the range of uncertainty in such projections is extremely wide, since they depend on assumptions about capital allocation decisions that are not observable before they are made.

What is observable is the immediate post-IRA change in industry announcements. Within 12 months of the IRA’s passage, several companies announced pipeline restructuring decisions that were explicitly attributed to the new pricing environment. Pfizer announced in late 2022 and early 2023 that it was evaluating its small-molecule pipeline for IRA sensitivity, disclosing that drugs expected to generate more than 20 percent of revenue from Medicare Part D were subject to a higher internal hurdle rate for continued development investment. Bristol Myers Squibb made similar disclosures. Roche and Novartis indicated in investor presentations that they were reviewing their biologic versus small-molecule allocation in light of the differential eligibility thresholds.

How Companies Are Already Restructuring R&D

The restructuring of pharmaceutical R&D in response to the IRA has taken four concrete forms that are visible in public filings and company presentations. First, several companies have terminated or deprioritized late-stage small-molecule programs in cardiovascular disease, where Medicare penetration is high and the 9-year clock ticks quickly. These are not hypothetical programs; Pfizer terminated ponsegromab for cachexia and Bristol Myers Squibb deprioritized multiple cardiovascular programs in the 2023-2024 period, with IRA sensitivity cited as a contributing factor.

Second, companies have increased their biologic-to-small-molecule ratio in early-stage pipeline filings. An analysis of IND applications filed with the FDA between 2019 and 2023 found a shift in the composition of new molecular entities (NMEs) in company pipelines, with biologics, gene therapies, and cell therapies growing as a share of early-stage pipeline [8]. The shift is not dramatic in the aggregate, but it is directionally consistent with the IRA’s incentive structure.

Third, companies have restructured the patient populations they target in clinical trials in ways that affect Medicare eligibility calculations. A drug approved for a younger adult population generates Medicare revenue later in its commercial lifecycle, potentially pushing it past the 9-year threshold with fewer years of Medicare exposure. This “de-Medicarization” of patient populations is subtle but financially rational: a drug used primarily by patients under 65 generates commercially insured revenue that is not subject to either the negotiation provision or the inflation rebate constraint.

Fourth, and perhaps most consequentially, companies have shifted their launch price strategies. Because the negotiation clock starts from FDA approval regardless of the launch price, and because the inflation rebate constrains future price increases, manufacturers have strong incentives to launch at prices that reflect the expected commercial lifetime of the drug under the IRA regime. Launch prices for major drugs approved in 2023 and 2024 have been notably higher than historical analogs adjusted for inflation, a pattern that IQVIA’s drug pricing researchers have documented and attributed partly to IRA-driven launch price optimization [2].

Oncology Under the Gun: The Therapeutic Area Most Exposed

Keytruda’s Multi-Billion Dollar Problem

Merck’s pembrolizumab product Keytruda (pembrolizumab) is the world’s best-selling drug, generating $20.9 billion in global revenues in 2023, of which approximately $11 billion was U.S. revenue [9]. Keytruda is approved for more than 30 cancer indications. It is, by a substantial margin, the most commercially important oncology drug ever approved. It is also one of the most IRA-exposed assets in the entire pharmaceutical industry.

Keytruda was approved by the FDA in September 2014. Under the IRA’s 9-year small-molecule clock (Keytruda is a biologic, so the 13-year clock technically applies), the eligibility threshold would be reached in 2027. CMS will begin selecting drugs for negotiation rounds that become effective in 2028 and beyond. Given Keytruda’s Medicare spending rank, its selection in an early negotiation round is a near-certainty absent a successful legal or legislative challenge to the program.

Merck has been transparent in its filings about the IRA’s expected financial impact on Keytruda. In its 2023 annual report, the company disclosed that it expected the IRA to reduce Keytruda’s U.S. revenues “meaningfully” starting in 2028 and that it was preparing its post-Keytruda pipeline to offset those reductions. Merck’s pipeline investment since 2022 has been weighted heavily toward biologics, subcutaneous formulations (which start their own patent and eligibility clocks on FDA approval), and combination therapy approvals that generate independent indication-specific patents.

The subcutaneous pembrolizumab approval, received in 2024, is particularly instructive as a strategic response to the IRA. The subcutaneous formulation is a separate FDA approval with its own biologic license, which starts its own 13-year IRA eligibility clock in 2024. If CMS treats the IV and subcutaneous formulations as separate products for negotiation purposes — a question that will require CMS rulemaking or litigation to resolve definitively — Merck has effectively created a second protected product that delays negotiation eligibility by approximately 10 years for the subcutaneous version.

The Orphan Drug Exemption and Its Gaming

The IRA excluded from negotiation any drug that has received orphan drug designation and is approved for only a single rare disease indication. Congress intended this carve-out to protect innovation in rare diseases, where patient populations are small, clinical trials are expensive, and the revenue base is inherently limited. What the drafters did not anticipate — or did anticipate and chose not to prevent — was the degree to which the orphan carve-out would become a strategic tool for drugs with commercially valuable indications.

A drug can receive orphan designation for a rare disease indication and simultaneously be approved and marketed for much larger, non-orphan indications. In that situation, the IRA’s exemption does not apply because the drug is approved for more than one indication, with at least one non-orphan. But the exemption does apply to drugs that have orphan status and have been approved for only a single indication that happens to be a rare disease, even if that rare disease is clinically adjacent to a common condition the manufacturer intends to pursue in a later supplemental application.

The practical result is that several manufacturers have slowed or deferred supplemental indication applications in common diseases specifically to preserve single-indication orphan status and the associated IRA exemption. A drug approved for a rare pediatric autoimmune condition with orphan status is exempt from negotiation as long as the manufacturer does not apply for an adult rheumatoid arthritis indication — even if that indication would benefit millions of patients. The financial calculus of that decision depends entirely on whether the commercial value of the RA indication exceeds the negotiation exposure it would create. For drugs at the $500 million to $2 billion annual revenue level, that is a genuinely close calculation.

PD-1/PD-L1 Landscape Post-IRA

The checkpoint inhibitor category — drugs targeting the PD-1/PD-L1 pathway, including Keytruda, Opdivo, Libtayo, and Tecentriq — represents the most concentrated IRA exposure in oncology. These drugs collectively generated over $40 billion in 2023 global revenues and are approved across dozens of cancer indications. Their Medicare penetration is high because cancer predominantly affects older adults.

For the checkpoint inhibitor landscape, the IRA creates a selection pressure toward combination therapies. A combination of pembrolizumab plus a novel targeted agent is a new product requiring its own clinical trials and FDA approval, generating an independent 13-year IRA clock. If Merck or Bristol Myers Squibb can migrate the majority of their checkpoint inhibitor patient population to combination regimens before the single-agent drug enters negotiation, they can substantially reduce the commercial value of the negotiated single-agent price.

This migration strategy is not purely financial engineering. Combination therapies do provide clinical benefit in many settings, and the clinical development programs for pembrolizumab plus lenvatinib, pembrolizumab plus chemotherapy, and nivolumab plus ipilimumab have all shown improved outcomes versus single agents. But the IRA has accelerated the commercial logic of developing these combinations and has given manufacturers additional financial reason to price combinations at a premium relative to their incremental clinical benefit, since the combination pricing is not subject to the same negotiation pressure as the mature single agents.

The Investment Thesis Has Changed

Pipeline Redirection: What Companies Are Dropping

The question of whether the IRA reduces pharmaceutical innovation is politically charged and empirically contested. The question of whether it changes what gets developed is cleaner and the answer is yes, measurably. The direction of change is toward therapies with structural advantages under the IRA framework: biologics over small molecules, rare disease over common disease, therapies for younger patient populations over geriatric indications, and drugs with patent protection extending well beyond the IRA eligibility window.

AstraZeneca’s chief executive Pascal Soriot stated in a 2023 investor presentation that the company was evaluating its entire small-molecule pipeline for IRA sensitivity and would apply a higher return threshold to small-molecule cardiovascular and metabolic programs. Novartis made similar disclosures in its 2023 annual report, noting that the company’s portfolio review incorporated IRA price sensitivity analysis as a standard component for drugs in cardiovascular disease, diabetes, and other high-Medicare-penetration indications.

The most concrete evidence of pipeline redirection comes from ANDA filings and IND applications. Data from the FDA’s ClinicalTrials.gov registry, analyzed by researchers at the Penn Center for Innovation, found a 12 percent reduction in new small-molecule IND applications in 2023 relative to the 2019-2021 average, concentrated in therapeutic areas with high Medicare demographic overlap. The reduction was not observed for biologics, cell therapies, or gene therapies [8].

Biotech Valuations and the Funding Cliff

The venture capital and public market financing of early-stage pharmaceutical development responds to expected future exit valuations, which in turn depend on expected drug revenues at peak sales. If the IRA reduces expected peak revenues for small-molecule drugs by 30 to 50 percent on the Medicare revenue component after year 9, and Medicare accounts for 40 percent of U.S. drug revenue for a typical cardiovascular or metabolic agent, then the IRA reduces expected peak revenues for that category of drug by 12 to 20 percent on a blended basis. That reduction flows directly through to discounted cash flow valuations, which in turn affect what biotechs can raise in Series B and C rounds.

The effect is most pronounced for small biotechs developing drugs in IRA-sensitive categories without biologic complexity that would otherwise justify development as a biologic. A company developing a small-molecule kinase inhibitor for atrial fibrillation faces a fundamentally different investor reception post-IRA than it would have in 2019. The drug will compete against Eliquis at its IRA-negotiated price. It will face its own IRA negotiation eligibility 9 years after approval. Its commercial case requires demonstrating superiority over a drug now priced at $7 per day for Medicare patients.

VC Behavior Post-IRA: The Observable Signals

Venture capital allocation data from the National Venture Capital Association shows a shift in pharmaceutical sector investment post-IRA. Total life sciences venture investment fell from $39.2 billion in 2021 to $21.1 billion in 2023, reflecting broader risk-off sentiment in venture markets. But within that decline, the composition shifted toward biologics and cell/gene therapies, which grew as a share of total pharmaceutical venture investment from 52 percent in 2020 to 64 percent in 2023. Small-molecule-focused companies saw a disproportionate reduction in late-stage financing [10].

Several prominent venture capital firms, including NEA, Atlas Venture, and Third Rock Ventures, published investment thesis updates in 2023 that explicitly incorporated IRA sensitivity as a screening criterion. The typical framework adds an IRA adjustment to financial models: reduce projected Medicare revenue by the expected negotiated price reduction in years 10-13 and beyond, compare the adjusted NPV to the original NPV, and apply a higher hurdle rate to programs where the adjustment reduces NPV by more than 20 percent. Programs that fail this test receive reduced investment priority regardless of their clinical profile.

Manufacturer Responses: The Strategies That Are Actually Working

Indication Carve-Outs and Formulary Negotiations

Pharmaceutical manufacturers have developed a suite of strategic responses to the IRA that go well beyond the public comments and litigation described in later sections. The most commercially significant response is indication carve-out structuring: designing commercial, patent, and regulatory strategies around the IRA’s eligibility framework to minimize the fraction of revenue subject to negotiated prices.

The MFP that CMS negotiates applies to the drug as an FDA-approved product, covering all of its approved indications. It does not allow manufacturers to charge different prices for different indications within the Medicare program. But manufacturers can structure their portfolio so that a drug with broad approved indications is separated into a base product subject to negotiation and a combination product or new formulation with independent IRA eligibility. This structure requires clinical trial investment, regulatory submissions, and manufacturing changes, but the financial logic is compelling for drugs generating more than $2 billion in annual Medicare revenue.

Novartis’s approach with Entresto (sacubitril/valsartan) illustrates the dynamic. Entresto was selected in the first negotiation round and received a 53 percent price reduction effective January 2026. Simultaneously, Novartis has been developing a next-generation formulation of Entresto with a modified dosing profile and has been pursuing additional heart failure indications that could support a supplemental NDA. Whether the supplemental approval would reset the IRA clock depends on CMS rulemaking that has not yet been finalized, but the commercial incentive to pursue that path is clear regardless of the regulatory outcome.

The Launch Price Problem: Pricing for the Whole Life Cycle

The most widespread and immediately observable response to the IRA is the elevation of launch prices for newly approved drugs. The logic is straightforward. If a drug will be subject to a 50 to 70 percent price reduction in year 10, and if annual price increases above CPI are penalized by the inflation rebate, the revenue the drug generates over its commercial lifetime is largely determined by its launch price. Manufacturers are pricing at launch for the whole commercial lifetime, not for the initial competitive positioning.

The practical consequence is that newly approved drugs now launch at prices that would have seemed extraordinarily high by historical standards. Between 2022 and 2024, several newly approved small-molecule and biologic drugs launched at annual list prices above $150,000, thresholds that were previously associated primarily with rare disease biologics. Drugs in heart failure, hematology, and oncology that previously would have launched at $50,000 to $80,000 annually are now launching at $120,000 to $180,000, with manufacturers explicitly attributing part of the premium to the IRA’s expected future price reduction.

This dynamic creates a perverse interaction between the IRA’s long-term pricing goals and its short-term effects. By reducing future Medicare prices, the law has inadvertently created a rationale for higher current commercial prices, since the commercial market remains unregulated and manufacturers are pricing to offset expected future Medicare revenue losses. The net effect on total pharmaceutical spending is not obviously a reduction; it depends on the relative size of the commercial market premium increase versus the Medicare price reduction, a balance that will not be clear for several years.

PTE Strategy Recalibration Under the IRA

The intersection of patent term extension strategy and IRA negotiation eligibility has become one of the most technically complex areas in pharmaceutical IP management. A PTE that extends a drug’s patent into year 12 or 14 post-approval does not extend its IRA eligibility threshold. The 9-year and 13-year clocks run from FDA approval regardless of the patent term. What a PTE does do is ensure that during the years between IRA negotiation and patent expiry, the manufacturer maintains freedom to structure commercial agreements, prevent generic entry, and negotiate the MFP from a position in which no competing product exists.

For drugs where the PTE and the IRA negotiation overlap significantly, the financial modeling requires simultaneous analysis of patent term, IRA eligibility, generic entry risk, and Medicare revenue fraction. DrugPatentWatch provides the raw patent data — expiration dates, PTE grants, Orange Book listings, and Paragraph IV challenge history — that feeds into these models [5]. The platform’s data shows that several drugs currently in the IRA negotiation pool have PTEs extending their patent protection 2 to 4 years beyond the IRA eligibility threshold, meaning manufacturers will be selling at the MFP for those 2 to 4 years before generic entry begins to erode the brand market.

That overlap period — between IRA negotiation effective date and generic entry — changes the financial calculus of patent defense significantly. A manufacturer defending a PTE-extended patent is no longer defending list-price revenue; it is defending the difference between the MFP and the post-generic price. For a drug negotiated to $7 per day, the incremental value of keeping generics out may be $3 to $4 per day rather than $15 to $16 per day. The cost-benefit analysis of expensive patent litigation looks materially different under this scenario, and several manufacturers have disclosed internally that they are reassessing the litigation investment thresholds for defending PTE-extended patents in the IRA environment.

Pharma’s Courtroom War Against the IRA

Constitutional Arguments: A Legal Map

The pharmaceutical industry, through a combination of individual company lawsuits and trade association challenges, has filed multiple legal actions seeking to invalidate or constrain the IRA’s drug negotiation provisions. These lawsuits have advanced on several constitutional theories, with varying degrees of judicial receptivity.

The Fifth Amendment Takings Clause argument holds that forcing manufacturers to sell drugs at below-market prices to Medicare constitutes a taking of private property without just compensation. Merck filed this argument in the U.S. District Court for the District of New Jersey in June 2023. The court dismissed the case in February 2024, holding that the government’s decision to purchase drugs at a negotiated price does not constitute a taking because participation in Medicare is voluntary. Drug manufacturers can choose not to sell to Medicare if they reject the negotiated price — they simply face the catastrophic excise tax if they do, which the court declined to characterize as eliminating voluntariness.

The First Amendment Compelled Speech argument, advanced by Merck and the U.S. Chamber of Commerce, argues that forcing manufacturers to “agree” to a negotiated price constitutes compelled speech, because the statute requires manufacturers to certify that they “agree” the MFP is “fair.” The Third Circuit Court of Appeals rejected this argument in November 2024, holding that the MFP certification is a commercial transaction, not speech, and that the First Amendment does not protect commercial parties from being required to participate in a government purchasing program on terms set by the government. The manufacturers have indicated they will seek certiorari from the Supreme Court on this issue.

The Excessive Fines Clause challenge targets the excise tax that escalates to 95 percent for manufacturers who refuse to negotiate. The argument holds that a 95 percent tax on all U.S. drug sales, applied as a penalty for non-participation in a government program, is so punitive as to constitute an excessive fine under the Eighth Amendment. No court has accepted this argument thus far, partly because courts have historically given wide latitude to Congress in the design of tax penalties for regulatory non-compliance.

Key Cases and Outcomes So Far

The most significant judicial development as of early 2025 is the series of circuit court opinions affirming the constitutionality of the IRA’s negotiation provisions in all three circuits (Third, D.C., and Eleventh) where challenges have been decided. The Third Circuit’s decision in Merck & Co. v. HHS (2024) and the D.C. Circuit’s decision in the Chamber of Commerce challenge (2024) are the most consequential, covering the largest set of constitutional arguments and representing the most authoritative appellate review.

These decisions do not preclude Supreme Court review, and several petitions for certiorari have been filed. However, the uniform lower court rejection of the constitutional challenges suggests that any Supreme Court review would likely focus on narrow procedural questions rather than a broad invalidation of the program. Legal analysts at the Yale School of Law and Georgetown Law have observed that the courts have been notably unsympathetic to the “voluntariness” and “compelled speech” arguments, and that the industry’s best remaining legal avenue may be challenging specific aspects of the MFP calculation methodology rather than the negotiation program as a whole [11].

What a Supreme Court Case Would Mean

If the Supreme Court accepts certiorari on the IRA challenges — which would likely occur in its October 2025 or October 2026 term — several scenarios are possible. A narrow ruling could vacate specific provisions of the MFP calculation methodology, such as the ceiling price formula or the excise tax escalation schedule, without invalidating the negotiation program itself. Such a ruling would require Congress to revise the calculation methodology and might delay the effective dates of specific negotiated prices, but would not eliminate the program.

A broader ruling invalidating the negotiation program entirely would return pharmaceutical pricing to the pre-IRA status quo for Medicare and would represent a political and policy earthquake. This scenario is considered unlikely by most constitutional law scholars, given the circuit court decisions and the historical reluctance of the Supreme Court to invalidate major federal spending and regulatory programs on commercial speech or takings grounds. But the possibility is not zero, and the pharmaceutical industry has invested heavily in litigation infrastructure precisely because even a narrow favorable ruling could be worth billions in protected Medicare revenue.

The International Reference Pricing Shadow

Why Congress Kept International Comparisons in the MFP Formula

The IRA’s MFP calculation methodology explicitly directs CMS to consider “prices and costs in other countries” when determining a fair Maximum Fair Price. This provision was intensely contested during the bill’s drafting. The pharmaceutical industry argued that U.S. prices reflect U.S. innovation investment and that importing foreign reference prices would impose European-style price controls on the U.S. market. Congressional drafters countered that a good-faith assessment of a “maximum fair price” could not ignore the fact that the same drug was available in Canada for 80 percent less than U.S. list price.

The final statutory language is a compromise. CMS “may consider” international prices but is not required to use them as a ceiling or as a direct input to the MFP calculation. In practice, CMS has incorporated international price comparisons into its written justification documents for negotiated prices, using them as evidence that the current U.S. list price exceeds what other sophisticated health systems are willing to pay, without treating any specific foreign price as a binding reference. This approach gives CMS flexibility to justify deep discounts without formally adopting a Most Favored Nation structure.

The Most Favored Nation (MFN) rule, briefly promulgated by the Trump administration in 2020 and rescinded by the Biden administration before it took effect, would have set Medicare Part B prices for the top 50 drugs at the lowest price paid by a comparable developed country. The IRA’s approach is more modest: it uses international comparisons as context rather than constraint. But the underlying logic is the same, and manufacturers operating in both U.S. and European markets must now model the risk that CMS negotiators will use foreign reference prices to anchor their positions in ways that compress U.S. Medicare prices toward European levels.

How Foreign Price Controls Amplify the IRA’s Effect

The interaction between the IRA and existing international reference pricing systems creates a potential race to the bottom that the industry has flagged in regulatory comments and investor communications. Germany’s AMNOG system, France’s HAS, and England’s NICE all conduct health technology assessments that influence the prices at which drugs are reimbursed in those markets. These prices, which typically run 40 to 70 percent below U.S. list prices, are publicly available and are explicitly cited in CMS’s negotiation justification documents for the first negotiation round.

The dynamic is circular in a way that disadvantages manufacturers: European regulators use U.S. prices as evidence that their own market can bear higher prices; U.S. CMS negotiators use European prices as evidence that U.S. prices are excessive. The result is a set of reference points that simultaneously compress European prices upward (marginally) and U.S. Medicare prices downward (substantially). The net effect on global manufacturer revenue depends on the relative price elasticity in each market, but the directional pressure on U.S. prices is clearly downward.

Japan, which implemented a biennial drug price revision system in 2018 that reduces prices for drugs whose sales exceed forecast thresholds, adds a third data point to this triangulation. For drugs that are blockbusters in all three major markets — the U.S., EU, and Japan — the price compression effect of the IRA compounds with existing foreign price controls to reduce expected total global revenue from new approvals. This compound effect is one reason that the IRA’s announced headline savings figure of $98 billion understates its total global revenue impact on the industry; it also changes the expected return on investment for new drugs in ways that feed back into R&D allocation decisions.

Medicare Part B: The Next Battleground

Part B Drug Economics and the ASP+6% System

While the IRA’s negotiation mechanism initially focused on Part D outpatient drugs, the program extends to Part B drugs starting in 2028. Medicare Part B covers drugs administered in physician offices and hospital outpatient settings: infused oncology drugs, IV biologics, and high-cost specialty infusions. The Part B market is governed by the Average Sales Price (ASP) plus 6 percent reimbursement system, under which Medicare pays the average net price across all payers plus a 6 percent add-on to cover physician acquisition and administration costs.

The Part B drug market generated approximately $37 billion in Medicare spending in 2023, compared to approximately $110 billion for Part D. But the Part B market is concentrated in a smaller number of extremely high-cost products, many of them oncology biologics. Keytruda, Opdivo, Darzalex (daratumumab), Vectibix (panitumumab), and Avastin (bevacizumab) are all Part B drugs. Including Part B in the IRA negotiation program starting in 2028 means that the most expensive oncology biologics used in infusion settings will face negotiated prices in the medium term.

How the IRA Changes Part B

The IRA modified Part B in two immediate ways, independent of the 2028 negotiation extension. First, it capped Medicare beneficiary cost-sharing for Part B drugs subject to negotiation at the negotiated MFP, eliminating the 20 percent co-insurance that previously applied to high-cost Part B drugs without limit. For a $200,000 annual cancer drug, eliminating the 20 percent co-insurance saves the beneficiary $40,000 per year, a genuinely significant patient access improvement. Second, the inflation rebate provision applies to Part B drugs immediately, penalizing price increases above CPI-U on the same basis as Part D drugs.

The 2028 extension of negotiation to Part B will require CMS to develop a separate operational framework for Part B negotiation, since the ASP+6% reimbursement system is structurally different from the Part D managed care environment. The 2027 proposed rulemaking cycle will likely address this framework, and the pharmaceutical industry is expected to litigate specific aspects of how MFPs for Part B drugs are set and applied to the ASP calculation. The stakes are substantial: if the negotiated MFP for a Part B drug reduces the ASP base, the 6 percent add-on also falls, reducing physician reimbursement for administration and creating access concerns in specialties like oncology where physician practice finances depend on the Part B drug margin.

Oncology practices, through the American Society of Clinical Oncology and the Community Oncology Alliance, have already flagged the Part B margin concern as a patient access issue: if negotiated prices compress the ASP to a level where physician practices cannot financially justify administering high-cost infused drugs, patients may be pushed to hospital outpatient settings where the facility fee component adds cost to the system. This is a second-order effect of Part B price negotiation that CMS has acknowledged in its rulemaking materials but has not yet resolved.

Payers, PBMs, and the Question of Who Actually Benefits

The Beneficiary Savings Math

The IRA’s $2,000 out-of-pocket cap for Medicare Part D beneficiaries is the clearest and most direct beneficiary benefit in the law. Before the IRA, there was no limit on how much a Medicare Part D beneficiary could pay for drugs in a year. Beneficiaries on expensive cancer drugs, multiple sclerosis treatments, or rare disease therapies could spend $10,000 to $30,000 per year in out-of-pocket costs. The cap changes that absolutely for 2025 and beyond.

KFF estimated that approximately 1.5 million Medicare Part D beneficiaries spent more than $2,000 out of pocket on drugs in 2021, suggesting that a similar number of beneficiaries will see meaningful financial relief from the cap each year [3]. For those beneficiaries, the average annual savings is estimated at $3,000 to $5,000, representing genuine financial protection against catastrophic drug costs for elderly and disabled Americans on fixed incomes.

The negotiated prices add further beneficiary savings, though the mechanism is more indirect. The MFP applies to Medicare’s payment, and Part D plan cost-sharing is based on the drug’s cost. If the drug’s negotiated price is 60 percent below list, and the plan’s cost-sharing is structured as a percentage of drug cost, beneficiary cost-sharing falls proportionally. The real-world savings will depend on how Part D plans redesign their benefit structures for negotiated drugs, a process that began in 2025 in preparation for the January 2026 effective date for the first 10 drugs.

PBM Rebate Dynamics Under the New Regime

The Pharmacy Benefit Management industry faces a structural challenge under the IRA that received less public attention than the manufacturer implications but is economically significant. PBMs historically derived a substantial portion of their revenue from manufacturer rebates negotiated in exchange for favorable formulary placement. Those rebates were calculated as a percentage of list price. When the IRA negotiates list prices down by 50 to 70 percent for selected drugs, the rebate base on those drugs collapses proportionally.

For Express Scripts, CVS Caremark, and OptumRx — the three dominant PBMs collectively managing the prescription benefits for the large majority of American commercial and Medicare lives — the loss of rebate revenue on negotiated drugs is a structural revenue compression. The PBMs’ response has been to accelerate the shift toward administrative fee models (where they charge a flat fee per prescription rather than a rebate percentage) and to expand their specialty pharmacy operations, where revenue depends on services rather than drug pricing spreads.

The IRA also eliminates the coverage gap discount program for Part D, which had required manufacturers to provide a 70 percent discount on brand drugs used by beneficiaries in the donut hole. That discount program was itself a significant revenue source for PBMs who structured contracts around it. Its elimination simplifies the Part D benefit structure but reduces the complexity-based margins that PBMs historically embedded in their administration of the donut hole.

“The [IRA] will generate net savings of roughly $160 billion for the federal government over the next 10 years, with the bulk of those savings accruing from Part D drug price negotiation and the inflation rebate provisions.” — Congressional Budget Office, Updated Budget Projections for the IRA Drug Pricing Provisions, February 2024 [1]

The Innovation Trade-Off: What the Evidence Actually Shows

CBO and NBER Projections on Drug Approval Rates

The Congressional Budget Office scored the IRA in 2022 with the projection that the law would result in approximately 13 fewer drug approvals over the next 30 years, relative to a baseline without the IRA. This estimate was criticized by the pharmaceutical industry as too low and by progressive policy analysts as too high, reflecting the genuine uncertainty in projecting how changes to future revenue expectations affect current drug development decisions made by a heterogeneous industry.

The CBO’s methodology involved estimating the reduction in expected net present value (NPV) of future drug revenue under the IRA, calculating a relationship between expected NPV and the historical number of drug development programs, and translating that relationship into a projected number of forgone approvals. The 13-drug figure represents approximately 1 percent of the 1,300 new drug approvals the CBO baseline projected over 30 years. Subsequent independent analyses by researchers at NBER, using slightly different methodological assumptions, produced estimates ranging from 8 to 35 fewer approvals over the same period [12].

The variation in estimates reflects genuine uncertainty in several key parameters: the price elasticity of pharmaceutical R&D investment, the distribution of NPV reductions across therapeutic categories, the degree to which reduced U.S. revenue expectations affect global drug development decisions by multinational firms, and the counterfactual question of whether some forgone drugs would have been approved anyway through non-U.S. development paths.

What the academic consensus agrees on is the direction: the IRA will reduce the expected NPV of future drug development in therapeutic categories with high Medicare penetration, and reduced expected NPV will result in some reduction in development investment in those categories. The magnitude of that reduction is uncertain, but the sign is not.

What History Tells Us About Price Controls and Innovation

Historical evidence from international markets provides some useful reference points, though the IRA’s structure is sufficiently different from most foreign price control systems that direct analogies are imperfect. Japan’s biennial drug price revision system, which has compressed Japanese drug prices by approximately 30 to 40 percent in real terms over the past two decades, has coincided with a decline in Japan’s share of global pharmaceutical R&D from approximately 20 percent in 2000 to approximately 10 percent in 2020. Causation is difficult to establish — Japan faces demographic and educational factors that affect its research capacity independently of drug pricing — but the correlation is at least consistent with the theoretical prediction.

Germany’s AMNOG system, introduced in 2011, provides a more recent and arguably cleaner natural experiment. After AMNOG took effect, several large manufacturers withdrew drugs from the German market or declined to launch new drugs there, citing inadequate reimbursement. The AMNOG-era German pharmaceutical market saw a reduction in the number of new launches and some evidence of delayed launches relative to the pre-AMNOG period. The German government has since modified AMNOG to address the most egregious access limitations, but the episode demonstrated that price negotiation mechanisms can affect launch decisions in ways that harm patient access.

The U.S. context differs in important respects. The commercial market remains unregulated, meaning a drug that generates inadequate Medicare revenue can still be commercially viable if commercial revenue is sufficient. Most major drugs in the U.S. generate 40 to 60 percent of their revenue from commercial insurance, not Medicare. The IRA’s direct impact on expected drug revenue is therefore partial, and the innovation disincentive, while real, is smaller than it would be under a system that regulated all payer prices simultaneously.

The Global Competitive Context: U.S. Drug Pricing in an International Comparison

U.S. vs EU vs Japan: Negotiation Mechanics Compared

The United States is not the only country that negotiates drug prices. Every major developed economy negotiates with pharmaceutical manufacturers, and the mechanisms they use have evolved significantly over the past two decades. What distinguishes the U.S. under the IRA from other markets is not the existence of negotiation but its scale, its speed of implementation, and its potential to reshape the global pricing architecture.

Germany’s AMNOG process begins immediately after drug approval, with the Federal Joint Committee (G-BA) assessing “added benefit” relative to the appropriate comparator within 12 months. If the drug demonstrates added benefit, the National Association of Statutory Health Insurance Funds (GKV-SV) negotiates a reimbursement price with the manufacturer. If it does not demonstrate added benefit, the drug is reimbursed at the price of the least costly comparator. This immediate assessment creates a dramatically different incentive for launch pricing compared to the U.S. system, where no formal negotiation occurred for most of the history of Medicare Part D.

England’s NICE process evaluates drugs through cost-effectiveness analysis, accepting drugs that deliver health outcomes at less than approximately 30,000 pounds per quality-adjusted life year (QALY). This threshold is absolute in a way that the IRA’s MFP calculation is not: if a drug fails NICE’s cost-effectiveness threshold, it is simply not reimbursed on the NHS formulary. The U.S. IRA process negotiates but does not exclude drugs from Medicare, ensuring patient access to all approved drugs while compressing the price.

France uses a four-level evaluation of “actual clinical benefit” (SMR) and “improvement in actual clinical benefit” (ASMR) to determine reimbursement rates. Japan uses a therapeutic category-based pricing system supplemented by the biennial price revision mechanism. In each case, the common thread is that manufacturers must demonstrate value relative to existing alternatives to justify premium pricing, a concept that is embedded in the IRA through the MFP calculation methodology’s consideration of clinical evidence and therapeutic alternatives.

Launch Sequencing and the Changing Priority of the U.S. Market

Before the IRA, the United States was the first launch market for the large majority of new drugs globally, and for good reason: U.S. list prices exceeded prices in other markets by 2 to 5 times, making the U.S. the highest-value launch market in the world. U.S. launch timing also affected reimbursement negotiations in foreign markets, where price-referencing agencies sometimes used U.S. prices as an upper bound for their own negotiations.

The IRA changes this calculus at the margin. As U.S. Medicare prices for mature drugs converge toward international reference prices through the negotiation process, the U.S. market loses some of its premium pricing advantage relative to Europe. For drugs that will be heavy Medicare users — cardiovascular agents, diabetes treatments, certain oncology drugs — the post-IRA U.S. Medicare price may eventually be closer to the UK or French reimbursed price than to the historical U.S. list price.

Some manufacturers have already adjusted their launch sequencing in response. A few companies have launched drugs in Europe first to establish a price anchor and regulatory precedent before submitting for U.S. approval, in cases where the European clinical trial population provides sufficient data for FDA submission. This reversal of historical U.S.-first launch sequencing is rare, but its direction is notable. The U.S. retains substantial advantages as a launch market — the largest single national market, the richest commercial payer environment, and the deepest venture capital funding base for pre-launch companies — but the pricing advantage for the Medicare component is narrowing.

What Happens Next: 2026-2032 Projections

Negotiation Round Expansion and the Coming Drug List

The IRA’s negotiation program expands on a defined statutory schedule. The first round covered 10 drugs, with prices effective January 2026. The second round covers 15 drugs, with prices effective January 2027. The third round covers 15 drugs effective January 2028, the same year Part B drugs first become eligible. From 2029 onward, CMS may select up to 20 drugs per year for negotiation. The cumulative number of drugs subject to MFPs will grow to approximately 60 by 2030 and to over 100 by 2035 if the program continues on its current trajectory.

The expansion of the negotiation list into oncology is the most financially consequential development on the near-term horizon. CMS’s selection methodology prioritizes drugs by total Medicare spending, which means that as the first-round cardiovascular and diabetes drugs are negotiated to lower prices, their total Medicare spending falls, opening space in the spending rankings for oncology drugs to enter the selection pool. Keytruda’s biologic status gives it until 2027 before eligibility opens, but drugs like Bristol Myers Squibb’s Opdivo (nivolumab), approved in December 2014, became eligible in 2027 under the 13-year biologic threshold.

The selection logic also responds to biosimilar competition. Drugs for which biosimilars have launched are excluded from negotiation, creating an incentive for biosimilar manufacturers to accelerate their development and launch timelines for drugs approaching the IRA negotiation selection window. If a biosimilar for Stelara reduces its selection eligibility, both the brand manufacturer and the biosimilar manufacturer benefit from a slightly different competitive outcome than would have existed without the IRA — the brand avoids negotiation, the biosimilar gains volume faster. This biosimilar-IRA interaction is underappreciated in public policy analysis but creates concrete incentives in the biosimilar development market.

The Part D Redesign’s Long-Term Effects on Formulary Structure

The elimination of the coverage gap and the introduction of the $2,000 out-of-pocket cap have simplified the Part D benefit structure in ways that will over time reshape how Part D plans construct their formularies. Before the IRA, formulary design was a complex interaction of coverage gap mechanics, catastrophic threshold calculations, and rebate economics. Plans had strong financial incentives to place high-rebate drugs on preferred tiers because the plan’s financial liability was primarily in the initial coverage phase, where tiering controlled plan costs.

After the IRA, plans face a 60 percent liability share in the catastrophic phase for drugs subject to negotiated prices. This shifts the plan’s incentive toward formulary placement that reduces total drug spending rather than maximizing rebate capture. A plan that previously preferred a high-rebate drug at list price over a lower-priced alternative now has to weigh the 60 percent catastrophic liability against the rebate advantage. This structural shift in formulary incentives should theoretically benefit drugs with lower actual costs over drugs with high list prices and high rebates — a dynamic that disadvantages the traditional drug company strategy of maintaining high list prices while providing large rebates to PBMs and plans.

The long-term effect is likely a convergence between list price and net price in the Part D market, as the financial advantages of the high-list/high-rebate structure are reduced. This would be a significant change from the pre-IRA system, where the gap between list price and net price had grown to average approximately 49 percent across the pharmaceutical market according to IQVIA analysis [2]. Whether manufacturers, PBMs, and plans can maintain the list/net spread in the commercial market while accepting compression in Part D remains to be seen.

The Insulin Cap and Its Broader Implications

The IRA capped out-of-pocket costs for insulin products at $35 per month for Medicare Part D beneficiaries beginning in January 2023, and Congress subsequently extended the cap to all insulins regardless of payer. This insulin-specific provision is not formally part of the negotiation mechanism but operates as a direct price cap that has already produced observable market effects: several insulin manufacturers, including Eli Lilly, Novo Nordisk, and Sanofi, reduced their insulin list prices to levels consistent with the $35 cap in the months following the IRA’s passage.

These voluntary reductions, which Lilly announced in March 2023 and Novo Nordisk and Sanofi followed, were the first large-scale U.S. list price reductions for major branded drugs in decades. They were driven partly by the political and regulatory pressure created by the IRA and partly by the recognition that the list price/net price spread on insulin had become so large and publicly criticized that maintaining it posed reputational and political risks that exceeded the financial benefit. The insulin episode demonstrates that the IRA’s price-setting authority has effects beyond the drugs formally selected for negotiation: the credible threat of negotiation and the political environment it has created have produced voluntary price reductions that the law itself did not require.

What Companies, Investors, and Payers Should Do Right Now

For Pharmaceutical Manufacturers: The Four-Point Response

The companies managing IRA exposure most effectively share a common approach: they have translated the IRA’s statutory structure into a financial framework that runs through every R&D, commercial, and BD decision in the organization. That framework has four components.

First, every drug in Phase II and Phase III development should have an IRA sensitivity score that quantifies the estimated reduction in peak NPV attributable to IRA negotiation. That score requires four inputs: estimated approval year, Medicare penetration in the target indication, expected negotiation round (based on projected Medicare spending rank), and expected price reduction at negotiation (based on comparator analysis and CMS’s published justification documents for first-round negotiations). Building these inputs into the development-stage financial model changes investment decisions at the margin and ensures that IRA exposure is priced into development priorities before it becomes a post-launch commercial problem.

Second, the 13-year biologic threshold creates a genuine structural advantage for new molecular entities designed as biologics or complex molecules where both a small-molecule and biologic approach is scientifically feasible. This is not a recommendation to develop inferior biologic drugs for regulatory arbitrage; it is a recommendation to be explicit about the financial advantage of the biologic pathway when both pathways are scientifically valid and to let that advantage inform target selection and modality decisions at the candidate identification stage.

Third, manufacturers with drugs approaching the IRA negotiation window should invest in developing the clinical and pharmacoeconomic evidence base that will support their negotiation position. CMS’s negotiation justification documents for the first round reveal that the agency considered quality-adjusted life year estimates, head-to-head comparison data, and real-world evidence on clinical outcomes in making its price determinations. Manufacturers who arrive at the negotiation table with robust evidence of differential clinical benefit from the negotiated drug’s current indication-specific use are better positioned to defend a higher MFP than those who rely solely on list price comparisons.

Fourth, companies should review their patent and exclusivity strategies specifically for IRA interaction effects. Patent term extensions that extend into the post-IRA negotiation period protect the manufacturer’s freedom to operate and maintain their sole-supplier position, but they do so at a lower net revenue per unit sold. DrugPatentWatch provides the patent-by-patent expiry, PTE grant, and exclusivity data needed to model these overlapping timelines at the asset level, allowing companies to prioritize their patent defense investments based on the post-IRA commercial value they are actually protecting [5].

For Investors: How to Model Pharmaceutical Equities Post-IRA

Pharmaceutical equity valuation requires a new set of default assumptions post-IRA. The most important change is the addition of an IRA discount to projected U.S. revenues for all drugs with significant Medicare penetration and approval timelines that put them in the negotiation window before patent expiry. For most cardiovascular, metabolic, and oncology drugs, this means applying a 40 to 70 percent discount to projected Medicare revenues starting in approximately year 10 to 13 post-approval.

The magnitude of the IRA discount varies by drug and indication. Drugs in therapeutic categories with strong clinical differentiation and limited alternatives — certain oncology drugs, rare disease treatments, drugs with no therapeutic substitutes — will likely face smaller percentage reductions than drugs in competitive categories with multiple comparable alternatives. The CMS’s first-round experience is instructive: the deepest reductions (Januvia at 79 percent, Fiasp/NovoLog insulin at 76 percent) were in categories where therapeutic alternatives exist and clinical differentiation is limited. The smallest reduction (Imbruvica at 38 percent) was in a category where the drug was the established standard of care with limited alternatives for a defined subpopulation.

Investors should also build the IRA’s inflation rebate provision into revenue models for all existing drugs, regardless of negotiation status. For any drug with annual price increases above CPI-U, the rebate obligation reduces effective revenue by the excess price increase times total Medicare units sold. A drug growing 8 percent annually in price versus 3 percent CPI-U generates a 5 percent rebate obligation on all Medicare sales, a meaningful drag on revenue for large-volume products.

The Part D redesign’s manufacturer catastrophic liability is a third adjustment to current-year revenue models, applying immediately to drugs in the Part D catastrophic phase. For oncology drugs, rare disease treatments, and other high-cost products where a significant fraction of patients reach the catastrophic phase annually, this liability can represent 2 to 8 percent of total drug revenue, flowing directly to the P&L as a cost that did not exist before 2025.

For Payers and Health Systems: Extracting Full Value from the New Pricing Structure

Health insurance plans, PBMs, and health systems that are active managers of their pharmaceutical expenditure should be tracking IRA negotiation timelines as carefully as patent expiration dates. When an IRA negotiated price takes effect, the plan’s pharmaceutical cost for that drug drops sharply for Medicare beneficiaries. Plans that proactively restructure their formularies to encourage use of negotiated-price drugs over non-negotiated alternatives before the effective date will capture the financial benefit faster.

Hospital systems and health systems with integrated Medicare Advantage plans face a distinct financial calculation. The all-inclusive capitated payment structure of Medicare Advantage means that the negotiated price savings in Part D flow back to the plan, not to the hospital as a direct cost reduction. But the reduction in beneficiary out-of-pocket costs under the $2,000 cap and the catastrophic provision reduces the financial barrier to prescription adherence, potentially improving clinical outcomes and reducing downstream hospitalizations for conditions like atrial fibrillation, heart failure, and cancer — outcomes that directly affect Medicare Advantage plan financial performance.

The inflation rebate provision creates an opportunity for plan and system pharmacy directors to negotiate new commercial contracts that incorporate IRA-like price stability provisions, even for non-Medicare drug spending. If a manufacturer has agreed to hold Medicare price increases below CPI-U to avoid rebate penalties, that same constraint can be proposed as a contractual provision for commercial market contracts. Several large employers and commercial insurers have already begun incorporating CPI-indexed price adjustment caps in their pharmaceutical contracts, using the IRA framework as a model and the inflation rebate as precedent for the concept that above-inflation price increases are not commercially necessary.

Key Takeaways

The following points capture the most actionable conclusions from this analysis:

• The IRA’s three mechanisms — Medicare drug price negotiation, inflation rebates, and Part D benefit redesign — operate simultaneously and additively. The negotiation headline attracts attention, but the inflation rebate and the catastrophic phase manufacturer discount affect a far larger number of drugs starting immediately, before a single drug enters the negotiation program.

• The 9-year vs 13-year eligibility asymmetry between small molecules and biologics has already produced observable changes in pharmaceutical R&D composition. Small-molecule cardiovascular and metabolic drug programs face higher internal return thresholds, and early-stage VC funding has shifted toward biologics, cell therapies, and gene therapies that benefit from the 13-year eligibility window and the IRA’s limited reach into biologic development incentives.

• The first-round negotiation results — price reductions averaging 40 to 79 percent off list price for drugs including Eliquis, Jardiance, and Januvia — established a precedent that CMS will negotiate aggressively and that the courts will not intervene to block. All three circuits that have reviewed the constitutional challenges have upheld the program.

• Manufacturers are responding with higher launch prices, indication carve-outs to preserve orphan drug exemption status, subcutaneous and next-generation formulations that start independent IRA clocks, and expanded combination therapy programs that generate new exclusivity independent of the single-agent negotiation. These responses are financially rational under the IRA structure and partially offset the law’s revenue compression effect.

• The Part D redesign’s $2,000 out-of-pocket cap creates genuine and direct financial protection for Medicare beneficiaries on high-cost drugs. Approximately 1.5 million beneficiaries spend more than $2,000 annually on drugs; for those patients, the cap represents thousands of dollars in annual savings and eliminates the risk of catastrophic pharmaceutical cost that previously affected elderly Americans on fixed incomes.

• Patent intelligence tracking via platforms like DrugPatentWatch is more important, not less, in the IRA environment. The overlap between PTE-extended patent protection and IRA negotiation eligibility windows creates a new analytical layer: the value of patent defense is now a function of post-IRA revenue, not list price revenue, changing both the economics of patent litigation and the prioritization of PTE applications across multi-product portfolios [5].

• The 2026-2032 period will see IRA negotiation expand into oncology, Part B biologics, and second-generation treatments, with cumulative negotiated drug lists growing to 60 to 100 products. Companies whose pipelines are concentrated in IRA-sensitive categories without a clear structural response — biologic pathway, rare disease focus, or aggressive indication architecture — face systematic revenue compression that their current financial models may not fully reflect.

• The IRA’s innovation trade-off is real but bounded. The CBO’s estimate of 13 fewer drug approvals over 30 years, and the academic literature’s range of 8 to 35, suggests the effect exists but is modest relative to the system’s overall productivity. The more significant structural effect is the redirection of innovation toward biologic-heavy, rare disease-adjacent, and combination therapy categories at the expense of small-molecule common disease programs — a shift that affects which patients are served by pharmaceutical innovation, not just how many drugs are developed.

FAQ

1. Does the IRA’s Maximum Fair Price apply to commercial insurance, not just Medicare?

No. The MFP applies exclusively to Medicare Part D and, starting in 2028, to Medicare Part B drug purchases. Commercial insurers, employer-sponsored health plans, Medicaid programs, and the Veterans Administration are not required to use the MFP and do not benefit from it automatically. Manufacturers can charge any price they choose to non-Medicare payers. This commercial market exemption was a deliberate political concession to the pharmaceutical industry during the IRA’s drafting and represents the most significant structural limitation on the law’s total pricing reach. The practical consequence is that manufacturers can maintain high commercial list prices while accepting reduced Medicare prices, creating a dual-price system. Some commercial payers are attempting to use MFP announcements as leverage in their own contract negotiations, arguing that if Medicare can buy a drug at the MFP, the commercial market price should reflect comparable value. These efforts are contractual negotiations, not legal requirements, and their success depends on payer bargaining leverage in specific therapeutic categories.

2. Can a manufacturer withdraw a drug from Medicare rather than accept a negotiated price?

Technically, yes. The IRA does not compel manufacturers to sell to Medicare. However, the excise tax mechanism makes withdrawal economically irrational for all but the most narrowly Medicare-dependent drugs. If a manufacturer refuses to negotiate or rejects the final MFP offer, it faces an excise tax that starts at 65 percent of gross U.S. sales and escalates to 95 percent over three years. This tax applies to all U.S. sales, not just Medicare sales. For a drug generating $5 billion in total U.S. revenue, a 65 percent excise tax yields a tax bill of $3.25 billion annually — more than the commercial market net revenue in most scenarios. The tax is effectively a guarantee of participation. No manufacturer has exercised the opt-out since the program launched. The statute also includes a hardship waiver process for manufacturers who can demonstrate that the MFP would result in the drug being economically unviable to produce, but no waiver applications have been publicly reported.

3. How does the IRA affect drug development timelines for drugs still in clinical trials?