The biopharmaceutical sector is entering a period of revenue contraction that threatens the financial stability of the largest players in the industry. Between 2025 and 2030, nearly 200 drugs will lose patent protection, putting an estimated $400 billion in annual revenue at risk.1 This phenomenon is often termed the patent cliff, but for the current wave of biologics, it is better described as a slope. Unlike small-molecule drugs that see 90% revenue erosion within weeks of generic entry, complex biologics face a more gradual decline due to the high cost and technical difficulty of biosimilar development.1

The scale of this impending shift is historic. Industry analysts project that the 2025–2030 window will see approximately 190 drugs lose exclusivity, including 69 blockbusters with annual sales exceeding $1 billion each.3 Companies like Merck, Bristol Myers Squibb (BMS), and Pfizer face the highest absolute exposure. Merck, for instance, has 56% of its total revenue concentrated in a single product, Keytruda, which faces its primary patent expiration in 2028.4 This high level of concentration creates an existential need for aggressive lifecycle management (LCM) strategies that extend beyond the molecule itself.

Biopharma business development teams are shifting their focus toward the delivery mechanism. By redesigning the drug-device combination, manufacturers can migrate the patient population from a clinic-based intravenous (IV) infusion to a home-based subcutaneous (SC) injection. This strategy creates a new patent wall and effectively makes the original IV version commercially obsolete before biosimilars can gain a foothold. The target for many of these redesigns is a high-volume autoinjector or on-body pump that can handle the increased viscosity and volume required for large-molecule therapies.

The Anatomy of the 2024–2030 Patent Cliff

The current cliff is different in composition from the 2010 wave that took out Lipitor and other small-molecule blockbusters. The 2010 wave was about chemistry. The 2025–2030 wave is about biology. Monoclonal antibodies (mAbs) are the backbone of this market, representing over 46% of large-molecule injectables in 2024.5 These drugs are used in oncology, autoimmune diseases, and metabolic disorders, often requiring specialized delivery systems to maintain stability and efficacy.

Table 1: Blockbuster Revenue Exposure and Expiration Timelines

Product

Brand Owner

2024 Revenue

Primary LOE Year

Strategic Response

Keytruda

Merck

$29.5B

2028

Qlex (SC) reformulation 4

Eliquis

BMS/Pfizer

$13.0B

2026/2028

Pediatric extensions/Legal settlements 4

Opdivo

BMS

$9.0B

2028

Qvantig (SC) formulation 7

Stelara

J&J

$6.4B+

2023/2025

Momenta patent thicket 8

Humira

AbbVie

$14.0B+

2023

High-concentration/Citrate-free 5

Eylea

Regeneron

$5.9B

2025/2026

High-dose formulation 6

The Role of DrugPatentWatch in Market Analysis

To navigate these timelines, procurement and business development teams rely on specialized patent intelligence. DrugPatentWatch provides an index of Orange Book and Purple Book patent listings alongside expiration data for 134 countries.1 This platform allows competitors to map structural gaps in a biologic’s patent estate. When a brand company’s core composition-of-matter claims rest on functional definitions without sufficient sequence disclosure, that gap appears in the prior art and claim structure.

Strategic investors use this data to identify when a drug will face competition and what secondary patents might delay that entry. The platform tracks US drug prices, top drug sales, and investigational drugs in Phase I-III trials, providing a holistic view of the competitive landscape.1 This intelligence is vital for device companies looking to partner with biopharma firms on redesigns that can bypass the “GLP-1 patent lock” or extend the revenue life of an immunology franchise.1

Archetyping the Loss of Exclusivity

There is no one-size-fits-all approach to managing the end of a drug’s monopoly. Best-in-class teams categorize their brands into loss of exclusivity (LOE) archetypes to guide their decisions.11 This categorization depends on the molecule type, the route of administration, and the unique features of the drug.

Table 2: Molecule Type and Delivery Complexity

Molecule Type

Market Share (2024)

Delivery Format

Key Innovation

Monoclonal Antibodies

46%

IV / Subcutaneous

Bispecifics and ADCs

Peptides and Proteins

~20%

Prefilled Pens

GLP-1 agonists (Obesity)

Fc Fusion Proteins

High Growth

Wearable Pumps

Half-life extension

Cell & Gene Therapy

Emerging

Intramuscular

Lipid nanoparticle platforms

Complex biologics do not follow the same rules as small molecules. Biosimilar uptake is often slower due to market inertia and the complexity of manufacturing. For example, AbbVie’s Humira maintained brand share post-LOE but lost 60% of net sales because of the steep discounting required to fend off biosimilars.11 This highlights that volume can be defended, but net value requires a different strategy, such as introducing a redesigned device that offers a superior patient experience.

The Manufacturing Moat

The technical difficulty of manufacturing a biologic serves as a natural barrier to entry. Many biologics are temperature-sensitive and require a “cold chain” for distribution and storage.3 Companies that master these supply chain logistics can use them as a “manufacturing moat.” For example, Samsung Biologics expanded its injectable fill-finish capacity in 2023 to meet the demand from global biotech clients launching subcutaneous biologics and biosimilars.5

CDMOs are moving upstream by offering formulation design and device integration alongside manufacturing.5 This allows biotechs to co-develop smart autoinjectors and prefilled syringes that integrate adherence tracking. By embedding the device into the manufacturing process, a company can ensure that any biosimilar competitor would have to replicate not just the molecule, but also the specific device-drug interaction, which is a significant engineering hurdle.

The Subcutaneous Pivot

The pivot from intravenous infusion to subcutaneous injection is a sophisticated defensive tactic. This strategy aims to change the standard of care before the original IV patents expire, creating commercial obsolescence for the biosimilars that copy the older IV standard.13

The transition is enabled by hyaluronidase enzymes, such as Halozyme’s ENHANZE platform, which temporarily degrade hyaluronan in the subcutaneous space.4 This allows for the delivery of large volumes (up to 10 mL) of antibodies in a single rapid injection. The strategic goal is to launch the SC version 2 to 3 years before the IV patent cliff to migrate the oncology workflows and the patient population.

Keytruda Qlex: A Masterclass in Defense

Merck’s Keytruda is the definitive example of this “Subcutaneous Shield.” While the IV patent is set to expire in 2028, the 2025 launch of Keytruda Qlex (pembrolizumab and berahyaluronidase alfa-pmph) aims to switch 30% to 40% of the patient base to a form protected by patents into the 2040s.4

Keytruda generated $29.5 billion in 2024, representing 56% of Merck’s entire business.4 Without the SC reformulation, Merck faced an 80% revenue erosion post-2028. By investing $500 million to $1 billion in the Qlex program, Merck preserves $9 billion to $12 billion in annual revenue, achieving an ROI of over 1,000%.4

Table 3: Keytruda SC vs. IV Comparison

Feature

Keytruda IV (Original)

Keytruda Qlex (Redesign)

Administration Type

Infusion

Subcutaneous Injection

Time to Administer

30 minutes

2 minutes 4

Dosing Frequency

Every 3 weeks

Every 6 weeks 4

Patent Protection

Expires 2028

Potential to 2042 4

Technology

Standard IV

Halozyme ENHANZE 4

The formulation change is dramatic. It moves the drug from a clinical infusion setting to a rapid injection that can be performed in a doctor’s office or eventually at home. This shift targets the oncologist’s workflow, freeing up infusion chairs for other patients and making the SC version the preferred option for both clinicians and patients.

Engineering the High-Volume Delivery

As biopharma companies target higher-dose therapies, the engineering of the delivery device becomes a primary focus. Large-volume subcutaneous injections (greater than 1 mL) are becoming more common in oncology, autoimmune, and metabolic disorders.16

BD and Ypsomed expanded their partnership in 2026 to address this need with a 5.5 mL version of the BD Neopak XtraFlow glass prefillable syringe.16 This syringe incorporates a shorter 8-millimeter needle and thinner cannula walls to improve flow and reduce injection time for high-viscosity medicines. The device is designed for full compatibility with Ypsomed’s YpsoMate 5.5 autoinjector platform.

Technical Challenges in Large-Volume Injections

Standard syringes have limits when dealing with high volumes and viscosities. The break-loose force required to start the stopper moving can be high, and the force needed to deliver the drug through a fine needle can cause pain or lead to incomplete doses.19

Electromechanical devices or advanced autoinjectors can overcome these issues. Some devices use a separate motor to provide a constant force while deploying the needle, preventing the sudden jolts seen in spring-driven systems.19 These systems also have a power reserve that can overcome the break-loose force while controlling the rate of injection, which is essential for patient comfort.

Table 4: Syringe and Autoinjector Performance Metrics

Device Type

Max Volume

Viscosity Support

Key Benefit

Standard PFS

1 mL

Low

Low cost, simple

BD Neopak 2.25

2.25 mL

Up to 70 cP

Fast injection, optimized flow

YpsoMate 5.5

5.5 mL

High

Large volume, ergonomic

Wearable Pump

10 mL+

Variable

Hands-free, long duration

The Human Factors Equation

Human factors testing is used to optimize device design concerning cognitive and ergonomic interactions.20 The FDA requests these studies to ensure that users can operate devices safely and effectively. This includes proof of adequacy of the instructions for use and the identification of potential use errors. For example, if a device is too difficult to grip or requires too much force to activate, an elderly patient with rheumatoid arthritis may struggle to use it, leading to non-adherence and revenue loss for the brand.

Janssen and the Stelara Thicket

Johnson & Johnson’s Stelara (ustekinumab) provides another case study in complex IP defense. J&J has focused on the commercialization of newer therapies like Tremfya to transition patients before the Stelara patent expiry.21 However, the company also asserted manufacturing patents acquired through its 2020 purchase of Momenta Pharmaceuticals to delay biosimilar entry.8

Stelara’s primary “composition of matter” patent expired in September 2023, but the “patent thicket” around the drug remains formidable. J&J listed manufacturing patents that cover the animal cell cultures used to produce the antibody, controlling what carbohydrates and amino acids are attached to the proteins.8 These patents were awarded a decade ago and have been used as a bargaining chip to negotiate later market entry dates for biosimilars.

Table 5: Stelara Patent and Indication Timeline

Indication

US Approval Year

Key Patent Expiry

Plaque Psoriasis

2009

Sep 2023 (Composition) 21

Psoriatic Arthritis

2013

2031 (Estimated) 21

Crohn’s Disease

2016

2032 (Estimated) 23

Ulcerative Colitis

2019

Sep 2039 (Method of use) 22

Every extra day of US market exclusivity for Stelara is worth nearly $18 million in revenue.8 By defending method-of-use patents that expire in 2039, J&J can preserve a significant portion of its immunology franchise value even as the core molecule becomes generic.

Biosimilar Development and the “Void”

Only 12 molecules set to lose patent protection from 2025 to 2034 had biosimilars in development as of mid-2024, leaving a “biosimilar void” for over 100 other biologic expiries.24 This void is driven by market potential, manufacturing complexity, and the risk of patent litigation.

Developing a biosimilar is a massive undertaking. It typically takes 6 to 9 years and costs between $100 million and $300 million.25 These programs require sophisticated analytical testing to prove that the biosimilar is highly similar to the reference product with no clinically meaningful differences.

The High Cost of Comparative Efficacy Studies

Comparative efficacy studies (CES) are often the most expensive and time-consuming part of the biosimilar approval process. These studies generally have low sensitivity compared to analytical assessments but cost $24 million on average.26

The FDA is now moving to accelerate biosimilar development by recommending when comparative analytical assessments (CAA) may be used instead of CES.28 Modern analytical technologies can characterize purified proteins and model their effects with high specificity. If the FDA accepts CAA as more sensitive than CES, it could reduce the development timeline by 1 to 3 years and significantly lower the barrier to market entry.25

Interchangeability as a Value Driver

Designating all approved biosimilars as interchangeable could increase their lifetime net revenue by $2 billion.29 An interchangeable designation allows pharmacists to substitute a biosimilar for the brand-name drug at the pharmacy level without the intervention of the prescriber. This is a key component of the strategy to combat the limited access to affordable biologics in the US.

Table 6: Biosimilar Approval and Market Adoption Metrics

Metric

Current Status (2024)

Potential Impact of Reform

Total Approved Biosimilars

76 26

Sharp Increase

Market Share of Biosimilars

Below 20% 26

Targeted 50%+ 25

Development Cost

$100M – $300M 25

Potential 30% Reduction

Time to Market

6 – 9 Years 25

Reduction by 1-3 Years 27

The Economics of Device Redesign ROI

For a device company, the value proposition is anchored in the brand’s ability to defend its pricing power. When a drug is delivered via a proprietary device, the “effective patent life” is often extended because a generic competitor cannot simply copy the device without infringing on its own set of patents.30

A study of medicine/device combination products found that unexpired device patents existed for 90% of products.30 These device patents afforded a median of 4.7 years of additional protection beyond the active ingredient patent. For a multi-billion dollar drug, this extension is worth hundreds of millions in net present value.

Calculating the Return on Reformulation

The ROI of reformulation is often superior to the ROI of new molecule discovery. Discovery and clinical development of a new molecule can exceed $2 billion and have low success rates.30 In contrast, reformulating an existing, proven asset into a new delivery system has a much higher probability of regulatory success.

The math of the Keytruda Qlex program illustrates this:

With a program cost of approximately $1 billion and preserved revenue of $10 billion per year, the ROI exceeds 1,000% in the first year alone.4 This creates a powerful economic incentive to focus on incremental innovations that improve patient adherence rather than gambling on the high-risk search for new chemical entities.

The Adherence Bonus

Better devices lead to better outcomes. In a study comparing the subcutaneous injection of infliximab via an autoinjector versus a prefilled syringe, patients using the autoinjector reported higher satisfaction and better treatment compliance.32

Higher satisfaction leads to increased adherence, which prevents the “suboptimal dosing” that can cause treatment failure.20 From a business perspective, every patient who stays on therapy longer is a source of recurring revenue. In some categories, such as immunology or multiple sclerosis, improving adherence by 10% can be worth more than a new indication launch.

Structing the Business Development Deal

Biopharma companies are diversifying their funding and partnership approaches as capital needs grow. Royalty funding is gaining prominence as a non-dilutive capital source.33

Synthetic royalties, which are created for a transaction rather than being part of an existing license, have quadrupled in growth over the last five years.33 In 2024, synthetic royalties accounted for over 50% of all royalty funding for biopharma companies. These deals allow a company to secure long-term capital in exchange for a portion of future revenues without giving up operational control or product rights.

Upfronts, Milestones, and Royalties

A typical licensing or partnership deal involves three core components: an upfront payment, milestone payments, and ongoing royalties.

Table 7: Licensing Deal Component Benchmarks

Component

Early-Stage Deal

Late-Stage Deal

Upfront Payment

Low single-digit millions

$100M – $1B+ 34

Milestone Payments

$50M – $200M

$500M – $3B+ 34

Royalty Rate

1% – 5%

8% – 20% 34

Risk-Adjusted Discount

15% – 20%

10% – 15% 35

Upfront payments compensate the licensor for initial IP rights. Milestones are triggered by development events like Phase III starts or FDA approvals. Royalties are typically a percentage of net sales, often tiered based on volume. For example, a deal might pay 8% on the first $500 million in sales and 12% on everything above that threshold.35

Option-to-License Deals

Option-to-license deals are common in the medtech space. A big pharma company might pay an upfront fee for the right to obtain a license for a new device platform at a future date, usually after seeing human factors data or clinical trial results. This limits the upfront commitment while ensuring the pharma firm has a first-mover advantage if the technology proves successful.

Human Factors and Regulatory Friction

The US FDA defines a combination product as comprising two or more constituents, such as a drug and a device.36 These products are regulated by the Office of Combination Products, and the regulatory process is entirely different from a standard drug application.

A change in the drug delivery device is considered a fundamental change. If a manufacturer switches devices mid-trial, it introduces an uncontrolled variable that can mess with the clinical data.37 The FDA has seen that big effects can come from small changes. For example, a slightly different needle gauge or plunger speed can change the bioavailability of the drug, requiring new bridging studies.

The Risk of Mid-Development Switches

Switching devices mid-development is never a good idea. If patients cannot get their doses correctly in the middle of a study due to a device malfunction or user error, tens of millions of dollars in study work can go out the window.37

However, if a team is early enough in the process, they can execute a “simpler” solution by running a safety-related study like a relative bioavailability study or a Phase I PK study.37 Taking a small delay to rerun a study with the actual device significantly increases the probability of regulatory success compared to submitting an unsuccessful application with an old device presentation.

Table 8: Human Factors and Design Validation Steps

Step

Goal

Outcome

Threshold Analysis

Identify critical tasks

Risk-based study design

Formative Testing

Optimize device design

User feedback for refinement

Summative Testing

Design validation

Proof of safe/effective use

Design Verification

Technical testing

Confirmation of device specs

Bridging and Bioequivalence

When changing the mode of application—such as moving from a vial to an autoinjector—the FDA requests bridging testing. This includes bioequivalency data to show that the new device delivers the same amount of drug to the bloodstream as the old method. FDA approval delays can take up to a year for complete response letters if there are requirements for additional clinical testing for changes to combination products.20

The PBM and Private Label Threat

A new dynamic is reshaping the post-LOE landscape: the rise of PBM private labels. CVS Health launched Cordavis in April 2024 and excluded branded Humira in favor of its co-licensed biosimilar.2 Evernorth (Express Scripts) followed with Quallent Pharmaceuticals.

This shift allows PBMs to capture more of the margin by acting as both the pharmacy and the “manufacturer” (via co-licensing). For an originator company, this means the traditional “rebate wall” strategy is losing its effectiveness. If the PBM owns the biosimilar, it has a direct financial incentive to prioritize its own product over the branded one, regardless of the rebate offered.

Value-Based Procurement

In Europe and increasingly in the US, procurement is moving toward value-based frameworks. The MEAT (Most Economically Advantageous Tender) framework evaluates products based on therapeutic interest and contribution to “good use” rather than just price.2

Table 9: MEAT Framework Evaluation Criteria

Category

Weight

Specific Metrics

Therapeutic & Technical

25%

Presentation, labeling, stability data

Contribution to Good Use

35%

Help in clinical follow-up, training

Price / Cost

40%

Total cost of ownership, net price

By redesigning a device to include better labeling, traceability support, or features that help in clinical follow-up, a manufacturer can score higher in these value-based tenders, even if their price is higher than a generic competitor.

The Manufacturing Shift to Single-Use

Process life-cycle management in biopharmaceutical manufacturing is also evolving. There is a strong trend toward single-use processes to reduce the cradle-to-grave impact of manufacturing monoclonal antibodies.38 Single-use systems are more flexible and can handle smaller batch sizes, which is necessary for the high-cost biologics used in treating rare diseases.

Quality by Design (QbD)

The FDA’s Quality by Design initiative emphasizes the assessment and management of risks to product safety and quality.38 Manufacturers must identify Critical Process Parameters (CPPs) and ensure that their purification processes are robust. For example, during the late-stage development of the purification process for Tysabri (natalizumab), a potency assay revealed subtle differences between early clinical and late-stage versions.38 An investigation found that the large-scale process was removing a minor molecular species, and understanding this change allowed the program to proceed without interruption.

Model-Based Methods

Biopharma companies are increasingly using mathematical models for process monitoring and control.39 These models help in the generation of process knowledge and the optimization of process parameters. This is essential for continuous improvement during the entire process lifecycle, from scale-up to product discontinuation.

Table 10: Biopharmaceutical Process Challenges

Challenge

Model-Based Solution

Benefit

Knowledge Generation

Mathematical modeling

Transparency in decision-making

Process Monitoring

Supervision of kPPs

Real-time control of quality

Process Optimization

Data mining techniques

High productivity and yield

Continuous Improvement

Iterative process loops

Reduction of by-products

The “Situation Room” for LOE

Proactive teams do not wait until the patent expiration date to act. They set up an “LOE Situation Room” years ahead of expiry to monitor market activity and measure the impact of their tactics.11

This situation room uses historical analogs to forecast competitor entries and pricing. It allows for real-time alignment on strategic options, such as whether to launch an authorized generic or shift promotional effort toward a different therapeutic segment where brand loyalty is higher. For example, in a case study of a large retail brand, shifting resources away from low-margin prescribers allowed the manufacturer to redeploy value to longer-term growth strategies.11

The Total Cost of Ownership (TCO) Approach

Procurement teams are also moving toward a TCO approach when evaluating biosimilars. This looks beyond the unit price to the costs associated with storage, training, and potential medication errors.2

“Expensive biologic medications make up only 5% of prescriptions in the U.S. but account for 51% of total drug spending as of 2024”.26

A branded product with a superior delivery system might have a higher unit price but a lower TCO if it reduces waste and improves patient safety. By utilizing patent intelligence to monitor these windows, procurement firms can lock in supply and plan for generic entry years in advance.

The Connected Future of MedTech

The future of drug delivery is connected. The convergence of smartphone adoption and increased digital fluency is driving the growth of digital health offerings.40 MedTech companies are no longer just making devices; they are building connected infrastructures that provide real-time connectivity between patients and healthcare providers.

Digital Health as a Differentiator

Digital health tools can enhance workflow efficiency and extend geographical reach.40 For a biopharma company, a digital health partnership can supplement and differentiate a core therapy. Common criteria for these solutions include an engaging user experience, secure data, and seamless integration into the patient’s daily life.

Gen X, Y, and Z already make up 75% of the workforce, and these digital-native generations prefer tailored, connected experiences.40 If a manufacturer can offer an autoinjector that syncs with an app to track symptoms and adherence, they can build a level of patient loyalty that a traditional “dumb” generic cannot match.

Biosimilar Adoption Hesitance

Despite the cost-saving potential, there is still hesitancy in biosimilar adoption among some physicians and patients. This is often driven by aggressive marketing from originator manufacturers and concerns about switching patients who are stable on a branded product.41

Innovative adoption strategies, such as providing enhanced patient support programs and demonstrating equivalent immunogenicity and PK profiles, are essential for biosimilar success.32 However, the slower-than-expected adoption of biosimilars highlights the continued importance of brand reputation and the “intangible” value of a proven delivery system.

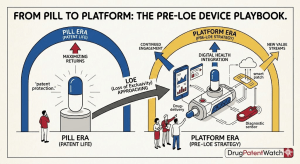

Conclusion: Defend the Moat

The patent cliff is a predictable climax of a multi-year strategic battle. It is not a sudden accident, but a known variable that dictates strategy from the moment a molecule is discovered.31 To survive the 2025–2030 precipice, biopharma and device companies must work in lockstep.

The redesign of the drug-device combination is the most powerful tool in the lifecycle management arsenal. By engineering clinical superiority through better delivery—whether via high-volume autoinjectors, SC reformulations with hyaluronidase, or connected digital platforms—originators can command premium pricing and neutralize the threat of biosimilars. The financial stakes are in the hundreds of billions, and the winners will be those who invest with scientific clarity and strategic foresight.

Key Takeaways

Pivot to Subcutaneous (SC) Delivery: Migrating from IV to SC using Halozyme’s ENHANZE technology can preserve over $10 billion in annual revenue for oncology blockbusters like Keytruda and Opdivo.4

High-Volume Engineering is Critical: The expansion of the subcutaneous delivery space to 5.5 mL and beyond is a primary focus for partners like BD and Ypsomed to handle next-generation high-dose biologics.16

Manufacturing Patents as a Barrier: J&J’s use of Momenta’s manufacturing patents for Stelara demonstrates that IP protection can extend far beyond the core molecule patent.8

FDA Streamlining of Biosimilars: New draft guidance reducing the requirement for comparative efficacy studies could accelerate the entry of biosimilars, making the device-led defense even more urgent.27

The Power of Synthetic Royalties: Biopharma firms are increasingly using synthetic royalty funding as a non-dilutive capital source to fund these expensive redesign and reformulation programs.33

The “Situation Room” Strategy: Successful brands start LOE planning years in advance, using archetypes and real-time data to decide where to defend and where to walk away.11

FAQ

What is the “Subcutaneous Shield” in pharmaceutical IP strategy? This is a defensive tactic where a company reformulates an intravenous drug as a subcutaneous injection shortly before the IV patents expire. This moves the standard of care to a new, patent-protected presentation, making incoming biosimilars commercially obsolete.13

Why are BD and Ypsomed developing a 5.5 mL glass syringe? As biologics move toward higher doses and concentrations, they become more viscous. Standard 1 mL or 2.25 mL syringes cannot deliver these large volumes comfortably. The 5.5 mL syringe, compatible with large-volume autoinjectors, addresses this gap in oncology and rare disease markets.16

How does hyaluronidase enable high-volume drug delivery? Recombinant human hyaluronidase (PH20) temporarily degrades hyaluronan in the subcutaneous space. This opens up the tissue matrix to allow for the rapid delivery of up to 10-15 mL of fluid, enabling drugs like Keytruda to be injected in 2 minutes instead of 30.4

What is the ROI of reformulating a drug before its patent expires? For blockbusters like Keytruda, the ROI can exceed 1,000%. By spending $1 billion on reformulation, Merck can preserve $9–$12 billion in annual revenue that would otherwise be lost to biosimilars.4

Why is the “biosimilar void” significant for manufacturers? The void refers to the 100+ biologics losing patent protection with no biosimilars currently in development. This indicates that factors like manufacturing complexity and legal risk are deterring competition, providing a longer window for originators to execute lifecycle management strategies.24

The Adherence and Outcomes Benefits of Using a Connected, Reusable Auto-Injector for Self-Injecting Biologics: A Narrative Review – PMC, accessed February 26, 2026, https://pmc.ncbi.nlm.nih.gov/articles/PMC10567963/

Pharmacokinetic comparison of subcutaneously administered CT‐P13 (biosimilar of infliximab) via autoinjector and pre‐filled syringe in healthy participants – PMC, accessed February 26, 2026, https://pmc.ncbi.nlm.nih.gov/articles/PMC11443321/