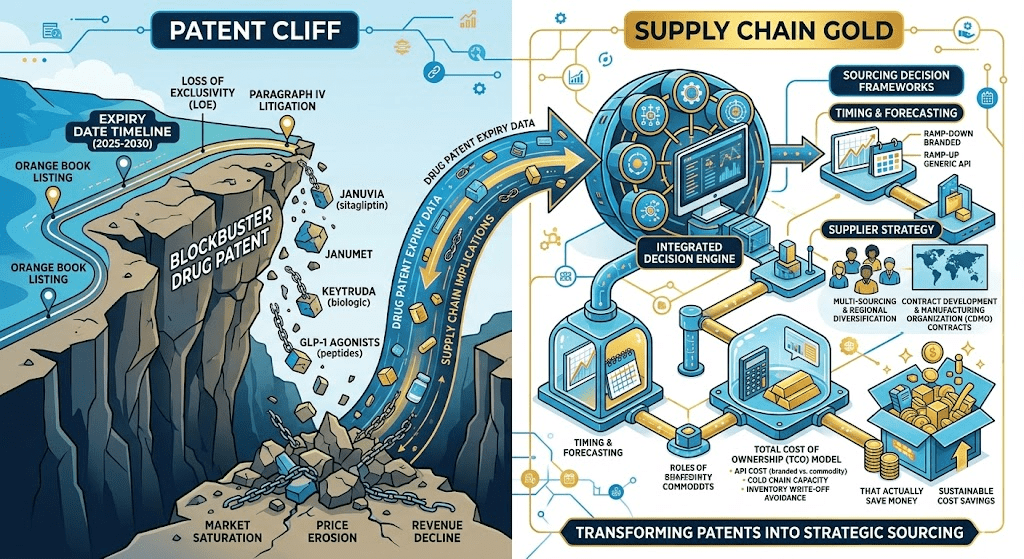

The $300 Billion Window Procurement Teams Are Missing

Between now and 2030, an estimated $300 billion in branded drug revenue will lose patent exclusivity in the United States alone, covering roughly 200 drugs and approximately 70 blockbusters, each generating more than $1 billion annually. That figure is three times the size of the previous patent cliff, which erased around $100 billion in brand-name sales in 2016 [1].

For innovator companies, the headlines are grim: Bristol-Myers Squibb faces an estimated 47% revenue erosion by 2030 as Eliquis and Opdivo fall off the cliff; Merck confronts the prospect of losing more than half its total revenue when Keytruda’s core composition-of-matter patent expires in 2028 [2]. For procurement organizations, hospital systems, pharmacy benefit managers, payers, and generic manufacturers, the same event looks entirely different.

Every expiring patent is a sourcing event. It is an advance notice that a drug costing, say, $400 per month will transition to a drug costing $40 per month, on a schedule that is largely knowable years in advance. The organizations that treat patent expiry data as strategic procurement intelligence consistently outperform those that wait for the manufacturer’s press release. The ones that ignore it pay brand prices for products where cheaper alternatives have already entered, or they scramble during shortage conditions that were entirely predictable.

This article is for practitioners: procurement directors at hospital networks, supply chain leads at pharmacy benefit managers, portfolio managers at generic manufacturers, and the analysts feeding them intelligence. The goal is to show exactly how patent data translates into sourcing decisions, why the translation is harder than it looks, and what tools and frameworks produce results.

One of the most useful data infrastructure assets in this space is DrugPatentWatch, which aggregates FDA Orange Book listings, Paragraph IV challenge filings, court dockets, regulatory exclusivity timelines, and ANDA pipeline data into a single queryable system. It is not the only resource, but for practitioners who need to map real entry dates rather than nominal expiry dates, it is a reference point worth understanding.

What ‘Patent Expiry’ Actually Means for a Sourcing Professional

Nominal expiry dates are not entry dates. Understanding the difference between the two is where most procurement errors originate.

The Legal Structure of Drug Exclusivity

A pharmaceutical product’s market exclusivity comes from two legally distinct systems that interact in ways most supply chain professionals never fully map. The first is patent law: the USPTO grants 20-year patents from the filing date, which translates to roughly 10 to 14 years of post-approval market protection after accounting for development time. The second is FDA regulatory exclusivity: a parallel system of statutory protections that run independently of patents.

Regulatory exclusivity periods include five-year new chemical entity (NCE) exclusivity for first-in-class small molecules, three-year clinical investigation exclusivity for new formulations, seven-year orphan drug exclusivity for treatments targeting rare diseases, and six months of pediatric exclusivity attached to existing patents when sponsors conduct FDA-requested pediatric studies [3]. These statutory protections can extend effective exclusivity well past a patent’s nominal expiry date, and they are tracked separately in the Orange Book.

For sourcing purposes, the effective date of generic entry is determined by whichever barrier falls last: the final expiring relevant patent or the final regulatory exclusivity period, compounded by the duration of any Paragraph IV patent litigation that has triggered the automatic 30-month FDA stay on approval. This is not theoretical complexity. It is the difference between modeling generic entry in 2026 versus 2028 for the same molecule.

Reading the Orange Book — and Its Limits

The FDA’s Orange Book, officially titled ‘Approved Drug Products with Therapeutic Equivalence Evaluations,’ lists the patents a brand company has submitted as covering each approved product. It is a starting point, not a complete picture. Brand manufacturers control what they list, and they have financial incentives to list every plausibly relevant patent to trigger 30-month stays when generics file Paragraph IV challenges.

The Orange Book also does not capture continuation patents, method-of-use patents tied to specific indications, or patents that are filed but not yet granted at the time an ANDA is submitted. A generic company targeting a molecule with an Orange Book expiry in 2026 may still face litigation on formulation patents running to 2030. Patent databases like the USPTO’s Public PAIR system, European Patent Office registers, and aggregated tools like DrugPatentWatch fill in the gaps the Orange Book leaves.

For biologics, the analogous resource is the Purple Book, which lists reference products and their exclusivity periods. Biosimilar entry follows the 351(k) pathway rather than the ANDA process, with a mandatory 12-year reference product exclusivity period from first approval before any biosimilar can launch, regardless of patent status [4]. This distinction matters enormously for the sourcing horizon on Keytruda, Stelara, Eliquis’s biologic equivalents, and the rest of the coming biosimilar wave.

The Paragraph IV Filing: The Real Signal

For procurement professionals, the most actionable single data point in the generic drug pipeline is not the patent expiry date. It is the Paragraph IV certification filing.

When a generic company files an ANDA with a Paragraph IV certification, it is formally declaring that one or more Orange Book-listed patents are invalid, unenforceable, or will not be infringed by the proposed generic product. This triggers two immediate consequences: the brand manufacturer typically has 45 days to file a patent infringement suit, and if it does, FDA approval of the generic is automatically stayed for 30 months [5].

The first company to file a substantially complete ANDA containing a Paragraph IV certification earns an incentive that Congress created under the Hatch-Waxman Act: 180 days of marketing exclusivity against all other ANDAs once it launches. For a drug with $1 billion in U.S. branded revenue, that 180-day window can generate $200 to $400 million in gross revenue for the first filer, depending on brand price retention and volume conversion [6]. This is why filing a Paragraph IV challenge is as much a financial decision as a scientific one.

For buyers, a Paragraph IV filing is an advance notice system. The moment a filer serves notice to the brand company, that information becomes discoverable. When multiple companies file on the same day, which happens regularly for high-value targets, they all share the 180-day exclusivity. When only one company files, it monopolizes the window. The difference determines whether a payer sees one generic entrant at 60% of brand price for six months, or six generic entrants within 30 days of launch driving prices to 15% of brand within a year.

‘When a small-molecule drug loses exclusivity, its revenue often drops by 80% to 90% within the first 12 months of multi-source generic entry. Price erosion below 95% of brand WAC occurs reliably once six or more generic competitors enter the market.’DrugPatentWatch, ‘Master the Patent Cliff for Better Pharmacy Margins,’ February 2026 [7]

The 2025–2030 Patent Cliff: A Molecule-by-Molecule Sourcing Calendar

Abstract figures about total revenue at risk are useful for headlines. What procurement teams need is a specific timeline by product, with expected entry dates, competition structure, and price trajectory.

Small Molecules: The Predictable Cliff

Small-molecule patent cliffs follow a well-documented pattern. A single generic entrant typically prices at 20% to 30% below brand within 30 days of launch. The price erosion accelerates sharply once three to five competitors are approved. By the time six or more generics are on the market, prices typically settle at 5% to 15% of the original brand WAC, effectively extinguishing brand revenues [7].

The table below summarizes the key small-molecule expiries and their expected sourcing implications.

Drug (Generic Name)

Brand Holder

2024 Revenue

Expected LOE

P-IV Status / Notes

Eliquis (apixaban)

BMS / Pfizer

~$13B

April 2028

Multiple generics approved (Mylan, Micro Labs); BMS secured court win extending exclusivity from initial 2026 date [8]

Januvia (sitagliptin)

Merck

~$4.7B

2026

Multiple ANDA filers; multi-source entry expected shortly after LOE

Fixed-dose combination; LOE already triggered; generic sourcing available [9]

Ozempic / Wegovy (semaglutide)

Novo Nordisk

~$26B combined

2031–2033 (U.S.)

Patent thicket and device patents likely to delay generic entry; compounding pharmacy dynamics already active

Eliquis is the most consequential single small-molecule sourcing event in the immediate planning window. BMS and Pfizer secured a critical court ruling in 2020 that pushed the effective LOE from an initial expectation of 2026 to April 2028 [8]. For hospital pharmacy procurement teams, this two-year delay cost billions in foregone savings across the payer landscape. It is exactly the kind of litigation outcome that a patent monitoring system flags in real time, while a procurement team relying on formulary updates learns about it from their PBM quarterly report.

Entresto: The Cliff That Already Fell

Novartis’s Entresto provides the most instructive recent case study in translating patent intelligence into sourcing action. The drug, a fixed-dose combination of sacubitril and valsartan for heart failure, generated $7.8 billion in 2024 revenue [9]. Market exclusivity ended in mid-2025. For any hospital system that had been tracking the Entresto patent portfolio and preparing procurement contracts in advance, the transition from brand to generic pricing represented immediate and significant budget relief.

The complication, which patent monitoring tools surface, is that Entresto is a fixed-dose combination of two agents with different patent landscapes. Sacubitril as a neprilysin inhibitor prodrug and valsartan as an angiotensin receptor blocker each have their own patent histories and regulatory data. A generic filer must demonstrate bioequivalence for the combination product, not just the individual components. That scientific complexity means fewer generic ANDA applicants at initial entry than a simple single-agent small molecule would attract, which in turn means slower price erosion in the first 12 to 18 months after LOE.

For sourcing professionals, this is the difference between expecting Lipitor-style immediate collapse and planning for a slower curve with fewer competitors at entry. The smart procurement approach: lock in contracts with the first two or three generic entrants at meaningful discounts to brand, accepting that you will not immediately reach the floor price you would get with a fully commoditized market.

Biosimilars: The Slope, Not the Cliff

For biologics, the same structural transition happens on a different timeline and with a different price curve. Innovator biologics typically lose only 30% to 70% of market share in the first year after biosimilar entry, compared to the 80% to 90% share loss small molecules experience. Multiple factors drive this: physician switching inertia, patient stabilization concerns, formulary contracting complexity, and the fact that most biosimilar approvals require separate prescriber actions rather than automatic pharmacy substitution [10].

The 2025–2030 wave of biologic expiries includes some of the most commercially significant molecules in history.

Stelara (ustekinumab, Johnson & Johnson) lost U.S. exclusivity in 2023. The biosimilar market opened with multiple entrants from companies including Amgen, Celltrion, and Teva. Hospital systems that contracted early for biosimilar ustekinumab achieved immediate savings, while those that waited faced formulary transition delays. The J&J experience here previews what Keytruda and Opdivo buyers will face post-2028.

Keytruda (pembrolizumab, Merck) is the single largest patent expiry event in pharmaceutical history. The IV formulation’s core composition-of-matter patent expires in 2028, putting more than $29 billion in annual revenue in play [11]. Biosimilar development programs are underway at Amgen, Samsung Bioepis, Bio-Thera Solutions, and several Indian manufacturers. For oncology procurement teams at integrated delivery networks, this is a five-year planning cycle item. The contracts you negotiate in 2027 for 2028–2030 biosimilar ustekinumab will determine whether your oncology pharmacy budget looks like a managed transition or a chaotic scramble.

Merck’s Subcutaneous Pivot: A Case Study in Evergreening

Merck’s response to the Keytruda cliff is the most technically aggressive evergreening strategy in modern pharmaceutical IP management. In September 2025, the FDA approved Keytruda Qlex, a subcutaneous formulation of pembrolizumab co-formulated with hyaluronidase [12]. The subcutaneous version carries independent patent protection on the formulation, delivery device, and administration method, creating an exclusivity extension well beyond the 2028 IV patent expiry.

The strategic play is straightforward: convert as many patients as possible to the subcutaneous formulation before 2028, so that when IV biosimilars enter, they face a converted patient population already on a product that carries its own separate protection. Analysts at I-MAK found that Merck has filed nearly 300 patents and holds over 100 granted patents on Keytruda, with method-of-treatment and manufacturing process claims that could extend some exclusivity into 2042 [13].

For procurement, this creates a specific challenge: even when IV biosimilar pembrolizumab enters in 2028, the clinical population may have shifted to subcutaneous Keytruda Qlex, which remains branded. The price savings on IV biosimilar pembrolizumab are real, but they only apply to patients who can be transitioned back or who were never converted. Formulary design in 2027 and 2028 should account for this dynamic explicitly.

The Anatomy of a Generic Drug’s Supply Chain

Procurement professionals who understand only the finished drug miss the two upstream failure points that actually cause shortages and price spikes: active pharmaceutical ingredient (API) supply and key starting material (KSM) geography.

From KSM to Finished Dose: The Three-Layer Structure

A generic drug reaches the pharmacy shelf through three production stages that are often geographically separated by thousands of miles and governed by three different sets of regulatory requirements.

The first stage is key starting material (KSM) and intermediate synthesis, which converts basic chemical feedstocks into the complex chemical precursors that an API manufacturer then transforms into the active drug substance. This stage is dominated by China. The second stage is API manufacture, converting those intermediates into pure, pharmaceutical-grade drug substance. India and China together control the overwhelming majority of this stage. The third stage is finished drug product manufacturing: tableting, encapsulation, fill-finish for injectables, or packaging, which happens more broadly across global geographics including in the U.S. and Europe.

The critical insight for sourcing professionals is that the supply concentration at stage one propagates upstream risk through seemingly diversified stage two suppliers. India sources approximately 70% of its pharmaceutical intermediates and KSMs from China [14]. A company that claims to have dual-sourced its API from both a Chinese and an Indian supplier has not diversified its supply chain. It has added a processing step between the same geographic risk and the pharmacy shelf.

API Sourcing Geography in 2025–2026

The U.S. Pharmacopeia’s Medicine Supply Map data for 2024 shows the U.S. accounting for just 22% of FDA-registered API manufacturing sites, India holding 21%, China holding 20%, and the European Union 19% [15]. That facility count understates actual volume dependency. China and India’s combined share of registered facilities translates to roughly 80% of actual production volume, reflecting their scale and specialization advantages relative to Western facilities.

In 2024, for the first time in more than two decades, China surpassed India in new Drug Master File (DMF) filings, capturing 45% of new API DMFs versus India’s declining share [15]. Chinese API manufacturing capacity has grown rapidly: from 134 new DMF filings in 2021 to 392 in 2024, almost a tripling over three years [15]. This concentration creates the supply chain vulnerability that U.S. policymakers have spent three years trying to address.

The 2024 Drug Shortage Context: In 2024, the U.S. recorded the highest number of active drug shortages since the American Society of Health-System Pharmacists began tracking the data in 2001. Shortages spanned central nervous system drugs, antimicrobials, hormone agents, injectable fluids, and chemotherapy drugs. The oncology shortage affecting cisplatin, carboplatin, and methotrexate forced oncologists to shift patients to more expensive alternatives: cisplatin use fell 15% while carboplatin use rose 40% and paclitaxel use rose 24% [16].

The BIOSECURE Act: What It Does, and What It Does Not Do

The BIOSECURE Act, passed by the U.S. House of Representatives and awaiting Senate action as of early 2026, prohibits firms receiving federal funds from working with five named Chinese biotechnology companies, including WuXi AppTec, effective January 1, 2032 [17]. A grandfather clause allows existing contracts with designated firms to continue until 2032.

For supply chain purposes, the distinction that matters most: the BIOSECURE Act targets the five named firms specifically, and it applies to federal procurement, not commercial pharmaceutical supply. It does not stop the current massive volume of Chinese API trade for generic drugs. The more immediate threat to API continuity is FDA enforcement. When a Chinese supplier receives an Import Alert for data integrity violations, its product is detained at the U.S. border immediately, creating instant supply disruption. FDA enforcement is a tactical, day-to-day risk; BIOSECURE is a long-term structural signal [21].

Despite this, surveys show a significant perception-action gap. By late 2024, 26% of life sciences companies expressed intent to shift away from Chinese manufacturing partners, but only 2% had taken concrete steps to unwind relationships [21]. The integration of Chinese manufacturers into the global pharmaceutical supply chain is so deep that rapid extraction is commercially impossible for most products without triggering the very shortages the policy is trying to prevent.

For procurement teams at payers and hospital networks, BIOSECURE’s most relevant implication is this: if you are sourcing generics that depend on API from BIOSECURE-named entities, or from the limited number of Chinese firms likely to face future regulatory action, your long-term supply is structurally at risk. PatentWatch data on API sourcing for specific molecules can help identify which of your current generic suppliers are most exposed.

India as an Alternative: The Real Dependency Picture

India is the world’s largest supplier of finished generic medicines, providing approximately 20% of global generic drug supply and serving about 40% of the U.S. generic drug market by prescription volume [18]. India’s FDA-registered manufacturing sites exceed 750, more than any other country [26]. When BIOSECURE chilled new business with Chinese CDMOs, Indian contract manufacturers saw a 50% jump in request-for-quotation volumes during 2024 [26].

The structural problem: Indian API manufacturers import approximately 70% of their bulk drug intermediates from China [14]. A sudden shift to Indian sourcing does not eliminate Chinese supply chain dependency; it adds a value-adding processing step on top of the same dependency. True supply chain diversification requires qualifying API sources whose KSM supply is not primarily Chinese, and in 2025, that means either European or U.S.-based KSM sourcing, both of which carry meaningful cost premiums.

A resilient supply chain design for a major generic product in 2025 should include at least two qualified API suppliers in geographically distinct regions, with at least one supplier outside China, and a strategic API inventory buffer of six to twelve months of commercial demand for any product where supply disruption risk is rated high [3]. That inventory buffer carries a real cost: holding cost, warehouse space, quality management for API stability, and the capital tied up in safety stock. Procurement teams need to model this total cost of resilience against the cost of shortage scenarios before making supplier selection decisions.

Pay-for-Delay, Patent Thickets, and the Mechanisms That Move the Entry Date

The single most dangerous assumption in pharmaceutical sourcing is that a patent’s nominal expiry date is the date generic drugs will be available for purchase. Three mechanisms routinely shift that date by months or years.

Reverse Payment Settlements: The Cork in the Bottle

A reverse payment settlement, commonly called ‘pay-for-delay,’ occurs when a brand manufacturer settles patent litigation with a generic challenger by compensating the generic company in exchange for an agreement to delay market entry until a negotiated date, typically at or near the patent’s expiry [19]. The settlement benefits both parties: the brand retains its monopoly longer; the generic gets compensated without the cost and risk of litigation. The loser is the payer, who continues paying brand prices for drugs where cheaper alternatives could have entered earlier.

The FTC has estimated that these anticompetitive settlements historically cost U.S. consumers and taxpayers approximately $3.5 billion annually in higher drug costs [19]. Independent research published in 2024 suggests the industry-wide harm is significantly larger, estimating total overcharges at roughly $12 billion, more than double the FTC’s 2010 figure adjusted for inflation [20].

The legal landscape shifted with the Supreme Court’s 2013 decision in FTC v. Actavis, which ruled that reverse payments are subject to antitrust scrutiny under a ‘rule of reason’ standard. Since Actavis, explicit cash reverse payments have declined. What has replaced them, per the FTC’s January 2025 report analyzing settlements from fiscal years 2018 through 2021, is increasingly complex settlement terms: quantity restrictions on generic sales volumes, supply agreements, co-promotion arrangements, and so-called implicit no-authorized-generic commitments that serve the same economic function [38].

For procurement professionals, the practical takeaway is this: when a highly anticipated generic’s market entry date is later than the patent’s nominal expiry would suggest, a settlement is a likely explanation. Monitoring Paragraph IV dockets through litigation tracking services and tools like DrugPatentWatch surfaces these settlement events early enough to adjust sourcing plans before budget cycles lock in brand drug spending assumptions.

Patent Thickets: When One Patent Is Just the Beginning

A patent thicket is a dense cluster of overlapping patents covering different aspects of the same pharmaceutical product: the molecule itself (composition of matter), its crystalline form, its formulation, its manufacturing process, its dosing regimen, its packaging, and its method of use for each individual approved indication. Each patent in the thicket is an additional litigation risk for a generic challenger, because a successful Paragraph IV challenge to the primary composition-of-matter patent does not invalidate the other patents. The generic must either challenge each relevant patent separately or design around it.

Keytruda is the most extreme current example. Merck holds over 100 granted patents on pembrolizumab and has filed nearly 300 patent applications in total, with method-of-treatment claims that could theoretically extend exclusivity on specific uses to 2042, fourteen years past the core composition patent’s 2028 expiry [13]. Even if biosimilar manufacturers succeed in invalidating the primary claims, individual indication patents could expose them to infringement suits on specific uses, creating a partial-market entry scenario where the biosimilar can be used for some indications but not others.

This matters for formulary design at oncology pharmacy operations. A pembrolizumab biosimilar entering in 2028 may be freely substitutable for first-line non-small cell lung cancer use but face litigation on its use in specific HER2-positive or MSI-H indications. Procurement contracts written for biosimilar pembrolizumab need to account for indication-specific access, which is a level of contract complexity most hospital pharmacy teams are not currently equipped for.

Pediatric Exclusivity: The Six-Month Bonus Round

Pediatric exclusivity adds six months to any existing patents and regulatory exclusivity periods when a sponsor completes FDA-requested pediatric studies under the Best Pharmaceuticals for Children Act [3]. This six-month extension attaches to all Orange Book-listed patents simultaneously, effectively delaying the entry date for any drug where the brand has completed pediatric studies. For a drug with $3 billion in annual sales, six months of extended exclusivity is worth approximately $1.5 billion. For procurement teams, it is a sourcing delay that is entirely knowable from FDA public records.

Authorized Generics: Competition That Undermines the First Filer

An authorized generic (AG) is a generic drug marketed by or on behalf of the brand company under the original NDA, which means it does not require its own ANDA approval. Brand manufacturers can launch AGs at any time, including during the 180-day exclusivity period that is supposed to reward the Paragraph IV first filer [11]. Because courts have ruled that the 180-day exclusivity only blocks other ANDA approvals, not products marketed under the original NDA, the AG can compete directly with the first-filer throughout the exclusivity window.

FTC data consistently shows that AG entry during the 180-day period reduces the first filer’s revenue by 40% to 52% compared to periods without AG competition [13]. For a drug with $1 billion in annual sales, the difference between a solo exclusivity and one contested by an AG can represent $75 million to $150 million in foregone revenue for the first filer.

For buyers, the AG is actually a favorable event: it means a second competitor in the market during the exclusivity window, which produces lower prices faster. Recent data shows that brand companies are less frequently exercising the AG option, in part because no-AG commitments have become standard elements of Paragraph IV settlement negotiations [13]. Understanding whether a specific LOE event will include an AG requires monitoring settlement agreements and brand company licensing disclosures.

Building a Patent-Informed Procurement Calendar

The following section is operational. It translates patent intelligence into process steps that a procurement organization can run on a repeatable schedule.

Step 1: Map Your Current Spend Against the Expiry Timeline

Start with your existing formulary or drug spend database and match every line item to its LOE timeline. This means going beyond the nominal patent date to the effective entry date, which requires accounting for Paragraph IV litigation status, pediatric exclusivity additions, regulatory exclusivity periods, and any known settlement events.

Tools like DrugPatentWatch allow you to pull this data at the molecule level, with granularity on each Orange Book-listed patent, its expiry date, and the active Paragraph IV certifications filed against it. The output of this step is a spend-weighted expiry calendar: your total drug spend organized by the year in which each product’s LOE occurs, updated quarterly as litigation outcomes shift the effective dates.

For a large hospital system, this exercise typically reveals that 15% to 25% of branded drug spend is within 24 months of a LOE event. That is the first-mover opportunity set, and it is almost always larger than procurement leadership expects before they run the analysis.

Step 2: Identify the Competition Structure at LOE

Knowing when a drug goes off-patent tells you when savings become available. Knowing how many competitors will enter tells you how deep those savings will go. The difference matters enormously.

A drug with one generic entrant at LOE is likely to see 20% to 30% price reduction. A drug with six generic entrants within 90 days of LOE is likely to see 70% to 90% price reduction. The competition structure at LOE is largely predictable 18 to 24 months in advance through ANDA pipeline monitoring: counting the approved ANDAs, the tentatively approved ANDAs, and the pending ANDAs with Paragraph IV certifications that are expected to be approved once litigation resolves.

DrugPatentWatch’s ANDA tracking function provides this pipeline view by product. The practical application: for drugs that will enter with limited competition (one to three entrants), negotiate supply contracts with the anticipated first filers before LOE, accepting a modest premium over the eventual multi-source floor in exchange for supply certainty and a defined entry price. For drugs with large ANDA pipelines (six or more entrants), wait for the competitive market to develop and use GPO contracting once prices have compressed to commoditized levels.

Step 3: Pre-Qualify API Suppliers Before Demand Peaks

This step is for organizations further upstream in the supply chain: generic manufacturers, specialty pharmacy operators, and procurement teams that engage directly with manufacturers rather than through distributors. It is also relevant for any hospital system or PBM with enough volume to consider direct manufacturer contracts.

The moment a high-value patent cliff event becomes certain (through final court rulings, settlement dates, or regulatory exclusivity expiry confirmations), demand for the relevant API surges among all the generic companies targeting that molecule. An API supplier that is comfortable running one dedicated production campaign per year suddenly faces requests for five. Lead times extend, and qualification backlogs develop.

Pre-qualifying alternative API suppliers before the demand peak requires: identifying suppliers with active Drug Master Files for the relevant molecule or a closely related one, understanding their KSM sourcing geography (not just their own facility location), auditing their cGMP compliance history including any FDA warning letters or import alerts, and negotiating supply agreements that reserve capacity at contracted pricing.

The regulatory reality: an API source change for a drug currently being manufactured triggers a Prior Approval Supplement under FDA’s SUPAC guidance, which requires demonstrating no adverse impact on quality, purity, stability, or performance. A BIO survey from February 2025 found that 80% of biotech firms need at least 12 months to find and qualify an alternative API supplier [24]. That 12-month minimum validation timeline means supply chain diversification decisions made in 2025 and 2026 determine supply resilience in 2027 and 2028.

Step 4: Structure Contracts to Capture Value Across the Price Erosion Curve

The price erosion trajectory for a newly generic drug follows a curve, not a cliff. Day-one generic pricing is rarely at the floor. A hospital network or PBM that waits for the absolute price floor gives up 12 to 24 months of significant savings in order to capture the final 10% to 20% of discount depth.

The procurement-optimal strategy for most high-volume LOE events: commit to a preferred supplier relationship with one or two of the anticipated early ANDA entrants in exchange for day-one supply at a meaningful discount to brand WAC (typically 25% to 40% below WAC at entry), with contractual price steps tied to market entrant milestones. As the fourth and fifth generic entrants receive FDA approval, the contract triggers a price reduction. As the sixth entrant launches, a second reduction. The brand is protected from the floor by the committed volume; the buyer captures value across the erosion curve rather than waiting for the floor.

For biosimilars, the contracting structure is more complex because hospital formulary committees and prescribers control the conversion rate in ways that do not apply to small-molecule generics (where pharmacists can substitute automatically in most states). Biosimilar contracts typically require a minimum market share conversion commitment from the hospital system in exchange for price certainty from the biosimilar manufacturer. Negotiating these contracts requires understanding interchangeability designations, which FDA grants separately from biosimilar approval and which permit automatic substitution at the pharmacy level without a new prescription.

Step 5: Monitor for LOE Date Shifts in Real Time

Patent litigation outcomes change effective entry dates. A generic company that was on track for a 2026 launch loses a trial court ruling in early 2025 and faces an appeal that pushes entry to 2028. A settlement agreement filed with the FTC in late 2025 delays another product by 18 months. The brand company files for a pediatric exclusivity extension that adds six months to a formulation patent nobody had flagged in the initial analysis.

Each of these events requires a corresponding adjustment to budget models, formulary planning, and supplier contracts. Organizations that rely on manual monitoring of court dockets and FDA databases will always be a quarter behind. Tools like DrugPatentWatch automate alert systems for these events, flagging Orange Book changes, new P-IV filings, trial court decisions, and settlement disclosures as they occur.

For organizations that allocate drug budget in annual planning cycles, the relevant question is: what is the confidence interval around your LOE date assumptions? A 12-month planning cycle that assumes a specific generic entry date for Eliquis at April 2028 is reasonable today. But if litigation produces a surprise ruling in late 2027 that pushes that date to mid-2028 or later, the budget impact is measured in hundreds of millions of dollars for a large payer. Building scenario ranges rather than point estimates into budget models, with quarterly refreshes from a patent monitoring feed, is the responsible planning approach.

Complex Generics and Biosimilars: Where the Real Supply Chain Complexity Lives

Not all generic entry events are created equal. Complex generics and biosimilars require supply chain preparation that starts years earlier, involves different regulatory pathways, and produces different competitive dynamics at launch.

What Makes a Generic ‘Complex’

The FDA classifies complex drug products as those where the route of administration, dosage form, or active ingredient makes the demonstration of bioequivalence scientifically challenging. This category includes locally acting drugs (like inhaled products and topical dermatologicals), drug-device combination products (like autoinjectors and metered-dose inhalers), and drugs with complex polymer structures or extended-release mechanisms [3].

From a sourcing standpoint, complex generics matter because they attract fewer ANDA filers than simple small molecules, produce shallower price erosion at LOE, and often require specialized manufacturing equipment that limits the supplier pool. A generic entrant for a dry-powder inhaler formulation needs inhalation-grade manufacturing capabilities that most generic tablet manufacturers do not have. The result: LOE events for complex generics often produce three to four competitors at best, and price erosion of 40% to 60% rather than 80% to 90%.

This changes the procurement calculus. For complex generics, the first-mover advantage of locking in early supplier relationships is more valuable than for commoditized small molecules, because the eventual floor price is higher and supply alternatives are fewer. Planning for complex generic sourcing should start 36 to 48 months before the expected LOE date.

The Biosimilar Market: Five Years In, and Still Developing

The U.S. biosimilar market launched in earnest with Zarxio (filgrastim-sndz, Sandoz) in 2015 and has matured significantly since, but it remains a market in transition. As of early 2026, the U.S. has approved more than 50 biosimilars across multiple therapeutic categories, with the largest cohort targeting Humira (adalimumab), which lost exclusivity in 2023 and attracted over a dozen biosimilar entrants [10].

The Humira biosimilar experience is instructive for planning the Keytruda and Opdivo transitions post-2028. Despite more than a dozen approved biosimilars for Humira, AbbVie retained significant market share well into 2024 and 2025 through an aggressive contracting strategy: offering deep rebates to PBMs and formulary managers in exchange for preferred status over biosimilars. This ‘rebate wall’ strategy means that the nominal entry of biosimilar competition does not automatically produce the price reduction the payer community expects [10].

For procurement organizations, the lesson from Humira: interchangeability designation, patient-level switching protocols, and formulary positioning are all required elements of a biosimilar transition plan, not optional add-ons. A biosimilar approval without formulary action to drive prescriber switching produces biosimilar market share in the low single digits, which does not generate meaningful savings for the payer or the hospital system.

Oncology Biosimilars: The 2028–2030 Opportunity

The next major wave of biosimilar entry will concentrate in oncology immunotherapy. The PD-1/PD-L1 inhibitor class, led by Keytruda and Opdivo (nivolumab, Bristol-Myers Squibb), represents the highest-value biologic patent cliff in pharmaceutical history. Combined, Keytruda and Opdivo generated approximately $38 billion in 2024 revenue, with Keytruda alone accounting for roughly $29.5 billion [11].

High-value cancer treatments are projected to create approximately $25 billion in generic and biosimilar market opportunities in oncology and immunology by 2029 [4]. For oncology pharmacy procurement teams at academic medical centers and integrated delivery networks, the 2026 to 2028 window is when supplier qualification, formulary planning, and prescriber transition protocols need to be built. The actual LOE events in 2028 are too late to start.

Biosimilar manufacturers currently in clinical development for pembrolizumab include Samsung Bioepis, Amgen, and Bio-Thera Solutions, among others. Each must complete a totality-of-evidence package demonstrating structural similarity, functional similarity, and clinical comparability across at least one indication before seeking FDA approval. This is a more demanding regulatory pathway than small-molecule ANDA bioequivalence, which is why the biosimilar pipeline for any given biologic is thinner than the ANDA pipeline for a comparable small molecule [42].

Applying Patent Intelligence Tools: What DrugPatentWatch Does and How It Fits Into a Procurement Workflow

Commercial patent intelligence platforms aggregate, normalize, and alert on the data that would otherwise require teams of attorneys and analysts to compile manually. This section describes what that intelligence looks like in practice.

From Raw Data to Actionable Signal

The FDA Orange Book is public and free. Court dockets through PACER are accessible for a small fee. USPTO patent records are searchable online. In theory, everything a procurement team needs is available in public sources. In practice, the volume and complexity of tracking hundreds of molecules across multiple patent databases, litigation dockets, regulatory exclusivity registries, and ANDA pipeline databases makes manual monitoring unworkable at scale.

DrugPatentWatch consolidates this data into a searchable platform that a procurement analyst can query by drug name, patent number, company, or therapeutic category. For a given molecule, the platform shows all Orange Book-listed patents with expiry dates, all active Paragraph IV certifications and the identity of the filers, the litigation status of each P-IV challenge, any known settlement events, the regulatory exclusivity periods active for the product, and the ANDA/biosimilar pipeline. It also integrates EU patent data, important because European LOE events often preview U.S. competitive dynamics [21].

The practical workflow for a procurement analyst: run a monthly query of upcoming LOE events in the 18- to 36-month window, flag any where the ANDA pipeline has changed since the last review (new filers, approvals, or settlement events), update the spend-weighted expiry calendar, and escalate contracts where the competitive picture has shifted enough to change the sourcing strategy. This is a two-to-four-hour monthly process with the right tooling, versus a full-time analyst job without it.

For biosimilar-specific procurement planning, interchangeability designations deserve a dedicated monitoring track. FDA grants interchangeable designation to biosimilars that have demonstrated through specific switching studies that alternating between the reference product and the biosimilar multiple times does not produce different results than staying on either product alone [3]. Interchangeable biosimilars can be substituted by pharmacists without prescriber intervention in states with substitution laws, which is the mechanism that drives automatic price competition similar to small-molecule generics.

As of early 2026, interchangeable designations have been granted for products in the insulin, adalimumab (Humira), and filgrastim categories, among others. The list is growing. For a hospital formulary committee, tracking which biosimilars in your therapeutic categories have achieved interchangeable designation determines which products can be substituted at the pharmacy level and which require prescriber outreach for each individual switch. DrugPatentWatch’s Purple Book integration provides real-time status on biosimilar approval and interchangeability designations across the biologics pipeline.

Using Patent Data to Anticipate Shortage Conditions

Patent intelligence is useful not only for identifying savings opportunities but also for anticipating shortage risks. A product with a single API supplier, manufactured at a facility with a recent FDA warning letter, facing LOE in 18 months will attract significant new demand from generic competitors qualifying new API sources. If the existing API supplier cannot scale fast enough, or if FDA enforcement creates an import alert that disrupts supply, a shortage develops.

The 2023 to 2024 cisplatin and carboplatin shortage followed exactly this logic: a small number of generic manufacturers had been producing the drugs on thin margins with a concentrated API supply base. When economic conditions caused some producers to exit, supply fell sharply, and the oncology community was left scrambling. A patent monitoring and supply chain intelligence approach would have flagged the concentration risk on these molecules years earlier.

For hospital systems that depend on specific chemotherapy agents or other high-dependency generics, mapping the API supplier concentration for those molecules is a risk management activity, not just a cost optimization exercise. The FDA’s Drug Shortage database, combined with API DMF data from DrugPatentWatch, provides the inputs for that analysis.

The Policy Layer: How Legislative and Regulatory Changes Shift the Sourcing Environment

Patent expiry timelines and supply chain geography do not exist in a policy vacuum. Legislative and regulatory changes in 2024 and 2025 have materially altered the environment for generic drug sourcing.

The Inflation Reduction Act and Drug Price Negotiation

The Inflation Reduction Act (IRA) established for the first time a mechanism for Medicare to negotiate prices directly with pharmaceutical manufacturers for certain high-spend drugs. The initial list of ten drugs subject to negotiation included Eliquis, Xarelto (rivaroxaban), Januvia, and seven others. Negotiated prices for these products take effect in 2026 for Medicare Part D enrollees [1].

The IRA creates a specific procurement dynamic for the patent cliff: drugs on the negotiation list that also face LOE within the negotiation period present a dual pricing event. Eliquis, for example, is subject to negotiated Medicare pricing starting in 2026 and faces generic entry in April 2028. For Medicare-covered populations, the negotiated price applies from 2026 to 2028, followed by the generic transition. For commercially insured populations, the negotiation does not apply directly, but the precedent and pricing signal influence what PBMs and hospital systems can negotiate with manufacturers.

The IRA also includes provisions that alter the patent cliff economics for low small-molecule generics differently than for high-price biologics. The legislation exempts small-molecule drugs from the negotiation list for four years after FDA approval but exempts biologics for 13 years, a difference that critics argue creates a structural incentive for manufacturers to develop biologic rather than small-molecule treatments, because biologics escape price negotiation pressure for longer [1].

Tariffs and the Cost Structure of Generic APIs

Section 301 tariffs, initiated in 2018, impose up to 25% duties on certain Chinese imports including pharmaceutical chemicals, APIs, raw materials, and intermediates [19]. The Trump administration’s second executive order in 2025, targeting pharmaceutical imports broadly, added additional uncertainty to the pricing environment for generic drugs that depend on Chinese API supply [1].

The immediate sourcing implication: generic drug manufacturers with heavy Chinese API exposure face cost inflation that their notoriously thin margins cannot absorb easily. Manufacturers will respond in one of three ways: pass costs to buyers through price increases (creating a reversal of the expected post-LOE savings), exit the market for the most cost-sensitive products (creating shortage risk), or accelerate supplier diversification to non-tariffed geographies (increasing API costs in the short term while building long-term resilience).

A December 2024 Chinese policy change compounds this: China removed a 13% export tax rebate for chemically modified oils and other pharmaceutical intermediates, permanently raising the cost structure of Chinese API exports [21]. Combined with tariff exposure, this has reset the landed cost of Chinese APIs for U.S. buyers upward in ways that are not temporary.

The BIOSECURE Act’s Chilling Effect on Future Sourcing

While the BIOSECURE Act has not yet been enacted into law as of mid-2026, its chilling effect on new business development with Chinese CDMOs is already measurable. Indian API manufacturers saw a 50% spike in request-for-quotation volumes and audit requests from U.S. and European buyers since Q3 2024 [26]. U.S. CDMOs report programs shifting from Chinese partners, though not yet at widespread scale. The five named Chinese firms in the BIOSECURE Act, including WuXi AppTec, have seen reduced inflows of new program business from U.S. biotechs.

For procurement teams at generic manufacturers and at the payer and hospital system level, the BIOSECURE Act is a planning horizon marker. If the Act passes in its current form, the 2032 effective date creates a seven-year window to diversify supply chains for products that currently rely on the named firms. Seven years is enough time to qualify alternative suppliers, complete the required FDA Prior Approval Supplements for API source changes, and build inventory buffers during the transition. Organizations that treat 2032 as a distant problem and wait to start planning will find themselves in 2029 unable to execute a three-year qualification timeline before the restriction takes effect.

Case Studies: Patent Cliff Sourcing Decisions That Created (or Destroyed) Value

Case Study 1: Humira and the Rebate Wall Trap

When Humira’s U.S. exclusivity ended in January 2023, the pharmaceutical industry widely anticipated a rapid market share shift to biosimilars. More than a dozen biosimilars had been approved and were ready to launch. By mid-2024, biosimilar adalimumab had captured only a small fraction of the market in the U.S. compared to European markets where Humira biosimilars had quickly gained 50% to 80% market share.

The explanation: AbbVie pre-emptively offered PBMs and pharmacy benefit managers extraordinarily deep rebates in exchange for preferred formulary positioning over biosimilars. The net price after rebates for branded Humira remained competitive with biosimilar list prices, and many PBMs found it financially rational to maintain Humira preferred status.

Procurement organizations that had built formulary transition plans assuming rapid biosimilar adoption faced a specific problem: they had committed to biosimilar contracts that assumed market share conversions their formulary positioning could not achieve, because the rebate economics of the brand made preferred biosimilar positioning financially suboptimal for many intermediaries.

The lesson: patent intelligence identifies when competition becomes possible. Contract intelligence and formulary analytics determine whether competition is actually economically superior for a given payer in a given market. Both are required. Tools like DrugPatentWatch provide the patent intelligence layer; rebate modeling and formulary analytics require separate capability.

Case Study 2: The Chemotherapy Shortage — Predictable, Not Predicted

The 2023 to 2024 shortage of cisplatin, carboplatin, and methotrexate was one of the most severe oncology supply crises in recent U.S. history. Cisplatin supply fell sharply when one manufacturer exited the market for economic reasons. The shortage began in February 2023 and did not resolve until June 2024 [16].

The proximate cause was well-understood: the generic chemotherapy market had become so price-compressed that margin economics made continued investment in manufacturing capacity unattractive. The number of manufacturers had fallen to levels where a single exit created critical shortage. But the conditions that produced this outcome were visible years before the crisis through generic market concentration data: products with fewer than four manufacturers, with API sourced from a small number of facilities, manufactured on thin margins without buffer stock, are structurally vulnerable.

Hospital pharmacy procurement teams that had identified cisplatin and carboplatin as shortage-risk products and maintained six to twelve months of safety stock did not face treatment delays. Those relying on just-in-time replenishment were forced to ration, substitute, or delay treatment. The patent intelligence layer that enables this kind of risk identification is the same API sourcing and market concentration data available through FDA databases and commercial aggregators.

Case Study 3: Eliquis — Monitoring Litigation to Avoid a Budget Error

When Bristol-Myers Squibb and Pfizer’s Eliquis (apixaban) initially faced generic competition expectations in 2026, payers and hospital systems began building budget models that assumed savings from generic apixaban starting that year. Multiple generic manufacturers had received FDA approval in 2019 and 2020: Mylan Pharmaceuticals and Micro Labs were among the early approved ANDAs [8].

Then BMS and Pfizer won a critical court ruling in August 2020 that extended their ability to block generic entry until 2026, and subsequent litigation outcomes shifted the final expected generic entry date to April 2028 [8]. Organizations that had budgeted for generic apixaban savings starting in 2026 faced a two-year gap in their financial models, having committed to plans and member-facing programs premised on a savings event that would not materialize for two additional years.

The organizations that tracked the Eliquis litigation through Paragraph IV docket monitoring tools were not surprised. The August 2020 ruling was visible to anyone monitoring the case. The implication for budget models was immediate and the adjustment was made in the quarter the ruling was issued. The organizations that relied on industry news coverage and formulary update cycles learned about the shift months later, after budget commitments had already been made.

Building the Internal Capability: What a Patent-Informed Procurement Function Looks Like

The Analyst Role: Where Patent Intelligence Meets Procurement

The gap between patent intelligence and procurement action in most organizations is an analyst role that does not currently exist at the right level. Patent attorneys understand IP law but not sourcing economics. Procurement analysts understand supplier contracts but not Paragraph IV mechanics. The organizations that convert patent cliff data into sourcing advantage most effectively have built a hybrid function: analysts with enough patent literacy to read Orange Book data and court outcomes, combined with enough commercial knowledge to translate that into contract strategy.

This does not require hiring patent attorneys into procurement. It requires training existing procurement analysts in pharmaceutical IP basics: how to read an Orange Book entry, what a Paragraph IV filing means, how the 30-month stay works, what the difference between composition-of-matter and method-of-use patents means for entry date certainty. A two-day training program combined with the right monitoring tools is sufficient to lift a competent procurement analyst to a useful level of patent intelligence fluency.

The Technology Stack: Minimum Viable Patent Intelligence

A pharmaceutical procurement function’s minimum patent intelligence capability requires four components. The first is an Orange Book and Purple Book monitoring system, either through a commercial aggregator like DrugPatentWatch or a manual quarterly review of FDA database updates, which handles the core U.S. exclusivity data. The second is a Paragraph IV litigation tracker, monitoring court dockets for the molecules in the priority spend portfolio. The third is an ANDA and biosimilar pipeline tracker, showing which products are tentatively approved, pending approval, or in active challenge status for each target molecule. The fourth is an API supply chain mapping tool, identifying the API manufacturer and KSM sourcing geography for each generic product in the formulary, to surface concentration risk before it becomes a shortage event.

Commercial platforms like DrugPatentWatch, PatSnap, and Citeline provide various combinations of these capabilities. The decision about which to license versus which to replicate internally with free data sources depends on the scale of the procurement function and the volume of patent cliff events in the planning window. For a payer covering millions of lives with drug spend in the billions, the cost of a comprehensive commercial platform is trivial relative to the budget at risk.

Governance: Making Patent Intelligence a Budget Planning Input

The most common failure mode in patent-informed procurement is not a lack of data. It is a governance failure: patent intelligence that gets produced but does not reach budget planning cycles in time to influence decisions. A monitoring function that updates LOE calendars in August but feeds into a budget cycle that closes in September will produce useful analysis that arrives too late to change anything.

The solution is a quarterly patent intelligence review that is a formal input to drug budget planning, with defined protocols for how LOE date changes trigger contract reviews, formulary planning adjustments, and budget model updates. The review should have attendance from pharmacy leadership, procurement, finance, and (for payers) the actuarial team that uses drug cost assumptions to set premiums. When a Paragraph IV settlement shifts an expected entry date by 18 months, that information should flow to each of those functions within 30 days, not at the next annual planning cycle.

The Biosimilar Naming and Substitution Rules: A Sourcing Wrinkle That Matters

FDA policy on biosimilar naming and substitution creates a procurement complexity that has no direct analog in the small-molecule generic world. Each biosimilar receives a four-letter suffix appended to the nonproprietary name, distinguishing it from the reference product and from other biosimilars of the same reference. The intent is pharmacovigilance: adverse event reporting can distinguish between products. The practical effect is that prescriptions written for the reference product name do not automatically trigger biosimilar substitution in the way that a branded small-molecule drug triggers generic substitution.

For interchangeable biosimilars, state-level substitution laws govern whether pharmacists can substitute without prescriber intervention. As of 2025, most U.S. states have enacted biosimilar substitution laws, but their specific requirements for prescriber notification, patient consent, and recordkeeping vary [3]. A hospital system operating in multiple states needs a state-specific formulary and substitution protocol for each biosimilar in its formulary, not a single national policy.

This regulatory complexity is one reason biosimilar market share in the U.S. lags behind European biosimilar adoption rates significantly. In EU tender markets, biosimilar adoption frequently reaches 80% to 90% of market share within the first year after LOE. U.S. adoption curves for the same molecules run 30% to 50% market share over the same period, reflecting the additional administrative friction of the substitution process and the competing influence of brand rebate strategies [10].

For procurement, understanding state-specific substitution law is not optional for biosimilar contracting. The contract commitment to a biosimilar manufacturer that includes a market share conversion guarantee must account for the actual achievable conversion rate under the applicable substitution laws, not the theoretical maximum. Overstating conversion potential in biosimilar contracts creates financial exposure when actual share falls short of committed minimums.

Specialty Pharmacy and the Direct Procurement Model

When to Contract Directly Versus Through a GPO

Group Purchasing Organizations (GPOs) aggregate purchasing volume across member institutions to negotiate pricing from manufacturers and distributors. For fully commoditized generic drugs, with six or more manufacturers, stable supply, and well-established pricing, GPO contracts often provide adequate pricing without the complexity of direct manufacturer agreements. The GPO model works because the drug’s competitive market is already doing the work of price compression, and the GPO is simply capturing and passing through that market price.

For early-LOE generic products, before the market is fully commoditized, and for complex generics and biosimilars where supply concentration is high, direct manufacturer contracting produces meaningfully better outcomes than GPO reliance. The reason: a GPO contract for a drug with two generic entrants is typically negotiated against list price, with limited insight into the supply constraint dynamics at each manufacturer. A direct contract with the anticipated first filer, negotiated 12 to 18 months before LOE, can produce better pricing in exchange for volume commitment and can include supply guarantees that a GPO agreement typically does not.

For large hospital systems, integrated delivery networks, and large PBMs, the question of GPO versus direct contracting for each upcoming LOE event should be an explicit annual analysis, not a default. The analysis inputs are: expected number of competitors at entry, expected price erosion curve, supply constraint risk at the API level, and the incremental administrative cost of a direct contract versus GPO enrollment. For any LOE event with fewer than three expected competitors and annual spend above $5 million, direct contracting typically wins the analysis.

Specialty Drug LOE and the 340B Program

The 340B drug pricing program, which requires pharmaceutical manufacturers to provide outpatient drugs to qualified health centers and covered hospitals at significantly reduced prices, intersects with the patent cliff in a specific way. When a specialty drug’s LOE produces a generic, 340B-covered hospitals must decide whether to transition their formularies to generic products or continue utilizing 340B brand pricing for the populations they serve.

The 340B discount on many high-cost biologics and specialty drugs is significant, but generic pricing at multi-source LOE often falls below even the 340B price. For covered entities, the patent cliff creates a periodic re-evaluation of whether the 340B program’s value for a specific drug exceeds the value of open-market generic competition. For drugs with high 340B participation (like many oncology and HIV treatments), the LOE event is both a formulary transition planning item and a 340B program utilization review.

Practical Intelligence: Ten Things Procurement Teams Get Wrong About Patent Expiry

Across the common errors observed in pharmaceutical procurement practice, ten recur most frequently. Each maps to a correctable knowledge or process gap.

First: treating the nominal patent expiry date as the entry date. It is not. The effective entry date accounts for regulatory exclusivity, pediatric extensions, litigation stay periods, and settlement terms. For half the products on a typical LOE calendar, the effective entry date is later than the nominal expiry date.

Second: assuming all generic entries produce the same price impact. A single-filer LOE event and a six-filer LOE event have dramatically different price trajectories. Competition structure determines savings depth.

Third: overlooking the regulatory exclusivity layer. Many procurement teams monitor patent data but not Orange Book regulatory exclusivity periods, which are listed separately and can extend effective exclusivity well past the last patent’s expiry.

Fourth: treating a biosimilar approval as equivalent to a small-molecule generic approval in terms of prescriber switching dynamics. Biosimilar market penetration requires active formulary management; it does not happen automatically from approval.

Fifth: ignoring API sourcing geography when evaluating generic supplier reliability. A supplier that sources its API from a facility with a recent FDA warning letter is a supply risk regardless of what its finished product price is.

Sixth: waiting for a generic to launch before starting supplier evaluation. By launch date, all the first-mover advantage has been captured by competitors. Supplier evaluation should begin 18 to 24 months before expected LOE.

Seventh: accepting GPO default pricing for all LOE events without analyzing whether direct contracting would produce better outcomes on early-competition drugs.

Eighth: failing to adjust budget models when litigation shifts an LOE date. A two-year shift in a $500 million annual spend drug’s LOE timeline represents hundreds of millions of dollars in foregone or accelerated savings. That warrants a budget model revision within weeks of the ruling, not at the next annual cycle.

Ninth: assuming pay-for-delay settlements are ancient history. The FTC’s January 2025 report found that complex settlement terms including quantity restrictions and implicit no-AG commitments remain prevalent and continue to delay generic entry [38]. This practice has not ended; it has evolved.

Tenth: underestimating the administrative complexity of biosimilar substitution at the formulary and state law level. Biosimilar contracting requires a state-specific substitution analysis before committing to market share conversion targets.

Looking Forward: The 2026–2033 Supply Chain Opportunity Map

The Near-Term Priority List

For procurement organizations building their sourcing calendars today, the near-term priority events by expected LOE and anticipated value are as follows. Januvia (sitagliptin, Merck) and related DPP-4 inhibitors are entering multi-source generic competition in 2026, with a large ANDA pipeline. Ibrance (palbociclib, Pfizer) faces LOE in 2027 with significant oncology spend implications. Eliquis (apixaban) enters generic competition in April 2028, representing the largest single small-molecule LOE event in the current planning window. Opdivo (nivolumab, Bristol-Myers Squibb) faces biosimilar entry challenges beginning around 2028, with its composition-of-matter patents running concurrent to Keytruda’s [47]. Keytruda (pembrolizumab, Merck) presents the most complex planning challenge, combining the largest revenue at risk of any single biologic LOE with the most aggressive evergreening strategy in current IP management practice.

GLP-1s: The Patent Cliff That Is Not (Yet) a Cliff

Ozempic and Wegovy (semaglutide, Novo Nordisk) generated a combined $26 billion in revenue in 2024 [6]. U.S. patent protection for semaglutide’s core composition of matter extends into the early 2030s, and Novo Nordisk has been actively building a secondary patent estate around formulation, device, and dosing-regimen claims.

The GLP-1 category’s LOE events will not produce meaningful sourcing opportunities in the 2025 to 2027 window covered by most current procurement planning cycles. However, compounding pharmacy dynamics have already created an informal parallel market for semaglutide during periods of shortage designation, a situation that revealed significant demand for lower-cost access and previewed what the market will look like when generic entry actually occurs in the early 2030s.

For procurement teams with a longer planning horizon, the GLP-1 LOE event is worth modeling now because the savings magnitude is potentially larger than any previous generic transition. A drug class generating $50 to $100 billion in combined annual sales by 2030 (likely, given current growth trajectories) transitioning to generic pricing would represent the largest single cost reduction event in pharmaceutical sourcing history. The organizations that are prepared with supplier relationships, formulary transition protocols, and contract structures will capture that value; the ones that wait for the press release will scramble.

The Oncology Pipeline’s Next Wave

Behind Keytruda and Opdivo, the oncology pipeline includes a second generation of targeted therapies whose patents will begin expiring in the early to mid-2030s: CDK4/6 inhibitors like Ibrance and Kisqali, PARP inhibitors like Lynparza, and ADC therapies whose patent structures are only beginning to be understood by generic challengers. The oncology sector has the fastest-growing generic opportunity, with a projected growth rate of 9.21% per year until 2030 driven by cancer drug patent expirations [4].

For procurement planning, oncology generics and biosimilars require the earliest planning lead times because of the complexity of the regulatory pathway, the high clinical stakes of formulary transitions for oncology patients, the deep brand relationships between oncologists and manufacturer medical science liaisons, and the managed care contracting complexity of oncology drug coverage. A 36-month planning lead time for oncology LOE events, versus the 18 to 24 months adequate for primary care drug transitions, is a reasonable minimum.

Key Takeaways

The following points summarize the core actionable conclusions from this analysis:

1. The 2025–2030 patent cliff is the largest in history, covering an estimated $300 billion in branded drug revenue across roughly 200 drugs. For procurement organizations, this is a once-in-a-generation sourcing opportunity that requires advance preparation, not reactive response.

2. Nominal patent expiry dates are not entry dates. Regulatory exclusivity, Paragraph IV litigation stays, pediatric extensions, and settlement agreements all shift effective generic entry. The organizations that plan around effective entry dates rather than nominal expiry dates make far fewer budget errors.

3. Competition structure at LOE determines savings depth. A single-entrant LOE produces 20% to 30% savings; a six-entrant LOE produces 80% to 90% savings. Knowing the ANDA pipeline 18 to 24 months in advance determines whether you should pre-negotiate with first filers or wait for the commodity market to develop.

4. API supply chain geography is a strategic variable, not a procurement detail. India sources approximately 70% of its pharmaceutical intermediates from China. True supply chain diversification requires qualifying suppliers with non-Chinese KSM sourcing, which takes 12 to 24 months to execute from the decision point.

5. Biosimilar transitions require active formulary management. Unlike small-molecule generics, biosimilars do not automatically capture prescriber market share at approval. Interchangeability designation, state-specific substitution law compliance, and formulary positioning decisions all determine actual savings, not just the approval date.

6. Patent intelligence tools like DrugPatentWatch convert publicly available data into actionable procurement signals. The raw data exists in FDA databases and court dockets; the value of commercial platforms is aggregation, normalization, and real-time alerting that makes the intelligence usable at procurement scale.

7. Pay-for-delay has not disappeared; it has evolved. FTC reports confirm that complex settlement terms including quantity restrictions and implicit no-AG agreements continue to delay generic entry. Monitoring settlement disclosures is a standard part of LOE date validation.

8. The 2026 to 2028 window before BIOSECURE restrictions take effect is the most critical period for API supply chain risk assessment. Organizations that have not mapped their KSM-to-finished-product supply chains at a granular level cannot act on source diversification before the window closes.

Frequently Asked Questions

Q1: How far in advance should a hospital system or payer begin preparing for a specific drug’s LOE event?

For standard small-molecule generics with a well-populated ANDA pipeline, 18 to 24 months before expected LOE is sufficient to build a supplier evaluation, pre-qualify vendors, and structure GPO versus direct contract decisions. For complex generics, biosimilars, or drugs where the patent landscape involves active litigation, 36 months is the appropriate lead time. For oncology biosimilars specifically, 48 months allows for the full cycle of formulary committee review, prescriber communication planning, and interchangeability designation monitoring that these transitions require. The practical test: if you cannot specify today which suppliers you intend to use for the three most valuable LOE events in your drug budget in the next 36 months, you are behind schedule.

Q2: What is the single most common reason generic drug savings fail to materialize after a patent expiry?

For small-molecule generics, the most common failure is a litigation outcome that shifts the LOE date later than the original estimate, with no corresponding update to budget models. For biosimilars, the most common failure is an assumption that FDA approval of a biosimilar automatically produces rapid market share conversion when, in practice, brand rebate strategies, formulary positioning decisions, and prescriber inertia all intervene. The two problems have different solutions: patent litigation monitoring fixes the small-molecule failure; formulary strategy and prescriber engagement programs fix the biosimilar failure.

Q3: How should procurement teams think about the difference between a drug’s ‘patent expiry’ and its ‘loss of exclusivity’ date?

Patent expiry refers to the end date of one or more specific USPTO-granted patents listed in the FDA’s Orange Book. Loss of exclusivity (LOE) is the effective date on which the combination of all relevant patent protections and all regulatory exclusivity periods has ended, and a generic can legally enter the market. A drug can have its primary composition-of-matter patent expire in Year 1 but remain effectively protected until Year 3 because of a pediatric exclusivity extension that attaches to all remaining patents. The LOE date, not the patent expiry date, is the number that belongs in sourcing calendars. Services like DrugPatentWatch calculate and track LOE dates by accounting for all overlapping protections, which is why they are more useful than a simple Orange Book patent lookup for procurement planning.

Q4: Is a Paragraph IV challenge always a reliable signal that generic entry is imminent?

A Paragraph IV filing signals that at least one generic manufacturer believes the Orange Book-listed patents are invalid or will not be infringed, and has invested in the development and regulatory work required to file an ANDA. It is not a guarantee of imminent entry. The brand company has 45 days to file an infringement suit, which triggers a 30-month FDA approval stay. The litigation that follows can take one to three additional years to reach final resolution. A Paragraph IV filing on a high-value drug typically precedes actual generic availability by three to five years in contested cases. What a P-IV filing does signal reliably is that a manufacturer has made a significant commercial bet on the molecule, which narrows the uncertainty around eventual LOE. Multiple P-IV filings from different companies on the same day is the stronger signal: when five or six companies all file on the same date, the competitive pressure for a resolution that clears the path to entry increases significantly, and the LOE date uncertainty narrows.

Q5: What specific data points from patent and regulatory databases produce the highest ROI in a pharmaceutical procurement workflow?

Four data points produce disproportionate value. First: the ‘first potential entry date’ for each ANDA in a product’s pipeline (the date on which a generic could first legally launch), which is derived from combining the litigation 30-month stay end date with any regulatory exclusivity remaining. This is the single most action-forcing number for contract timing decisions. Second: the count of approved and tentatively approved ANDAs for each product at LOE, which predicts competition structure and price erosion depth. Third: any API Drug Master File (DMF) changes for the active ingredient of a product in your formulary, which can signal a new generic entrant is qualifying a source, or an existing supplier exiting. Fourth: FTC settlement filings under the Medicare Modernization Act, which disclose pay-for-delay arrangements and shift the LOE date for affected products. These four data streams, monitored on a quarterly basis, cover the majority of material LOE date and competition structure changes that would otherwise surprise a procurement organization.

References

DrugPatentWatch. (2026, February 25). Beyond the drug patent cliff: How procurement can drive immediate savings with generics and biosimilars. DrugPatentWatch. https://www.drugpatentwatch.com/blog/beyond-the-drug-patent-cliff-how-procurement-can-drive-immediate-savings-with-generics-and-biosimilars/

DeepCeutix. (2026, February 2). $300 billion in pharma revenue loses patent protection by 2030. DeepCeutix Strategic Briefings. https://deepceutix.com/insights/patent-cliff-reformulation

DrugPatentWatch. (2026, March 24). The regulatory pathway for generic drugs: A strategic guide to market entry and competitive advantage. DrugPatentWatch. https://www.drugpatentwatch.com/blog/the-regulatory-pathway-for-generic-drugs-explained/

Credevo. (2026, March 5). Trending molecules and generic drug opportunities: Blockbuster drugs with upcoming patent expirations (2026–2030). Credevo. https://credevo.com/articles/2026/03/05/trending-molecules-and-generic-drug-opportunities-blockbuster-drugs-with-upcoming-patent-expirations-2026-2030/

Association for Accessible Medicines. (2022, June 8). The Hatch-Waxman 180-day exclusivity incentive accelerates patient access to first generics. Association for Accessible Medicines. https://accessiblemeds.org/resources/fact-sheets/the-hatch-waxman-180-day-exclusivity-incentive-accelerates-patient-access-to-first-generics/

DrugPatentWatch. (2024, November 19). Generic drug partnerships: The complete playbook for biosimilars, CDMOs, and the $200B patent cliff. DrugPatentWatch. https://www.drugpatentwatch.com/blog/the-future-of-partnerships-in-generic-drug-development/

DrugPatentWatch. (2026, February 5). Master the patent cliff for better pharmacy margins. DrugPatentWatch. https://www.drugpatentwatch.com/blog/master-the-patent-cliff-for-better-pharmacy-margins/

BioSpace. (2025, February 19). 5 pharma powerhouses facing massive patent cliffs—And what they’re doing about it. BioSpace. https://www.biospace.com/business/5-pharma-powerhouses-facing-massive-patent-cliffs-and-what-theyre-doing-about-it

DrugPatentWatch. (2026, March 10). The patent cliff playbook: Pharmaceutical IP valuation, generic entry timing, and biosimilar strategy. DrugPatentWatch. https://www.drugpatentwatch.com/blog/patent-expirations-seizing-opportunities-in-the-generic-drug-market/

Global Pricing Innovations. (2025, November 4). Patent cliff in pharma: Navigating disruption and creating opportunity. Global Pricing Innovations. https://globalpricing.com/patent-cliff-in-pharma-navigating-disruption-and-creating-opportunity/

DrugPatentWatch. (n.d.). KEYTRUDA (pembrolizumab) patent and exclusivity data. DrugPatentWatch. https://www.drugpatentwatch.com/p/biologics/tradename/KEYTRUDA

BioSpace. (2025, September 22). As exclusivity loss looms, Merck wins subcutaneous approval for Keytruda. BioSpace. https://www.biospace.com/fda/as-exclusivity-loss-looms-merck-wins-subcutaneous-approval-for-keytruda