Every supply chain director in pharmaceuticals knows the standard risks: a manufacturer fails a GMP audit in Hyderabad, a hurricane shuts a Puerto Rican plant, a ship runs aground in the Suez Canal. These events get war-room treatment. Yet the most predictable disruption in the industry — the one with a publicly known countdown clock, a federal database tracking it in real time, and decades of case-study data — rarely gets more than a quarterly slide in a supply review meeting.

That disruption is patent expiry. And the intelligence that anticipates it most precisely is drug patent data.

Between 2025 and 2030, industry analysts project that nearly 70 high-revenue products will lose market exclusivity, putting roughly $236 billion in annual branded revenue at risk [1]. Drugs like Keytruda, Eliquis, and Opdivo cluster in a narrow 2026–2028 window. That cliff doesn’t just threaten branded manufacturers — it reshapes the entire supply architecture for APIs, excipients, packaging, and cold-chain logistics for everyone downstream.

Yet most pharmaceutical supply chain teams treat patent data as an IP department problem. They plan inventory based on historical demand signals and manufacturer capacity, not on the legal calendar that governs when and how that demand will shift. The result is a predictable pattern of over-stocked branded APIs, under-prepared generic supply chains, and emergency sourcing that costs multiples of what proactive planning would have required.

This article explains how to close that gap — using patent intelligence not as a legal tool but as a supply chain forecasting input. The operational implications are concrete, the data is largely public, and the organizations already doing this systematically hold a durable advantage over those that aren’t.

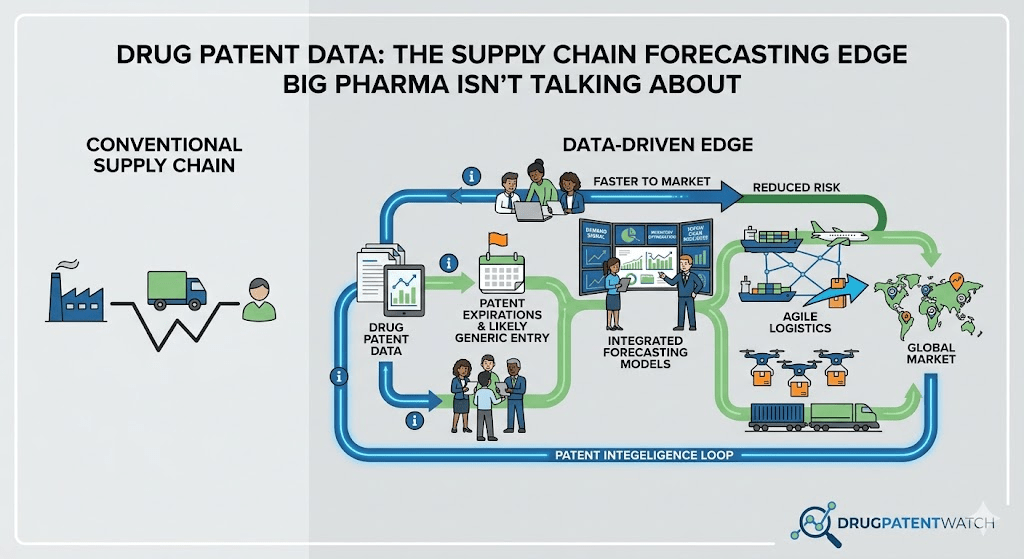

Why Supply Chain Teams Systematically Ignore Patent Data

The disconnect between IP intelligence and supply chain planning isn’t accidental. It reflects organizational structure. In most large pharmaceutical companies and GPOs, patent monitoring sits inside legal or business development. Supply chain planning sits inside operations. The two groups report to different executives, use different software, and meet in different rooms.

That silo creates concrete operational problems. A supply chain planner running a 24-month demand model for a branded API has no automatic feed from the patent database tracking whether that API’s exclusivity will hold, get challenged by a Paragraph IV filer, or evaporate in a court settlement. The planner sees historical sales velocity. She doesn’t see the Orange Book filing that signals six generic manufacturers are already queued behind a 30-month stay.

On the generic side, the problem inverts. A procurement team building inventory for a generic product launch needs to time API orders against legal risk — not just regulatory risk. If a brand company’s Paragraph IV lawsuit is likely to succeed, the launch date shifts by years. If a settlement is likely, it may contain a specific launch date or a volume-based trigger. Neither piece of intelligence shows up in an ERP system that only tracks purchase orders and lead times.

The cost of this blindness is measurable. Supply chain delays, in the pharmaceutical context, consistently cost more than the carrying cost of safety stock that anticipated the disruption [2]. A six-month safety stock position on a commodity API purchased before patent expiry creates options. An emergency spot purchase of that same API after a supply shock — when every generic manufacturer simultaneously enters the market and API demand spikes — eliminates margin entirely.

The organizations closing this gap share one practice: they treat patent data as a first-class input to demand planning, not an afterthought.

The Architecture of a Drug Patent: What Supply Chain Teams Actually Need to Know

Patent law is complex. The supply chain implications of patent law are not. What a planner needs to understand is a simplified but accurate model of the IP protection stack — and specifically, where that stack is vulnerable to compression or extension.

Composition of Matter Patents vs. Formulation Patents

Every drug’s IP protection begins with a composition of matter (CoM) patent, which covers the active molecule itself. CoM patents are the strongest and the most valuable. When one expires, generic entry becomes legally possible at the molecular level. For supply chain purposes, the CoM expiry is the primary clock to track.

But pharma companies don’t rely on a single patent. They build what patent analysts call “thickets” — clusters of secondary patents on formulations, delivery mechanisms, dosing regimens, and manufacturing processes. These secondary patents can extend practical market exclusivity years beyond the CoM date, and they’re the primary target of Paragraph IV challenges.

For a supply chain planner, the key question isn’t just “when does the CoM expire?” It’s: “What is the probability that the secondary patent thicket holds, and for how long?” That probability question requires patent-level data, not just a summary date.

The Orange Book and What It Tells You

The FDA’s Orange Book is the official list of approved drug products with therapeutic equivalence evaluations. For supply chain intelligence purposes, it does two things. First, it lists every patent protecting each approved product, with expiry dates. Second, it shows every Paragraph IV challenge filed against those patents, which tells you exactly which products generic manufacturers are pursuing and how aggressively.

A product with ten Orange Book-listed patents and no Paragraph IV certifications is protected, practically speaking, until the last patent expires — assuming litigation doesn’t overturn it. A product with the same ten patents but five active Paragraph IV challenges is in a different situation entirely: the effective exclusivity date is subject to litigation outcomes and settlement timelines, not just patent calendars.

Platforms like DrugPatentWatch aggregate and structure this Orange Book data alongside litigation histories, court decisions, FDA exclusivity records, and ANDA filing data, making it accessible to analysts who aren’t patent attorneys. For supply chain teams specifically, this kind of structured intelligence transforms a legal database into a demand signal.

Market Exclusivity: The FDA Layer That Sits On Top of Patents

Separate from patent protection, the FDA grants periods of market exclusivity that prevent generic approval regardless of patent status. New Chemical Entity (NCE) exclusivity runs five years from approval. New clinical investigation exclusivity runs three years. Orphan drug exclusivity runs seven years. Pediatric exclusivity tacks on six months to existing patents.

These exclusivities create the Hatch-Waxman Act’s layered protection system — the framework under which pharmaceutical patent prosecution intersects with FDA clinical timelines that take 8–12 years [3]. A supply chain team that knows only patent expiry dates misses the FDA exclusivity layer. A team that tracks both has a complete picture of when generic approval is legally possible.

Paragraph IV Litigation: The Supply Chain Signal Hidden in Plain Sight

Of all the patent intelligence signals available to supply chain planners, Paragraph IV certifications are the most operationally useful — and the most systematically ignored outside legal circles.

When a generic manufacturer files an Abbreviated New Drug Application (ANDA) and certifies that an Orange Book-listed patent is invalid, unenforceable, or will not be infringed — known as a Paragraph IV certification — it sets in motion a specific legal and commercial sequence. The brand company has 45 days to sue for patent infringement. If it sues within that window, the FDA is automatically prohibited from approving the generic for up to 30 months, unless the court rules before that clock expires [4].

For supply chain teams, this sequence is a forecast generator. A Paragraph IV filing tells you that at least one generic manufacturer has done enough development work to file an ANDA. It tells you the company believes the relevant patents are beatable. And it starts a legal clock that, with reasonable probability assessment, gives you a window for when generic supply will enter the market.

“Between 2025 and 2030, industry analysts project that nearly 70 high-revenue products will lose market exclusivity, placing a colossal $236 billion in annual branded revenue at risk — and creating an equally large API demand shock for generic manufacturers trying to meet that opportunity.”DrugPatentWatch, “The Patent Cliff Protocol: Advanced Methodologies for Forecasting Generic Drug Launches and Market Erosion,” December 2025 [1]

The 30-Month Stay as a Planning Horizon

The 30-month stay is not just a legal mechanism. It’s a supply chain planning horizon. If a Paragraph IV challenge is filed today and the brand sues within 45 days, the earliest possible generic approval — absent a court ruling — is 30 months from now. That window tells a generic manufacturer’s supply chain team exactly when to start API procurement, equipment qualification, and commercial batch manufacturing.

It also tells a branded manufacturer’s supply chain team when to start modeling revenue erosion scenarios. And it tells hospital formulary managers and GPO procurement teams when to start evaluating supplier alternatives.

The practical complication is that Paragraph IV litigation increasingly ends in settlement [5]. Settlements often include specific launch dates — called “authorized generic” launch dates or “launch-at-risk” provisions — that differ from both the 30-month stay expiry and the underlying patent expiry. Those settlement dates are often not public at the time they’re negotiated, creating genuine uncertainty. But the existence of a settlement is usually disclosed, and platforms that track litigation outcomes can narrow the range of probable launch dates substantially.

First-Filer Exclusivity and the API Timing Problem

This creates an API sourcing race that most planners don’t see until it’s already underway. The first-filer generic manufacturer typically begins API qualification and inventory building 18–24 months before anticipated launch — which means they’re creating demand on a set of API suppliers before the product’s legal status is fully resolved. Second-wave generic entrants then arrive at those same suppliers after the 180-day window closes, facing tighter capacity and higher spot prices.

Supply chain teams that monitor Paragraph IV filings can identify this demand surge well in advance. They know which APIs are likely to see a demand inflection and when — before the competition starts bidding up capacity.

The Patent Cliff Is Not One Event: It’s a Cascade

The phrase “patent cliff” implies a sudden drop. The reality is a cascade of interconnected events spread across months or years, each with distinct supply chain implications. Understanding the sequence — not just the calendar date — is what separates actionable forecasting from headline reading.

Phase 1: Patent Expiry and the First Generic Approvals

The initial expiry of the primary CoM patent is the event that gets media coverage. It’s also the least operationally useful signal for supply chain planning, because by the time a CoM expires, well-informed competitors have been planning for it for years. The useful signal comes earlier: when Paragraph IV filings appear, when ANDA counts grow, and when litigation outcomes start favoring generic challengers.

At expiry, the FDA can approve generics that have been in its review queue. The first approvals typically arrive within weeks. If multiple manufacturers have filed, some may receive tentative approvals that convert to full approvals on the expiry date. The supply market transitions from monopoly to oligopoly — typically a 2-to-4 manufacturer duopoly in the first months.

Phase 2: Price Erosion and the API Sourcing Shift

Price erosion after patent expiry follows a mathematically predictable curve for small molecules. Prices typically decline by 70–90% within 12–18 months following generic entry [7]. This erosion drives API margin compression simultaneously: as finished product prices fall, generic manufacturers squeeze suppliers, and API manufacturers who were serving the branded supply chain face volume loss from a customer base that shrinks or disappears.

For API suppliers, this creates a transition that requires active management. A supplier that has been providing API exclusively to a branded manufacturer under a long-term supply agreement may face a cliff of its own as that contract terminates or volumes drop. The smart response is to pre-qualify as a supplier to generic entrants — which requires knowing those entrants’ development timelines. Patent intelligence provides exactly that context.

Phase 3: Market Concentration and Shortage Risk

The counterintuitive consequence of generic market entry is that it increases shortage risk over the medium term. Over twice as many generic drug shortages begin as brand drug shortages, and market concentration is a primary driver [8]. As the generic market matures and prices compress, manufacturers with thin margins exit. The market consolidates around one or two suppliers. When either has a manufacturing disruption — a GMP failure, an API quality issue, a natural disaster — the supply system has no buffer.

This is the dynamic that makes long-range patent intelligence so valuable. A supply chain team that identifies a drug moving from branded to generic status can model not just the initial transition but the 3-to-5-year trajectory of market concentration. That model tells you when to establish dual-source agreements, when to build safety stock, and when a drug becomes a shortage risk even though it looks adequately supplied today.

The Biologic Exception: Why Biosimilar Timelines Require Different Models

Small-molecule generic entry is relatively predictable once you have patent data. Biosimilar entry is not. Data from Humira biosimilar entry in 2023–2024 shows what analysts call a “scalloped” erosion curve — market share didn’t shift immediately but instead in steps coinciding with PBM formulary contracting cycles, typically January 1st and July 1st [7]. By 2025, biosimilars had captured roughly 20–30% of volume, far from the 90% penetration seen in small-molecule markets.

This means biologic supply chain forecasting requires a different model: a 2-to-3-year ramp to peak erosion rather than the 6-month cliff characteristic of small molecules. API sourcing timelines, manufacturing capacity commitments, and inventory management all need to reflect that slower transition curve. A generic-style rapid clearance model applied to biosimilar planning will produce systematically wrong inventory positions.

How to Build a Patent-Informed Supply Chain Forecast: A Practical Framework

Patent intelligence doesn’t automatically produce supply chain decisions. It needs to be integrated into a forecasting framework that translates legal events into demand signals and procurement timelines. The framework below draws on practices used by leading generic manufacturers and GPO procurement teams.

Step 1: Build a Patent Expiry Calendar with Probability Weights

The starting point is an inventory of every relevant product in your portfolio (or your procurement scope), mapped against its complete patent expiry profile — not just the CoM date but the full secondary patent stack. For each product, assign probability weights to three scenarios:

Base case: patents expire on schedule, generics enter at or near the calendar expiry date

Accelerated case: Paragraph IV challenge succeeds, court rules before 30-month stay expires, generic enters early

Extended case: secondary patents hold, litigation settles with delayed launch date, authorized generic prevents full generic competition

These probability weights should come from patent intelligence data — specifically, litigation history for similar patent types, court ruling patterns, and settlement frequency data. DrugPatentWatch and comparable platforms structure this historical data in a way that makes probability calibration tractable.

Step 2: Map API Sourcing Requirements to Each Scenario

For each scenario, define the API sourcing requirements. In the base case, API sourcing proceeds according to the standard planning timeline. In the accelerated case, sourcing needs to begin earlier, with a higher probability of supply market tightness as multiple generic manufacturers compete for the same API capacity. In the extended case, sourcing may need to support a longer branded supply relationship, with different quality and volume requirements.

This scenario mapping translates patent probability into procurement decisions. It answers the question: given the probability distribution of generic entry dates, what safety stock position minimizes expected cost while maintaining service level? That calculation is straightforward once you have the patent intelligence to parameterize it.

Step 3: Monitor ANDA Filing Activity as a Leading Indicator

ANDA filing counts are public information — the FDA publishes them. For a supply chain planner, the number of ANDAs filed for a specific product is a leading indicator of the eventual generic market structure. More filers means more manufacturers entering at expiry, faster price erosion, tighter API market competition in the ramp-up phase, and lower post-expiry API prices over the medium term.

Tracking ANDA activity also tells you which therapeutic categories are attracting generic investment — which is useful for API suppliers trying to anticipate where demand will grow. A therapeutic area with heavy ANDA activity today will have mature generic market competition in three to five years, with corresponding API demand shifts.

Step 4: Integrate Litigation Status as a Dynamic Input

Patent litigation is not a static input. Court decisions, appeal outcomes, and settlement announcements change the probability distribution of generic entry dates continuously. A supply chain team that only looks at patent data once a year when building the annual plan misses the most operationally relevant information.

The practical solution is to establish a monitoring cadence — quarterly at minimum, monthly for high-priority products — that tracks litigation status and flags events that require plan updates. A court ruling in favor of a generic challenger doesn’t just affect the product in question; it changes the legal risk calculation for similar secondary patents across the portfolio.

Case Studies in Patent-Informed Supply Chain Planning

Case Study 1: Entresto (Sacubitril/Valsartan) — Reading the Legal Calendar

For supply chain teams managing cardiology formularies or GPO contracts for heart failure medications, Entresto’s patent trajectory was visible years in advance. The Paragraph IV filings against Novartis’s patent portfolio were public. The litigation outcome, while not certain, was telegraphed by the appellate court’s reasoning. And the ANDA approvals — awarded to multiple manufacturers before the July 2025 expiry — meant that staggered market launches were a near-certainty.

Teams that tracked this patent data had time to build formulary transition plans, renegotiate branded contracts with volume-based pricing to reflect upcoming competition, and establish supplier relationships with two or three of the approved generic manufacturers before launch day. Teams that didn’t track it faced an abrupt pricing cliff, emergency renegotiations, and a supplier selection process conducted under time pressure.

Case Study 2: Xarelto (Rivaroxaban) — Country-by-Country Patent Complexity

Bayer’s Xarelto illustrates what happens when global IP protection fragments. The primary composition of matter patent was set to expire in August 2024 but extended to February 2025 in the U.S. due to pediatric exclusivity. A key dosage patent was revoked in European courts while being challenged in U.S. proceedings. Generic 2.5mg tablets received FDA approval in March 2025 [1].

For a global supply chain team, Xarelto’s situation required separate modeling for each major market. A generic launch in Germany in 2024 did not trigger supply availability in the United States — each market’s patent and regulatory protections operate independently. A procurement team that assumed simultaneity in global generic availability either over-built EU API inventory or under-built U.S. API inventory, depending on which assumption they made.

The lesson: global pharmaceutical supply chains cannot use a single patent expiry date per product. They need country-level patent intelligence and country-level supply planning linked to it. The data exists; the organizational process to use it often doesn’t.

Case Study 3: Humira (Adalimumab) — The Biosimilar Slow Burn

AbbVie’s Humira dominated the rheumatology and immunology markets for years before biosimilar entry in 2023. The patent thicket AbbVie built around adalimumab — over 100 patents — delayed biosimilar competition well beyond the primary composition of matter expiry. When biosimilars finally entered, the market response followed the scalloped curve rather than the small-molecule cliff.

By 2025, adalimumab biosimilars had captured roughly 20–30% of volume — not the 80–90% market share that generic small molecules achieve within 18 months [7]. Formulary cycling, PBM contracting, and physician inertia all slowed the transition. Supply chain teams that modeled biosimilar uptake using a small-molecule template systematically over-ordered biosimilar API and over-negotiated volume commitments with biosimilar manufacturers who then underperformed sales targets.

The Humira case established an empirical baseline for biosimilar supply planning that now informs how sophisticated teams approach all major biologic patent expirations. It also demonstrated that the patent thicket strategy — which any competent patent intelligence platform makes visible years in advance — is itself a supply chain signal. The size and complexity of a brand’s secondary patent portfolio predicts the difficulty of generic entry and, by extension, the slope of the erosion curve.

API Sourcing in the Post-Exclusivity World

The drug patent cliff creates specific and predictable pressure on active pharmaceutical ingredient supply. Understanding that pressure — and using patent intelligence to anticipate it — is one of the highest-value applications of IP data for supply chain teams.

When a major product loses exclusivity and multiple generic manufacturers simultaneously scale up, they often draw on the same pool of Chinese and Indian API suppliers. Demand spikes predictably. Lead times extend. Spot prices rise. Manufacturers that secured supply agreements in advance — using patent intelligence to time those agreements — pay contracted prices. Manufacturers that entered the spot market after the demand spike pay premiums.

The valsartan contamination crisis of 2018 illustrated this vulnerability at scale. The contamination was traced to API manufactured in India and China, and the resulting shortage affected 1.9 million patients, reducing the population using valsartan from 1.9 million to 1.1 million by 2019 [10]. The root cause was not malicious — it was a chemical byproduct of a manufacturing process change made to reduce costs in a low-margin generic market. The systemic cause was predictable: price compression from generic market competition created the economic incentive to cut manufacturing costs in ways that created quality risk.

Patent intelligence can’t prevent contamination events. But it can tell you when a drug’s market structure is moving toward the conditions that make contamination events more likely: concentrated API supply, low-margin generic competition, and suppliers under pressure to cut costs.

Freedom-to-Operate Analysis as a Sourcing Tool

For generic manufacturers selecting API suppliers in emerging markets, freedom-to-operate (FTO) analysis is a sourcing requirement — not a legal luxury. An API supplier’s manufacturing process may itself infringe a valid patent. If a generic manufacturer sources from that supplier and launches, it exposes itself to infringement claims that halt production and can end the entire generic program.

Conducting FTO analysis before signing a supply agreement costs weeks of analyst time. Discovering a process patent infringement after launch costs the entire investment in the generic program, plus litigation exposure. The economics are not close.

Drug Master Files and the Sourcing Intelligence Layer

Drug Master Files (DMFs) are FDA submissions by API manufacturers that describe their manufacturing process and quality controls. They’re linked to specific ANDAs — meaning that a generic manufacturer’s ANDA identifies its API supplier by DMF number. This creates a public intelligence layer that sophisticated competitors use to assess each other’s supply chain strategies.

For a supply chain analyst, DMF activity is a leading indicator of API supplier qualification progress. A supplier filing a new DMF for a specific API, or updating an existing one, is investing in manufacturing capacity for that molecule. If the timing coincides with an upcoming patent expiry and a queue of ANDA filers, the commercial intent is clear.

Tracking DMF activity alongside Paragraph IV filing data and patent expiry timelines gives supply chain planners a three-layer picture of where the generic market is heading — which companies are entering, which suppliers are qualifying, and when the commercial pressure will arrive at the API level.

The Forecasting Tools: What’s Available and What It Actually Does

DrugPatentWatch: The Core Patent Intelligence Layer

DrugPatentWatch is the most widely cited pharmaceutical patent intelligence platform in the industry. It aggregates Orange Book patent listings, Paragraph IV certification history, litigation outcomes, FDA exclusivity records, ANDA filing data, and DMF information into a searchable database that covers thousands of drugs across multiple markets.

For supply chain purposes, the platform’s most valuable features are its patent expiry timelines (which show the complete secondary patent stack, not just headline dates), its litigation tracking (which shows real-time status of Paragraph IV suits and settlements), and its ANDA monitoring (which shows the queue of generic applicants for each product). As one pharmaceutical executive described it, the platform is “one of the greatest tools for us to manage our suppliers in API business,” providing “unique and serious data for those who are responsible in supply management, control and new product development” [11].

The operational use case is direct: a supply chain planner monitoring a specific drug can see, in a single dashboard, the remaining patent life, the number of active Paragraph IV challenges, the litigation status of each, and the number of ANDA filers queued for approval. That information parameterizes the probability model for generic entry timing — and that probability model drives the API sourcing and inventory planning decisions.

IQVIA and Commercial Data Integration

Patent intelligence tells you when generic entry is legally possible. IQVIA and comparable commercial data platforms tell you what the market looks like when it gets there — prescription volumes, market share trajectories, channel dynamics, and formulary coverage patterns. Combining both data streams produces a more accurate demand forecast than either alone.

The integration point is the generic erosion model. Patent intelligence gives you the probability distribution of launch dates. IQVIA data gives you the historical erosion rate for comparable products — small-molecule vs. biologic, number of entrants, therapeutic area, payor mix. Put them together and you get a probabilistic demand forecast with a real distribution of outcomes, not a point estimate.

FDA Databases: Public but Underutilized

The FDA maintains several public databases with direct supply chain relevance. The Orange Book is the primary patent reference. The FDA’s ANDA approval database shows every approved generic product with its manufacturer and approval date. The Drug Shortages database shows active shortages, their causes, and resolution status. The Warning Letters database shows which manufacturers have received GMP findings — which are predictive of supply disruption.

None of these databases requires a paid subscription. All of them are underutilized by supply chain teams outside the pharmaceutical sector who source pharma products for hospital systems, GPOs, or specialty distributors. The data exists; building the workflow to monitor it systematically is the gap most organizations haven’t closed.

Integrating Patent Intelligence into S&OP: Practical Barriers and How to Break Them

Sales and Operations Planning (S&OP) in pharmaceuticals typically runs on a monthly cycle. Demand signals from commercial teams, capacity signals from manufacturing, and inventory targets from finance all feed into a consensus plan that determines production schedules and procurement decisions. Patent intelligence is almost never a standard S&OP input in companies that haven’t deliberately built the process to include it.

The Cross-Functional Integration Problem

Adding patent intelligence to S&OP requires crossing the legal-operations divide that most pharmaceutical companies have institutionalized. Legal teams that own patent data often don’t understand supply chain planning cycles. Supply chain teams that own S&OP processes often don’t have the technical capacity to interpret patent data. Bridging this requires either a dedicated patent intelligence function that translates legal data into operational inputs, or technology that automates that translation.

The most effective model, in practice, is a shared patent-tracking tool that both legal and supply chain teams access — with a defined protocol for how legal events (new filings, court decisions, settlements) trigger supply chain plan reviews. Companies like Mylan (now Viatris) and Teva have built internal versions of this; smaller generic manufacturers typically rely on external platforms with monitoring alerts.

Forecast Horizons and Patent Data Relevance

Standard S&OP processes operate on a 12-to-18-month planning horizon. Patent intelligence is most valuable over a 24-to-60-month horizon — the window between when you can observe Paragraph IV filings and when generic entry typically occurs. This mismatch means that patent data needs to feed the strategic planning process (annual operating plan, 3-to-5-year financial plan) rather than just the monthly S&OP cycle.

In practice, the most operationally effective integration point is the annual supply review, where patent intelligence informs multi-year demand models and drives API supplier strategy decisions — dual-sourcing commitments, long-term supply agreements, capacity reservation contracts. The monthly S&OP cycle then tracks against those strategic commitments and flags deviations when litigation events change the timing assumptions.

Patent intelligence doesn’t eliminate the need for safety stock. It optimizes it. Specifically, it allows procurement teams to calculate the expected cost of a shortage (weighted by the probability and magnitude of supply disruption) against the carrying cost of additional inventory. That calculation produces a target safety stock level that is explicitly tied to the legal risk profile of the product — not just its historical demand variability.

The Generic Manufacturer’s Perspective: Using Patent Data Offensively

Everything discussed so far applies to branded manufacturers, GPOs, and hospital systems managing the supply consequences of patent expiry. For generic manufacturers, patent intelligence serves an additional strategic function: it identifies which opportunities to pursue and when.

Product Selection: The Patent Opportunity Screen

Generic manufacturers evaluate hundreds of potential products against a common screen: patent expiry timing, market size, number of likely competitors, API availability, and manufacturing complexity. Patent intelligence is the first filter. A product with a clear expiry date, no active Paragraph IV litigation pending from others, and no secondary patent thicket is a cleaner opportunity than one with six competing ANDA filers, active litigation, and a dense formulation patent portfolio.

Platforms like DrugPatentWatch democratize this analysis, allowing smaller, more agile generic manufacturers to identify niche opportunities that larger firms might overlook [12]. A specialty generic product in a narrow therapeutic area — small revenue relative to Humira or Entresto but with limited competition and a straightforward API supply chain — may offer better risk-adjusted returns than a high-profile blockbuster with twelve competing ANDAs.

Winning that race requires supply chain readiness at the moment of approval — not six months after. A first-filer that wins in court but can’t ship product loses the exclusivity advantage to a competitor that launches faster. This is why first-filer supply chain preparation begins, in practice, during the litigation period — before the outcome is certain. API qualification, process validation, commercial batch manufacturing, and packaging are all started at risk, on the assumption that the litigation will be won. Patent intelligence that accurately assesses the probability of a favorable outcome is directly connected to the decision of how much at-risk manufacturing investment to make.

At-risk launch decisions are fundamentally supply chain decisions as much as they are legal decisions. A company that launches at risk needs to have product manufactured and ready to ship. It needs to have distribution agreements in place. It needs to have managed the logistics of a rapid market entry. And it needs to have a contingency plan for product withdrawal — including inventory disposition and customer notification — if the court rules against it. Patent intelligence shapes all four of those decisions.

The Geopolitical Layer: When Supply Chain Risk Meets Patent Strategy

Patent intelligence operates in a legal system. Pharmaceutical supply chains operate in a geopolitical system. The two intersect in ways that create risks not visible in patent databases alone.

China’s API Dominance and Its Strategic Implications

China’s dominance in API production is even more pronounced in the Asia-Pacific region [7]. For generic manufacturers dependent on Chinese APIs, the patent expiry calendar intersects with geopolitical risk in a direct way: a supply disruption from China — whether from regulatory action, trade policy, or a manufacturing quality event — hits hardest in the period immediately following patent expiry, when demand for a newly genericized API is highest and alternative supply has not yet been qualified.

The response from sophisticated supply chain teams is geographic diversification of API sourcing — nearshoring or multi-sourcing strategies that reduce dependence on any single country. But geographic diversification requires lead time. A supply chain team that identifies a Chinese API dependency five years before patent expiry has time to qualify an Indian or European alternative, secure a supply agreement, and complete the regulatory filing required to use that alternative source in a commercial product. A team that identifies the dependency six months before expiry does not.

Patent intelligence provides the time horizon that makes geographic diversification tractable. The combination of a patent expiry calendar and an API sourcing risk assessment produces a priority list for diversification projects — ranked by urgency and commercial exposure.

Tariff Policy and the Cost of Inaction

The pharmaceutical industry has operated under a series of trade policy shocks since 2018. Tariffs on Chinese goods — including chemical precursors and APIs — have forced cost recalculations across the generic supply chain. Companies that had locked in long-term API contracts before tariff escalation were insulated. Companies on spot-market sourcing absorbed the full cost.

Patent intelligence improves tariff risk management by identifying which APIs are most likely to face sudden demand shifts — and therefore most exposed to spot-market pricing. An API approaching its first generic applications is an API where procurement teams across the industry are simultaneously evaluating supply. That coordination creates price volatility. Tariff shocks in that environment compound the impact.

Regulatory Events as Supply Chain Signals

Patent expiry is the primary legal event driving supply chain transitions. But it’s not the only regulatory event with supply chain implications. A sophisticated patent-informed forecasting framework also tracks FDA actions that can accelerate, delay, or disrupt the generic entry timeline.

FDA Warning Letters and Import Alerts

FDA enforcement actions can cause shortages. A manufacturer receiving a Warning Letter for GMP deficiencies may face an import alert that blocks its products from the U.S. market — regardless of patent status. If that manufacturer is the primary API supplier for a generic product, the supply chain impact is immediate and severe [13].

Monitoring FDA Warning Letters and import alerts for API suppliers is a supply chain risk practice that most companies conduct reactively — after an alert is issued. The more sophisticated practice is predictive: identifying which API suppliers have inspection histories suggesting deficiencies that could trigger a future Warning Letter, and diversifying away from those suppliers before the disruption occurs.

REMS Programs and Generic Access

Risk Evaluation and Mitigation Strategies (REMS) — FDA-mandated safety programs for high-risk drugs — can be used by branded manufacturers to restrict generic access to reference samples needed for bioequivalence testing. The FTC has pursued litigation against manufacturers for this practice, and the Hatch-Waxman Act includes specific provisions intended to prevent REMS abuse.

For supply chain planners, REMS programs add regulatory uncertainty to the patent uncertainty already present in the generic entry timeline. A product with an active REMS may face delayed generic entry even when the patent clock has expired, because generic manufacturers cannot complete the bioequivalence studies required for ANDA approval without access to the reference drug. Tracking REMS status — and the regulatory and litigation history around REMS-related generic delays — is part of a complete patent intelligence picture.

The Inflation Reduction Act’s Supply Chain Effects

The IRA creates a new pricing dynamic that affects supply chain economics. Drugs subject to Medicare price negotiation face compressed net pricing before generic entry — which changes the financial model for both branded supply chain investment and generic manufacturer launch timing calculations. A drug that generates lower net revenue under negotiated pricing may face earlier manufacturer exit from the branded supply chain, earlier diversion of R&D investment to successors, and potentially earlier supply vulnerability as branded manufacturing capacity is wound down.

Supply chain planners need to track IRA negotiation status alongside patent expiry data. The two events together define the economic trajectory of a product’s supply chain — and that trajectory determines when supply investment decisions need to be made.

Building the Capability: Organizational and Technological Requirements

The analytical framework described in this article requires organizational capability that most supply chain functions don’t currently have. Building it involves decisions across four dimensions: people, process, technology, and governance.

People: The Patent Intelligence Analyst Role

The most effective implementation of patent-informed supply chain planning requires at least one dedicated analyst who can translate patent data into supply chain inputs. This person needs enough legal literacy to understand Orange Book listings, Paragraph IV mechanics, and litigation outcomes — without being a patent attorney. And they need enough supply chain literacy to frame those legal events as demand signals — without being an S&OP manager.

This is a genuinely cross-functional role, and it’s relatively rare in the industry. Companies that have built the capability typically sourced it from one of two directions: hiring patent analysts with supply chain interest and training them on operational processes, or embedding supply chain analysts in legal teams with access to patent intelligence platforms and training on IP fundamentals.

Technology: Connecting Legal and Operational Systems

Patent intelligence platforms — DrugPatentWatch and its competitors — typically don’t integrate directly with ERP systems or S&OP planning tools. Data flows between them require either manual extraction and analysis or custom integration work. Companies making the largest investments in patent-informed planning are building those integrations: automated exports from patent intelligence platforms into the data environments where supply planners work.

Process: Embedding Patent Reviews in Planning Cycles

Technology without process doesn’t produce decisions. The organizational process for patent-informed planning needs to define: who reviews patent data, how often, what events trigger a plan update, and how patent intelligence findings get translated into procurement decisions. Without that process, the capability sits unused between planning cycles — exactly when the most operationally relevant events (new filings, court decisions, settlements) are occurring.

The most effective process design creates standing patent intelligence reviews at quarterly intervals, with an alert-triggered exception process for significant events. Significant events include new Paragraph IV filings against products in the company’s portfolio or procurement scope, court decisions in ongoing cases, settlement announcements, and unexpected FDA actions against key API suppliers.

The Financial Case: Quantifying the Value of Patent Intelligence

Every capability investment requires a financial justification. For patent-informed supply chain planning, the ROI case is straightforward — if you’re willing to model it honestly.

The Cost of Getting It Wrong

The cost of not using patent intelligence shows up in four places: emergency API sourcing premiums, inventory write-offs (branded API purchased in excess of post-expiry demand), lost revenue from stockouts during generic entry transitions, and contract penalties from supply agreements that didn’t account for legal risk.

Emergency sourcing premiums in the API market can run 30–100% above contracted prices when supply is tight. For a drug moving from brand to generic with $500 million in annual U.S. sales, the procurement exposure is material. A conservative model of avoided emergency sourcing premiums alone — capturing 10% of the premium on 20% of annual API spend — produces a dollar value that exceeds the cost of a dedicated patent intelligence function.

The Value of Earlier Entry Timing

For generic manufacturers, the financial case for patent intelligence is even sharper. The difference between winning 180-day exclusivity and entering as a day-180 second wave is, on major products, a difference of hundreds of millions of dollars in gross profit. The probability of winning first-filer status depends partly on legal strategy — which is outside supply chain’s remit — but it also depends on supply chain readiness at the moment of approval, which is entirely within supply chain’s control.

A generic manufacturer that wins first-filer status but can’t ship product because API qualification isn’t complete loses the entire exclusivity advantage. Conversely, a manufacturer that has built supply chain readiness based on accurate patent intelligence — qualifying API 24 months before expected launch, building safety stock, securing distribution agreements — captures the full value of the legal win. The supply chain investment is a multiplier on the legal investment.

What the Next Five Years Look Like

The 2025–2030 patent cliff is the largest revenue exposure event in pharmaceutical industry history. Total pharma M&A deal value reached $240 billion in 2025, an 81% year-over-year increase, as companies tried to replace revenue that patents would no longer protect [15]. But M&A alone cannot fill a $236 billion hole [1], and the supply chain implications of that exposure are just beginning to materialize.

Every one of the major drugs losing exclusivity in this window — Keytruda, Eliquis, Opdivo, Stelara, Jardiance — represents a substantial API market transition. Branded API supply chains will wind down. Generic API markets will scale up. The timing, speed, and competitive structure of each transition is different — and patent intelligence is the tool that makes those differences tractable.

The Biosimilar Decade

The next decade will be a biosimilar decade as biologics that entered the market in the 2000s and 2010s move through their exclusivity windows. Biosimilar supply chains are more complex than small-molecule generics — manufacturing biologics requires specialized equipment, tighter process controls, and longer technology transfer timelines. Patent intelligence for biologics needs to account for both the patent landscape and the manufacturing readiness of potential biosimilar entrants, because the bottleneck to biosimilar entry is often manufacturing capability, not legal clearance.

Supply chain teams managing formulary transitions for biologic products need biosimilar-specific intelligence: which manufacturers have clinical programs in progress, which have manufacturing capacity, and which have settlement agreements that define launch windows. All of that information is partially visible in public databases — patent filings, FDA biological product submissions, litigation records — and structured for analysis by platforms designed for pharmaceutical IP monitoring.

The Role of AI in Patent-Informed Forecasting

Artificial intelligence is beginning to change how patent intelligence gets generated and applied to supply chain planning. Machine learning models trained on historical patent litigation outcomes can produce probability distributions for new cases with reasonable accuracy. Natural language processing applied to court filings and settlement documents can extract launch date commitments and trigger conditions that would otherwise require manual review.

The practical application for supply chain planning is not AI replacing the patent analyst — it’s AI processing the volume of data that a single analyst cannot. There are thousands of patents, hundreds of active litigations, and dozens of settlement negotiations relevant to a large pharmaceutical portfolio at any given time. AI can surface the highest-priority signals for human review, prioritize monitoring alerts by commercial importance, and update probability models in real time as new information arrives.

The companies building this capability now will have a forecasting advantage in the 2030 patent environment that those waiting for mature off-the-shelf solutions will not. Building the data architecture, the analytical models, and the organizational processes takes time — and the 2025–2030 cliff is already underway.

Key Takeaways

Patent data is a demand signal, not just a legal tool. Patent expiry timelines, Paragraph IV filings, and litigation outcomes all predict when and how supply markets will shift — giving supply chain teams a planning horizon that historical demand data alone cannot provide.

The 30-month Hatch-Waxman stay is a built-in planning horizon. A Paragraph IV challenge filed today sets a 30-month minimum window before generic approval — time that generic supply chains can use for API qualification, capacity reservation, and launch preparation.

Biosimilar erosion curves are fundamentally different from small-molecule curves. Biosimilars follow a 2-to-3-year erosion ramp, not a 6-month cliff. Supply models that use small-molecule templates for biologic transitions will systematically misplace inventory.

The patent thicket size predicts generic entry difficulty. A drug with a large secondary patent portfolio signals slower generic entry, lower short-term erosion, and more complex supply transition management — all visible in patent databases years before expiry.

API geographic concentration and patent timing interact directly. The risk of an emergency sourcing event is highest when a patent expires and multiple generic manufacturers simultaneously compete for the same API supply. Building dual-source agreements before that demand surge is the mitigation — and patent intelligence gives you the lead time to do it.

Platforms like DrugPatentWatch make this intelligence accessible. Structured patent monitoring doesn’t require a team of patent attorneys. Purpose-built platforms aggregate and translate the relevant legal data into operational inputs that supply chain planners can act on.

Frequently Asked Questions

Q1: How far in advance should supply chain teams start monitoring patent data for a specific drug?

The operationally useful window begins when the first Paragraph IV certifications appear — which can be five to eight years before a primary patent expires for blockbuster drugs. By the time you see an ANDA filing with a Paragraph IV certification, at least one manufacturer has done enough development work to challenge the patent. That’s when API qualification, supplier evaluation, and supply scenario modeling should begin. For drugs without Paragraph IV challenges, start the formal monitoring process 36 to 48 months before the earliest plausible patent expiry date. That window gives you time to qualify alternative suppliers, negotiate agreements, and build safety stock without emergency sourcing exposure.

Q2: What’s the practical difference between tracking patent expiry dates vs. effective exclusivity dates, and does it matter for supply chain planning?

It matters enormously. A patent expiry date tells you when a specific patent’s legal protection ends. Effective exclusivity — the date at which generic competition actually becomes commercially possible — depends on the complete secondary patent stack, FDA market exclusivity grants (NCE, orphan, pediatric), pending litigation outcomes, and settlement terms. For a drug with a primary CoM patent expiring in 2026 but 15 secondary patents covering formulations and delivery systems running through 2031, the effective exclusivity date could be 2028 under a settlement, or 2031 if the thicket holds. A supply chain plan built around the 2026 date will be wrong in ways that matter: either over-building generic supply capacity or under-preparing branded supply continuity. Effective exclusivity requires the full legal picture, not just the headline date.

Q3: How should hospital systems and GPOs use patent intelligence differently from pharmaceutical manufacturers?

Hospital systems and GPOs use patent intelligence primarily as a contracting and formulary management tool. The key questions are: when will generic alternatives become available for drugs currently on contract, what will the price impact be, and how many generic suppliers are likely to enter (which determines how quickly prices will compress). A hospital system can use patent expiry timelines and ANDA filing counts to time formulary reviews, negotiate branded contracts with generic-entry-contingent pricing structures, and build volume commitments with generic manufacturers entering the market. GPOs can use the same intelligence to structure tiered purchasing agreements that position members to capture savings from generic entry while maintaining supply continuity during the transition. The intelligence is the same; the application is formulary and contracting strategy rather than manufacturing and sourcing strategy.

Q4: What happens to supply chain risk when a Paragraph IV challenge fails — i.e., when the brand wins in court?

A brand win in Paragraph IV litigation restores the original patent expiry timeline — at least for that specific challenger. But it doesn’t eliminate supply chain uncertainty. Other potential challengers may still file their own Paragraph IV certifications against different patents in the portfolio. The brand company may face additional litigation from the losing challenger’s appeal. And the commercial pressure that prompted the original challenge — a large, unmet generic market opportunity — hasn’t disappeared. Supply chain teams should model a brand litigation win as a probability-weighted outcome, not a certain resolution. The planning implication is to maintain a range of scenarios — from “brand wins and full exclusivity holds to expiry” to “subsequent challengers succeed at some point before expiry” — rather than treating a favorable ruling as a closed question.

Q5: How does the Inflation Reduction Act’s Medicare drug price negotiation change the patent cliff calculus for supply chain teams?

The IRA introduces a pricing compression that begins before patent expiry for drugs selected for Medicare negotiation. This changes the supply chain economics in two specific ways. First, branded manufacturers facing compressed negotiated pricing earlier in the product lifecycle have less revenue to fund supply chain investment and maintenance — which can reduce supply reliability before the formal patent transition. Second, for generic manufacturers evaluating when to invest in launch preparation, the IRA changes the branded revenue baseline against which they’re competing. If a drug’s peak revenue is already declining due to negotiated pricing, the first-filer exclusivity prize is smaller, and the investment case for aggressive Paragraph IV litigation is correspondingly weaker. Supply chain teams need to account for this dynamic when modeling generic entry timing for IRA-negotiated drugs — the competitive pressure to challenge patents early may be lower, which could mean later, more compressed generic market entry rather than the staggered multi-year rollout seen in non-negotiated categories.

References

DrugPatentWatch. (2025, December 11). The patent cliff protocol: Advanced methodologies for forecasting generic drug launches and market erosion. https://www.drugpatentwatch.com/blog/the-patent-cliff-protocol-advanced-methodologies-for-forecasting-generic-drug-launches-and-market-erosion/

LGM Pharma. (2023, February 21). Risk management practices to address pharmaceutical sourcing challenges. https://lgmpharma.com/blog/risk-management-practices-to-address-pharmaceutical-sourcing-challenges/

Meyer, M. (2026). Pharmaceutical patent prosecution: Hatch-Waxman and FDA guide. The Law Office of Michael Meyer. https://www.michaelmeyerlaw.com/blog/pharmaceutical-patent-prosecution-hatch-waxman/

DrugPatentWatch. (2025). The Paragraph IV playbook: Turning patent challenges into market dominance. https://www.drugpatentwatch.com/blog/the-paragraph-iv-playbook-turning-patent-challenges-into-market-dominance/

Helland, E., & Seabury, S. (2023). Settled: Patent characteristics and litigation outcomes in the pharmaceutical industry. International Review of Law and Economics. https://www.sciencedirect.com/science/article/abs/pii/S0144818823000479

DrugPatentWatch. (2026). Drug patent challenges: The complete strategic playbook for IP teams and portfolio managers. https://www.drugpatentwatch.com/blog/when-science-meets-law-the-art-and-strategy-of-challenging-drug-patents/

DrugPatentWatch. (2026, January 22). The patent cliff and beyond: A definitive guide to generic and biosimilar market entry. https://www.drugpatentwatch.com/blog/generic-drug-entry-timeline-predicting-market-dynamics-after-patent-loss/

U.S. Department of Health and Human Services, Office of the Assistant Secretary for Planning and Evaluation. (2025, January 10). Analysis of drug shortages, 2018–2023. https://aspe.hhs.gov/sites/default/files/documents/efa332939da2064fa2c132bb8e842bb5/Drug%20Shortages_Data%20Brief_Final_2025.01.10.pdf

Pharmacy Times. (2026, May 7). A pharmacist’s guide to blockbuster patent expirations: 2025 and beyond. https://www.pharmacytimes.com/view/a-pharmacist-s-guide-to-blockbuster-patent-expirations-2025-and-beyond

American Progress. (2024, July 23). Industrial policy to reduce prescription generic drug shortages. https://www.americanprogress.org/article/industrial-policy-to-reduce-prescription-generic-drug-shortages/

DrugPatentWatch. (2025, December 18). API sourcing in emerging markets: The new epicenter of opportunity and risk. https://www.drugpatentwatch.com/blog/api-sourcing-in-emerging-markets-the-new-epicenter-of-opportunity-and-risk/

DrugPatentWatch. (2025, December 8). The strategic core: A definitive guide to API sourcing for generic drug manufacturers. https://www.drugpatentwatch.com/blog/the-strategic-core-a-definitive-guide-to-api-sourcing-for-generic-drug-manufacturers/

DrugPatentWatch. (2026). These 62 drugs face patent expirations and generic entry from 2026–2027. https://www.drugpatentwatch.com/p/expiring-drug-patents-generic-entry/

TraxTech. (2025, October 31). Pharmaceutical supply chain data integration addresses API sourcing vulnerability. https://www.traxtech.com/ai-in-supply-chain/pharmaceutical-supply-chain-data-integration-addresses-api-sourcing-vulnerability

DeepCeutix. (2026, February 2). $300 billion in pharma revenue loses patent protection by 2030. https://deepceutix.com/insights/patent-cliff-reformulation

for Pharmaceutical APIs")