Pharmaceutical executives spend billions building patent portfolios. Analysts spend months modeling their worth. And yet the conversation about what actually makes a drug patent valuable — not merely granted — stays locked inside law firm memos and licensing term sheets that never see the light of day.

That needs to change. Patent value is not an abstract concept for IP attorneys. It is the single most powerful lever determining whether a drug company captures two decades of monopoly rent or watches a generic manufacturer walk away with the market six years after launch. Get it wrong in either direction — overvaluing a patent that collapses under challenge, or undervaluing one before a licensing negotiation — and the financial consequences can dwarf the cost of any R&D program.

This guide dissects the mechanics of drug patent valuation from first principles. We move through the core methodologies, the objective and subjective indicators that actually correlate with commercial worth, the industry-specific risk factors that make pharma valuation categorically harder than other sectors, and the emerging tools reshaping how analysts work. Along the way, we examine the legal and strategic realities — evergreening, patent thickets, the Hatch-Waxman Act’s unintended consequences, the biosimilar void — that no valuation model can responsibly ignore.

The data is concrete. The cases are real. And the analysis applies equally to a $200 billion blockbuster and an early-stage biotech deciding which patents to pursue.

Part One: Why Patent Value Is Hard to Measure

What a Patent Actually Confers

Before measuring value, it helps to be precise about what a patent is. A patent grants its owner the exclusive right to prevent others from commercially exploiting the patented invention for a limited period within a specific jurisdiction [1]. The invention cannot be commercially made, used, distributed, imported, or sold by third parties without the patent owner’s consent. When that boundary is crossed, the patent holder can seek legal remedies for infringement.

That legal exclusivity is foundational, but it is not the same thing as value. A patent protecting a compound that never reaches clinical approval has almost no commercial value despite being fully enforceable. The value of a patent is the difference between an invention’s worth with patent protection — effectively a monopolistic position — and what that same invention would fetch in a competitive market [2]. That delta is what analysts are trying to quantify.

The economic value of a pharmaceutical patent reflects the measurable benefits it generates for its owner: the margin protected by exclusivity, the revenues enabled by market access, the barriers it creates against competition, and the optionality it affords through licensing and partnership. A patent can also enhance the value of other associated assets — manufacturing infrastructure, regulatory approvals, branded prescribing habits — by making those assets harder to replicate without infringement.

Why the Distribution of Patent Value Is Brutally Skewed

Here is a fact that should immediately recalibrate any generic assumption about portfolio value: patent values follow a heavily skewed distribution. A 2005 study — the PatVal-EU survey — found that only 7.2% of patents were valued above €10 million, while approximately 68% were valued below €1 million [7]. In other words, the overwhelming majority of granted patents have minimal economic worth.

This is not a minor statistical nuance. It is the central operating reality of IP management in pharma. Most patents in a portfolio are not assets — they are costs. They consume prosecution budgets, maintenance fees, and management attention. Only a small fraction of filings generate the disproportionate returns that justify the entire enterprise.

The practical implication: you cannot evaluate a company’s IP strength by counting patents. You have to evaluate the value of each patent — or at minimum, of the portfolio’s material assets — using the indicators and methodologies that correlate with commercial worth, not merely with granted status.

The Strategic Stakes of Getting Valuation Right

Patent valuation matters in concrete, high-consequence contexts. Each situation creates different incentives for accuracy and different risks for getting it wrong [3, 4]:

Mergers and acquisitions: When Bristol-Myers Squibb acquired Celgene for $74 billion in 2019, a significant portion of the deal price was anchored on the commercial longevity of Revlimid’s patent portfolio. Overvaluing the defensibility of those patents — or underestimating the litigation exposure — would have moved the implied deal price materially. Understanding the real worth of IP assets is not supplementary to M&A diligence; it is the diligence.

Licensing negotiations: A patent licensor and licensee are negotiating over the same underlying commercial reality from opposing directions. Both need an independent and defensible valuation to establish a rational royalty rate. Without it, the negotiation defaults to leverage rather than economics.

Securing financing: Lenders treating patents as collateral need to be able to value them separately from the business. A patent that has not been validated through licensing, litigation, or third-party analysis is a weak foundation for a credit facility.

Litigation strategy: Knowing the value of a patent under dispute — and the damages that could flow from infringement — directly shapes whether to litigate, settle, or license. The average patent damages award reached $24.4 million in 2023, with the highest award exceeding $2 billion [22]. That range alone illustrates why valuation precision matters.

Portfolio management: Internally, companies make daily decisions about which patents to prosecute, maintain, abandon, or license. Those decisions compound over time into portfolio quality. Systematic valuation is what separates strategic IP management from ad hoc filing.

Part Two: The Core Valuation Methodologies

No single methodology reliably captures the full value of a pharmaceutical patent. Analysts use multiple approaches in combination, treating each as a different lens on the same underlying asset. The three principal frameworks — income, market, and cost — each have distinct strengths and blind spots [3, 9].

The Income Approach: Cash Flows Are the Point

The income approach is the primary workhorse of pharmaceutical patent valuation. The logic is direct: an intangible asset is worth the present value of the future cash flows it will generate over its economic life [3, 9]. Four distinct methods sit under this umbrella.

Discounted Cash Flow (DCF) Analysis

DCF projects future revenues attributable to the patented drug, deducts costs (manufacturing, distribution, regulatory maintenance, royalties payable), and discounts the resulting cash flows back to present value at a rate reflecting the investment’s risk [9, 11]. For pharmaceutical applications, the discount rate is the most contested input. Late-stage pipelines — Phase 3 with positive clinical data — might use a 10-15% discount rate. Early-stage biotech assets might use 30-40%, reflecting the much higher probability of failure [12]. The range matters: the same revenue projection discounted at 15% versus 35% yields dramatically different present values.

The key discipline in pharmaceutical DCF is attribution — isolating the cash flows specifically generated by the patent from those that would exist without it. A drug’s revenues depend on manufacturing capability, a sales force, regulatory approvals, and branded prescribing habits. The patent protects a subset of that value. Overcounting the patent’s contribution leads to systematically inflated valuations that collapse when the exclusivity expires and the generic enters with a fraction of the originator’s cost structure.

Relief-from-Royalty

This method avoids the attribution problem by asking a different question: if the company did not own this patent and had to license the technology from a third party, what royalty would it pay? The patent value is the present value of those hypothetical royalty savings [3]. The method depends on finding comparable royalty rates — a task complicated by the fact that most licensing terms are confidential. Published benchmarks exist by therapeutic area, and databases of disclosed deals provide reference points, but the comparability analysis requires judgment.

Relief-from-royalty works particularly well for valuing patents on formulation technologies, drug delivery systems, or manufacturing processes where the technology has licensing analogs. It is less reliable for a novel therapeutic target with no market history.

Incremental Cash Flow

The incremental method directly compares a scenario with the patent to a hypothetical scenario without it. The difference in cash flows is the patent’s value [3]. This works cleanly for patents protecting a meaningful competitive differentiator — a superior efficacy profile, a better tolerability, a first-in-class mechanism — where the counterfactual is a competitor drug generating lower market share. It is harder to apply when the patent covers something like a manufacturing process that is not directly visible to prescribers.

Multi-Period Excess Earnings

The most technically demanding income method, this approach deducts “contributory asset charges” — returns attributable to all other assets supporting the product: the manufacturing plant, the workforce, the regulatory approvals, the trade name — and treats the remaining earnings as attributable to the patent [3, 9]. What is left after paying all those other assets is excess earnings, and those excess earnings are discounted to present value. This method is most useful when a patent is deeply integrated into a larger business and when the analyst has detailed internal financials.

The Market Approach: Looking for Comparables

The market approach values a patent by benchmarking it against actual prices paid for comparable IP assets in arm’s-length transactions [3]. In theory, if a patent on a similar compound in a similar therapeutic area sold for X in a licensing deal last year, that is useful anchoring information.

In practice, the market approach runs into the core problem of IP markets: they are not active markets in the economic sense. An active market requires homogeneous goods, multiple buyers and sellers, and publicly known prices [3]. Patent transactions meet none of these criteria. Every patent is unique, most transactions are private, and disclosed terms are rarely detailed enough to support rigorous comparability analysis.

The market approach’s appropriate role in pharmaceutical patent valuation is as a sanity check or calibration input, not as a primary method. It can validate or challenge DCF-derived royalty rate assumptions, and it provides useful ranges. Treating it as the principal valuation framework invites the error of anchoring to transactions that look comparable on the surface but differ fundamentally in legal strength, claim scope, or remaining term.

The Cost Approach: What It Cost Has Little to Do with What It Is Worth

The cost approach values a patent based on the investment required to create or replicate it — R&D expenditures, patent prosecution costs, and related development spending [3]. The conceptual flaw is straightforward: the cost of developing a drug patent has essentially no predictive relationship with that patent’s commercial value. The research that generated a failed compound and the research that produced a blockbuster may have cost roughly the same amount. What separates them is efficacy, safety, timing, and market context — none of which the cost approach captures.

The cost approach has legitimate uses: establishing a floor price in negotiations, providing a plausibility check for early-stage assets where future benefits are genuinely unquantifiable, and pricing patents for insurance and tax purposes where replacement cost is the relevant standard. It is not a tool for assessing the commercial worth of a patent with market potential.

Hybrid Models: The Realistic Practitioner’s Choice

Professional patent valuers in the pharmaceutical sector almost always combine methods. The income approach provides the primary financial model; the market approach calibrates key assumptions; the cost approach provides the floor. Qualitative indicators inform the discount rate, the probability weightings in risk-adjusted models, and the judgment calls embedded in every financial projection [10].

The value of a hybrid framework is not just comprehensive coverage. It also surfaces internal inconsistencies. If a DCF yields a present value of $800 million but comparable licensing transactions suggest a market value of $200 million, the gap demands explanation. Either the revenue projections are too optimistic, the discount rate too low, the royalty rate comparables too pessimistic, or the asset is genuinely undervalued relative to the market’s current understanding. The hybrid approach forces that conversation rather than allowing any single method to produce an unchallenged number.

Part Three: The Indicators That Actually Signal Patent Value

Research has identified a set of concrete indicators — some extractable directly from public databases, others requiring expert assessment — that correlate meaningfully with a patent’s economic worth. Understanding these indicators lets analysts build a more reliable picture of patent value without solely relying on financial projections [7, 8].

Objective Indicators: What the Data Says

Forward Citations: The Most Reliable Quantitative Signal

The number of times a patent is cited by subsequent patents — forward citations — is consistently the strongest single quantitative predictor of patent value in the research literature [7, 8]. When a later inventor cites your patent, it signals that your work was foundational enough to be recognized as prior art. That is a measure of technological influence.

A patent’s forward citation count forms part of a larger citation network that tracks the diffusion of technical knowledge. Patents that anchor important clusters in that network — those cited by many subsequent patents across multiple technology classes — tend to be the ones covering genuinely fundamental innovations rather than marginal improvements [7].

For pharmaceutical analysts, forward citation counts are accessible through patent databases and commercial IP intelligence platforms. The relevant question is not just the raw count but the quality of citing patents: citations from major competitors in the same therapeutic area carry more signal than citations from unrelated technology domains.

Backward citations — references to prior patent and non-patent literature within the patent document itself — also carry information. A patent that extensively cites peer-reviewed scientific articles tends to reflect higher science intensity, suggesting a deeper inventive step [7]. That “science intensity” correlates with patents covering genuinely novel mechanisms rather than incremental formulation work.

Patent Family Size: Voting with Prosecution Budgets

A patent family includes all the patent applications filed in different countries for the same underlying invention. Prosecuting a patent in each additional country requires translation costs, local prosecution fees, and maintenance payments throughout the life of the patent. Companies are not irrational — they pay those costs when they believe the underlying invention justifies the investment [7, 8].

Patent family size is therefore a revealed preference signal. A compound protected in the US, EU, Japan, China, Canada, Australia, and a dozen additional markets has a much larger family than one protected only domestically. The scale of that investment signals the patent owner’s assessment of global commercial potential.

For due diligence purposes, family size helps analysts quickly screen for strategic intent. A 20-country family suggests the company believes this asset has global commercial relevance. A 2-country family suggests either geographic focus or limited commercial ambitions — both of which are relevant to valuation. Databases like those provided by DrugPatentWatch allow analysts to map patent families efficiently across jurisdictions, integrating this data with expiration dates, Orange Book listings, and litigation history for a consolidated view.

Claim Scope and IPC Classification Breadth

The scope of a patent’s claims defines the legal territory it controls. Broad claims that prevent competitors from designing around the invention without significant engineering investment are more valuable than narrow claims confined to a specific compound, dose, or use [7, 8]. This seems obvious, but the practical assessment of claim scope requires technical and legal judgment that quantitative databases cannot fully capture.

One useful proxy: the number of International Patent Classification (IPC) codes assigned to a patent. A patent covering multiple IPCs signals broader technological applicability — the invention has relevance across more than one technical domain [7]. A drug delivery system that applies to multiple therapeutic classes, or a manufacturing process that works across different compound types, will typically carry more IPC codes and command broader protection than a compound patent specific to a single molecule.

Claim scope analysis requires reading the actual claims, not just counting them. A patent with 20 narrow dependent claims is not necessarily broader than one with 3 well-drafted independent claims. The quality and drafting of the independent claims — specifically, how much design-around space competitors have — is what determines commercial protection.

Prosecution History and Patent Lifetime

A patent’s prosecution history — the record of office actions, responses, amendments, and examiner interviews between filing and grant — contains information about how hard the patent was to obtain and what limitations were imposed during the process [7]. Patents that sailed through prosecution with minimal restriction may have claims that were never truly tested. Patents that emerged from a contested prosecution after successfully arguing for broader claim scope represent a stronger validated asset.

The age of a patent matters in two ways. Remaining term sets a ceiling on the revenue-generating period — a patent with 18 months remaining has less value than an identical patent with 12 years remaining, all else equal. But the longevity of prosecution itself — patents with long examination histories that ultimately emerged granted — often signals that the examiner’s challenges were ultimately overcome, which strengthens the legal position.

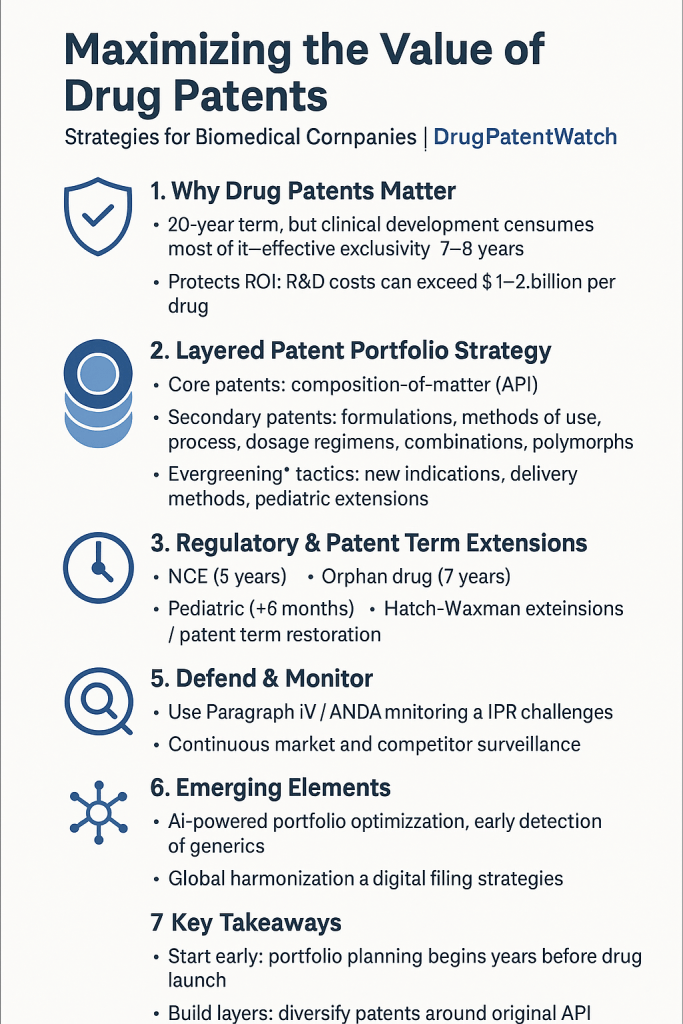

In pharmaceutical contexts, patent term extensions under Hatch-Waxman — which can extend effective exclusivity by up to 5 years — are worth incorporating explicitly into remaining term calculations rather than using the nominal 20-year term [13, 14].

Grant Decision and Opposition Outcomes

The most direct validation of a patent’s legal strength is surviving a challenge. A patent that has successfully defended itself against an opposition at the European Patent Office, or against an inter partes review (IPR) petition at the USPTO’s Patent Trial and Appeal Board (PTAB), has been tested under adversarial conditions and held up [7].

IPR petitions at PTAB grew to over 1,500 filings in 2023, with petitioners succeeding in invalidating or limiting claims at a 70% rate [21]. That success rate means patents that have survived an IPR belong to a relatively select group. A patent that was petitioned and survived represents a meaningfully stronger legal asset than one that has never been challenged — not because the challenge itself adds value, but because surviving it provides independent validation.

Subjective Indicators: Expert Assessment

Objective indicators provide quantitative screens. They do not substitute for expert technical and legal judgment on the factors that determine whether a patent will hold up in litigation, whether competitors can design around it, and whether it covers commercially essential technology.

Genuinely Novel Technology vs. Incremental Filing

The patentability requirements — novelty, non-obviousness, utility — are legal standards, but they exist on a spectrum of stringency in practice. A compound patent covering a first-in-class mechanism of action represents a qualitatively different level of innovation than a method-of-use patent covering a dosing schedule that any clinician could have derived from existing data.

Expert assessment of the inventive step — the degree to which the claimed invention would have been non-obvious to a person skilled in the relevant art — is among the most important qualitative inputs to pharmaceutical patent valuation. High inventive step correlates with harder-to-design-around claims, stronger prosecution position, and more credible exclusivity.

Difficulty of Designing Around

Even a validly granted patent with broad claims does not guarantee competitive protection if a sophisticated medicinal chemist can produce a structurally modified compound with the same therapeutic effect. The practical question is: how hard is it for a competitor to achieve the same clinical outcome without infringing the claims?

Patents on specific mechanisms of action, on novel biological targets, or on fundamental process chemistry tend to be harder to design around than patents on specific formulations or dosing regimens, which are more amenable to modification. This assessment requires technical depth — it is not available from a database query.

Dependence on Complementary Assets

A patent’s commercial value is not independent of the ecosystem around it. A patent on a biologic manufacturing process is more valuable to a company that already has the relevant bioreactor infrastructure than to one that would need to build it from scratch. The requirement for complementary assets to realize a patent’s value affects both its standalone worth and its transferability through licensing or sale.

For valuation purposes, the question is whether the patent creates value primarily through the patented technology itself, or whether its value is contingent on difficult-to-replicate complementary assets that the patent owner already controls. High complementary asset dependence increases value for the current owner and reduces the patent’s licensing appeal to parties who lack those assets.

Part Four: Industry-Specific Risks That Change Everything

Standard IP valuation methods require significant adaptation for the pharmaceutical and biotechnology sectors. The risks are different in kind, not just in degree.

Clinical Trial Failure Is the Default, Not the Exception

Only about 11% of drugs that enter clinical trials reach market approval [12]. That is the baseline failure rate against which all pharmaceutical patent valuations must be calibrated. A compound patent filed at the start of Phase 1 has, statistically, less than a 15% chance of generating any commercial revenue from that specific application. Most drug patents are written on assets that will fail.

Risk-adjusted net present value (rNPV) is the standard tool for incorporating this reality. Rather than projecting unconstrained revenue and applying a discount rate that implicitly accounts for failure risk, rNPV multiplies the projected cash flows at each development stage by the probability of reaching the next stage [12]. The resulting number is smaller than an unadjusted DCF — often dramatically so — but it is more honest about where value actually lies.

The rNPV approach has a specific implication for patent portfolio valuation: a portfolio containing 10 early-stage patents and 2 Phase 3 assets may have most of its expected value concentrated in the late-stage assets. The early-stage patents are not worthless, but their contribution to portfolio value is heavily discounted by failure probability.

The market’s reaction to clinical news provides a rough validation of this framework. Positive Phase 1 results may produce a 3% increase in share price; negative Phase 3 results — where the asset has already consumed most of its development capital — typically cause a 22% decline [12]. The asymmetry reflects the skewed value distribution within clinical-stage pipelines.

The Regulatory Approval Premium

A patent without regulatory approval is unmonetizable. FDA or EMA approval transforms a molecule from a theoretical commercial asset into an actual product. This binary outcome — approved or not — creates a step change in patent value that is not easily modeled through a continuous discount rate [11].

Regulatory risk manifests in multiple forms: complete response letters requiring additional studies, safety signals that emerge in Phase 3, manufacturing deficiencies at the time of inspection, and post-approval label restrictions that constrain prescribing. Each of these outcomes affects the commercial value of the underlying patent, sometimes catastrophically.

Valuation models for pre-approval patents must incorporate explicit probability estimates for approval. Historical approval rates by therapeutic area, by mechanism, and by indication provide useful base rates, but asset-specific factors — particularly the strength of the Phase 3 package and any existing safety signals — should dominate generic historical probabilities.

Market Size Is Not Static

Revenue projections for pharmaceutical patents require a careful distinction between total addressable market and realistic market share under competition. Disease prevalence provides the ceiling; competitive intensity, prescribing dynamics, payer coverage, and patient adherence determine where market share actually lands [11].

Two variables that most models underweight: the speed of generic entry after exclusivity loss and the depth of the post-exclusivity revenue cliff. Pharmaceutical revenues do not erode gradually when generics enter — they collapse. Within 12-18 months of the first generic entry for an oral small molecule, originator market share typically falls to below 20% by volume, even if value share remains higher due to patient assistance programs and branded pricing. Projections that model a gradual erosion substantially overvalue the remaining patent term.

For biologics, the erosion curve is different. Biosimilar uptake historically has been slower than generic uptake for small molecules, due to prescriber comfort, product complexity, and reimbursement dynamics. But that advantage is eroding as payers become more aggressive about biosimilar substitution.

The Inflation Reduction Act Recalibration

The Inflation Reduction Act’s Medicare drug price negotiation provisions, which became active starting in 2026, introduced a new variable into the valuation of high-revenue pharmaceutical patents. Drugs selected for negotiation — initially small molecules with more than 7 years post-approval and biologics with more than 11 years — face government-set prices that may significantly reduce their revenue trajectories within the period of otherwise-valid patent exclusivity.

This means a patent’s legal exclusivity and its commercial exclusivity are no longer synonymous for drugs in the negotiation pool. A compound patent extending to 2032 on a drug selected for price negotiation in 2027 is worth considerably less than the same patent on a drug outside the negotiation pool. Patent valuation models for Medicare-relevant drugs now need to incorporate negotiation probability and negotiated price estimates as explicit inputs — a structural change in how analysts think about the income approach for these assets.

Part Five: The Legal Strategies That Reshape Patent Lifespans

Evergreening: The Numbers Behind the Strategy

“Evergreening” describes the practice of filing new patents on modifications, formulations, combinations, or new uses of an existing drug to extend market exclusivity beyond the original patent term. The term is contentious — industry representatives prefer “lifecycle management” — but the strategic logic is consistent regardless of terminology [15, 16].

The scale of evergreening in the pharmaceutical industry is not subtle. Studies show that nearly 80% of the top 100 best-selling drugs have extended their patent protection with new patents filed after initial approval [23]. The modifications covered by these secondary patents range from genuinely useful — new pediatric formulations, improved stability, new delivery systems with real clinical benefits — to minimally innovative — chiral switches, salt form changes, new dosage strengths covering a range already derivable from existing data.

Humira is the canonical example. AbbVie applied for over 300 patents on the drug over its 20+ years on the market, securing more than half of them, with 94% of the patents filed after the drug was initially approved by the FDA. The strategy helped block competition for years and generated almost $200 billion for AbbVie. Humira’s original compound patent expired in 2016. Through an aggressive thicket of secondary patents, AbbVie maintained effective exclusivity in the US until 2023, seven years after the primary patent fell.

Merck’s Keytruda (pembrolizumab) is following a similar trajectory. Merck has filed 129 patent applications on Keytruda, with over half filed after initial FDA approval, and has received 53 granted patents on this single drug. I-MAK estimates that Americans will spend at least $137 billion on Keytruda due to the extended exclusivity these patents enable [23].

For analysts, the practical implication is that a drug’s “patent expiry” is almost never a single date. It is a sequence of potential expiration events across a patent thicket, each of which a generic manufacturer must challenge or design around. DrugPatentWatch is particularly useful here: its Orange Book integration, combined with coverage of PTAB litigation and paragraph IV certifications, allows analysts to map the full expiration landscape for a given drug rather than relying on a single nominal date.

The Hatch-Waxman Act: Intent vs. Reality

The Drug Price Competition and Patent Term Restoration Act of 1984 was designed as a deliberate compromise. Generic manufacturers received an expedited approval pathway — the Abbreviated New Drug Application (ANDA) — allowing them to rely on originator safety and efficacy data without independent clinical trials [13, 14]. Originators received patent term extensions (PTEs) of up to 5 years to compensate for time lost during regulatory review, capped at a total of 14 years post-approval.

The quid pro quo looked balanced on paper. The reality has diverged substantially. A study published in the Yale Law and Policy Review found that 91% of drugs that obtained PTEs continued their monopolies past the extension’s expiration, primarily through secondary patents [13]. The “last-man-standing” protection — the final patent blocking generic entry — was provided by secondary patents for roughly 75% of drugs studied, directly contrary to Congress’s intent.

The average total monopoly period in that dataset was 18.9 years, with a maximum of 27.5 years — well beyond the 14-year ceiling Hatch-Waxman envisioned [13]. The consumer cost of that extended secondary patent protection averaged 7.8 years per drug, with an estimated aggregate cost to consumers of $53.6 billion from delayed generic competition [13].

For patent valuation purposes, this research has a specific and often overlooked implication: when projecting exclusivity timelines, analysts should not assume that the patent landscape is adequately described by the primary compound patent and the Orange Book-listed secondary patents. The full portfolio — including formulation patents, method-of-use patents, and process patents that may not be Orange Book-listed — determines actual competitive exclusivity.

Biosimilars: A Different Kind of Patent Problem

Biologics present patent valuation challenges that have no direct analog in small molecule pharmaceuticals. The molecules are dramatically more complex — large proteins, often glycosylated, produced in living cell systems — and the patents protecting them cover not just the molecular entity but manufacturing processes, formulations, and methods of use in a web that can be more difficult to navigate than a conventional small molecule thicket [17].

The regulatory pathway for biosimilar approval under the Biologics Price Competition and Innovation Act (BPCIA) is also more demanding than the ANDA pathway. Demonstrating biosimilarity requires extensive analytical, preclinical, and clinical studies. Development costs range from $100 million to $250 million [18]. For originator companies, this barrier provides a de facto extension of commercial exclusivity beyond what the formal patent landscape would suggest. <blockquote> ‘90% of biologics losing exclusivity over the next decade currently lack a biosimilar in development, representing a massive untapped opportunity for cost savings in U.S. healthcare.’ — Center for Biosimilars, 2025 [18] </blockquote>

That “biosimilar void” has real valuation consequences. Originator biologic patents that would otherwise generate robust exclusivity assumptions face weaker competitive pressure than equivalent small molecule patents — good for originator valuations, but a systemic failure from a healthcare cost perspective.

The payer and reimbursement landscape compounds the problem. Even when biosimilars reach market, originator strategies — rebate walls, patient assistance programs, and active efforts to maintain formulary exclusivity — reduce biosimilar uptake below what patent expiration alone would predict. Biosimilar market share after 2 years in the US has historically been lower than biosimilar share in European markets by a substantial margin, partly because European payer systems are more aggressive about biosimilar adoption. US-based biosimilar valuations need to model this slower market share capture explicitly.

Part Six: Patent Litigation as a Valuation Input

The Baseline Statistics

Pharmaceutical patent litigation is not an edge case — it is routine. Pharmaceutical patents accounted for 18% of all patent litigation cases in 2023 [21]. Cases grew 12% year-over-year as competitive pressure and the financial stakes of blockbuster patent protection intensified.

The economics of pharmaceutical patent litigation are substantial. The average cost through trial reached $3 million in 2023, with complex pharmaceutical cases often exceeding that figure significantly [21]. The median time to trial was 24.5 months [21]. These facts shape litigation strategy: 40% of cases settle before trial, reflecting the preference to avoid prolonged uncertainty rather than any particular view of case merits [21].

Damages in pharmaceutical cases reflect the patent’s commercial importance. The pharmaceutical industry accounted for 25% of total patent damages awarded in 2023 [22]. Median awards reached $8.7 million; the average hit $24.4 million, pulled up by a handful of very large awards including one that exceeded $2 billion [22]. Royalty-based damages were the most common structure, representing 60% of total awards [22].

These figures feed directly into patent valuation in two ways. First, the potential damages recoverable in a successful infringement suit represent a component of the patent’s value — the “enforcement premium” available to a holder who is willing to litigate. Second, the cost and risk of defending against an infringement suit affect the value of a patent from the perspective of a potential infringer, and therefore inform licensing negotiations.

IPR Petitions: The Strategic Validity Challenge

Inter Partes Review allows patent challengers to contest validity at PTAB without the expense of full district court litigation. With over 1,500 IPR petitions filed in 2023 and a 70% success rate for petitioners in achieving claim cancellation or limitation [21], IPRs have become the generic industry’s primary tool for clearing patent thickets.

For originators, an IPR petition against a key patent is an existential commercial threat that needs to be incorporated into patent valuation. A patent facing an active IPR petition has materially lower expected value than an unchallenged patent, even before PTAB rules. The patent’s market exclusivity contribution should be probability-weighted against the outcome of the proceeding.

For generic and biosimilar companies evaluating market entry opportunities, IPR is both a risk-clearing tool and a cost center. The decision to file an IPR, challenge in district court, or pursue licensing rather than litigation depends on a cost-benefit analysis that requires patent value assessment on both sides. The expected value of successfully invalidating an originator’s key formulation patent — enabling generic entry years earlier than planned — can easily justify a multi-million dollar IPR campaign.

DrugPatentWatch provides comprehensive litigation coverage that enables this analysis, including district court and PTAB case data integrated with patent and drug information. That integration is what makes it possible to assess litigation exposure at the drug level rather than purely at the patent level — a critical distinction for drugs protected by thickets of patents that any generic entrant must navigate simultaneously.

Part Seven: Emerging Tools Reshaping Valuation Practice

AI and Machine Learning: What They Actually Do Well

Artificial intelligence is changing pharmaceutical patent analysis in specific, concrete ways — not through magic, but through the ability to process volumes of data that would take human analysts weeks or months [27].

Citation network analysis is one clear application. AI can identify foundational patents within a citation network, flag patents with unusually high forward citation velocity (suggesting they are gaining influence faster than peers), and cluster patents by technological proximity. These capabilities let analysts prioritize which patents in a large portfolio deserve deep qualitative analysis rather than applying that depth uniformly to thousands of filings.

Prosecution history analysis offers a second concrete application. Natural language processing tools can read the exchanges between applicants and examiners and flag amendments that narrowed claim scope in response to prior art rejections. This analysis informs enforceability assessments — a patent that made significant concessions during prosecution may have weaker claims than its current language suggests, due to prosecution history estoppel.

Predictive modeling for litigation outcomes and IPR success rates represents a third area. Machine learning models trained on historical PTAB and district court outcomes, calibrated against patent characteristics and claim features, can generate probability estimates for litigation outcomes. These probabilities belong in rNPV models for patents facing active or probable legal challenges [27].

Tools like IPRally and DeepIP represent the commercial implementation of these capabilities [28, 29]. IPRally uses graph-based AI to enable precise patent searches and portfolio analysis, helping analysts navigate large datasets efficiently. DeepIP focuses on patent drafting and prosecution support, using generative AI to help practitioners produce better-quality patents from the start — with claim scope that survives prosecution.

The honest qualification: AI tools augment rather than replace expert judgment. They accelerate data processing and surface patterns. They do not substitute for the clinical or technical expertise needed to assess whether a claimed compound mechanism is genuinely novel, or the legal judgment needed to evaluate claim scope against specific prior art. Patent valuation remains a human discipline aided by AI, not an AI discipline.

Blockchain for IP Management

Blockchain’s theoretical applications in patent management center on two capabilities: immutable timestamping and automated execution through smart contracts [30, 31].

Immutable timestamping matters for establishing priority dates — a critical legal element in patent disputes. If an invention disclosure, laboratory notebook entry, or provisional application filing can be time-stamped on a blockchain with cryptographic proof of non-alteration, that record becomes nearly impossible to dispute. For industries where priority dates determine who gets the patent, this is not a trivial improvement.

Smart contracts offer the possibility of automated royalty payments triggered by license conditions: sales thresholds, milestone achievement, territory penetration. This would reduce administrative friction in licensing relationships and potentially open up more granular, performance-linked royalty structures. The technology is not yet widely deployed in pharmaceutical licensing — standard licensing agreements are complex enough that full automation remains aspirational — but the direction of travel is clear [30, 31].

ESG Integration: Green Patents and Valuation Effects

ESG considerations have reached pharmaceutical patent valuation through two channels. The first is reputational: companies with strong ESG profiles — including transparent pricing, access commitments, and environmental manufacturing practices — attract a growing pool of ESG-oriented investors who price that profile into equity valuations. Patents that underpin products with clear access problems (aggressive pricing on life-saving drugs, active litigation against generic manufacturers in low-income markets) represent reputational liabilities as much as financial assets.

The second channel is more specific to green innovation. Research shows that patent production related to environmentally friendly technologies has risen sharply alongside ESG investment flows [36, 37]. Valuing green patents requires integrating regulatory sensitivity — these patents are highly dependent on government policy for their commercial relevance — alongside the standard income approach. A patent on a novel manufacturing process that reduces a biologic’s carbon footprint may have minimal standalone commercial value but significant strategic value if carbon pricing or regulatory pressure makes that efficiency necessary for operating licenses [38].

Part Eight: Putting It Together — Building an Actionable Patent Valuation Framework

Start With What the Data Tells You

An effective patent valuation process begins with the objective indicators available in public databases: forward citation counts, family size, claim count, IPC breadth, prosecution duration, and litigation history. Platforms like DrugPatentWatch consolidate the pharmaceutical-specific layer of this information — Orange Book listings, paragraph IV certifications, PTAB case status, clinical trial status, and international patent data including Supplementary Protection Certificates — into a single integrated view.

These objective signals are screening tools. They identify which patents in a large portfolio warrant deeper analysis and which can be efficiently de-prioritized. A patent with zero forward citations, a two-country family, narrow claim scope, and a clean prosecution history that has never been challenged is almost certainly not a high-value asset. A patent with 200 forward citations, a 30-country family, broad independent claims, and one survived IPR challenge is a candidate for deep valuation work.

Layer in Qualitative Expert Analysis

Once the quantitative screen identifies the material assets, qualitative assessment drives the valuation. This requires technical experts to evaluate inventive step and design-around difficulty, legal experts to assess claim scope and prosecution history estoppel, and commercial analysts to stress-test revenue projections against competitive and regulatory scenarios.

The qualitative assessment should answer four specific questions: How genuinely novel is the claimed technology? How hard is it for a competitor to achieve the same clinical outcome without infringement? What is the realistic competitive landscape at the time of likely generic entry? And what is the probability that this patent’s key claims survive challenge at PTAB?

The answers to those questions inform the inputs to the financial model — discount rates, probability weightings, revenue trajectories, and terminal values — far more directly than any single quantitative metric.

Model the Full Exclusivity Landscape, Not Just the Primary Patent

For pharmaceutical assets, single-patent valuation is rarely the right unit of analysis. What matters commercially is the effective exclusivity period — the span from now until the first generic or biosimilar with realistic market prospects can enter without infringing anything in the portfolio.

Mapping that landscape requires identifying every patent in the Orange Book listing for the drug, every related patent in the portfolio that could be asserted against generic entry, the current legal status of each, and the realistic outcome of each potential challenge. This is precisely the analysis that DrugPatentWatch enables at scale — not just for a company’s own portfolio but for competitors’ portfolios as part of competitive intelligence or due diligence.

The effective exclusivity period — derived from the full patent landscape rather than just the primary compound patent — is the input that drives the commercial valuation. Two drugs with the same primary patent expiry date may have effective exclusivity periods that differ by five years or more, depending on secondary patent coverage and vulnerability to challenge.

Price the Litigation Risk Explicitly

Any pharmaceutical patent valuation that does not explicitly price litigation probability is incomplete. For drugs with revenue above roughly $500 million annually, the probability of at least one paragraph IV filing — and the resulting litigation — is close to 100%. For drugs in the $100 million to $500 million range, the probability is substantial. Generic manufacturers, particularly the larger ones operating with sophisticated IP analysis capabilities, monitor the patent landscape continuously and file Paragraph IV certifications strategically.

Litigation risk should appear in the valuation as an expected value adjustment: the probability of a successful challenge multiplied by the value reduction from early generic entry, discounted to present value. For a drug generating $1 billion annually, even a 20% probability of generic entry three years early represents hundreds of millions of dollars of expected value reduction that should be reflected in any rigorous patent valuation.

Part Nine: The Competitive Intelligence Application

Patent valuation is not just an internal discipline — it is a competitive intelligence tool. Understanding the value and vulnerability of a competitor’s patent portfolio is as strategically important as understanding your own.

Reading Competitor Portfolios

The same indicators that signal your patents’ value also reveal your competitors’ exposure. A competitor drug protected primarily by formulation patents — with a compound patent that expired years ago — is vulnerable to challenge in ways that a drug protected by broad, valid composition-of-matter claims is not. Patent family size and forward citation data for competitor portfolios are publicly available. Forward citation counts, prosecution histories, IPC breadth, and PTAB petition histories are extractable and analyzable.

For generic and biosimilar companies, this analysis is the core of market entry strategy. The decision of which brand drugs to pursue, and when, depends directly on an assessment of the brand’s patent vulnerability. A drug generating $2 billion annually with a primary compound patent expired, one secondary formulation patent that has already survived one IPR petition, and a large patent family in 25 countries is a categorically different entry opportunity than a drug generating $2 billion annually with a valid, unchallenged composition-of-matter patent with seven years of remaining term.

Licensing Negotiations and Third-Party Royalty Rate Setting

When a company is entering into a licensing negotiation — either as licensor or licensee — an objective patent valuation is the foundation of a credible negotiating position. Without it, the negotiation defaults to leverage: who needs the deal more. With it, both parties can anchor to a defensible economic framework.

The relief-from-royalty method, calibrated against comparable licensing transactions where available, provides a market-anchored starting point for royalty rate negotiations. Adjustments for relative patent strength — claim scope, litigation history, design-around difficulty — move the rate up or down from that baseline. The qualitative indicators discussed above are the inputs to those adjustments.

Approximately 45% of pipeline assets at top pharmaceutical companies originate from external innovation through licensing and collaborations [20]. Every one of those transactions involves a negotiation over royalty rates, milestone payments, and licensing terms that implicitly reflects a valuation of the underlying patents. Companies that systematically build valuation capabilities — using platforms like DrugPatentWatch for objective data, combined with expert technical and legal analysis — negotiate from a more defensible position than those relying on intuition or precedent alone.

Conclusion

Patent value is determinable. It is not easy to determine, and it resists the temptation to reduce to a single metric. But it is not opaque. The indicators exist — forward citations, family size, claim scope, IPC breadth, prosecution history, litigation outcomes — and they carry meaningful predictive signal when used systematically alongside rigorous financial modeling and expert qualitative assessment.

What the pharmaceutical and biotechnology sectors require is not just familiarity with valuation methodology in the abstract. They require the discipline to apply that methodology to the industry’s specific risk profile: the clinical failure rates, the regulatory approval step changes, the secondary patent thickets that extend nominal exclusivity far beyond what primary patents would suggest, the biosimilar void leaving vast commercial territory uncontested, and the litigation economics that should appear explicitly in every revenue projection.

The companies that build this capability — that know which of their own patents are genuinely valuable and which are expensive maintenance liabilities, that can read competitor portfolios for vulnerability, and that can enter licensing negotiations with defensible numbers — will consistently outperform those treating IP as a legal function rather than a financial asset. The data is available. The frameworks exist. The constraint is the willingness to do the work.

Key Takeaways

Most drug patents have minimal commercial value. Research shows approximately 68% of patents are valued below €1 million. Portfolio management requires identifying the small fraction of high-value assets — not maximizing count.

The income approach, specifically risk-adjusted net present value (rNPV), is the primary tool for pharmaceutical patent valuation. It must explicitly incorporate clinical failure probabilities, regulatory approval risk, and post-loss-of-exclusivity revenue cliffs.

Effective exclusivity is not the same as nominal patent expiry. Secondary patent thickets — formulation, method-of-use, and process patents — routinely extend commercial exclusivity years beyond primary compound patent expiration. Only 91% of drugs that obtained patent term extensions continued their monopolies past those extensions by relying on secondary patents.

Humira’s 300+ patent portfolio, 94% filed post-approval, and Keytruda’s 129 applications (53 granted, majority post-approval) show how aggressively secondary patent strategies extend commercial exclusivity — and how much is at stake in patent valuation of those portfolios.

The Inflation Reduction Act’s Medicare price negotiation provisions have decoupled legal patent exclusivity from commercial exclusivity for high-revenue drugs selected for negotiation. Patent valuations for Medicare-relevant assets must reflect negotiated price risk as an explicit input.

The ‘biosimilar void’ — 90% of biologics losing exclusivity over the next decade with no biosimilar in development — materially elevates originator biologic patent values compared to what competitive dynamics alone would predict.

Forward citations are the single strongest quantitative predictor of patent value identified in the research literature. Patent family size, claim scope, and IPR survival history are the next most informative objective indicators.

AI tools are useful for citation network analysis, prosecution history screening, and litigation probability modeling. They do not replace technical or legal expert judgment on inventive step, design-around difficulty, or claim interpretation.

Platforms like DrugPatentWatch consolidate the data layers — Orange Book listings, PTAB cases, paragraph IV certifications, international patent coverage, clinical trial status — needed to assess effective exclusivity at the drug level rather than the individual patent level.

Patent valuation is a competitive intelligence discipline as much as an internal finance one. Reading competitor portfolios for vulnerability is as strategically important as assessing the strength of your own.

FAQ

Q1: If a pharmaceutical company’s primary compound patent has expired, should the drug still be treated as having valuable IP?

Not automatically, but often yes. The expiry of a compound patent is frequently not the end of effective IP protection — it may be the beginning of the secondary patent period. Method-of-use patents, formulation patents, and process patents filed years after initial approval can extend commercial exclusivity substantially. The first step in any answer to this question is mapping the full patent landscape for the drug, not just its primary patent status. A platform like DrugPatentWatch, with its Orange Book integration and paragraph IV certification data, provides the starting point for that landscape analysis. The answer depends entirely on the scope, validity, and legal status of every remaining patent — not just the headline compound patent.

Q2: How should a company value a patent on a drug that is being considered for Medicare price negotiation under the IRA?

This requires modeling two separate scenarios and probability-weighting them. In the non-negotiation scenario, project revenues under standard market dynamics. In the negotiation scenario, estimate the negotiated price (using the statutory maximum fair price calculations as a baseline, adjusted for the drug’s specific characteristics) and project revenues under that price. Weight each scenario by the probability of selection. For drugs that have already been identified as candidates — or that fall clearly into the statutory eligibility criteria — the negotiation probability approaches certainty and should be modeled as a near-certain scenario rather than a risk factor. The value reduction from negotiation for many blockbuster biologics is material — in some cases eliminating the revenue premium that justified original patent valuations.

Q3: What is the most common error in biosimilar patent landscape analysis?

Focusing only on the Orange Book listing and the formal ‘patent dance’ under the BPCIA, while missing the broader portfolio of process patents, formulation patents, and manufacturing patents that are not required to be listed but could still be asserted. Originator biologic companies often hold substantial manufacturing process IP that is not Orange Book-disclosed because it is not tied to a specific regulatory submission. A biosimilar entrant who has cleared all Orange Book-listed patents may still face infringement exposure from this shadow portfolio. Thorough biosimilar entry analysis requires searching the full assignee portfolio — not just the disclosed listings — and assessing the likelihood that process patents would survive challenge.

Q4: How do forward citations in pharmaceutical patents differ in significance from forward citations in, say, semiconductor patents?

The citation dynamics are similar in structure but different in the typical citation velocity and timeframe. Pharmaceutical patents tend to have longer citation lag periods — it takes more time for a new drug mechanism to propagate through subsequent patent filings than for a semiconductor process innovation to appear in downstream patents. This means that a pharmaceutical patent with strong forward citations accumulated over 5 years may be more foundational than a tech patent with the same count accumulated over 20 years. The comparison is most meaningful within the same technology domain and patent generation cohort. Cross-sector citation comparison requires careful normalization.

Q5: Can a patent’s value actually increase after a failed IPR petition?

Yes, and this is underappreciated. A patent that survives an IPR petition — particularly one where the petitioner presented the strongest available prior art — has been validated under adversarial conditions. The USPTO considered the best challenge the petitioner could mount and upheld the claims. That outcome makes the patent harder to attack in subsequent proceedings, either at PTAB (where the same prior art cannot be relitigated) or in district court. The practical effect is that survived-IPR patents often command higher licensing rates and are more defensible in infringement suits. For portfolio valuation purposes, a patent with a survived IPR is a categorically stronger asset than an equivalent unchallenged patent.

References

[1] World Intellectual Property Organization. (n.d.). What is a patent? https://www.wipo.int/en/web/patents

[2] World Intellectual Property Organization. (2009). To determine the contributions of patents to corporate success patents should be managed and valued. https://www.wipo.int/edocs/mdocs/sme/en/wipo_insme_smes_ge_10/wipo_insme_smes_ge_10_ref_theme06_01.pdf

[3] World Intellectual Property Organization. (n.d.). IP valuation. https://www.wipo.int/en/web/business/ip-valuation

[4] PatentPC. (n.d.). The role of patent valuation in strategic IP management. https://patentpc.com/blog/the-role-of-patent-valuation-in-strategic-ip-management

[5] Hall, A. (n.d.). Assessing strength of patent portfolios. https://aaronhall.com/assessing-strength-of-patent-portfolios/

[6] European Patent Office. (n.d.). What are good indicators of patent value? https://www.epo.org/en/service-support/faq/searching-patents/patent-management-and-valuation/what-are-good-indicators

[8] World Intellectual Property Organization. (2011). IP valuation of early stage technology. https://www.wipo.int/export/sites/www/dcea/en/meetings/2011/tt_belgrade/docs/Topic_13_IP_Valuation_of_Early_Stage_Technology_Spasic.pdf

[9] FasterCapital. (n.d.). A hybrid approach to valuation. https://fastercapital.com/content/A-Hybrid-Approach-to-Valuation.html

[10] PatentPC. (n.d.). Patent valuation in the pharmaceutical industry: Key considerations. https://patentpc.com/blog/patent-valuation-in-the-pharmaceutical-industry-key-considerations

[11] Arrowfish Consulting. (n.d.). How to value a biotechnology firm. https://www.arrowfishconsulting.com/how-to-value-biotechnology-firm/

[12] Yale Law and Policy Review. (n.d.). Patent term extensions and last man standing. https://yalelawandpolicy.org/patent-term-extensions-and-last-man-standing

[13] Bryn Mawr Scholarship Repository. (n.d.). The Hatch-Waxman Act. https://scholarship.tricolib.brynmawr.edu/bitstreams/0db6db1d-e2f1-4302-902e-973903a1dab5/download

[14] Wikipedia. (2025, May 29). Evergreening. https://en.wikipedia.org/wiki/Evergreening

[15] KENFOX IP & Law Office. (n.d.). Evergreening strategy: Extending patent protection — Innovation or obstruction? https://kenfoxlaw.com/evergreening-strategy-extending-patent-protection-innovation-or-obstruction

[16] Biosimilars Council. (2025, July 9). Patent thickets and litigation abuses hinder all biosimilars. https://biosimilarscouncil.org/news/patent-thickets-and-litigation-abuses-hinder-all-biosimilars/

[17] Center for Biosimilars. (2025, February 5). The biosimilar void: 90% of biologics coming off patent will lack biosimilars. https://www.centerforbiosimilars.com/view/the-biosimilar-void-90-of-biologics-coming-off-patent-will-lack-biosimilars

[18] GeneOnline News. (2025, April 14). Drug Patent Watch: Five key factors, including patent portfolio strength, determine pharma company valuation. https://www.geneonline.com/drug-patent-watch-five-key-factors-including-patent-portfolio-strength-determine-pharma-company-valuation/

[19] PatentPC. (n.d.). Patent litigation statistics: An overview of recent trends. https://patentpc.com/blog/patent-litigation-statistics-an-overview-of-recent-trends

[20] PatentPC. (n.d.). Patent damages statistics: What innovators should know. https://patentpc.com/blog/patent-damages-statistics-what-innovators-should-know

[21] CSRxP. (n.d.). Fact sheet: Big Pharma’s patent abuse costs American patients, taxpayers, and the U.S. health care system billions of dollars. https://www.csrxp.org/fact-sheet-big-pharmas-patent-abuse-costs-american-patients-taxpayers-and-the-u-s-health-care-system-billions-of-dollars-2/

[22] DrugPatentWatch. (2024, July 27). The top 10 longest-running drug patents. https://www.drugpatentwatch.com/blog/the-top-10-longest-running-drug-patents/

[23] PatentPC. (n.d.). How to leverage AI in patent valuation. https://patentpc.com/blog/how-to-leverage-ai-in-patent-valuation

[24] DeepIP. (n.d.). DeepIP — Better and faster patents with Gen AI. https://www.deepip.ai/

[25] IPRally. (n.d.). IPRally: AI patent search, review and classification. https://www.iprally.com/

[26] ETB Law. (n.d.). What is blockchain IP? Benefits and applications explained. https://www.etblaw.com/what-is-blockchain-ip/

[27] Financial Crime Academy. (n.d.). Blockchain and intellectual property. https://financialcrimeacademy.org/blockchain-and-intellectual-property/

[28] Rödl & Partner. (2024, December 12). The role of ESG factors in business valuation. https://www.roedl.com/insights/tax-newsletter-italien/2024-11/role-esg-factors-business-valuation

[29] UN Principles for Responsible Investment. (n.d.). The ESG innovation disconnect: Evidence from green patenting. https://www.unpri.org/pri-blog/the-esg-innovation-disconnect-evidence-from-green-patenting/7219.article

[30] PatentPC. (n.d.). How to value patents in the renewable energy sector. https://patentpc.com/blog/how-to-value-patents-in-the-renewable-energy-sector

[31] PowerPatent. (n.d.). Valuation of climate change and environmental patents. https://powerpatent.com/blog/valuation-of-climate-change-and-environmental-patents/