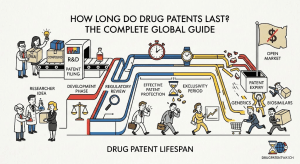

Drug companies don’t make drugs. They make time. Patents are the mechanism by which a pharmaceutical firm converts a decade of laboratory failures, clinical trial costs, and regulatory risk into a window of exclusivity that must generate enough revenue to fund the next ten years of failures. Get the timing right, and you have a blockbuster franchise. Miss it, or misread it, and generics arrive before you have covered your sunk costs.

Yet the question “how long does a drug patent last?” does not have a simple answer. The textbook response — 20 years from the filing date — is technically correct and practically misleading. By the time a drug reaches pharmacy shelves, the clock has usually been running for eight to twelve years. That leaves somewhere between eight and twelve years of effective protection. Extensions, exclusivities, and challenges can add or subtract years from that window in ways that shift billions of dollars between innovators, generic manufacturers, insurers, and patients.

This guide explains the full system: how patents are filed, how they are extended, how they expire, and how they vary across the world’s major pharmaceutical markets. It covers the difference between patent protection and regulatory exclusivity, the tactics companies use to stretch their monopolies, the tools investors and analysts use to track expiry dates, and the implications of all of this for drug pricing and market access globally.

Whether you are a biotech investor, a health policy analyst, a generic drug company evaluating entry timing, or a hospital procurement officer trying to forecast budget exposure, understanding drug patent duration is the closest thing this industry has to reading a balance sheet.

Part One: The Foundations

What a Drug Patent Actually Protects

Before counting years, you need to understand what you are counting from. A pharmaceutical company does not file a single patent on a drug. It typically files dozens, sometimes hundreds, covering different aspects of the same molecule and its commercial application. Each has its own filing date, its own expiry date, and its own vulnerability to legal challenge.

Composition of Matter Patents

The composition of matter patent is the crown jewel. It covers the active ingredient itself — the specific chemical compound or biological molecule that produces the therapeutic effect. This is the most powerful patent type because it is the broadest: no competitor can make, sell, or use that molecule anywhere in the jurisdiction for the life of the patent, regardless of what indication they are pursuing or what formulation they use.

Because composition of matter patents are filed early in the development process — often during preclinical research, before the company knows which indication or formulation will succeed — they also tend to have the most time ticking off the clock before the drug reaches patients. A company that files a composition of matter patent in 2010 and receives FDA approval in 2022 has already consumed twelve years of a twenty-year term. The effective remaining protection is eight years, unless an extension is granted.

When a composition of matter patent expires, it is usually the single event that triggers the most aggressive generic entry. It is the cliff the industry talks about. Everything else is the slope leading up to it.

Method of Use Patents

A method of use patent covers a specific application of a compound — treating a particular disease, at a particular dose, by a particular route. These patents are narrower than composition of matter patents but strategically valuable. They allow a company to protect new uses discovered after the original patent was filed, or to create legal complications for generic companies seeking to launch for specific indications.

The tactic known as “skinny labeling” is a direct response to method of use patents. Generic manufacturers seeking to launch before a method of use patent expires can carve that indication out of their approved label, limiting their product to the uses they are free to practice. Courts have repeatedly wrestled with whether a generic that markets a product for its approved uses induces infringement of a method of use patent when doctors prescribe it for the carved-out indication. The answer, depending on jurisdiction and specifics, is sometimes yes.

Formulation and Delivery Patents

Once a company knows a molecule works, its next job is to make it work reliably in a patient’s body. That requires solving problems: the molecule might be unstable, poorly absorbed, metabolized too quickly, or painful to administer. The solutions — specific salt forms, extended-release formulations, nanoparticle delivery systems, transdermal patches, fixed-dose combinations — are all patentable.

Formulation patents are frequently filed years after the composition of matter patent, which means they expire years later. A drug with a composition of matter patent expiring in 2026 might have a controlled-release formulation patent expiring in 2031 and a combination product patent expiring in 2034. Generic companies can launch the immediate-release form on the earlier date but face ongoing litigation risk over the later-expiring patents until they invalidate them or design around them.

Process Patents

Process patents cover the manufacturing method used to synthesize the active ingredient. They are less visible than the other categories but commercially significant because they can prevent a generic company from using the most efficient synthesis route even after the composition of matter patent has expired. In practice, experienced generic manufacturers develop alternative synthesis routes, but this adds cost and complexity that can delay launch.

Process patents also matter acutely in biologics, where the manufacturing process and the product are nearly inseparable. Two companies following different manufacturing processes for the same biologic antibody can end up with products that are similar but not identical, which has significant regulatory and legal implications explored in the biologics section of this guide.

The Standard 20-Year Term: What the Clock Actually Measures

The 20-year patent term is the baseline established under the Agreement on Trade-Related Aspects of Intellectual Property Rights (TRIPS), which the World Trade Organization administers and which all 164 WTO member states are required to implement [1]. Before TRIPS came into force in 1995, patent terms varied significantly by country — the United States, for instance, used a 17-year term measured from the grant date rather than the filing date.

Filing Date vs. Priority Date

The 20-year clock starts at the filing date of the patent application, not the date of invention and not the date the patent is granted. For most patents, the relevant filing date is the date of the earliest application to which the patent claims priority.

This creates an important distinction. A company that files a provisional patent application in the United States in January 2020, then files a full PCT (Patent Cooperation Treaty) application in January 2021 claiming priority to that provisional, will have a patent that expires in January 2041 — 20 years from the PCT filing date. The provisional does not start the clock in the same way, but it establishes the priority date that determines what prior art can be used against the patent.

Priority date management is a significant part of pharmaceutical patent strategy. Companies file early to secure priority against competitors but must balance this against how much useful patent life will survive the development and approval process.

Why the Filing Date Creates a Structural Problem for Drug Patents

In most industries, the gap between a patent filing and the product reaching market is measured in months or at most a couple of years. A consumer electronics company might file a patent on a new chip architecture in March and have a product incorporating it on sale by October. The effective commercial life of that patent is nearly the full 20 years.

Drug development does not work this way. From the filing of a composition of matter patent to FDA approval, the average time has historically run between ten and thirteen years [2]. That is ten to thirteen years of the 20-year term consumed before a single prescription is written. The remainder — seven to ten years — is the window in which the company must recoup its investment, which the Tufts Center for the Study of Drug Development has estimated at over $2.5 billion per approved drug when accounting for the cost of failures [3].

This is not an accident of the regulatory system. It reflects the genuine scientific and safety requirements of drug development: years of animal studies, phase I safety trials, phase II dose-finding studies, phase III efficacy and safety trials, and a regulatory review process that can itself take one to two years. Each step is necessary. Each step also consumes patent life.

The structural mismatch between when pharmaceutical patents are filed and when the products they protect reach market is the reason patent term extension systems were created.

Patent Term Extensions: How Companies Buy More Time

Every major pharmaceutical market operates some form of patent term extension or supplementary protection system specifically designed to compensate innovators for the regulatory review time consumed before approval. These systems represent a deliberate policy choice: without them, the effective market exclusivity available to pharmaceutical innovators would be so short that the financial model for risky, long-development drugs would collapse. With them, companies can recover five or more additional years of exclusivity, which in the case of a blockbuster drug can be worth billions of dollars per year.

Hatch-Waxman and Patent Term Restoration in the United States

The Drug Price Competition and Patent Term Restoration Act of 1984, universally known as the Hatch-Waxman Act, is the foundational piece of legislation governing both generic drug entry and patent term extension in the United States [4]. It created two parallel systems in one statute, balancing the interests of innovators (who wanted longer effective exclusivity) against the interests of generic manufacturers (who wanted a streamlined pathway to market).

The patent term restoration provision of Hatch-Waxman allows the holder of a patent covering an approved drug to apply to the USPTO for an extension of up to five additional years. The extension compensates for time spent in regulatory review — defined as the period from the date the IND application was submitted to the date of NDA approval. Half of the IND phase time is recoverable (up to two years), and all of the NDA review time is recoverable.

The total extended term cannot exceed 14 years of effective protection from the date of first approval, and the extension applies to only one patent per product. This last restriction is critical: a company with dozens of patents covering a single drug must choose which one to extend, usually the composition of matter patent with the most remaining term. The other patents expire on their natural schedule.

The maximum possible extension under Hatch-Waxman is five years. In practice, the average extension granted has been around three years, because the regulatory timeline does not always produce the maximum [5].

To claim the extension, the applicant must file within 60 days of FDA approval. Late filings forfeit the right entirely, which has happened at least once with commercially significant consequences. The USPTO then calculates the extension period and issues a certificate.

Supplementary Protection Certificates in the European Union

The European Union uses a different mechanism called the Supplementary Protection Certificate (SPC). Rather than extending the original patent, an SPC is a separate intellectual property right that takes effect when the patent expires and provides up to five additional years of exclusivity [6]. An additional six months is available if pediatric studies have been conducted under the EU pediatric regulation.

SPCs are granted by national patent offices in each EU member state, based on the date of the first marketing authorization in the EU. The formula for calculating SPC duration is the time between the date of the patent application and the date of the first EU marketing authorization, minus five years, with a cap of five years total and a minimum SPC term of zero (i.e., if approval came less than five years after filing, no SPC is granted).

Because marketing authorizations may be granted on different dates in different EU member states, and because SPCs are national rights, the SPC landscape across the EU can be genuinely complex. A drug might have an SPC in Germany expiring in December 2028 and an SPC in France expiring in February 2029 due to differences in national application processing and authorization dates.

The European Court of Justice has issued dozens of rulings on SPC eligibility over the past two decades, many of them addressing the question of whether a product “is protected by a basic patent in force” — the foundational requirement for SPC eligibility under Regulation (EC) No 469/2009. The rulings on combination products, metabolites, and products covered by Markush claims have progressively narrowed SPC eligibility in ways that have cost innovators significant commercial value.

Patent Term Extensions in Japan

Japan grants patent term extensions for pharmaceutical products through its Patent Act, allowing extensions of up to five years when regulatory review has delayed commercialization. Japan’s system is notable for permitting multiple extensions for the same patent covering the same product when new indications receive approval, provided the regulatory review time for each new indication is distinct. This approach differs from the United States and EU systems, which generally limit extensions to a single product per patent.

Japan’s Pharmaceuticals and Medical Devices Agency (PMDA) has among the most rigorous regulatory processes in the world, with review timelines that have historically been longer than FDA or EMA timelines. This has meant that Japanese patent term extensions have often hit the five-year ceiling. Reforms aimed at accelerating PMDA review in recent years have begun to compress this timeline, which may reduce extension lengths for drugs approved going forward.

Patent Extensions in Canada, Australia, and Other Markets

Canada historically offered no patent term extension specifically for pharmaceuticals, leaving innovators with whatever natural patent life remained after regulatory approval. Canadian patent law reform under the Canada-United States-Mexico Agreement (CUSMA) changed this, introducing a certificate of supplementary protection system that came into force in September 2017 and allows extensions of up to two years — shorter than the five-year maximum available in the United States and EU [7].

Australia introduced patent term extensions for pharmaceutical substances in 1999, permitting a maximum extension of five years subject to a 15-year cap on effective protection from the first regulatory approval date. The Australian system is administered by IP Australia and has generated its own body of case law on questions such as what constitutes a “pharmaceutical substance per se” eligible for extension.

The Real Effective Patent Life: What Survives Approval

Statistics on patent term extensions can create the impression that pharmaceutical companies routinely enjoy the full maximum protection available. The reality is messier.

Average Drug Development Timeline by Phase

Drug development follows a roughly predictable structure, though the timeline varies enormously by therapeutic area, molecule type, and development strategy. Breaking down the phases:

Preclinical research typically runs two to four years before an IND application is filed. Phase I clinical trials (safety and dose-finding, small numbers of healthy volunteers or patients) usually run one to two years. Phase II trials (proof of concept, dose selection, typically 100-500 patients) run two to three years. Phase III trials (pivotal efficacy and safety, typically 1,000-10,000 patients) run three to five years. NDA or BLA submission to approval typically takes one to two years, though priority review and breakthrough therapy designation can compress this.

The sum of these phases, from IND to approval, averaged 8.9 years across all approvals between 2010 and 2019 according to an analysis published in the Journal of Health Economics, with considerable variation by therapeutic area [8]. Oncology drugs frequently had shorter development timelines (benefiting from accelerated approval pathways) while cardiovascular and metabolic disease drugs tended to run longer.

How Much Patent Life Typically Survives to Approval

A composition of matter patent filed during or shortly after the discovery phase — typically two to three years before the IND — and subject to an average IND-to-approval timeline of roughly nine years would have consumed approximately twelve years of its 20-year term by the time of approval. That leaves eight years of remaining natural patent life.

With a Hatch-Waxman extension (average of approximately three years), effective protection extends to roughly eleven years post-approval. With the maximum five-year extension and a shorter-than-average development timeline, effective protection might reach fourteen years. With a standard development timeline and no extension (for instance, if the company missed the filing window or the patent is not eligible), effective protection drops to eight years or less.

According to data compiled by the Congressional Budget Office, the mean effective patent life for drugs approved in the 1990s and 2000s was approximately 11.5 years after approval [9]. More recent data from DrugPatentWatch shows that for new molecular entities approved between 2015 and 2022, the median time from approval to first patent expiry (excluding the composition of matter patent where still in term) ranged widely, but the composition of matter patent extension typically provided between 10 and 13 years of post-approval exclusivity.

The range matters enormously for revenue. A drug with $3 billion in annual peak sales and ten years of exclusivity generates $30 billion in cumulative revenue before generic entry. The same drug with fourteen years generates $42 billion. The difference — $12 billion — is the financial value of four years of extension.

Regulatory Exclusivity: The Other Clock

Patent protection and regulatory exclusivity are two distinct and separately governed systems that often operate in parallel. Confusing them is a common mistake, particularly among non-specialists. Patents are granted by patent offices under intellectual property law. Regulatory exclusivities are granted by drug regulatory agencies under pharmaceutical law. They can overlap, reinforce each other, or operate independently.

New Chemical Entity Exclusivity in the United States

When the FDA approves a new chemical entity (NCE) — a drug with an active moiety never previously approved in any form — the agency grants five years of data exclusivity during which no generic manufacturer can submit an Abbreviated New Drug Application (ANDA) relying on the innovator’s safety and efficacy data [10]. This exclusivity runs regardless of patent status. Even if a composition of matter patent had only three years remaining at the time of approval, the NCE exclusivity would extend the effective period of generic entry protection to five years from approval.

The flip side is also true: if patents expire before the five-year NCE exclusivity period ends, the NCE exclusivity continues to block generic entry. This is relatively rare but does occur, particularly for products where composition of matter patents were filed late in development.

After four years of the five-year NCE exclusivity period, generic companies are permitted to file a Paragraph IV certification (challenging patents) even though they cannot receive approval until the five-year period ends. This rule creates a complex interaction: generic companies routinely begin the Paragraph IV litigation process during the exclusivity period so that if they win, they can launch immediately upon exclusivity expiry.

Three-Year Exclusivity for New Clinical Investigations

Beyond NCE exclusivity, the Hatch-Waxman Act grants three years of exclusivity for drugs that required the submission of new clinical investigations (other than bioavailability studies) essential to the approval. This covers new formulations, new combinations, new indications, and new uses that were approved based on new clinical data.

Three-year exclusivity does not block the filing of ANDAs — only their approval. It also does not prevent approval of ANDAs for the original indication or formulation if those are no longer protected. This form of exclusivity is primarily a tool for extending protection on specific product innovations rather than the core molecule itself.

Biologics Data Exclusivity: Twelve Years in the United States

For biological products approved under the Biologics License Application (BLA) pathway, the Biologics Price Competition and Innovation Act of 2009 (BPCIA), part of the Affordable Care Act, established a twelve-year period of reference product exclusivity [11]. During this period, no biosimilar application can be approved using data from the reference biological product.

Twelve years of data exclusivity for biologics, compared to five years for small-molecule drugs, reflects the greater complexity of biologics development and the higher cost of creating biosimilars compared to conventional generics. However, the policy has been controversial. Critics, including the Obama and Biden administrations, have argued that twelve years is excessive and that reducing it to seven years (as proposed in multiple budget proposals) would save the federal government tens of billions of dollars over a decade.

The twelve-year clock starts from the date of first licensure of the reference product, not from any patent filing date. A biologic with strong patents might enjoy protection well beyond twelve years through patent exclusivity, but one whose patents are successfully challenged or invalidated cannot fall back on data exclusivity past the twelve-year mark.

European Data Exclusivity: The 8+2+1 System

The European Union’s data exclusivity system for pharmaceuticals is structured differently from the US system. Under the 8+2+1 framework: the innovator’s dossier is protected for 8 years from first approval (during which generic applications referencing the data cannot be filed), followed by 2 years during which generics can be approved but not yet marketed, with an additional 1 year of market protection available if the innovator obtained approval for a new indication with significant clinical benefit during the first 8 years [12].

The practical effect is 10 years of market exclusivity from the date of first European approval, extendable to 11 years. This runs separately from patent protection. For products with expired patents but ongoing data exclusivity, the data exclusivity is the effective barrier to generic market entry.

Pediatric Exclusivity and Orphan Drug Protection

Beyond the standard extension and exclusivity systems, two specialized categories of protection can materially alter a drug’s patent and exclusivity timeline: pediatric exclusivity and orphan drug designation.

Pediatric Exclusivity: Six Months That Move Markets

The FDA’s pediatric exclusivity provision, established under the Best Pharmaceuticals for Children Act and subsequently made permanent, grants six months of additional exclusivity to any holder of an existing patent or regulatory exclusivity who conducts pediatric studies in response to an FDA written request [13].

The six months attaches to all existing patents and exclusivities, not just the one that is longest. If a drug has three separate patents and an NCE exclusivity all expiring on different dates, each of those dates is pushed back by six months when pediatric exclusivity is earned.

For a drug generating $5 billion in annual sales, six months of additional exclusivity is worth roughly $2.5 billion in revenue. This is why companies almost always conduct pediatric studies when requested, regardless of whether their drug has any realistic pediatric use case. The FDA’s written request process was designed to incentivize pediatric research, and the exclusivity reward has proven effective enough that critics periodically question whether the reward is too large relative to the cost of the studies required.

The European equivalent — a six-month SPC extension for pediatric studies under Regulation (EC) No 1901/2006 — functions similarly, attaching to the SPC rather than to underlying patents.

Orphan Drug Designation: Seven Years of Exclusivity in the United States

Drugs approved for rare diseases affecting fewer than 200,000 people in the United States can qualify for orphan drug designation, which carries seven years of market exclusivity for that indication from the date of approval [14]. During this period, the FDA will not approve a competitor’s application for the same drug in the same indication, with narrow exceptions for clinical superiority.

Orphan drug exclusivity is distinct from patent protection and operates independently. A company can hold orphan drug exclusivity for an indication even after all its patents have expired. It can also hold orphan drug exclusivity while its patents are being challenged in litigation, and the exclusivity will continue regardless of the patent litigation outcome.

The strategic implications are significant. Companies frequently seek orphan drug designation for rare disease applications of existing drugs precisely because the seven-year exclusivity term provides robust protection even in the absence of strong patents. The drug Gleevec (imatinib) for gastrointestinal stromal tumors is a well-documented example of orphan drug exclusivity extending effective market protection beyond what the underlying patents provided for that particular indication.

The EU orphan drug system works similarly, granting ten years of market exclusivity for orphan medicines, extendable to twelve years if pediatric data requirements are met.

Global Patent Landscapes: Country-by-Country

The 20-year TRIPS standard creates a floor, not a ceiling, and the systems built on top of it vary enough to matter commercially. A pharmaceutical company launching globally cannot assume that patent expiry in the United States means simultaneous generic competition in all other markets. Patent prosecution timelines, extension systems, legal enforcement quality, and compulsory licensing policies all differ enough to create a genuinely complex global picture.

United States

The United States patent system is administered by the USPTO and is among the most transparent and well-documented in the world. The FDA’s Orange Book (formally, “Approved Drug Products with Therapeutic Equivalence Evaluations”) lists patents that cover approved drugs along with their expiry dates, and it is publicly searchable. Every patent listed in the Orange Book for an approved NDA is a potential target for a Paragraph IV challenge.

The US system’s defining feature is the Hatch-Waxman framework, which simultaneously makes generic entry faster (through the ANDA pathway and 30-month stay mechanism) and creates litigation risk for generic filers (through Paragraph IV challenges). The 30-month automatic stay of ANDA approval that triggers when an innovator sues on a Paragraph IV certification means that even a fully invalid patent can delay generic entry by 30 months after the ANDA filing. This delay has real financial value to innovators and has generated a litigation industry of its own.

The United States does not permit compulsory licensing of pharmaceutical patents under normal circumstances, and the political barriers to invoking such measures are substantial. This distinguishes it from many other markets.

European Union

The EU patent landscape is split between national patent rights and, increasingly, the Unitary Patent system that began operation in June 2023. Before the Unitary Patent, a European Patent granted by the EPO had to be validated in each national market separately, creating a patchwork of national patents with potentially different expiry dates (due to SPC variations) and different enforcement records. The Unitary Patent provides a single patent valid across all participating EU member states (currently 17, with more joining) administered through the Unified Patent Court (UPC).

For pharmaceutical companies, the UPC is a double-edged sword. A favorable ruling is valid across all participating states. So is an unfavorable one. A successful invalidity challenge at the UPC could strip patent protection across the entire EU participating territory simultaneously — a risk that has led some patent holders to opt out their most valuable patents from the UPC jurisdiction during the transitional period.

EMA marketing authorization granted through the centralized procedure applies EU-wide, which means first approval date for SPC purposes is consistent across member states for centrally approved drugs, reducing one source of complexity.

Japan

Japan is the third-largest pharmaceutical market globally and its patent system is administered by the Japan Patent Office (JPO). As noted above, Japan permits multiple patent term extensions for the same patent covering different indications, which is unique among major markets. The maximum single extension is five years, but successive extensions for new indications can accumulate.

Japan’s system also includes a “re-examination” period for new pharmaceuticals — a data protection regime that provides six years of protection for new chemical entities and four years for new indications, during which generic applications based on the original data cannot be approved. This runs separately from patent protection.

The PMDA approval process has historically been slower than the FDA or EMA, though the agency has made significant strides under various reform programs. “Drug lag” — the delay between approval in the US or EU and approval in Japan — has narrowed considerably for priority products but remains a factor for some drug classes.

China

China’s pharmaceutical patent landscape has undergone dramatic transformation since the country joined the WTO in 2001 and committed to TRIPS compliance. The CNIPA (China National Intellectual Property Administration) administers patents, and China now grants patent term extensions of up to five years for pharmaceutical products where regulatory review delayed commercialization, a system formalized in the 2020 amendments to China’s Patent Law [15].

China also introduced a pharmaceutical linkage system in 2021 that creates a formal connection between drug approvals and patent status, modeled partly on the US Orange Book/Hatch-Waxman system. Generic applicants must certify the status of relevant patents, and patent holders can initiate disputes through the CNIPA or courts.

Despite these reforms, enforcement quality varies, and China has used compulsory licensing provisions for public health emergencies, though it has invoked this power sparingly for Western pharmaceuticals. The country’s domestic innovation ecosystem has expanded rapidly, and major Chinese biopharmaceutical companies now hold globally competitive patent portfolios of their own.

Data exclusivity in China is six years for new drugs with new active ingredients, applied through the National Medical Products Administration (NMPA). China’s regulatory approval pathway has accelerated significantly for innovative drugs under priority review programs.

India

India occupies a unique position in the global pharmaceutical patent landscape and cannot be analyzed through the same framework as the United States or Europe. India is simultaneously a large generic drug manufacturing base serving global markets and a country with a sovereign policy commitment to affordable medicine access — commitments that have directly shaped its patent law.

Section 3(d) of India’s Patents Act 1970, as amended in 2005, prohibits patent protection for new forms of known substances (new polymorphs, salts, esters, isomers) unless they demonstrate significantly enhanced efficacy compared to the known substance [16]. This provision — tested and upheld in the Supreme Court of India’s 2013 Novartis AG vs. Union of India ruling on Gleevec — means that many secondary pharmaceutical patents routinely granted in the US, EU, and Japan are simply not available in India.

The practical consequence is that India’s effective patent protection for pharmaceuticals is substantially narrower than TRIPS’s nominal 20-year term for a wide category of secondary patents. Composition of matter patents on genuinely new chemical entities generally survive, but the formulation, polymorph, and combination patents that form the bulk of pharmaceutical companies’ defensive portfolios in Western markets face a much higher invalidity risk in India.

India also has an active compulsory licensing framework, invoked in the 2012 case involving Bayer’s sorafenib (Nexavar) — the only compulsory license granted for a patented pharmaceutical in India to date — and its government has repeatedly signaled willingness to use this tool for high-cost medicines.

Brazil

Brazil’s patent system has been shaped by a similar tension between intellectual property protection and public health imperatives. The Brazilian Patent Act provides for 20-year patent terms under TRIPS, but the country has notably invoked compulsory licensing for antiretrovirals at various points — most significantly in 2007 when President Lula issued a compulsory license for efavirenz, manufactured by Merck.

Brazil’s ANVISA (National Health Surveillance Agency) has historically had a formal role in the patent granting process for pharmaceutical products, with the right to issue prior approval opinions that could lead the INPI (National Institute of Industrial Property) to reject pharmaceutical patent applications on public health grounds. This system, known as the “prior consent” mechanism, has been a persistent source of tension with the pharmaceutical industry. Legal reforms in recent years have modified but not eliminated this mechanism.

Data exclusivity in Brazil applies for a period tied to regulatory approval, but practical enforcement has been inconsistent compared to North American and European standards.

Canada

Canada’s patent protection system has historically been less generous to pharmaceutical innovators than the US or EU systems. As noted, patent term extension was only introduced in 2017 under CUSMA pressure, with a maximum of two years compared to five years in the US and EU.

Canada’s linkage system — governed by the Patented Medicines (Notice of Compliance) Regulations — allows innovators to list patents in Health Canada’s patent register (the Therapeutic Products Directorate equivalent of the US Orange Book) and to trigger litigation against generic applicants. The system has been reformed multiple times, most recently in 2017, to improve its functioning. The 24-month automatic prohibition period that a court challenge triggers (analogous to the US 30-month stay) has been a point of contention.

Canada’s Patented Medicine Prices Review Board (PMPRB) regulates the maximum prices at which patented medicines can be sold, creating an additional constraint on commercial value that is unrelated to patent duration but affects the financial value of exclusivity.

Australia

Australia’s patent system grants pharmaceutical patents on a 20-year term from filing, with patent term extensions of up to five years (subject to a 15-year effective protection cap from first therapeutic goods registration). Extensions are administered by IP Australia.

Australia’s Therapeutic Goods Administration (TGA) operates a system that has historically shadowed the FDA’s decisions, with many drugs receiving TGA approval within one to two years of FDA approval. Data exclusivity of five years applies to new chemical entities.

Australia has comprehensive patent linkage legislation under the Therapeutic Goods Act, allowing innovators to list patents and receive notification when generic applications are filed. The system is simpler than its US and Canadian counterparts but has been periodically criticized by generic manufacturers as providing insufficient protection against spurious patent listings.

Generic Drug Entry: When Patents Actually Expire in Practice

Understanding when patents expire on paper is only the first step. Understanding when generic competition actually arrives requires accounting for the entire Hatch-Waxman mechanism, the litigation strategy of the parties involved, and the settlement dynamics that have attracted significant antitrust scrutiny.

Paragraph IV Certifications and the 30-Month Stay

When a generic manufacturer files an ANDA for a drug listed in the Orange Book, it must certify the status of each listed patent. Paragraph IV certification states that the listed patent is either invalid or would not be infringed by the generic product. This certification is treated as an act of infringement, allowing the brand company to sue immediately without waiting for the generic to actually launch.

If the brand company sues within 45 days of receiving notice of the Paragraph IV certification, an automatic 30-month stay on ANDA approval goes into effect. During these 30 months, the litigation proceeds. If the brand wins, the generic is blocked. If the generic wins (or if 30 months pass without a resolution), the generic can receive approval and launch.

The first generic filer who successfully challenges a patent receives 180 days of market exclusivity during which no other generic can receive final ANDA approval. This 180-day exclusivity is enormously valuable — a generic launching six months ahead of all other generic competition in a large-volume drug market can capture substantial market share at near-brand prices before the market is fully genericized. This incentive was deliberately designed to encourage Paragraph IV challenges as a mechanism for removing invalid patents from the register.

Pay-for-Delay Settlements and Reverse Payment

Litigation under Hatch-Waxman has produced a settlement mechanism that courts and the FTC have spent years debating. In a reverse payment settlement (also called a “pay-for-delay” agreement), the brand company pays the generic company to drop its Paragraph IV challenge and agree not to enter the market until a specified date. From the brand company’s perspective, this exchanges a lump sum (or other consideration) for certainty about the exclusivity period. From the generic company’s perspective, it exchanges the risk of litigation for a guaranteed payment.

The Federal Trade Commission has vigorously challenged these settlements as anticompetitive. The Supreme Court’s 2013 FTC v. Actavis decision held that reverse payment settlements can violate antitrust law and must be evaluated under the rule of reason, without creating a presumption of illegality [17]. Since Actavis, large cash payments from brand to generic have become less common, though companies continue to use non-cash consideration (licenses, supply agreements, authorized generics) in ways that raise similar concerns.

Patent Cliffs and Post-Patent Market Dynamics

When an important composition of matter patent expires and a generic version launches, the branded drug’s market share typically collapses within months. The generic entry pattern in the United States follows a well-documented trajectory: within three months of generic entry, branded volume share drops to under 20%; within twelve months, the branded product often retains under 5% of volume. The branded product’s price typically remains at or near pre-generic levels while volume migrates to generics priced 80-90% below brand.

This pattern — the patent cliff — has been studied extensively and is remarkably consistent across therapeutic categories. The IQVIA Institute for Human Data Science and similar research organizations have documented that the average brand drug retains roughly 10% of its pre-generic revenue two years after generic entry [18]. For drugs generating $2 billion or more annually, the revenue impact of patent expiry is a defining event in the company’s financial trajectory.

Using DrugPatentWatch and Other Patent Research Tools

Tracking drug patent expiry dates is a specialized research task that requires access to multiple data sources and the expertise to interpret them. Patent databases, regulatory filings, and court records all contribute to a complete picture.

DrugPatentWatch

DrugPatentWatch is one of the most widely used commercial tools for tracking pharmaceutical patent and regulatory exclusivity data. The platform aggregates information from the FDA’s Orange Book, patent databases, ANDA filing records, and litigation tracking to provide a consolidated view of the intellectual property landscape for any given drug product.

For a given drug, DrugPatentWatch typically provides the listed patents and their expiry dates, any pending Paragraph IV challenges, the generic applicants seeking approval, the regulatory exclusivity status and expiry dates, and historical litigation outcomes for related Paragraph IV filings. This level of integrated information is difficult to assemble from primary sources alone, which is why tools like DrugPatentWatch have become standard infrastructure for generic manufacturers, brand companies’ competitive intelligence teams, investors analyzing patent cliff exposure, and policy researchers studying pharmaceutical market dynamics.

Analysts using DrugPatentWatch to research a drug’s patent status typically start by searching the brand or generic name, review the Orange Book listings and their expiry dates, cross-reference the listed patents with Paragraph IV notifications on file, and then assess the litigation history to understand the probability that any given patent will survive challenge. The tool also provides alerts on changes to patent listings and new ANDA filings, making it useful for ongoing monitoring rather than just point-in-time research.

The FDA’s Orange Book

The FDA’s Orange Book remains the primary public source for patent information on approved small-molecule drugs in the United States. Brand companies are required by law to list patents covering an approved drug in the Orange Book — specifically, patents claiming the drug substance, the drug product, or the approved method of use. The listings must be submitted with the NDA or within 30 days of a patent being issued after NDA approval.

The Orange Book lists are not a comprehensive inventory of all patents that might be infringed by a generic version of a drug. Companies list the patents they want generic filers to have to certify against, which creates strategic incentives that have led to both under-listing (to avoid Paragraph IV challenges on weak patents) and over-listing (to trigger 30-month stays). The FTC has periodically challenged Orange Book listings it considers improper.

The Orange Book is freely accessible at the FDA’s website, updated monthly, and searchable by brand name, active ingredient, or applicant name. For biologics, the Purple Book serves the equivalent function, listing reference products and biosimilar and interchangeable biological products.

The EPO and WIPO Databases

For European and international patent research, the European Patent Office’s Espacenet database provides free access to over 150 million patent documents from around the world, including the full text of granted European patents and published applications. Espacenet supports searches by inventor, applicant, classification code, and keyword, and provides legal status information showing whether a patent is in force, expired, or the subject of opposition proceedings.

The WIPO PatentScope database covers PCT international applications, providing a single-point-of-access for the international phase of PCT applications before they enter national/regional phases. For a drug whose composition of matter patent was filed as a PCT application, PatentScope will show the original filing, the national phase entry dates, and the family members in different jurisdictions.

For US patents, the USPTO’s Public Patent Application Information Retrieval (PAIR) system and Patent Center provide detailed prosecution histories, correspondence with the examiner, and current legal status for all published US patent applications and granted patents.

The FDA’s Purple Book for Biologics

The Purple Book (formally the “Lists of Licensed Biological Products with Reference Product Exclusivity and Biosimilarity or Interchangeability Evaluations”) is the biologics equivalent of the Orange Book, listing all FDA-licensed biological products and indicating which have been determined to be biosimilar or interchangeable with a reference product [19]. Unlike the Orange Book, the Purple Book does not list patents. Patent information for biologics is governed by the BPCIA’s patent dance mechanism, a complex information-exchange process between biosimilar applicants and reference product sponsors that operates outside the public record for much of its duration.

Biologics and Biosimilars: A Different Patent Ecosystem

The patent landscape for biologics — drugs derived from living cells, including monoclonal antibodies, recombinant proteins, and gene therapies — is fundamentally different from the small-molecule patent landscape. The differences affect how long these drugs are protected, how competition enters, and how patent strategy is designed.

The Complexity That Makes Biologics Patents Different

Small-molecule drugs are defined chemical entities. The patent structure that protects them — composition of matter patent on the specific molecule — has clear boundaries. Biologics are not single molecular entities in the same sense. A monoclonal antibody like adalimumab (Humira) is a large, complex protein whose activity depends not just on its amino acid sequence but on its three-dimensional folding, its glycosylation pattern, and hundreds of other structural features that result from the manufacturing process. Different cell lines, different fermentation conditions, different purification methods produce products that are similar but not identical.

This complexity means that the intellectual property covering a biologic tends to be spread across a much larger portfolio of patents than a small-molecule drug. AbbVie’s Humira patent portfolio, which became a cause célèbre in discussions of pharmaceutical patent strategy, included over 130 separate US patents at its peak, covering not just the antibody sequence but manufacturing processes, formulations, methods of use across different indications, and devices (prefilled syringes and auto-injectors) [20]. This portfolio approach — sometimes called a “patent thicket” — meant that even after the composition of matter patents expired, biosimilar developers faced a wall of secondary patents that could support litigation risk for years.

The 12-Year Exclusivity Cliff for US Biologics

The BPCIA’s 12-year reference product exclusivity applies to biological products approved under the Public Health Service Act’s 351(a) pathway. The exclusivity period runs from the date of first licensure and blocks FDA approval of biosimilar applications relying on the reference product’s data.

For reference products like Humira, Enbrel, Remicade, and Keytruda that generated annual revenues of $5 billion to $20 billion, the 12-year exclusivity period represents tens of billions of dollars in cumulative protected revenue. The transition from exclusivity to biosimilar competition has been more gradual than the small-molecule generic cliff, partly because of residual patent litigation, partly because biosimilars require significantly more clinical development than conventional generics and are priced higher, and partly because prescribing patterns change more slowly when physicians have concerns about interchangeability.

Humira’s US experience illustrates the dynamics. The compound patent expired in 2016. Biosimilar applications were filed, biosimilar applicants and AbbVie entered the BPCIA patent dance, and litigation and settlements resulted in agreements that delayed US biosimilar launches until January 2023 — seven years after the compound patent expired [21]. The first US biosimilars launched in 2023 at 5-85% discounts to the brand, but market uptake was complicated by formulary dynamics and rebate structures that preserved Humira’s market share longer than many analysts anticipated.

The BPCIA’s “Patent Dance”

The BPCIA established an elaborate information-exchange mechanism between biosimilar applicants and reference product sponsors designed to identify and resolve patent disputes before the biosimilar reaches market. The mechanism — colloquially called the “patent dance” — involves a series of sequential information disclosures, lists of relevant patents, negotiation of patents to litigate, and litigation timelines.

The patent dance is optional, not mandatory, for biosimilar applicants. A biosimilar applicant that elects not to participate in the dance loses certain litigation protections but avoids the disclosure obligations that benefit the reference product sponsor. Courts have ruled on various aspects of the patent dance’s operation, and the case law continues to develop.

The practical result is that biosimilar patent litigation tends to be more prolonged and more complex than Hatch-Waxman Paragraph IV litigation, with multiple patents litigated across longer timeframes. This benefits reference product sponsors whose secondary patent portfolios can sustain litigation risk that delays biosimilar launches even after the primary exclusivity periods have ended.

Evergreening: How Companies Extend Market Exclusivity Beyond Natural Patent Life

“Evergreening” is the colloquial term for a collection of strategies pharmaceutical companies use to extend their effective market exclusivity beyond the natural expiry of their core patents. The term is generally pejorative when used by critics of pharmaceutical pricing, and it describes strategies that range from clearly legitimate (developing improved formulations) to legally contested (filing patents on minor variations of known substances to delay generic entry) to sometimes anticompetitive (reverse payment settlements, product hopping).

Product Hopping

Product hopping involves switching patients from a formulation facing generic entry to a new formulation protected by later-expiring patents, before the generic version of the original formulation is available. The company typically discontinues the original formulation (reducing its supply and preventing pharmacies from substituting generics) and redirects prescribers to the reformulated product.

The classic documented case involved Warner Chilcott and Doryx (doxycycline), where the company reformulated from capsules to tablets to scored tablets to avoid auto-substitution of generics [22]. Courts have divided on whether product hopping violates antitrust law. The Second Circuit in Abbott Laboratories v. Teva Pharmaceuticals (the Tricor/fenofibrate litigation) found that product hopping could be anticompetitive if the original product was deliberately withdrawn to prevent substitution. Other courts have been more permissive.

Authorized Generics

An authorized generic is a generic version of a brand drug that the brand company itself sells (or licenses to a partner) at a reduced price, typically at or near the time of first generic entry. Authorized generics do not require ANDA approval because they are manufactured under the brand company’s NDA.

The strategic function of authorized generics is to dilute the 180-day first-filer exclusivity. When a first filer’s 180-day exclusivity would otherwise give it a period of duopoly (brand and one generic), the brand’s authorized generic converts that into a three-way competition (brand, authorized generic, first-filer generic). This reduces the first filer’s profits from the 180-day period, potentially discouraging Paragraph IV challenges in the future.

The FTC has studied authorized generics and concluded that while they reduce the value of first-filer exclusivity, they also tend to lower drug prices more quickly after patent expiry. The practice is legal in the United States and has been challenged but upheld by the courts.

Citizen Petitions as Delay Tactics

The FDA’s citizen petition process allows any person to ask the FDA to take (or refrain from taking) regulatory action. Pharmaceutical companies have sometimes used citizen petitions filed immediately before expected generic approvals to raise technical objections to the generic’s bioequivalence or labeling — even when the petitions ultimately lack merit — because the FDA must respond to petitions before approving affected ANDAs.

Congress addressed this practice in the FDA Amendments Act of 2007, which requires the FDA to deny citizen petitions submitted primarily to delay generic drug approval and authorizes civil penalties. The FDA now more aggressively denies petitions it identifies as delay tactics, but the practice has not disappeared entirely.

The Limits of Evergreening

It would be inaccurate to present evergreening as uniformly harmful or uniformly effective. Many “evergreening” strategies represent genuine innovation: an extended-release formulation that improves patient adherence by enabling once-daily instead of twice-daily dosing creates real patient value. A new indication discovered after the original patent was filed reflects real scientific investment. The challenge is that the patent system cannot easily distinguish between improvements that justify additional exclusivity and trivial variations engineered purely to delay generic entry.

The policy response has been gradual and multi-pronged: India’s Section 3(d) approach (limiting patentability of new forms), enhanced FTC scrutiny of reverse payment settlements, FDA citizen petition reforms, and increasingly skeptical courts that are more willing to invalidate obvious variations. None of these responses is comprehensive, and the debate about where to draw the line between legitimate innovation and gaming the system continues actively in both legislative and academic forums.

Patent Cliffs: The Revenue Timebombs Pharma Companies Face

A patent cliff occurs when a company faces the near-simultaneous expiry of patents covering one or more high-revenue products, creating a sudden and severe revenue decline as generics enter and prices collapse. Patent cliffs are not novel — the industry has experienced several major ones — but their scale and timing vary, and the pharmaceutical industry’s strategic response to them shapes the entire structure of pharmaceutical R&D investment.

Historic Patent Cliffs: 2010-2015

The early 2010s saw what was widely described at the time as a catastrophic patent cliff for the branded pharmaceutical industry. Between 2010 and 2015, patents expired on drugs generating a combined estimated $200 billion in annual global revenues [23]. The affected molecules included some of the industry’s most commercially successful products:

Lipitor (atorvastatin), which had been generating over $12 billion annually for Pfizer, lost patent protection in November 2011. Within months, generic entry reduced Pfizer’s atorvastatin revenues by over 80%. Plavix (clopidogrel), Bristol-Myers Squibb and Sanofi’s blockbuster antiplatelet, lost its US patent in May 2012 after a Paragraph IV challenge. Singulair (montelukast), Merck’s allergy medication, Zyprexa (olanzapine), Eli Lilly’s antipsychotic, and Cymbalta (duloxetine), Lilly’s antidepressant, all fell off the cliff within this period.

The financial consequences for affected companies were severe. Eli Lilly, facing patent expiries on Zyprexa (2011), Gemzar (2010), and Cymbalta (2013-2014) in rapid succession, saw its earnings decline sharply even as it invested billions in its pipeline. The company’s stock significantly underperformed the pharmaceutical sector index during this period. Pfizer, the world’s largest pharmaceutical company by revenue, saw its total revenues decline from over $65 billion in 2010 to under $52 billion by 2014, with Lipitor’s patent expiry being the dominant factor.

The 2025-2030 Patent Cliff: What’s Coming

The pharmaceutical industry is in the midst of another significant patent cliff period that will extend through the late 2020s. Several of the industry’s highest-revenue products face patent expiries in this window.

Humira (adalimumab, AbbVie) began facing biosimilar competition in the US in January 2023, following the settlement of patent disputes that allowed multiple biosimilar manufacturers to enter the market under agreed timelines. AbbVie has been explicitly preparing for this transition, having built up its immunology pipeline (Skyrizi, Rinvoq) to partially offset Humira’s anticipated revenue decline.

Keytruda (pembrolizumab, Merck) — now the world’s best-selling drug by revenue — faces patent expiries beginning in 2028 for its core composition of matter patents, with additional SPCs extending European protection. As a biologic in a category of exceptional clinical value (PD-1 checkpoint inhibitors for cancer), its biosimilar transition may be slower than Humira’s, but the patent cliff is clearly on the horizon and drives much of Merck’s pipeline investment.

Eliquis (apixaban, Bristol-Myers Squibb and Pfizer), the blood thinner generating over $12 billion in annual sales, has US patent protection that extends through 2026-2031 depending on the specific patent, with ongoing Paragraph IV litigation determining the actual entry date.

Ozempic and Wegovy (semaglutide, Novo Nordisk), despite being newer products, are already the subject of patent litigation as generic and biosimilar manufacturers position themselves for eventual entry. Novo Nordisk’s composition of matter patent for semaglutide in the US runs through approximately 2032, but the drug’s success has made it a high-value target for Paragraph IV challenges.

According to IQVIA data, drugs with combined annual sales exceeding $200 billion are expected to face US patent expiry or first generic entry between 2023 and 2030 [24]. The structure of this cliff is different from the 2010-2015 cliff in one important respect: biologics now constitute a larger share of the expiring portfolio, and biosimilar transitions are financially different from small-molecule generic transitions, proceeding more slowly and retaining higher prices relative to the reference product.

Patent Strategy in Practice: What Companies Actually Do

Understanding the rules of patent duration is necessary but not sufficient to understand pharmaceutical patent strategy. The real competition happens in the decisions that companies make about when to file, how to structure a portfolio, which patents to list in the Orange Book, when to litigate and when to settle, and how to manage the commercial transition when exclusivity ends.

Filing Strategy: The Priority Cascade

Professional pharmaceutical patent strategy begins years before clinical trials with a disciplined approach to building a priority cascade — a series of patent applications filed at strategic intervals to create overlapping layers of protection with staggered expiry dates.

The composition of matter patent is filed early, establishing the core protection. It will expire earliest. As the molecule progresses through development and more is learned about its optimal use, additional patents are filed: salt form patents (if the lead salt form is identified during development), formulation patents (as the delivery system is finalized), method of use patents (when clinical data establishes efficacy in specific indications), dosing regimen patents (when trial results identify optimal dose and frequency), device patents (for injectable biologics requiring prefilled syringes or pens), and combination patents (if the drug is used in combination with other agents).

Each layer is filed later and expires later. The result is that the total duration of intellectual property protection, aggregated across all patents, substantially exceeds 20 years even though no individual patent does.

The Importance of Continuation Practice in the United States

The US patent system permits filing continuation applications — new applications that claim priority to a parent application but contain new or different claims. Continuation applications allow a company to pursue additional claims, refine claim scope in light of competitor activity, and maintain a pending application in examination for an extended period. A continuation filed on the same subject matter as a 2005 parent application will still expire when the parent expires (20 years from the earliest effective filing date), but it allows the company to obtain new, narrowly-targeted claims that might not have been in the original application.

This matters because pharmaceutical companies cannot always predict in 2005 what competitor molecules will exist in 2020 and whether their original claim language covers them. Continuation practice allows claim language to be tailored to competitive threats that emerge during prosecution. The practice is legitimate under US patent law but has attracted criticism when used to extend prosecution indefinitely across many continuation generations.

Orange Book Listing Strategy

Not all patents are listable in the Orange Book, and not all listable patents are listed. The decision about which patents to list is strategic. A patent listed in the Orange Book triggers a certification obligation for ANDA filers and provides the platform for a 30-month stay. This is valuable for strong patents — you want the litigation clock running in your favor. For weak patents, however, listing invites Paragraph IV challenges that could result in an invalidity ruling, which is far worse than never listing the patent and allowing it to expire quietly.

The FDA has increasingly scrutinized improper Orange Book listings under its authority to require patent information from NDA holders that is accurate and complete. FTC enforcement actions under Biden administration leadership also challenged listings by companies including Pfizer, Sanofi, Lantheus, and others that the agencies deemed improper, seeking to remove listings that delayed generic competition.

Settlement Mathematics

When a brand company faces a Paragraph IV challenge, the litigation decision is fundamentally a financial calculation. If the composition of matter patent has four years remaining and generates $3 billion annually, the expected value of prevailing in litigation (assuming equal probability of winning or losing) is roughly $6 billion (four years times $3 billion times 50% probability). A settlement that allows generic entry in three years, as opposed to the risk of losing and allowing immediate entry, has a determinable financial value. So does paying the generic company some consideration to delay entry for the full four years.

This calculation explains both why brand companies settle and why they pay. It also explains why the FTC views large reverse payments with suspicion: payments that substantially exceed the generic company’s litigation costs are evidence, under the Actavis framework, that the brand company recognizes the patent is vulnerable and is paying for delay rather than for any legitimate business reason.

The Investment Implications of Drug Patent Expiry

For pharmaceutical sector investors, understanding patent duration and the timing of generic or biosimilar entry is a fundamental input into equity valuation. A company whose revenues depend on a single blockbuster drug approaching patent expiry is a fundamentally different investment proposition from one with a diversified portfolio of products with staggered expiry dates and a robust pipeline.

Modeling Patent Cliff Exposure

Sell-side pharmaceutical analysts routinely build patent cliff models that project brand revenue under different generic entry scenarios. These models require inputs on:

The date of first generic entry, which may differ from the patent expiry date depending on Paragraph IV litigation outcomes, authorized generic strategies, and settlement agreements. Post-entry brand retention, which varies by therapeutic category, physician prescribing behavior, and whether the generic is automatically substitutable. The pricing trajectory of generics over time, which depends on the number of generic entrants and the speed of formulary switching. The company’s pipeline to offset lost revenues, evaluated both by likelihood of approval (pipeline probability-weighted value) and expected launch timing relative to the cliff.

A company like Bristol-Myers Squibb approaching the Eliquis patent cliff is being analyzed through exactly this framework by every major institution with a position in the stock. The sensitivity of the equity valuation to the date of first generic Eliquis entry — the difference between 2027 and 2029, say — can be measured in double-digit percentage points of enterprise value for a company at BMS’s revenue concentration.

Generic Company Investment Thesis

For investors in generic pharmaceutical companies — Teva, Viatris, Hikma, Dr. Reddy’s — the patent landscape creates the opposite investment thesis. The value in a generic pipeline depends on the probability of Paragraph IV success (or settlement value), the expected launch date, and the competitive dynamics among ANDA filers for the same product.

Generic company investors pay close attention to the first-filer exclusivity landscape. A generic company that is the first ANDA filer for a $5 billion drug with a strong Paragraph IV case has a potentially enormous asset on its books — the 180-day exclusivity that, if won, provides a semi-monopoly period worth hundreds of millions of dollars. The probability of success and the timing of resolution are the key investment variables.

Biosimilar Market Dynamics

The biosimilar investment thesis is distinct from both the brand and conventional generic theses. Biosimilar development requires substantially more investment than small-molecule generic development — regulatory agencies require comparative clinical data demonstrating biosimilarity, which small-molecule ANDAs do not require. The regulatory cost pushes biosimilar development costs toward $100-250 million per product, compared to under $5 million for typical small-molecule generics.

This higher cost base means biosimilar companies need higher margins than conventional generic companies to generate adequate returns. Biosimilars typically launch at 15-35% discounts to reference products (rather than 80-90% like small-molecule generics), and market uptake is slower due to prescriber hesitancy and payer formulary dynamics. The interchangeability designation, which allows pharmacists to automatically substitute a biosimilar for the reference biologic without physician intervention, is a critical variable in biosimilar market success and depends on additional comparative clinical studies.

The Policy Debate: Is the Patent System Getting It Right?

The duration and structure of pharmaceutical patent protection is one of the most contentious areas of health policy. The competing interests — patient access to affordable medicines, innovation incentives for drug development, generic industry viability, and government healthcare budget sustainability — do not resolve to a single optimal policy, which is why the debate is genuinely contested rather than just politically performative.

The Innovation Incentive Argument

The pharmaceutical industry’s core argument for robust and long patent protection is that drug development is uniquely expensive and risky. The cost of developing a new drug — inclusive of the cost of failures — has been estimated at over $2.5 billion per approved drug by the Tufts Center for the Study of Drug Development [3]. The vast majority of drug candidates that enter clinical trials fail, meaning that the revenues from the drugs that succeed must cross-subsidize the development costs of the drugs that fail.

Without the price premium that exclusivity enables, the revenue from successful drugs would be lower, reducing the expected return on the investment portfolio of a pharmaceutical R&D program and consequently reducing the level of investment the market would support. This argument is well-grounded in economic theory and supported by the historical pattern: the pharmaceutical industry has consistently delivered more therapeutic innovation than any comparable sector, and the patent system is the primary mechanism aligning private incentives with public benefit.

The Access Argument

Critics of the current patent duration regime, including health economists, public health researchers, and patient advocacy organizations, argue that 20-year patent terms (plus extensions) provide excessive protection that results in prices unaffordable to large populations globally and unsustainable for government healthcare budgets.

The empirical relationship between patent protection length and innovation rate is genuinely contested. A 2019 analysis in the Journal of Law and Economics found that reducing the US biologics exclusivity from 12 to 7 years would have minimal effect on biologic drug development while saving the US healthcare system tens of billions of dollars in drug spending [25]. The Pharmaceutical Research and Manufacturers of America (PhRMA) disputes the methodology of such analyses, arguing they underestimate the sensitivity of R&D investment to expected returns.

The TRIPS Waiver Debate

The COVID-19 pandemic renewed global debate about patent waivers for medicines in public health emergencies, culminating in a partial TRIPS waiver adopted by the WTO in June 2022 specifically for COVID-19 vaccines [26]. The waiver, after two years of negotiation, was more limited than initially proposed by India and South Africa and has had limited practical impact because manufacturing capacity, not patent access, was the primary bottleneck for vaccine distribution in low-income countries.

The TRIPS waiver debate revealed the structural tension in the global intellectual property system: the same rules that incentivize innovation in high-income markets with large pharmaceutical R&D sectors can impede access in lower-income markets with limited ability to pay patent-protected prices. How the system resolves this tension — through differential pricing, compulsory licensing, time-limited waivers, or fundamental reform — remains unresolved.

Tracking Patent Expiry in Real Time

For professionals who need to monitor pharmaceutical patent status as part of their work — whether as competitive intelligence analysts, investors, policy researchers, or legal practitioners — the combination of public databases and commercial tools provides a reasonably comprehensive picture.

Building a Patent Monitoring System

A practical patent monitoring workflow for a generic pharmaceutical company evaluating entry opportunities might look like this:

Identify the target product using the FDA Orange Book or Purple Book. Review all Orange Book-listed patents, their expiry dates, and any Paragraph IV certifications already on file. Access the full patent file wrappers through the USPTO Public Patent Application Information Retrieval system to assess prosecution history estoppel and claim scope. Search DrugPatentWatch for ANDA filing history, first-filer status, and any settlement agreements filed with the FTC (which public companies must submit under the Medicare Prescription Drug, Improvement, and Modernization Act). Cross-reference with Espacenet to assess the international patent situation, identify SPCs in key European markets, and evaluate the litigation history in jurisdictions where the company plans to file.

For biologics, the process is more complex: the patent dance has historically occurred partly outside the public record, though litigation filings become public when cases are filed in federal court.

Regulatory Intelligence Integration

Patent expiry dates tell you when you can potentially enter a market. Regulatory exclusivity dates tell you when you are actually permitted to file for and receive approval. These two timelines must be integrated. A generic company that wins a Paragraph IV challenge on a drug with three years remaining on its NCE exclusivity has won the litigation battle but cannot receive final ANDA approval for three years. This is a common scenario and one that requires careful timeline modeling.

Commercial database providers including Citeline, Evaluate Pharma, and GlobalData provide integrated views of patent, exclusivity, and pipeline data for pharmaceutical products globally. These platforms are standard tools for large pharmaceutical companies and institutional investors but carry subscription costs that put them out of reach for smaller organizations, which rely more heavily on public databases and tools like DrugPatentWatch.

Special Cases: Combination Products, Pediatric Drugs, and NCEs vs. NBEs

Not all drugs fit neatly into the frameworks described above. Several special cases are worth addressing explicitly.

Fixed-Dose Combination Products

A fixed-dose combination (FDC) product contains two or more active ingredients in a single dosage form. FDCs are common in HIV (where three-drug regimens in a single pill improve adherence dramatically), cardiovascular medicine, and diabetes. The patent landscape for FDCs is layered: each component may have its own composition of matter patent (potentially expiring at different dates), the combination itself may be patented if it involves inventive activity beyond combining known drugs, and the formulation technology enabling stable co-formulation may also be patented.

The regulatory exclusivity situation is similarly complex. An FDC may qualify for NCE exclusivity only if one of its components is a new chemical entity; if both components are previously approved, the FDC generally receives only the 3-year new clinical investigation exclusivity. The practical consequence is that FDCs sometimes face generic competition earlier than the individual component drugs, particularly when the components themselves are already off-patent.

NCEs vs. NBEs

New chemical entities (NCEs) are small molecules approved through the NDA pathway. New biological entities (NBEs) are large-molecule biologics approved through the BLA pathway. The distinction matters because they are subject to different exclusivity regimes (5 years vs. 12 years in the US, as described above), different competition pathways (ANDAs and Paragraph IV for NCEs; the BPCIA patent dance and biosimilar applications for NBEs), and different pricing dynamics after patent expiry.

The pharmaceutical industry has shifted dramatically toward NBEs over the past two decades. Of the top 20 best-selling drugs globally in 2024, approximately half were biologics approved under the BLA pathway. This shift has extended average effective exclusivity periods for the pharmaceutical industry’s highest-revenue products, contributing to sustained high drug prices in the US market in ways that small-molecule patent policy alone cannot explain.

Drugs containing controlled substances face an additional regulatory layer: DEA scheduling. A generic version of a scheduled drug requires DEA quota allocation, which has historically been a bottleneck for high-demand controlled substance generics. This constraint operates independently of patent and exclusivity status and can delay generic market entry even after all legal barriers to approval have been removed.

The opioid crisis and subsequent regulatory attention to controlled substance prescribing has made the DEA quota allocation process more complex and subject to greater scrutiny for new controlled substance generics.

How Biosimilars Are Changing the Long-Term Patent Math

The biosimilar market is maturing in ways that are gradually changing the long-term financial model for reference biological products. The US, which was slow to develop a functional biosimilar pathway compared to Europe (where biosimilars have been approved since 2006), is now experiencing a significant expansion of biosimilar competition as the BPCIA’s 12-year exclusivity periods expire for the first major wave of biologics approved in the 2000s.

European Leadership in Biosimilars

Europe has the most mature biosimilar market in the world, with over 100 biosimilars approved by the EMA since 2006 covering therapeutic proteins including human growth hormone, erythropoietin, filgrastim, and monoclonal antibodies including infliximab (Remicade), adalimumab (Humira), trastuzumab (Herceptin), and bevacizumab (Avastin) [27]. European biosimilar pricing and uptake have been significantly more favorable to competition than initial US biosimilar experience, with some biosimilars achieving 50-80% market share within two years of launch.

The more favorable European biosimilar experience reflects differences in healthcare system structure: many European countries have centralized procurement systems, national tender processes, and automatic substitution policies that direct volume to biosimilars more aggressively than the US market’s fragmented payer system. This structural difference has contributed to substantially lower prices for biosimilars of major biologics in Europe compared to the United States.

The Interchangeability Question