Section 1: The Broken Bargain: How a 20-Year Monopoly Became a 40-Year Rent

The patent system’s foundational premise is blunt: disclose your invention fully, accept a 20-year exclusive window to commercialize it, then step aside. That sequence worked tolerably well for most of the 20th century pharmaceutical market. It has since been replaced, at least for U.S. blockbuster drugs, by something functionally different: a layered, renewable set of monopoly claims that can push effective market exclusivity well past the initial patent term, sometimes by a decade or more.

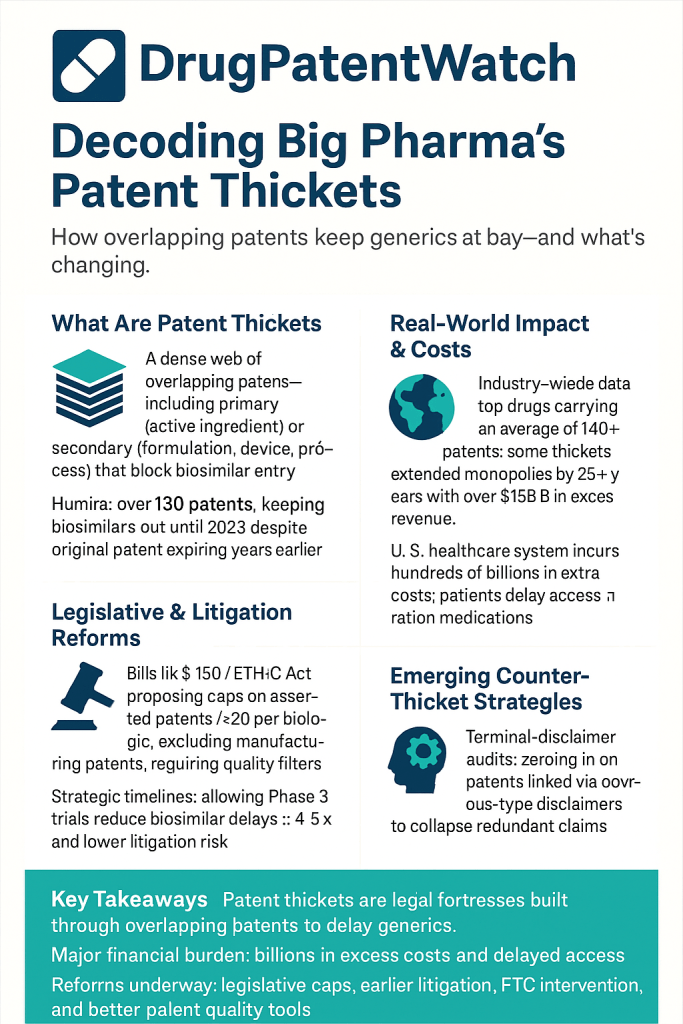

The mechanism driving this shift is the patent thicket, a term coined in competition economics to describe a dense web of overlapping intellectual property rights that a company must clear in order to bring a competing product to market. In pharmaceuticals, the thicket is less a metaphor than a precise operational description. AbbVie holds more than 130 granted U.S. patents on Humira. Merck has secured between 53 and 78 granted patents on Keytruda. Celgene filed more than 200 patent applications on Revlimid. None of those counts represent the foundational patent on the active molecule, the compound that first cleared the FDA. They represent secondary, tertiary, and quaternary patents on manufacturing processes, dosage concentrations, delivery devices, new salt forms, and methods of treating conditions the drug was never originally approved to treat.

This is not illegal under current U.S. law. That’s the point.

The pharmaceutical industry does not build patent thickets because its lawyers are unusually aggressive. It builds them because the U.S. patent and regulatory framework, through specific structural features, makes thicket construction a rational, low-risk, extremely high-return corporate strategy. Those structural features, the 30-month automatic stay triggered by a Paragraph IV filing response, the USPTO’s permissive non-obviousness standards for secondary modifications, the BPCIA’s allowance for unlimited patent assertions against biosimilar challengers, and the FDA’s historical failure to vet Orange Book listings for anticompetitive intent, did not emerge from a single legislative error. They accumulated through decades of industry lobbying, agency inertia, and judicial decisions that treated each tactic in isolation rather than as a coordinated system.

The result is a system that forces every generic or biosimilar challenger to win 100% of its patent battles, while the brand-name manufacturer needs only one of its hundred-plus patents to survive to preserve the monopoly. That asymmetry is not a quirk. It is the product.

Key Takeaways: Section 1

Patent thickets are a predictable output of specific U.S. legal and regulatory design choices, not a byproduct of pharmaceutical complexity.

The core competitive asymmetry: a generic challenger must defeat every patent in a thicket; the brand needs one patent upheld.

Effective market exclusivity for blockbuster drugs now regularly exceeds the 20-year statutory patent term by five to twelve years.

This is a domestic U.S. problem. European drug markets do not replicate it, for reasons the EPO comparison in Section 9 makes explicit.

Section 2: The Legal Architecture of Exclusivity in the United States

Pharmaceutical market exclusivity in the United States runs on two parallel tracks: patent exclusivity, administered by the U.S. Patent and Trademark Office (USPTO), and regulatory exclusivity, administered by the FDA. Both tracks grant temporary monopolies. Both can run simultaneously on the same drug. Together, they produce a multi-layer protection stack that is considerably longer and more complex than the headline 20-year patent term.

Track One: Patent Exclusivity and the USPTO

A utility patent filed with the USPTO grants 20 years of exclusivity from the application filing date, not from approval. Since drug development typically consumes eight to twelve years between first filing and FDA approval, a brand-name drug often has only eight to twelve years of effective patent-protected market exclusivity left by the time it reaches pharmacy shelves. This erodes the commercial case for the initial patent, and the industry has responded by layering secondary patents that start their 20-year clocks later, after the drug is already generating revenue.

The USPTO examines applications under three statutory criteria: novelty, utility, and non-obviousness. Non-obviousness is the central battleground. Under USPTO practice, a modification to an existing drug is non-obvious if there was no clear reason, at the time of filing, to expect the modification would work as claimed. The bar is permissive. A new crystalline polymorph that dissolves at a slightly different rate can meet it. A new subcutaneous formulation of an intravenous antibody drug can meet it. A patent on a device button used to administer an existing drug has met it.

The USPTO’s stated mission includes ensuring the system is not used to ‘improperly delay’ generic entry, but its examination procedures do not require it to evaluate whether a claimed invention offers any clinical advantage over the parent compound. That is the gap where thickets form.

Track Two: FDA Regulatory Exclusivity

The FDA grants several categories of regulatory exclusivity that block generic or biosimilar approval regardless of patent status. New Chemical Entity (NCE) exclusivity runs five years from FDA approval for drugs with no previously approved active moiety. Orphan drug exclusivity runs seven years. Pediatric exclusivity adds six months to any existing patent or regulatory exclusivity period upon completion of qualifying pediatric studies. New Clinical Investigation exclusivity runs three years for approved changes to existing drugs supported by new clinical trials.

These exclusivities stack. A drug can hold NCE exclusivity, pediatric exclusivity, and multiple unexpired secondary patents simultaneously. Each layer reinforces the others, and each has a different expiration date, meaning the effective protection stack has a jagged profile rather than a clean cliff. This staggered profile is deliberate: it converts a single patent expiry into a multi-year exclusivity taper that biosimilar or generic entrants must model precisely before committing capital to a development program.

The Orange Book: The Listing that Launches a Thousand Lawsuits

The FDA’s Approved Drug Products with Therapeutic Equivalence Evaluations, universally called the Orange Book, is the authoritative list of approved small-molecule drugs and the patents that cover them. Under the Hatch-Waxman Act, brand-name manufacturers must list patents that claim the approved drug or a method of using it. Any generic applicant filing an Abbreviated New Drug Application (ANDA) must certify its position with respect to every listed patent.

The Paragraph IV certification, a declaration that listed patents are invalid, unenforceable, or will not be infringed by the generic product, is the formal mechanism for challenging brand patents. Filing a Paragraph IV triggers the right of the brand to file an infringement suit within 45 days. That lawsuit, once filed, activates an automatic 30-month stay of FDA generic approval regardless of the underlying patent’s merits. The brand collects monopoly revenue during those 30 months simply by filing. The patent does not need to be strong. It needs to exist and be listed.

The FTC challenged more than 100 Orange Book listings as improper in 2024, alleging patents on drug-device combination components were listed to trigger stays rather than because they claimed the drug itself. That action, while administratively novel, is a reactive enforcement tool rather than a structural fix.

The Purple Book: Biologics’ Information Gap

The Purple Book, the FDA’s equivalent list for licensed biological products and biosimilars, historically contained no patent information. A biosimilar developer preparing a Biologics License Application (BLA) had no formal mechanism to identify which of the brand’s patents it might infringe before committing years of development capital. The Biologic Patent Transparency Act, part of the Consolidated Appropriations Act of 2021, began requiring patent listings in the Purple Book, but the requirement is often triggered only after the ‘patent dance’ litigation process has commenced, limiting its utility as a pre-investment planning tool. This information asymmetry is a structural advantage for brand manufacturers in the biologics market.

Hatch-Waxman’s Structural Design: The 30-Month Stay as a Profit Engine

The Drug Price Competition and Patent Term Restoration Act of 1984 (Hatch-Waxman Act) created the ANDA pathway and, with it, the formal apparatus for generic patent challenges. The law’s design rests on a deliberate trade-off: generic companies get an expedited approval pathway that lets them rely on the brand’s safety and efficacy data; brand companies get formalized patent protection and, critically, the 30-month automatic stay.

What Congress did not fully anticipate was that the stay would be triggered not just on core compound patents but on every listed secondary patent, making the accumulation of secondary patents a reliably profitable strategy. A brand company that files 30 secondary patents and lists all of them in the Orange Book can generate up to 30 sequential or overlapping 30-month stays against a single generic challenger, provided it files infringement suits for each. The practical litigation timeline across a large thicket can extend well beyond the statutory 30-month period as case schedules compound.

BPCIA’s Patent Dance: Why Biologics Thickets Are Worse

The Biologics Price Competition and Innovation Act of 2009 (BPCIA) created the biosimilar approval pathway but substituted a completely different patent dispute process for Hatch-Waxman’s Paragraph IV framework. The BPCIA’s multi-step disclosure and negotiation sequence, the ‘patent dance,’ requires the biosimilar applicant to share its manufacturing and product information with the brand, after which the parties exchange lists of patents they believe are relevant and their positions on infringement and validity. The process unfolds across a series of statutory deadlines over roughly six months.

The critical design difference from Hatch-Waxman is that the BPCIA imposes no numerical limit on patent assertions. Under Hatch-Waxman, only listed Orange Book patents can be asserted in litigation linked to a Paragraph IV filing. Under the BPCIA, a brand can assert any patent it believes is relevant, which in practice means its entire portfolio can bear down on a single biosimilar applicant. AbbVie asserted more than 60 patents against each early Humira biosimilar developer in the patent dance. That number alone, at $775,000 to $1 million per patent in inter partes review (IPR) costs, creates a litigation liability approaching $60 million before a single hearing.

Key Takeaways: Section 2

Patent exclusivity and FDA regulatory exclusivity run on separate tracks and stack on the same drug, producing effective monopoly periods substantially longer than 20 years.

The 30-month automatic stay triggered by a Paragraph IV filing turns any listed Orange Book patent, regardless of merit, into a guaranteed revenue-extension tool.

The BPCIA’s unlimited patent assertion framework makes biologics thickets structurally more burdensome for biosimilar challengers than the Hatch-Waxman framework is for generic challengers.

The Purple Book’s patent information gap gives brand biologics manufacturers a pre-litigation information advantage.

Section 3: Anatomy of a Thicket: Corporate Strategies, Terminal Disclaimers, and Lifecycle Roadmaps

Primary vs. Secondary Patents: The Scaffold and the Fortification

A brand-name drug’s patent portfolio has two distinct architectural layers. The primary patent protects the novel active pharmaceutical ingredient (API), the molecule that produces the therapeutic effect. This patent typically files during or shortly after initial synthesis and represents the genuine scientific discovery that the patent system is designed to reward. A primary patent on a new molecular entity has a 20-year term from filing, but since it often files before IND submission, its effective commercial life is shorter still after subtracting the development and approval timeline.

Secondary patents, by contrast, file after the molecule is characterized, often after it is already approved, and target peripheral aspects: manufacturing processes, specific crystalline polymorphs, new salt forms, tablet coatings, delivery devices, extended-release formulations, fixed-dose combinations, new dosing regimens, and use patents for every additional indication the drug eventually gains approval to treat. An I-MAK analysis of the ten top-selling drugs in 2021 found that 72% of their patent applications were filed after initial FDA approval. A separate study found that 78% of all new drug-related patents cover existing medicines rather than novel therapeutic compounds. These two data points together describe a patent strategy that has shifted from protection of new discoveries to fortification of existing revenue streams.

The Evergreening Technology Roadmap

Evergreening is the systematic deployment of secondary patents to extend market exclusivity beyond the primary patent’s expiration. It operates through a predictable sequence of tactics, each tied to a specific phase of a drug’s commercial lifecycle.

Phase 1: Formulation Mining (Pre-Approval to Year 3) Before or shortly after approval, the company files patents on every viable salt, polymorph, and cocrystal of the API. A single small molecule can adopt dozens of crystalline forms with different solubility, stability, and bioavailability profiles. Each form can potentially support a separate patent. Some offer genuine pharmaceutical advantages; many are defensive filings designed to occupy IP space and complicate generic synthesis. Companies also file on every plausible oral formulation: immediate-release, extended-release, delayed-release, and dispersible tablet. If the drug has parenteral applications, they file on lyophilized formulations, reconstitution concentrations, and sterile fill-finish processes.

Phase 2: Indication Expansion Patenting (Year 3 to Year 10) As the drug moves through post-approval clinical trials for additional indications, each new therapeutic use generates a method-of-use patent. These patents run 20 years from their own filing dates, meaning a use patent filed in year 8 of a drug’s commercial life extends protection to year 28 from that filing. For biologics with multiple approved indications, this creates a portfolio of use patents with staggered expirations stretching years past the compound patent’s expiry.

Phase 3: Delivery System and Device Patenting (Year 5 to Year 15) Drugs delivered via autoinjectors, pen devices, prefilled syringes, or inhaler systems generate separate device patents. These patents cover the injector mechanism, force required for actuation, needle retraction systems, dose-confirmation windows, and, as in AbbVie’s case, the firing button itself. Device patents are filed on the delivery hardware, not the drug, making them resistant to the therapeutic equivalence arguments that work against compound or formulation patents. A biosimilar manufacturer must either design around the device or offer its own device, adding both cost and regulatory complexity.

Phase 4: Manufacturing Process Patenting (Ongoing) For biologics especially, cell-line development, purification chromatography steps, viral inactivation procedures, and fill-finish specifications are each independently patentable. Biosimilar manufacturers must demonstrate their manufacturing process produces a product with no clinically meaningful differences from the reference biologic. Any process patent that covers a step in the brand’s manufacturing process, even if the biosimilar uses a different process to achieve the same endpoint, can serve as the basis for an infringement claim that the brand must prove during the patent dance.

Phase 5: Product Hopping (Year 8 to Primary Patent Expiry) As the primary patent approaches expiry, the company launches a reformulated next-generation version of the drug. This new version, with its own package of secondary patents extending its protection, becomes the target of the company’s promotional investment. The original formulation may be deprioritized commercially or withdrawn entirely (‘hard switch’), stranding generic developers whose ANDA references the original product. Where a full withdrawal is not executed (‘soft switch’), prescribers are migrated through detailing, samples, and formulary management until the generic’s addressable market is too small to justify launch economics.

AstraZeneca’s migration from Prilosec (omeprazole) to Nexium (esomeprazole) remains the canonical product hop. The two molecules share structural near-identity: Nexium is the S-enantiomer of Prilosec’s racemate. AstraZeneca obtained patent protection on the isolated enantiomer, shifted its promotional budget entirely to Nexium before Prilosec’s patents expired, and sustained premium pricing through the transition. Merck is executing a contemporary version of this playbook with Keytruda’s subcutaneous reformulation, timed to launch before the IV formulation’s primary patents expire in 2028.

Terminal Disclaimers: The Legal Mechanism That Makes Duplicative Patenting Possible

Terminal disclaimers are the linchpin of patent thicket construction. When the USPTO examines a secondary patent application and finds it is ‘not patentably distinct’ from an earlier patent held by the same applicant, it rejects the application on grounds of obviousness-type double patenting. The standard rejection: you already have a patent on substantially this invention.

The applicant’s solution is to file a terminal disclaimer. This is a formal document in which the applicant agrees to two conditions: the new patent’s term will expire no later than the earlier patent’s term, and the two patents will be held by a common owner. By accepting these conditions, the applicant overcomes the double-patenting rejection and obtains the new, legally separate patent, even though it is substantively indistinguishable from the first.

The strategic value is precise. Each granted patent, however duplicative, is a distinct legal instrument that requires a separate legal proceeding to invalidate or design around. Rachel Goode’s peer-reviewed analysis found that approximately 80% of Humira’s U.S. patent portfolio was comprised of non-patentably distinct patents held together by terminal disclaimers. Each one can anchor a separate infringement lawsuit. Each lawsuit adds to the attrition cost for a biosimilar or generic challenger.

The Eliminating Thickets to Improve Competition (ETHIC) Act, introduced with bipartisan support in both chambers in 2025, targets terminal disclaimers directly. Its central provision would limit a brand-name company to asserting a single patent from any family of terminally disclaimed patents against a single challenger. If enacted, this change would collapse a 100-patent thicket of terminally disclaimed duplicates into a handful of distinct inventive groups, dramatically reducing the litigation attrition burden on challengers.

‘Pay-for-Delay’ as the Thicket’s Safety Valve

When a patent thicket produces litigation a brand is not fully confident it can win, the alternative is a reverse payment settlement, colloquially called ‘pay-for-delay.’ The brand compensates the generic challenger to drop its Paragraph IV filing and agree to a specific delayed market entry date, sometimes years beyond the date the brand’s patent is expected to expire or be invalidated. From the brand’s perspective, paying a generic company tens or hundreds of millions of dollars to stay off the market is rational so long as the expected settlement payment is less than the monopoly revenue that would be lost to earlier generic competition. The FTC has long argued these settlements violate antitrust law; the Supreme Court’s 2013 decision in FTC v. Actavis established that reverse payment settlements can be anticompetitive but declined to declare them per se illegal, leaving the analysis to a ‘rule of reason’ standard that is difficult and expensive to prove.

Key Takeaways: Section 3

Evergreening unfolds in a predictable five-phase sequence: polymorph and formulation mining, indication expansion patenting, device and delivery system patenting, manufacturing process patenting, and product hopping.

Terminal disclaimers allow companies to hold dozens of legally separate but substantively identical patents, converting a single inventive concept into a multi-front litigation campaign.

The ETHIC Act targets terminal disclaimers specifically; its passage would reduce effective thicket size without altering substantive patent rights on genuinely distinct inventions.

Pay-for-delay settlements function as a profit-sharing arrangement that resolves patent risk while preserving shared monopoly rent at the expense of patients and payers.

Section 4: IP Valuation Mechanics: How a Patent Portfolio Becomes a Balance Sheet Asset

For institutional investors and pharma/biotech IP teams, a patent portfolio is not just a legal asset. It is the primary driver of a drug’s net present value (NPV) model, and its effective life determines the discount rate applied to projected cash flows. Understanding how patent thickets translate into financial value requires understanding three valuation methodologies and the specific inputs that patent data feeds into each.

Discounted Cash Flow and Effective Market Exclusivity

The dominant pharmaceutical IP valuation approach applies DCF methodology to projected revenue streams, discounted to present value using risk-adjusted rates. The critical patent-specific input is effective market exclusivity (EME), the period during which the drug faces no generic or biosimilar competition. Each additional year of EME, whether generated by a primary patent, a secondary patent, or a regulatory exclusivity period, adds the full net revenue per year, multiplied by the probability that exclusivity is successfully maintained, to the drug’s NPV.

A drug generating $10 billion per year in net U.S. revenue with a 20% probability of biosimilar entry in year 5 has a different NPV than the same drug with a 5% probability of entry in year 10. Patent thicket density directly affects the entry probability estimate. When an internal IP team or investment bank builds a DCF model for a blockbuster biologic, the number of granted secondary patents, the proportion linked by terminal disclaimers, the number of active patent dance cases pending, and the settlement history with biosimilar developers all feed the entry probability estimate. A thicker, more recently filed, more litigated portfolio justifies a longer modeled exclusivity runway and a higher NPV.

This creates a direct financial incentive at the board and CFO level to invest in thicket construction. Filing and prosecuting 100 secondary patents costs tens of millions of dollars. The revenue benefit from extending a $10 billion-per-year drug’s exclusivity by a single year is $10 billion, net of generic erosion. The return on that IP investment is several orders of magnitude above the cost of any other capital allocation.

Comparable Transaction and Royalty Rate Methodology

When a patent portfolio is being acquired, licensed, or valued in an M&A context, analysts often benchmark to comparable transaction multiples or established royalty rates. For pharmaceutical patents, royalty rates on active compound patents typically range from 6% to 15% of net sales, depending on therapeutic area, remaining patent life, and Freedom to Operate (FTO) risk. Secondary patents, particularly those covering delivery devices or manufacturing processes, command lower standalone royalty rates but add value through their contribution to EME, which is captured in the DCF analysis rather than in royalty rate benchmarking.

The AbbVie acquisition of Allergan in 2020 ($63 billion) and the Bristol Myers Squibb acquisition of Celgene in 2019 ($74 billion) were both substantially valued on the basis of patent portfolio life. In Celgene’s case, the Revlimid thicket’s ability to sustain exclusivity through the mid-2020s was a core underwriting thesis for the $74 billion price. When BMS subsequently disclosed the volume-restricted settlement structure for Revlimid generic entry, that structure, limiting generic volumes as a percentage of total market in the early entry years, was a direct product of Celgene’s accumulated patent and REMS leverage. The acquisition price effectively purchased those restrictive settlement terms.

Real Options Valuation for Pipeline Patents

For earlier-stage assets, where clinical and commercial success is uncertain, real options valuation (ROV) provides a framework that explicitly prices the optionality of secondary patent filings. A Phase 2 asset with primary compound patent protection and a pipeline of filed-but-not-yet-granted secondary applications has option value embedded in those pending applications: the right, but not obligation, to obtain additional exclusivity layers as the drug advances. ROV models assign probability weights to each pending application based on grant rate, litigation risk, and expected commercial lifecycle timing.

This framework explains why pharma companies continue filing secondary patent applications throughout a drug’s commercial lifecycle rather than concentrating investment in the pre-approval period. Each new application is a low-cost real option on additional exclusivity. The filing cost is a few hundred thousand dollars. The option payoff, if the patent grants and withstands challenge, is years of additional monopoly revenue on a multi-billion-dollar product.

Investment Strategy: Patent Expiry Cliffs vs. Thicket-Protected Revenue

For analysts modeling pharmaceutical company revenues, the distinction between a true patent cliff and a thicket-protected revenue taper is the most important variable in near-term earnings estimates.

A true cliff occurs when a primary compound patent expires without meaningful secondary patent coverage and no product hop in progress. The brand loses 80-95% of unit volume to generics within 12-18 months. The revenue impact is sharp and largely irreversible.

A thicket-protected taper occurs when secondary patents create overlapping waves of litigation risk for generic or biosimilar entrants, staggering entry dates and suppressing the pace of volume erosion. For large biologics, the biosimilar interchangeability designation, which allows pharmacist-level substitution without prescriber intervention, is a separate and critical inflection point. Biosimilars launched without interchangeability status face a slower uptake curve regardless of price, because substitution requires active prescriber participation. Brand companies therefore have strong incentive to litigate biosimilar interchangeability designations as well as the core patent landscape.

The practical investment heuristic: for any drug generating more than $2 billion in annual U.S. revenue, model the full secondary patent landscape before estimating generic or biosimilar entry dates. Relying on primary patent expiry alone produces estimates that are systematically too early, undervaluing the brand’s near-term cash flow and overvaluing the generic or biosimilar entrant’s near-term earnings opportunity.

Key Takeaways: Section 4

Patent thicket density directly lengthens modeled effective market exclusivity, increasing a drug’s NPV and the return on portfolio IP investment.

The financial case for filing secondary patents is asymmetric: filing costs are tens of millions; the revenue benefit from even one year of extended exclusivity on a multi-billion-dollar product is multiple orders of magnitude higher.

M&A valuations in pharma routinely incorporate thicket depth as a core underwriting variable, as the Celgene acquisition demonstrates.

Biosimilar interchangeability designation is a separate competitive variable from patent status; brands contest it independently as part of their exclusivity defense strategy.

Section 5: Economic Consequences: The Price of Prolonged Monopoly

The Generic Entry Savings Data and What It Reveals

In 2022, generic and biosimilar medicines saved the U.S. healthcare system $408 billion. In 2023, the figure was $445 billion. Over the decade ending in 2023, cumulative savings reached $3.1 trillion. These numbers are presented by the industry as evidence of the generic system’s success, which they are, but they are also a direct measure of monopoly rent. Every dollar in generic savings represents a dollar that was extracted at brand-name prices before generic entry occurred. Every year of delayed generic entry captures an additional year of that rent for the brand.

Brand-name drugs represent approximately 10% of all prescriptions dispensed in the United States. They account for 86.9% of total prescription drug spending. That ratio, 10% of prescriptions consuming 87% of spending, is not a market outcome. It is a policy outcome, the result of a patent and regulatory framework designed to permit and sustain premium pricing across a small, high-revenue product segment.

Quantifying the Thicket Tax

An analysis of five drugs with documented patent thickets identified more than $16 billion in lost annual savings from delayed generic or biosimilar competition. Projecting that figure across the full landscape of thicket-protected drugs and years of delayed entry produces an estimated annual cost to the U.S. healthcare system measured in the tens to hundreds of billions of dollars.

The out-of-pocket burden falls with particular weight on lower-income patients. The average copay for a generic prescription in 2023 was $7.05. The average for a brand-name drug was $56.12. Among Americans earning less than $40,000 annually, approximately 37% report skipping doses, splitting pills, or forgoing prescriptions entirely because of cost. This is not a distributional accident. It is a predictable consequence of pricing structure that a competitive market would constrain but a patent-protected monopoly does not.

Patent Thickets as an Inflation Driver

Patent thickets do not merely hold prices at monopoly level; they enable continued price increases on that monopoly base. With no competitive pressure, brand manufacturers raise prices annually. Humira’s list price increased by approximately 18% per year between 2012 and 2016. Revlimid was repriced 22 times after launch, with its monthly cost rising from roughly $6,000 to over $24,000. Eliquis sustained high pricing through its entire pre-generic period because its patent landscape successfully deterred any competitive threat.

Annual price increases on patent-protected drugs compound over the thicket’s duration. A drug with a 5% annual list price increase held at monopoly pricing for eight extra years due to a patent thicket will, by year eight, cost 47% more than it did at primary patent expiration. This compounding effect means that the total cost of a patent thicket to the system is not simply the monopoly revenue multiplied by the delay years. It is the integral of an escalating price curve over the delay period.

The Infectious Disease Perverse Incentive

Gilead’s sofosbuvir (Sovaldi), launched in 2014 at $84,000 per complete treatment course for Hepatitis C, demonstrates a structurally distinct distortion. A curative drug for an infectious disease, priced at monopoly level, creates an incentive to limit access to the wealthiest patients while allowing the disease to circulate within lower-income populations. This sustains the disease reservoir and, consequently, future demand. The logic is not unique to Gilead; it applies to any curative therapy for an infectious condition where patent-protected pricing excludes a material fraction of the infected population.

Academic work by Cao et al. formalizes this relationship between patent-enabled pricing and income inequality. In highly unequal markets, the optimal monopoly price is set at a level that excludes a large proportion of potential patients, because the steep demand curve for high-income individuals yields greater revenue per unit than broad access pricing would. Greater financial inequality within a market widens the therapeutic gap between patent-price-accessible and price-excluded patients. The patent system, through the mechanism of exclusivity-based pricing, amplifies the healthcare impact of the pre-existing income distribution.

Key Takeaways: Section 5

Generic and biosimilar savings figures are simultaneously evidence of the generic system’s success and a direct measure of monopoly rent collected during the exclusivity period.

The 10%-of-prescriptions, 87%-of-spending split is a policy outcome, not a market outcome.

Annual price increases on patent-protected drugs compound over the thicket’s delay period, making the total cost of a thicket higher than a simple years-of-delay calculation suggests.

For curative infectious disease therapies, patent-protected pricing creates a structural incentive to maintain disease prevalence in populations that cannot afford treatment.

Section 6: The Innovation Paradox: R&D Displacement and Breakthrough Drug Attrition

The Industry’s Recoupment Argument

The pharmaceutical industry’s defense of extensive patenting rests on the economics of drug development. The cost estimates vary widely. Published figures range from $161 million to $4.5 billion per approved drug, with the industry as a whole spending $83 billion on R&D in 2019. The patent monopoly, in this framing, is what allows a company to recover that investment and generate the surplus needed to fund the next round of research.

This argument is not wrong in principle. It is wrong in its application to secondary patents on existing drugs. The recoupment argument justifies the primary patent on the novel compound. It does not justify the 78th patent on a new injector mechanism for a drug whose development costs were recovered years ago. By year ten of a blockbuster drug’s commercial life, the original R&D investment has typically been recovered many times over, and the revenue being protected by secondary patents is pure economic rent.

R&D Capital Displacement: The Hidden Cost

The most consequential and least quantifiable cost of patent thicket strategy is the R&D it displaces. Every dollar spent filing, prosecuting, and litigating secondary patents on existing drugs is a dollar not spent on the high-risk, high-cost research programs that produce genuinely new therapeutic modalities.

I-MAK’s analysis of the top ten drugs in 2021 found that 72% of their post-approval patent applications covered secondary characteristics. The scientific and regulatory talent involved in identifying patentable features of existing approved drugs, running the confirmatory studies needed to support those applications, and managing the resulting litigation dockets represents a substantial diversion of human capital from discovery research. Quantifying this displacement precisely is impossible because we cannot observe the R&D programs that were not initiated. But the data on where patent activity is concentrated, overwhelmingly in post-approval secondary patenting on commercially proven drugs rather than in pre-clinical or early clinical-stage novel therapies, indicates that the system’s incentive gradient points systematically toward lifecycle management and away from breakthrough discovery.

The High-Tech Analogy: A False Equivalence

Industry advocates frequently compare pharmaceutical patent portfolios to those of technology companies, noting that Apple or Samsung holds tens of thousands of patents. This comparison obscures a structural difference.

In the technology sector, a smartphone contains thousands of patented components owned by many different companies. A company builds a large patent portfolio primarily for cross-licensing: to gain the freedom to operate in markets where competitors hold relevant IP. The dominant economic function of a large technology patent portfolio is enabling participation through reciprocal licensing, not blocking it.

In pharmaceuticals, a single company typically holds all commercially relevant patents on its own drug. There is no competitor whose technology must be licensed for the drug to be manufactured or administered. The portfolio’s economic function is exclusionary, not collaborative. The asymmetric structure of pharmaceutical IP means that portfolio size directly translates into litigation attrition power against challengers, a purpose that has no equivalent in the cross-licensing dynamics of the technology sector.

Empirical Data on Thickets and Innovation

Econometric studies have found that patent thickets reduce R&D investment and slow innovation in industries with complex, overlapping IP environments. For biologics specifically, the multi-layered BPCIA patent dance process imposes transaction costs on both sides that deter early-stage research investment by smaller companies and startups that lack the capital to sustain a full patent dance engagement.

One analysis found that while large incumbent firms did not directly reduce absolute R&D spending in response to thicket density, the thickets negatively affected firm market value after controlling for R&D activity. Financial markets appear to discount thicket-heavy companies’ innovative capacity relative to their current patent count, treating dense secondary portfolios as cost centers rather than value generators. Separately, the presence of a large incumbent’s patent thicket in a given therapeutic area has measurable effects on the probability that smaller biotech companies initiate research programs in adjacent areas, suggesting a deterrent effect on the competitive innovation that typically drives down prices through different mechanisms in contested therapeutic categories.

Key Takeaways: Section 6

The R&D recoupment argument justifies primary compound patents, not post-approval secondary patents on drugs whose development costs were recovered years earlier.

R&D capital displaced by secondary patent prosecution and litigation represents a real opportunity cost in breakthrough drug attrition that cannot be directly quantified but is empirically directional.

The technology sector cross-licensing analogy fails because pharmaceutical IP portfolios serve an exclusionary rather than collaborative function.

Financial markets do not treat dense secondary patent portfolios as value-creating assets; empirical data suggests they associate thicket density with reduced innovative capacity relative to patent count.

Section 7: Case Studies in Strategic Patenting: The Blockbuster Playbook

7A: AbbVie / Humira (Adalimumab): IP Valuation Deep Dive

The Thicket

Humira, approved by the FDA in December 2002 for rheumatoid arthritis, generated peak annual U.S. revenues exceeding $20 billion before biosimilar entry. AbbVie filed more than 250 patent applications and secured at least 132 to 136 granted U.S. patents. Of those applications, 89% were filed after the initial FDA approval. Rachel Goode’s peer-reviewed analysis established that approximately 80% of the U.S. portfolio was non-patentably distinct from other portfolio patents, held together by terminal disclaimers.

The portfolio covered formulation variations, different concentration presentations (40mg/0.4mL vs. 40mg/0.8mL), administration methods, manufacturing processes, antibody purification techniques, the citrate-free formulation introduced around 2018, the autoinjector device, and the autoinjector’s firing button. Each element was a separately granted patent representing a separate litigation instrument.

The Biosimilar Delay and Its Cost

European biosimilar competition began in 2018. U.S. biosimilar entry did not occur until January 2023, a five-year gap attributable entirely to AbbVie’s U.S. patent thicket and the settlement agreements it produced. By the time biosimilars entered the U.S. market, Humira had generated daily revenues estimated at $47.5 million to $57 million. The economic cost of the five-year delay to U.S. payers has been estimated at $80 billion to more than $100 billion, depending on assumptions about biosimilar pricing and market penetration rates.

IP Valuation Analysis: AbbVie’s Humira Portfolio

At the time of U.S. biosimilar entry in 2023, the Humira portfolio’s residual patent value rested primarily on its citrate-free formulation patents (potentially extending to 2027) and device patents (extending to 2029 and beyond). These secondary patents contributed no FDA-recognized therapeutic advantage. The citrate-free formulation reduces injection site pain; it is a patient experience improvement, not a clinical efficacy advance. Under DCF methodology, the revenue contribution attributable to these secondary patents, measured as the difference between Humira’s price and the price at which the drug would have traded under full biosimilar competition, represents the patent thicket’s IP value to AbbVie’s balance sheet.

AbbVie’s market capitalization tracked closely with Humira exclusivity projections throughout the 2018-2023 period. Analyst consensus price targets for AbbVie during this window embedded 24 to 36 months of post-primary-patent U.S. exclusivity as a base case, with the secondary patent thicket providing the legal basis for that assumption. When biosimilar developers settled with AbbVie on January 2023 entry dates, those settlement dates were immediately reflected in sell-side revenue bridge models as the primary driver of near-term earnings estimates.

Antitrust Litigation: In re Humira Adalimumab Antitrust Litigation

The antitrust class action In re Humira Adalimumab Antitrust Litigation alleged that AbbVie’s accumulation of overlapping, duplicative patents constituted sham litigation and illegal monopolization under Section 2 of the Sherman Act. The Seventh Circuit affirmed the district court’s dismissal in 2022. The court’s reasoning: AbbVie engaged in hardball competitive tactics, not illegal conduct. Filing patents, listing them in the Orange Book equivalent for biologics, and asserting them against challengers is lawful petitioning activity protected by the Noerr-Pennington doctrine. The sham exception to Noerr-Pennington requires proving that the litigation was objectively baseless and subjectively motivated by anticompetitive intent. The court found the threshold not met.

The case is significant because it defines the outer boundary of permissible thicket conduct under current antitrust doctrine and establishes that density and duplicativeness alone are insufficient for a successful Section 2 claim. Future antitrust challenges will need to develop alternative legal theories, potentially focusing on settlement terms or conduct during the patent dance, to succeed where In re Humira failed.

Investment Strategy: AbbVie Post-Humira

AbbVie’s post-2023 revenue bridge relies on Skyrizi (risankizumab) and Rinvoq (upadacitinib), both of which are earlier in their commercial lifecycle and carry their own secondary patent portfolios. Analysts tracking AbbVie should model the secondary patent coverage on each successor asset with the same rigor applied to Humira. AbbVie’s institutional knowledge of thicket construction is its most durable competitive advantage; the question is whether its next-generation assets have the commercial scale to sustain a Humira-level IP defense.

7B: Merck / Keytruda (Pembrolizumab): The Subcutaneous Hop and the $137B Patent Wall

The Thicket

Keytruda received its first FDA approval in September 2014 for melanoma. It now holds approvals across more than 30 indications, making it the most widely approved oncology drug in history and the world’s best-selling pharmaceutical by revenue. Merck has filed at least 129 to 180 patent applications on pembrolizumab, generating 53 to 78 granted U.S. patents as of 2024. Over 60% of those applications were filed after the 2014 approval; 74% cover secondary features including new formulations, dosing regimens, and methods of treating specific cancer subtypes rather than the core anti-PD-1 antibody.

The primary patents on Keytruda’s active antibody structure are projected to expire in 2028. Secondary patents in the thicket extend protection to at least 2036, an eight-year gap representing the exclusivity window Merck’s lifecycle management strategy is designed to defend.

IP Valuation Analysis: Merck’s Keytruda Portfolio

I-MAK projected that the secondary patent wall would cost U.S. payers $137 billion in brand-price spending that would otherwise have been subject to biosimilar competition between 2028 and 2036. That figure represents the NPV of Merck’s secondary patent portfolio, expressed in healthcare expenditure terms.

Under DCF methodology, analysts modeling Merck’s revenue beyond 2028 must assign probability weights to two scenarios: full biosimilar interchangeability entry beginning in 2028 (the patent cliff case) and phased, litigated biosimilar entry with market share erosion that takes 5-7 years to reach 50% biosimilar penetration (the thicket taper case). The secondary patent count and structure, including the proportion covered by later-expiring use patents for specific oncology indications, is the primary variable distinguishing these scenarios. At Keytruda’s 2023 revenue run rate of over $25 billion annually, even a one-year difference in the modeled entry date changes Merck’s NPV by more than $25 billion.

The Subcutaneous Product Hop

Merck is actively developing a subcutaneous (SC) formulation of pembrolizumab, which delivers the drug via injection rather than a 30-minute intravenous infusion. The SC formulation is covered by its own set of secondary patents, separate from those on the IV formulation. The commercial strategy is to transition as many patients as possible to the SC formulation before IV patents expire in 2028, ensuring that the dominant commercial form of pembrolizumab at the time of biosimilar entry is covered by a newer, longer-lasting patent structure.

This is a technically sophisticated product hop. The SC formulation’s clinical differentiation, patient convenience and potential for outpatient administration without an infusion center, is real. That genuine clinical benefit does not change the competitive intent of the timing: launching the new formulation specifically to dilute the biosimilar market for the IV version is lifecycle management executed under cover of clinical development. For biosimilar developers building their reference product strategy now, the key question is whether to reference the IV formulation (facing a 2028 cliff with heavy secondary patent litigation risk) or to develop a biosimilar SC formulation (requiring its own regulatory pathway and facing the SC formulation’s patent structure). Neither option is straightforward.

Sell-side models for Merck post-2028 diverge significantly depending on thicket durability assumptions. A conservative model assuming rapid biosimilar entry in 2028 produces an earnings-per-share estimate 30-40% lower than a model assuming the secondary patent wall holds to 2034. Given the magnitude of this variance, investors should treat Keytruda exclusivity timeline as a scenario variable rather than a point estimate, and should track patent dance engagement notices from biosimilar developers as a leading indicator of expected entry dates.

Revlimid (lenalidomide), approved for multiple myeloma and myelodysplastic syndromes, generated over $12 billion in annual global revenue at its peak. Celgene (acquired by BMS in 2019) filed more than 200 patent applications on the drug, producing a thicket of over 100 granted patents. The primary compound patent expired in 2019.

Celgene’s most operationally distinctive tactic was the weaponization of Revlimid’s Risk Evaluation and Mitigation Strategy (REMS). FDA-mandated REMS programs exist for drugs with serious safety risks requiring specific controls. Revlimid carries a strict REMS, RevAssist, because of its severe teratogenicity (it is structurally related to thalidomide) and venous thromboembolism risk. The program requires prescriber certification, patient enrollment, mandatory pregnancy testing, and controlled distribution.

Under the REMS framework, generic manufacturers seeking FDA approval must conduct bioequivalence testing, which requires access to the reference listed drug for comparison studies. Celgene refused to provide Revlimid samples to generic developers, arguing that the REMS program’s safety controls prevented distribution to parties outside the controlled network. Several generic developers filed suit; Celgene settled and eventually agreed to provide samples, but the delay added years to the development timelines of generic entrants. A Federal Trade Commission study found that REMS programs had been used by multiple brand manufacturers as gatekeeping tools against generic competition, prompting the FTC to pursue rulemaking that would prohibit this practice.

Volume-Restricted Generic Settlement Structure

Even after generic entry, Celgene and BMS structured settlement agreements with generic manufacturers that allowed only limited market share in the early entry years, with restrictions specified as a percentage of total Revlimid dispensing. This volume-restriction framework, first exposed in I-MAK’s 2025 analysis, means that generic competition has existed nominally since early 2022 but has not produced the 80-95% price erosion typical of fully competitive generic markets. The brand and a handful of authorized generic manufacturers are sharing a controlled market under the settlement terms, with volumes calibrated to sustain pricing above what unrestricted competition would produce.

IP Valuation Analysis: Revlimid’s Residual Portfolio

BMS’s $74 billion acquisition of Celgene in 2019 was substantially valued on the expectation that Revlimid’s patent thicket and REMS leverage would sustain meaningful exclusivity through the mid-2020s. The volume-restricted settlement structure, which BMS negotiated from the position of control that Celgene’s pre-acquisition patent litigation created, is the financial realization of that IP value. The patent portfolio did not block generic entry indefinitely; it produced settlement terms that share monopoly economics rather than eliminate them.

For analysts valuing BMS, Revlimid’s royalty streams and contracted generic volumes through the settlement period represent a declining but still material revenue contributor. The settlement architecture’s specific volume caps and entry timing should be modeled as a distinct revenue scenario from either full monopoly (no generics) or full competition (unrestricted generics).

BMS faces a simultaneous cliff profile across Revlimid, Opdivo (nivolumab), and Eliquis. Revlimid’s volume-restricted settlements provide a managed revenue taper rather than a cliff. Opdivo faces biosimilar competition on a timeline that depends on its own secondary patent landscape. Eliquis, co-developed with Pfizer, is analyzed in Section 7D.

7D: Bristol Myers Squibb and Pfizer / Eliquis (Apixaban): Patent Term Extension Stacking and the 2031 Settlement Map

The Thicket and PTE Mechanism

Eliquis (apixaban), an oral factor Xa inhibitor for atrial fibrillation and venous thromboembolism, was approved by the FDA in December 2012. BMS and Pfizer co-market the drug, which generated approximately $12 billion in annual U.S. revenue at peak. The base compound patent was nominally set to expire on September 17, 2022.

The companies extended that date through a nearly five-year Patent Term Extension (PTE), the maximum statutory extension available under Hatch-Waxman to compensate brand-name manufacturers for the regulatory review period. A PTE is granted by the USPTO upon application, up to a ceiling of five years, calculated as half the IND period plus the NDA review period. The Eliquis PTE extended the effective compound patent expiry to approximately April 2028.

On top of the PTE, BMS and Pfizer accumulated a portfolio of 48 filed and 27 granted secondary patents. The combination of a maximum PTE and a secondary patent thicket produced settlements with generic challengers that pushed effective generic entry to specific managed dates, the earliest of which are April 2028, with several settlements extending to 2031. The projected additional U.S. revenue collected during the period from the original 2022 expiry to 2028, which generic competition would otherwise have eroded, has been estimated at over $50 billion.

Patent Term Extension Mechanics

A PTE under 35 U.S.C. 156 compensates for two periods: the clinical testing phase after IND submission and the FDA regulatory review after NDA submission. The maximum extension is five years; the maximum total patent life, including the PTE, cannot exceed 14 years from approval. Only one patent per approved drug is eligible for a PTE, and the applicant selects which patent to extend.

The strategic decision of which patent to designate for PTE extension is itself IP strategy. Designating the compound patent maximizes the extension’s commercial value because it protects the broadest claim. Designating a formulation or use patent is sometimes chosen when the compound patent is already expiring or has been successfully challenged, but this is a secondary strategy.

For analysts, the Eliquis settlement map requires a waterfall model rather than a single entry date. Different generic manufacturers hold settlements with different entry dates: some enter in April 2028, others are conditioned on specific litigation outcomes, and others extend to 2031. The practical commercial impact is phased volume erosion beginning in 2028, with the pace of generic market share gain determined by the number of manufacturers commercially active at each stage. Analysts should map each settlement’s terms against each generic developer’s manufacturing readiness and pricing strategy to build a credible revenue bridge through 2031.

Summary Comparison Table: The Blockbuster Playbook

Drug (Manufacturer)

Primary Patent Expiry

Total Patents Filed / Granted

Core Tactics

Effective Monopoly Extension

Estimated System Cost

Humira (AbbVie)

2016

250+ / 130+

Thicket, terminal disclaimers, device patents

7 years (2016-2023)

$80B-$100B+

Keytruda (Merck)

2028

180+ / 78+

Patent wall, SC product hop, indication use patents

Maximum PTE, secondary patents, managed settlements

6-9 years (2022-2028/2031)

$50B+

Section 8: The Biologics-Specific Thicket: BPCIA Patent Dance Mechanics and Biosimilar Interchangeability Barriers

How the Patent Dance Operates in Practice

The BPCIA’s patent exchange process begins when a biosimilar applicant files a BLA referencing an approved biologic as its reference product. Within 20 days of FDA notification that the BLA is accepted for filing, the biosimilar applicant must provide the brand manufacturer (reference product sponsor, or RPS) with a copy of the application and manufacturing information. The RPS then has 60 days to provide a list of patents it believes could reasonably be asserted against the biosimilar. The biosimilar applicant counters with its own list and its positions on infringement and validity for each patent. The parties then enter a 15-day negotiation to agree on which patents will be litigated in the first wave of litigation. If no agreement is reached, the applicant selects up to one patent and the RPS selects the remaining disputed patents for the first wave.

This sequence means that a biosimilar developer is compelled to disclose its manufacturing process to the brand manufacturer early in the approval process, before litigation has been initiated. The brand manufacturer can use the disclosed manufacturing information to identify process patents it might assert. The information flow is formally reciprocal but practically asymmetric: the biosimilar developer needs to disclose everything about how it makes the product, while the brand’s disclosure is limited to identifying relevant patents, which the brand was already aware of.

The unlimited patent assertion feature is the most commercially damaging element. AbbVie designated more than 60 patents for immediate litigation against each biosimilar developer in Humira’s patent dance. At $775,000 to $1 million per patent in IPR proceedings, a developer facing 60 asserted patents confronts a litigation liability exceeding $60 million before a single hearing on validity. Most biosimilar developers are not large enough to sustain that litigation burden unilaterally, producing the settlement dynamic that allows brands to extract delayed entry dates as the price of resolving the litigation.

Biosimilar Interchangeability Designation: The Second Barrier

Biosimilar interchangeability, as defined under the BPCIA, means that a biosimilar can be substituted for the reference product at the pharmacy level without prescriber intervention, the same mechanism that governs generic substitution for small-molecule drugs. An interchangeable biosimilar requires separate FDA approval beyond basic biosimilarity, including evidence from a switching study demonstrating that alternating between the biosimilar and the reference product produces no greater risk than using the reference product alone.

Brand manufacturers contest interchangeability applications independently of patent litigation, using the FDA’s comment period on biosimilarity and interchangeability designations to raise scientific objections. The practical effect is that biosimilars launching without interchangeability status face a slower commercial uptake than generic drugs, because substitution requires active prescriber participation. Physicians accustomed to prescribing the brand may not switch patients without a specific reason, limiting the biosimilar’s market penetration even when it is priced at a 20-30% discount.

The combination of patent litigation, BPCIA patent dance burden, and interchangeability hurdle creates a three-stage barrier for biologic competition that has no equivalent in the small-molecule generic market.

The Biologic Technology Roadmap: Post-Patent Competition Dynamics

Once patent barriers are cleared and biosimilar interchangeability is established, biologic market dynamics differ from small-molecule generic markets in ways that are important for pricing and market share models.

In small-molecule generics, automated substitution drives rapid and deep price erosion. Brand-to-generic price discounts of 80-95% are reached once five or more generics compete. In biologics, price erosion is slower for structural reasons: manufacturing complexity limits the number of competitive entries, payer contracts and rebate structures favor formulary consolidation around one or two preferred biosimilars, and physicians have genuine, if sometimes overstated, concerns about immunogenicity and switching that sustain some brand preference. Empirically, biosimilar price discounts have averaged 15-35% versus reference product list prices, compared to 40-95% for small-molecule generics.

This slower price erosion in biologics means that even after full biosimilar market entry, the brand can sustain meaningful revenue at a reduced price level, particularly among patient populations covered by plans that prefer the brand for rebate-related reasons. The brand’s patent thicket therefore does not need to delay entry indefinitely to be financially valuable; it needs only to sustain monopoly pricing long enough to optimize the NPV of the thicket construction investment.

Key Takeaways: Section 8

The BPCIA patent dance compels manufacturing disclosure to the brand before litigation begins, creating an information asymmetry that favors the reference product sponsor.

Unlimited patent assertion under the BPCIA converts large secondary portfolios into litigation cost weapons; each patent asserted adds $775,000 to $1 million in potential IPR costs for the biosimilar developer.

Biosimilar interchangeability designation is a separate regulatory hurdle from patent clearance; brands contest it independently and its absence slows biosimilar market penetration regardless of pricing.

Biologic price erosion post-patent entry averages 15-35%, compared to 80-95% for small-molecule generics, making the biologic market structurally more favorable to brand value retention even after competition enters.

Section 9: The Global Patent Gap: USPTO vs. EPO Standards and the Price Differential They Produce

Where the Systems Diverge

The European Patent Office administers patent examination under the European Patent Convention (EPC) with standards that are, in aggregate, materially stricter than the USPTO’s, particularly for the types of secondary pharmaceutical patents that form thickets. The divergence is not a matter of European regulatory philosophy being inherently anti-innovation; it reflects a consistent application of higher evidentiary bars across four specific doctrinal areas.

Non-Obviousness vs. Inventive Step

The USPTO’s non-obviousness standard, codified under 35 U.S.C. 103, requires that a claimed invention would not have been obvious to a person of ordinary skill in the relevant art at the time of filing. Courts and examiners have interpreted this standard in ways that generally require a specific ‘teaching, suggestion, or motivation’ in the prior art to combine existing elements before a combination can be deemed obvious. Absent such specific prior art motivation, the combination is treated as non-obvious even if it produces predictable results.

The EPO applies an ‘inventive step’ analysis using its problem-solution approach, which asks whether the claimed invention would have been obvious to a skilled person in view of the closest prior art, given the technical problem the invention solves. Critically, the EPO asks whether the skilled person would have had a reasonable expectation of success in arriving at the claimed solution, a framing that tends to find obvious combinations more readily when the technical domain is well understood. For pharmaceutical formulations, where the chemistry of salt forms, polymorphs, and extended-release mechanisms is mature science, the EPO’s standard rejects more secondary applications as obvious than the USPTO’s does.

Double Patenting

The EPO prohibits double patenting outright under Rule 36 EPC: two European patents cannot be granted to the same applicant for the same invention. There is no mechanism equivalent to the terminal disclaimer for overcoming this prohibition. This rule closes the single most important structural pathway through which U.S. thickets are built. An applicant who exhausts its inventive concept in a first patent cannot obtain a second, substantively identical patent by agreeing to link expiration dates.

Added Matter

EPO Article 123(2) EPC prohibits amendment of a European patent application to add subject matter not disclosed in the application as filed. This is a strict standard, enforced during both examination and post-grant opposition. Its practical effect is to prevent the gradual broadening of claims during prosecution that allows U.S. applicants to expand a narrow filing into a broad patent covering developments discovered after the original filing date.

Prophetic Examples and Enablement

The EPO’s sufficiency of disclosure standard requires that the claimed invention be plausibly achievable across its full claimed scope based on information available at the filing date, supported by actual experimental data for biological activity claims. The USPTO has historically permitted ‘prophetic examples,’ descriptions of experiments that have not been conducted, framed in past tense as if completed. This distinction allows U.S. applicants to obtain broader claims on the basis of less empirical evidence, producing patents that cover more territory than the applicant has actually demonstrated.

The Real-World Output: Four Times More Patents Per Drug in the U.S.

An I-MAK analysis comparing patent grants for the top-selling drugs in 2021 found that over four times as many patents were granted per drug in the United States as in Europe. For Humira, the practical consequence was that biosimilar competition began in Europe in 2018, compared to the U.S. in 2023. For U.S. patients, that five-year gap cost an estimated $80-100 billion in healthcare spending at brand-name prices.

The divergence is not a consequence of different legal philosophies about the value of innovation. Both the U.S. and EU grant robust patent protection for genuinely novel inventions. The divergence is specific to secondary pharmaceutical patents on existing drugs, where the EPO’s stricter standards systematically prevent the accumulation of the type of duplicative, marginally inventive IP that forms thicket infrastructure.

Comparative Analysis: USPTO vs. EPO Secondary Patent Standards

Doctrine

USPTO Standard

EPO Standard

Thicket Impact

Inventive Step / Non-Obviousness

Requires specific teaching/suggestion/motivation to combine prior art

Problem-solution approach; reasonable expectation of success in combination can establish obviousness

USPTO’s standard allows more marginal secondary patents to issue

Double Patenting

Permitted via terminal disclaimer linking expiration dates

Strictly prohibited; no equivalent mechanism to terminal disclaimer

EPO prohibition blocks the core thicket construction tactic

Added Matter

Flexible; claim broadening during prosecution is permitted

Strict prohibition on matter not present in original filing

EPO rule prevents gradual thicket expansion from a single initial filing

Enablement / Sufficiency

Allows prophetic examples without empirical data

Requires actual experimental data for biological activity claims

EPO standard filters out speculative patent applications

Medical Method Patents

Methods of treating patients are patentable

Surgical and therapeutic methods excluded from patentability

EPO exclusion removes a category of use patents common in U.S. thickets

Investment Strategy: Geographic IP Strategy for Multinational Portfolio Analysis

For analysts or IP teams evaluating a pharma company’s global IP position, the USPTO/EPO divergence has direct financial implications. A U.S. patent grant does not predict European grant for the same application. A company with 100 U.S. secondary patents may hold 20-25 European patents, and the European portfolio offers considerably less thicket utility under the stricter standards.

For biosimilar developers considering global commercialization, European market entry is structurally easier than U.S. entry for most reference biologics. This creates a revenue opportunity in Europe that partially offsets the higher U.S. litigation costs and longer U.S. entry timelines. Conversely, for brand-name manufacturers relying on U.S. thicket strategy, European market share erosion begins years earlier than U.S. erosion, and the European revenue decline is a leading indicator of the trajectory that U.S. revenues will eventually follow once the domestic thicket is cleared.

Section 10: The Formulary Wall: How PBM Rebate Architecture Extends Brand Monopoly After Patent Expiration

PBM Market Structure and Vertical Integration

Pharmacy Benefit Managers sit between drug manufacturers and health plan members, administering prescription drug benefits for insurers, employer health plans, and government programs. The market is highly concentrated: CVS Caremark (part of Aetna/CVS Health), Express Scripts (part of Cigna), and Optum Rx (part of UnitedHealth Group) manage benefits for more than 80% of commercially insured Americans.

Each of the three dominant PBMs is a subsidiary of a vertically integrated healthcare conglomerate that also owns a major health insurer and, in CVS’s case, the largest retail pharmacy chain in the United States. This vertical integration means the same corporate parent can simultaneously decide which drugs are covered on the formulary, determine the insurance plan’s cost-sharing structure for those drugs, and process the prescription at its own pharmacy. The alignment of these decisions within a single corporate structure concentrates market power in ways that have drawn sustained Congressional scrutiny.

Rebate Mechanics and the Brand Drug Preference Incentive

PBMs negotiate rebates from manufacturers as a condition of favorable formulary placement. Rebates are paid retrospectively, calculated as a percentage of a drug’s list price (gross price before discounts). A drug with a $1,000 monthly list price offering a 30% rebate generates $300 per patient-month for the PBM and its plan sponsor. A therapeutically equivalent drug with a $200 monthly price offering a 15% rebate generates $30 per patient-month.

The per-unit rebate dollar amount on the brand drug is ten times higher than on the lower-priced competitor, despite the brand costing five times as much to dispense. Under formulary systems where the PBM retains a portion of the rebate or where plan sponsor contracts tie PBM compensation to rebate performance, the financial incentive favors formulary placement of higher-priced, higher-rebate brands over lower-priced alternatives, even when the lower-priced drug is therapeutically equivalent.

This mechanic produces the ‘formulary wall’: a commercial barrier that can block a generic or biosimilar from gaining market share even after it has cleared every patent in a thicket and received FDA approval. If the PBM places the generic on a non-preferred formulary tier with a higher patient copay than the brand’s preferred tier copay, patient and prescriber behavior will favor the brand on cost grounds at the point of dispensing, regardless of the drug’s actual price to the plan.

The Rebate Trap: How High Prices Enable Better Formulary Position

The rebate system creates a self-reinforcing loop with the patent thicket. The thicket maintains high brand list prices. High list prices support large absolute rebate payments. Large rebate payments purchase preferred formulary placement. Preferred formulary placement sustains brand market share and the revenue base from which the next round of price increases is applied. The PBM system does not create patent thickets; it provides a commercial mechanism that extends their effective monopoly period beyond patent expiry.

Congressional investigation of this dynamic has produced legislative proposals to delink PBM compensation from list price, require PBMs to pass rebate value to patients at the point of sale, and ban ‘spread pricing,’ a practice by which PBMs charge plan sponsors more for a drug than they reimburse the dispensing pharmacy, retaining the spread as revenue. The Inflation Reduction Act of 2022 included limited rebate reform provisions for Medicare Part D, though the full restructuring of the rebate system for commercial markets remains unaddressed by federal legislation.

Key Takeaways: Section 10

The three dominant PBMs control benefits for more than 80% of commercially insured Americans, concentrating commercial gatekeeper power in an oligopoly.

Rebates calculated as a percentage of list price create a per-unit revenue incentive that favors higher-priced brand drugs over lower-priced generics, even when the lower-priced drug is therapeutically equivalent.

The formulary wall can sustain brand market share and pricing after patent expiry, extending the practical monopoly period independent of any remaining legal exclusivity.

A comprehensive solution to the patent thicket problem that does not also address PBM rebate mechanics will produce patent reform that is commercially neutralized at the formulary level.

Section 11: Legislative, Regulatory, and Antitrust Pathways to Reform

The ETHIC Act: Targeting Terminal Disclaimers Directly

The Eliminating Thickets to Improve Competition (ETHIC) Act, introduced with bipartisan support in both the House and Senate, is the most precisely targeted legislative proposal in the current reform landscape. Its operative provision: limit a brand-name manufacturer to asserting a single patent from any family of terminally disclaimed patents against a single generic or biosimilar challenger.

Under the current framework, a company holding 80 terminally disclaimed patents can file 80 separate lawsuits against the same challenger or assert all 80 in a single proceeding, each requiring independent invalidity analysis. The ETHIC Act collapses that arsenal: if 80 patents are terminally disclaimed to a common parent, the company picks one to defend. If that one fails, the family is cleared. This does not invalidate the patents; it removes their attrition value as litigation instruments, which is precisely their function in a thicket.

C4IP (Coalition for Intellectual Property) filed formal opposition in August 2025, arguing the Act would ‘destabilize the innovation ecosystem’ by reducing the value of follow-on pharmaceutical innovation. The opposing argument: secondary patents on existing drugs that are non-patentably distinct from the primary compound are, by definition, not independently innovative. The USPTO has already determined they are duplicative; the terminal disclaimer is how the applicant overcomes that determination. Limiting the litigation value of patents that have been formally classified as duplicative is not destabilizing innovation; it is enforcing the implications of the USPTO’s own analysis.

Inter Partes Review as a Thicket-Clearing Tool

Inter partes review (IPR), established by the America Invents Act in 2011, allows any party to challenge a granted patent’s validity before the USPTO’s Patent Trial and Appeal Board (PTAB). IPR proceedings are faster and less expensive than full district court litigation, and the PTAB has a higher invalidity rate than federal courts.

At $775,000 to $1 million per patent, IPR is a meaningful tool for targeted challenges against the most commercially important patents in a thicket. For a thicket of 100 patents, IPR for all is prohibitively expensive; for a targeted set of 5 to 10 patents covering the most clinically relevant aspects of the drug, IPR can be a viable clearance strategy. Generic and biosimilar developers have used IPR to knock out individual thicket patents, though the brand’s ability to file continuation applications and assert new patents after IPR decisions limits the strategic value of this approach when the brand has a large active application pipeline.

USPTO-FDA Collaboration: Closing the Information Gap

The USPTO and FDA launched formal collaboration initiatives to address the regulatory gap that allows patents on trivially different modifications to trigger competition delays. The collaboration focuses on providing USPTO patent examiners with FDA data on clinical context, including whether a claimed modification to an existing drug offers measurable therapeutic benefit.

This is structurally necessary: a USPTO examiner assessing the non-obviousness of a new extended-release formulation currently has no systematic access to FDA clinical trial data showing whether the extended-release version produces better patient outcomes than the immediate-release original. Without that context, the examiner is assessing a chemistry question (is this formulation new and non-obvious as a matter of synthesis?) rather than a clinical value question (does this formulation do anything meaningfully different for patients?). The patent system as currently designed does not require clinical differentiation for secondary formulation patents, but closer inter-agency coordination could at least ensure examiners are making informed decisions about whether the ‘utility’ requirement is genuinely met.

FTC and DOJ Antitrust Enforcement: The Limits of Current Doctrine

The FTC’s aggressive challenge to more than 100 Orange Book listings in 2024 as improper represents a targeted use of administrative authority rather than a structural antitrust case. The FTC can challenge a specific listing as covering a device component rather than the drug itself; it cannot challenge the listing practice in general.

For a direct antitrust challenge to patent thicket construction, the FTC or DOJ must prove either an illegal monopolization scheme under Section 2 of the Sherman Act or a per se illegal restraint of trade under Section 1. The In re Humira outcome demonstrates the difficulty of Section 2 claims against thickets: Noerr-Pennington protects the act of filing patents and lawsuits, and the sham exception requires meeting an objective baselessness standard that courts have been reluctant to apply to pharmaceutical patent litigation.

The more promising antitrust path runs through settlement analysis. Reverse payment settlements (pay-for-delay) have been litigable under the rule of reason since FTC v. Actavis (2013), and volume-restricted generic settlement structures may offer a theory of harm that the in-litigation patent assertion cases do not. An antitrust challenge to a volume-restricted settlement could argue that restricting generic market share through a settlement agreement, separate from any patent that has been adjudicated, constitutes an unlawful division of the market.

The Whack-a-Mole Risk in Piecemeal Reform

Any reform strategy that addresses a single component of the thicket system risks displacement: companies shift resources from the constrained tactic to an unconstrained one. If the ETHIC Act limits terminal disclaimer-based litigation, companies may respond by filing more structurally distinct secondary patents earlier in the drug’s lifecycle. If Orange Book listing reform constrains device patent assertions, companies may shift emphasis to manufacturing process patent litigation under the BPCIA framework.