The pharmaceutical patent cliff narrative has dominated investor and analyst conversations for two decades, but it increasingly misses the point for a large and growing portion of the market. A significant share of blockbuster revenue sits behind barriers that have almost nothing to do with composition-of-matter patent expiry. The real moat is built from advanced drug delivery systems, and the tools for building and reading that moat are poorly understood outside specialist circles.

This article is a technical deep-dive for pharma IP teams, portfolio managers, R&D leads, and institutional investors. It goes significantly further than the original treatment of this topic at DrugPatentWatch, expanding each section with the specific technical, regulatory, and financial detail that decision-makers need. The goal is a single authoritative reference for understanding how delivery-system complexity functions as durable market exclusivity — and how to price it.

The Landscape: From Hatch-Waxman to the Delivery Age

The Hatch-Waxman Act of 1984 created the modern generic industry. Its central mechanism, the Abbreviated New Drug Application (ANDA), allowed generic manufacturers to reference an innovator’s clinical data without repeating it, provided they demonstrated bioequivalence (BE) to the Reference Listed Drug (RLD). The result has been substantial: the U.S. healthcare system saved over $3 trillion from generics in the decade through 2024, and generics account for more than 90% of all prescriptions filled.

That mechanism worked well when the RLD was a small-molecule oral tablet. It began to break down when the ‘product’ was no longer a pill but an intricate delivery system.

The shift has been gradual but now reaches a critical mass. Injectables, inhaled therapies, transdermal systems, ocular formulations, and the early wave of nanomedicines collectively represent a market segment where the ANDA pathway, in its traditional form, cannot function as designed. The FDA acknowledged this explicitly through its Drug Competition Action Plan (DCAP) and the near-1,900 Product-Specific Guidances (PSGs) it has published — more than 25 of the 47 new draft PSGs issued in a single 2023 update targeted complex drugs alone.

The commercial stakes are substantial. The global specialty generics market was valued at approximately $69.9 billion in 2022 and is projected to reach $148.7 billion by 2030, compounding at roughly 9.9% annually. Injectable formulations account for over 64% of that revenue. Behind those numbers is a structural reality: the products generating that revenue are materially harder to copy than anything the industry dealt with in the 1990s.

Defining Advanced Drug Delivery Systems (ADDS): A Technical Reference

What ADDS Does That a Pill Cannot

An Advanced Drug Delivery System is a formulation, device, or integrated formulation-device combination engineered to control drug behavior after administration. The two governing objectives are spatial targeting — getting the drug to the site of action rather than distributing it systemically — and temporal control, which governs the release rate and concentration-time profile over the dosing interval.

These objectives matter clinically because conventional immediate-release formulations produce concentration peaks that often drive adverse effects and troughs that allow disease breakthrough. The design of an ADDS directly manipulates that curve, compressing peak-to-trough ratios, extending therapeutic windows, or directing drug to tissue compartments where systemic exposure would be toxic.

Platform Categories with Mechanistic Detail

Lipid-based systems span a wide spectrum of structural complexity. Simple oil-in-water emulsions occupy one end; PEGylated liposomes, such as those used in Doxil, occupy the other. A liposome is a phospholipid bilayer vesicle that encapsulates a hydrophilic drug in its aqueous core while simultaneously accommodating lipophilic agents in the bilayer itself. PEGylation — grafting polyethylene glycol chains to the outer surface — reduces uptake by the mononuclear phagocyte system and extends circulation half-life from hours to days, producing the ‘stealth’ effect that allows doxorubicin to accumulate preferentially in tumor tissue through the enhanced permeability and retention (EPR) mechanism. Replicating this exact architecture, including the PEG density, chain length, and resulting zeta potential, is analytically demanding and manufacturing-sensitive.

Polymer-based systems use biodegradable polymers — most commonly poly(lactic-co-glycolic acid), or PLGA — to form microspheres or in-situ forming depots that hydrolyze slowly in vivo, releasing the encapsulated drug over days to months. The critical quality attributes (CQAs) that govern release kinetics include the polymer’s molecular weight and polydispersity index, the lactide-to-glycolide ratio, and whether the terminal groups are acid-capped or ester-capped. The differences between a 50:50 PLGA with acid end groups and a 75:25 PLGA with ester end groups are invisible in a standard chemical assay but produce dramatically different in-vivo release profiles. This mechanistic invisibility is one reason PLGA microsphere products have proven so resistant to generic entry.

Drug-device combinations range in complexity from a relatively simple transdermal patch to an auto-injector co-engineered with a specific drug formulation. The defining characteristic is that the device is not passive packaging — it actively controls the dose, rate, or targeting of delivery. Dry powder inhalers (DPIs) generate turbulent flow fields that de-agglomerate drug-lactose blends into respirable particles; the device geometry directly determines the fine particle fraction (FPF), which in turn determines therapeutic effect in the lungs. A generic that copies the drug but uses a different device cannot be assumed therapeutically equivalent without clinical proof.

Antibody-drug conjugates (ADCs) represent the most technically sophisticated ADDS category currently in commercial use. They consist of a monoclonal antibody, a cytotoxic payload, and a linker chemistry that must remain stable in circulation but release drug efficiently within the target cell. The drug-to-antibody ratio (DAR), the site-specificity of conjugation, and the linker’s stability profile are all critical and interrelated. The analytical characterization required to define these attributes — let alone replicate them — exceeds what most generic manufacturers have encountered in any prior development program.

The ‘Enabling’ Function of ADDS

A point frequently underweighted in strategic discussions: ADDS does not just protect existing molecules. It enables molecules that could not otherwise reach the market. A highly potent cytotoxic compound with poor aqueous solubility may be physically impossible to administer safely without nanoparticle encapsulation. A peptide drug with a 20-minute half-life is clinically useless without a depot formulation that extends activity to weeks. In both cases, the delivery system does not improve the drug; it creates it as a commercial product. This means the ADDS platform carries independent commercial value separable from the API itself — a point with direct implications for IP valuation.

Key Takeaways: ADDS Technology

ADDS controls drug fate through spatial targeting and temporal release engineering, not just passive absorption.

PLGA microsphere CQAs (MW, PDI, lactide:glycolide ratio, end-cap chemistry) are the primary determinants of release kinetics and are extremely difficult to replicate without the innovator’s proprietary manufacturing process.

PEGylated liposomes achieve extended circulation through steric stabilization; the PEG density and chain length are themselves patentable and analytically detectable.

ADDS can be ‘enabling’ for molecules that have no viable alternative delivery route — making the platform’s IP value independent of the API patent estate.

ADC complexity (DAR distribution, linker stability, conjugation site-specificity) is categorically beyond the characterization and manufacturing capabilities of traditional generic firms.

The Complex Generic Classification: FDA vs. EMA, Compared

FDA: The ‘Complex Generic’ Framework

The FDA classifies a drug as a complex generic when it has one or more of the following characteristics: a complex active ingredient (peptide, polymeric compound, naturally derived substance); a complex formulation (liposome, colloid, emulsion); a complex route of delivery (topical, ophthalmic, otic); a complex dosage form (transdermal patch, metered-dose inhaler, extended-release injectable); or a complex drug-device combination. Each category triggers a distinct evidentiary burden.

The regulatory home for most complex generics remains the ANDA pathway under Section 505(j) of the FD&C Act, or occasionally the 505(b)(2) pathway when hybrid innovation-plus-reference-data submissions are appropriate. The difference matters for exclusivity: a 505(b)(2) NDA can earn three years of new exclusivity for a change qualifying as a ‘new clinical investigation’ contributing to approval, which an ANDA cannot.

EMA: The ‘Hybrid Medicine’ Framework

The EMA’s operative term is ‘hybrid medicine,’ defined under Article 10(3) of Directive 2001/83/EC. A hybrid application ‘relies partly on the results of tests on the reference medicine and partly on new data from clinical trials.’ This is not a minor distinction. The EMA’s framework presupposes that the follow-on product will require applicant-generated clinical or non-clinical data — it is built into the definition. The FDA’s framework treats new clinical data as a possible requirement for specific products; the EMA treats it as a structural expectation.

This divergence in philosophy has direct consequences for any company planning a global launch of a complex follow-on product. A data package designed to satisfy FDA’s enhanced ANDA requirements may be insufficient for EMA review, which can require a standalone Phase III trial in the target indication. A developer facing both agencies must either design a single program to the higher standard (expensive upfront, more efficient globally) or run two substantially different programs (duplicative but allows regional prioritization of resources). Neither path is cheap.

The FDA and EMA launched a Parallel Scientific Advice (PSA) pilot program specifically for complex generics to address this divergence. It provides concurrent feedback from both agencies on a single development plan, reducing the risk of designing a program that satisfies one regulator and fails the other. As of 2025, uptake has been limited but growing, primarily from larger generic companies with the resources to engage both agencies simultaneously.

Comparative Framework Table

Feature

FDA (U.S.)

EMA (EU)

Terminology

Complex Generic

Hybrid Medicine

Legal Basis

Hatch-Waxman ANDA (505(j) or 505(b)(2))

Directive 2001/83/EC, Article 10(3)

Core Requirement

Bioequivalence to the RLD

Partial reliance on reference data, supplemented by new applicant-generated data

Typical Data Required

Extensive in vitro characterization, PK studies, sometimes comparative clinical endpoint studies

Often requires new non-clinical or clinical trial data

Key Challenge for Generics

Proving Q1/Q2/Q3 sameness across all critical quality attributes

Bridging the data gap to the reference product with costly new studies

Harmonization Mechanism

FDA/EMA PSA Pilot Program

FDA/EMA PSA Pilot Program

Exclusivity Available to Follow-On

None via ANDA; up to 3 years via 505(b)(2) NDA

Varies; hybrid applications can earn data protection in EU

Investment Strategy: FDA vs. EMA Regulatory Risk

For portfolio managers assessing complex generic pipeline assets, the regulatory pathway determination is not administrative detail — it is a primary driver of NPV. A product requiring a comparative clinical endpoint study at FDA costs an order of magnitude more than one approvable on a PK study alone, with a materially higher failure probability. When a product additionally requires an EMA hybrid application with a new Phase III, the risk-adjusted cost of global market access can exceed $100 million in development spend. At that capital intensity, only products in markets exceeding $500 million in annual U.S. sales typically justify the investment, and even then, the number of credible challengers is small. Analysts should use the presence or absence of a PSG — and its specific study requirements — as a first filter when evaluating complex generic pipeline risk.

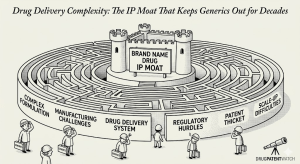

The Three Pillars of the Complexity Advantage

The complexity advantage is not a single barrier. It is a system of three reinforcing pillars that a generic challenger must overcome simultaneously. Weakness in any one pillar still leaves the other two operational. Strength across all three creates a moat that has, in documented cases, extended effective market exclusivity by ten or more years beyond the life of the original composition-of-matter patent.

Pillar I: The Scientific and Manufacturing Moat

Why ‘The Process Is the Product’

For small-molecule oral generics, reverse-engineering is a well-understood discipline. Identify the API, quantify the excipients, replicate the manufacturing process using standard unit operations. The regulatory concept of Q1 (qualitative sameness in ingredients) and Q2 (quantitative sameness) covers the relevant analytical space.

For ADDS products, Q3 — physicochemical and structural sameness — is frequently the dominant challenge, and it is the hardest to achieve because it is governed by the innovator’s manufacturing process, not their disclosed formulation. The polymer science of PLGA microspheres illustrates this concretely. A generic firm can source PLGA from a commercial supplier and match the molecular weight and lactide:glycolide ratio of the innovator’s specification. What they cannot directly observe is the precise homogenization pressure, solvent system, quench conditions, and washing procedure that produce the innovator’s specific microsphere morphology, porosity, and surface area distribution. These process parameters determine the in-vivo release profile as surely as the polymer chemistry does, and they are held as trade secrets.

Aseptic Manufacturing: The Capital and Expertise Barrier

Complex injectables and ophthalmic products must be manufactured under aseptic conditions. A commercial-scale aseptic fill-finish facility — compliant with FDA’s 21 CFR Part 211 and EMA’s Annex 1 (revised 2023) — requires capital investment in the range of $200 to $400 million for a greenfield build, plus several years of qualification and regulatory inspection before a single commercial batch can be released. The operational expertise to manage contamination control strategies, environmental monitoring programs, and media fill validation is scarce and takes years to develop. Many generic firms have the analytical chemistry capability to characterize a complex product but lack the sterile manufacturing infrastructure to produce it. This capital and expertise barrier is as real as any patent.

Inhaler Device Engineering: A Separate Discipline

Dry powder inhalers require an entirely different engineering capability. The Diskus device used in Advair — and its generic equivalents — must generate a specific turbulent flow profile that de-agglomerates the drug-lactose blend at the inhalation flow rates typical of the patient population. The fine particle fraction (FPF) — the proportion of the emitted dose with an aerodynamic particle diameter below 5 micrometers — must match the RLD’s across a range of flow rates, typically 30 to 90 liters per minute. Getting this right requires computational fluid dynamics modeling, device prototyping, and Next-Generation Impactor (NGI) testing under a battery of conditions. A generic firm cannot simply adapt an existing DPI design; they must engineer a new one that produces equivalent aerosol characteristics without infringing the originator’s device patents.

The Nanoscale Characterization Problem

Nanomedicines add a layer of analytical complexity that has no parallel in traditional generics. A liposomal formulation like Doxil must be characterized across at minimum the following attributes: mean particle size and size distribution (polydispersity index); zeta potential; encapsulation efficiency; drug-to-lipid ratio; bilayer phase behavior (gel-to-liquid crystalline transition temperature); lamellarity (unilamellar vs. multilamellar); and in-vitro drug release kinetics. No single instrument measures all of these. Dynamic light scattering (DLS) gives size data but is sensitive to aggregates. Cryo-transmission electron microscopy (cryo-TEM) gives morphological data but is low-throughput. Asymmetric flow field-flow fractionation coupled to multi-angle light scattering (AF4-MALS) can fractionate and size populations but requires specialized expertise.

Even with this suite of orthogonal methods, batch-to-batch variability in the branded product itself complicates the comparison. A generic must hit a moving target defined by the statistical distribution of the innovator’s commercial batches — not a fixed specification.

Manufacturing Steps as a Complexity Metric

Teva’s Adrian Andrews provided a concrete benchmark: a simple generic tablet involves roughly five to six manufacturing steps; some complex products Teva produces involve up to 28 individual steps. Each additional step is an additional source of variability and a potential point of failure. For regulators, a high step count signals the need for more rigorous process validation. For generic developers, it means longer development timelines, higher out-of-pocket costs before a single ANDA is filed, and more ways to fail a pre-approval inspection.

Key Takeaways: Pillar I

Q3 sameness (physicochemical and structural equivalence) is the dominant challenge for ADDS generics and is governed by the innovator’s proprietary manufacturing process, not their disclosed formulation.

Aseptic fill-finish infrastructure requires $200-400M in capital investment and years of qualification, making it a credible standalone barrier to entry for many potential competitors.

DPI generics require the invention of an entirely new device that produces equivalent aerosolization performance — a fluid dynamics and mechanical engineering problem, not a chemistry problem.

Nanomedicine characterization requires multiple orthogonal analytical methods; no single technique captures all CQAs relevant to therapeutic performance.

The innovator’s commercial batch-to-batch variability defines the equivalence target for generics, which may itself be a distribution rather than a point specification.

Pillar II: The Regulatory Gauntlet

When Bioequivalence Cannot Be Measured in Blood

Standard BE methodology rests on the assumption that systemic drug concentration serves as a reliable surrogate for therapeutic effect. This assumption holds for drugs that are absorbed from the gastrointestinal tract and act systemically. It fails for the three largest categories of complex ADDS products: inhaled drugs (intended to act on airway and lung tissue), topical drugs (intended to act on dermal layers), and ophthalmic drugs (intended to act on ocular surface or anterior chamber).

For these products, measuring plasma concentration tells you how much drug escaped the intended site of action — it measures the safety variable, not the efficacy variable. The efficacy variable is drug concentration at the target tissue, which is not directly measurable in a living human by any approved technique. This created a decade-long regulatory impasse for products like Advair Diskus, where the science of proving equivalence had to be developed from scratch after the drug patents expired.

The ‘Weight of Evidence’ Approach: What It Actually Requires

The FDA’s resolution to the locally-acting BE conundrum is a multi-tier evidentiary package that the agency calls the ‘weight of evidence’ approach. For a DPI like Advair, this package includes four distinct tiers of data, each with its own study design challenges.

The first tier is in vitro equivalence: the generic device must demonstrate equivalent dose delivery, FPF, particle size distribution (measured by cascade impaction with an Next-Generation Impactor), spray pattern, and plume geometry across the range of patient-typical inhalation flow rates. This testing must be conducted on multiple batches of the generic and the RLD, and statistical equivalence must be demonstrated under all conditions, not just average conditions.

The second tier is PK equivalence: a crossover PK study in healthy volunteers measuring systemic exposure to both the inhaled corticosteroid and the long-acting beta-agonist components. This study is not measuring efficacy — it is measuring the total lung dose as a safety surrogate and to rule out unexpectedly high systemic absorption from the generic formulation.

The third tier is PD equivalence: pharmacodynamic marker studies may be required in addition to or instead of PK studies for certain products, measuring biological responses such as bronchodilation or systemic cortisol suppression.

The fourth tier is a comparative clinical endpoint study: a large, randomized, placebo-controlled trial in the target patient population, measuring a validated clinical endpoint — for Advair, the change from baseline in FEV1. This is the most expensive, time-consuming, and high-risk requirement. The study must be appropriately powered to detect a clinically meaningful difference between the generic and the brand, and it must include a placebo arm to validate assay sensitivity. A failed clinical endpoint study can terminate a development program after five to eight years and tens of millions of dollars in investment.

The Pre-ANDA Program: Useful, But Signals Risk

The FDA’s Pre-ANDA program, established under GDUFA, allows complex generic developers to meet with the agency before filing to discuss study designs and regulatory expectations. Over 200 such meetings have been granted to date. The program reduces the risk of a Complete Response Letter on bioequivalence grounds — but its existence signals that the product in question carries enough complexity that regulators themselves want to review the development plan before any study is run.

For a generic company’s investment committee, the need to secure a Pre-ANDA meeting is a meaningful risk indicator. It adds 12 to 18 months to the pre-submission timeline, introduces the possibility that the FDA will impose requirements beyond what the applicant proposed, and signals that the product lacks a validated, off-the-shelf regulatory pathway.

First-Cycle Approval Rates: The Statistical Reality

Complex drug applications are approved at materially lower rates in the first review cycle than standard oral solid generics. The average generic application goes through three review cycles before approval. Each complete response letter (CRL) adds approximately 12 months and up to $2 to 3 million in additional GDUFA fees, not counting the cost of the additional studies typically required. For a complex product requiring a clinical endpoint study, a CRL on bioequivalence grounds effectively restarts a two-to-four-year development clock.

This failure rate is not uniformly distributed. Products with published PSGs that include clear in vitro and PK study designs have substantially better first-cycle approval odds than products where the regulatory pathway is contested or being developed in real time. The presence of a PSG is one of the strongest predictors of eventual approval, but it does not predict the timeline or the number of cycles required.

Investment Strategy: Regulatory Risk Scoring for Complex Generics

Analysts evaluating complex generic pipeline assets should apply a four-factor regulatory risk score:

First, PSG status: Does a final PSG exist? A draft PSG reduces uncertainty but is subject to revision. No PSG signals a pioneer environment where the regulatory pathway may be contested.

Second, study design requirement: Does the PSG require a comparative clinical endpoint study? If so, apply a meaningful discount to the probability of approval and add 3 to 5 years to the expected approval timeline relative to a PK-only pathway.

Third, prior Paragraph IV history: Have other companies filed Paragraph IVs against this product’s patents? Multiple filers signals a contested market with a developed patent landscape; zero filers may signal an IP fortress too dense to challenge cost-effectively.

Fourth, first-cycle approval rate for the product class: Historical data on approval rates for products in the same ADDS category (e.g., DPIs, LAIs, topical creams) provides a base rate for failure probability that should inform NPV modeling.

Key Takeaways: Pillar II

The standard PK-based BE pathway cannot demonstrate equivalence for locally-acting drugs in the lung, skin, or eye.

The ‘weight of evidence’ approach for DPIs requires four tiers of data: in vitro, PK, optional PD, and clinical endpoint — the last being the most expensive and failure-prone.

The Pre-ANDA program is valuable for risk reduction but itself signals complexity risk to investment committees.

Average complex generic applications require three review cycles; each CRL adds approximately 12 months and $2-3M in fees above study costs.

PSG status, study design requirement, Paragraph IV filing history, and class-level first-cycle approval rates are the four variables that matter most for regulatory risk scoring.

Pillar III: The Intellectual Property Fortress

From Single Patent to Patent Thicket

The composition-of-matter patent on an API — the primary target of Paragraph IV ANDA challenges under Hatch-Waxman — is no longer the central IP asset for ADDS-protected franchises. Innovators have systematically constructed multi-layered patent portfolios that protect every commercially relevant attribute of a complex product: the formulation, the device, the manufacturing process, the dosing regimen, and all viable secondary indications.

This architecture is sometimes called a ‘patent thicket’ or ‘picket fence,’ and both terms are apt. A thicket is dense and difficult to traverse in any direction; a picket fence surrounds the asset completely with individually narrow but collectively impenetrable barriers. The goal is not to have any single patent that is legally unassailable but to have so many patents that the cost and risk of litigating all of them simultaneously exceeds the NPV of the generic opportunity. At that point, the rational decision for a generic company is to wait, negotiate a settlement, or target a different product.

Anatomy of the IP Fortress for a Complex Auto-Injector

The table below uses a constructed auto-injector franchise to illustrate how each layer of the IP fortress functions as a distinct barrier, not merely a redundant protection.

Patent Layer

Specific Example

Barrier Function

API Polymorph

Crystal form II of the biologic, shown to have 40% greater storage stability than amorphous form

Blocks the most manufacturable and stable API form; forces generic to use a less stable polymorph or challenge the patent

Formulation

Combination of specific buffering agents and surfactant concentrations that prevent aggregation at 150 mg/mL

Requires generic to develop a non-infringing, high-concentration formulation and prove it is comparably stable

Device Utility

Two-stage spring mechanism that reduces needle insertion speed, with clinical data showing reduced patient-perceived pain

Blocks the most patient-friendly injection mechanism; generic device may carry an unproven pain profile

Device Design

Unique ergonomic curved body geometry with specific grip indentations

Prevents visually similar copycat; affects prescriber and patient brand recognition

Drug-Device Interaction

Container composed of cyclo-olefin polymer reducing drug adsorption to container walls by 52%

Protecting the integrated system: substituting either drug or device component alone will infringe

Method of Use

Use of the device-drug combination for a newly approved secondary indication in a rare autoimmune disorder

Extends exclusivity in a new patient population independently of the primary indication’s patent timeline

Manufacturing Process

Proprietary aseptic filling process for high-viscosity formulation under controlled temperature and pressure

Creates a ‘black box’ manufacturing barrier; process cannot be replicated without the innovator’s undisclosed SOP

Dosing Regimen

Monthly maintenance dosing following an initial loading dose schedule, shown to produce faster symptom control

Blocks the prescribing pattern most supported by clinical evidence; generic labeled with a different dosing schedule may be commercially disadvantaged even if approved

Evergreening: Not a Pejorative, a Business Strategy

‘Evergreening’ refers to the practice of extending a drug franchise’s market exclusivity through a sequence of IP-protected product improvements. The term has acquired a negative connotation in policy circles, but from a portfolio management perspective, it is rational and often patient-beneficial when the successive formulations provide genuine clinical advantages.

The mechanism most relevant to ADDS is the delivery system upgrade: launching a new ADDS-based version of the molecule before the original product faces generic competition, then using commercial and clinical strategies to migrate the patient base to the new, patent-protected platform. The original product goes generic; the new version does not. Revenue continuity is maintained.

This strategy requires lead times of five to eight years for complex ADDS products, given development and regulatory timelines. Companies that execute it successfully have typically been planning the successor product before the predecessor’s NDA was approved. The decision to invest in, for example, a two-month injectable formulation while the one-month version is still in Phase III is a deliberate lifecycle management commitment, not an afterthought.

The 30-Month Stay Mechanism and Its Strategic Use

When a generic company files an ANDA containing a Paragraph IV certification — asserting that the innovator’s listed patents are invalid or not infringed — and the innovator files suit within 45 days, FDA approval of the ANDA is automatically stayed for 30 months. This stay is one of Hatch-Waxman’s most commercially significant provisions. For a product protected by multiple listed patents, the innovator can potentially stack multiple 30-month stays across different patents, creating a legally-imposed exclusivity period that has nothing to do with the underlying technical merit of the patents. The generic must either win in court or wait out the stay.

For complex products with dense patent thickets, the 30-month stay interacts with the scientific and regulatory complexity to compound delays. A generic facing 40 listed patents, a two-to-three-year clinical endpoint study requirement, and a 30-month stay on the first patent challenged may realistically project a 12 to 15-year delay from its initial ANDA filing to commercial launch — even if the underlying API patent expired a decade earlier.

Key Takeaways: Pillar III

The composition-of-matter API patent is no longer the central IP asset in ADDS-protected franchises; formulation, device, process, and method-of-use patents collectively produce a denser barrier.

A patent thicket functions strategically by making the total cost of litigation exceed the NPV of the generic opportunity, not by ensuring any individual patent survives challenge.

Evergreening through ADDS upgrade is a rational, often patient-beneficial lifecycle management strategy when the new delivery system provides genuine clinical advantages.

The 30-month stay mechanism compounds delays when stacked across multiple Paragraph IV certifications against a dense patent portfolio.

For complex products, the combined effect of 30-month stays, clinical study requirements, and manufacturing development timelines can push effective market exclusivity 12 to 15 years past the API patent expiry.

IP Valuation: How ADDS Assets Are Priced by the Market

Why the Standard DCF Undervalues Complex Delivery Franchises

The standard discounted cash flow (DCF) model for pharmaceutical assets uses patent expiry as the primary determinant of exclusivity duration. Revenue is modeled at full brand pricing until expiry, then subjected to a rapid erosion curve based on generic entry assumptions. This model works adequately for simple oral solid products. It systematically undervalues ADDS-protected franchises by conflating the legal patent expiry date with the effective loss of exclusivity (LOE) date.

For a product like Abilify Maintena or Advair Diskus, the effective LOE date is determined not by when the oldest listed patent expires but by when a generic manufacturer can successfully navigate all three complexity pillars simultaneously: reverse-engineer the product and manufacturing process, complete the required regulatory studies, and either design around or successfully challenge all relevant patents. Each of those timelines is uncertain and long. The standard DCF model treats patent expiry as LOE; the correct model treats it as the beginning of a countdown whose endpoint is itself probabilistic.

Valuing the Complexity Premium

A more accurate valuation model for ADDS franchises incorporates the following components. First, patent expiry date for the primary listed patents, which starts the clock. Second, probability-weighted time to first generic entry, derived from: the number of active ANDA filers (information available through DrugPatentWatch); the regulatory pathway requirements (PSG-specified study designs and timelines); the strength assessment of the key patents (freedom-to-operate analysis, prior litigation outcomes, inter partes review history). Third, the price erosion curve post-LOE, which for complex products is structurally shallower than for oral solids because fewer competitors enter and some are incapable of achieving full formulary substitution without prescriber confidence.

Fourth — and most commonly omitted — is the terminal value contribution of the next-generation ADDS platform already in development. For companies executing a genuine multi-generational franchise strategy (Otsuka’s progression from Abilify to Maintena to Asimtufii is the clearest example), the second platform has nonzero value before it is even in pivotal trials, because the probability of a follow-on in an established therapeutic category is high and the commercial migration path is already partially built.

M&A Implications: What Acquirers Pay for ADDS IP

In pharmaceutical M&A, the premium paid for ADDS-protected franchises reflects the complexity moat. Acquirers with strong ADDS manufacturing capability — either in-house or through a strategic CDMO relationship — will price complex delivery IP at a higher multiple than acquirers lacking that capability, because the incremental cost of defending and commercializing the asset is lower for them. This creates deal structures where strategic fit (manufacturing and regulatory capability) drives acquirer-specific valuation differences exceeding 20 to 30% on comparable assets.

Due diligence on ADDS M&A targets should include: a freedom-to-operate analysis covering all patent layers (not just API patents); a regulatory pathway assessment for all major markets; a manufacturing capability gap analysis between the target’s current platform and what the acquirer can absorb; and a competitive intelligence assessment of active ANDA filers and their technical capabilities.

Case Study: Abilify Maintena (Aripiprazole LAI)

The Asset and Its Strategic Purpose

Aripiprazole reached the market as Abilify, an oral atypical antipsychotic approved by the FDA in 2002. Peak annual revenues exceeded $6 billion. When the API’s primary patent expired and generic oral aripiprazole entered, Otsuka had already developed Abilify Maintena, a once-monthly intramuscular depot suspension of aripiprazole monohydrate crystals. FDA approved Maintena in February 2013. The product did not just extend the franchise — it targeted a different and clinically superior value proposition: medication adherence in a patient population where non-adherence is the single largest driver of psychiatric hospitalization and associated costs.

Pillar I: The Manufacturing Science

Maintena is a sterile aqueous suspension of micronized aripiprazole monohydrate crystals. The therapeutic profile — 30 days of controlled plasma concentration after a single 400 mg intramuscular injection — is governed entirely by the particle size distribution and crystal form of the suspended API. Smaller particles dissolve faster, larger particles dissolve more slowly; the innovator’s controlled milling and classification processes produce a specific particle size distribution that generates the target pharmacokinetic profile.

A generic manufacturer must replicate this distribution precisely enough to demonstrate equivalent in-vivo performance. This requires: a crystallization or milling process that produces the same mean particle size, distribution width, and crystal morphology; an aseptic suspension manufacturing process that maintains that distribution without causing aggregation or particle growth during storage; and a formulation of suspending agents and viscosity modifiers that maintains injectability over the product’s shelf life without causing dose dumping on injection.

The complexity of this challenge is validated by market history: the first generic approval for any LAI product in the atypical antipsychotic class did not come until 2023, a decade after Maintena’s approval.

Pillar II: The Regulatory Program

BE for Maintena cannot be demonstrated by a standard crossover PK study in healthy volunteers. The drug is released over 30 days; its full pharmacokinetic profile cannot be assessed without a steady-state design requiring multiple monthly injections. FDA requires that BE studies for this product be conducted in patients with schizophrenia or bipolar I disorder — the labeled indications — rather than healthy volunteers, adding recruitment complexity, ethical oversight requirements, and longer enrollment timelines. The inter-individual variability in absorption from intramuscular depots is substantially higher than for oral formulations, requiring larger sample sizes to achieve adequate statistical power for 90% confidence intervals within the standard 80-125% acceptance limits.

A complete BE program for Maintena realistically requires 18 to 30 months of patient enrollment and follow-up, with per-patient costs substantially higher than standard oral BE studies.

Pillar III: The IP Estate and Lifecycle Succession

Otsuka’s patent portfolio on Maintena covers the specific polymorph of aripiprazole monohydrate used in the suspension, the formulation of the suspension (including the particle size range and suspending agents), and the method of treatment via monthly intramuscular injection. As of late 2021, at least one Paragraph IV certification had been filed against Maintena’s listed patents, initiating the 30-month stay clock.

Otsuka pre-empted that competitive threat before it materialized commercially. Abilify Asimtufii — a two-month (8-week) LAI formulation of aripiprazole — received FDA approval in June 2023 and carries its own patent protection extending to at least 2033. The commercial strategy is explicit: migrate patients from Maintena to Asimtufii before Maintena’s generic competition arrives. Prescribers who switch patients to the two-month formulation are then managing patients on a product that faces no generic competition for another decade. This is franchise defense through delivery system succession.

IP Valuation: Maintena/Asimtufii Franchise

A standard DCF model using Maintena’s primary patent expiry as the LOE date would miss two key variables: the probability-weighted delay to first generic entry (likely 2 to 4 years past nominal expiry, given the LAI manufacturing and regulatory barriers), and the terminal value contributed by Asimtufii’s patent-protected cash flows. Analysts modeling the Otsuka atypical antipsychotic franchise should treat the two products as a sequenced revenue stream, with Maintena revenues subject to a delayed and gradual erosion curve and Asimtufii revenues protected until the early 2030s.

Key Takeaways: Abilify Maintena

Maintena’s 30-day release profile is governed by aripiprazole monohydrate crystal particle size distribution — a manufacturing-controlled attribute, not a disclosed formulation attribute.

BE studies require steady-state designs in patient populations, not healthy volunteer crossover studies, adding 18-30 months to the study timeline.

The Asimtufii two-month LAI represents a textbook multi-generational franchise defense, with protection extending to at least 2033.

DCF models using Maintena’s primary patent expiry as the LOE date undervalue the franchise by ignoring both BE-driven delay to generic entry and Asimtufii’s independent terminal value.

Case Study: Advair Diskus (Fluticasone/Salmeterol DPI)

The Commercial Scale of the Barrier

Advair Diskus reached peak annual revenues exceeding $8 billion globally, making it one of the most commercially significant DPI franchises in pharmaceutical history. The core patents on fluticasone propionate and salmeterol xinafoate expired in the mid-2000s. The first fully-substitutable generic, Mylan’s Wixela Inhub, was not approved until January 2019 — nearly a decade of patent-expiry-free market exclusivity attributable almost entirely to regulatory and manufacturing complexity.

Pillar I: The Device Engineering Problem

The Diskus device is not a passive container. Its internal geometry produces a specific turbulent airflow when the patient inhales, and that turbulence must be sufficient to de-agglomerate the drug-lactose blend into individual particles with an aerodynamic diameter below 5 micrometers. The FPF — the proportion of the dose that reaches the lower respiratory tract — is the primary determinant of therapeutic effect. For a generic to be substitutable, its FPF must be equivalent to the Diskus’s across the full range of patient inhalation flow rates, from the slow breath of an elderly COPD patient to the faster inhalation of a younger asthmatic.

Developing a device that achieves this without copying the Diskus’s internal geometry (protected by GlaxoSmithKline’s device patents) required generic manufacturers to solve a computational fluid dynamics problem with a high-dimensional solution space. Multiple device prototypes must be tested across flow rate ranges using cascade impaction with a Next-Generation Impactor, with iterative redesign until the FPF profile matches the RLD’s within FDA’s specified equivalence criteria.

Pillar II: The Four-Tier BE Program

Advair became the canonical example of a four-tier ‘weight of evidence’ BE program. The in vitro tier alone required demonstration of equivalence across dose uniformity, FPF, aerodynamic particle size distribution, spray plume characteristics, and delivered dose consistency over the life of the inhaler at specified flow rates. The PK tier required a crossover study in healthy volunteers measuring plasma concentrations of both active components. The clinical endpoint tier required a large randomized controlled trial in adult asthma patients, measuring FEV1 as the primary endpoint, with a placebo arm for assay sensitivity. That trial, for a generic manufacturer, means running the equivalent of a Phase III clinical program at their own cost and risk with no exclusivity reward — the approved product is substitutable at no premium.

GlaxoSmithKline filed a citizen petition in 2009 requesting that the FDA impose even stricter standards on potential Advair generics, a tactic that added regulatory uncertainty and delayed the issuance of clear PSG guidance. Independent research subsequently identified significant batch-to-batch pharmacokinetic variability in the branded Advair product itself, which complicated the reference standard against which generics were measured and contributed to multiple Complete Response Letters for early ANDA filers.

Pillar III: Device Patent Moat

GlaxoSmithKline held multiple utility patents on the Diskus device’s mechanical components and design patents on its aesthetic appearance. Generic developers were legally required to invent a device different enough to avoid infringement while producing aerosol characteristics equivalent enough to pass the FDA’s in vitro standards. The intersection of ‘sufficiently different from the Diskus’ and ‘sufficiently similar in performance to the Diskus’ is a narrow solution space. The engineering effort required to find a design within that space — combined with the cost of clinical endpoint studies — deterred most potential competitors entirely.

Lesson for IP and R&D Teams

Advair proves that device IP can outlast drug IP as the primary driver of effective market exclusivity. GlaxoSmithKline’s investment in the Diskus’s proprietary engineering produced more than ten years of exclusivity after the drug patents expired. For any company developing a drug-device combination product, this is the template: the device is not packaging, it is a therapeutic component with independent IP value. Designing for maximum device complexity — within the constraint of clinical usability — is a legitimate and strategically rational choice.

Key Takeaways: Advair Diskus

Drug patents expired mid-2000s; first generic approval came in January 2019, demonstrating approximately ten years of post-patent effective exclusivity driven purely by regulatory and device complexity.

The four-tier ‘weight of evidence’ BE program required in vitro testing, PK studies, optional PD studies, and a full clinical endpoint trial in asthma patients.

Citizen petitions can be used to impose regulatory uncertainty and delay PSG issuance — a tactic that added years to the generic development timeline.

Batch-to-batch PK variability in the branded product created a moving equivalence target for generic filers, contributing to multiple CRLs.

Device patent protection is independently durable from drug patent protection; the Diskus’s engineering complexity was itself the primary exclusivity mechanism after drug patents expired.

Case Study: Butrans (Buprenorphine Transdermal)

The Multi-Laminate Structure as Patentable Innovation

Butrans is a transdermal patch delivering buprenorphine continuously for seven days through the stratum corneum. The seven-day wear duration — the primary clinical differentiator from oral opioids — is not achievable with a simple drug-in-adhesive architecture. It requires precise engineering of the rate-controlling membrane, the drug matrix composition, and the adhesive properties across the full seven days of contact with human skin.

The patch architecture includes a rate-controlling microporous membrane positioned between the drug reservoir and the skin contact layer. This membrane’s permeability to buprenorphine — determined by its material composition, pore size distribution, and thickness — is the primary engineering lever controlling the release rate. The adhesive itself must maintain adequate skin contact and peel resistance for seven days across a range of skin conditions, body sites, and physical activity levels, without causing clinically significant irritation or sensitization.

Formulation Patents as the Primary IP Weapon

Napp Pharmaceuticals (Purdue Pharma’s UK subsidiary) held a patent not on buprenorphine — a long-established molecule — but on the specific formulation of the drug matrix within the patch: a composition comprising approximately 10% by weight buprenorphine base, 10-15% levulinic acid, and approximately 10% oleyloleate. This formulation patent was the primary IP barrier to generic entry in the UK.

When generic companies sought to launch buprenorphine transdermal patches in the UK, Napp sued for infringement. The litigation successfully prevented market entry until August 2016, when the patent was invalidated in court. An economic analysis estimated the cost of this delayed generic entry to the NHS at approximately £1.2 million in foregone savings. The case illustrates a structural feature of transdermal ADDS IP: the excipients are not inert diluents. Levulinic acid functions as a flux enhancer that increases buprenorphine’s permeability through the stratum corneum; oleyloleate is a penetration enhancer and plasticizer for the adhesive matrix. Patenting their specific combination and proportions is patenting enabling technology, not simply protecting a recipe.

Regulatory Complexity: Adhesion and Irritation Studies

The FDA’s PSG for transdermal buprenorphine generic products requires, in addition to standard PK BE studies, specific clinical studies to evaluate: adhesion performance (ensuring the patch remains adherent for the full seven-day wear period across representative body sites and patient activities); skin irritation potential (comparing the local tolerability profile of the generic to the RLD at approved application sites); and skin sensitization potential (assessing the risk of delayed-type hypersensitivity reactions from repeated patch application). These study types are specific to transdermal systems and require specialized protocol designs, dermatological assessments, and longer study durations than standard BE studies.

Key Takeaways: Butrans

Formulation patents on excipient combinations — not the API — were the primary IP barrier in the Butrans transdermal case.

Levulinic acid and oleyloleate function as enabling excipients (flux enhancer and penetration enhancer, respectively), making their patented combination genuinely protective of the delivery mechanism.

Generic entry delay in the UK cost the NHS approximately £1.2 million in foregone savings — quantifying the direct economic impact of formulation IP.

FDA requires transdermal generic developers to conduct specific adhesion, irritation, and sensitization studies beyond standard PK BE, adding cost and complexity to the regulatory program.

Case Study: Doxil (Liposomal Doxorubicin) and the Nanosimilar Problem

The Product That Broke the Generic Paradigm

Doxil was the first FDA-approved nanomedicine, receiving approval in 1995. Its active ingredient — doxorubicin, a cytotoxic anthracycline — had been generic for decades. The innovation was the delivery system: a PEGylated liposome with a mean diameter of approximately 100 nanometers, encapsulating doxorubicin in an ammonium sulfate gradient-generated remote loading configuration. The PEG coating reduces uptake by the reticuloendothelial system, extending plasma half-life from roughly 2 hours (free doxorubicin) to approximately 45-55 hours. The net result is preferential accumulation in tumor tissue through the EPR effect, enabling higher tumor exposure with substantially reduced cardiotoxicity compared to free doxorubicin.

Why ‘Sameness’ Fails at the Nanoscale

The regulatory challenge for a follow-on liposomal doxorubicin product is that no two manufacturing processes produce nanomedicines with genuinely identical properties. Minor differences in lipid composition, hydration conditions, extrusion parameters, and drug loading conditions produce differences in particle size distribution, encapsulation efficiency, drug release rate, zeta potential, and — critically — in-vivo biodistribution and tumor accumulation. These differences may be analytically detectable but clinically imperceptible, or they may translate into meaningful differences in efficacy and toxicity. Regulators cannot know which outcome applies without clinical data.

This is why the concept of a ‘nanosimilar’ has emerged. Like a biosimilar, a follow-on nanomedicine cannot be presumed equivalent on physicochemical comparability alone. It must demonstrate clinical similarity through a tiered evidence approach: extensive analytical characterization, non-clinical comparative studies, PK similarity, and — depending on the product — clinical endpoint comparability. This approach is significantly more demanding and expensive than the traditional ANDA pathway.

The Regulatory Vacuum: No Harmonized Nanosimilar Pathway

As of 2026, neither the FDA nor the EMA has published a finalized, product-class-specific regulatory framework for nanosimilars. The FDA has addressed specific products (liposomal doxorubicin, iron sucrose nanoparticles) through individual PSGs and guidance documents, but has not established the overarching framework that the biosimilar pathway provides for biologics. The EMA’s Committee for Medicinal Products for Human Use (CHMP) has produced reflection papers on nanomedicines, but these stop short of a prescriptive regulatory framework.

This vacuum has two effects. For follow-on developers, it creates uncertainty: the data package required for approval is determined on a product-by-product basis, and there is limited precedent to anchor expectations. For innovators, it is protective: without a clear and streamlined pathway, potential competitors face unquantifiable regulatory risk on top of the already formidable scientific and IP barriers.

IP Valuation: Nanomedicine Franchises

The combination of scientific complexity, regulatory vacuum, and IP protection makes nanomedicine franchises uniquely resistant to generic erosion on a post-patent-expiry basis. Standard DCF models should apply a longer and shallower revenue erosion curve than is used for oral solids — the 80-90% revenue decline seen within 12 months of generic entry for simple oral drugs is simply not achievable for nanomedicines, where the number of credible competitors is small, the regulatory timeline is long, and prescriber confidence in substitutability is lower.

Institutional investors should treat the ‘nanosimilar’ regulatory pathway development timeline as a key watch item. If FDA or EMA establishes a clear, streamlined nanosimilar pathway — analogous to the 2010 BPCIA framework for biosimilars — the effective market exclusivity of existing nanomedicine franchises will contract. That event is a material risk that belongs in any long-horizon valuation model.

Evergreening Roadmaps: The Technology Succession Playbook

The Multi-Generational Franchise Architecture

Evergreening through ADDS is not a reactive tactic. Companies that execute it successfully plan product generations five to ten years in advance. The architecture has four phases.

Phase one is the foundation product: the original drug-delivery combination that creates the initial patent thicket and establishes the franchise in clinical practice. The clinical data from this product is both the commercial asset and the regulatory reference point for all successors.

Phase two is the complexity upgrade: before the foundation product faces generic competition, the company launches a successor with a meaningfully improved delivery system. The successor must offer a genuine clinical advantage — longer dosing interval, improved tolerability, more convenient administration — sufficient to justify prescriber switching and support premium pricing versus the foundation product once it goes generic.

Phase three is the secondary indication expansion: independent of the delivery system upgrades, the company’s clinical team pursues new indications for the same molecule or the same drug-device platform, each generating independent method-of-use patent protection and, potentially, regulatory exclusivity (Orphan Drug designation, Breakthrough Therapy designation).

Phase four is platform licensing: the proprietary ADDS platform, once validated in one commercial product, can be licensed to other companies developing drugs in adjacent therapeutic areas. This generates royalty revenue and creates a strategic dependency relationship that discourages those partner companies from supporting generic entry efforts.

Otsuka’s Aripiprazole Succession: A Documented Example

Abilify (oral tablet) established aripiprazole in psychiatry. Abilify Maintena (one-month LAI) re-established the franchise on a protected delivery platform. Abilify Asimtufii (two-month LAI) extended that platform before Maintena’s generic window opened. The trajectory is consistent and deliberate: each generation provides a longer dosing interval, stronger adherence data, a new patent portfolio, and — critically — a new commercial migration opportunity that moves patients out of reach of the previous generation’s generics.

The strategic lesson is that the dosing interval itself is a controllable variable. For LAI products, the sequence oral daily, monthly injection, two-month injection, quarterly injection represents a natural progression, each step offering a clinical rationale for patient switching and a new IP window. Companies with strong PLGA or crystalline suspension manufacturing capability can extend this succession for decades.

Technology Roadmap: LAI Platform Succession

Generation

Formulation Technology

Dosing Interval

IP Protection Window

Clinical Differentiator

1 (Foundation)

Oral tablet

Daily

Primary API patent (expired or near expiry)

Established efficacy and tolerability profile

2

PLGA microsphere or crystalline suspension LAI

Monthly

Formulation + process patents; 10-15 years

Adherence advantage over daily oral; depot convenience

Near-complete removal of injection burden; implant may be non-biodegradable with removal option

Competitive Intelligence Infrastructure: What You Actually Need

Beyond Patent Expiry Dates

Knowing when a drug’s primary patent expires is table stakes. For ADDS-protected products, the commercially relevant information is a multi-dimensional data set that requires integration across patent databases, regulatory filings, litigation records, and clinical trial registries. The specific questions that drive strategic decisions include: How many active ANDA filers are pursuing a specific complex product? What Paragraph IV certifications have been filed against which patents? Has the FDA issued a PSG, and what study designs does it require? Have any filers received Pre-ANDA meeting feedback that signals a clearer or more difficult pathway? Are any filers pursuing a 505(b)(2) NDA rather than an ANDA, which would signal a higher-complexity development approach?

These questions cannot be answered by a simple patent expiry date search. They require an integrated CI platform that aggregates and analyzes all of these data streams in a structured and searchable format.

For Innovator IP Teams: Proactive Fortress Monitoring

IP teams at innovator companies should use CI platforms not just to monitor competitors but to audit their own fortresses. The relevant questions are: Which of the products’ listed patents have been challenged by Paragraph IV certifications? Which patents are most vulnerable based on prior art identified in IPR petitions? Are there gaps in the patent thicket — product attributes that are commercially protected by manufacturing know-how rather than patents, and that could theoretically be reverse-engineered? Are competitors building the CDMO partnerships or analytical capabilities that would make a complex generic development program plausible?

The goal is to identify vulnerabilities before a challenger does and address them, either by filing additional patents on previously unprotected attributes or by accelerating the timeline of the next-generation product launch.

For Generic R&D Teams: The Candidate Scoring Model

Generic companies pursuing complex products should apply a formal candidate scoring model before committing development resources. A rigorous model includes the following inputs: patent thicket density (number of listed patents, expiry distribution, Paragraph IV history, IPR outcomes); regulatory pathway requirements (PSG status, study design classification, estimated timeline and cost); technical feasibility assessment (manufacturing capability gap analysis against the product’s CQA requirements); competitive field analysis (number of active ANDA filers, estimated competitive launch timing); and market opportunity size (branded revenue, price erosion assumptions calibrated to the product’s complexity class).

Products scoring highly on all dimensions are rare. For most complex products, at least one dimension presents a material constraint. The discipline to walk away from technically fascinating but commercially marginal opportunities — a discipline that standard generic companies rarely needed to exercise — is a defining capability of sophisticated complex generic operators.

The CDMO Ecosystem: Complexity as a Service

From Contract Manufacturer to Strategic Partner

The traditional CMO relationship was transactional: a pharmaceutical company provided a process and a specification; the CMO executed it at scale. This model is inadequate for complex ADDS products, where the process and the specification are often co-developed by the manufacturing partner rather than provided by the drug company. Modern CDMOs with ADDS capabilities are more accurately described as technical development partners who happen to also manufacture.

This shift has structural implications for how agreements are structured. An ADDS-capable CDMO brings proprietary process knowledge, specialized equipment, and regulatory expertise that the pharmaceutical company may lack entirely. The CDMO’s contribution to the final product’s IP estate is therefore potentially substantial, creating questions about IP ownership, licensing rights, and exclusivity arrangements that must be negotiated explicitly in the development agreement.

ADDS-Specialized CDMO Capabilities by Technology Class

ADDS Technology

Key CDMO Capabilities Required

Representative Capabilities Gap for Traditional Generic Manufacturers

PLGA Microsphere LAI

Polymer synthesis or sourcing, emulsification process development, aseptic manufacturing, lyophilization

Aseptic manufacturing, particle characterization expertise, in-vivo PK correlation development

PEGylated Liposome

Lipid film hydration or microfluidic manufacturing, extrusion, remote drug loading, aseptic fill-finish

Nanoparticle characterization suite (DLS, cryo-TEM, AF4-MALS), sterile manufacturing scale-up

Bioconjugation chemistry, high-potency API handling, sterile fill-finish for complex biologics

Virtually all capabilities (ADCs require specialized facilities standard generic firms do not possess)

Build, Buy, or Partner: The Capability Acquisition Decision

For an innovator or specialty generic company assessing how to access ADDS manufacturing capability, the build-buy-partner decision involves a tradeoff between control, speed, and capital. Building in-house provides maximum IP control and long-term cost competitiveness but requires $200M to $500M in capital investment and five to seven years of regulatory qualification before first commercial batch. Buying a CDMO or acquiring a company with the relevant manufacturing assets accelerates capability acquisition but at premium valuation multiples and integration risk. Partnering with an established CDMO provides access to validated capability without capital intensity but creates IP dependency and potential supply chain vulnerability.

For most companies that are not among the largest ten pharmaceutical manufacturers by revenue, CDMO partnership is the rational choice for initial market entry in ADDS-protected categories. The question of whether to internalize capability over time should be driven by volume thresholds at which in-house economics become favorable, not by a reflexive preference for vertical integration.

Standard sell-side DCF models for pharmaceutical companies underperform on ADDS-heavy portfolios because they use patent expiry as a proxy for LOE. The adjustments needed to correct this systematic underestimation are as follows.

Adjust the LOE date using a probabilistic model of generic entry timing, derived from patent landscape analysis, regulatory pathway assessment, and competitive field analysis. For complex ADDS products, a probability-weighted expected LOE date is typically two to eight years later than the primary patent expiry, with the distribution varying by product class: LAIs and nanomedicines at the longer end, transdermal patches at the shorter end.

Adjust the post-LOE revenue erosion curve to reflect the competitive intensity realistic for the product class. An LAI with two ANDA filers who each face multi-year clinical study requirements will erode more slowly than an oral solid with fifteen day-one generic filers. A reasonable first-year post-LOE erosion assumption for a complex product with fewer than five credible competitors is 30 to 50%, versus the 70 to 85% typical for simple oral solids.

Incorporate the terminal value of next-generation ADDS platforms in development. If the company has already filed an NDA for a successor product with independent patent protection, model that cash flow stream separately and assign a probability to its commercial success based on the clinical and regulatory maturity of the program.

Sector-Level Trends for Portfolio Managers

The specialty generics market is the fastest-growing segment of the generic pharmaceutical industry, compounding at approximately 9.9% annually. Within that segment, injectables dominate by revenue share (over 64%). The pipeline of ADDS products in late-stage development at innovator companies has grown substantially over the past decade, driven by the commercial validation of the strategy in products like Maintena and the maturation of PLGA, PEGylated liposome, and DPI platform technologies.

For sector-level portfolio construction, this has several implications. Innovator companies with strong ADDS pipeline depth — measured by the number of Phase II/III programs featuring a proprietary delivery platform — command a premium over innovators with APIs in development but no proprietary delivery differentiation. Specialty generic companies with proven manufacturing capability in at least one ADDS category (particularly sterile injectables or DPIs) command a premium over traditional oral solid generic manufacturers. CDMOs with ADDS-specific capabilities have structurally higher EBITDA margins than generalist CMOs, reflecting the scarcity value of their technical expertise.

The Regulatory Frontier: Nanosimilars, Smart Implants, and What Comes Next

The Coming Nanosimilar Pathway

The closest regulatory analogue for what nanomedicine follow-ons will require is the biosimilar pathway established under the Biologics Price Competition and Innovation Act of 2009 (BPCIA) in the U.S. and the EMA’s biosimilar framework, which has been operational since 2004. Both require a ‘totality of the evidence’ approach, with the analytical similarity package anchoring the program and clinical data filling any residual uncertainty.

For a nanosimilar, the analytical similarity package would need to address: particle size and size distribution (mean, PDI, and full distribution profile); surface charge and PEG density (for PEGylated products); encapsulation efficiency and drug-to-carrier ratio; in-vitro drug release profile under physiologically relevant conditions; lipid or polymer composition and structural characterization; and — specific to nanomedicines — protein corona formation characteristics in relevant biological fluids.

The clinical data requirement will vary by product. For a nanosimilar of a well-characterized nanomedicine with a clear PK-efficacy relationship, a PK similarity study in patients may be sufficient to support a clinical bridge. For products where the PK-efficacy relationship is less established — or where biodistribution differences could affect both efficacy and safety — a comparative clinical endpoint study will be required. The FDA’s CRCG and EMA’s Nanomedicine Characterization Laboratory are actively developing the scientific framework; formal guidance documents are expected in the 2026-2028 period.

Smart Microneedle Arrays: The Next Transdermal Frontier

Microneedle array patches dissolve or retract after penetrating the stratum corneum, creating transient microchannels for drug delivery. Current commercial and late-development applications include influenza vaccination (MicronJet600, NanoPass Technologies), cosmetic hyaluronic acid delivery, and investigational programs for insulin and hormone delivery. The key regulatory question for follow-ons is whether the microneedle array itself will be regulated as a device, a drug, or a combination product — a determination that drives the entire approval pathway.

The next-generation vision — stimulus-responsive microneedles that release drug in response to a physiological signal — multiplies the complexity. A glucose-responsive insulin patch would incorporate a biosensor element (detecting glucose concentration), a feedback mechanism (controlling release rate), and a drug delivery function. The regulatory classification would span all three product categories simultaneously (drug, device, biologic for insulin-containing versions), requiring FDA’s Office of Combination Products to make a primary mode-of-action determination before any approval pathway can be defined. This classification uncertainty is itself an IP and competitive barrier: companies that resolve it first, by engaging the FDA early and obtaining clear regulatory designation, secure a first-mover advantage that compounds the technical lead time.

In-Situ Forming Depots: The Next LAI Generation

In-situ forming depots are injectable formulations that transition from liquid to solid after injection, forming a biodegradable polymer matrix (typically PLGA) within the subcutaneous or intramuscular tissue. The liquid-to-solid transition can be triggered by solvent exchange with biological fluids (Atrigel technology) or by temperature-responsive gelation. The resulting depot releases drug over weeks to months as the polymer hydrolyzes.

The advantages over microsphere-based LAIs are significant: the product can be supplied as a ready-to-use liquid rather than a reconstituted suspension, eliminating the patient and caregiver burden associated with vial-and-syringe reconstitution. The manufacturing process, while still requiring aseptic conditions, is potentially simpler than microsphere manufacturing.

For follow-on developers, the analytical characterization challenge is substantial. In-situ depot properties — gelation kinetics, depot morphology, drug distribution within the matrix, degradation rate — are all a function of the liquid formulation’s composition and the physiological environment at the injection site. These properties cannot be fully characterized in a vial; they emerge in-vivo. This makes in-vivo performance demonstration essentially unavoidable, pushing the regulatory requirement toward the clinical end of the BE spectrum.

Emerging ADDS Risk Matrix for Long-Horizon Portfolio Planning

Emerging Platform

Estimated First Commercial Scale: 5-year horizon

Regulatory Pathway Status

Generic Entry Barrier Level

IP Density Potential

In-situ forming depots

High (several in Phase III as of 2025)

Addressed by existing ANDA/PSG framework on product-by-product basis

Very High

High

Glucose-responsive microneedles

Low to medium (pre-commercial)

Not yet defined; combination product designation required

Extreme

Extreme

Smart implants (biodegradable, sensor-actuated)

Low (early clinical)

Not yet defined

Extreme

Extreme

Nanosimilars (follow-ons to approved nanomedicines)

Design for complexity from the earliest formulation screening stage, not after lead molecule selection. Every patentable attribute of the delivery system — the polymer chemistry, the device mechanism, the excipient function, the dosing regimen — should have a patent application filed before the NDA submission. The IP estate should be reviewed annually against new Paragraph IV certifications and IPR filings, with proactive patent prosecution to close identified gaps. The next-generation ADDS platform should be in IND-stage development before the current product’s primary patents are in their final five years.

For Generic R&D and Regulatory Affairs Teams

Apply a formal candidate scoring model before committing resources to any complex generic program. PSG status, study design classification (PK-only vs. clinical endpoint), patent thicket density, and competitive field size are the four variables that most reliably predict risk-adjusted return. Products requiring comparative clinical endpoint studies have development economics that differ categorically from standard ANDA programs — treat them as Phase III investments with no exclusivity upside, priced accordingly.

For Portfolio Managers and Institutional Investors

Adjust LOE date assumptions for ADDS-protected franchises upward by two to eight years depending on product class. Apply a shallower post-LOE revenue erosion curve for products where the competitive field at generic entry is expected to be fewer than five players. Value next-generation ADDS platforms in development as separate but correlated assets. Monitor FDA/EMA nanosimilar pathway development as a material risk to existing nanomedicine franchise valuations. Treat CDMO partnerships in ADDS categories as a signal of technical capability at specialty generic companies — it is a positive indicator, not a cost concern.

For Business Development and M&A Teams

ADDS IP due diligence requires all patent layers, not just the API patent estate. Freedom-to-operate analysis should cover formulation, device, process, and method-of-use patents. Manufacturing capability gap analysis is mandatory — an IP asset is only as valuable as the acquirer’s ability to defend and commercialize it. LOE date modeling should use the probabilistic approach described above, not a single-scenario patent expiry assumption.

FAQ

What is the most commonly underestimated barrier to complex generic entry?

Manufacturing capability. Most complex generic analysis focuses on the patent thicket and regulatory pathway, both of which are visible and documented. The aseptic manufacturing infrastructure, nanoparticle characterization expertise, and device engineering capability required to physically produce a complex ADDS product are less visible but equally deterministic. A generic firm can win every patent challenge and satisfy every regulatory requirement — and still not be able to make the product at commercial scale with acceptable quality. The CDMO ecosystem exists precisely to address this gap, but accessing the right CDMO for a specific ADDS category requires technical judgment and may involve multi-year partnership development.

How does a Paragraph IV filing strategy differ for a complex ADDS product versus a simple oral drug?

For a simple oral drug, the strategy is typically to challenge the strongest patent — usually the composition-of-matter patent — in Paragraph IV litigation, while preparing the ANDA for a straightforward ANDA review. The BE study is quick and low-risk; the litigation timeline determines when the product can launch. For a complex ADDS product, the regulatory program and the litigation are both long and costly, and they run in parallel with substantial uncertainty on both tracks. A generic company must assess whether any of the thicket’s patents are genuinely vulnerable, prioritize those for Paragraph IV challenge, and simultaneously determine whether it can satisfy the regulatory requirements before the challenged patents expire naturally anyway. In many cases, the rational answer is that a Paragraph IV challenge is not worthwhile — the legal costs exceed the time-value benefit — and the company should wait for natural patent expiry and then execute the regulatory program.

What does a robust ADDS competitive intelligence program actually look like in practice?

It is an integrated function combining patent analysis (monitoring new filings, IPR petitions, and Paragraph IV certifications against the product of interest), regulatory intelligence (tracking PSG status, ANDA filing activity, FDA meeting grants), clinical trial monitoring (tracking competitor Phase III programs that may signal a 505(b)(2) approach), and manufacturing intelligence (tracking CDMO partnerships, facility expansions, and regulatory inspections at facilities known to be developing the product). These data streams come from different sources — USPTO, FDA’s Orange Book and Paragraph IV database, ClinicalTrials.gov, FDA inspection records — and must be integrated and analyzed continuously. Platforms like DrugPatentWatch that aggregate these streams into a single queryable interface reduce the manual burden and improve signal detection.

Will the nanosimilar regulatory pathway look more like the generic or the biosimilar pathway?

The scientific consensus, and the trajectory of agency thinking in both FDA and EMA communications, is that it will be substantially closer to the biosimilar pathway. The ‘sameness’ concept that enables the ANDA pathway is not scientifically defensible for nanomedicines, where manufacturing-induced differences in physicochemical properties can translate into clinically meaningful differences in biodistribution, efficacy, and toxicity. A ‘totality of the evidence’ approach — with analytical characterization anchoring the package and clinical data required to fill residual uncertainty — is the expected framework. For products where a clear PK-efficacy relationship exists, the clinical burden may be limited to a PK similarity study. For products where it does not, a full comparative clinical endpoint study is probable. This means the economics of nanosimilar development will look substantially more like biosimilar development than like standard ANDA development.