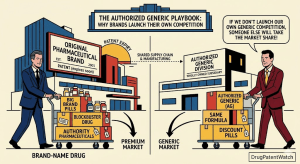

The Counterintuitive Move That Makes Perfect Business Sense

A brand pharmaceutical company holds an approved drug. No generic competitor has filed a Paragraph IV certification. No abbreviated new drug application (ANDA) is pending. The Orange Book shows clean patent coverage for years. By every conventional measure, the brand sits in an uncontested market.

Then it licenses an authorized generic.

To anyone unfamiliar with pharmaceutical commercial strategy, this looks like self-sabotage. A company deploys its own lower-priced version of its own product, competes directly against itself, and accepts reduced per-unit revenue in a market it controls entirely. The business press periodically frames authorized generic launches as signs of competitive weakness, regulatory capitulation, or financial desperation.

That framing is wrong.

The decision to launch an authorized generic in the absence of any competitive threat is almost always a deliberate, carefully modeled commercial or strategic choice. It is a tool that sophisticated pharmaceutical companies use to accomplish objectives that have nothing to do with generic competition and everything to do with market architecture, pipeline management, regulatory positioning, supply chain economics, and long-term brand protection.

This article works through the full spectrum of reasons why a brand manufacturer might make that choice. It covers the commercial logic, the regulatory framework, the IP strategy, the tax and financial structures, and the specific scenarios in which an authorized generic in an uncontested market makes clear economic sense. It also examines the tools and data sources, including DrugPatentWatch, that inform these decisions with real patent and exclusivity timeline data.

Understanding why brands launch authorized generics without competitive pressure is, in many respects, a more revealing exercise than understanding why they do it defensively. The defensive case is obvious. The proactive case tells you how pharmaceutical companies actually think about market structure, revenue optimization, and competitive positioning over multi-year product life cycles.

What an Authorized Generic Actually Is

Before examining the strategic rationale, the definition requires precision, because “authorized generic” is a term that gets used loosely across commercial, regulatory, and legal contexts in ways that can obscure meaningful distinctions.

The Regulatory Definition and FDA Framework

An authorized generic (AG) is a drug that the brand-name drug company sells or licenses to be sold under the generic drug’s labeling. Under 21 U.S.C. § 355(t), the FDA defines an authorized generic as a listed drug that is marketed, sold, or distributed directly or indirectly to retail class of trade as a generic drug after the date of enactment [1]. Critically, an authorized generic uses the same FDA-approved new drug application (NDA) as the brand. It does not require a separate ANDA approval. The brand manufacturer already has the approval.

This NDA-based approval path is what distinguishes authorized generics from independent generic versions, which require their own ANDA submissions, bioequivalence studies, and FDA review. An authorized generic skips all of that. The brand’s existing approval covers it. The brand can license the product to a generic distribution partner the day after it decides to do so, with no additional regulatory approval timeline.

The FDA maintains a list of marketed authorized generics under 21 U.S.C. § 355(t)(2), which requires manufacturers to notify the agency of their intent to market an authorized generic. DrugPatentWatch tracks authorized generic activity alongside Orange Book patent and exclusivity data, making it straightforward to see which products have authorized generic versions in market, who the licensed distributors are, and how the AG launch timing relates to patent expiration dates and ANDA filing activity.

How Authorized Generics Differ from Licensed Products

The authorized generic label typically shows the generic nonproprietary name rather than the brand name. The product is physically identical to the brand – same active pharmaceutical ingredient, same formulation, same dosage form, same manufacturing facility in many cases. It sells at a price between the brand price and independent generic prices, typically at a 20 to 40 percent discount to the brand.

This is distinct from a licensed product, where the brand grants rights to a partner to manufacture and sell a separate product using the brand’s compound or technology. In an authorized generic arrangement, manufacturing often stays with the brand or a designated contract manufacturer, and the brand or its licensee sells the NDA-covered product under generic labeling.

The economics are also distinct. In a licensed product arrangement, the brand typically receives royalties on net sales. In an authorized generic arrangement, the brand either sells the product to a distribution partner at a transfer price and shares in the margin, or captures the margin itself if it controls the distribution channel.

The Market Segmentation Imperative

The most straightforward commercial reason to launch an authorized generic in an uncontested market is price segmentation. Brand pharmaceutical markets are not monolithic. They contain multiple segments with genuinely different willingness to pay, formulary positions, and purchasing behaviors. A single brand price point cannot optimally capture revenue across all of them simultaneously.

Pharmacy Benefit Manager Formulary Dynamics

Pharmacy benefit managers (PBMs) manage drug benefits for health insurance plans covering tens of millions of lives. Their fundamental tool is the formulary – a tiered list of covered drugs, where tier placement determines patient copayment levels and, critically, plan rebate economics. Brand drugs typically sit on Tier 2 or Tier 3, with higher copayments. Generic drugs sit on Tier 1, with the lowest copayments.

For a brand manufacturer whose drug is approaching middle age in its product life cycle, losing favorable formulary placement to a therapeutic competitor is a genuine revenue risk even without generic competition. PBMs negotiate aggressively for formulary placement, and a brand that refuses to offer competitive terms may find itself excluded in favor of a therapeutically equivalent competitor or switched to a less favorable tier.

An authorized generic gives the brand manufacturer a Tier 1 formulary product. The brand’s commercial team can negotiate formulary placement for the AG on Tier 1, capturing volume that would otherwise flow to therapeutic competitors, while maintaining the brand on Tier 2 or Tier 3 for segments where brand loyalty is price-insensitive. The result is effective price discrimination across payer segments without requiring a separate molecular entity.

Research by Berndt, Mortimer, Bhattacharjee, and Parece [2] documented that brand price discrimination through authorized generics and multiple price points became more sophisticated during the 2000s as PBM formulary management matured. Their analysis found that brands with multiple SKUs targeting different payer tiers generated higher total revenue across the patient population than brands maintaining a single price point.

Cash-Pay and Uninsured Patient Segments

In the United States, a meaningful segment of prescription drug buyers pays cash, either because they lack insurance coverage for a specific drug or because their out-of-pocket cost under insurance exceeds the cash price. This segment is price-elastic in ways that insured patients are not, and it is particularly large for chronic disease drugs taken over years or decades.

A brand priced at $400 per month is simply inaccessible to a cash-pay patient earning a median income. That patient does not buy the brand at reduced frequency or switch to a lower dose. They either use a patient assistance program (which is costly for the brand to administer and does not generate revenue), buy from foreign pharmacies (illegal and generating zero revenue), or go without treatment.

An authorized generic priced at $80 to $120 per month for the same patient captures revenue that the brand’s pricing structure entirely forfeits. For a drug treating a chronic condition with high prevalence in uninsured populations – hypertension, diabetes, depression – the cash-pay AG can represent a genuinely additive revenue stream rather than a cannibalistic one.

GoodRx and similar discount programs have partially addressed the cash-pay market by negotiating prices between brand and generic levels for insured patients, but these programs extract margin through the distribution channel rather than routing revenue back to the brand. An authorized generic structure, managed by the brand manufacturer through a generic distribution partner, keeps more of that margin within the brand’s corporate structure.

International Market Tiering

For pharmaceutical companies with significant revenues outside the United States, authorized generic structures can enable price tiering across international markets in ways that protect the brand’s domestic pricing.

Reference pricing rules in many countries – where government payers adjust their reimbursement for a branded drug based on prices in a basket of reference countries – mean that brand price concessions in lower-income markets can mechanically reduce reimbursement rates in higher-income markets. An authorized generic sold through a separate entity in a tiered-price market can be structured to sit outside the reference pricing basket, capturing revenue in markets where brand pricing would be unaffordable while protecting the brand price in reference pricing-sensitive markets.

This structure requires careful design to avoid parallel trade concerns and regulatory scrutiny, but it is a legitimate commercial strategy with documented use among major pharmaceutical companies operating in both developed and emerging markets.

Life Cycle Management and the Pipeline Bridge

Authorized generic launches in uncontested markets frequently serve a life cycle management function that has nothing to do with current competitive conditions and everything to do with the brand’s position on its product life cycle curve.

Managing the Revenue Cliff Before Patent Expiry

A drug generating $1 billion in annual revenue today but facing compound patent expiration in three years presents a revenue planning problem for its manufacturer. Financial analysts and investors mark down the stock price now for the expected revenue loss then. The brand’s commercial team is under pressure to demonstrate a credible revenue trajectory that mitigates the cliff.

Launching an authorized generic three years before patent expiry, in a market with no current ANDA filings, accomplishes several things simultaneously. It builds a functioning generic distribution channel under conditions the brand controls entirely, before the channel gets populated with independent generic competitors. It establishes relationships with wholesalers and pharmacy chains in the generic procurement process. It gives the brand’s commercial team empirical data about how the generic segment of its market behaves – what pricing clears, what volumes flow through which channels, how PBM formulary managers respond to the AG’s availability.

All of that institutional knowledge has operational value when independent generic competition eventually arrives. The brand that has been running an authorized generic for three years understands its own market’s generic dynamics better than the brand that encounters generic competition for the first time at patent expiry.

From a financial planning perspective, a controlled AG launch also smooths the revenue cliff mathematically. A three-year ramp of gradually increasing AG volume alongside gradually declining brand volume is a less severe income statement event than an instant cliff when multiple independent generics enter simultaneously. Investors and analysts generally respond better to managed transitions than to binary events.

Protecting the Next-Generation Product Launch

Authorized generic launches in uncontested markets sometimes serve as competitive inoculation for a next-generation product.

Consider the scenario: a brand manufacturer has a drug generating significant revenue and a next-generation version of the same drug in late-stage development – a reformulation, a new delivery mechanism, a new indication, or a combination product. The brand wants to transition its patient base from the current product to the next-generation product, which will carry a higher price and a fresh patent life cycle.

The problem is competitive. If independent generic manufacturers enter the current product’s market at the same time the brand is trying to push patients up to the next-generation version, the brand faces simultaneous pressure on both fronts. Independent generics erode the current product’s revenue, reducing the marketing budget available to promote the next-generation product. PBMs, aware of generic availability for the current product, may resist favorable formulary placement for the next-generation product, arguing that the therapeutic equivalence question has been answered cheaply.

Launching an authorized generic of the current product before generic competitors enter controls that dynamic. The brand manages the timing and pace of the current product’s genericization, maintains the distribution relationships, and preserves marketing resources for the next-generation launch. When independent generics eventually enter the current product market, the patient population has already been partially transitioned to the next-generation product, and the transition has been managed on the brand’s timeline rather than the generic industry’s.

This strategy is sometimes called the “authorized generic bridge,” and it has been documented in the commercial strategies of several major pharmaceutical companies managing franchise products across multiple generations of compounds in the same therapeutic class.

The Patent Expiry Preemptive Strategy

Some of the most commercially interesting authorized generic launches in uncontested markets are driven not by current competitive conditions but by anticipated future competition – specifically, by the strategic desire to shape the competitive landscape before independent generic manufacturers can establish positions.

Disrupting the First-Filer Economics Before the First Filer Arrives

Under the Hatch-Waxman Act, the first generic manufacturer to file an ANDA with a Paragraph IV certification challenging a listed patent receives 180 days of generic exclusivity – a period during which the FDA will not approve any other ANDA filer [3]. This first-filer exclusivity is enormously valuable. During those 180 days, the first-filer typically captures 80 to 90 percent of the generic market volume while charging prices only modestly below the brand price, generating revenues that can recoup the litigation costs of the Paragraph IV challenge and then some.

The economic value of first-filer exclusivity is the primary incentive that motivates generic manufacturers to invest in Paragraph IV litigation in the first place. Eliminate or substantially reduce that economic value, and you reduce the incentive to file.

An authorized generic launched before any ANDA is filed – or before any ANDA holder triggers their 180-day exclusivity period – competes directly in the generic market during whatever first-filer exclusivity period eventually exists. The authorized generic does not receive or deplete the 180-day exclusivity clock; it is not an ANDA product. It simply exists in the market as a competitor.

A 2011 analysis by the FTC found that when a brand launched an authorized generic during a first-filer’s 180-day exclusivity period, generic market prices were 13 to 20 percentage points lower than when no AG competed, and the first-filer’s revenue during exclusivity fell by approximately 40 to 52 percent [4]. That is a substantial reduction in the economic prize that motivates Paragraph IV litigation.

If generic manufacturers conducting pre-filing commercial analyses know that this brand consistently deploys authorized generics and that the AG will be present during any future first-filer exclusivity period, they may conclude that the economics of Paragraph IV litigation against this brand’s patents do not justify the investment. The brand’s preemptive AG strategy in an uncontested market functions as a deterrent against future ANDA filings that have not yet occurred.

The Branded Equivalent to a Blocking Patent

IP strategists are familiar with the concept of a blocking patent – a patent whose purpose is not to protect specific commercial activity but to foreclose competitive moves by rivals. A blocking patent on a formulation the brand does not commercially use prevents generic manufacturers from pursuing that formulation as a design-around.

An authorized generic in a clean market functions analogously at the commercial level. It blocks the 180-day first-filer economics that otherwise incentivize generic entry challenges. It occupies the generic formulary tier before a competitor can. It establishes the brand’s manufacturing and distribution infrastructure in the generic segment of the market.

Unlike a blocking patent, an authorized generic requires no IP rights beyond the existing NDA. The brand’s approval already covers it. The strategic cost is accepting a lower price in the generic market segment. The benefit is making future generic entry – and the litigation that precedes it – economically less attractive than it would otherwise be.

DrugPatentWatch’s Orange Book patent and ANDA tracking data allow analysts to identify which drugs have authorized generics present in the market alongside their patent coverage status. The pattern of AG launches in markets with clean patent coverage and no pending ANDAs is observable in the data, and it clusters disproportionately around drugs with high revenue and medium-term patent expiry windows – precisely the profile where first-filer Paragraph IV incentives are strongest.

Supply Chain Economics and Manufacturing Utilization

Authorized generic launches in uncontested markets are sometimes driven by manufacturing economics rather than commercial strategy. The dynamics of pharmaceutical manufacturing create specific scenarios where producing and selling an authorized generic generates net positive economics even at generic prices.

Fixed-Cost Absorption in Underutilized Facilities

Pharmaceutical manufacturing plants are capital-intensive facilities with high fixed costs. A single-product API synthesis facility or a specialized tablet compression line has capacity that, once built, costs roughly the same whether it runs at 60 percent utilization or 90 percent utilization. Variable costs – raw materials, direct labor, energy – scale with volume, but fixed costs, depreciation, and site overhead do not.

When a drug’s brand-market volume is declining – because the drug is aging, patient populations are shifting to newer therapeutic options, or prescribing guidelines have evolved – the manufacturing facility built to produce that drug at peak volume begins running well below its economic design point. Each unit produced under those conditions carries a high allocated fixed cost, which squeezes margins even at brand prices.

Adding authorized generic volume to the same manufacturing facility absorbs fixed costs across more units. Even at a 60 percent discount to brand pricing, if the generic volume fills excess capacity, the total financial contribution can be positive when the fixed-cost absorption benefit is properly accounted for. A simplistic per-unit margin analysis misses this because it allocates full fixed costs to each unit rather than recognizing that the incremental cost of the generic units is primarily variable.

Pharmaceutical companies with vertically integrated manufacturing operations – particularly large-molecule biologics manufacturers running fermentation and purification facilities – face this economics structure acutely. The capital cost of a biologic manufacturing line is orders of magnitude higher than a solid oral dosage form line, and the utilization economics are correspondingly more sensitive.

Contract Manufacturing Organization Relationships

Brand manufacturers who outsource their manufacturing to contract manufacturing organizations (CMOs) often have take-or-pay minimum purchase commitments in their CMO contracts. These commitments guarantee minimum volumes regardless of actual commercial demand, and they are negotiated based on projected peak volumes during the product’s commercial life.

As a brand’s commercial volume declines late in its life cycle, the take-or-pay commitments may exceed what the brand can sell at brand prices. The brand is paying for more product than it can commercially move. Launching an authorized generic channels that contracted production volume through the generic market segment, converting a stranded obligation into a revenue-generating distribution.

This is not purely hypothetical. Contract manufacturing agreements in pharmaceutical markets regularly create volume overhang that authorized generic distribution resolves. The brand avoids paying for product it cannot sell, the CMO meets its production commitments, and the authorized generic captures revenue from market segments accessible only at generic prices.

Regulatory Compliance and Batch Manufacturing Requirements

FDA regulations require manufacturers of approved drug products to maintain validated manufacturing processes and to periodically produce batches for stability testing and regulatory compliance purposes, even for products with low or declining commercial demand. A drug with a three-year shelf life must demonstrate that its manufacturing process remains validated and that stability specifications are met across the shelf life.

For low-volume brand products, the minimum batch sizes required for regulatory compliance under cGMP standards may produce significantly more product than the brand market demands at brand prices. The surplus product either sits in inventory (generating carrying costs and exposure to expired inventory write-offs) or is destroyed (generating a direct loss).

An authorized generic distribution channel creates a market for the regulatory compliance batch production. Rather than destroying or warehousing product from mandatory production runs, the brand sells it through generic channels. The regulatory compliance cost becomes partially offset by generic market revenue.

Tax, Transfer Pricing, and Corporate Structure Considerations

Authorized generic arrangements between a brand parent and a generic subsidiary, or between a brand and a third-party generic licensee, create financial and tax structures that motivate AG licensing independent of any commercial strategy rationale.

Inter-Company Transfer Pricing and IP Location

In multinational pharmaceutical companies, intellectual property is frequently held by subsidiaries in favorable tax jurisdictions – Ireland, Switzerland, the Netherlands, Singapore. The manufacturing entity, sales entity, and IP-holding entity may all be in different countries, and the pricing of inter-company transfers of product and IP rights determines where taxable income accrues.

An authorized generic licensing arrangement between a brand’s IP-holding subsidiary and its generic distribution subsidiary creates inter-company transactions with defined transfer prices. Properly structured, these transactions can route taxable income toward lower-tax jurisdictions within the constraints of OECD transfer pricing guidelines and local tax law.

This is standard multinational tax planning, applied to the authorized generic context. The economic substance requirements of modern transfer pricing rules mean that the structure must reflect genuine commercial reality – it cannot simply be a paper arrangement designed to shift income. But where genuine commercial activity exists on both sides of the transaction, the AG licensing arrangement can be structured to optimize the distribution of taxable income within the corporate group.

Tax strategy alone is not sufficient to drive authorized generic licensing decisions. But in scenarios where multiple motivations exist – manufacturing economics, market segmentation, pipeline protection – the tax structuring upside can make an otherwise marginal decision clearly positive.

Royalty Streams and Revenue Diversification

For pharmaceutical companies managing their investor relations, revenue structure matters. A company generating 100 percent of its revenue from brand drug sales is more exposed to single-product binary risks than one with diversified revenue streams. Authorized generic licensing arrangements generate royalty or transfer pricing income that analysts may classify differently from brand drug revenue, providing a degree of revenue diversification visible in financial reporting.

This consideration is more relevant for mid-sized pharmaceutical companies than for large diversified firms. A company with a single blockbuster drug facing a patent cliff needs to demonstrate to investors that its revenue base will not simply collapse when the compound patent expires. An authorized generic revenue stream, established before the cliff and operating through a well-structured licensing arrangement, demonstrates that management has a plan for the post-cliff period. That demonstration itself has value in reducing the discount that equity markets apply to near-term patent expiry events.

Patient Access, Advocacy, and Reputational Strategy

Commercial and strategic considerations are not the only drivers. Brand pharmaceutical companies operate within a political and social environment where drug pricing and patient access are under constant scrutiny, and authorized generic launches can serve reputational and advocacy objectives.

Responding to Congressional and Executive Branch Pressure

The political pressure on pharmaceutical pricing has intensified consistently since the early 2000s. Drug pricing hearings before the Senate Finance Committee, executive orders on international reference pricing, and the negotiation provisions of the Inflation Reduction Act of 2022 [5] have all created an environment in which brand manufacturers face genuine reputational and regulatory risk from pricing practices that can be characterized as exploitative.

A brand manufacturer that launches an authorized generic in an uncontested market, making a lower-priced version available before any generic competitor forces the issue, has a defensible story to tell in that political environment. It demonstrates proactive access commitment rather than reactive capitulation to competition. This narrative has value in Congressional testimony, FDA relations, and public communication with patient advocacy groups.

The reputational benefit is difficult to quantify financially, but it is not zero. Pharmaceutical companies spend hundreds of millions of dollars annually on patient assistance programs, co-pay cards, and access initiatives that generate no direct revenue specifically because the reputational and regulatory cost of being seen as denying access is genuinely high. An authorized generic, which also generates actual revenue, is a more efficient access investment.

Patient Adherence Economics for Chronic Disease Drugs

For drugs treating chronic conditions – diabetes, hypertension, HIV, psychiatric disorders – patient adherence to the treatment regimen is a commercially material variable for the brand manufacturer as well as a public health concern.

Research consistently shows that medication adherence declines as out-of-pocket cost increases. A study in the New England Journal of Medicine by Choudhry et al. [6] found that patients with higher prescription co-payments had meaningfully lower adherence rates across several chronic disease categories, and that lower adherence was associated with higher rates of hospitalization and emergency care.

For the brand manufacturer, a patient who stops taking a $200-per-month drug because they cannot afford it does not become a revenue loss; they were already not generating revenue through patient assistance programs or uninsured pathways. But if the brand’s authorized generic at $60 per month keeps that patient in therapy, the manufacturer captures the AG revenue while also maintaining population-level outcomes data that supports the drug’s label and future indications.

The adherence economics are particularly compelling for drugs where patient outcomes data drives prescribing decisions. A chronic disease drug with strong real-world adherence data, generated partly by the AG’s accessible price point enabling adherence in cost-sensitive patient segments, supports the clinical narrative that justifies the brand’s continued use in adherent, less price-sensitive patients.

The Authorized Generic as a Litigation Settlement Tool

Patent litigation between brand manufacturers and generic challengers produces settlements, and authorized generic rights are among the most common currencies in those settlements. But a brand’s ability to offer AG rights as a settlement tool depends on having previously established the commercial and operational infrastructure to actually deliver an authorized generic. A brand that has never contemplated an AG launch cannot credibly offer one as a settlement term.

The Actavis Framework and Authorized Generic Settlements

Following the Supreme Court’s decision in FTC v. Actavis [7], pay-for-delay settlements – in which brand manufacturers pay generic challengers to stay out of the market – are subject to antitrust scrutiny under the rule of reason. The Actavis decision fundamentally changed the economics of Hatch-Waxman settlement negotiations, because the most straightforward form of value transfer (cash payment to the generic to delay entry) now carries antitrust liability risk.

Authorized generic licenses emerged as a prominent settlement currency in the post-Actavis environment, because they transfer value to the generic challenger without involving cash payments. A settlement in which the brand grants an AG license gives the generic challenger a revenue-generating product to sell during an agreed exclusivity period or prior to their ANDA approval, compensating them for litigation costs and providing a business rationale for early entry without the explicit cash transfer that Actavis scrutinized.

The antitrust analysis of AG-as-settlement-currency is itself complex and unresolved. The FTC has argued that AG licenses can function as implicit reverse payments and should be scrutinized similarly to cash payments. Courts have reached varying conclusions on this analysis, and the issue has not been definitively resolved at the circuit court level as of 2024.

What is clear is that brands that have established authorized generic programs – with real pricing structures, real distribution relationships, and real operational capability – are better positioned to offer credible AG rights as settlement currency than brands that are proposing a hypothetical arrangement. Building the AG infrastructure before it is needed in a litigation settlement context has option value that is not always captured in the immediate commercial analysis of whether to launch an AG in an uncontested market.

Negotiating Entry Dates and License Parameters

The terms of an authorized generic settlement license matter considerably for the brand’s economics. Licenses can be structured to limit the AG’s pricing freedom (minimum price provisions prevent the licensee from undercutting the brand by more than an agreed percentage), to restrict distribution channels (retail-only or specific geographic limitations), or to expire automatically upon certain events (the entry of a third independent generic, the expiration of a specified exclusivity period).

A brand that has never run an authorized generic has little operational experience to inform the negotiation of these parameters. It does not know what price a generic licensee will actually set in the market, what volume to expect through different distribution channels, or what the realistic margin sharing should look like. These are questions that can be answered definitively by prior operational experience, and they are questions on which a brand negotiating an AG settlement license without that experience will be at an informational disadvantage relative to the generic manufacturer who lives in that market every day.

Specialty and Rare Disease Drug Dynamics

The authorized generic logic described so far applies most straightforwardly to standard small-molecule oral dosage drugs with large patient populations. Specialty drugs and rare disease drugs present specific dynamics that create additional authorized generic rationales.

Controlled Distribution and REMS Programs

Some pharmaceutical products require distribution through restricted programs under the FDA’s Risk Evaluation and Mitigation Strategy (REMS) framework. REMS programs impose specific conditions on distribution – specialized pharmacies, prescriber certification, patient enrollment, and dispensing restrictions – to manage drugs with serious safety concerns.

For REMS-covered drugs, independent generic manufacturers face regulatory barriers beyond just patent and exclusivity. They cannot freely distribute through standard pharmacy channels and must either access the brand’s REMS-restricted distribution system or establish equivalent restricted distribution systems of their own.

The FTC and multiple generic manufacturers have accused brand companies of using REMS programs as distribution barriers to generic entry – specifically, by refusing to share samples needed for bioequivalence testing on the grounds that doing so would require the brand to participate in the generic’s development program. This practice, sometimes called “REMS abuse,” has been addressed in part by the FDA Reauthorization Act of 2017 [8], which created a pathway for generics to obtain samples without brand cooperation, but implementation has been slow.

In this context, an authorized generic licensed by the brand through its own REMS-compliant distribution infrastructure is sometimes the fastest and most practically achievable path to lower-cost access. The brand controls the distribution system and can authorize a partner to sell through it without establishing a new REMS equivalent.

Payers and policy advocates who might otherwise support aggressive generic competition recognize that in REMS drug markets, brand-authorized access through existing infrastructure may be the only near-term mechanism for price competition. This creates social license for authorized generic arrangements in specialty drug markets that might not exist in standard commodity generics.

Orphan Drug Market Architecture

Orphan drugs, treating conditions affecting fewer than 200,000 patients in the United States [9], receive seven years of market exclusivity from the FDA independent of patent status. During that exclusivity period, the FDA will not approve any other application for the same active moiety for the same orphan disease indication.

After orphan exclusivity expires, independent generic entry requires bioequivalence testing on a drug with a small patient population – a genuinely challenging logistical problem, since recruiting patients for bioequivalence studies in rare diseases with small prevalence may not be practically feasible. The FDA has struggled with how to apply standard bioequivalence requirements to rare disease drugs, and several important orphan drugs have remained effectively uncontested for years after orphan exclusivity expired simply because generic manufacturers found the bioequivalence pathway impractical.

For a brand manufacturer whose orphan drug exclusivity is expiring, an authorized generic – which requires no separate bioequivalence testing because it operates under the brand’s NDA – can be launched the moment exclusivity expires without waiting for the generic entry infrastructure to develop. This gives the brand a lower-priced option in the market before independent generics can establish a regulatory pathway.

The commercial rationale in orphan markets is particularly strong because the patient population is small, price-sensitive segments are concentrated, and payer decisions are made at the formulary level with substantial focus on total cost of care. An authorized generic in an orphan disease market can provide payers with price relief while maintaining the brand’s manufacturing economics, since the same controlled supply chain services both the brand and AG demand.

Biosimilar Authorized Generics: A Distinct Strategic Layer

The authorized generic concept extends, with important differences, to the biologics market under the biosimilar framework established by the Biologics Price Competition and Innovation Act (BPCIA).

Authorized Biosimilars vs. Independent Biosimilar Competition

A reference product sponsor – the brand biologic manufacturer – can authorize a biosimilar applicant to market its biologic product as an “authorized biosimilar” under an arrangement that functions analogously to the small-molecule authorized generic. The reference product sponsor grants the authorized biosimilar licensee rights to market the biologic under the same Biologics License Application (BLA) under which the reference product is approved.

This is not the same as an independent biosimilar, which requires its own BLA, its own manufacturing process characterization, and its own demonstration of biosimilarity to the reference product. An authorized biosimilar uses the originator’s manufacturing process – often because it is manufactured by the originator or under the originator’s direct technical supervision.

The competitive implications are significant. During the period when independent biosimilar manufacturers are completing their complex and expensive development programs – a process that routinely takes five to seven years and costs hundreds of millions of dollars – the reference product sponsor can authorize a biosimilar entrant at considerably lower cost by providing access to the manufacturing process and the regulatory approval.

Rebate Strategy in the Biologic Market

The biologic market differs from the small-molecule market in its rebate structure. PBMs negotiate large rebates from biologic manufacturers in exchange for favorable formulary placement, and these rebates can represent 40 to 60 percent of the list price for major biologic drugs. The net price actually received by the manufacturer is dramatically lower than the list price, but the rebate-driven formulary position maintains high-volume prescribing.

Authorized biosimilar launches are sometimes structured to allow the reference product sponsor to participate in a market segment that operates outside the rebate-heavy channel. An authorized biosimilar distributed through specialty pharmacy at a lower list price but with minimal rebate may actually generate higher net revenue per unit than the brand biologic, which carries a high list price but pays a massive rebate to maintain formulary position.

Modeling this dynamic properly requires data on both the biologic’s net price after rebates and the operating economics of the authorized biosimilar distribution channel – data that is not publicly available in detail but can be approximated using SEC disclosure of average selling prices and PBM contract disclosures.

Case Study: The ADVAIR Authorized Generic Decision

GlaxoSmithKline’s ADVAIR (fluticasone propionate/salmeterol) inhaler franchise illustrates how multiple authorized generic rationales converge in practice.

ADVAIR was the top-selling branded respiratory drug in the United States for much of the 2010s, with peak annual sales exceeding $4 billion [10]. Its active patent protection was complicated – the individual compound patents on fluticasone and salmeterol had expired or were near expiry, but device patents on the DISKUS dry powder inhaler and formulation patents on the specific fixed-dose combination provided continuing protection.

Generic entry was delayed not only by patents but by the complexity of demonstrating bioequivalence for inhaled drugs, where the particle size distribution, device mechanics, and lung deposition characteristics all affect clinical efficacy in ways that standard bioequivalence testing metrics do not fully capture. The FDA required additional device and clinical testing for inhaled generic products that extended the effective generic entry delay years beyond what the underlying compound patent status would suggest.

GSK launched an authorized generic version of ADVAIR through its Prasco subsidiary partnership, which distributed the product at a discount to the brand. The launch occurred in a market where independent generic ADVAIR was not yet available and would not be available for several more years.

The commercial logic operated across multiple dimensions simultaneously. The authorized generic captured the volume of price-sensitive and uninsured patients who were not buying ADVAIR at brand prices. It gave GSK market position and channel relationships in the generic distribution segment before independent competition arrived. It demonstrated to payers that GSK was actively managing access, providing some insulation from the formulary exclusion pressure that competing inhaled corticosteroid/LABA combinations were creating. And it provided empirical pricing and volume data about how the ADVAIR patient population behaved in the generic price segment – data that informed GSK’s commercial planning for the eventual independent generic entry period.

DrugPatentWatch’s product-level tracking showed the ADVAIR AG launch timing in relationship to the device and formulation patent expiration schedule, the pending generic applications status, and the FDA’s regulatory action dates on generic ADVAIR applications – providing the multi-dimensional view of competitive positioning that each individual data source, considered alone, could not deliver.

Case Study: HIV Drug Authorized Generic Programs

The HIV drug market provides some of the most extensively documented examples of authorized generic programs in therapeutic areas where both commercial and access rationales operate simultaneously.

Gilead Sciences built a complex authorized generic architecture around its HIV franchise, partially through a voluntary licensing program administered through the Medicines Patent Pool [11] and partially through direct authorized generic distribution in middle-income countries.

The commercial and access rationales intersected clearly in this case. In high-income markets, Gilead’s branded HIV drugs generated revenue at brand prices that funded the research and development pipeline for next-generation compounds. In low-income markets, those brand prices were simply unaffordable, and negotiated access programs operating through the Medicines Patent Pool licensed generic manufacturers to produce and distribute versions of Gilead’s compounds at dramatically lower prices.

The middle-income market segment – countries where the disease burden is high, the healthcare system has some purchasing capacity, but brand prices remain unaffordable – was the commercially interesting gray zone. Authorized generic arrangements allowed Gilead to participate in revenue from those markets through transfer pricing structures while maintaining the pricing architecture of the high-income branded market.

This structure was not without controversy. Critics argued that the tiered pricing produced by authorized generic programs still left many middle-income country patients unable to afford treatment. Proponents argued that the alternative – refusing to permit any authorized generic in middle-income markets to protect brand pricing – would have resulted in zero revenue from those markets and far less treatment access.

The HIV case also illustrates the reputational dimension. Gilead’s authorized generic and Medicines Patent Pool participation was cited repeatedly by the company in Congressional testimony and public communications as evidence of its commitment to access. Whether this reputational benefit influenced specific regulatory outcomes is difficult to assess, but the company clearly believed it had commercial and regulatory value.

Case Study: Insulin and Biosimilar Authorized Generic Dynamics

Insulin’s transition from analog brand dominance to the biosimilar and authorized generic market structure of the 2020s illustrates how the dynamics shift when political and policy pressure specifically targets a product’s pricing.

Eli Lilly, Novo Nordisk, and Sanofi faced intense Congressional and executive branch pressure over insulin pricing beginning around 2019, with high-profile cases of patients rationing insulin due to cost receiving national media attention. The political environment created specific and immediate pressure for lower-cost insulin availability.

All three manufacturers responded with authorized generic insulin programs – lower-priced versions of their existing insulin products sold under the unbranded nonproprietary name. Lilly’s authorized generic insulin lispro launched at $35 per vial, compared to the brand Humalog’s list price of over $300. Novo Nordisk launched an unbranded authorized generic version of NovoLog.

These launches were not responses to competitive generic entry. No meaningful independent insulin biosimilar competition existed in the U.S. market at the time of most of these announcements. They were proactive authorized generic launches in uncontested or lightly contested markets, driven explicitly by the combination of political pressure, reputational risk management, and the commercial recognition that a significant portion of the insulin patient population was either not being reached at brand prices or being reached through costly patient assistance programs that generated no revenue.

The Lilly authorized generic insulin lispro example is particularly instructive. The product is physically identical to Humalog – same active ingredient, same formulation, same manufacturing facility. The price difference is determined entirely by the channel and pricing architecture, not by any difference in the product or its manufacturing cost. The authorized generic structure allowed Lilly to maintain its brand pricing for commercially insured patients who continued to pay through PBM-managed pharmacy benefits (where Lilly’s rebate structure depended on maintaining high list prices), while simultaneously making the product accessible to the cash-pay patient who was the focus of the political and media attention.

This dual-price structure – identical product, very different price depending on channel – is only possible through the authorized generic mechanism. A simple brand price reduction would have cascaded through the rebate negotiation structure and reduced net revenue across the entire commercial channel. The authorized generic preserved brand channel pricing while adding a new market segment.

Regulatory Pathways and Practical Launch Mechanics

Understanding the mechanics of how a brand actually launches an authorized generic in an uncontested market clarifies why the option is more accessible than it might appear and why it does not require the regulatory work that independent generic entry does.

The NDA Supplement Route

An authorized generic can be launched without any NDA supplement if the product is manufactured and sold exactly as described in the existing NDA – same formulation, same dosage form, same strength, same manufacturing facility, using the brand’s already-approved specifications. The brand simply notifies the FDA under 21 U.S.C. § 355(t) and begins distribution under the generic label.

If the brand wants to make any change to the product for the authorized generic version – a different excipient, a different dosage form, a different delivery device – it needs to evaluate whether that change requires a Prior Approval Supplement, a Changes Being Effected Supplement, or an Annual Reportable Change under the FDA’s scale of manufacturing change categories. For most common authorized generic scenarios – same formulation, different packaging and labeling – no supplement is required.

This absence of a separate regulatory approval pathway is what makes the authorized generic structurally different from an independent generic. The brand already has the approval. Launching the AG is a commercial decision, not a regulatory one.

Labeling Requirements and FDA Notification

The FDA requires that the authorized generic’s label accurately reflect the product, which means it must carry the generic nonproprietary name rather than the brand name if it is being marketed as a generic. The label cannot include brand-specific trade dress or trademarks. The FDA notification under § 355(t) must include the name of the drug, the date on which marketing will begin, and the identity of the entity marketing the authorized generic.

The FDA maintains a publicly accessible list of authorized generics marketed under § 355(t), updated annually. DrugPatentWatch indexes this list alongside Orange Book patent and exclusivity data, allowing analysts to identify exactly which drugs have authorized generic versions in market, who is marketing them, and when they launched relative to patent expiration dates and ANDA activity.

This transparency is commercially significant. Generic manufacturers considering Paragraph IV filings against a drug can check whether an authorized generic is already present in the market – and factor that into their economic analysis of first-filer exclusivity value – before committing resources to a litigation campaign.

What the Data Shows About Uncontested Authorized Generic Launches

Systematic analysis of authorized generic launch patterns reveals that a meaningful portion of AG launches occur in markets without concurrent independent generic competition. The academic literature on this pattern, while focused primarily on the post-Hatch-Waxman competitive context, provides empirical evidence consistent with the strategic rationales described above.

Frequency and Product Characteristics

Research by Berndt and Aitken [12], analyzing AG launch patterns across a sample of brand drugs, found that approximately 25 to 30 percent of authorized generic launches in their sample occurred before independent generic entry, in markets where the brand faced no competitive generic presence at the time of AG launch. These products were disproportionately concentrated in specific categories: drugs with high cash-pay demand, drugs with near-term patent expiry within two to four years, and drugs in therapeutic classes where the political visibility of drug pricing was high.

The revenue profile of products with pre-entry AG launches showed a characteristic pattern: the AG captured 8 to 15 percent of total product revenue in uncontested markets, primarily from cash-pay and Medicaid managed care channels where price sensitivity was highest, while the brand maintained its revenue base in commercially insured channels.

Pricing Behavior in Uncontested AG Markets

In markets where the authorized generic is the only competition to the brand – where both the brand and the AG come from the same corporate structure – the pricing equilibrium is very different from markets with independent generic competition.

Independent generic competition drives prices down toward marginal manufacturing cost because generic manufacturers are competing for volume against each other, not just against the brand. Two independent generics in a market typically produce price erosion to 20 to 40 percent of brand price. Ten independent generics drive prices to 10 to 20 percent of brand price [13].

An authorized generic in an uncontested market is controlled by the brand manufacturer or a licensee who has contractual pricing constraints. The AG is typically priced at 20 to 40 percent below the brand, not at the floor levels that competitive generic markets produce. This controlled pricing structure preserves far more total revenue per prescription than the fully competitive generic scenario, which is another reason why brands with near-term patent expiry prefer to reach the fully competitive generic period having already established an AG at a controlled price point, rather than watching independent generics immediately compete prices to cost.

The Role of Authorized Generics in Medicaid and Government Pricing

Federal pricing rules for Medicaid create specific financial incentives that make authorized generic decisions more complicated for brand manufacturers than the commercial analysis alone suggests.

Best Price Calculations and Medicaid Rebates

Under the Medicaid Drug Rebate Program, manufacturers of brand drugs must pay rebates to state Medicaid programs calculated as a percentage of Average Manufacturer Price (AMP), and must also report their “Best Price” – the lowest price paid by any commercial customer [14]. If the brand sells product to any commercial customer at a deeply discounted price, that price potentially becomes the Best Price and reduces the Medicaid rebate calculation.

An authorized generic sold through a separate legal entity – a generic subsidiary or a third-party licensee – is not automatically the brand’s “Best Price” for Medicaid rebate calculation purposes. The Best Price is calculated at the labeler level, and the authorized generic may be sold under a different labeler code. This separation allows the brand to price the AG at generic market levels without mechanically reducing its Medicaid rebate baseline.

However, the structure requires careful legal analysis. If the authorized generic transaction is structured in a way that the brand effectively controls the price and receives the economic benefit, regulatory authorities may look through the corporate structure and treat the AG price as the brand’s effective price. CMS has issued guidance on when authorized generic prices must be included in brand manufacturers’ Best Price calculations, and the analysis turns on the specific contractual and economic relationship between the brand and its AG distributor.

Getting this structure wrong is expensive. Understated Medicaid rebates generate liability for the difference plus significant penalties, and CMS has actively examined authorized generic arrangements during Medicaid audit activities. Brands considering AG launches in uncontested markets should obtain specific legal analysis of the Medicaid pricing implications of their intended structure before launch.

340B Program Dynamics

The 340B drug pricing program requires covered manufacturers to sell outpatient drugs to eligible healthcare entities – primarily safety-net hospitals and community health centers – at ceiling prices equal to or below a specified discount from AMP [15]. The authorized generic’s AMP, if it is covered under the program, affects the 340B ceiling price calculations.

For drugs with significant 340B purchasing volume, the pricing architecture of an authorized generic launch in an uncontested market needs to account for how the AG’s pricing will affect 340B ceiling prices for both the brand and the AG. This is another layer of financial modeling complexity that reinforces the point that authorized generic decisions in pharmaceutical markets require multidisciplinary analysis across commercial, regulatory, legal, and financial functions.

Building the Business Case: A Framework for the Decision

For a pharmaceutical company evaluating whether to launch an authorized generic in an uncontested market, the analysis needs to systematically address the full range of factors described in this article rather than focusing narrowly on the direct commercial cannibalization question.

The Eight-Factor Assessment

A rigorous business case for an uncontested AG launch should work through eight primary considerations:

The market segmentation analysis: What share of current prescriptions are in price-sensitive segments that are either not being captured at brand prices or being captured through costly access programs? What price point would convert these unconverted potential patients into paying customers?

The manufacturing economics: Does the brand have excess capacity or take-or-pay obligations that make incremental generic volume financially positive at the contribution margin level? What is the incremental cost of goods for generic volume versus the incremental revenue it generates?

The pre-emptive competitive positioning: When is the earliest realistic Paragraph IV ANDA filing likely? What would the 180-day first-filer exclusivity economics look like with and without an existing authorized generic competing during that window? Does the presence of an AG materially change the expected value of filing?

The patent cliff transition: How does an AG launch before the cliff change the revenue trajectory around patent expiry? What is the value of institutional knowledge about generic distribution dynamics, built through AG operations before the cliff, relative to the cost of generic channel revenue cannibalized from the brand?

The next-generation product implications: Is there a successor product in late-stage development? How does the current drug’s AG launch affect the transition timeline and the commercial resources available to support the new product launch?

The tax and financial structure: Can the AG be structured through entities in favorable tax jurisdictions in a way that reduces the effective tax rate on the AG revenue stream? What are the Medicaid Best Price and 340B implications?

The reputational and political calculus: Is the drug in a therapeutic category under active Congressional or executive scrutiny? Would an AG launch generate favorable narrative value that has quantifiable benefit in regulatory relationships, Congressional testimony, or formulary negotiations?

The litigation option value: What is the expected value of having established AG operational capability for use in future Paragraph IV settlement negotiations?

These eight factors may not all point in the same direction. In many real-world evaluations, some factors support AG launch and others counsel against it. The business case synthesizes them into a net assessment using whatever financial modeling approach – DCF, real options, scenario analysis – fits the company’s analytical infrastructure.

DrugPatentWatch’s data on AG launch timing, Paragraph IV filing activity, and exclusivity status provides the empirical inputs for the pre-emptive competitive positioning assessment – specifically, the analysis of which drugs with similar patent profiles attracted first-filer ANDA filings and at what lag from commercial launch, which informs the expected timing of competitive challenge and therefore the value of pre-emptive AG positioning.

When Not to Launch an Authorized Generic in an Uncontested Market

The strategic case for AG launches in uncontested markets is not universal. Specific conditions reduce the attractiveness of the strategy and can make it actively counterproductive.

When Medicaid Pricing Exposure Is Material

For drugs with very high Medicaid market share – drugs where state Medicaid programs represent 40 percent or more of prescriptions – the Best Price exposure risk associated with an AG launch at generic price levels may outweigh the commercial benefits. If the corporate structure cannot cleanly separate the AG pricing from the brand’s Best Price calculation, the Medicaid rebate liability exposure could materially exceed the AG revenue generated.

Drugs with high Medicaid share tend to be concentrated in therapeutic areas serving lower-income populations: psychiatric drugs, substance use disorder treatments, certain HIV drugs, and drugs for chronic conditions prevalent in lower-income demographics. In these therapeutic areas, the access narrative might support an AG launch, but the Medicaid pricing mechanics may not.

When Patent Challenges Are Genuinely Unlikely

The pre-emptive competitive positioning rationale requires that Paragraph IV filings are a realistic near-to-medium-term risk. For drugs with very broad compound patents with many years remaining, highly specialized drug-device combinations with no clear generic pathway, or drugs in therapeutic categories where generic manufacturers historically have not invested in Paragraph IV litigation, the deterrence value of an AG is low.

Investing in the commercial and operational infrastructure to run an authorized generic program – establishing distribution relationships, managing a second SKU, addressing the compliance and regulatory notification requirements – has real cost. If the probability of first-filer competition that would threaten those costs is very low, the investment may not generate sufficient expected return.

When the Brand Is Supporting a Premium Positioning Strategy

Some pharmaceutical companies actively invest in brand positioning that commands a significant price premium based on perceived quality, service, or innovation attributes. Launching an authorized generic in this market – advertising, in effect, that the brand and a cheaper version are identical – directly undermines the premium positioning logic.

This tension is particularly acute for specialty drugs where prescribers make brand-versus-generic decisions and may use AG availability as evidence that brand-exclusive quality claims are commercially motivated rather than clinically substantiated. In these markets, the brand’s commercial team may correctly conclude that the AG revenue generated does not compensate for the brand equity erosion it produces.

The Competitive Intelligence Lens: Reading AG Decisions as Market Signals

For pharmaceutical analysts, investors, and competitive intelligence professionals, an uncontested authorized generic launch by a brand manufacturer is a signal worth decoding.

What an AG Launch Reveals About Internal Patent Confidence

A brand that launches an authorized generic in a market with clean patent coverage and no pending ANDA filings is, by implication, communicating something about its internal assessment of that patent coverage. If management believed the patent was impenetrable for the full remaining term, they might reasonably wait to capture the full brand revenue stream for as long as possible before accepting any generic-level pricing.

The willingness to accelerate generic pricing in a market the brand legally controls suggests that the brand’s legal team has identified potential vulnerability in the patent coverage that is not visible in the Orange Book listing. It may reflect ongoing freedom-to-operate analysis that reveals potential design-around paths. It may reflect internal projections that a first-filer Paragraph IV campaign is more likely to succeed than the patent’s face validity suggests.

For a generic manufacturer evaluating which brand drugs to target with Paragraph IV campaigns, a brand’s preemptive AG launch in an uncontested market is evidence worth weighing. It does not definitively establish patent vulnerability – the AG may be purely market segmentation or manufacturing economics-driven – but it shifts the probability assessment.

Revenue Trajectory Signals for Investors

For equity investors, a brand’s decision to launch an authorized generic in an uncontested market communicates management’s assessment of the product’s future competitive trajectory. If the brand expected to maintain clean exclusivity through the natural patent life, the incremental revenue from an AG at generic prices would be incrementally positive but modest. If the brand expected competitive generic entry sooner than the patent expiry would suggest, an AG launch now positions the company more favorably for the transition.

Financial analysts covering pharmaceutical stocks track authorized generic launches specifically as signals about the patent life cycle assessments embedded in guidance. An AG launch that precedes official guidance of generic entry risk by several quarters is sometimes a leading indicator that revenue guidance for the product will be revised downward in subsequent periods.

DrugPatentWatch’s tracking of authorized generic launch dates alongside Orange Book patent status and ANDA filing activity provides the data infrastructure to systematically analyze this signaling relationship across a large product set, identifying statistical patterns in how pre-emptive AG launches relate to subsequent Paragraph IV challenge timing.

Conclusion: The Authorized Generic Is a Strategic Choice, Not a Concession

Across all the scenarios examined in this article, one pattern holds consistently: brand pharmaceutical companies that launch authorized generics in uncontested markets are exercising strategic optionality, not surrendering to competitive pressure.

The decision reflects a sophisticated recognition that pharmaceutical market structure is not binary. A drug does not simply have full exclusivity or no exclusivity. Between those poles lies a continuous space of market segmentation, pricing architecture, channel economics, and competitive positioning that authorized generic programs can actively shape.

The specific rationale varies by product, by company, and by market circumstances. For one drug, the primary driver is capturing cash-pay volume that the brand price forfeits entirely. For another, it is building the distribution infrastructure and institutional knowledge needed to manage the competitive cliff that is now only three years away. For a third, it is managing political pressure in a therapeutic class under Congressional scrutiny. For a fourth, it is the manufacturing economics of a take-or-pay CMO agreement that makes generic volume financially positive at the contribution margin level.

In none of these cases is the brand “giving away” its market. It is making a calibrated commercial decision to serve a segment of the market at a price point that segment will actually pay, for reasons that extend well beyond the immediate revenue impact of that pricing decision.

The professionals who most need to understand this logic are not only brand commercial teams. They include generic manufacturers conducting pre-filing economic analyses, pharmaceutical investors interpreting AG announcements as signals, policymakers designing pricing and access frameworks, and IP litigators assessing how AG infrastructure affects settlement economics. For all of them, the authorized generic in an uncontested market is not a curiosity. It is evidence that the brand manufacturer has thought more carefully about its product’s competitive future than the clean patent cover of the Orange Book would suggest.

Key Takeaways

An authorized generic launched in a market with no competing generics is almost always a proactive strategic decision, not a defensive response to competitive pressure. The absence of generic competitors does not eliminate the commercial logic for AG deployment.

Market segmentation is the most straightforward rationale. Brand pharmaceutical markets contain multiple payer segments with very different price sensitivity. A single brand price cannot capture all of them. An authorized generic captures the cash-pay, Medicaid managed care, and price-sensitive insured segments that brand pricing forfeits.

Preemptive AG launches reduce the economic value of future first-filer Paragraph IV exclusivity by competing in the generic market during whatever exclusivity window eventually materializes. This deterrent effect has documented empirical support, with first-filer revenues falling 40 to 52 percent when an authorized generic competes during the 180-day exclusivity period.

Manufacturing economics, including fixed-cost absorption and take-or-pay CMO obligations, can make AG volume financially positive at the contribution margin level even at significant price discounts to the brand, when properly accounting for cost allocation.

Life cycle management strategy, specifically building generic distribution infrastructure and market knowledge before independent generic entry, positions the brand manufacturer more favorably for the competitive transition around patent expiry.

Next-generation product launches benefit when the authorized generic manages the current product’s genericization on the brand’s timeline, preserving marketing resources and patient population transitions.

Reputational and political considerations in therapeutic classes under active pricing scrutiny can justify AG launches that generate favorable narrative value alongside direct commercial revenue.

Medicaid Best Price and 340B pricing mechanics create financial risks that must be specifically analyzed for each AG launch scenario. The corporate separation between brand and AG distributor must reflect genuine economic substance to withstand regulatory review.

Authorized generic rights are valuable settlement currency in post-Actavis Hatch-Waxman litigation. Brands that have established operational AG infrastructure before they need to offer it in settlement negotiations are in a stronger position than those proposing hypothetical arrangements.

For competitive intelligence purposes, a brand’s preemptive AG launch in a clean patent market is a signal about management’s internal patent confidence assessment and projected competitive timeline, and should be weighted in patent challenge economic analysis.

DrugPatentWatch provides the structured integration of FDA authorized generic notifications, Orange Book patent status, ANDA filing records, and exclusivity timelines that makes systematic analysis of AG launch patterns across a large product set operationally feasible.

FAQ

Q1: Does launching an authorized generic in an uncontested market automatically trigger any FDA regulatory requirements or filings beyond the § 355(t) notification?

A1: The § 355(t) notification is the primary requirement for most standard authorized generic launches where the product is sold exactly as described in the existing NDA. The notification must be submitted at least 60 days before the AG is marketed. Beyond notification, no separate FDA approval is required unless the AG differs from the brand’s approved specifications in a way that constitutes a manufacturing change requiring a supplement. If the AG will be labeled and sold with a different lot coding, packaging configuration, or any modified excipient, the brand’s regulatory affairs team needs to assess whether those modifications require a Prior Approval Supplement or Changes Being Effected Supplement under 21 C.F.R. § 314.70. For most standard oral solid dosage AG launches – same formulation, same strength, different label – the notification alone suffices, and the brand can begin marketing as soon as the 60-day period expires.

Q2: Can a brand manufacturer license authorized generic rights to more than one generic distributor simultaneously, and would that violate antitrust law?

A2: There is no FDA limit on the number of authorized generic licensees for a single NDA. A brand can theoretically license multiple entities to distribute an authorized generic simultaneously. The antitrust analysis turns on whether the licensing structure, in combination with any market allocation, pricing coordination, or information-sharing provisions between licensees, constitutes a horizontal agreement in restraint of trade. Multiple AG licensees operating independently with no coordination provisions raise minimal antitrust concerns. Multiple AG licensees with pricing floors or market allocation provisions – for example, one licensee covering retail pharmacy and another covering mail order, with agreements preventing cross-channel competition – require more careful antitrust analysis under the rule of reason. Post-Actavis, any AG licensing arrangement connected to a Hatch-Waxman settlement with a potential reverse payment element receives heightened scrutiny regardless of how many licensees are involved.

Q3: How do authorized generic programs interact with co-pay assistance cards and patient assistance programs that brands typically offer?

A3: The interaction is commercially significant and often not well-modeled in initial AG launch business cases. A patient who uses a co-pay assistance card for the brand drug is already paying a low out-of-pocket cost, which means the AG’s lower list price does not necessarily represent a meaningful access improvement for that patient. If the brand migrates those patients to the AG to reduce co-pay card program costs, it exchanges the patient assistance expense for lower per-unit AG revenue, which may or may not be a net financial improvement depending on the co-pay card subsidy level and the AG margin structure. The commercially optimal outcome is for the AG to capture patients who are not on co-pay assistance programs – cash-pay patients, uninsured patients, patients in Medicaid managed care programs that do not accept co-pay cards – while co-pay assistance supports insured patients on commercial plans who remain on the brand. Designing the AG launch and the co-pay assistance program to target genuinely different patient segments requires careful patient flow analysis at the pharmacy claims level.

Q4: What happens to an authorized generic’s market position when independent generic competition eventually enters the market?

A4: The authorized generic’s competitive position changes materially when independent generic competition arrives. Before independent entry, the AG competes primarily against the brand and typically holds a stable price at 20 to 40 percent below brand levels. Once independent generics enter and begin competing against each other, the market price for all generic versions, including the AG, is pulled toward the competitive generic floor, which can be 80 to 90 percent below brand price for highly competitive markets. The authorized generic does not receive the Hatch-Waxman 180-day first-filer exclusivity period, so it provides no legal barrier to independent generic entry. The brand manufacturer’s commercial calculation at that point is whether the AG distribution infrastructure and relationships it built during the uncontested period provide any durable competitive advantage in the fully generic market, or whether the AG economics have become sufficiently thin that withdrawing from active distribution and allowing the licensee to operate independently is the better choice.

Q5: Are there documented cases where an authorized generic launch in an uncontested market demonstrably deterred subsequent Paragraph IV ANDA filings against the same product?

A5: Direct causality is difficult to establish because the counterfactual, what ANDA filings would have occurred absent the AG, is not observable. The empirical literature provides indirect evidence. The FTC’s 2011 study on authorized generics documented that generic manufacturers explicitly modeled AG competition into their first-filer exclusivity economic analyses, and that the expected presence of an AG reduced the calculated net present value of Paragraph IV campaigns. Generic manufacturers interviewed in that study confirmed that AG competition was a material factor in their filing decisions. More recently, academic work by Hollis [16] modeled the deterrence economics and found that for drugs with moderate first-filer exclusivity value, the presence of an authorized generic with realistic pricing parameters was sufficient to push the NPV of Paragraph IV litigation below the cost threshold for filing. For drugs with very high first-filer exclusivity value – drugs with enormous revenue and many years of patent remaining – the deterrence effect was insufficient to prevent filing. The practical implication is that AG deterrence is most effective for drugs with moderate revenue profiles and five to ten year patent horizons, which are exactly the drugs that are economically marginal for Paragraph IV investment.

Sources

[1] 21 U.S.C. § 355(t). (2024). Authorized generic drugs. United States Code.

[2] Berndt, E. R., Mortimer, R., Bhattacharjee, A., & Parece, A. (2007). Authorized generic drugs, price competition, and consumers’ welfare. Health Affairs, 26(3), 790-799. https://doi.org/10.1377/hlthaff.26.3.790

[3] 21 U.S.C. § 355(j)(5)(B)(iv). (2024). First applicant 180-day exclusivity. United States Code.

[4] Federal Trade Commission. (2011). Authorized generics: An interim report. Federal Trade Commission. https://www.ftc.gov/reports/authorized-generics-ftc-interim-report

[5] Inflation Reduction Act of 2022, Pub. L. No. 117-169, 136 Stat. 1818 (2022).

[6] Choudhry, N. K., Avorn, J., Glynn, R. J., Antman, E. M., Schneeweiss, S., Toscano, M., Reifel, L., Fernandes, J., Spettell, C., Lee, J. L., Levin, R., Brennan, T., & Shrank, W. H. (2011). Full coverage for preventive medications after myocardial infarction. New England Journal of Medicine, 365(22), 2088-2097. https://doi.org/10.1056/NEJMsa1107913

[7] FTC v. Actavis, Inc., 570 U.S. 136 (2013).

[8] FDA Reauthorization Act of 2017, Pub. L. No. 115-52, 131 Stat. 1005 (2017).

[9] 21 U.S.C. § 360bb. (2024). Designation of drugs for rare diseases or conditions. United States Code.

[11] Medicines Patent Pool. (2023). Annual report 2022. Medicines Patent Pool. https://medicinespatentpool.org/uploads/2023/06/MPP-Annual-Report-2022.pdf

[12] Berndt, E. R., & Aitken, M. L. (2011). Brand loyalty, generic entry and price competition in pharmaceuticals in the quarter century after the 1984 Waxman-Hatch legislation. International Journal of the Economics of Business, 18(2), 177-201. https://doi.org/10.1080/13571516.2011.584428

[13] Grabowski, H., Long, G., Mortimer, R., & Boyo, A. (2016). Updated trends in US brand-name and generic drug competition. Journal of Medical Economics, 19(9), 836-844. https://doi.org/10.1080/13696998.2016.1176578

[14] 42 U.S.C. § 1396r-8. (2024). Payment for covered outpatient drugs. United States Code.

[15] 42 U.S.C. § 256b. (2024). Limitation on prices of drugs purchased by covered entities. United States Code.