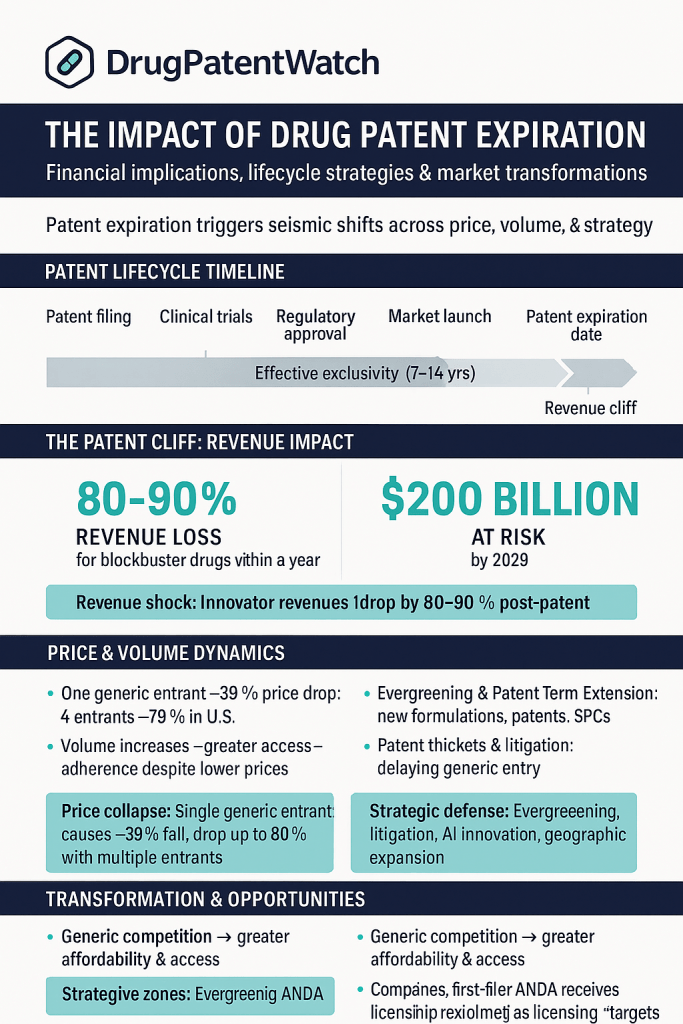

The $400 Billion Ticking Clock: Quantifying the Patent Cliff

Between 2025 and 2030, the global pharmaceutical industry faces a Loss of Exclusivity (LOE) wave that puts an estimated $200 billion to $400 billion in branded drug revenue at direct risk. That range reflects genuine uncertainty about litigation outcomes, biosimilar entry timelines, and IRA price negotiation schedules — not analytical imprecision. The high end of that estimate assumes successful multi-front biosimilar entry and aggressive Paragraph IV (P.IV) challenges against the decade’s biggest small-molecule franchises.

The revenue erosion following generic or biosimilar entry is not gradual. For a small-molecule blockbuster with thin secondary patent protection, the initial year of multi-source generic competition typically produces an 80-90% price and volume decline. For biologics, where the interchangeability barrier and PBM rebate dynamics slow substitution, the erosion is more prolonged — but the trajectory is identical.

The drugs at the center of this cliff are not niche products. Merck’s pembrolizumab (Keytruda), which generated approximately $29.5 billion in 2023 revenue, faces its core U.S. LOE around 2028. Bristol Myers Squibb’s apixaban (Eliquis), producing over $10 billion annually, sees its key U.S. patents expire between 2027 and 2029. Johnson & Johnson’s ustekinumab (Stelara), a $10.8 billion immunology franchise, entered its biosimilar era in 2025. Regeneron’s aflibercept (Eylea), Pfizer’s palbociclib (Ibrance), and Eli Lilly’s dulaglutide (Trulicity) follow in rapid succession.

The 2025-2030 Blockbuster LOE Table

Drug (INN)

Brand

Company

Indication

~2023/24 Revenue

U.S. LOE Window

Pembrolizumab

Keytruda

Merck

Oncology

~$29.5B

~2028

Apixaban

Eliquis

BMS/Pfizer

Anticoagulant

>$10B

2027-2029

Nivolumab

Opdivo

BMS

Oncology

~$9B

~2028

Ustekinumab

Stelara

J&J

Immunology

~$10.8B

2025

Aflibercept

Eylea

Regeneron/Bayer

Ophthalmology

~$5.9B (U.S.)

2025-2026

Palbociclib

Ibrance

Pfizer

Oncology

~$4.7B

~2027

Rivaroxaban

Xarelto

Bayer/J&J

Anticoagulant

~$4.5B (Bayer share)

~2026

Dulaglutide

Trulicity

Eli Lilly

Diabetes/GLP-1

~$7.1B

~2027

Ocrelizumab

Ocrevus

Roche

Multiple Sclerosis

~$7.1B

2028-2029

Denosumab

Prolia/Xgeva

Amgen

Osteo/Oncology

~$6.5B (combined)

2025-2026

Revenue figures and LOE dates are approximations based on public reporting, SEC filings, and patent litigation settlements. Effective LOE dates are subject to change based on litigation outcomes, settlement agreements, and regulatory decisions.

For the strategist or investor, these dates do not simply mark the end of a product cycle. They mark the beginning of a commercial war whose outcome depends entirely on preparation, data quality, and the sophistication of the playbook executed on both sides.

Part 1: The Anatomy of Exclusivity — What ‘Loss of Exclusivity’ Actually Means

Key Takeaways: Part 1

‘Exclusivity’ is not a single wall. It is a multi-layered fortress built from composition-of-matter (CoM) patents, secondary patent thickets, FDA regulatory exclusivities, and, for biologics, the interchangeability standard under the BPCIA.

The ‘effective patent life’ for most drugs is 7-12 years, not the nominal 20-year USPTO term, because patents are filed early in discovery while the FDA review clock burns through them.

The Orange Book (small molecules) and Purple Book (biologics) are structurally different databases that create asymmetric information advantages, heavily favoring innovators in the biologics space.

Regulatory exclusivities (New Chemical Entity exclusivity, Orphan Drug Exclusivity, pediatric exclusivity) are wholly separate from patents and are often the last line of defense when a CoM patent is invalidated.

The 20-Year Myth: Understanding Effective Patent Life

The standard description of a pharmaceutical patent as a ’20-year monopoly’ is misleading enough to be dangerous in a strategic planning context. A U.S. patent grants a 20-year term measured from its filing date at the USPTO — not from FDA approval, and not from first commercial sale. By the time a drug reaches patients, a substantial portion of that term has already expired.

A pharmaceutical company files its core composition-of-matter (CoM) patent early in the drug development process, often at the preclinical stage before the molecule has ever been tested in a human being. From that filing date forward, the drug must survive preclinical toxicology studies, three phases of clinical trials that collectively take six to eight years on average, and an FDA review process that adds another twelve to eighteen months under standard NDA procedures (or six months under Priority Review). By the time the drug launches commercially, the average small-molecule drug has consumed between eight and twelve years of its patent term.

The result: the ‘effective patent life,’ meaning the period of commercial exclusivity actually available to the innovator, averages seven to twelve years. That compressed window must generate enough cash to cover the sunk cost of development (industry estimates range from $1.3 billion to over $2.6 billion per approved drug when capital costs and failure rates are included) and fund the next pipeline cycle. This financial pressure is the structural engine behind every lifecycle management strategy described in this report.

The Defense-in-Depth Architecture of Pharmaceutical Exclusivity

No serious blockbuster relies on a single patent. The standard exclusivity architecture is a multi-layered construct that IP teams build deliberately and continuously from early development through post-approval lifecycle management.

Layer 1: The Composition of Matter Patent

The CoM patent claims the active pharmaceutical ingredient (API) itself — the specific molecular structure, its salts, hydrates, and prodrugs. This is the strongest form of patent protection available in pharmaceuticals. It covers the molecule regardless of how it is used, what disease it treats, or how it is formulated. A valid CoM patent blocks all generic or biosimilar entry for its remaining term, regardless of what a challenger does with formulation or manufacturing.

The CoM patent expiration date is the date every competitor’s planning team has circled in red for years before it arrives. For small molecules, a generic manufacturer with an approved ANDA files a P.IV certification against the CoM and, if successful, enters the market immediately upon patent expiration (or earlier, via at-risk launch). For biologics, the reference product exclusivity under the BPCIA provides a 12-year market protection period that may extend beyond the CoM patent term.

IP Valuation Insight: CoM Patents as Core Balance Sheet Assets

For institutional investors modeling a pharma company’s revenue trajectory, the CoM patent expiration date is not simply a legal data point — it is the primary driver of discounted cash flow (DCF) model assumptions for that asset. A drug with seven years of CoM protection remaining trades at a structurally different terminal value than one with twelve. Investment banks running sum-of-the-parts (SOTP) valuations for Big Pharma use patent expiration calendars as the primary input to their ‘at risk’ revenue calculations and LOE haircuts. Analysts at firms like Bernstein and SVB Leerink apply portfolio-level LOE risk scores to large-cap pharma equities precisely because the aggregate COm exposure across a company’s commercial portfolio is what determines whether a stock is a value trap or a compounder.

Layer 2: The Secondary Patent Estate and the ‘Thicket’

Once a CoM patent is filed, the IP team’s work shifts to building a secondary patent estate designed to cover every commercially valuable attribute of the drug beyond the molecule itself. These patents are filed on a rolling basis throughout development and post-approval, and they collectively form what competition lawyers call a ‘patent thicket.’

Secondary patents fall into four broad categories. Formulation patents cover the delivery system, including extended-release (XR) coatings, depot injections, transdermal patches, fixed-dose combinations, specific particle size distributions, and novel excipient systems. Method-of-use patents cover specific therapeutic indications (claiming a new disease the drug treats) or dosing regimens that the innovator has documented in clinical trials. Process patents (methods of manufacture) cover novel or non-obvious synthetic routes, purification methods, crystallization processes, or bioreactor conditions for biologics. Polymorph and solvate patents cover specific crystalline or amorphous forms of the API that may offer stability, solubility, or bioavailability advantages.

Layer 3: FDA Regulatory Exclusivities

Regulatory exclusivities are market protections granted by the FDA upon drug approval. They are independent of the USPTO patent system and run concurrently with patents. The critical distinction: if a CoM patent is invalidated in court litigation, a valid regulatory exclusivity can still block generic entry. This backstop function makes regulatory exclusivities strategically essential in P.IV litigation planning.

The primary exclusivity types in the U.S. system are: New Chemical Entity (NCE) exclusivity (five years for a small-molecule drug containing an active ingredient never previously approved by the FDA); Orphan Drug Exclusivity (seven years of market exclusivity for drugs treating diseases affecting fewer than 200,000 U.S. patients); new clinical study exclusivity (three years for a new indication or formulation requiring new clinical trials to support approval); and pediatric exclusivity (a six-month extension added to all existing patents and exclusivities as a reward for conducting FDA-requested pediatric studies).

Pediatric exclusivity deserves specific attention because its economic value is wildly asymmetric to its scientific cost. Conducting pediatric trials on a blockbuster drug costs tens of millions of dollars. But a six-month extension on a drug generating $10 billion per year — where every month of exclusivity is worth roughly $833 million — makes the pediatric study investment return several billion dollars on a marginal cost basis. This is why the pediatric exclusivity program has been repeatedly criticized as a windfall for innovators, and why it was a deliberate policy choice by Congress to incentivize pediatric drug research.

The Orange Book vs. The Purple Book: An Asymmetric Information Problem

The FDA maintains two public patent databases that function as the official maps of the exclusivity battlefield. Their structural differences are not incidental — they create fundamentally different competitive dynamics for small-molecule generics versus biosimilar challengers.

The Orange Book

The FDA’s ‘Approved Drug Products with Therapeutic Equivalence Evaluations’ was created by the Hatch-Waxman Act of 1984. It requires innovator companies to proactively list, at the time of NDA approval, every patent they claim covers the approved drug or its approved method of use. The Orange Book is comprehensive, regularly updated, and publicly searchable. For a generic manufacturer, it is a complete roadmap of every patent that must be certified against (via Paragraph I, II, III, or IV certification) before an ANDA can be filed. This transparency was the deliberate design of the Hatch-Waxman framework: it creates a clear target and enables the generic company to plan its legal strategy before investing in product development.

The Purple Book

The ‘Lists of Licensed Biological Products with Reference Product Exclusivity and Biosimilarity or Interchangeability Evaluations’ was created by the BPCIA in 2010 and has undergone major statutory revision since then. Its function is analogous to the Orange Book, but its structure creates an information environment that systematically favors the innovator.

For years post-BPCIA enactment, the Purple Book did not list patents at all. Subsequent legislation (the Biological Product Patent Transparency Act) added patent listing requirements, but with crippling limitations relative to the Orange Book. Innovator companies are not required to publish their patent lists proactively at the time of biologics license application (BLA) approval. Instead, patent information is often revealed through the ‘Patent Dance’ information exchange process, meaning a biosimilar developer may have already invested several years and hundreds of millions of dollars in development before it sees the full patent landscape it will have to litigate.

Research published in peer-reviewed literature has documented that the Purple Book’s patent information is frequently incomplete, inconsistently updated, and not subject to the same statutory disclosure obligations that govern the Orange Book. This structural asymmetry is not an accident. It reflects the legislative compromise embedded in the BPCIA, which gave innovator biologics companies structural information advantages as a counterweight to the massive development cost of reference products. The practical effect is that biosimilar developers operate with substantially less pre-investment visibility into patent risk than their generic drug counterparts — a key reason why the biosimilar market has matured more slowly than the generic drug market despite being launched with similar policy intent.

Part 2: The Small-Molecule Battlefield — Hatch-Waxman’s Rules of War

Key Takeaways: Part 2

The Drug Price Competition and Patent Term Restoration Act of 1984 (Hatch-Waxman Act) created a deliberate, bilateral system of incentives designed to produce generic competition while protecting brand innovation, and it has worked: generics now account for over 90% of U.S. prescriptions while representing only about 12% of drug spending.

The 180-day first-to-file exclusivity is the ‘golden ticket’ that fuels the entire generic litigation ecosystem. Generic companies can generate 60-80% of a product’s total profit during this six-month window — the reason they litigate aggressively and sometimes launch at risk.

The 30-month stay is the central economic lever of the Hatch-Waxman system. It gives the brand two-and-a-half years of automatic protection after filing an infringement suit, essentially converting the innovator’s decision to sue into a free near-term market extension.

At-risk launches — where a generic enters the market before patent litigation concludes — are high-stakes financial decisions modeled on NPV and scenario probability, not legal conviction alone. The Protonix/pantoprazole case ($2.15 billion in damages) is the permanent benchmark for what a wrong call looks like.

The Hatch-Waxman Bargain: A Bilateral Incentive Architecture

The Drug Price Competition and Patent Term Restoration Act of 1984 solved two simultaneous problems with a single piece of legislation. The first problem: before 1984, generic companies had to independently demonstrate a drug’s safety and efficacy through full clinical trials to get FDA approval, making generic competition economically impossible for most drugs. The second problem: innovator companies were losing years of patent-protected revenue while drugs sat in FDA review, and had no statutory mechanism to recover that lost time.

The Act’s solution was a formal bilateral bargain. Innovators received, for the first time, the right to petition for patent term extensions of up to five years to recover FDA review time (capped at 14 years of post-approval patent term), plus new regulatory exclusivity periods (the 5-year NCE exclusivity and the 3-year new clinical study exclusivity) that block generic entry independent of the patent system. Challengers received the Abbreviated New Drug Application (ANDA) pathway, which allows a generic to demonstrate bioequivalence to the reference listed drug without repeating the innovator’s clinical trials, plus a research ‘safe harbor’ allowing them to conduct development activities during the patent term without infringement liability, and the 180-day exclusivity reward for challenging brand patents via P.IV certification.

The economic results of this bargain are measurable. Before Hatch-Waxman, generics accounted for approximately 19% of U.S. prescriptions. By 2024, that figure exceeded 90%. The 2025 U.S. Generic and Biosimilar Medicines Savings Report, published by the Association for Accessible Medicines, found that generics and biosimilars generated $467 billion in system-wide savings in 2024 alone and $3.4 trillion over the preceding decade. Those numbers represent the successful operation of a policy framework designed to balance innovation rewards with competitive access — and they explain why Hatch-Waxman remains the most consequential piece of pharmaceutical market legislation ever enacted.

The ANDA Pathway: What Bioequivalence Actually Requires

The ANDA pathway allows generic applicants to rely on the FDA’s prior finding of safety and efficacy for the reference listed drug (RLD). The generic must demonstrate that its product is pharmaceutically equivalent (same active ingredient, dosage form, route of administration, and strength) and bioequivalent (no clinically significant difference in rate and extent of absorption) to the RLD.

Bioequivalence is typically established through a crossover pharmacokinetic (PK) study in healthy volunteers, comparing area under the plasma concentration-time curve (AUC) and maximum concentration (Cmax) between the generic and the brand. The FDA’s standard bioequivalence criterion requires that the 90% confidence interval for the ratio of geometric means fall within 80-125% for both AUC and Cmax. This is a well-established scientific threshold, but it is not trivial to achieve for complex dosage forms, narrow therapeutic index drugs, or locally acting products. For complex generics — including products with modified-release mechanisms, topical delivery systems, or inhalation devices — demonstrating bioequivalence requires additional in vitro testing and sometimes in vivo pharmacodynamic studies, adding development time and cost.

The FDA’s Center for Drug Evaluation and Research (CDER) publishes product-specific guidance documents for complex generics that specify the bioequivalence approach for individual reference products. These guidance documents have been used by branded companies to argue that their products cannot be bioequivalently replicated by a generic, effectively creating additional regulatory barriers. The FDA has pushed back on this strategy in several high-profile cases, but the tactic remains part of the innovator defensive toolkit.

The 180-Day Exclusivity: Economic Structure and Competitive Dynamics

The 180-day first-to-file exclusivity is awarded to the ANDA applicant that is first to file a P.IV certification against a patent listed in the Orange Book for a given reference product. The exclusivity is triggered upon the first commercial marketing of the generic product and runs for 180 calendar days, during which the FDA cannot approve any other ANDA for the same drug that also contains a P.IV certification against the same patent.

The economic value of this exclusivity window is not simply 180 days of generic revenue. It is the value of 180 days of market access before multi-source competition drives prices to commodity levels. Academic and industry research consistently shows that first-to-file generics can generate 60-80% of a product’s total generic market profit during the exclusivity period, because they can price at 10-20% below the brand rather than the 70-90% discounts that become necessary once five or more generics enter the market simultaneously.

This front-loaded profit structure is the fundamental driver of Paragraph IV litigation economics. Generic companies are willing to invest tens of millions of dollars in patent litigation because they are competing for a time-limited, high-margin window that can be worth hundreds of millions — or even billions — for the right product. It is also why multi-filer situations are among the most analytically complex in the generic industry: when multiple applicants file P.IV certifications against the same patent on the same day, the 180-day exclusivity is shared among all same-day filers, substantially diluting its value.

The Paragraph IV Gauntlet: Notice, Lawsuit, and the 30-Month Stay

The P.IV certification is the formal legal mechanism that triggers both the 180-day exclusivity race and the Hatch-Waxman litigation system. When a generic company files an ANDA with a P.IV certification, it must promptly send a ‘Notice Letter’ to the NDA holder and every patent owner listed in the Orange Book. This notice must include a detailed, paragraph-by-paragraph statement of the factual and legal basis for the applicant’s position that the challenged patent is invalid, unenforceable, or will not be infringed by the proposed generic product.

The Notice Letter is a highly strategic document. It defines the scope of the litigation by specifying which invalidity and non-infringement arguments the generic intends to pursue, and it starts the 45-day clock during which the brand may file a patent infringement suit. If the brand sues within that 45-day window, the FDA’s approval of the generic ANDA is automatically stayed for 30 months, or until the court issues a final decision on patent validity and infringement, whichever comes first.

The 30-month stay is the central economic lever of the entire Hatch-Waxman system. It gives the innovator two-and-a-half years of automatic generic-free market operation from the date of suit filing — without any requirement to prove likelihood of success on the merits. The brand does not need to win a preliminary injunction; it merely needs to file the lawsuit. This structure creates an overwhelming incentive for the brand to sue: the cost of filing a patent infringement action is trivial compared to 30 months of uncontested blockbuster revenue.

The generic company knows this and accepts it. Filing the P.IV and being sued is not a setback for a first-to-file applicant — it is the expected pathway. The 30-month stay locks in the generic’s first-to-file priority status and sets up the eventual litigation resolution (whether settlement, trial win, or loss). The system, by design, funnels both parties into federal court for every commercially significant drug patent challenge.

For equity analysts covering branded pharmaceutical companies or generic drug manufacturers, P.IV litigation timelines are directly material to earnings models. Every P.IV challenge against a branded company’s product represents a potential LOE event that will be disclosed in SEC filings (Form 10-K, Form 10-Q) under ‘Legal Proceedings.’ Analysts should track P.IV filing dates, 30-month stay expiration dates, and expected trial schedules against their revenue models. A branded company that receives a P.IV challenge against a $5 billion product with a trial scheduled for month 28 of the stay has a 90-day window of genuine near-term LOE risk that may not be fully reflected in consensus estimates. Conversely, a generic filer with a strong P.IV claim against a weak secondary patent is a potential 180-day exclusivity winner worth modeling explicitly.

Case Study: Teva and Sun’s At-Risk Pantoprazole Launch — A $2.15 Billion Lesson

In 2007, generic manufacturers Teva and Sun Pharmaceutical Industries were so confident in their invalidity arguments against Wyeth’s pantoprazole (Protonix) patents that they launched their generic versions at risk — meaning commercial sales began while the underlying patent infringement case was still pending in federal court. Their legal theory was that the formulation and method-of-use patents Wyeth had listed in the Orange Book were invalid and would not withstand trial.

Their confidence was incorrect. In 2010, a jury found against their invalidity and non-infringement arguments. The damages award was calculated on the brand’s total lost profits during the at-risk period — a methodology that produces catastrophic liability when applied to a blockbuster. The final settlement required Teva and Sun to pay approximately $2.15 billion in combined damages, making the Protonix case one of the largest patent damages awards in pharmaceutical history.

The Protonix case defines the at-risk launch decision framework. An at-risk launch is not a legal decision; it is a scenario-weighted NPV calculation. The generic company must estimate the probability-weighted value of early market access against the probability-weighted cost of a damages award. Inputs include: the estimated probability of winning on each invalidity and non-infringement argument, the brand’s annual revenue (which determines the potential damages base), the generic’s own launch revenue projections, the expected timeline to final judgment, and the company’s balance sheet capacity to absorb a worst-case damages award. A company that cannot survive a maximum damages scenario should not launch at risk, regardless of its confidence in the legal case. A company with strong balance sheet capacity and a genuinely high probability of success may rationally accept the risk.

Part 3: The Biologic Frontier — BPCIA, the Patent Dance, and Biosimilar Interchangeability

Key Takeaways: Part 3

Biologics are fundamentally different from small-molecule drugs in their manufacturing complexity. Because the ‘process is the product’ for biologics, an exact copy is scientifically impossible — which is why the regulatory standard is ‘biosimilarity’ (highly similar, no clinically meaningful differences), not bioequivalence.

The BPCIA’s 351(k) pathway created two approval tiers: the ‘biosimilar’ standard and the higher ‘interchangeable’ standard. Only interchangeable biosimilars can be automatically substituted at the pharmacy without prescriber intervention, making biosimilar interchangeability the single most commercially important designation in the BPCIA framework.

The ‘Patent Dance’ — the BPCIA’s multi-step information exchange process — is optional per the Supreme Court’s 2017 ruling in Sandoz v. Amgen, but the consequences of opting out shift the patent dispute into a different procedural posture that biosimilar developers must model carefully.

Biosimilar adoption in the U.S. has been structurally slowed by three converging factors: patent thickets, the interchangeability barrier, and PBM formulary economics that sometimes favor high-list/high-rebate branded biologics over low-cost biosimilars.

Why ‘Generic Biologic’ Is a Scientific Contradiction

The conceptual gap between a small-molecule generic and a biosimilar is larger than most non-technical stakeholders appreciate, and the strategic implications of that gap are enormous.

A small-molecule drug like atorvastatin (Lipitor) is a defined chemical compound with a known molecular structure that can be synthesized to identical specifications by any competent chemist with the right equipment. Two tablets containing 40mg of atorvastatin — one from Pfizer, one from a generic manufacturer — contain the same molecule in the same amount. Bioequivalence testing confirms that the body handles them identically. The product is fully replicable.

A biologic like adalimumab (Humira) is a fully human monoclonal antibody (mAb) consisting of approximately 1,330 amino acids arranged in a precise three-dimensional structure, with complex post-translational modifications including glycosylation patterns that are exquisitely sensitive to the specific cell line used for production, the growth media composition, temperature cycling, pH control, oxygen levels, and dozens of other manufacturing variables. The glycosylation pattern — the specific arrangement of sugar chains attached to the protein — directly affects the drug’s efficacy, immunogenicity, and safety profile, and it varies batch-to-batch within the same manufacturer’s own process.

Because the manufacturing process determines the product’s characteristics, two manufacturers using even the most similar processes will produce proteins that are ‘highly similar’ but never identical. ‘Highly similar’ is not a marketing claim — it is the regulatory standard that the BPCIA explicitly codified. And ‘highly similar’ carries a specific burden of proof: the biosimilar developer must demonstrate no clinically meaningful differences in safety, purity, and potency relative to the reference product. That demonstration typically requires a substantial analytical comparability package, often including pharmacokinetic and pharmacodynamic bridging studies, and in some cases, comparative efficacy or safety clinical trials.

The cost differential from this complexity is material. Developing a small-molecule generic ANDA typically costs $1-5 million. Developing a biosimilar 351(k) application costs $150-300 million or more. This is the first structural reason why the biosimilar market has developed more slowly and concentrated among better-capitalized players than the generic market.

The BPCIA 351(k) Pathway: Two Tiers, One Critical Commercial Distinction

The BPCIA created the 351(k) abbreviated biologics license application (aBLA) pathway, which allows a biosimilar applicant to rely on the FDA’s prior review of the reference product’s safety, purity, and potency data rather than independently generating that entire dataset. The 351(k) pathway has two distinct approval standards, and the difference between them determines the commercial strategy for the entire product lifecycle.

The ‘Biosimilar’ Standard

A biosimilar approval requires the applicant to demonstrate that its product is ‘highly similar’ to the reference product, with no clinically meaningful differences in terms of safety, purity, and potency. The evidence package typically includes extensive analytical characterization data comparing structure, function, and biological activity; a PK/PD bridging study demonstrating similar behavior in the body; and, depending on the product and residual uncertainty after analytical and PK/PD comparison, one or more comparative clinical trials. The FDA has the authority to waive clinical trial requirements when the totality of evidence from analytical and PK/PD studies is sufficiently robust.

A biosimilar-approved product can be dispensed when a prescriber writes a prescription for the reference product only if the prescriber specifically includes the biosimilar on the prescription or indicates substitution is acceptable. Without automatic substitution authority, the biosimilar company must deploy a commercial team equivalent in scale to a branded drug launch to specifically drive prescribers toward its product — a cost structure that fundamentally undermines the low-price, high-volume generic business model.

The Interchangeability Standard

Biosimilar interchangeability is a higher approval standard that requires the applicant to demonstrate not only biosimilarity but also that patients can be switched between the reference product and the biosimilar — and back again — multiple times without any change in safety or efficacy. This is typically demonstrated through dedicated switching studies. An interchangeable biosimilar can be automatically substituted for the reference product at the pharmacy level, subject to state pharmacy substitution laws, without additional prescriber authorization.

The commercial value of interchangeability is transformative. It enables the same pharmacy-level automatic substitution mechanism that drives generic drug adoption. It eliminates the need for biosimilar-specific prescriber-level marketing for products in therapeutic areas where pharmacy-level dispensing is common. It allows PBMs and payers to mandate substitution on formulary, generating the volume that justifies the low-price, high-volume biosimilar business model.

The first interchangeable biosimilar in U.S. history was Semglee (insulin glargine-yfgn), approved by the FDA in July 2021. Since then, the FDA has approved interchangeable designations for several other products, including Cyltezo (adalimumab-adbm), one of the Humira biosimilars. The pace of interchangeability approvals is accelerating as biosimilar developers invest in the required switching studies — because the commercial payoff justifies the investment.

The Patent Dance: Mechanics and the Sandoz v. Amgen Decision

The ‘Patent Dance’ is the informal name for the BPCIA’s multi-step, timed information exchange process between a biosimilar applicant and the reference product sponsor (RPS). It was designed to create an orderly mechanism for identifying, narrowing, and litigating the specific patents at issue before biosimilar launch, rather than having the RPS dump every patent in its portfolio into a single massive lawsuit the day a biosimilar is approved.

The Dance proceeds in a series of rigid, statutorily defined steps. Within 20 days of FDA acceptance of its 351(k) application, the biosimilar applicant ‘shall’ provide the RPS with a copy of its complete application and detailed manufacturing information — including the cell line, expression system, purification process, formulation, and quality control specifications. The RPS then has 60 days to provide a list of patents it reasonably believes could be infringed by the commercial manufacture, use, importation, sale, or offer for sale of the biosimilar product. The applicant must respond within 60 days with detailed patent-by-patent positions: for each patent on the RPS list, the applicant must state whether it agrees to a license or provide a detailed claim chart explaining its invalidity and non-infringement arguments. The RPS then has a further period to respond, and the parties negotiate to identify a subset of patents for ‘first wave’ litigation. A ‘second wave’ of patents not included in the first litigation phase can be asserted later, at or around the time of commercial launch.

The Supreme Court’s 2017 ruling in Sandoz Inc. v. Amgen Inc. fundamentally changed the strategic calculus of Patent Dance participation. The Court held that the Dance’s information exchange steps are optional — a biosimilar applicant may refuse to provide its application and manufacturing information to the RPS. If it does, the RPS loses access to the structured, negotiated process of narrowing the patent dispute, and must instead immediately sue on any patent it believes may be infringed, based on whatever public information is available. Critically, the Court also held that the BPCIA’s 180-day pre-commercial-marketing notice requirement is mandatory and can be provided either before or after FDA approval — meaning a biosimilar developer can give notice at-risk and launch immediately upon BLA licensure.

The strategic implications of Sandoz v. Amgen are substantial. Biosimilar developers now choose between two materially different postures: participate in the Dance and engage in the structured, discovery-rich information exchange (which gives the RPS visibility into the biosimilar’s manufacturing process) or opt out of the Dance, deny the RPS that manufacturing transparency, and accept the broader but less structured initial patent litigation that follows. Neither choice is categorically superior — the optimal posture depends on the specific patent landscape, the biosimilar’s manufacturing process, and the developer’s litigation budget and risk tolerance.

IP Valuation Insight: Keytruda’s BPCIA Exposure

Merck’s pembrolizumab (Keytruda) is the most commercially consequential biologic facing LOE in the 2025-2030 window. With $29.5 billion in 2023 revenue, Keytruda is not merely a product — it is effectively the financial engine of the entire company. Merck has built a patent estate around pembrolizumab that includes composition-of-matter patents on the antibody structure, method-of-use patents covering its approved indications (pembrolizumab has over 40 FDA-approved indications and indication-specific dosing regimens), and formulation patents on its IV formulation and concentration. Additionally, Merck holds device patents on its administration systems.

The reference product exclusivity period under the BPCIA means no biosimilar can rely on the FDA’s pembrolizumab safety data until 12 years after first approval — which for pembrolizumab (approved September 2014) is September 2026. The earliest biosimilar applicants filed 351(k) applications well in advance of that date (since development takes several years), and the market should expect first biosimilar approvals around 2027-2028, with commercial launch timelines dependent on Patent Dance litigation resolution or settlement.

Merck’s LOE strategy for Keytruda is clearly a multi-front operation. The company has invested heavily in subcutaneous (SC) pembrolizumab, a next-generation formulation developed with Halozyme’s ENHANZE drug delivery technology (using recombinant human hyaluronidase PH20). An approved SC formulation — with its own patent protection extending beyond the IV formulation patents — combined with a clinical program demonstrating non-inferiority to IV pembrolizumab, would execute a classic ‘product hop’ that positions Merck to transition the market to a formulation that biosimilar IV competitors cannot automatically substitute for. The SC formulation’s patent coverage and the manufacturing complexity of reproducing Halozyme’s ENHANZE platform represent a structural competitive moat that biosimilar developers will need to address separately.

U.S. vs. E.U. Biosimilar Adoption: A Tale of Two Payer Systems

The contrast between European and U.S. biosimilar adoption rates is one of the most instructive case studies in how payer system structure determines competitive market dynamics.

In major European markets — Germany, France, the U.K., Scandinavia — biosimilar adoption for reference products like adalimumab, infliximab, and etanercept has been rapid and deep, with some reference products losing 80-90% of their market share within 12-18 months of biosimilar entry. European national health systems are single-payer purchasers with direct procurement authority, tendering mechanisms, and explicit cost-containment mandates. When a biosimilar enters at a 30-50% discount to the reference product, the national payer has both the authority and the economic incentive to mandate or strongly incentivize its use. The result is a functioning, competitive market that generates the cost savings biosimilar policy was designed to produce.

The U.S. market structure generates more complex dynamics. Several factors slow adoption specifically in the U.S. context.

The PBM rebate system creates a perverse incentive for high-list branded products. A reference biologic with a $70,000 annual list price may pay PBMs a 40-50% rebate, producing a net realized price of $35,000-42,000. A biosimilar entering at a $50,000 list price with a 20% rebate has a net realized price of $40,000 — offering the PBM a smaller absolute rebate dollar amount, even though the list price is lower. Some PBMs have historically preferred to keep the high-list branded product on formulary because the rebate revenue is larger, even when the net cost to the plan is similar. The IRA’s drug price negotiation provisions and the ongoing Congressional and FTC scrutiny of PBM practices are beginning to change this dynamic, but the structural misalignment persists.

In physician-administered settings — oncology clinics, infusion centers, rheumatology practices — biosimilar adoption has been faster because physicians and oncology group practices make purchasing decisions based on acquisition cost (which directly affects their economic margin under the buy-and-bill model) rather than PBM formulary dynamics. A 340B-eligible hospital or outpatient oncology clinic has a direct financial incentive to use the lowest-acquisition-cost biosimilar available. This is why biosimilar filgrastim, bevacizumab, and trastuzumab penetrated their U.S. markets more rapidly than biosimilar adalimumab, where pharmacy-dispensed, self-administered use dominates.

Part 4: The Innovator Playbook — Six Defensive Lifecycle Strategies, Fully Decoded

Key Takeaways: Part 4

Pharmaceutical lifecycle management (LCM) is a multi-front war executed simultaneously on legal, regulatory, formulation science, and commercial dimensions. No single strategy is sufficient for a major blockbuster; successful defense requires combinations.

AbbVie’s Humira patent thicket — 250+ patents, 90% filed after market launch, delivering seven additional years of U.S. exclusivity worth over $100 billion — is the canonical example of evergreening executed at maximum scale. The strategy’s legal success does not make it less controversial from a health policy standpoint.

The authorized generic (AG) strategy (e.g., Pfizer’s Lipitor defense) is designed to ‘cannibalize and conquer’: by launching an AG the same day the first-to-file generic enters, the innovator captures approximately 70% of the generic market’s revenue and systematically devalues the 180-day exclusivity prize that generic companies have been racing to win.

Product hopping — transitioning the market to a new, patent-protected formulation before the generic for the old version launches — is most effective when combined with a clinical differentiation narrative. AbbVie’s citrate-free, high-concentration Humira formulation is the definitive contemporary example.

Citizen Petitions, when filed close to a generic’s expected approval date, generate delay that can be worth hundreds of millions of dollars, even when the FDA ultimately denies the petition. This has attracted FTC scrutiny and Congressional attention.

‘Pay-for-delay’ reverse payment settlements have evolved from direct cash transfers (now presumptively illegal after FTC v. Actavis, 2013) into ‘complex side business deals’ that accomplish the same market division through less traceable arrangements.

Strategy 1: Building and Litigating the Patent Thicket

A patent thicket is a deliberate, multi-patent defensive perimeter around a commercial drug franchise. The goal is not necessarily to win every individual patent case — it is to make the aggregate cost, time, and legal uncertainty of challenging the thicket high enough that rational challengers either delay their entry or settle for a licensed entry date rather than litigating to verdict.

The operational mechanics of thicket construction involve three parallel activities that must be executed continuously from pre-launch through post-launch. The IP team files patent applications covering every commercially valuable product attribute as data is generated: formulation work during Phase 2, manufacturing process optimizations during scale-up, method-of-use patents as each new indication is clinically developed, and polymorph and solvate patents following crystallization studies. Separately, the patent prosecution team manages continuation and continuation-in-part applications to ensure that the latest filings maintain live patent families connected to early priority dates, preserving the ability to capture broad coverage under older priority claims. The litigation team then uses the Orange Book listing process strategically, listing patents that will force challengers into P.IV certification and trigger the 30-month stay on ANDA approval.

The Humira Thicket: A Quantitative Anatomy

AbbVie’s adalimumab (Humira) patent thicket is the most studied example of this strategy in history, and the quantitative detail of its construction illustrates precisely how the strategy operates.

Humira’s core composition-of-matter patent, covering the adalimumab antibody, expired in the United States in December 2016. By standard analysis, biosimilars should have entered the U.S. market in 2017. They did not. AbbVie had built a patent estate of over 250 granted U.S. patents around Humira, and the most telling characteristic of that estate is its filing chronology: research by academic IP analysts found that approximately 90% of the patent filings for Humira were made after the drug was already on the market. These were not discovery-stage inventions — they were late-stage evergreening filings covering formulation refinements, new concentrations, device innovations, manufacturing process variations, and method-of-use claims across Humira’s expanding indication list (which grew to include rheumatoid arthritis, psoriatic arthritis, ankylosing spondylitis, Crohn’s disease, ulcerative colitis, plaque psoriasis, and pediatric extensions of several of those indications).

When biosimilar developers including Amgen, Sandoz, Boehringer Ingelheim, Mylan, Samsung Bioepis, and Fresenius Kabi attempted to enter the U.S. market with their FDA-approved products, they each faced a thicket of over 130 active patents. The cost of litigating all of them simultaneously was prohibitive, and the probability-weighted outcome analysis did not justify the risk. One by one, the biosimilar manufacturers settled with AbbVie, agreeing to licensed entry dates beginning in 2023 — seven years after the CoM patent expired, and seven years of peak Humira revenue that AbbVie retained without competition. At Humira’s peak revenue of $21.2 billion in 2022, seven additional years of U.S. exclusivity represents a rough order of magnitude of $100 billion or more in cumulative, competition-free sales.

IP Valuation Insight: Humira’s Patent Estate as a Realized Balance Sheet Asset

From an IP valuation standpoint, AbbVie’s Humira patent thicket generated realized value that is quantifiable and can be modeled prospectively for similar assets. The seven-year exclusivity extension from a patent thicket that cost, conservatively, several hundred million dollars in prosecution, litigation, and settlement costs generated tens of billions of dollars in incremental revenue. The ROI on that IP investment is extraordinary by any conventional metric. The appropriate lesson for IP valuation teams is that the quantified value of a strategic patent portfolio is not the sum of individual patent values — it is the value of the exclusivity the portfolio collectively defends.

For biosimilar companies planning challenges to future reference biologics, the Humira case establishes the benchmark for pre-entry due diligence: mapping the entire secondary patent estate, identifying the subset most vulnerable to invalidity or non-infringement attack, and modeling the litigation cost and timeline against the expected commercial window under 180-day-equivalent market exclusivity.

Strategy 2: The Authorized Generic — ‘Cannibalize and Conquer’

The authorized generic (AG) strategy converts the innovator’s loss of exclusivity from a pure revenue loss event into a managed market transition where the innovator retains a significant share of the economics from its own generic competition.

An AG is the reference listed drug itself — same molecule, same manufacturing process, same manufacturer — marketed under a different label, typically through a licensing agreement with a generic partner. The key is timing: the brand launches its AG on the same day as the first-to-file generic’s 180-day exclusivity begins. This creates a duopoly where the first-to-file generic, which expected six months of exclusive generic market access, instead finds itself competing against the brand’s own generic product from Day 1.

Case Study: Pfizer’s Lipitor Defense — The Three-Pronged 180-Day War

Pfizer’s response to atorvastatin (Lipitor) losing patent protection on November 30, 2011, is the most analytically complete documented example of a multi-pronged LOE defense strategy. Lipitor had generated peak annual sales of $12.9 billion in 2006 and remained a $9+ billion product through 2011. Ranbaxy Laboratories had secured first-to-file status for atorvastatin via a P.IV certification and was positioned to enjoy 180 days of generic market exclusivity.

Pfizer executed three simultaneous defensive tactics.

First, it launched an AG through Watson Pharmaceuticals (now Allergan/AbbVie) on the same day Ranbaxy’s generic launched. This AG was manufactured by Pfizer to the same specifications as branded Lipitor but sold at a generic price point under Watson’s label. Industry analysts estimated that Pfizer retained approximately 70% of the economics from Watson’s AG sales through the licensing arrangement. The AG immediately destroyed the ‘solo’ component of Ranbaxy’s 180-day exclusivity by creating a two-generic market rather than a one-generic market.

Second, Pfizer launched the ‘Lipitor for You’ direct-to-patient subsidy program, offering branded Lipitor co-pay cards that reduced patient out-of-pocket cost to as little as $4 per month. For patients with commercial insurance, this made branded Lipitor price-competitive with the generic copay at many pharmacy benefit managers. By removing the price incentive for patients to switch, Pfizer maintained a substantial portion of branded prescriptions during the 180-day exclusivity window, when the generic price was still relatively high.

Third, Pfizer leveraged its years of direct-to-consumer advertising investment in the Lipitor brand, including campaign elements featuring cardiologist Robert Jarvik discussing Lipitor’s cardiovascular outcome data, to maintain physician and patient brand preference during the transition period.

The combined effect was that Ranbaxy’s 180-day exclusivity prize was systematically devalued. Rather than a duopoly with the brand at full price and the generic at a 15-20% discount, Ranbaxy found itself in a three-way market against a $4/month brand, a Pfizer-backed AG, and its own product. Pfizer’s LOE year revenue decline was dramatically smaller than the 80-90% expected from a standard generic entry scenario.

Investment Strategy: Modeling AG Launch Probability

For investors modeling LOE scenarios, the probability of an AG launch by the innovator should be explicitly included in revenue bridge models. Brands with large market caps and established generic partner relationships (Pfizer, Teva partnerships; AstraZeneca’s AG history; Boehringer Ingelheim’s branded generics business) have demonstrated willingness to execute AG strategies. The economic signal to watch: an innovator that has publicly discussed ‘managing the LOE’ or ‘maintaining brand value through the transition’ is telegraphing AG consideration. A brand that is silent about its LOE strategy is more likely to simply concede the generic market.

Strategy 3: Product Hopping — Transition the Market Before the Generic Arrives

Product hopping exploits the commercial power of the innovator’s marketing infrastructure to shift prescribing behavior from an about-to-expire product to a new, patent-protected variant, leaving the generic competitor to enter a largely abandoned market segment.

The mechanics of a product hop are straightforward. The innovator develops a next-generation version of its product — an extended-release formulation, a new dosing schedule, a fixed-dose combination with another drug, a new delivery device, or a new concentration — with its own patent protection extending beyond the original product’s CoM expiration. It then runs a coordinated marketing campaign to convert prescriptions from the old version to the new version, typically beginning 18-36 months before the generic enters. By the time the generic of the original formulation launches, the market has moved. The generic is an ‘imperfect substitute’ that cannot be automatically dispensed in place of the new formulation, because pharmacy substitution rules apply only between a generic and its specific reference listed drug.

AbbVie’s Citrate-Free Humira: A Product Hop Executed Under Biosimilar Pressure

AbbVie’s transition of the Humira market to a high-concentration (100mg/mL vs. 50mg/mL), citrate-free formulation in the years before 2023 biosimilar entry is the defining contemporary example of a product hop in the biologic space. The new formulation reduces injection pain by eliminating citrate as a buffer (citrate causes a burning sensation at the injection site) and allows the same dose to be administered in half the injection volume.

Clinically, these attributes represent genuine improvements in patient experience, not merely cosmetic differentiation. AbbVie invested in a substantial patient and prescriber communication program to drive uptake of the high-concentration formulation. The commercial effect: by the time biosimilar competition launched in January 2023, a substantial fraction of Humira patients had already been transitioned to the citrate-free, high-concentration formulation.

The challenge this creates for biosimilar competitors is structural. The biosimilars that had been approved by the FDA were formulated and clinically studied against the original Humira formulation (50mg/mL with citrate). They are not automatically interchangeable with the high-concentration, citrate-free formulation. To compete directly with AbbVie’s new formulation, biosimilar developers needed to develop their own high-concentration, citrate-free versions and submit supplemental applications to the FDA — a process that adds development time, cost, and regulatory delay. Several biosimilar developers have done exactly this, but the product hop gave AbbVie additional months of reduced competitive pressure in the most actively prescribed segment of its market.

Strategy 4: Rx-to-OTC Conversion

The Rx-to-OTC switch strategy seeks to convert a prescription drug to over-the-counter (OTC) status, transforming the competitive landscape from one governed by generic substitution rules to one governed by consumer brand loyalty and retail shelf positioning. If successful, this strategy moves the battleground from the pharmacy benefit (where price competition is fierce and payers can mandate generic substitution) to the consumer health aisle (where brand name commands a price premium and advertising drives purchase decisions).

The strategy works best when the drug has a highly recognizable brand name, an established consumer awareness base from years of prescription-level advertising, and a safety profile that the FDA’s OTC drug advisory committees will accept as supportive of self-administration without physician supervision. The commercial theory is that patients familiar with the brand from its prescription history will continue purchasing the OTC version even when cheaper generic OTC alternatives are available.

The WellPoint Citizen Petition: The Involuntary OTC Switch of Antihistamines

The Rx-to-OTC switch of loratadine (Claritin), cetirizine (Zyrtec), and fexofenadine (Allegra) is a case study in how external stakeholders can use the FDA’s citizen petition process to force the switch against the innovator’s commercial preference.

In 1998, WellPoint Health Networks (now Anthem/Elevance) filed a citizen petition with the FDA requesting that the agency mandate the Rx-to-OTC switch of second-generation antihistamines. WellPoint’s argument was straightforward: these drugs have safety profiles that make self-administration entirely appropriate for the general population, and their prescription-only status was generating hundreds of millions of dollars in unnecessary prescription drug spending that payers were absorbing through formulary coverage. WellPoint estimated that OTC availability would allow patients to purchase these drugs out-of-pocket at competitive retail prices, reducing plan expenditures significantly.

The innovators — Schering-Plough (loratadine), Pfizer (cetirizine), and then-Aventis (fexofenadine) — aggressively opposed the petition. Their resistance was commercially rational: prescription sales of these drugs were more profitable than OTC sales would be, because prescription prices were higher and insurance coverage insulated patients from direct price sensitivity. The FDA’s advisory committee ultimately agreed with WellPoint that the safety evidence supported OTC availability. Switches proceeded. The Claritin, Zyrtec, and Allegra brands transitioned to OTC status in the early 2000s.

The outcome was nuanced. The innovators lost their prescription monopoly. But the strength of their brand names allowed them to dominate the OTC antihistamine market even in the face of cheaper generic OTC competition — because consumers, primed by years of prescription-level advertising, continued purchasing the branded OTC product at premium prices. The brands survived the patent cliff not by preventing competition, but by converting their prescription brand equity into consumer brand loyalty.

Strategy 5: Pay-for-Delay Settlements and Evolved Reverse Payment Arrangements

Reverse payment settlements — in which a brand-name innovator pays a generic challenger to drop its P.IV patent challenge and delay market entry — were, until the Supreme Court’s 2013 decision in FTC v. Actavis, a standard (if controversial) component of pharmaceutical patent settlement practice. The core logic was commercial: a brand company willing to pay a generic company $200 million to settle a P.IV case was implicitly acknowledging that the patent was worth less than the settlement amount, and that the generic’s claim had some merit. But from the brand’s perspective, any payment that secured delay worth billions in continued monopoly revenue was rational.

The FTC viewed these agreements as per se anticompetitive market division and litigated several high-profile cases. The Supreme Court’s Actavis decision established that reverse payment settlements are subject to antitrust rule-of-reason analysis, making them risky enough that straightforward cash payments from brand to generic have largely disappeared from settlement practice.

What has replaced them is more complex. Modern ‘evolved’ reverse payment settlements involve the innovator providing value to the generic challenger through indirect means: supply agreements, co-promotion arrangements, licensing deals for other products, or royalty-free licenses on unrelated patents. These deals accomplish the same market division objective — the generic agrees to a delayed entry date in exchange for economic value from the innovator — but the non-cash structure makes the antitrust analysis more complex and the FTC’s enforcement burden heavier. The FTC continues to challenge these agreements, and several pending cases will further define the boundaries of permissible settlement terms.

Case Study: Novartis Gleevec (Imatinib) — The Anatomy of a Modern Settlement

Novartis’s imatinib mesylate (Gleevec) was one of oncology’s most transformative drugs, generating over $4.6 billion in annual revenue at peak. The primary U.S. patent was set to expire in July 2015, and Sun Pharmaceutical Industries had secured first-to-file status through a P.IV certification.

Novartis and Sun settled the P.IV litigation before trial. The settlement terms provided that Sun would delay its generic launch for an additional seven months beyond the patent expiration date — until February 2016 — in exchange for terms that the parties did not fully disclose. The seven-month delay was estimated by analysts to be worth approximately a 6% boost to Novartis’s 2015 earnings per share, providing a material, quantified cash value to the delay.

When Sun did launch its generic imatinib in February 2016 with its 180-day exclusivity, analyst observers noted something unusual: the generic launch price was not dramatically lower than branded Gleevec’s net price. This pricing behavior is consistent with a settlement that, in substance, created a managed duopoly during the 180-day window — where both Novartis and Sun captured elevated returns relative to a fully competitive generic market — rather than a genuinely competitive LOE event.

Strategy 6: Citizens Petitions as Regulatory Delay Instruments

The FDA’s citizen petition process, codified in 21 CFR 10.30, allows any person — including corporations and trade associations — to petition the FDA to issue, amend, or revoke a regulation, or to take other action. In the context of drug patent litigation, citizen petitions filed by brand-name innovators shortly before a competitor’s ANDA or 351(k) approval has become a documented tactic for generating regulatory delay.

The mechanics are straightforward. An innovator files a CP raising scientific or regulatory concerns about a competitor’s pending approval — questions about bioequivalence methodology, manufacturing controls, formulation characterization, or potential safety signals. The FDA is legally required to respond to all citizen petitions before taking ‘final action’ on the application at issue. Even if the FDA ultimately denies the petition (which it does in the vast majority of cases where the petition appears primarily motivated by competitive concern rather than genuine safety issues), the review process takes time — often three to six months — during which the competitor’s approval is effectively delayed.

Congress recognized this problem and included a provision in the FDA Amendments Act of 2007 (FDAAA) giving the FDA authority to deny a citizen petition if it determines the petition was filed primarily to delay a competitor’s approval and does not raise legitimate safety or effectiveness concerns. The FDA has used this authority in a number of cases. But the tool remains in the innovator’s kit because even an ultimately denied CP can generate months of market protection while the FDA completes its required review.

Part 5: The IRA’s Hidden Patent Reform — How the Inflation Reduction Act Rewrites the Exclusivity Map

Key Takeaways: Part 5

The Inflation Reduction Act (IRA) of 2022 created a new, non-patent-based Loss of Exclusivity event: mandatory price ‘negotiation’ (effectively price setting) for high-spending single-source drugs in Medicare, backed by a prohibitive excise tax for non-compliance. This negotiation clock runs independently of patent expiration and can arrive decades before patents expire.

The ‘pill penalty’ — the IRA’s disparate treatment of small molecules (9-year negotiation clock) versus biologics (13-year clock) — is not a minor policy distinction. It is a structural financial disincentive for small-molecule R&D that empirical research shows is already reducing investment in small-molecule drug development.

The IRA is ‘cryptic patent reform’: it never amends a single line of patent law, yet it fundamentally reduces the economic value of every secondary or late-stage patent that an innovator would have filed to extend exclusivity from year 9 to year 17 or beyond. The ROI on late-stage evergreening patents has declined materially.

The IRA’s Maximum Fair Price (MFP), once negotiated and published, will function as a de facto national price ceiling — not just for Medicare — because commercial payers and PBMs will use it as a reference point in their own negotiations, exporting the negotiated discount across the entire market.

Medicare Drug Price Negotiation: The Mechanism and Its Strategic Consequences

The IRA empowers the Centers for Medicare and Medicaid Services (CMS) to directly ‘negotiate’ prices for a defined set of drugs — those with the highest Medicare Part D expenditure, with no FDA-approved generic or biosimilar competition, and that have been on the market beyond their applicable negotiation-free period. The negotiated price, called the Maximum Fair Price (MFP), applies to Medicare Part D (and eventually Part B) coverage.

The word ‘negotiation’ is somewhat misleading. The process is closer to price arbitration than true negotiation. CMS sets an initial offer price based on the drug’s comparative clinical effectiveness and cost-effectiveness benchmarks. The manufacturer may submit a counter-offer. The negotiation proceeds through defined rounds, but if agreement is not reached, the manufacturer faces a prohibitive excise tax on U.S. drug revenues — beginning at 65% and escalating to 95% — effectively forcing agreement. The only practical alternative to accepting the MFP is withdrawing the drug from Medicare entirely, which most companies cannot commercially afford.

CMS negotiated its first tranche of 10 drugs in 2023-2024, targeting the highest-spending Medicare Part D drugs. The list included Eliquis (apixaban), Jardiance (empagliflozin), Xarelto (rivaroxaban), Januvia (sitagliptin), Farxiga (dapagliflozin), Entresto (sacubitril/valsartan), Enbrel (etanercept), Imbruvica (ibrutinib), Stelara (ustekinumab), and Fiasp/NovoLog insulin products. The negotiated MFPs published in August 2024 reflected discounts of 38-79% from the drugs’ list prices.

The MFP’s commercial impact extends well beyond Medicare. Once published, the MFP is a public price point. Commercial payers and PBMs — who have long operated in information environments where the ‘true’ net price after rebates was closely guarded by both manufacturers and PBMs — now have a public, government-negotiated reference price for the highest-spending drugs. In contract negotiations, a PBM can point to an MFP of $200/month for Drug X and argue that its current net price of $350/month (after rebates) is indefensible relative to what Medicare is paying. This ‘price exportation’ dynamic is not a hypothetical — it is the predictable commercial consequence of introducing a public price point into an opaque market.

Institutional investors and sell-side analysts should build ‘MFP contagion’ scenarios into revenue models for any drug with significant Medicare exposure that is approaching its negotiation eligibility window. The baseline assumption should not be that the MFP applies only to Medicare revenues. A conservative model applies the MFP discount across 40-60% of the commercial market over a 3-5 year period as payer contracts come up for renewal and MFP visibility is incorporated into negotiating benchmarks. A base case applies the discount to the full non-Medicare book over that period. Running these scenarios against consensus revenue estimates reveals whether the market is correctly pricing IRA contagion risk for specific assets.

The Pill Penalty: A Quantified R&D Disincentive

The IRA’s disparate treatment of small-molecule drugs versus biologics in determining negotiation eligibility timelines is the legislation’s most consequential and most controversial structural feature.

Small-molecule drugs become eligible for CMS price negotiation after 9 years from FDA approval. Biologics become eligible after 13 years. The practical meaning of this 4-year difference is that biologics retain full commercial pricing power during the period — roughly years 9 through 13 post-approval — when a drug is typically at or near peak revenue. Its indication list is fully established, its label has been refined, physician familiarity is maximal, and marketing spending is declining as a percentage of sales. This is the most profitable period in a drug’s lifecycle, and the IRA strips it entirely from small-molecule drugs while protecting it for biologics.

The pharmaceutical industry began warning, from the moment the IRA passed, that this differential treatment would shift R&D incentives away from small-molecule drugs toward biologics. Critics argued this was both medically suboptimal (small-molecule drugs are often more convenient for patients, more orally bioavailable, and more amenable to global manufacturing) and economically distorting (it adds complexity and cost to the therapy development process without clinical justification).

Research published in peer-reviewed economics and health policy literature has begun to quantify these effects. One study found that since the IRA’s introduction, aggregate small-molecule investment by pharmaceutical companies valued under $2 billion has declined by 68%. For treatments specifically targeting diseases with a high proportion of Medicare beneficiaries — where IRA negotiation risk is most immediate — median investment amounts fell by 74%. These are not marginal shifts in portfolio composition. They represent a structural realignment of early-stage pharmaceutical R&D capital allocation.

The IRA is, in effect, conducting an uncontrolled clinical trial on pharmaceutical innovation policy: can you selectively price-control small molecules without redirecting R&D toward biologics? The early evidence suggests the answer is no.

Cryptic Patent Reform: How the IRA Defangs Evergreening

The IRA’s effect on the pharmaceutical patent system operates not through any change to patent law, but through a change in the economic calculus of filing late-stage secondary patents. This is what Michigan Law’s ‘Cryptic Patent Reform Through the Inflation Reduction Act’ analysis describes — a fundamental alteration of patent value achieved entirely through price control legislation.

To understand the mechanism, consider the following. A brand company with a small-molecule drug approved in year 0 under the pre-IRA regime had strong incentives to build a secondary patent thicket protecting the product through year 17, 18, or beyond. Every year of additional exclusivity beyond the CoM patent expiration was worth substantial commercial value — the product’s annual revenue multiplied by the probability that the patent would survive litigation.

Under the IRA, a small-molecule drug’s price is negotiated by CMS at year 9. From year 9 forward, the commercial value of the drug is constrained by the MFP. Secondary patents that would have protected revenue in years 10-17 are now protecting revenue at MFP-constrained prices rather than free-market prices. The ROI on filing those late-stage patents has plummeted. A formulation patent worth, hypothetically, $500 million in protected revenue under pre-IRA pricing assumptions might be worth $150 million under post-IRA MFP-constrained assumptions. The patent is not invalidated — it is economically devalued.

This creates a rational decision for IP teams: reduce investment in late-stage secondary patent filings for small-molecule drugs and redirect that IP budget toward earlier-stage patents (where the compound is still within its pre-negotiation window) or toward biologic assets (where the 13-year clock preserves the value of secondary patents in years 9-13). The IRA has, without touching a word of patent statute, reshaped the rational IP filing strategy for the entire industry.

Technology Roadmap: The Innovator’s IRA Response Strategy

Given the IRA’s structural impact, innovator companies are executing a portfolio-level pivot across four dimensions.

The first dimension is indication sequencing acceleration. A drug’s first FDA approval date starts the IRA clock. Companies are accelerating development timelines to get their most commercially important indications approved early, maximizing the pre-negotiation revenue window. Filing earlier for each subsequent indication, rather than sequentially developing them, is now an explicit IRA-response strategy.

The second dimension is biologic format preference for new development programs. When a therapeutic target can be addressed by either a small-molecule drug or a biologic (antibody, bispecific, ADC), the 4-year extension of the pre-negotiation window creates a clear financial argument for the biologic format. Business development and portfolio prioritization decisions are increasingly factoring in this IRA-derived clock differential.

The third dimension is geographic revenue diversification. Because the IRA applies specifically to Medicare (a U.S. government payer), drugs with dominant revenue profiles in non-U.S. markets face reduced IRA impact. This creates an incentive to accelerate ex-U.S. launches and to develop indication packages that maximize commercial value in markets where the IRA’s price controls do not apply.

The fourth dimension is early-stage patent portfolio construction. If late-stage secondary patents are now economically less valuable for small molecules, IP teams should concentrate prosecution resources on broader, earlier-stage patents that can be used to capture more commercial value during the pre-negotiation window, rather than filing dense thickets of late-stage formulation and method-of-use patents that will be economically devalued by the IRA clock.

Part 6: Turning Patent Data into Commercial Weapons — The ROI of Competitive Intelligence

Key Takeaways: Part 6

Patent and litigation data is an offensive commercial tool, not a defensive legal archive. The companies that generate the best returns from the LOE cycle are those that see further ahead than their competitors — identifying P.IV opportunities before competitors file, anticipating LOE events before they reach consensus estimates, and securing API supply chain relationships before generic launch day.

For the innovator, the primary data questions are: ‘Who has filed a P.IV against my products?’ ‘What are the weak patents in my thicket?’ ‘What is the patent cliff exposure of my M&A target, and how does it affect the deal’s NPV?’

For the generic and biosimilar challenger, the primary questions are: ‘Which high-value products have thin or weak patent estates?’ ‘Can we be first to file a P.IV?’ ‘What API suppliers are qualified and available for our target drug’s active ingredient?’

For institutional investors, the questions are: ‘What is the aggregate LOE exposure in this company’s commercial portfolio over the next 5 years?’ ‘Is the market correctly pricing the risk that a P.IV challenge will succeed and generate an early generic?’ ‘What does the biosimilar pipeline look like for the top five drugs in this Big Pharma’s revenue mix?’

The CI Playbook for Each Market Participant

Competitive intelligence in pharmaceutical patent strategy is not a single discipline — it is a set of distinct analytical functions tailored to the decision-making context of each player in the LOE ecosystem.

Innovator Brand Teams

For the brand company’s IP, commercial, and business development teams, the most time-sensitive intelligence need is early warning of P.IV activity against marketed products. ANDA filings with P.IV certifications are public records once the generic company sends its Notice Letter, but the most sophisticated brands monitor ANDA filing activity continuously to anticipate the Notice Letter before it arrives. Platforms that provide real-time ANDA filing alerts allow brand IP teams to begin pre-litigation preparation — organizing the patent litigation team, running claim mapping analyses, and identifying prosecution history vulnerabilities — weeks before the formal notice arrives, rather than scrambling reactively.

For business development teams evaluating M&A or in-licensing targets, patent estate quality assessment is a prerequisite for deal valuation. A drug with $2 billion in annual revenue and a single, broad CoM patent expiring in four years is a fundamentally different asset than one with the same revenue protected by a deep secondary thicket extending twelve years. The patent estate is a core input to the DCF model, and the due diligence process must include a comprehensive analysis of patent validity risk, LOE timing probability distributions, and competitive biosimilar or generic development timelines.

For R&D portfolio teams, patent landscape analysis identifies ‘white space’ where genuinely novel approaches to a therapeutic target are not yet claimed by either the innovator or competitors. This is the most intellectually honest application of patent intelligence: using the published record of what has been claimed to find what has not been claimed, generating insights for truly new development directions rather than incremental evergreening.

Generic and Biosimilar Challengers

For generic manufacturers, the CI workflow begins with target identification: screening the universe of currently commercialized drugs for products with high annual revenue, near-term CoM expiration, thin secondary patent estates, and limited prior P.IV activity. Products that have already attracted multiple P.IV filers are less attractive targets for new entrants, because the 180-day exclusivity opportunity has already been captured. Products whose CoM expiration is 24-36 months away, with no documented P.IV filings and a secondary patent estate that analysis suggests is weak or narrow, represent the highest-value opportunity set.

Once a target is identified, the ‘de-thicketing’ analysis begins: a systematic, claim-by-claim assessment of every patent in the innovator’s Orange Book listing and broader portfolio to identify those most vulnerable to P.IV challenge on invalidity (obviousness, anticipation, inadequate written description, enablement) or non-infringement grounds. This analysis directly determines the content and strength of the Notice Letter.

For biosimilar developers, the equivalent analysis focuses on the 351(k) landscape: reference product exclusivity expiration dates (which establish the earliest possible FDA approval date), the biosimilar patent dance posture (whether to engage or opt out), and the competitive field of other biosimilar developers targeting the same reference product. Given the first-mover commercial advantages documented in biosimilar markets (the first two to three entrants have consistently captured over 90% of biosimilar market share in physician-administered settings), the race-to-market analysis is as commercially important as the patent litigation analysis.

Institutional Investors

For equity research analysts and portfolio managers at institutional investors, pharmaceutical patent expiration data is a core input to earnings model construction. The standard analytical framework begins with a drug-by-drug LOE calendar for each company in the coverage universe, mapping CoM expiration dates, secondary patent expiration dates, biosimilar reference product exclusivity end dates, and IRA negotiation eligibility dates against the company’s revenue model.