Generic drug companies do not compete on science. They compete on timing, legal nerve, and an encyclopedic understanding of a regulatory statute that has not been fundamentally rewritten since Ronald Reagan signed it into law in 1984. The Hatch-Waxman Act — formally the Drug Price Competition and Patent Term Restoration Act — created the framework that now governs how generic manufacturers enter the U.S. market, when they can enter, and whether they get to do so alone for six profitable months before anyone else.

That six-month window, the 180-day exclusivity period, has become one of the most fought-over prizes in the pharmaceutical industry. It rewards the first generic applicant willing to challenge a branded drug’s patents. The reward can be worth hundreds of millions of dollars, occasionally billions. And collecting it requires navigating a legal and regulatory gauntlet that has spawned a body of case law, FDA guidance documents, and strategic maneuvering that fills law firm libraries and shapes M&A decisions across the industry.

This article covers how the Abbreviated New Drug Application (ANDA) process works, what triggers the 180-day clock, how branded companies fight back, and what the competitive dynamics look like from the vantage point of generic drug executives who have actually tried to collect this prize — and sometimes failed.

Part I: The Architecture of Hatch-Waxman

Why Congress Built This System

Before 1984, a generic manufacturer had to run its own clinical trials to prove a drug was safe and effective, even if those trials had already been run by the branded manufacturer. That requirement was, in practice, a nearly absolute bar to generic competition. The cost and time made it irrational for a generic company to develop a copy of a branded drug when the branded manufacturer held a patent. You’d spend years and hundreds of millions of dollars, and then still be blocked from the market.

Senator Orrin Hatch and Representative Henry Waxman struck a deal that restructured this bargain. Generic manufacturers could rely on the innovator’s safety and efficacy data by filing an ANDA, demonstrating only that their product was bioequivalent to the reference listed drug. In exchange, branded manufacturers got patent term restoration — up to five years added back to a patent to compensate for time lost during FDA review — plus a new layer of patent protection through the Orange Book.

The deal was premised on a tension that has never been fully resolved: the public interest in affordable generic drugs versus the private interest of branded companies in recouping their R&D investment. Forty years of litigation, lobbying, and regulatory evolution have produced a system that serves both interests imperfectly and generates enormous legal fees in the process.

The Orange Book: The Foundation Everything Else Rests On

The FDA’s Approved Drug Products with Therapeutic Equivalence Evaluations — universally called the Orange Book — is a public database listing every approved drug and every patent the brand manufacturer has listed as covering that drug. When a generic company wants to challenge a brand, the Orange Book is the starting point.

Branded manufacturers have an incentive to list as many patents as possible. Each listed patent triggers a procedural sequence that can delay generic entry. Critics have long argued this creates an opportunity for ‘evergreening’ — the strategic listing of secondary patents on formulations, methods of use, or delivery systems that extend effective market exclusivity well beyond the life of the underlying compound patent.

A compound patent — protecting the active molecule itself — typically provides the strongest and most durable protection. Method-of-use patents, covering a particular approved indication, and formulation patents, covering how the drug is delivered, have been litigated with mixed results. Courts and the FDA have spent decades working out which types of claims properly belong in the Orange Book and which do not.

The 2021 amendments to the Orange Book submission rules, codified in the CREATES Act and related FDA guidance, tightened the listing standards. The FDA now has authority to require delisting of patents that do not meet the statutory requirements. But the core problem — that any patent listing triggers a delay mechanism — persists.

Paragraph IV: The Certification That Starts the Clock

When a generic applicant files an ANDA, it must certify its position with respect to each Orange Book patent. There are four possible certifications:

Paragraph I: No patent has been listed.

Paragraph II: The listed patent has expired.

Paragraph III: The applicant will not market its drug until the patent expires.

Paragraph IV: The listed patent is invalid, unenforceable, or will not be infringed.

Paragraph I and II certifications are the easiest path — file your ANDA, prove bioequivalence, wait for FDA approval, and launch. But most commercially significant drugs carry active patent protection, which means the interesting action happens at Paragraph IV.

A Paragraph IV certification is simultaneously an administrative filing and a declaration of war. By certifying that a listed patent is invalid or not infringed, the generic applicant is announcing its intention to enter the market over the brand’s objection. Federal law treats this act as an artificial act of infringement — enough to give the brand manufacturer standing to sue, even before a single generic tablet has been manufactured.

The notice requirement matters here. Once an ANDA with a Paragraph IV certification is filed, the applicant must notify both the patent holder and the NDA holder within 20 days. That notification starts a 45-day window during which the brand can file suit.

If the brand sues within 45 days, a 30-month stay automatically kicks in. FDA cannot approve the ANDA during that period unless the lawsuit concludes or the 30 months expire first. This automatic stay is the single most important mechanism protecting branded companies from immediate generic competition after a Paragraph IV challenge, and it is why generic litigation timelines routinely span three to five years from ANDA filing to product launch.

Part II: The 180-Day Exclusivity — Mechanics and Meaning

First Filer Status: What It Means and Why It Matters

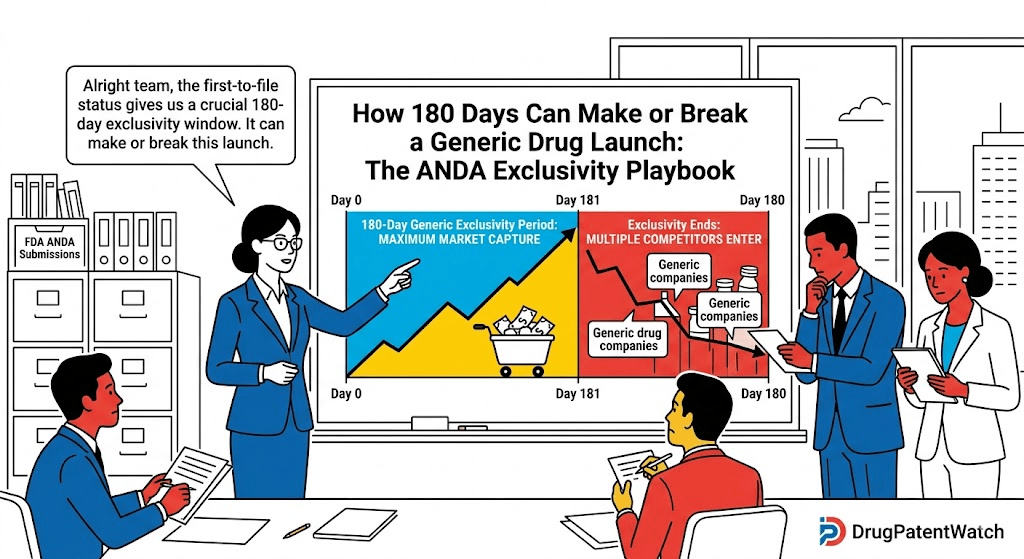

The 180-day exclusivity belongs to the first applicant — or applicants — to file a substantially complete ANDA containing a Paragraph IV certification against a given listed patent. FDA grants this status administratively, and it has enormous commercial consequences.

During the 180-day exclusivity window, FDA cannot approve any other ANDA for the same drug product with the same Paragraph IV certification. Only the first filer (or first filers, if multiple applications arrived on the same day) can market the generic. Because the branded manufacturer and first-filer generic are the only products in the market for six months, the generic can maintain a higher price point — typically 20% to 40% below branded — rather than the sub-10% levels that prevail after five or more generics enter.

The revenue implications are substantial. For a drug doing $2 billion in annual sales, even a modest 20% price discount on a 70% market share capture during 180 days of exclusivity generates revenues in the $180 million to $250 million range. For blockbusters, the numbers are proportionally larger. The first generic entrant for Plavix (clopidogrel bisulfate) — Apotex’s challenge against Bristol-Myers Squibb and Sanofi — was settled controversially, but the commercial prize at stake was estimated at over $1 billion in first-year revenues for whoever reached market first [1].

How the Exclusivity Clock Starts

The 180-day exclusivity does not start automatically on the date of FDA approval. It starts on the earlier of two events:

The first commercial marketing of the drug by a first filer.

A court decision finding that the challenged patent is invalid, unenforceable, or not infringed (a so-called ‘court forfeiture trigger’).

This timing mechanism creates a strategic problem. A first-filer generic can hold its ANDA approval and delay the start of the clock. If it does not launch and no court decision has issued, the 180 days do not begin. Subsequent filers remain blocked. The patent owner keeps getting royalties (if any) or simply keeps its market intact.

Congress recognized this problem and created forfeiture provisions in the 2003 Medicare Modernization Act. Under those provisions, a first filer can lose its exclusivity if it fails to market the drug within specified timeframes, if it enters into certain disqualifying agreements with the brand, or under several other triggering conditions. The forfeiture provisions have been extensively litigated, and their application to specific fact patterns is still being worked out case by case.

Shared Exclusivity and Same-Day Filers

If two or more generic applicants file substantially complete ANDAs with Paragraph IV certifications on the same day against the same patent, they share the 180-day exclusivity. This means each of them can launch as soon as it receives approval, but no subsequent filer can enter the market until the shared exclusivity period expires.

Shared exclusivity dilutes the prize. Two generics splitting a market produce more price competition than one. The economics are still attractive — both companies benefit from six months of limited competition — but the per-company revenues are lower.

This dynamic drives extraordinary behavior around ANDA filing windows. When a major patent expiration is anticipated, generic companies assign teams to monitor the date and file their ANDAs on the first possible day. Filing rooms at the FDA’s offices in Silver Spring, Maryland have seen the pharmaceutical equivalent of a midnight madness sale, with courier services queuing up at the door to deliver stacks of applications the moment they open.

With the FDA’s shift to electronic submissions, the bottleneck has changed but not disappeared. Applicants try to submit within the same minute of the same day. The FDA’s receipt timestamp determines who qualifies as a same-day filer.

The Citizen Petition Problem

Brand manufacturers have used citizen petitions — a regulatory mechanism that allows any person to ask the FDA to take an action — to slow ANDA approvals. A brand company files a petition raising safety or scientific concerns about a generic’s bioequivalence approach or labeling. FDA must respond before approving the ANDA. Even if the petition has no merit, the response process can add months.

Congress addressed this in the FDA Amendments Act of 2007, allowing FDA to deny petitions submitted with the primary purpose of delaying generic drug approval. But the line between legitimate scientific concerns and delay tactics is often blurry, and the agency exercises its authority here cautiously. Citizen petitions remain a tool in the branded company’s defensive arsenal, and experienced patent litigators track petition filings as a signal of a brand’s competitive strategy.

Part III: The Litigation Ecosystem

Paragraph IV Litigation as an Industry

Hatch-Waxman patent litigation is effectively its own legal industry. Major law firms — Kirkland & Ellis, Latham & Watkins, Quinn Emanuel, Fish & Richardson, Axinn Veltrop & Harkrider — have dedicated pharmaceutical patent practices that run simultaneously on both sides of the ‘v.’ The cases combine patent law, administrative law, regulatory science, and commercial litigation in ways that require teams of 20 or more attorneys on significant matters.

The U.S. District Court for the District of Delaware handles a disproportionate share of these cases. Delaware’s courts have developed specialized expertise in pharmaceutical patent disputes, and many NDA holders incorporate there, giving defendants a predictable venue argument. The District of New Jersey is the other primary forum, particularly for companies headquartered in the region.

The Patent Trial and Appeal Board (PTAB), created by the America Invents Act of 2011, added another dimension. Generic companies now routinely file inter partes review (IPR) petitions challenging branded patents at PTAB, either in parallel with district court litigation or as a standalone strategy. PTAB proceedings move faster than district court litigation — final written decisions come within 12 to 18 months of institution — and the success rate for petitioners has historically been higher than in district court.

Brand companies have pushed back against the PTAB route through the Supreme Court (Cuozzo Speed Technologies v. Lee [2], Oil States Energy Services v. Greene’s Energy Group [3]) and through regulatory advocacy. The Federal Circuit has refined the standards for institution and the scope of estoppel that flows from IPR proceedings. For generic companies, IPR can be a way to clear a patent path faster and more cheaply than full district court litigation, but the estoppel risk — you cannot later raise in district court arguments you raised or reasonably could have raised at PTAB — requires careful tactical planning.

The 30-Month Stay: Strategic Management

The automatic 30-month stay that follows a timely brand lawsuit is both a protection for innovators and a strategic tool. Brands can file infringement suits on every listed patent, even weak ones, triggering the stay. If multiple patents are listed, each one that receives a Paragraph IV certification and generates a suit can potentially extend the effective delay.

Courts have cabined this somewhat. The stay runs from the date of the patent owner’s receipt of the Paragraph IV notice, not from the filing date of the suit. And stay periods can be shortened if the district court finds a case is being unreasonably delayed by either party.

Some generic companies have tried to avoid the stay altogether by filing only Paragraph III certifications on certain patents — agreeing to wait until those patents expire — while filing Paragraph IV only on others. This segmented strategy requires careful analysis of which patents are truly vulnerable and which are likely to survive challenge.

Reverse Payment Settlements: The ‘Pay-for-Delay’ Controversy

No aspect of Hatch-Waxman law has generated more regulatory and political controversy than reverse payment settlements, also called pay-for-delay agreements. In a typical settlement of commercial litigation, the party that has allegedly done something wrong pays the aggrieved party. In a reverse payment settlement, it runs the other way: the brand manufacturer pays the generic to settle the case and agree to delay its market entry.

The brand’s logic is clear. If the generic’s patent challenge succeeds, the brand loses its entire market to generic competition years early. A one-time payment to the generic — which preserves the brand’s monopoly for the remaining patent period — is worth it economically if it is less than the present value of the brand’s expected future profits.

The FTC spent years arguing these agreements were per se anticompetitive. Generic companies received a payment that had no other reasonable explanation than to compensate them for staying out of the market. In FTC v. Actavis, Inc. [4], the Supreme Court in 2013 held that reverse payment settlements must be analyzed under the rule of reason — neither per se legal nor per se illegal, but subject to a fact-specific antitrust inquiry. Justice Breyer’s majority opinion created space for the FTC to challenge settlements that exceed a threshold of reasonable litigation value, while acknowledging that some settlements can be procompetitive.

Post-Actavis litigation has continued. The key factual question is whether the payment — which is often disguised as a co-promotion agreement, a licensing deal, or some other commercial arrangement rather than a cash transfer — reflects legitimate commercial value or amounts to compensation for staying out. Courts have wrestled with how to assess ‘large and unjustified’ payments in the absence of a publicly visible cash transfer.

The FTC’s 2023 pharmaceutical competition report noted ongoing enforcement attention to these arrangements [5]. Generic companies and their counsel monitor Actavis-compliant settlement structures carefully. Plaintiffs’ class action attorneys watch settlement filings for the same reason — reverse payment class actions are now a standard feature of pharmaceutical antitrust litigation.

Part IV: Strategic Dynamics for Generic Entrants

The ANDA Portfolio Approach

Large generic manufacturers — Teva Pharmaceutical Industries, Viatris (formerly Mylan), Sandoz (now independent), Amneal Pharmaceuticals, Hikma Pharmaceuticals — maintain portfolios of ANDA filings that span hundreds of products at various stages of approval. Managing this portfolio requires tracking patent expiration dates, litigation status, competitive intelligence on what other generic applicants have filed, and commercial forecasts for each product.

DrugPatentWatch, a commercial database, is a standard tool in this analysis. The platform aggregates Orange Book patent data, ANDA filing information, litigation status, and patent expiration dates into a searchable format. Portfolio managers at generic companies use it to identify products approaching patent expiration, to assess who else has filed for a given product, and to track litigation outcomes that affect their own exclusivity position. Investment analysts covering the pharmaceutical sector use the same data to estimate future generic entry timelines for branded drugs and model the resulting revenue impact.

Generic pipeline decisions turn on several factors: the commercial size of the branded market, the strength of the patent portfolio protecting it, the likelihood of first-filer exclusivity, the cost of ANDA development and potential litigation, and the anticipated competitive landscape upon launch. A drug with $500 million in annual sales, a single vulnerable compound patent, and no other ANDA filers identified might be worth significant litigation risk. A drug with $100 million in sales, four listed patents with good validity arguments, and seven other identified filers is probably not.

The Para IV Challenge Calculus

Deciding whether to file a Paragraph IV certification on a given patent requires legal and commercial analysis in combination. The legal questions are:

Is this patent valid? Does the prior art support an invalidity challenge? Were there prosecution history estoppels that limit the claims?

Does our product infringe? Can we design around the claims?

If we litigate and lose, what is our exposure — damages, injunctions, attorneys’ fees under 35 U.S.C. § 285?

The commercial questions are:

If we win, what is the market opportunity during exclusivity?

If we lose, what have we spent on litigation and ANDA development?

Where do competitors sit — are other filers already in line for shared exclusivity?

An underappreciated complication is the timing interaction between patent litigation and FDA review. ANDA review times at FDA have varied significantly over the years. Backlogs grew in the mid-2010s as FDA received record numbers of filings. The Generic Drug User Fee Amendments (GDUFA) program, which began in 2012 and was reauthorized in subsequent years, imposed performance goals on FDA review times in exchange for industry user fees. GDUFA II goals for standard applications target a 10-month review period for applications filed after GDUFA II implementation; priority applications get a shorter window.

If the FDA approval is expected before the 30-month stay expires, the generic may have an approved product ready to launch the day the litigation concludes or the stay expires. If FDA review runs slower, the litigation may effectively be moot — the product isn’t approved anyway. Conversely, an early FDA approval creates pressure to settle litigation on terms that allow launch, or to press hard for a court ruling before the brand manufacturer is ready for trial.

Section 505(b)(2) Applications: A Different Route to Market

Not every branded generic strategy runs through a standard ANDA. Section 505(b)(2) of the Federal Food, Drug, and Cosmetic Act allows an applicant to file a new drug application relying in part on the FDA’s prior findings of safety and efficacy for a reference drug — without needing a full ANDA.

This pathway is available for products that differ from the reference listed drug in ways that prevent a straightforward bioequivalence showing: different dosage forms, new routes of administration, different strengths, or reformulations. A company developing an extended-release version of a drug that exists only in immediate-release form might file a 505(b)(2).

The patent certification requirements apply to 505(b)(2) applications just as they do to ANDAs, including the right to file a Paragraph IV certification and potentially to receive 180-day exclusivity. But the regulatory landscape is more complex, and the FDA has issued extensive guidance attempting to specify what additional data a 505(b)(2) applicant must provide.

For branded generic companies — those that market differentiated versions of existing drugs under proprietary names — the 505(b)(2) route can provide market exclusivity through a combination of Hatch-Waxman regulatory protections and new patent filings of their own. Companies like Assertio Holdings, Supernus Pharmaceuticals, and various specialty pharma firms have built their business models partly on this pathway.

Part V: The Branded Manufacturer’s Defense

The Patent Thicket Strategy

Branded pharmaceutical companies have learned, over four decades of Hatch-Waxman experience, to build dense patent portfolios around successful drugs. The term ‘patent thicket’ describes a situation where a drug is protected by multiple overlapping patents, each covering a different aspect of the product, and any one of which could block generic entry independently.

AbbVie’s Humira (adalimumab) is the paradigmatic example. As the world’s best-selling drug for much of the 2010s, Humira generated roughly $21 billion in global revenues in 2022 [6]. AbbVie constructed a patent portfolio of over 100 patents covering the antibody, its manufacturing process, specific formulations, and methods of treatment for various conditions. Generic (biosimilar) manufacturers faced the prospect of challenging not one patent but dozens, sequentially.

The small-molecule equivalent of this strategy is no less aggressive. Branded companies file continuation applications, divisional applications, and continuation-in-part applications that extend the life of a patent family and create new blocking positions. Method-of-treatment patents, which cover the use of a drug for a specific indication rather than the molecule itself, can sometimes outlast the compound patent by years.

Risk Evaluation and Mitigation Strategies (REMS) as a Barrier

Some drugs carry FDA-mandated Risk Evaluation and Mitigation Strategies — programs designed to manage serious risks associated with the drug’s use. Opioids, immunosuppressants, drugs with teratogenicity risks, and others may require REMS programs.

For generic manufacturers, REMS can be a practical barrier even after all patent issues are resolved. To conduct bioequivalence testing, a generic company may need samples of the branded drug. If the REMS program restricts distribution — for example, by limiting sales to certified pharmacies or requiring a special prescription system — the generic manufacturer may have difficulty obtaining sufficient samples.

The CREATES Act [7], which became law in 2019, addressed this problem by creating a private right of action allowing generic and biosimilar applicants to sue brand manufacturers that have refused to provide drug samples on commercially reasonable terms. The act was a direct response to documented instances where branded manufacturers invoked REMS safety programs as a pretext for withholding samples from generic competitors.

CREATES Act litigation has resulted in settlements and policy changes at some branded manufacturers. Ampio Pharmaceuticals, Catalyst Biosciences, and other branded companies have faced CREATES Act suits. The act has not fully resolved the access problem — some brand companies continue to cite legitimate safety concerns that blur into competitive strategy — but it has changed the calculus.

Pediatric Exclusivity: Six More Months on Top

A separate but interacting mechanism — pediatric exclusivity under the Best Pharmaceuticals for Children Act — can add six months to all Orange Book patents and market exclusivity periods for a drug. Branded manufacturers earn this by conducting FDA-requested pediatric studies.

The six months attach to each patent separately, meaning that if the compound patent and the formulation patent are both listed, both get extended by six months. For a drug with a significant pediatric use potential and a valuable franchise to protect, the investment in pediatric studies can pay for itself many times over in delayed generic entry.

Critics have argued that pediatric exclusivity has been granted too readily for drugs unlikely to be used in children, effectively functioning as a subsidy to branded manufacturers without delivering meaningful pediatric data. The FDA has tightened the standards somewhat, but the mechanism remains a standard defensive tool.

Part VI: The Biosimilar Parallel — A Different But Related Battle

Biologics Price Competition and Innovation Act

When Congress passed the Affordable Care Act in 2010, it included the Biologics Price Competition and Innovation Act (BPCIA), which created an abbreviated approval pathway for biosimilar drugs — biologics that are highly similar to an already-approved reference biological product. The BPCIA was explicitly modeled on Hatch-Waxman but adapted for the much more complex scientific and regulatory landscape of biologics.

Where small molecules can usually be shown bioequivalent through pharmacokinetic studies, large-molecule biologics require a more extensive demonstration of biosimilarity. The analytical complexity is significantly higher, and the manufacturing process is itself part of the product in ways that have no parallel in small-molecule chemistry.

The BPCIA created its own patent dispute mechanism — the ‘patent dance,’ a structured disclosure and negotiation process between the reference product sponsor and the biosimilar applicant — and its own exclusivity provisions, including 12 years of data exclusivity for reference biological products.

The 180-day first-interchangeable-biosimilar exclusivity, introduced in the BPCIA, applies specifically to the first biosimilar designated as interchangeable with the reference product. An interchangeable designation means FDA has concluded the biosimilar can be substituted for the reference product at the pharmacy level without a prescriber’s involvement. This is the rough biosimilar equivalent of AB-rated generic substitutability in the small-molecule world.

The Humira Biosimilar Experience

The Humira biosimilar launches beginning in 2023 — delayed by years of patent litigation and licensing negotiations — illustrate both the potential and the complications of the biosimilar pathway. AbbVie negotiated licensing agreements with multiple biosimilar manufacturers that allowed them to launch in the United States starting January 2023, with royalty payments to AbbVie that effectively made AbbVie a financial beneficiary of the biosimilar market it could not block entirely.

By mid-2023, multiple Humira biosimilars were on the market, including products from Amgen (Amjevita), Pfizer (Abrilada), Sandoz (Hyrimoz), Coherus BioSciences (Yusimry), Boehringer Ingelheim (Cyltezo, the first interchangeable biosimilar), and others [8]. Pricing and payer adoption moved more slowly than proponents expected, because the branded biosimilar market operates differently from the small-molecule generic market — pharmacy benefit managers, formulary decisions, and rebate economics all play roles that have no real analogue in generic substitution.

The Humira biosimilar situation is likely to replicate, on a longer timeline, for Stelara (ustekinumab), Keytruda (pembrolizumab), Dupixent (dupilumab), and other high-revenue biologics approaching biosimilar eligibility.

Part VII: The FDA’s Role — Approval, Delay, and Orange Book Delisting

FDA Approval Standards for ANDAs

FDA approval of an ANDA requires demonstration that the generic product:

Contains the same active ingredient(s) as the reference listed drug.

Has the same dosage form, route of administration, and strength.

Is bioequivalent to the reference listed drug.

Meets FDA requirements for labeling, manufacturing (cGMP), and other applicable standards.

Bioequivalence is typically demonstrated through in vivo pharmacokinetic studies in healthy volunteers. The FDA requires that 90% confidence intervals for the ratio of key pharmacokinetic parameters (AUC and Cmax) fall within 80%-125% of the reference product’s values. This standard has been criticized as imprecise for some drug classes — particularly for drugs with narrow therapeutic windows, where variations of this magnitude could be clinically meaningful — but it has been the governing standard since the agency adopted it.

For certain drug classes — modified-release formulations, locally acting drugs, inhaled drugs, topical products — bioequivalence demonstration is more complex. FDA has issued product-specific guidance documents for hundreds of drugs specifying what studies are required to support ANDA approval for those products.

Complete Response Letters and Refuse-to-File Actions

The FDA review process for ANDAs is not a rubber stamp. Complete Response Letters (CRLs) — FDA’s mechanism for communicating deficiencies that must be resolved before approval — are common. They can address bioequivalence study design flaws, labeling issues, manufacturing facility deficiencies identified during inspection, or other matters.

Each CRL resets the review clock in some respects. Multiple CRL cycles on a single ANDA can extend the time from filing to approval by years. Generic companies with large ANDA portfolios manage CRLs as a normal part of the pipeline, but the cumulative drag on specific products can be significant.

The FDA can also refuse to file an ANDA if it is not substantially complete as submitted. A refuse-to-file action effectively restarts the exclusivity clock implications — if the FDA refuses to file, the application is treated as not having been submitted for purposes of first-filer status.

Orange Book Delisting: A Growing Weapon

Recent years have seen increased use of Orange Book patent delisting challenges by generic manufacturers. Under the Hatch-Waxman Act, patent holders must certify that listed patents claim the drug or a method of using the drug. Patents that do not meet this standard should not be listed.

Generic manufacturers have filed petitions asking FDA to delist patents they believe do not properly cover the approved drug. The FDA’s authority here has been contested — in some cases, courts have held that FDA must defer to the patent owner’s listing certification — but recent legislative and regulatory changes have expanded FDA’s role.

The FTC has separately filed amicus briefs and intervened in proceedings arguing that improper Orange Book listings are anticompetitive. Novo Nordisk, Sanofi-Aventis, and other branded manufacturers have faced delisting challenges to patents covering device components (pens, auto-injectors) associated with injectable drugs, with courts ruling in several cases that device patents do not properly belong in the Orange Book for the drug product [9].

This front of the Hatch-Waxman battle is relatively new but growing. Generic and biosimilar manufacturers increasingly challenge the composition of branded companies’ Orange Book listings as a standalone strategy, separate from ANDA filings.

Part VIII: Notable Litigation and Landmark Cases

Pfizer v. Apotex: Teaching Old Amlodipine New Tricks

Pfizer’s Norvasc (amlodipine besylate) generated approximately $5 billion annually at its peak. When Apotex filed a Paragraph IV certification challenging Pfizer’s besylate salt patent, the stage was set for a case that would define how courts analyze salt-form patents.

The Federal Circuit ultimately ruled in Apotex’s favor, finding that the besylate salt claimed in Pfizer’s patent would have been obvious to a person of ordinary skill in the art, given prior art describing the free base form and established techniques for salt selection [10]. The case became required reading in pharmaceutical patent law courses and is cited routinely in debates over the standards for obviousness in patent challenges.

The economic consequence was immediate and dramatic. Dozens of generic amlodipine products entered the market. Wholesale prices fell by more than 90% within months. The case demonstrates both the upside of successful Paragraph IV litigation for generic manufacturers and the catastrophic downside for brands when a key patent falls.

In re K-Dur Antitrust Litigation: Reverse Payments Get Their Day in Court

Schering-Plough (later acquired by Merck) marketed K-Dur 20 (potassium chloride), a controlled-release potassium supplement. When generic manufacturers challenged patents, Schering-Plough entered into settlement agreements that included payments to the generics in exchange for delayed entry. The FTC challenged these agreements.

The Third Circuit’s 2012 ruling in In re K-Dur Antitrust Litigation [11] adopted a rule that any reverse payment settlement was presumptively anticompetitive — a harder line than other circuits had taken. The circuit split this created was resolved by the Supreme Court in Actavis (2013), but the K-Dur litigation set the stage for that resolution and established important principles about how antitrust courts analyze settlements of Hatch-Waxman patent disputes.

AstraZeneca v. Apotex: Nexium’s Last Stand

AstraZeneca’s Nexium (esomeprazole magnesium) was among the most commercially successful drugs in pharmaceutical history, generating over $70 billion in cumulative global revenues. When multiple generic manufacturers sought to challenge the patents protecting it, AstraZeneca mounted a defense built on its patent covering the pure enantiomer form of omeprazole.

The central legal question was whether a patent claiming a single enantiomer of a racemic compound was obvious given prior art on the racemate. The District of New Jersey ruled for AstraZeneca, finding the enantiomer patent valid and infringed [12]. Multiple generic manufacturers ultimately had to wait for patent expiration, and Nexium maintained much of its branded market position longer than the generic industry expected.

The Nexium litigation has been used ever since as a case study in both branded patent strategy — the enantiomer patent bought AstraZeneca years of additional exclusivity for a drug that was itself a derivative of the earlier Prilosec — and the risks of relying on ‘next-generation’ molecule patents that may be vulnerable to obviousness attack.

Forest Laboratories v. Ivax: The Lexapro Saga

Forest Laboratories’ Lexapro (escitalopram oxalate) and its predecessor Celexa (citalopram hydrobromide) presented a textbook example of lifecycle management. As citalopram approached patent expiration, Forest had developed escitalopram — the active enantiomer — and obtained regulatory approval for the new product.

When generic manufacturers challenged the escitalopram patents, the litigation turned on similar obviousness questions as the Nexium cases: was selecting the active enantiomer of a known racemic drug obvious? Courts generally applied a fact-specific analysis, and outcomes varied somewhat. But Forest’s ability to shift its market from the off-patent citalopram to the patent-protected escitalopram before generic citalopram hit the market allowed it to defend significant revenue — a strategy that has been widely studied and replicated.

Part IX: Commercial Outcomes and the Generic Industry’s Economics

Revenue Modeling for First-Filer Exclusivity

Generic companies build DCF models for Paragraph IV opportunities that attempt to quantify the value of first-filer status. The key variables are:

Branded product revenues (the market being entered).

Expected market share capture at launch.

Expected price per unit relative to brand.

Duration of exclusivity and transition dynamics post-exclusivity.

Probability of winning the patent litigation.

Cost of ANDA development and litigation.

Risk of settlement and what settlement terms might look like.

The probability-weighted net present value of a Paragraph IV opportunity determines whether it clears the hurdle rate for investment. For small generic companies with limited capital, even high-NPV opportunities may be out of reach if the litigation exposure is too large. For larger players — Teva with a market cap in the billions — significant litigation costs are manageable across a diversified portfolio. <blockquote> ‘The 180-day exclusivity period generates approximately $4 billion annually across all generic entrants who collect it, representing some of the highest-margin revenue in the pharmaceutical industry.’ — IQVIA Institute for Human Data Science, Medicines Use and Spending in the U.S., 2022 report estimates on first-filer generic economics [13]. </blockquote>

This revenue concentration in the hands of first filers has produced consolidation pressure in the generic industry. Companies that cannot maintain a robust Paragraph IV pipeline — either because they lack the legal resources to litigate or the scientific infrastructure to develop complex ANDAs — lose market position to larger competitors. The generic industry in the United States is significantly more concentrated today than it was 20 years ago, a trend that has attracted its own antitrust scrutiny.

The Authorized Generic Problem

Branded manufacturers have another tool to undercut the value of the 180-day exclusivity: the authorized generic. An authorized generic is a version of the branded drug that the brand manufacturer (or a company it licenses) markets as a generic product — using the approved NDA but sold at generic prices, without a branded name.

Authorized generics are not subject to the 30-month stay or the ANDA exclusivity provisions because they are marketed under the NDA, not an ANDA. A brand manufacturer can launch an authorized generic the same day the first-filer generic launches, immediately splitting the market and reducing the first filer’s price advantage.

The FTC studied this practice extensively. Its 2011 report [14] documented that authorized generics reduce first-filer revenues but that they may also reduce prices to consumers sooner. The competitive tradeoff is real: authorized generics harm generic companies’ first-filer profits but benefit patients through faster and deeper price competition.

From a generic company’s perspective, an authorized generic launch by the brand during the exclusivity window is a significant negative for the economic case for Paragraph IV investment. Some settlement agreements explicitly prohibit authorized generic launches as part of the deal — a fact that adds another dimension to the Actavis antitrust analysis, since ‘no-AG clauses’ may represent additional value transferred from brand to generic.

Price Erosion After Exclusivity: The Cliff

After the 180-day exclusivity expires, additional ANDA approvals typically arrive quickly. The FDA has usually been reviewing other applications during the exclusivity period, and they are approved in rapid succession. The result is a price cliff.

For a drug with seven or eight competitors, within three to six months of exclusivity expiration, average selling prices fall to 10%-20% of the branded price. The first-filer’s margins compress dramatically. Products that were generating $50 million quarterly during exclusivity may generate $5 million quarterly two years later.

This dynamic means that manufacturing economics matter enormously. Generic manufacturers with lower cost structures — often those with API manufacturing in India or China — can survive the post-exclusivity price environment better than domestic manufacturers. The shift of generic manufacturing to low-cost jurisdictions, and the FDA inspection and supply chain concerns that followed, is partly a product of this relentless margin pressure after exclusivity.

Part X: Regulatory Evolution and the Road Ahead

FDA’s Accelerated Review Initiatives

The FDA has run several programs aimed at reducing the ANDA review backlog and accelerating approval of first-generic applicants. The Complex Drug Substances and Drug Products program, informally called the Complex Generics initiative, targets products where bioequivalence demonstration is scientifically complex — metered-dose inhalers, topical products, injectable emulsions.

For these products, the first ANDA approval can confer extended effective market exclusivity simply because the regulatory and scientific barrier is high enough that few competitors qualify. The first approved ANDA for a complex generic like ProAir HFA (albuterol sulfate inhalation aerosol) or Advair Diskus (fluticasone propionate/salmeterol inhalation powder) can dominate the market for years even after the 180-day Hatch-Waxman exclusivity expires, because the technical hurdles keep competitors out.

The FDA has published product-specific guidance for dozens of complex generics. The Perrigo challenge to GlaxoSmithKline’s Advair Diskus took years of scientific development and multiple FDA review cycles before receiving approval in 2019. That approval, and subsequent approvals for Mylan and others, ultimately did produce significant price competition — but on a much longer timeline than simple oral generic substitution.

The CREATES Act in Practice

Three years of CREATES Act enforcement has produced mixed results. The act clearly changed the behavior of some branded manufacturers who were previously withholding samples. Several settled CREATES cases quietly, providing samples and ending litigation without admissions.

But some REMS programs continue to create practical access barriers. The act requires only that samples be provided on ‘commercially reasonable, market-based terms.’ Disputes over what constitutes commercially reasonable pricing and what quantity of samples is required for adequate bioequivalence testing continue.

The FDA has tried to support CREATES Act enforcement by publishing guidelines on REMS-shared systems that distinguish safety-based restrictions from commercially motivated ones. Whether that distinction holds up in specific cases often requires litigation to determine.

Patent Listing Reform: The FTC’s Push

The Federal Trade Commission under Chair Lina Khan (2021-2025) made pharmaceutical patent practices a significant enforcement priority. The FTC sent a series of letters to pharmaceutical companies challenging specific Orange Book patent listings, arguing that device patents, software patents covering drug delivery apps, and other patents did not properly belong in the Orange Book for the associated drug products.

Several companies voluntarily delisted patents in response to FTC pressure. Novo Nordisk removed certain patents from its Orange Book listings for its GLP-1 drugs. The FTC’s authority to require delisting — as opposed to simply urging it — remains a contested legal question, but the agency’s willingness to challenge listings has changed the calculus for branded companies deciding what to list.

The Biden administration’s broader pharmaceutical competition agenda, articulated in the executive order on promoting competition in the American economy [15] issued in 2021, included several provisions directing agencies to use their authority to reduce pharmaceutical patent barriers to generic entry. Specific rulemakings followed at both FDA and FTC.

The current direction of pharmaceutical patent policy under the Trump administration (2025-present) reflects a different set of priorities — one more focused on domestic manufacturing and supply chain security than on patent system reform. Generic manufacturers have continued to pursue ANDA filings and Paragraph IV challenges regardless of the administration in power, but the regulatory and enforcement environment around Orange Book listings, CREATES Act enforcement, and reverse payment scrutiny will likely evolve.

Part XI: Real-World Applications — Case Studies in ANDA Strategy

Teva’s Generic Provigil: The Art of Timing

Cephalon’s Provigil (modafinil) was approved for narcolepsy and related conditions and generated approximately $1.1 billion in annual U.S. revenues before generic entry. Teva was among the early Paragraph IV filers challenging Cephalon’s patents. The subsequent settlement — in which Teva agreed to delay entry in exchange for a payment that included a license to market an authorized generic for a period before other generics entered — became one of the most-scrutinized reverse payment settlements pre-Actavis.

The FTC sued Cephalon, and Teva eventually agreed to pay $1.2 billion to settle FTC and state attorney general claims [16]. The settlement fund compensated consumers and government purchasers who allegedly overpaid for modafinil because of the delayed generic entry. The case is now used in law school antitrust courses as the leading example of how reverse payment liability can cost companies far more than the original settlement was worth.

Watson (Now Allergan/Actavis) and Loestrin: The Authorized Generic Play

Warner Chilcott’s Loestrin 24 Fe (norethindrone acetate and ethinyl estradiol) generated significant revenue in the branded oral contraceptive market. When Warner Chilcott faced generic entry challenges, it employed an authorized generic strategy that was ultimately challenged by class action plaintiffs.

The resulting litigation was extensive. Courts found that the authorized generic strategy, combined with certain settlement provisions, created sufficient grounds for antitrust claims. The case contributed to the development of legal standards for evaluating no-AG clauses and authorized generic competition in the post-Actavis environment [17].

Amneal and Par: Attacking Concerta

Methylphenidate (Concerta’s generic name) is a high-volume ADHD medication with complex extended-release characteristics. Multiple generic manufacturers, including Amneal Pharmaceuticals and Par Pharmaceutical, received FDA approvals for generic methylphenidate products — only to have consumer groups and physicians complain that the generics did not perform equivalently to the branded product in some patients.

The FDA undertook a review of the bioequivalence standards applied to these products and ultimately changed the recommended bioequivalence methodology for certain modified-release drug products [18]. Some approved generic methylphenidate products were withdrawn from sale pending re-evaluation. The situation illustrates that FDA approval of an ANDA does not guarantee commercial success — formulary positions, prescriber behavior, and post-market performance data all influence how generics actually perform in practice.

Part XII: Data Resources and Competitive Intelligence

Using Patent Databases for Generic Strategy

Sophisticated generic manufacturers and their legal teams use multiple data sources to build their patent landscape assessments. The USPTO’s public patent database provides full text of issued patents and prosecution history. The Orange Book itself, maintained at the FDA website, shows which patents are listed for which products. DrugPatentWatch aggregates this information and layers on litigation data, ANDA filing information (derived from FDA sources), and patent expiration timelines.

For a generic manufacturer assessing a Paragraph IV opportunity, a complete analysis typically includes:

All Orange Book-listed patents for the drug product, with expiration dates including any patent term extensions (PTE) under 35 U.S.C. § 156 and any pediatric exclusivity.

Full prosecution history review for each listed patent, to identify potential prosecution history estoppel arguments and to understand the claim scope.

Prior art search — to identify published literature, foreign patents, and other prior art that might support invalidity.

A freedom-to-operate analysis for the proposed generic formulation, to assess non-infringement arguments.

A competitive intelligence review — using DrugPatentWatch and other sources — to determine whether other ANDA filers have been identified, whether any litigation is already pending, and what the settlement history looks like for the brand’s patent portfolio.

Investment analysts covering the pharmaceutical sector use similar databases to model generic entry timelines. When Pfizer’s Eliquis (apixaban) patent status is being assessed for a 2026 LOE (loss of exclusivity) forecast, analysts pull Orange Book data, check PTAB proceedings, review Federal Circuit decisions in the relevant litigation, and model probability-weighted scenarios. The resulting forecasts drive coverage recommendations and price targets for both Pfizer and the generic manufacturers positioned to enter.

FDA’s Electronic ANDA Filing and Transparency

The FDA’s Electronic Common Technical Document (eCTD) format and its online systems for ANDA submission have improved transparency in some ways. The FDA publishes lists of ANDAs received, first-cycle approval actions, and final approvals through its Drugs@FDA database. It also publishes paragraph IV certification information that is required to be submitted as part of ANDA filings.

This publicly available data — combined with commercial aggregators like DrugPatentWatch — means that a generic company’s Paragraph IV filing on a major drug is not secret. The brand manufacturer receives direct notice. But the competitive intelligence value runs in both directions: other generic manufacturers also see the filing and can assess whether shared exclusivity is likely.

Part XIII: International Dimensions

The U.S. System in Global Context

The Hatch-Waxman framework is distinctly American. Other major pharmaceutical markets have different structures for managing the transition from branded to generic drugs:

In the European Union, data exclusivity (eight years) and market exclusivity (two additional years) protect reference medicinal products, with an additional year available for new indications. There is no equivalent of the 180-day generic exclusivity, and there is no automatic 30-month stay equivalent in most EU member states’ patent systems. Generics compete on price once they enter, and national reference pricing systems further compress margins.

Canada uses a combination of data protection and its own patent linkage system, which is somewhat analogous to Hatch-Waxman but operates differently in important respects. The Canadian patent linkage regulations require generics to address listed patents before receiving final approval, but the consequences and remedies differ.

Japan has a different generic substitution culture and regulatory system; Japan’s generic penetration historically lagged far behind the United States and Europe, though this has changed somewhat as Japanese policymakers pushed generic adoption to control healthcare costs.

API Sourcing and the China/India Connection

The economics of the U.S. generic market are intimately connected to the global active pharmaceutical ingredient (API) supply chain. The majority of APIs for generic drugs sold in the United States are manufactured in India or China, where manufacturing costs are a fraction of U.S. levels.

FDA inspection of overseas API manufacturers has been a persistent challenge. The FDA’s 2019 inspection of Sun Pharmaceutical’s Halol facility in India — which resulted in import alerts affecting generic products in the U.S. market — is one of many examples where manufacturing quality issues at overseas facilities have disrupted generic supply. Warning letters, import alerts, and facility-level consent decrees have collectively affected a significant portion of the generic supply chain in recent years.

The COVID-19 pandemic focused significant political attention on API supply chain concentration in India and China. Drug shortages — for generic drugs whose patent protection had long since expired and whose prices were too low to support U.S. domestic manufacturing — prompted legislation and executive orders aimed at incentivizing domestic API production. The BIOSECURE Act and related legislative proposals reflect congressional concern about pharmaceutical supply chain security. Whether those policies produce lasting manufacturing reshoring, or simply add costs without meaningfully diversifying the supply chain, is a question the industry will spend the next decade answering.

Part XIV: Looking Forward — Policy Debates and Industry Trends

Drug Pricing Legislation and Generic Competition

The Inflation Reduction Act of 2022 (IRA) introduced Medicare drug price negotiation for the first time. While the IRA’s primary mechanism targets branded drugs whose prices the government negotiates directly, it interacts with generic competition in complex ways.

A drug that is subject to IRA negotiation — and has its price reduced pursuant to that process — may face a different competitive dynamic at loss of exclusivity. If the branded price has already been significantly compressed by government negotiation, the gap between brand and generic prices is smaller, potentially reducing the commercial attractiveness of first-filer exclusivity.

More broadly, the IRA creates incentives for branded manufacturers to focus on drugs where they can obtain maximum pricing before government negotiation kicks in. This may accelerate development of drugs that can command high prices for a short period, followed by earlier acceptance of generic competition — a different calculus than the traditional ‘evergreen and defend’ strategy.

Patent Term Restoration Under Scrutiny

Hatch-Waxman’s patent term restoration provisions — which allow manufacturers to recover up to five years of patent term lost during FDA clinical development and review — have drawn increasing scrutiny. Critics argue that term restoration is applied inconsistently, that manufacturers have gamed the restoration calculation, and that the resulting extended exclusivity contributes to drug pricing problems.

The USPTO’s administration of patent term restoration applications involves complex calculations of the ‘regulatory review period.’ Disputes between applicants and the USPTO over the length of restorable time are common. Federal Circuit litigation on these questions involves statutory interpretation and administrative law questions that do not obviously favor either side.

For generic manufacturers and their counsel, patent term restoration adds another variable to the exclusivity timeline analysis. DrugPatentWatch tracks PTE data for listed patents, allowing generic pipeline analysts to model adjusted expiration dates that account for restoration.

Interchangeable Biosimilars and the Emerging Market

The biosimilar market is positioned for significant growth as the first wave of blockbuster biologics — including major monoclonal antibodies and recombinant proteins — faces biosimilar competition. The 180-day exclusivity for the first interchangeable biosimilar designation represents a smaller but analogous prize to the small-molecule equivalent.

Amgen, Pfizer, Samsung Bioepis, Sandoz, and others compete in this space with multi-billion-dollar investments in biosimilar development and manufacturing. The interchangeable designation matters commercially because it enables pharmacy-level substitution in states that permit it — without requiring a prescriber action. Market penetration for interchangeable products has been faster than for non-interchangeable biosimilars in early data.

The biosimilar market structure differs from small-molecule generics in important ways. Manufacturing complexity keeps the number of competitors lower. Payer and PBM formulary decisions, which are heavily influenced by rebate arrangements, determine which biosimilar gets preferred status regardless of whether it carries an interchangeability designation. The first-interchangeable exclusivity advantage may be less decisive than it appears in theory if payer decisions override pharmacy substitution.

Part XV: Synthesis and Strategic Implications

What the System Produces

The Hatch-Waxman Act has, by any quantitative measure, succeeded in its core objective. The United States has one of the world’s highest generic drug penetration rates. Generic drugs account for approximately 90% of prescriptions dispensed in the United States, though they represent only about 20% of drug spending by dollar value [19]. That gap — high volume, low price — is the system working as designed.

The 180-day exclusivity has produced the intended incentive. Generic manufacturers invest in Paragraph IV challenges, in costly litigation, and in complex ANDA development because the prize is real. Without it, the incentive to challenge patents at all would be much weaker, and branded companies’ portfolios of secondary patents would provide longer-lasting protection than they currently do.

The system also generates significant litigation costs, delays market entry for consumers awaiting lower-priced generics, creates incentives for anticompetitive behavior (reverse payments, citizen petition abuse, REMS access restrictions), and has contributed to the financialization of the pharmaceutical industry in ways that are not obviously good for drug development.

Strategic Recommendations for Generic Manufacturers

Any generic manufacturer developing its Paragraph IV pipeline should:

Maintain continuous monitoring of Orange Book listings for target drugs using tools like DrugPatentWatch, and set alerts for new patent listings that could affect approved or pending ANDAs.

Build litigation assessment into ANDA filing decisions from day one — the 30-month stay and litigation costs are part of the product development economics, not an afterthought.

Evaluate PTAB IPR petitions in parallel with district court strategy, using the timing advantages of PTAB proceedings to accelerate patent resolution on favorable cases.

Analyze authorized generic risk for every significant Paragraph IV opportunity, since the economic case changes substantially if the brand can lawfully undercut the exclusivity period.

Track settlement precedent in the relevant therapeutic area, because brands’ willingness to settle, and on what terms, correlates with their experience in prior generic challenges.

Strategic Recommendations for Branded Manufacturers

Branded manufacturers defending against generic entry should:

Audit Orange Book listings regularly for patents that may not meet current listing standards, to avoid delisting challenges and the litigation risk that accompanies them.

Invest in lifecycle management planning at least five years before compound patent expiration — reformulations, new indications, and pediatric programs all require long lead times.

Evaluate authorized generic strategies before patent litigation concludes, since launching an authorized generic can mitigate the commercial impact of first-filer exclusivity but also affects settlement negotiation dynamics.

Monitor PTAB petition activity as an early warning system for which patents are being targeted, since a petition filing often precedes or accompanies an ANDA Paragraph IV challenge.

Key Takeaways

The 180-day first-filer exclusivity is the central commercial prize in U.S. generic drug market entry, worth hundreds of millions of dollars for major drugs, and it rewards the first generic applicant to file a Paragraph IV patent challenge.

Paragraph IV certification transforms an ANDA filing into a patent challenge and triggers a 30-month automatic stay if the brand sues within 45 days — the mechanism that most significantly delays generic market entry.

Reverse payment (pay-for-delay) settlements remain a major antitrust risk area following the Supreme Court’s Actavis decision. Any settlement involving payments from brand to generic must survive rule-of-reason antitrust scrutiny.

PTAB inter partes review proceedings provide a faster and sometimes cheaper path to patent invalidation than district court litigation, but carry estoppel risks that require careful strategic coordination.

Orange Book patent listings are increasingly contested terrain, with FTC enforcement pressure and CREATES Act litigation reshaping how brands can use patent listing and REMS mechanisms to delay generic competition.

Authorized generics — launched by the brand into the market during the 180-day exclusivity window — significantly dilute the commercial value of first-filer status and must be modeled in any Paragraph IV opportunity assessment.

The biosimilar pathway under the BPCIA replicates many Hatch-Waxman principles for biologics, including a first-interchangeable-biosimilar exclusivity period, but operates in a market structure that differs materially from small-molecule generic substitution.

Commercial data tools, including DrugPatentWatch, allow both generic manufacturers and investment analysts to model ANDA pipelines, patent expiration timelines, and litigation risk with granularity that was not available even a decade ago.

FAQ

Q1: Can a generic company that loses a Paragraph IV patent challenge in district court still collect 180-day exclusivity if it eventually wins on appeal?

Yes, in some circumstances. If the district court ruled against the generic applicant but the Federal Circuit reverses that decision, the generic’s ANDA can be approved and the 180-day clock triggered by commercial marketing. However, the practical complication is that other ANDA applicants may have been waiting, the litigation may have settled, or forfeiture conditions may have been triggered during the appellate period. The specific timeline and what events occurred during the district court-to-appellate gap determine whether the exclusivity is still available and collectible. Generic companies often keep their ANDAs technically viable during the appellate period precisely to preserve this optionality.

Q2: What happens if the first-filer generic company is acquired during the pendency of its ANDA litigation — does the acquirer inherit the 180-day exclusivity?

Generally, yes. The 180-day exclusivity attaches to the ANDA application, which is a transferable regulatory asset. Corporate acquisitions typically include assignment of pending ANDAs, and the FDA approves these transfers through the change-of-ownership process. The acquirer steps into the shoes of the original filer and assumes both the rights (including first-filer exclusivity) and the obligations (including the pending litigation). This has driven significant M&A activity — acquiring a company with a robust Paragraph IV pipeline can be a way to purchase future revenue streams that would otherwise require building a litigation infrastructure from scratch.

Q3: Can a brand manufacturer’s pediatric exclusivity attach to a patent that is already subject to a court decision of invalidity?

This is one of the more counterintuitive aspects of Hatch-Waxman. Pediatric exclusivity attaches to the patent term, not to a finding of patent validity. A court ruling that a patent is invalid eliminates the patent — meaning there is no patent term to which pediatric exclusivity can attach. If the patent has not yet been adjudicated invalid (even if litigation is pending), the FDA still treats the listed patent as providing the exclusivity anchor for pediatric purposes. Once a court issues a final ruling of invalidity that is not on appeal, the patent’s effect under the Hatch-Waxman framework is eliminated, and with it, the pediatric exclusivity that ran off of that patent. The interaction between post-trial appeals, stays of judgment, and pediatric exclusivity periods has generated some extremely technical legal disputes.

Q4: How does a ‘skinny label’ strategy allow generic manufacturers to avoid some method-of-use patents?

A skinny label generic (formally, a ‘carve-out’ label) is approved only for the uses not covered by the brand’s method-of-use patents. If the brand’s drug is approved for three indications but only two are patented, the generic can seek approval only for the unpatented indication, avoiding infringement of the method-of-use patents. The FDA’s practice of permitting these carve-outs was designed specifically to allow generic entry despite method-of-use patents on some but not all approved uses. GlaxoSmithKline’s attempt to hold Teva liable for induced infringement of method-of-use patents for Coreg (carvedilol) — even though Teva’s label explicitly carved out the patented indication — produced the Federal Circuit’s 2021 GlaxoSmithKline LLC v. Teva Pharmaceuticals decision [20], which initially found induced infringement and caused significant alarm in the generic industry before a subsequent en banc Federal Circuit softened the holding. The skinny label strategy remains viable but requires careful label drafting and communication strategy.

Q5: How does the Hatch-Waxman 30-month stay interact with PTAB proceedings — can a generic company use a favorable PTAB decision to cut short a district court stay?

A favorable PTAB final written decision finding a listed patent unpatentable does not automatically terminate the 30-month stay. The stay is a creature of the Hatch-Waxman statute and is tied to the resolution of the district court litigation or expiration of the 30-month period, not to the outcome of PTAB proceedings. However, a PTAB finding of unpatentability creates very strong pressure to settle the district court case. The patent owner can appeal a PTAB decision to the Federal Circuit, but pending that appeal, the validity of the challenged claims is in serious doubt. In practice, branded manufacturers often settle district court Hatch-Waxman litigation or agree to license terms relatively quickly after losing at PTAB, because continuing to litigate in district court with an unpatentability finding on the record is strategically difficult. The generic company that uses PTAB strategically — timing its petition filing relative to the district court schedule to maximize settlement leverage — may be able to achieve a resolution that effectively cuts short the stay period through negotiation, even if no formal legal mechanism directly accomplishes this.

References

[1] Hemphill, C. S., & Lemley, M. A. (2011). Earning exclusivity: Generic drug incentives and the Hatch-Waxman Act. Antitrust Law Journal, 77(3), 947–989.

[2] Cuozzo Speed Technologies, LLC v. Lee, 579 U.S. 261 (2016).

[3] Oil States Energy Services, LLC v. Greene’s Energy Group, LLC, 584 U.S. 325 (2018).

[4] FTC v. Actavis, Inc., 570 U.S. 136 (2013).

[5] Federal Trade Commission. (2023). Pharmaceutical supply chain and competition: 2023 report. FTC.gov.

[6] AbbVie Inc. (2023). 2022 Annual report and financial statements. AbbVie Investor Relations.

[7] Creating and Restoring Equal Access to Equivalent Samples Act of 2019, Pub. L. No. 116-94, §610, 133 Stat. 2534 (2019).

[8] U.S. Food and Drug Administration. (2023). Biosimilar product information: Humira biosimilars. FDA Drugs@FDA.

[9] Becton, Dickinson & Co. v. Baxter International, Inc., 22 F. Supp. 3d 888 (N.D. Ill. 2014). See also FTC amicus brief filings re: Orange Book delisting, 2023.

[10] Pfizer, Inc. v. Apotex, Inc., 480 F.3d 1348 (Fed. Cir. 2007).

[11] In re K-Dur Antitrust Litigation, 686 F.3d 197 (3d Cir. 2012).

[12] AstraZeneca AB v. Apotex Corp., No. 01-cv-9351 (D.N.J. 2008).

[13] IQVIA Institute for Human Data Science. (2022). Medicine use and spending in the U.S.: A review of 2021 and outlook to 2026. IQVIA Institute.

[14] Federal Trade Commission. (2011). Authorized generic drugs: Short-term effects and long-term impact. FTC.gov.

[15] Executive Order on Promoting Competition in the American Economy, 86 Fed. Reg. 36,987 (July 14, 2021).

[16] Federal Trade Commission. (2015). FTC v. Cephalon: Settlement requiring $1.2 billion payment. FTC press release.

[17] In re Loestrin 24 Fe Antitrust Litigation, 433 F. Supp. 3d 274 (D.R.I. 2019).

[18] U.S. Food and Drug Administration. (2014). Withdrawal of approval of abbreviated new drug applications for methylphenidate. 79 Fed. Reg. 66,956.

[19] Association for Accessible Medicines. (2023). 2023 generic drug & biosimilars access & savings in the U.S. report. AAM.

[20] GlaxoSmithKline LLC v. Teva Pharmaceuticals USA, Inc., 7 F.4th 1320 (Fed. Cir. 2021), reh’g en banc granted, vacated, 46 F.4th 1373 (Fed. Cir. 2022).