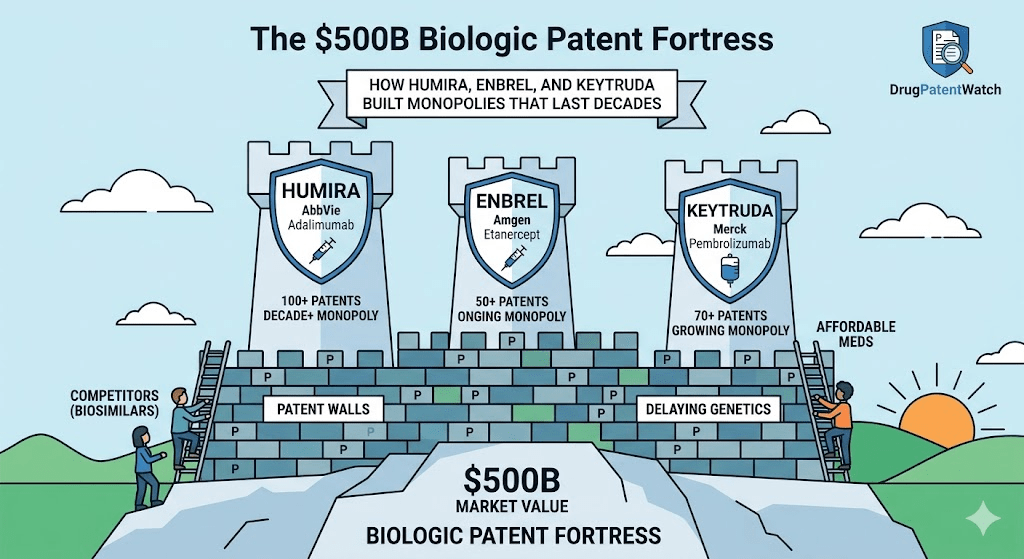

Biologic drugs generate more revenue per product than any other class of medicine. They also carry more patents, attract more litigation, and resist biosimilar competition longer than small molecules—by a factor so large it can only be explained by design, not science. The three drugs that dominate this conversation—adalimumab (Humira), etanercept (Enbrel), and pembrolizumab (Keytruda)—have collectively generated well over $500 billion in cumulative sales while biosimilar challengers spent years in courtrooms instead of pharmacies.

This is not a story about the patent system working as intended. It is a story about how the intersection of biologic science, regulatory exclusivity, BPCIA architecture, and aggressive IP strategy created conditions where monopoly extension is the default outcome, not an exception. For portfolio managers tracking loss of exclusivity timelines, for biosimilar developers planning entry strategy, and for pharma IP teams building or challenging patent estates, the mechanics of this system determine the stakes on every deal, every pipeline asset, and every litigation decision.

Why Biologics Are Different From Small Molecules—and Why That Distinction Defines Everything

The word “biologic” covers a wide category—monoclonal antibodies, fusion proteins, cytokines, blood-derived products, vaccines—but the commercially dominant form is the monoclonal antibody. Drugs like adalimumab, pembrolizumab, trastuzumab (Herceptin), and bevacizumab (Avastin) are all monoclonal antibodies. They work by binding with high specificity to a molecular target, either neutralizing it or triggering an immune response. They are produced in living cell lines—typically Chinese hamster ovary (CHO) cells—inside industrial bioreactors, purified through multi-step chromatography processes, and formulated into a product that must remain stable during storage and administration.

A small molecule like atorvastatin (Lipitor) has a molecular weight around 560 daltons. You can draw its chemical structure on a notepad, synthesize it via established chemistry, and reproduce it identically across batches and manufacturers. A monoclonal antibody like adalimumab exceeds 148,000 daltons. Its three-dimensional folded structure, glycosylation patterns (sugar chains attached to the protein), charge variants, and aggregation profile all affect its safety and efficacy. None of these can be “fully characterized” the way a small molecule can. The analytical toolkit—mass spectrometry, capillary electrophoresis, X-ray crystallography, peptide mapping—can describe the protein with extraordinary precision, but a complete characterization remains impossible by the standards applied to simple chemistry.

This complexity is not incidental. It is the foundation of the entire competitive strategy that follows.

Why ‘The Process Is the Product’ Creates a Patent Goldmine

Regulators recognized early that for biologics, the manufacturing process and the finished product cannot be separated. Minor changes to cell culture conditions—pH, dissolved oxygen, temperature ramps, nutrient feeding strategy—alter the post-translational modifications on the protein and can change how it behaves in the body. A bioreactor running at 36.5°C rather than 37°C may produce a molecule with slightly different glycoforms. The regulatory consequence is that any manufacturing change must go through the FDA’s prior approval or change reporting processes, depending on severity.

From an IP perspective, this creates an enormous patentable surface area. The active ingredient—the antibody sequence itself—is one patent. But the cell line engineered to express it, the specific culture media composition, each purification step, the formulation buffer that keeps the protein stable at room temperature, the auto-injector device that delivers it, the dosage regimen studied in Phase III trials, the new indication approved five years after launch—each of these is a distinct innovation, and each can be separately patented.

Compare this to a generic small-molecule entry. A generic manufacturer of atorvastatin needs to demonstrate pharmaceutical equivalence and bioequivalence. It does not need to replicate the originator’s manufacturing process. It can use any synthetic route that produces the same API. The patentable surface area is narrow: the molecule, maybe a formulation or salt form. For biologics, the patentable surface area is nearly unlimited.

This is why AbbVie ended up with 247 U.S. patent applications on a single drug.

The Dual Shield: How Patents and Regulatory Exclusivity Overlap to Extend Biologics Monopolies

A biologic launched in the United States benefits from two separate and legally distinct systems of market protection. Conflating them is one of the most common errors made in financial modeling, litigation strategy, and policy analysis.

What FDA-Granted Regulatory Exclusivity Actually Means—and What It Doesn’t

Regulatory exclusivity is not a patent. It is a statutory right granted by the FDA upon approval that prevents the agency from accepting or approving a biosimilar application during the exclusivity period. It is a marketing barrier, not a property right. The FDA cannot approve a 351(k) application referencing a biological product for 12 years after that product’s first licensure under the BPCIA. A biosimilar applicant can file its application four years after the reference product’s approval, but the FDA cannot grant approval for another eight years.

The 12-year exclusivity period was the most debated provision in the BPCIA’s passage. Industry, led by brand-side trade groups like PhRMA, pushed for 14 years. Patient advocates and generics manufacturers pushed for 5 or 7 years, arguing that the standard for small molecules (5 years of new chemical entity exclusivity under Hatch-Waxman) was sufficient. Congress settled on 12 years. The Obama administration repeatedly proposed reducing it to 7 years as a budget offset; Congress never acted on it.

By any comparison to the global standard, 12 years is long. The EU grants 8 years of data exclusivity plus 2 years of market protection, for a total 10-year period. Japan operates at 8 years. Canada provides 8 years. The U.S. 12-year figure is the most generous among major pharmaceutical markets and creates a longer competition-free runway than any equivalent framework.

The Menu of Overlapping Exclusivities That Stack on Top of Each Other

Sophisticated lifecycle management involves identifying which of the following can be layered:

Orphan Drug Exclusivity (ODE) grants 7 years of market exclusivity for a biologic designated to treat a rare disease affecting fewer than 200,000 Americans. This designation applies to the specific indication, not the entire molecule. A drug approved for multiple indications can hold orphan exclusivity for some of them while the 12-year biologic exclusivity covers others. Dupilumab (Dupixent), for instance, has accumulated multiple orphan designations across rare skin and pulmonary conditions.

Pediatric Exclusivity (PED) adds six months to all existing patents and exclusivities—not just one. For a drug generating $5 billion annually, six months of additional monopoly pricing is worth $2.5 billion in pre-tax revenue. The FDA requests pediatric studies under the Best Pharmaceuticals for Children Act; completing them earns the bonus regardless of what the studies show. This is not corruption; it is a policy choice to incentivize pediatric data generation. But its financial impact on exclusivity timelines is enormous, and it is routinely exploited.

Gaining Antibiotic Incentives Now (GAIN) exclusivity adds 5 years for qualifying infectious disease biologics, stacked atop existing exclusivities. The GAIN Act was designed to address antibacterial drug development shortfalls, but its scope extends to antifungals and some biologics.

New Clinical Investigation Exclusivity (3 years) applies when a new indication or formulation is supported by new clinical studies essential to approval. This is the vehicle for protecting label expansions—a new patient population, a new dosage form, a combination therapy—beyond the initial 12-year biologics exclusivity window.

The 1-year interchangeable biosimilar exclusivity under the BPCIA is the analogue of Hatch-Waxman’s 180-day first-filer exclusivity. It applies only to the first biosimilar designated interchangeable, and only from the date of commercial marketing, not FDA approval. In practice, few biosimilars have pursued interchangeability designation, limiting the real-world utility of this provision.

Key Exclusivity Periods: Biologic vs. Small Molecule Comparison

Exclusivity Type

Biologic (BPCIA)

Small Molecule (Hatch-Waxman)

Gap

Base Data Exclusivity (New Entity)

12 years

5 years (NCE)

+7 years

Orphan Drug

7 years

7 years

None

Pediatric Bonus

+6 months (on all)

+6 months (on all)

None

New Clinical Investigation

3 years

3 years

None

First Challenger Market Exclusivity

1 year (interchangeable only)

180 days (any Para. IV filer)

Significantly weaker

Global Comparator (EU)

10 years (8+2)

10 years (8+2)

U.S. 2 years longer

How the BPCIA Created the Conditions for Permanent Monopolies

The Biologics Price Competition and Innovation Act of 2010 was written with the Hatch-Waxman Act as a template and an explicit goal of replicating its success in reducing drug costs through generic competition. Hatch-Waxman brought generic penetration from near zero in 1984 to over 90% of dispensed prescriptions by 2020. In terms of biosimilars, the BPCIA has produced a far more modest result over a comparable timeframe. The structural reasons for this gap are not accidents.

Why the BPCIA’s ‘Patent Dance’ Gives Innovators a Strategic Advantage

Under the Hatch-Waxman framework, every patent the brand considers relevant to its drug must be listed publicly in the FDA’s Orange Book. A generic applicant filing a Paragraph IV certification challenges those patents directly. The brand knows exactly what it is defending; the generic knows exactly what it is attacking. Litigation is bounded.

The BPCIA provides no equivalent public list. Instead, it establishes the “patent dance”—a private, multi-step information exchange in which the biosimilar applicant shares its application and manufacturing process information with the innovator, and the innovator responds with a list of patents it believes could be infringed. The biosimilar applicant then responds with its non-infringement and invalidity arguments, and the parties negotiate which patents to litigate in an initial wave.

The Supreme Court confirmed in Sandoz v. Amgen (2017) that this exchange is entirely optional for the biosimilar applicant. A company can file its 351(k) application, notify the innovator 180 days before commercial marketing, and proceed. Skipping the dance means the innovator can sue immediately on any patent in its entire portfolio rather than the negotiated subset. This optionality transforms the dance from a neutral process into a strategic decision with major financial consequences.

For the innovator, the absence of a public list serves as a force multiplier on the patent thicket. Under Hatch-Waxman, the brand must pre-commit to a defined set of listed patents. Under the BPCIA, the brand can hold patents in reserve, asserting them at strategically advantageous moments—after initial litigation has been resolved, after a biosimilar has spent hundreds of millions in manufacturing buildout, or during commercial negotiations when leverage is highest. The “fog of war” this creates is not a design flaw. For innovator companies, it is a core feature.

Why the Absence of an Automatic 30-Month Stay Changes Everything

Under Hatch-Waxman, filing a patent infringement suit within 45 days of a Paragraph IV certification automatically stays FDA approval of the generic for 30 months. This stay is the central mechanism driving generic litigation strategy. It gives the brand a defined period to litigate its strongest patents, and it gives the generic a defined timeline to plan its market entry.

The BPCIA has no equivalent automatic stay. The FDA can approve a biosimilar while patent litigation is ongoing. The innovator cannot prevent approval through litigation; it can only seek an injunction through the courts on a case-by-case basis. This appears to favor biosimilar entry—there is no mandatory 30-month delay triggered by filing a complaint.

The reality is more complex. Without the stay, innovators have no incentive to litigate a small, defined set of key patents early in the biosimilar development timeline. The strategic calculus shifts entirely. The optimal innovation strategy under the BPCIA is not to identify and defend your three best patents—it is to file as many patents as possible, assert as many as you can in litigation, and force the biosimilar developer into a multi-year, multi-patent war of attrition where legal costs, manufacturing delays, and settlement pressure accumulate until the economics of entry no longer pencil out.

The patent thicket, under the BPCIA, is not just a competitive tactic. It is the structurally optimal response to how the law is written.

Why AbbVie’s Humira Patent Strategy Lasted So Long

Humira (adalimumab) was approved by the FDA in December 2002 for rheumatoid arthritis. Its core composition-of-matter patent, covering adalimumab itself, expired in the United States in 2016. Biosimilars did not enter the U.S. market until January 2023, seven years after the core patent fell. That seven-year gap is the direct product of a deliberate and systematic patent thicket construction.

The Anatomy of AbbVie’s 247-Patent Strategy

AbbVie filed 247 patent applications in the United States covering Humira. Of these, at least 132 resulted in granted patents. The portfolio covers adalimumab’s amino acid sequence, the methods used to manufacture it in CHO cells, specific cell culture media compositions, purification process steps, formulation characteristics including concentration and stabilizer selection, the citrate-free formulation approved in 2016, the auto-injector device, the pre-filled syringe, methods of treating rheumatoid arthritis, methods of treating Crohn’s disease, methods of treating psoriasis, dosage regimens, combination therapies, and anti-drug antibody management.

The timing pattern is the most revealing metric. Humira was approved in 2002. A full 89% of its U.S. patent applications were filed after that approval. Between 2014 and 2018—more than a decade after the drug was on market—AbbVie filed 122 additional applications. This is not the filing behavior of a company protecting its original invention. It is the behavior of a company extending its legal footprint around an existing commercial asset.

Key Humira Patent Expiry Dates and Their Strategic Significance

The chronology of Humira’s U.S. patent estate tells the story clearly:

The primary composition-of-matter patent expired in 2016. Had the U.S. operated under European patent standards, biosimilar competition would likely have entered at or near that date, as it did in the EU (October 2018 for European biosimilar entry, just two years after the core patent). Instead, AbbVie’s secondary patent wall—covering manufacturing, formulation, delivery device, and method of use—held U.S. biosimilar entry until a negotiated settlement with all major biosimilar developers. AbbVie reached agreements with Amgen (Amjevita), Samsung Bioepis (Hadlima), Pfizer (Abrilada), Sandoz (Hyrimoz), and others, granting licenses effective January 2023. These were not litigation losses. They were negotiated outcomes, timed to give AbbVie five more years of U.S. monopoly pricing after its core patent expired.

The settlements included royalty payments from biosimilar manufacturers to AbbVie. The royalty terms were not fully disclosed, but analyst estimates placed them in the range of 5–10% of net sales. AbbVie’s secondary patents—the very patents many experts characterized as legally weak—generated ongoing royalty income even after the monopoly ended.

How AbbVie’s EU vs. U.S. Patent Filing Strategy Reveals Intent

One data point cuts through the complexity: AbbVie filed over three times as many patent applications in the U.S. for Humira as it did in Europe. The molecule is the same. The clinical evidence is the same. The manufacturing science is the same. The divergence in patent applications is a direct response to differences in patent law—the U.S. Patent and Trademark Office’s more permissive standards for secondary patents compared to the European Patent Office’s stricter nonobviousness requirements. AbbVie filed where it could obtain patents, not where the inventions were meaningfully different.

The European Patent Office granted far fewer secondary patents on adalimumab, which is why biosimilar entry in Europe preceded U.S. entry by five years. European patients paid lower prices for adalimumab therapies starting in 2018. American patients continued paying list prices north of $80,000 per year until 2023.

The Antitrust Ceiling: Why the Seventh Circuit’s Ruling Matters for Future Thicket Challenges

The 2020 Seventh Circuit ruling in the Humira antitrust litigation is now the controlling precedent for patent thicket challenges. The court held that accumulating a large number of lawfully obtained patents does not constitute an antitrust violation, even when the aggregate effect is to foreclose competition. The court asked rhetorically: “If AbbVie made 132 inventions, why can’t it hold 132 patents?”

This ruling forecloses the most direct legal theory available to biosimilar developers and patient advocates—that the sheer size of a patent portfolio constitutes anticompetitive conduct. Future challengers will need to pursue Walker Process fraud claims (challenging specific patents obtained through deception of the USPTO) or sham litigation claims (arguing specific infringement suits lacked objective basis), both of which carry extremely high evidentiary burdens. The Humira precedent has materially reduced the antitrust risk for any innovator company building a comparable portfolio.

How Amgen Built a 37-Year Monopoly Around Enbrel

Enbrel (etanercept) is a fusion protein—not a monoclonal antibody—that combines the extracellular domain of the TNF receptor with the Fc region of human IgG1. It was initially developed by Immunex and approved in 1998. Amgen acquired Immunex in 2002, inheriting the product and, crucially, a set of pre-TRIPS patent applications that would later become the cornerstone of a monopoly extending to 2029.

The Pre-TRIPS Patent Strategy That Locked Out Enbrel Biosimilars Until 2029

Under U.S. patent law prior to the Uruguay Round Agreements Act (1994), patents granted a term of 17 years from date of issuance, not 20 years from filing. This distinction matters enormously when a company files an application early—say, in the early 1990s—and prosecutes it slowly through the patent office. Applications filed before June 8, 1995 could elect the longer of the pre-TRIPS 17-year-from-issuance or post-TRIPS 20-year-from-filing term.

Roche filed a patent application covering etanercept’s manufacturing process in the early 1990s. Amgen, after acquiring the relevant rights, prosecuted continuation applications derived from that family. Two resulting patents were issued in 2011 and 2012—decades after the original filing, but benefiting from the pre-TRIPS rule. Under that rule, these patents expire in 2028 and 2029, respectively. A patent family filed around 1992, prosecuted strategically across 20 years, yields protection running to 2029. That is 37 years of total market protection from original filing.

This is not a loophole. It is the law as written. Amgen did not invent the pre-TRIPS filing; it acquired it as part of the Immunex transaction and then managed the prosecution clock deliberately. The outcome is that Sandoz’s Erelzi—FDA-approved as an etanercept biosimilar in 2016—still has not launched commercially in the United States as of 2026. Amgen sued Sandoz for patent infringement; courts upheld the patents; the Supreme Court declined to take the case. A fully approved, lower-cost alternative has sat on the shelf for nearly a decade.

Revenue Exposure and the Enbrel Patent Cliff: What Investors Are Watching

Enbrel generated approximately $3.7 billion in U.S. net product revenues in 2023, down from peak sales but still a top-ten revenue contributor for Amgen. The drug’s U.S. revenue is almost entirely insulated from biosimilar competition until the late-expiring patents fall in 2028–2029. After that, the entry dynamic is likely to be swift. Pfizer has a fully developed co-promotion relationship with Enbrel in some markets and an understanding of the prescriber base. Sandoz’s Erelzi is ready to launch commercially within months of legal clearance. Samsung Bioepis’s SB4 (Benepali) is already marketed in Europe.

The 2028–2029 loss of exclusivity for Enbrel represents a potential rapid erosion from $3–4 billion in annual U.S. revenue. Historical biosimilar entry patterns for monoclonal antibodies in the U.S. show 40–60% volume erosion within 12 months of the first competitor launch, with further erosion when interchangeable designation or pharmacy substitution legislation accelerates switching. For Amgen’s portfolio, Enbrel’s revenue cliff is manageable only because Enbrel’s patent wall delayed it long enough for Amgen to build a post-Enbrel revenue base around Repatha (evolocumab), Otezla (apremilast), and its biosimilars business.

Why Keytruda’s Patent Expiry Matters for Merck Investors

Pembrolizumab (Keytruda) is the world’s best-selling drug by revenue, generating approximately $25 billion globally in 2023, equivalent to roughly 42% of Merck’s total pharmaceutical sales. Its mechanism—blocking PD-1, a protein that cancer cells exploit to suppress immune response—has demonstrated clinical activity in more than 20 tumor types, earned approval across dozens of indications, and established pembrolizumab as the backbone of combination oncology regimens worldwide. The revenue concentration in a single molecule is extraordinary and unprecedented in modern pharmaceutical history. The patent strategy around it reflects that exposure.

Keytruda’s Key Patent Expiry Dates and the 2028 Revenue Cliff

Keytruda’s primary patents in the United States are projected to expire around 2028. The composition-of-matter patents covering pembrolizumab itself were filed in the late 2000s, following Merck’s acquisition of Schering-Plough in 2009, which brought in the asset (originally developed as SCH 900475). Method-of-treatment patents covering specific indications extend several years further. Merck has pursued secondary patents aggressively—as of 2021, 129 U.S. patent applications had been filed, producing 53 granted patents, with 74% covering secondary features rather than the core antibody.

The projected patent expiry creates a $25 billion revenue exposure with a concentrated timeline. No drug in history has entered loss of exclusivity at this revenue scale. Humira peaked near $21 billion globally before biosimilar erosion. Keytruda will enter its exclusivity cliff from a higher base, and the biosimilar competitive response is already being prepared by companies including Samsung Bioepis, Fresenius Kabi, and Celltrion.

How Merck’s Subcutaneous Formulation Strategy Could Delay Keytruda Biosimilar Competition

The most significant element of Merck’s Keytruda lifecycle management strategy is the development and approval of a subcutaneous (SC) formulation. The IV formulation requires hospital or clinic administration over approximately 30 minutes; the SC version can be self-administered in roughly 90 seconds. The clinical convenience improvement is real. So is the patent extension it enables.

The SC formulation uses a technology for enhanced subcutaneous delivery—specifically, the use of hyaluronidase to break down the extracellular matrix and allow larger volumes of drug to be injected subcutaneously. Merck licensed this technology from Halozyme Therapeutics under its ENHANZE platform. In April 2025, Halozyme sued Merck for patent infringement, claiming the SC pembrolizumab product infringes Halozyme patents beyond the scope of the existing license agreement. This litigation is pending and introduces genuine uncertainty into Merck’s subcutaneous strategy.

If the SC formulation succeeds—both commercially and in litigation—it provides a platform for switching the bulk of Keytruda’s patient volume away from the IV formulation before the IV patents expire. Biosimilar developers benchmarking against the IV reference product would then face a market where the majority of prescribing has shifted to the SC version, which carries its own new patent set. This is a textbook product hop. The clinical benefit (convenience) is genuine, but the commercial timing—pushed hard just ahead of the IV patent cliff—reflects strategic intent as much as patient-centered innovation.

The BMS/Ono $625 Million Settlement: What the Anti-PD-1 Patent War Cost Merck

The foundational science behind PD-1 blockade dates to work by Tasuku Honjo at Kyoto University, for which he received the 2018 Nobel Prize. Bristol-Myers Squibb and its partner Ono Pharmaceutical held key patents on the therapeutic use of anti-PD-1 antibodies. Merck’s development of pembrolizumab implicated those patents, and in 2017, the parties settled litigation with Merck paying $625 million upfront and agreeing to ongoing royalties on Keytruda sales through 2026. At $25 billion in annual revenue, even a modest royalty rate generates hundreds of millions in annual payments.

This settlement illustrates a structural feature of high-value biologic markets: multiple patent holders can hold blocking positions across a therapeutic mechanism. Any developer entering PD-1 oncology, whether as an innovator or a biosimilar developer, must account for overlapping IP held by the original mechanism patent holders, the molecule patent holders, and the indication patent holders. These layers are not additive; they are multiplicative in their complexity.

Which Biosimilar Developers Are Positioned to Challenge Keytruda After 2028

The Keytruda biosimilar development pipeline is active. Samsung Bioepis has SC and IV candidates in development. Fresenius Kabi, which has a track record in oncology biosimilars (including a trastuzumab biosimilar marketed as Ogivri), has pembrolizumab development programs underway. Celltrion, which successfully launched infliximab and trastuzumab biosimilars in multiple markets, has pembrolizumab in its pipeline. Shanghai Junshi Biosciences’ toripalimab, approved by the FDA for nasopharyngeal carcinoma, is a different anti-PD-1 molecule that competes in some indications but is not a biosimilar.

The commercial challenge for pembrolizumab biosimilar developers goes beyond patent clearance. Keytruda’s clinical database—the evidence base supporting more than 20 approved indications—took Merck 15 years to assemble. A biosimilar approved via totality-of-evidence analytical comparison will carry the reference product’s labeling, but payer and physician confidence in indication-specific activity requires ongoing clinical data generation. For oncology biosimilars more than any other class, the soft barriers of prescriber hesitancy and payer formulary inertia matter as much as the hard barriers of patent litigation.

How Patent Thickets Work: The Mechanics of Evergreening in Biologics

A patent thicket is the outcome of systematic evergreening—the practice of filing secondary patents on incremental modifications to an existing approved drug with the explicit goal of extending the commercial monopoly beyond the expiry of primary patents. The process is not illegal. Many of the individual patents within a thicket are legitimately granted. The anticompetitive effect comes from their combination and from the cost structure of challenging them.

The Six Categories of Secondary Patents That Build a Biologic Thicket

Secondary patents in biologic thickets fall into predictable categories. Understanding each clarifies which types are most likely to be challenged, most likely to be upheld, and most strategically important to the innovator.

Formulation patents cover the specific composition of the drug product—the concentration of active ingredient, the choice of buffering agent, the addition of a stabilizer like polysorbate 80, the exclusion of an excipient like citrate (AbbVie’s citrate-free formulation was a specific strategy to differentiate the product and create a new patent layer). AbbVie’s citrate-free Humira, approved in 2016, carried a new patent family and became the version used in biosimilar interchangeability switching studies, creating a technical barrier for biosimilars that had been developing against the citrate formulation.

Manufacturing process patents cover cell line engineering, bioreactor operation parameters, harvest timing, chromatography resin selection, viral inactivation steps, and ultrafiltration/diafiltration procedures. Because these are proprietary to each manufacturer and essential to product quality, they are genuinely inventive in many cases. They are also extremely difficult to design around without compromising product quality or incurring regulatory risk.

Device and delivery patents cover auto-injectors, pre-filled syringes, needle safety systems, and the human factors engineering studies submitted to the FDA. These are often among the weakest patents in a thicket—a different auto-injector design may be entirely acceptable to regulators—but they require investment by the biosimilar developer to develop and validate an alternative device, and they add cost and time to the development program.

Method-of-treatment patents covering new indications are filed after post-marketing clinical studies demonstrate efficacy in additional diseases. Adalimumab’s label grew from rheumatoid arthritis at approval to include Crohn’s disease, ulcerative colitis, plaque psoriasis, psoriatic arthritis, ankylosing spondylitis, juvenile idiopathic arthritis, hidradenitis suppurativa, and uveitis. Each new indication added a method-of-treatment patent that, while not preventing a biosimilar from seeking approval for non-patented indications, complicates the product’s commercial positioning and label negotiations.

Dosage regimen patents cover specific administration schedules—once weekly, every other week, weight-based dosing, titration regimens—studied in dedicated clinical trials. For Humira, separate dose regimens for different indications are individually patented. A biosimilar approved for the same indications must typically replicate or bridge to these regimens.

Continuation and continuation-in-part applications are the procedural mechanism through which thickets grow over time. A continuation application claims the benefit of an earlier patent’s filing date while adding new claims. AbbVie’s approximately 80% “non-patentably distinct” continuation patents on Humira—patents where the claims were not meaningfully different from already-granted patents but were filed to maximize the number of assets in the portfolio—represent a use of continuation practice that patent reform proposals have specifically targeted.

The Cost Arithmetic That Makes Thickets Work

Challenging a single patent through Inter Partes Review (IPR) at the Patent Trial and Appeal Board costs roughly $300,000 to $800,000 in legal fees. A District Court patent litigation trial costs $5 million to $15 million per side, excluding appeals. A comprehensive challenge to a 100-patent thicket through litigation and IPR could cost a biosimilar developer $500 million to $1.5 billion before the first commercial unit ships.

A biologic manufacturing facility capable of commercial-scale production costs $200 million to $600 million to build and validate. A Phase I/Phase III biosimilar clinical program costs $100 million to $400 million. Total biosimilar development and launch costs for a major biologic run $250 million to $1 billion before any patent challenge costs are included.

The economics only work for high-revenue reference products. Biosimilar development for drugs generating less than $1 billion in U.S. annual revenues is often commercially unviable when patent thicket litigation costs are factored in. This is a structural market failure: the drugs most amenable to a single large thicket (blockbuster biologics) attract biosimilar development despite the costs; drugs with moderate revenues do not, even when their patents have expired.

Key Biologic Patent Expiry Dates and Revenue Cliffs Through 2030

The following drugs face material patent expiry events through the end of the decade. Each represents a revenue cliff for the innovator and a potential market entry opportunity for biosimilar developers.

Drug (INN)

Brand

Innovator

U.S. Annual Revenue (est.)

Key Patent Expiry

First Potential Biosimilar Entry

Therapeutic Class

Pembrolizumab

Keytruda

Merck

~$25B (global)

2028

2028–2036 (SC product hop risk)

Oncology / PD-1

Etanercept

Enbrel

Amgen

~$3.7B (U.S.)

2028–2029

2029

Immunology

Ustekinumab

Stelara

J&J

~$6B (global)

2023 (EU) / 2023–2025 (U.S.)

2025

Immunology

Dupilumab

Dupixent

Sanofi/Regeneron

~$14B (global)

2031–2035

Post-2031

Dermatology/Allergy

Aflibercept

Eylea

Regeneron

~$5B (U.S.)

2023–2024

2024–2025

Ophthalmology

Ibrutinib

Imbruvica

AbbVie/J&J

~$4B (U.S.)

2027–2036

Post-2027

Oncology

Nivolumab

Opdivo

BMS

~$9B (global)

2026–2028

Post-2026

Oncology / PD-1

Secukinumab

Cosentyx

Novartis

~$6B (global)

2025–2029

2025+

Immunology

Ustekinumab (Stelara) is the most immediate large-molecule loss of exclusivity event. J&J reached settlement agreements with multiple biosimilar developers, and Amgen’s Wezlana launched in early 2025 as the first interchangeable ustekinumab biosimilar. The commercial erosion pattern will provide a benchmark for how rapidly a $6 billion biologic loses revenue under competitive biosimilar pressure.

Dupilumab is the most forward-looking large-scale patent cliff. Sanofi and Regeneron’s IL-4/IL-13 inhibitor has expanded into atopic dermatitis across all age groups, asthma, chronic rhinosinusitis with nasal polyps, eosinophilic esophagitis, and prurigo nodularis. The patent estate is being actively built; primary composition-of-matter patents expire around 2031–2035. At $14 billion and growing, the eventual biosimilar entry scenario makes Keytruda’s cliff look small by comparison.

How Biosimilar Launch Timing Works: From FDA Approval to Commercial Entry

FDA approval and commercial launch are different events, often separated by months or years of additional litigation. Understanding this distinction is essential for financial modeling biosimilar impact.

The Gap Between FDA Approval and Actual Market Entry

Erelzi (etanercept biosimilar, Sandoz) was approved by the FDA in 2016. It has not launched commercially in the U.S. as of 2026. This is the most extreme example, but it is not unique. Zarxio (filgrastim-sndz, Sandoz), the first U.S. biosimilar approved under the BPCIA, was approved in March 2015 and launched in September 2015—a relatively short gap because Amgen’s key filgrastim patents had already expired. The contrast between Zarxio’s six-month gap and Erelzi’s ongoing delay illustrates the singular importance of patent clearance to commercial timing.

For major biosimilar developers planning a launch, the operative question is not “when will FDA approve our application?” but “when will we have patent certainty sufficient to launch commercially without existential damages exposure?” The at-risk launch decision—launching after FDA approval but before final patent resolution—is one of the highest-stakes decisions in pharmaceutical strategy. Apotex launched its at-risk clopidogrel generic in 2006, leading to $1.1 billion in damages. The biosimilar scale is larger.

How the First Interchangeable Biosimilar Exclusivity Affects Entry Strategy

The BPCIA’s 1-year exclusivity for the first interchangeable biosimilar is strategically underutilized because the evidentiary burden for interchangeability is high. Switching studies demonstrating equivalent outcomes when patients alternate between reference product and biosimilar are expensive and time-consuming to design and conduct. Nonetheless, the first mover to achieve interchangeability for a major biologic gains meaningful commercial advantages. Pharmacy-level substitution, which is automatic for interchangeable products in most states without prescriber notification, is the single largest driver of biosimilar market share after patent clearance. Without interchangeability, adoption requires active prescriber switching—a much slower and more expensive commercial process.

For investors evaluating biosimilar companies, the interchangeability pipeline is a key differentiator. Biocon Biologics, Amgen (which has a large and growing biosimilars portfolio), Samsung Bioepis, Fresenius Kabi, Pfizer, and Sandoz have the scale to pursue interchangeability designations. Smaller biosimilar developers typically cannot.

What Happens Financially After Biologics Lose Exclusivity: Revenue Erosion Patterns

The financial consequences of loss of exclusivity for a major biologic differ meaningfully from small-molecule generic entry patterns.

Why Biologic Revenue Erosion Is Slower Than Generic Drug Erosion

Small-molecule generic entry is rapid and brutal. When the first generic launches under Hatch-Waxman’s 180-day exclusivity, brand market share typically collapses 80–90% within 12 months. The generic is pharmaceutical identical, costs far less to manufacture, and pharmacists can substitute automatically. Price competition drives rapid share transfer.

Biologic biosimilar entry follows a different pattern. In the first year of biosimilar availability, brand share erosion often ranges from 20–40% rather than 80–90%. The reasons are structural. Prescribers have established protocols for administering the reference product and may resist switching stable patients. Payers must update formularies and manage prior authorization criteria for biosimilar substitution. Specialty pharmacy networks built around the reference product require reconfiguration. Innovator companies use patient support programs, co-pay assistance, and bundled rebates to maintain patient volume.

Humira’s first year of U.S. biosimilar competition (2023) produced lower-than-expected biosimilar share, partly due to the reference product’s heavy rebate contracting with PBMs and payers. AbbVie entered the biosimilar era with its rebate strategy already in place, having spent years negotiating formulary exclusivity agreements that made it economically unattractive for payers to cover the biosimilars at list price. By 2024, biosimilar share had increased substantially as payer contracts renewed, but AbbVie’s revenue decline was cushioned by a higher rebated net price on the remaining reference product volume and by transition into its new immunology products—skyrizi (risankizumab) and rinvoq (upadacitinib).

The Rebate Wall: AbbVie’s Post-LOE Strategy for Humira

The FTC has examined “rebate walls” as a separate category of anticompetitive conduct from patent thickets. A rebate wall works as follows: an innovator offers a payer or PBM a substantial rebate on its reference biologic on the condition that biosimilars are not given preferred formulary status. Because the reference product’s list price is high, the rebate value of formulary exclusivity is large enough that payers often find it economically rational to exclude the lower-cost biosimilar. This is not patent protection; it is commercial contracting. But the effect on biosimilar adoption and patient access is similar.

The FTC’s 2023 report on rebate walls found that this practice was prevalent in the adalimumab market and delayed meaningful biosimilar price competition. The practical consequence for investors is that even after patent thickets fall, commercial thickets can persist for 12–24 months until payer contracting cycles turn over.

Why Manufacturing Complexity Matters for Biologic Competitive Moats

For institutional investors evaluating whether a biologic franchise is defensible beyond its patent expiry, manufacturing complexity is a real, though often underweighted, factor. It does not provide legal protection, but it creates time, cost, and quality barriers that limit the number of credible biosimilar challengers.

The CHO Cell Line Problem and Its Implications for Biosimilar Entry

Most therapeutic monoclonal antibodies are produced in CHO cell lines. Developing a biosimilar requires generating a separate, independently derived cell line that expresses the same antibody sequence. The CHO cell line development, screening, and banking process takes 18–24 months before clinical manufacturing can begin. Cell line characterization, genetic stability testing, and master/working cell bank validation are extensive regulatory requirements. Each step is documented in the biosimilar’s Chemistry, Manufacturing, and Controls (CMC) section of the 351(k) application.

The resulting biosimilar molecule will have a slightly different glycosylation profile than the reference product because it is produced in a different cell. The totality-of-evidence assessment determines whether these differences affect clinical performance. For most monoclonal antibodies, minor glycosylation differences do not produce clinically meaningful differences—which is why the analytical characterization approach works. But the manufacturing investment required before that determination can even be made is substantial, and errors in cell line selection or characterization can invalidate years of development work.

Manufacturing process patents are therefore both a legal and a commercial barrier. They legally prevent certain manufacturing approaches and commercially signal that the innovator’s process represents the technically validated approach, adding regulatory risk to any design-around strategy.

Fill-Finish and Cold Chain Complexity as Competitive Moats

The final manufacturing steps for a biologic—filling the formulated drug product into vials, pre-filled syringes, or auto-injector cartridges under sterile conditions—require specialized aseptic manufacturing capability. Not all CDMOs have the capacity to run large-volume pre-filled syringe fills at commercial scale. Auto-injector assembly requires precision manufacturing environments. Cold chain distribution for biologics that must be stored at 2–8°C requires specialized logistics infrastructure.

These operational requirements create real competitive barriers to entry that are independent of patent protection. A biosimilar developer that lacks manufacturing partnerships with qualified fill-finish CDMOs faces material commercial execution risk even after patent clearance and FDA approval. This is one reason why large integrated pharmaceutical companies—Amgen, Pfizer, Sandoz—have structural advantages in biosimilar development over specialized biosimilar players.

Biosimilar Interchangeability: What the FDA Requires and Why It Matters Commercially

The FDA’s interchangeability designation is the regulatory threshold that enables pharmacy-level substitution without prescriber involvement. It is the single greatest commercial accelerant for biosimilar market penetration. Yet fewer than 10 biosimilars had received interchangeable designation as of early 2026, out of more than 40 approved biosimilar products.

Why So Few Biosimilars Pursue Interchangeability

The additional evidentiary requirement is a switching study: a clinical trial in which patients are alternated between the reference product and the biosimilar to demonstrate that alternation does not produce different outcomes compared to continuous reference product use. This study design is expensive, requires a dedicated protocol development and IND filing, and takes 18–24 months to execute and analyze. For a biosimilar already approved as “highly similar” and clinically non-inferior to the reference product, the switching study requirement can feel redundant—a regulatory hurdle that adds $30–80 million in cost without changing the clinical or scientific conclusion.

The FDA has acknowledged this tension and has signaled flexibility in how switching studies can be designed—shorter duration, smaller sample size, crossover designs—without compromising the evidentiary standard. But the burden remains higher than a standard biosimilar development program, and companies making the investment must believe the commercial premium from pharmacy substitution is worth the additional cost and time.

For ustekinumab (Stelara) biosimilars, Amgen’s Wezlana achieved interchangeability. For adalimumab, Cyltezo (Boehringer Ingelheim) and Hadlima (Samsung Bioepis) achieved interchangeability designations. These products immediately became preferred by pharmacy benefit managers seeking to drive automatic substitution. The commercial reward was visible within quarters of interchangeability designation.

How the Global Patent Thicket Varies: U.S. vs. EU vs. Canada

The patent thicket problem is an American phenomenon in its severity, though it exists in attenuated form in other markets.

Why European Biosimilars Launch Earlier Than U.S. Biosimilars

The European Patent Office applies stricter standards for novelty and inventive step than the USPTO. Secondary patents covering obvious modifications—a new salt form, a minor concentration change, a different excipient—are rejected at higher rates in Europe. This means the patent thicket around a European biologic is smaller in absolute terms than the U.S. equivalent, and individual patents within it face higher legal challenge risk.

A comparative analysis published in Health Affairs found that biosimilars faced nine to twelve times more asserted patents in the U.S. than in Canada and the United Kingdom. The Humira portfolio illustrates this: AbbVie filed over three times as many patent applications in the U.S. as in Europe. The molecule is identical. The science does not change across jurisdictions. The patent strategy does.

The EMA’s biosimilar framework also treats biosimilars as interchangeable upon approval—there is no separate interchangeability designation or higher evidentiary standard. This removes one of the U.S. market’s additional barriers to rapid biosimilar uptake.

The practical consequence: Humira biosimilars launched in Europe in October 2018. They launched in the U.S. in January 2023. This five-year gap was not driven by science, manufacturing readiness, or regulatory efficacy concerns. It was driven by patent strategy and litigation costs.

How Paragraph IV Litigation Compares to BPCIA Patent Disputes

For professionals transitioning from Hatch-Waxman litigation to BPCIA matters, the structural differences in how patent disputes are initiated, conducted, and resolved require significant recalibration.

Key Differences Between Paragraph IV and BPCIA Patent Challenges

Under Hatch-Waxman, a generic filer’s Paragraph IV certification is a legal declaration that each listed Orange Book patent is invalid, unenforceable, or not infringed by the generic product. The innovator then has 45 days to file suit, triggering the automatic 30-month stay. The battlefield is defined in advance by the Orange Book list. Both parties know exactly which patents are at issue from day one.

Under the BPCIA, the equivalent action is the biosimilar applicant’s notice of commercial marketing, given 180 days before launch. At this point, the innovator can seek an injunction in federal court against the commercial launch. But the patent dispute timeline begins earlier, in the patent dance exchange. The biosimilar applicant provides manufacturing information; the innovator responds with its patent list; the parties negotiate which patents to litigate in the first wave. If the biosimilar applicant skips the dance, the innovator can immediately sue on all potentially infringed patents upon receiving notice of commercial marketing.

The absence of a defined public list means BPCIA litigation is typically broader, with more patents asserted, longer dockets, and more complex fact patterns. Innovator companies routinely assert 30–60 patents in initial BPCIA lawsuits; under Hatch-Waxman, the typical Orange Book list covers 5–15 patents. The litigation economics are correspondingly different.

What Reforming the BPCIA Could Mean for Biologic Revenue Models

Legislative and regulatory reform proposals are active in multiple venues. The commercial implications for innovator and biosimilar companies are material.

The Affordable Prescriptions for Patients Act: Patent Assertion Caps and Their Revenue Impact

The Affordable Prescriptions for Patients Act (S. 150) would cap the number of patents an innovator can assert in BPCIA litigation to 20 (excluding certain manufacturing patents). The Congressional Budget Office estimated this reform would accelerate biosimilar entry and produce modest but real drug spending reductions.

From an investor perspective, a patent assertion cap materially changes the litigation economics. If AbbVie had been capped at 20 patents in Humira litigation rather than over 100, the litigation cost asymmetry would have narrowed. The biosimilar developers’ legal cost per challenged patent would have been lower; the innovator’s ability to sustain a war of attrition would have been reduced. The settlement dynamics—timing and royalty terms—would have shifted accordingly.

Assessing whether S. 150 or equivalent legislation will pass requires monitoring Senate Judiciary Committee hearings, FTC enforcement posture, and whether bipartisan consensus on pharmaceutical pricing reform is achievable. As of mid-2026, reform efforts remain active but not enacted.

USPTO Patent Quality Initiatives and Their Effect on Secondary Patent Grant Rates

The USPTO and FDA collaboration on pharmaceutical patent quality—designed to reduce secondary patent grants for obvious modifications—is a slower but potentially more durable reform pathway. If the grant rate for continuation applications covering minor reformulations declines, the thicket construction toolkit becomes narrower. This would not affect existing patents already granted but would limit the growth of thickets around drugs currently in development or early commercialization.

Common Investor Questions

How should investors model loss of exclusivity timing for a biologic with a large patent thicket?

The core patent expiry date is a starting point, not a forecast. Model a range of scenarios based on the number of secondary patents remaining at time of primary expiry, the litigation history of the innovator (aggressive defenders vs. early settlers), the number and financial resources of biosimilar developers with active development programs, and the historical pattern of settlements with royalty-bearing licenses. The Humira precedent suggests that even a dense thicket tends to resolve through negotiated settlement, but settlement timing is highly uncertain and deal-specific.

Which biosimilar developers are most likely to succeed commercially after patent entry?

Scale, manufacturing capability, commercial infrastructure, and interchangeability pursuit are the four differentiating factors. Amgen Biosimilars, Pfizer, Sandoz, Samsung Bioepis, and Biocon Biologics have the integrated capabilities to develop, manufacture, and commercially distribute biosimilars at scale. Smaller, pure-play biosimilar developers often partner with larger organizations for commercial launch.

Does the product hop strategy actually work from a commercial perspective?

The evidence is mixed. A product hop that provides genuine clinical benefit—longer duration of action, reduced administration burden, improved tolerability—can drive rapid patient migration and is supported by prescribers on clinical grounds. A product hop that delivers only marginal convenience improvements may face payer resistance if the new formulation carries a premium price. Merck’s SC pembrolizumab product will be a major test case. If payers contract at reference pricing for the SC product rather than paying a premium, the commercial and IP moat is preserved. If they push back on price or mandate IV continuation for stable patients, the strategy’s value is diluted.

What does the FTC’s current enforcement posture mean for biologic innovators?

The FTC under its current leadership has been more aggressive in examining anticompetitive pharmaceutical practices—rebate walls, sham litigation, improper patent listing—than in prior administrations. The Humira antitrust litigation precedent limits the most direct route of attack (sheer portfolio size), but the FTC is pursuing enforcement on adjacent theories. Innovator IP teams building thickets should expect more aggressive FTC scrutiny of individual patents obtained through continuation practice and of patent assertion strategies characterized as objectively baseless.

Investment Strategy: How to Position Around the Biologic Patent Cliff

The $200-plus billion in biologic revenue facing patent expiry through 2030 creates investment implications on both sides of the competitive dynamic.

For long positions in biosimilar developers, the best risk-adjusted opportunities are companies with interchangeability programs underway, manufacturing scale sufficient to compete commercially, and patent-cleared or near-cleared entry timelines for large-revenue reference products. The Stelara (ustekinumab) biosimilar market is the immediate test case. Eylea (aflibercept) biosimilars—following Regeneron’s Eylea HD (high-dose aflibercept, 8 mg) product hop—represent another active battleground. The Keytruda cliff, still 2–3 years away, requires monitoring for Halozyme litigation resolution and SC product hop commercial success.

For positions in innovator companies, the durability of revenue against biosimilar competition depends on how well the loss of exclusivity is managed commercially rather than just legally. AbbVie’s skyrizi and rinvoq revenue ramp is the model. Merck’s Keytruda cliff is the next major stress test, and the company has no equivalent single replacement in its current pipeline at comparable revenue scale.

For credit analysis, the patent cliff timeline for a company’s top revenue product is the single most important variable in assessing medium-term cash flow risk. A biologic generating 40% of company revenue facing loss of exclusivity in three years with no settled biosimilar agreement in place represents substantial refinancing and dividend risk, regardless of how strong the core patents look on paper.

Key Takeaways

The 12-year regulatory exclusivity under the BPCIA is not the ceiling on biologic market protection—it is the floor. The patent thicket construction that happens during and after that exclusivity period determines the actual competitive timeline, which routinely extends 20–35+ years from first approval.

The structural design of the BPCIA—no public patent list, no automatic 30-month stay, weak first-filer exclusivity for biosimilars—incentivizes innovators to build large, dense patent portfolios as their primary competitive defense. This is a rational response to the legal architecture, not a dysfunction of individual bad actors.

The U.S. patent thicket problem is not universal. It is an artifact of specific American policy choices: permissive USPTO secondary patent grant rates, BPCIA structural gaps, and the absence of early patent challenge mechanisms available in the UK, Canada, and the EU. European biosimilars launch earlier not because the science is different but because the legal system is.

The Seventh Circuit’s Humira antitrust ruling has effectively closed the most direct legal route for challenging patent thickets on aggregate-size grounds. Future challenges must proceed patent-by-patent through IPR, ex parte reexamination, or Walker Process fraud claims—each of which is slower and more expensive than a class-wide antitrust theory.

The Keytruda patent cliff, arriving around 2028 from a $25 billion revenue base, is the largest single loss-of-exclusivity event in pharmaceutical history. Its resolution—through biosimilar entry, SC product hop, litigation, or some combination—will define the commercial template for large-molecule oncology competition for the next decade.

Frequently Asked Questions

What is the difference between a biosimilar and an interchangeable biosimilar?

A biosimilar meets the FDA’s standard of being “highly similar” to the reference product with “no clinically meaningful differences” in safety, purity, or potency. An interchangeable biosimilar meets that standard and additionally demonstrates through switching studies that alternating between the biosimilar and the reference product produces the same clinical results as staying on one product continuously. Only interchangeable biosimilars can be substituted at the pharmacy level without prescriber involvement, which is the primary driver of rapid market share capture.

Why did Humira biosimilars launch in Europe five years before the United States?

Europe’s core Humira patent expired in 2016. The European Patent Office granted far fewer secondary patents on adalimumab than the USPTO, and those that were granted faced successful validity challenges from biosimilar developers. The U.S. secondary patent portfolio—247 applications, over 132 granted patents—created a litigation barrier that biosimilar developers addressed through settlement agreements rather than patent invalidation, pushing U.S. commercial entry to January 2023.

Can a biosimilar developer wait for all patents in a thicket to expire?

Commercially, no. For a thicket like Keytruda’s, which may extend to 2036 with successful product hop strategy, waiting for full patent clearance would require a biosimilar developer to hold an approved product on the shelf for 8+ years after FDA approval. The net present value of delayed entry, combined with competitive erosion from other biosimilar developers who chose earlier at-risk launches or negotiated settlements, typically makes waiting the least attractive option. Litigation and negotiated entry are the practical paths.

What is the ‘patent dance’ under the BPCIA and do biosimilar developers have to participate?

The patent dance is a private, multi-step information exchange between a biosimilar applicant and the reference product sponsor, intended to identify and narrow the patents that will be litigated before commercial launch. The Supreme Court confirmed in Sandoz v. Amgen (2017) that it is optional. Biosimilar developers who skip it avoid providing manufacturing confidential information to the innovator early in the process but accept the risk of broader, less predictable patent litigation upon commercial marketing notice.

How does Merck’s subcutaneous Keytruda strategy extend its patent protection?

The IV formulation of pembrolizumab has primary patents expiring around 2028. The SC formulation—which delivers the drug via subcutaneous injection using Halozyme’s hyaluronidase technology—will carry its own new set of patents covering the formulation, device, and delivery method. If Merck can switch the majority of patients to the SC product before 2028, the commercial market for IV pembrolizumab shrinks. Biosimilar developers benchmarking against IV pembrolizumab would then face a diminished reference product market, while the SC franchise remains patent-protected under new secondary patents potentially extending into the mid-2030s. Pending Halozyme litigation introduces execution risk on this strategy.

What legislative reforms are most likely to reduce patent thicket duration?

The Affordable Prescriptions for Patients Act’s patent assertion cap is the most direct and actionable proposal. A cap at 20 patents per BPCIA litigation changes the economics of thicket construction fundamentally. USPTO quality initiatives targeting continuation patent proliferation are slower but potentially more durable. Antitrust enforcement on rebate walls addresses commercial thickets that persist post-patent. None of these individually solves the problem; the combination of all three, if enacted or implemented simultaneously, would materially accelerate biosimilar competition on the major pending exclusivity cliffs.

")