1. The CDMO Market: Size, Consolidation, and the IP Stakes That Changed Everything

The global contract development and manufacturing organization market sat at approximately $259 billion in 2025 and will cross $375 billion by 2031 at a compound annual growth rate of around 6.3%, according to Research and Markets data published in February 2026. Biologics CDMOs are growing faster still, at 13.3% CAGR, with the segment valued at $21 billion in 2025 and projected to exceed $73 billion by 2035. Roughly 40 percent of all pharmaceutical manufacturing is now outsourced. Those numbers tell only part of the story.

The more consequential development of the past 18 months is structural. Novo Holdings completed its $16.5 billion acquisition of Catalent in December 2024, removing one of the three largest CDMOs from the independent market and creating a direct conflict-of-interest scenario: Catalent’s largest client in the GLP-1 segment is now owned by the parent company of Novo Nordisk. Any sponsor with Catalent manufacturing agreements signed before that acquisition needs to revisit its change-of-control provisions immediately and evaluate whether its proprietary formulation data sits in a facility owned by a direct competitor’s parent.

Simultaneously, the BIOSECURE Act catalyzed a forced restructuring of the cell and gene therapy CDMO landscape. In late 2024, WuXi AppTec agreed to sell its US and UK Advanced Therapies operations to private equity firm Altaris, which merged those assets with Minaris Regenerative Medicine to launch Minaris Advanced Therapies in May 2025. The new entity inherited WuXi ATU’s state-of-the-art Philadelphia campus and its commercial manufacturing track record, including production of Iovance’s AMTAGVI TIL therapy. The geopolitical risk that sponsors assumed was theoretical in 2022 materialized in full by 2025, and every contract that lacked an explicit geopolitical-trigger termination clause created a renegotiation crisis.

Samsung Biologics signed a $1.24 billion single-client contract in October 2024, running through December 2037 at its Songdo facility. That 13-year duration illustrates the extraordinary long-term IP and supply chain commitments sponsors are making. Lonza, meanwhile, announced in December 2024 that it would exit the capsules and health ingredients business and restructure into three platforms starting Q2 2025: Integrated Biologics, Advanced Synthesis, and Specialized Modalities. Fujifilm Diosynth committed $2 billion to a new gene therapy facility in North Carolina. Bachem pledged CHF 600 million to new European peptide capacity to capture GLP-1 demand.

The policy environment adds further complexity in 2026. Tariff pressure on imported pharmaceuticals and explicit FDA statements favoring domestic manufacturing have pushed sponsors to accelerate tech transfers and build dual-sourcing structures. CDMOs with US or European footprints are pricing that political premium into their contracts, and sponsors who signed capacity reservation agreements with Chinese CDMOs before 2024 now face either costly exits or exposure to the reputational and regulatory scrutiny that comes with maintaining those relationships.

Key Takeaways: Market Context

The Catalent-Novo Holdings transaction is the defining contract-risk event of 2024-2025. Sponsors with Catalent agreements must audit change-of-control, data-sharing, and IP-segregation clauses before the next contract renewal cycle.

BIOSECURE-driven restructuring created new entrants (Minaris Advanced Therapies) with inherited infrastructure. Sponsors evaluating these entities for the first time face the unusual challenge of diligencing an organization whose regulatory history and workforce originate from a different legal entity.

The 13-year Samsung Biologics contract signals that leading biologics CDMOs are moving aggressively toward long-term capacity reservations. Sponsors who lock in now pay a volume premium but gain supply security; those who wait face constrained capacity and higher pricing.

Geopolitical risk provisions, once treated as boilerplate, now require explicit triggering events, timelines, transition funding, and tech-transfer cost allocations in every new CDMO contract.

Investment Strategy: Market Structure

The Novo-Catalent deal compresses the number of true full-service biologics CDMOs with US commercial-scale capability to roughly four credible options: Lonza, Samsung Biologics, Fujifilm Diosynth, and Thermo Fisher Pharma Services. Capacity scarcity in this tier is real. Institutional investors tracking biotech sponsors should treat CDMO capacity reservation agreements as material contracts, equivalent in disclosure importance to licensing agreements. A sponsor without a secured commercial-scale manufacturing partner is carrying execution risk that does not always appear in pipeline-focused analyses. Patent portfolio analysis using tools like DrugPatentWatch should include a review of CDMO process-patent filings, which often reveal which manufacturing platforms a sponsor is actually dependent on and whether that dependency creates freedom-to-operate constraints.

2. From CMO to CDMO: What the Distinction Costs You Contractually

The operational difference between a Contract Manufacturing Organization and a Contract Development and Manufacturing Organization is straightforward: CMOs produce to specification, CDMOs develop the specification before producing it. A CMO receives a validated process and runs it. A CDMO receives a molecule, a regulatory target, and a development budget, then builds the process from the cell line or API synthesis route through formulation, analytical method validation, process characterization, and commercial tech transfer.

That expanded scope has a direct contractual consequence. A CMO contract is essentially a supply agreement with embedded quality terms. A CDMO contract is a hybrid development-services and supply agreement that generates intellectual property at every stage. The IP generated during development, which can include cell line improvements, host-cell protein reduction strategies, downstream purification innovations, novel excipient combinations, or analytical methods, belongs to someone. If the contract does not specify who, that question will eventually be litigated.

The drug development process averages 10 to 15 years and $2.6 billion in total cost. CDMOs that handle early-phase development work accumulate years of process knowledge about the sponsor’s molecule. That accumulated knowledge is worth something to the CDMO, independent of the manufacturing revenue, because it has defensive and offensive patent value. A CDMO that patents a manufacturing process it developed for a client’s biologic creates a potential freedom-to-operate obstacle if the sponsor later tries to switch manufacturers, even if the sponsor owns the molecule’s composition-of-matter patent. This conflict is not hypothetical. It has materialized in multiple arbitration proceedings, though the outcomes rarely become public.

‘The contract does not just govern what gets made. It governs who owns the knowledge that makes it possible to make anything at all.’

Why Scope Definition Determines IP Ownership Outcomes

A common failure mode in CDMO contracts is a Scope of Work that describes activities without describing outputs. ‘Process development for monoclonal antibody X’ covers an enormous range of activities: upstream cell culture optimization, media screening, bioreactor scale-up, downstream chromatography step development, viral clearance validation, and formulation development. Each of those activities can yield patentable innovations. A SOW that describes the activity without specifying who owns resulting inventions, who files patent applications, who bears prosecution costs, and what happens if the CDMO’s general-purpose platform patents read on the client-specific process, creates the conditions for a protracted IP dispute.

The fix is not simply adding a clause that says ‘client owns all IP.’ CDMOs will not accept that formulation wholesale, and for defensible reasons: their scientists and engineers conceive improvements during the development process using the CDMO’s proprietary platforms, equipment, and institutional knowledge. The negotiation has to distinguish between background IP (what each party brings to the relationship), foreground IP (what gets created during the engagement), and derivative IP (what the CDMO’s platform generates that is partly inspired by the client’s project). Each category needs its own ownership and licensing treatment.

Key Takeaways: CMO vs CDMO Distinction

A CDMO engagement generates IP continuously. Every development milestone, from first-in-man formulation to commercial process characterization, can yield patentable process innovations. The contract must address this before work begins.

CDMOs commonly hold foundational process patents on platform technologies (e.g., specific chromatography sequences, perfusion culture conditions, lipid nanoparticle formulation parameters) that may be relevant to a client’s molecule. Sponsors should run a freedom-to-operate analysis against the CDMO’s patent portfolio before executing the agreement.

The scope of work is the most important document in the contract package, more important than the master services agreement for day-to-day IP risk, because it defines what activities generate IP and, by reference, who owns what.

3. The Due Diligence Playbook: Before You Sign Anything

Quality Systems Assessment: Reading the FDA’s Inspection Record

FDA inspection records are public and granular. Before engaging any CDMO for a GMP activity, the sponsor’s quality team should pull the complete Form 483 and Warning Letter history through FDA’s Inspection Database and read the citations, not just the count. A CDMO that received a 483 in 2022 for inadequate out-of-specification investigation procedures but implemented a complete CAPA with root-cause analysis and trending improvements is a categorically different risk than one with a 2024 Warning Letter for data integrity failures. The character of a quality system reveals itself in how the organization responded to deficiencies, not in whether deficiencies occurred.

Data integrity failures are the highest-risk citation category. The FDA’s data integrity guidance makes clear that ALCOA-plus compliance (attributable, legible, contemporaneous, original, accurate, plus complete, consistent, enduring, and available) is non-negotiable for GMP records. A CDMO with a data integrity citation in the past four years should be able to provide a comprehensive remediation narrative, including an independent audit report, before a sponsor commits commercial-scale work. If the CDMO cannot or will not provide that documentation, the due diligence conversation should end there.

For biologics CDMOs, the FDA’s biologic process inspection model is more intensive than for small molecules. Inspectors evaluate cell bank characterization, in-process control strategies, container closure integrity, and the linkage between the CDMO’s process development data package and the client’s Chemistry, Manufacturing, and Controls filing. A CDMO that has navigated at least two successful pre-approval inspections for a comparable biologic modality demonstrates a level of regulatory capability that cannot be replicated by reviewing SOPs alone.

Intellectual Property Scrutiny: The Contamination Risk

IP contamination in the CDMO context describes what happens when a CDMO’s work for one client inadvertently or deliberately influences the process it develops for another. The mechanism varies. A CDMO scientist who worked on a competitor’s purification strategy may apply similar approaches to your program. The CDMO’s platform patent on a specific downstream process may have claims broad enough to read on your product’s manufacturing method. The CDMO may incorporate a third-party technology license into your process without disclosing that the license carries sublicensing restrictions or royalty obligations.

IP due diligence requires a structured review of the CDMO’s patent portfolio, its third-party technology agreements, and its IP assignment practices for employee inventions. Services like DrugPatentWatch enable systematic analysis of CDMO-affiliated patent filings by assignee, allowing sponsors to identify platform patents, continuation filings, and divisional applications that could intersect with a proposed development program. A CDMO with an active, growing process patent portfolio in your molecule’s therapeutic modality is not necessarily a bad partner, but the relationship requires explicit contractual carveouts and license grants before development begins.

The IP assignment chain for CDMO employees deserves specific attention. Many CDMOs employ scientists on contract or through staffing agencies. If those individuals contribute to inventions but their employment agreements do not explicitly assign invention rights to the CDMO, the CDMO cannot in turn assign those rights to the client. This creates title defects that surface during licensing transactions or enforcement actions. The due diligence checklist should include a review of the CDMO’s standard employment and contractor IP assignment agreements.

Financial Stability: What PE Ownership Signals

Private equity ownership of CDMOs has become ubiquitous. Approximately 60 percent of mid-tier CDMOs are PE-backed, according to Alvarez and Marsal’s CDMO M&A data. PE ownership is not inherently disqualifying, but it introduces specific risks that contract language must address. PE-owned CDMOs face pressure to optimize EBITDA in the near term, which can manifest as deferred facility maintenance, workforce reductions in quality functions, and resistance to capital expenditures that benefit the client but do not show up in the CDMO’s financial returns until years later.

A sponsor committing to a five-year commercial manufacturing agreement with a PE-backed CDMO should obtain audited financial statements for the past three years, understand the debt load on the operating entity (not just the holdco), and negotiate change-of-control provisions that provide meaningful exit rights or financial protections if the CDMO is sold or recapitalized. The Catalent situation demonstrated that even a publicly traded CDMO can be acquired and repositioned in ways that create conflicts with existing clients. Change-of-control clauses that trigger only on formal ownership transfer miss the risk: a new strategic investor can influence CDMO priorities without technically triggering ownership change.

Reference Checks: The Questions That Actually Matter

Standard reference checks ask whether the CDMO delivered on time and met quality specifications. Those questions tell you about the past, not about how the CDMO behaves when something goes wrong, which is the scenario that determines whether a partnership survives. The questions that generate useful information are: How did the CDMO communicate the first time a batch failed? How much notice did you receive before a key project manager was reassigned? When the CDMO identified a regulatory risk in your process, did it come to you with a proposed solution or with a problem? Was the CDMO’s cost estimate for unexpected scope changes reasonable and explained in detail, or did change orders arrive without adequate justification?

A CDMO that consistently communicates bad news early, proposes solutions alongside problems, and explains cost changes transparently is demonstrating the operational behavior that protects your project. A CDMO that conceals developing problems until they become crises, or that uses change order mechanisms to recover margin on a low-ball bid, will not change that behavior once you are a client.

Key Takeaways: Due Diligence

Pull the complete FDA inspection record and analyze the character of any citations, not just their count. Data integrity findings require an independent remediation audit before you proceed.

Run a patent landscape analysis against the CDMO’s portfolio using DrugPatentWatch or equivalent tools before executing any development agreement. Platform patents that read on your molecule’s manufacturing process create freedom-to-operate risk that survives the contract.

For PE-backed CDMOs, negotiate change-of-control provisions that trigger on material changes in strategic direction or new investor influence, not just formal ownership transfer. Obtain detailed debt-stack information for the operating entity.

Ask reference clients how the CDMO behaved during failures and unexpected scope changes. Operational culture during adversity is the most predictive indicator of partnership quality.

4. IP as the Core Asset: How CDMO Contracts Create or Destroy Patent Value

Background IP, Foreground IP, and the Derivative Problem

Every CDMO engagement starts with two pools of pre-existing intellectual property. The sponsor’s background IP typically includes the composition-of-matter patents on the drug substance, sequence claims for biologics, clinical data packages, and regulatory exclusivities including orphan drug designation or pediatric exclusivity. The CDMO’s background IP includes its manufacturing platform technology, cell culture media formulations, chromatography protocols, analytical methods, facility designs, and any patents it holds on those elements.

Foreground IP is what gets created during the engagement: new process innovations, improved cell line productivity, novel purification steps, formulation breakthroughs, analytical method developments. The critical question is who owns foreground IP created by CDMO scientists using the CDMO’s equipment, reagents, and institutional knowledge but in service of the sponsor’s molecule and funded by the sponsor’s development budget. The legal answer depends entirely on what the contract says. In the absence of explicit language, inventorship doctrine governs, and the inventor’s employer typically owns the patent rights. For process innovations developed by CDMO scientists, that employer is the CDMO.

The derivative IP problem is subtler. A CDMO that develops a superior upstream process for a client’s monoclonal antibody learns things that may apply to its next client’s biologic, even if the specific cell line is different. The institutional learning is not patentable as such, but it may inform future patent applications that the CDMO files on its platform. If those applications include claims broad enough to encompass the process the CDMO developed for the first client, the first client may find that its commercial manufacturing process is covered by the CDMO’s own patent, filed after the development work was completed. Contracts need explicit provisions that prohibit CDMOs from filing patent applications with claims that read on processes developed specifically for a client’s product, even when those claims are framed at the platform level.

Freedom to Operate and the Manufacturer-Switch Problem

One of the most significant IP risks in CDMO contracting is the loss of freedom to operate if the client needs to switch manufacturers. The client may own the composition-of-matter patent on the drug substance and the New Drug Application or Biologics License Application. However, if the CDMO owns patents on the manufacturing process, the client cannot instruct a new CDMO to replicate that process without the original CDMO’s consent. In a supply disruption, regulatory action, or commercial dispute, this creates leverage for the original CDMO that can amount to a manufacturing monopoly on the client’s own product.

The ‘springing license’ structure addresses this risk. Under this approach, the CDMO retains ownership of process patents but grants the client a limited, royalty-free license to practice those patents under specific conditions: failure to supply contracted volumes, regulatory action against the CDMO’s facility, insolvency, or a defined quality failure threshold. The springing license does not transfer IP ownership, which the CDMO resists, but it provides the client with operational continuity rights in the scenarios that matter most. The triggering conditions need precise drafting. ‘Failure to supply’ should specify a volume threshold and a duration, not just any single missed delivery. ‘Quality failure’ should reference defined non-conformance criteria rather than subjective quality assessments.

How CDMO Platform Patents Affect Drug IP Valuation

For institutional investors, CDMO process patents are relevant to drug IP valuation in two ways. First, they affect the total cost of manufacturing at commercial scale. A drug whose commercial manufacturing process is covered by a CDMO’s platform patent carries a royalty or license fee obligation that reduces the drug’s net manufacturing margin. If that obligation is not disclosed in the sponsor’s financial filings, it represents a material hidden cost. Second, CDMO process patents can affect the barriers to biosimilar entry. A biosimilar manufacturer attempting to replicate a biologic’s manufacturing process may face infringement claims from the CDMO that originally developed that process, even if the biologic’s composition-of-matter patent has expired. This creates a form of manufacturing exclusivity that extends beyond the primary patent term, functionally similar to evergreening through process patents rather than formulation or indication claims.

DrugPatentWatch tracks CDMO-affiliated patents by assignee and can identify which manufacturing entities hold process patents relevant to specific drug products. IP teams at both innovative sponsors and generic entrants should conduct this analysis as a standard component of patent landscape reviews, because process patents assigned to a CDMO rather than the drug’s sponsor will not appear in the sponsor’s patent list but will appear in any infringement analysis.

Table 1: IP Ownership Models in CDMO Development Contracts

Model

Description

Client Benefit

Client Risk

CDMO Resistance Level

‘I Paid For It’ (Client Owns All Foreground IP)

Client owns all IP developed using its development funding, regardless of inventorship

Full freedom to operate; unrestricted manufacturer switching; ability to license or enforce against competitors

CDMO may price in a premium to offset IP loss; CDMO scientists may have lower motivation to innovate

High for platform-adjacent innovations; moderate for product-specific process

Inventorship Follows Conception

IP ownership tracks to employer of the scientist who conceived the invention

Clear legal default; no negotiation friction on non-contentious IP

Most process innovations conceived by CDMO scientists; client may own little foreground IP

Low (default legal rule favors CDMO)

Joint Ownership

Both parties hold equal, undivided interest in co-developed IP

Some ownership stake; avoids full IP transfer negotiation

Either party can license to third parties without consent (US law); manufacturer-switch requires CDMO consent; enforcement requires joint action

Low (appears fair but disadvantages client in practice)

Client Owns, CDMO License-Back

Client owns all foreground IP; grants CDMO a limited, non-exclusive license for internal development use

Full ownership and control; CDMO cannot commercialize client’s IP; clean manufacturer switch

CDMO may restrict license-back scope narrowly, creating negotiation friction on subsequent programs

Moderate; CDMO wants internal-use rights for institutional learning

Springing License to CDMO Background IP

CDMO retains background IP; grants client a dormant license that activates on defined supply failures

Manufacturer-switch capability in supply disruption without full IP transfer

License triggers only on defined conditions; does not cover foreground IP developed during program

Moderate; CDMO accepts limited risk in exchange for retaining ownership

Field-of-Use Carveout

CDMO retains process IP; agrees not to license or use the specific process for defined competitive products

Competitive protection without full IP transfer; limits CDMO’s ability to use client’s process for rivals

Does not prevent CDMO from filing on improved versions; carveout scope subject to definitional disputes

Moderate to high; limits CDMO’s ability to leverage institutional learning commercially

Key Takeaways: IP Valuation

CDMO process patents are a form of manufacturing exclusivity that operates independently of the drug’s primary patent estate. They do not appear in standard patent analyses unless the analyst searches by CDMO assignee name.

Springing licenses are the most practical mechanism for protecting manufacturer-switch rights without requiring full IP transfer. Triggering conditions must be precise: volume thresholds, duration windows, and defined quality-failure criteria.

Joint ownership is functionally worse for clients than it appears. Under US law, either joint owner can license the IP to third parties without the other’s consent, which means the CDMO can license your jointly owned process to a competitor.

The ‘I paid for it’ model requires a premium to compensate the CDMO for IP loss. That premium is usually worth paying for programs with large commercial potential, because it eliminates the manufacturer-switch obstacle at commercial scale.

Investment Strategy: IP Valuation

When modeling a drug’s patent-protected revenue period, investors should account for three IP layers: the composition-of-matter patent, any formulation or method-of-use patents, and process patents held by the CDMO. The third layer is rarely discussed in analyst reports. A biologic whose commercial manufacturing process is covered by a CDMO’s platform patent may have effective manufacturing exclusivity extending beyond the composition-of-matter expiry, but that exclusivity does not belong to the sponsor. It creates a royalty obligation that reduces margin, and it limits the sponsor’s ability to qualify multiple manufacturers, which concentrates supply-chain risk. For biosimilar entry modeling, CDMO process patents should be included in the freedom-to-operate analysis. If a CDMO holds broad process patents and the biosimilar manufacturer cannot develop a non-infringing alternative process, the practical barrier to entry is higher than the composition-of-matter cliff alone suggests.

5. Biologics Manufacturing Technology Roadmap and Contract Implications

Monoclonal Antibodies: The Established Playbook and Its Residual Risks

Monoclonal antibody manufacturing is the closest thing the biologics CDMO sector has to a mature, standardized process. The upstream platform: CHO cell expression, fed-batch or perfusion bioreactor culture, platform media, and dissolved oxygen and pH control regimes, is well-characterized across the major CDMOs. The downstream platform: Protein A capture, two or three orthogonal viral clearance steps, polishing chromatography, and ultrafiltration-diafiltration, has been executed at commercial scale hundreds of times. The FDA’s regulatory expectations for a mAb BLA Chemistry, Manufacturing, and Controls section are codified and predictable.

That maturity does not mean contracts are low-risk for mAb programs. The risk in mAb CDMOs is not process novelty; it is process comparability after tech transfer. A sponsor that developed a mAb process at a research-scale CDMO and transfers it to a commercial-scale CDMO for Phase III and commercial supply must demonstrate to the FDA that the material made at the commercial site is analytically comparable to the clinical material used to generate efficacy and safety data. If the tech transfer introduces process changes that alter the product’s quality attributes, the sponsor may need additional bridging studies or a manufacturing supplement, both of which delay approval and cost money that should have been allocated in the original CDMO contract’s tech transfer provisions.

Contracts for mAb programs should specify a defined comparability protocol as a deliverable, with analytical acceptance criteria agreed upon before the tech transfer begins. They should also specify who bears the cost of additional development work if comparability is not achieved on the first transfer attempt. CDMOs that have successfully executed commercial-scale tech transfers for three or more mAbs have learned which parameters create comparability risk and can flag them early. CDMOs that have not done this work learn at the sponsor’s expense.

Antibody-Drug Conjugates: The HPAPI Constraint

ADC manufacturing combines mAb production with high-potency small molecule synthesis and bioconjugation, requiring containment capability for occupational exposure limits in the nanogram-per-cubic-meter range. Samsung Biologics expanded its ADC suites in 2024 on the strength of rapidly growing demand. Lonza’s Visp, Switzerland, site remains one of the few facilities globally with the containment infrastructure, mAb production capacity, and bioconjugation capability under one roof. WuXi STA (WuXi AppTec’s small molecule arm) holds a strong position in linker-payload synthesis, though its inclusion in BIOSECURE scrutiny has forced sponsors to evaluate dual-source strategies for the small molecule component.

CDMO contracts for ADC programs need to address the containment requirement explicitly, specifying the occupational exposure band the facility is certified to handle and the consequence if a new payload classification requires a higher containment level than the existing facility can provide. They also need to address payload supply: if the CDMO sources the cytotoxic payload from a third-party supplier, the contract must define what happens if that supplier cannot deliver on schedule, who qualifies alternative sources, and who bears the development cost of qualifying an alternative linker-payload combination if the primary is unavailable.

Cell and Gene Therapy: The Capacity and Scale Problem

Cell and gene therapy manufacturing is categorically more complex than mAb or small molecule production, and the contract implications reflect that complexity. Autologous therapies, where the manufacturing input is the patient’s own cells, create a one-batch-per-patient supply model that requires extraordinary scheduling coordination, chain-of-identity traceability from apheresis to infusion, and a quality system that can handle batch releases on a patient-by-patient basis rather than the lot-based release model for conventional drugs.

The CGT CDMO capacity overhang that developed in 2023-2024 has partially corrected, but the cell and gene therapy CDMO market remains structurally imbalanced. Several CDMOs built dedicated CGT facilities anticipating a wave of commercial approvals that has been slower to materialize than forecast. Underutilized facility time has made CDMO pricing for early-phase CGT programs relatively negotiable in 2025-2026. Sponsors should use this window to negotiate capacity reservation provisions for commercial-scale manufacturing in contracts that begin at Phase I or II, with defined pricing escalation structures that lock in reasonable commercial rates before the next wave of CGT approvals tightens capacity.

Viral vector manufacturing, specifically AAV and lentiviral vectors, has its own IP dimension. The major AAV production platforms, including the triple-plasmid transient transfection system developed at Penn and the baculovirus-insect cell platform licensed by various CDMOs, carry licensing obligations that a sponsor must understand before selecting a CDMO. If the CDMO’s AAV production platform is licensed from a foundation or institution under terms that include downstream royalties on product sales, those royalties are an undisclosed cost that reduces the sponsor’s commercial margin. Due diligence must include a review of the CDMO’s platform licensing stack.

Table 2: Biologics CDMO Technology Roadmap and Key Contract Provisions by Modality

LNP platform uses ionizable lipids subject to Alnylam/Acuitas licensing; no cGMP mRNA commercial-scale track record

Key Takeaways: Biologics Technology Roadmap

For mAb programs, comparability across manufacturing sites is the primary regulatory and commercial risk. The contract must specify the comparability protocol and cost allocation before tech transfer begins, not after a comparability failure creates a crisis.

ADC contracts must address HPAPI containment at the OEB level, not in general terms. A payload classification change during development can void a facility’s containment certification for your program.

AAV and lentiviral vector production platforms carry licensing obligations from academic institutions and prior commercial developers. These royalties appear in the CDMO’s cost structure and should be disclosed and analyzed before contract execution.

The CGT CDMO capacity window in 2025-2026 is favorable for negotiating commercial-scale capacity reservations at competitive rates. Sponsors who do not lock in commercial terms during Phase II risk facing constrained availability and premium pricing at Phase III transition.

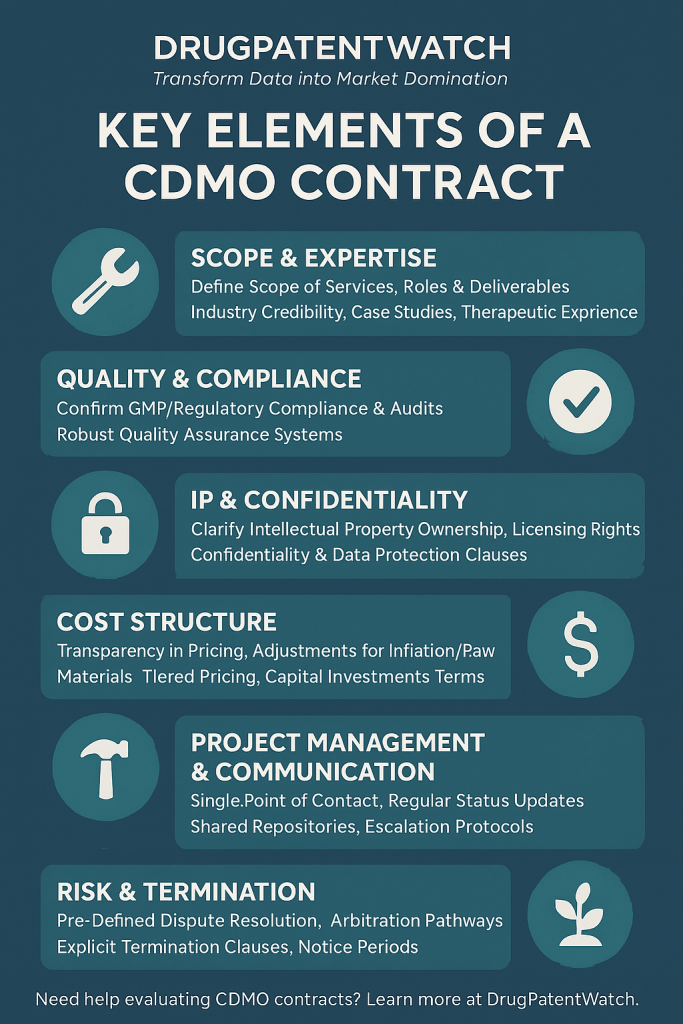

6. The Anatomy of a Defensible CDMO Contract: Clause-by-Clause Analysis

Scope of Work: The Blueprint That Prevents Cost Overruns

The Scope of Work is the document that determines whether a CDMO partnership succeeds or generates litigation. A well-constructed SOW specifies deliverables with measurable acceptance criteria, assigns responsibility for each activity to a named party, defines the information and materials each party must provide and when, and sets out what constitutes successful completion of each phase. A poorly constructed SOW describes activities at a level of abstraction that allows each party to interpret obligations differently until a dispute makes the ambiguity visible.

Common SOW failures include upstream fermentation ‘optimization’ with no defined productivity target, formulation development ‘support’ without specifying which formulation parameters are within the CDMO’s authority to change versus which require client approval, technology transfer ‘assistance’ without a defined transfer protocol, acceptance criteria, and a process for managing failed transfers, and regulatory ‘support’ without specifying which submissions the CDMO is responsible for authoring versus reviewing. Each of those vague formulations creates an argument about scope when something goes wrong, and something always goes wrong.

The SOW should be treated as a living document governed by a formal change control process. Every change to scope, whether driven by scientific findings, regulatory feedback, or operational constraints, should generate a written change order with an explicit cost and timeline impact. Contracts that require change orders to be ‘mutually agreed’ but do not specify a timeline for agreement allow either party to stall indefinitely, which effectively transfers leverage to whichever party is less eager to reach agreement.

Term, Termination, and the Change-of-Control Provision

CDMO agreements typically use a Master Services Agreement (MSA) with individual Product Schedules or Work Orders for each program. The MSA governs the overarching relationship and often has a term of three to five years with renewal options. Product Schedules contain program-specific terms and frequently include survival clauses that allow specific programs to continue past the MSA expiry. This structure makes sense operationally but creates complexity when drafting termination rights, because termination of the MSA does not automatically terminate active Product Schedules.

The most important termination clause in 2025-2026 is the change-of-control provision. Given the pace of M&A in the CDMO sector, sponsors need termination rights that are triggered not just by ownership change but by defined operational consequences of ownership change: reallocation of manufacturing capacity to new owner priorities, departure of named key personnel within a defined period following a transaction, or demonstrated conflict of interest between the new owner and the sponsor’s therapeutic area. The Catalent acquisition by Novo Holdings is the clearest recent example: sponsors in the GLP-1 and diabetes space who did not have robust change-of-control termination rights found themselves locked into agreements with a CDMO now owned by a direct competitor’s parent company.

Termination-for-convenience provisions typically require the terminating party to pay the CDMO’s committed costs, wind-down expenses, and a portion of anticipated profit. Negotiating these provisions before execution matters because the CDMO’s leverage is highest at execution, when both parties want the deal to close, and lowest after a quality failure or supply disruption, when the sponsor wants to exit. A sponsor should model the financial consequence of exercising termination-for-convenience at each stage of the program and negotiate the payment formula with that model in mind.

Pricing Models: Choosing the One That Fits Your Risk Profile

Fee-for-Service pricing compensates the CDMO for defined activities at stated rates. It provides budget predictability but no incentive for the CDMO to complete activities efficiently, and it creates arguments about whether specific activities were ‘in scope’ when actual work exceeds the quoted hours or materials. FFS works well for discrete, well-characterized activities like analytical testing or reference standard characterization, where the inputs and outputs are predictable.

Fixed-price contracts give the sponsor predictable total cost and transfer execution risk to the CDMO. CDMOs price fixed contracts with risk premiums that can be 20 to 30 percent above cost-plus estimates. For well-characterized programs with mature processes, that premium is usually worth paying for budget certainty. For early-phase development with high scientific uncertainty, fixed pricing is often the wrong structure because the CDMO will either price a massive contingency or will encounter losses that damage the relationship and lead to deferred quality investments.

Cost-plus pricing is transparent but requires that the sponsor have robust audit rights and the internal capability to evaluate whether claimed costs are legitimate. Without those capabilities, cost-plus devolves into a mechanism where the CDMO allocates overhead broadly and the sponsor has no practical ability to challenge it. Performance-based payments, which tie a portion of the CDMO’s fee to defined milestone achievements like a successful process performance qualification run or FDA approval, align incentives but require exceptionally precise milestone definitions. ‘FDA approval’ as a payment milestone sounds clean but creates disputes about whether delays attributable to the FDA’s review timeline (rather than manufacturing deficiencies) should affect the CDMO’s payment.

Quality Assurance Agreements: The Operational Constitution

The Quality Assurance Agreement (QAA) is a companion document to the MSA that the FDA describes as a ‘critical tool’ for cGMP compliance. It defines, at granular operational detail, which party is responsible for each quality-related activity: who approves or rejects raw materials, who conducts environmental monitoring, who is responsible for out-of-specification investigations, who approves batch records, and how the two organizations’ quality units communicate on deviations and change control.

The QAA must address change control in specific terms. Manufacturing process changes, facility modifications, equipment qualifications, and analytical method revisions each have different FDA notification requirements depending on their potential impact on product quality. The QAA should categorize changes by the level of regulatory action required (Prior Approval Supplement, Changes Being Effected, Annual Report) and assign each change type to one party for initiation and the other for approval. A QAA that simply says ‘major changes require client approval’ without defining what constitutes a major change creates precisely the ambiguity that leads to regulatory submissions being filed without adequate sponsor review.

The QAA should be executed before or simultaneous with the MSA, not deferred to a later negotiation. Deferring QAA execution is common but creates risk because the parties begin operating under the MSA’s commercial terms before the quality responsibilities are defined. When the first deviation occurs, the QAA negotiation becomes contentious because each party is now arguing from a position of operational history rather than clean-slate planning.

Confidentiality, Data Security, and the AI-Use Problem

CDMO confidentiality agreements have expanded significantly in scope as CDMOs have adopted digital manufacturing platforms, AI-driven process development tools, and cloud-based data management systems. The traditional confidentiality clause covers documents and physical samples. The current risk landscape requires provisions that explicitly govern data generated during the program, where that data is stored, who can access it, and whether the CDMO’s AI systems can use that data to train models that may benefit other clients or the CDMO’s own commercial development efforts.

If a CDMO’s process development platform generates predictive models trained partly on your molecule’s fermentation data or your proprietary formulation screening results, those models carry your proprietary information in encoded form. The CDMO may not be violating a traditional confidentiality clause by using them for other clients, because the models themselves are not your documents. Contracts need explicit provisions that prohibit using client data to train or improve AI models that benefit third parties or the CDMO’s own product development, and they need audit rights that allow the sponsor to verify compliance.

Data residency requirements have become material for programs subject to GDPR or for sponsors with national security constraints. If the CDMO’s data management platform stores program data on servers in jurisdictions where the sponsor has regulatory or security concerns, the contract must specify data residency requirements and the CDMO’s obligation to notify the sponsor if data is transferred to a new jurisdiction. The BIOSECURE context makes this non-theoretical: data stored by a CDMO with Chinese ownership on servers in China may be subject to the PRC’s national security law disclosure obligations.

Indemnification, Liability Caps, and Batch-Failure Economics

Liability allocation in CDMO contracts has two distinct regimes: the cap regime, which limits total financial exposure from all claims, and the carve-out regime, which specifies categories of claims that are not subject to the cap. Typical caps run at one to three times the fees paid in the prior 12 months. Typical carve-outs include gross negligence, willful misconduct, breaches of confidentiality, and IP infringement. The negotiation is about where to draw the line between capped and uncapped liability for manufacturing failures that do not rise to gross negligence.

A batch failure in commercial manufacturing causes financial harm in at least four categories: the cost of the failed batch (raw materials, CDMO processing fees, quality testing), the cost of reruns, the revenue lost during supply disruption, and the regulatory burden of investigating and remediating the failure. The last two categories are consequential damages that CDMO contracts nearly universally exclude from the liability regime. Sponsors should accept this exclusion for truly consequential damages (lost market revenue) but negotiate harder on direct damages that flow predictably and directly from a manufacturing failure, including the cost of emergency supply procurement from a backup source.

For batch failures, a practical risk-sharing model allocates the rerun cost as follows: the CDMO waives its processing fee for the first rerun of any batch that fails due to a manufacturing deviation within its control. The sponsor covers raw material costs regardless of fault, because raw material financing is not a reasonable obligation for the CDMO. For failures attributable to the sponsor’s process design rather than the CDMO’s execution, the CDMO charges its standard processing fee for reruns. Agreeing on this framework before any failure occurs eliminates the negotiation under pressure that otherwise happens when a batch fails and both parties are already in an adversarial posture.

Force Majeure: Writing for the Actual Risk Landscape

Standard force majeure clauses list natural disasters, government actions, and labor strikes as triggering events. The 2020-2025 experience added pandemic, supply chain disruption, and geopolitical restriction to the list of events that actually materialize. The 2026 context adds tariff-driven supply chain restructuring, BIOSECURE-style legislative risk, and facility-specific regulatory action (a site-specific FDA import alert) as events that can impair CDMO performance without qualifying as traditional force majeure.

A robust force majeure clause specifies what counts as a triggering event, how quickly the affected party must notify the other (24 to 72 hours is reasonable for manufacturing disruptions), what mitigation the affected party must undertake before invoking force majeure relief (including qualification of alternative sites or suppliers where feasible), how long the force majeure excuse can last before the other party has the right to terminate, and who bears the cost of transitioning to an alternative manufacturing site if the force majeure extends beyond the termination window.

The clause should not permit force majeure relief for events the CDMO could have prevented through reasonable business planning. A CDMO that relies on a single-source supplier for a critical raw material and then claims force majeure when that supplier fails has not exercised reasonable supply chain management. The contract should require CDMOs to maintain qualified backup suppliers for critical raw materials as a condition of the force majeure provision’s application.

Key Takeaways: Contract Anatomy

The SOW is the highest-leverage document in the contract package. Every ambiguity in deliverable definitions or activity assignments will become a dispute. Specify acceptance criteria, responsible parties, and change control procedures before execution.

Change-of-control termination provisions must address operational consequences of M&A, not just ownership transfer. Key personnel departure, capacity reallocation, and conflict-of-interest scenarios should each be defined as independent triggering events.

QAAs must be executed before or simultaneous with the MSA. Deferring QAA negotiation until after commercial terms are agreed transfers leverage to the CDMO on the quality provisions that actually govern day-to-day operations.

AI and digital platform data-use restrictions are now essential confidentiality clause elements, not optional additions. The prohibition on using client data to train CDMO AI models must be explicit and auditable.

Batch-failure cost allocation should be agreed in advance: CDMO waives rerun processing fees for first failure caused by CDMO deviation; sponsor covers raw materials regardless of fault. This prevents the adversarial renegotiation that happens after a failure under ambiguous contract terms.

Measurable acceptance criteria; formal change control with cost/timeline impact

Activity descriptions without outputs; vague ‘support’ language

Critical

Quality Assurance Agreement

Operationalize cGMP responsibilities between parties’ quality units

Change categorization by regulatory impact; deviation investigation responsibilities; audit rights

Deferred to post-MSA execution; ‘major changes require approval’ without defining major

Critical

IP Rights (Foreground)

Define ownership of innovations developed during engagement

Background/foreground distinction; prohibition on CDMO filing claims reading on client-specific processes; springing license on supply failure

Blanket ‘client owns all IP’ rejected by CDMO; no derivative IP provisions

Critical

Term and Termination

Define lifecycle of agreement and conditions for exit

Change-of-control provision addressing operational consequences; termination-for-convenience cost formula

Change-of-control triggers only on formal ownership transfer; no key-personnel departure provisions

High

Confidentiality / Data Security

Protect proprietary information and data during and after engagement

AI/ML data-use restrictions; data residency requirements; audit rights on digital systems

Covers documents but not data; no AI-training prohibition; no breach notification timeline

High

Indemnification / Liability Cap

Allocate financial risk for manufacturing failures and third-party claims

Batch-failure cost allocation framework; carve-outs for IP infringement, gross negligence, data breach

Consequential damages excluded too broadly; no practical batch-failure cost-sharing model

High

Pricing and Payment

Define compensation structure, escalation, and financial terms

Pricing model selection matched to risk profile; raw material cost pass-through mechanism; currency risk allocation

Fixed-price for early-phase development with high scientific uncertainty; no escalation formula for multi-year agreements

High

Force Majeure

Excuse non-performance during defined extraordinary events

Mitigation obligation before relief applies; duration limit before termination right triggers; alternative site cost allocation

Single-source supplier failure excused without mitigation obligation; no duration limit on relief period

Medium-High

Technology Transfer

Define responsibilities, acceptance criteria, and cost allocation for process transfers

Defined transfer protocol with analytical acceptance criteria; cost allocation for failed transfers; comparability protocol as a deliverable

Treated as a simple logistics activity; no acceptance criteria for transfer completion

High for biologics

Subcontracting

Govern CDMO’s use of third-party providers for contracted activities

Client approval for quality-critical subcontractors; CDMO retains full liability for subcontractor performance and compliance

Blanket subcontracting permission with no client approval right; CDMO’s liability limited to its own acts

Medium

Dispute Resolution

Define escalation path from operational disagreement to formal resolution

Multi-tiered structure: escalation to senior management, then mediation, then binding arbitration; defined timelines at each stage

Straight to litigation; no senior management escalation step that preserves relationships

Medium

7. Negotiation Strategy: Leverage Points, Pricing Models, and Common Failures

The Business Term Sheet: Where the Real Deal Gets Made

Negotiating CDMO contracts directly in legal document form is inefficient and expensive. By the time lawyers are drafting, the parties have already paid for their time regardless of outcome, and each redline carries an emotional valence that can harden positions unnecessarily. A business term sheet executed before legal engagement allows the commercial and scientific teams to agree on the key economic and operational terms, including price structure, volumes, payment milestones, agreement length, capacity reservation commitments, and forecasting obligations, before the legal teams translate those agreements into contract language.

The term sheet is non-binding but functionally shapes the outcome because positions agreed at the term sheet stage are difficult to walk back without damaging the relationship. The sponsor’s cross-functional team, encompassing operations, regulatory affairs, R&D, finance, legal, and quality, should contribute to the term sheet before it is presented to the CDMO. Internal alignment on priorities before negotiation begins is as important as the negotiation itself. Sponsors who present a term sheet with positions that their own internal teams have not agreed on often concede in ways they later regret.

Where Sponsors Give Up Leverage Unnecessarily

Price fixation is the most common leverage failure. A sponsor that treats CDMO selection primarily as a procurement exercise, optimizing for the lowest per-batch or per-gram cost, often ends up with a CDMO that low-balled its proposal, excluded necessary work from the scope, and recovers margin through change orders and scope disputes. The cost of a quality failure at commercial scale, including batch write-offs, supply disruption, regulatory remediation, and potential FDA enforcement action, can exceed the total fees paid to the CDMO over multiple years of the agreement. A CDMO with a premium bid and a track record of quality execution is almost always the better financial choice.

Sponsors also give up leverage by starting with CDMOs they have already decided to use. If the RFP process is structured as a formality to justify a predetermined choice, the winning CDMO knows it and prices accordingly. A genuine competitive process, with objective evaluation criteria published in the RFP and a commitment to select on merit, creates the conditions for CDMOs to put their best commercial terms on the table. A useful proxy: if a CDMO is reluctant to invest in a detailed technical response to the RFP before a contract is signed, that reluctance tells you something about how it will treat scope definition and communication once the contract is in place.

Technology transfer complexity is a category where sponsors consistently underestimate their negotiating position. A sponsor that has generated high-quality process development data, a well-characterized cell bank, a robust analytical method package, and a clear regulatory filing strategy for the receiving site makes the CDMO’s tech transfer work predictable and lower-risk. That certainty has value to the CDMO, and sponsors should claim it explicitly in negotiations rather than treating tech transfer as an obligation the CDMO performs for the sponsor’s benefit.

KPIs: Defining Performance Before It Becomes Disputed

Key performance indicators serve two functions: they provide an objective basis for evaluating CDMO performance, and they create a contractual mechanism for performance-based consequences, including fee adjustments, remediation obligations, and termination rights. Effective KPIs are specific enough to measure without ambiguity, within the CDMO’s operational control (excluding factors outside the CDMO’s influence), and connected to commercial consequences that create genuine incentive alignment.

On-time delivery consistently ranks as the highest-priority selection criterion for sponsors but historically performs at only median levels in CDMO benchmarking surveys. Contractually defined KPIs for on-time delivery should specify the percentage threshold (e.g., 95 percent of batches released within the agreed window), the measurement period (rolling 12 months rather than point-in-time), and the consequence of breach (remediation plan within 30 days, fee credit after sustained failure). A KPI that lacks a consequence is a reporting requirement, not a performance management tool.

Batch success rate, deviation frequency, out-of-specification investigation cycle time, and change control turnaround are each measurable and consequential. The KPI framework should be reviewed and, if necessary, recalibrated at each annual program review, because what constitutes acceptable performance at Phase II clinical manufacturing differs from commercial-scale expectations. A CDMO that consistently performs at 92 percent on-time delivery for clinical batches is performing acceptably by development standards; the same rate is problematic for a commercial product with a specialty patient population and no backup supply.

Key Takeaways: Negotiation Strategy

Execute a non-binding business term sheet before engaging legal teams. Internal alignment on the sponsor’s side is as important as the external negotiation. An internal disagreement that surfaces in front of the CDMO negotiating team destroys leverage.

The cheapest CDMO bid nearly always contains excluded scope that re-enters as change orders. Evaluate total cost of ownership, including tech transfer risk, change order history from reference clients, and the cost of a single batch failure, before selecting on price.

On-time delivery KPIs must include specific thresholds, measurement periods, and financial consequences. A KPI with no attached consequence is a reporting requirement. CDMOs optimize for contractual consequences, not aspirational metrics.

Sponsors with high-quality process development packages have negotiating leverage on tech transfer terms and should use it explicitly. Well-characterized programs reduce the CDMO’s execution risk, and that risk reduction has commercial value.

No ceiling on total cost without cap; incentivizes slow execution

Low; directly compensated for time invested

Not-to-exceed cap; defined deliverable milestones that allow sponsor to assess progress before authorizing additional time

Milestone-Based / Performance-Linked

Development programs where specific outcomes (PPQ success, IND acceptance, NDA filing) can be defined precisely

Milestone definitions subject to dispute; CDMO may over-invest to hit milestone at expense of long-term quality

Revenue timing uncertainty; risk of absorbing costs on milestones delayed by sponsor or regulatory factors

Milestone definitions must specify what constitutes achievement vs. delay; allocate milestone payment risk for regulatory-authority-caused delays separately from CDMO-caused delays

8. Performance Monitoring, KPIs, and Change Control

Building a Data-Driven Oversight Model

Performance monitoring in CDMO partnerships requires a structured cadence of reviews, a defined set of reported metrics, and a governance process that escalates issues before they become crises. The oversight model should operate at three levels: operational (weekly or bi-weekly project team calls covering batch progress, deviations, and upcoming milestones), tactical (monthly program reviews covering KPI performance, change control status, and budget tracking), and strategic (quarterly executive reviews covering the relationship health, pipeline evolution, and capacity planning).

At each level, the sponsor’s representative needs access to data, not summaries. If the CDMO’s quality system is fully digitized and the sponsor’s program has dedicated dashboards showing batch record status, environmental monitoring trends, and deviation investigation timelines in real time, the operational review becomes a discussion of exceptions rather than a status update. If the sponsor’s visibility is limited to what the CDMO chooses to report, the oversight model depends entirely on the CDMO’s transparency, which is the weakest possible control structure.

Deviation Management: The Early Warning System

Deviations are not failures; they are the manufacturing quality system working as designed. A CDMO that never reports deviations either has an exceptionally well-controlled manufacturing environment or has a deviation reporting culture that suppresses uncomfortable information. The latter is more common than the former. The QAA should specify deviation classification criteria, investigation timelines, CAPA requirements, and escalation triggers for deviations that affect or potentially affect the client’s product. A deviation that the CDMO classifies as minor but that involves a parameter with known impact on product quality should trigger client notification regardless of the CDMO’s internal classification.

Change control is the adjacent risk. Manufacturing changes that the CDMO’s quality unit classifies as minor may still require FDA notification, and the CDMO’s assessment of regulatory impact is not always aligned with the sponsor’s regulatory strategy. The QAA’s change control provisions should require the CDMO to notify the client of any manufacturing change before implementation, regardless of the CDMO’s internal classification, with a defined review window for the client to assess regulatory impact. A ‘Prior Approval Supplement’ that gets filed without sponsor review can delay the next site audit or create post-approval manufacturing supplement requirements that the sponsor did not anticipate.

Audit Rights: The Practical Exercise

Audit rights are common in CDMO contracts and rarely exercised with the frequency and specificity that would make them effective. A sponsor that audits once at program initiation and then relies on CDMO quality reports for ongoing oversight is not using its audit rights in a way that provides genuine assurance. The audit program should include scheduled annual GMP compliance audits, event-triggered audits following significant deviations or regulatory actions, and, for commercial programs, process-specific audits covering critical manufacturing steps.

For-cause audit rights, which allow the sponsor to conduct an unannounced or short-notice audit following a quality event, are among the most valuable and most contentiously negotiated provisions in the contract. CDMOs resist for-cause audit rights because unannounced audits disrupt operations. Sponsors need them because the most important information about a quality failure is often visible only in the immediate aftermath, before corrective actions are implemented and records are organized for external review. A reasonable compromise allows for-cause audits with 48 to 72 hours’ notice for events above a defined severity threshold, and unannounced audits only if the sponsor has documented evidence of data integrity concern.

Key Takeaways: Performance Monitoring

Three-level oversight (operational, tactical, strategic) with defined metrics at each level is the baseline. Relying on CDMO-curated reports without direct data access is not an oversight model; it is an information dependency.

Deviation frequency is a lagging indicator; deviation classification consistency is a leading one. A CDMO that systematically classifies deviations as minor to minimize client notification is a quality culture problem, not a data management one.

For-cause audit rights with 48-72 hour notice for defined quality events are a reasonable compromise. Unannounced audits should be reserved for documented data integrity concerns, not routine oversight.

Change control notification to the client before implementation, regardless of the CDMO’s internal change classification, prevents regulatory submission errors and post-approval manufacturing supplement surprises.

9. Investment Strategy: What CDMO Contract Intelligence Tells Analysts

CDMO contracts are material contracts for drug development companies. They determine whether a drug reaches market on schedule, what the manufacturing cost structure looks like at commercial scale, and who owns the process technology that makes commercial manufacturing possible. Analysts who evaluate biotech sponsors without analyzing the CDMO relationship are missing a category of execution risk that is not captured in pipeline status tables or clinical trial enrollment metrics.

Reading CDMO Risk in Sponsor Disclosures

SEC filings require disclosure of material contracts, and for development-stage companies, the CDMO agreement often qualifies. Reading the disclosed contract summary, or the contract itself when filed as an exhibit, reveals several things that are not in the pipeline summary: whether the sponsor has secured commercial-scale manufacturing capacity, what the change-of-control provisions are (relevant post-Catalent acquisition), whether IP ownership is clearly assigned to the sponsor, and what the termination economics look like if the program is discontinued.

Companies that have not secured commercial manufacturing commitments for late-stage programs are carrying execution risk that should be modeled in probability-of-approval adjustments. A Phase III asset with no commercial manufacturing partnership is not just awaiting regulatory approval; it is also awaiting a manufacturing negotiation that will take 12 to 18 months to complete and may result in capacity constraints, IP concessions, or cost structures that were not modeled in analysts’ commercial forecasts.

CDMO Sector Equity: What the Consolidation Wave Signals

The Novo-Catalent transaction values CDMO assets at approximately 4 to 5 times revenue, consistent with prior transactions including Thermo Fisher’s acquisition of Brammer Bio at a premium for viral vector capability. The premium drivers are facility certifications (EMA and FDA multi-product compliance), process development expertise (particularly for complex modalities like AAV, ADC, and mRNA), regulatory dossier history (demonstrated pre-approval inspection success), and capacity scarcity for specific modalities.

For investors in CDMO equity, the consolidation dynamic has two implications. Scale CDMOs with full-service biologics capability are attracting premium valuations and, post-Catalent, the independent full-service biologics CDMO universe is smaller. Remaining independent platforms, Lonza, Samsung Biologics, Fujifilm Diosynth, and Boehringer Ingelheim BioXcellence, carry strategic premium for potential acquirers including large pharmaceutical companies that want to secure manufacturing capacity without paying per-batch rates. The second implication is that niche CDMOs with specific modality expertise in areas like lentiviral vectors, lipid nanoparticle formulation, or high-potency API synthesis carry acquisition premium disproportionate to their current revenue if their technical capabilities are difficult to replicate.

Using Patent Landscape Data in CDMO Due Diligence

DrugPatentWatch and comparable patent intelligence platforms allow systematic analysis of CDMO-affiliated patent portfolios by assignee name, filing date, technology classification, and citation network. This analysis serves four functions in investment and business development contexts. First, it identifies CDMOs with genuine platform IP (patented process innovations, not just trade secrets), which indicates both technical depth and potential licensing revenue. Second, it flags potential conflict-of-interest situations where a CDMO holds platform patents that could intersect with a target sponsor’s manufacturing process. Third, it reveals which CDMOs are actively expanding their IP portfolios in specific modality areas, which is a leading indicator of where they are investing and what client categories they are competing for. Fourth, for generic and biosimilar manufacturers, CDMO process patents assigned to the originator’s manufacturing partner are part of the freedom-to-operate landscape even when the originator’s own patent portfolio shows no process claims.

Companies that systematically integrate patent landscape data into their CDMO selection, contracting, and competitive intelligence processes have a measurable information advantage over those that treat patent analysis as a one-time activity conducted only when litigation risk becomes obvious. The 61 percent higher market growth rate observed among companies that actively monitor patent data, cited in research across pharmaceutical business intelligence platforms, reflects the compounding benefit of early information on competitive positioning and IP risk.

Investment Strategy: Full Framework

Include CDMO contract analysis in due diligence for biotech investments, particularly for companies with Phase II or later assets. Key questions: Is commercial manufacturing capacity secured? Who owns the manufacturing process IP? What are the change-of-control provisions post-Catalent?

Model CDMO process patent royalties as a cost line in commercial manufacturing margin projections. For biologics, this cost is real and often undisclosed in sponsor financials. DrugPatentWatch analysis by CDMO assignee name can identify relevant process patents.

CDMO equity premium is concentrated in full-service biologics platforms with EMA and FDA commercial-scale capability and demonstrated multi-product compliance. The post-Catalent universe of independent platforms in this tier is thin, and strategic acquirer interest remains high.

Niche CDMOs with specific modality expertise in AAV, LNP, ADC, or HPAPI synthesis carry acquisition premium disproportionate to current revenue if their technical capabilities are regulatory-validated and capacity-constrained.

Geopolitical risk in CDMO contracts is now a material investment risk, not a boilerplate disclosure. Sponsors with Chinese CDMO dependencies and inadequate change-of-control or geopolitical-trigger provisions carry regulatory and reputational exposure that affects valuation.

The BIOSECURE Act and tariff pressure are structural tailwinds for US and European CDMOs through at least 2027. Investors in Western-domiciled CDMOs with clean regulatory records and domestic capacity should price in the friend-shoring premium that sponsors are now willing to pay for supply security.

10. Key Takeaways

Executive Summary: The Complete CDMO Contract Framework

Market structure has changed fundamentally. The Novo-Catalent acquisition, BIOSECURE-driven restructuring, and consolidation among full-service biologics CDMOs have reduced the supply of independent commercial-scale partners and elevated the strategic value of early capacity reservation. Sponsors in late-stage development without secured commercial manufacturing capacity are carrying material execution risk.

The SOW is the most important document in the contract package. Every ambiguity in deliverable definitions, acceptance criteria, or change control procedures becomes a dispute during development. Investing in SOW precision before execution is the highest-return risk management activity available to sponsor teams.

IP ownership in CDMO development agreements requires active management, not contractual boilerplate. Background IP, foreground IP, and derivative IP each need their own ownership and licensing treatment. Springing licenses protect manufacturer-switch rights without requiring full IP transfer. CDMO process patents should be analyzed as part of the sponsor’s total patent landscape and the biosimilar entry timeline.

Change-of-control provisions must address operational consequences of M&A, not just formal ownership transfer. Key personnel departure, capacity reallocation to new owner programs, and conflict-of-interest scenarios with new strategic investors should each be defined as independent termination triggers.

AI and digital platform data-use restrictions are now essential confidentiality clause elements. Prohibit CDMO use of client data to train or improve AI models that benefit third parties. Require data residency specifications and audit rights on digital systems, particularly for programs with national security or GDPR implications.

Quality Assurance Agreements must be executed before or simultaneous with the MSA. Deferring QAA negotiation until after commercial terms are agreed inverts the risk priority and transfers leverage to the CDMO on the quality provisions that govern actual operations.

CDMO patent portfolios are material to both IP valuation and biosimilar entry analysis. Process patents assigned to CDMOs do not appear in sponsor patent lists but are fully enforceable against alternative manufacturers. DrugPatentWatch and comparable tools enable systematic analysis of CDMO-affiliated patents by assignee, which should be a standard component of patent landscape reviews.

Geopolitical risk provisions are no longer optional. BIOSECURE Act consequences, tariff pressure on imported pharmaceuticals, and friend-shoring requirements from government-funded programs have made CDMO geographic risk a material contract risk. Every new CDMO agreement should specify geopolitical triggering events, transition funding obligations, and tech-transfer cost allocation in the force majeure and change-of-control provisions.

Market data: Research and Markets (February 2026), Mordor Intelligence (January 2026), ProGen Search CGT CDMO Report Q3 2025, Vision Lifesciences CDMO Market Analysis 2026, VectorBioMed (February 2026). Patent intelligence: DrugPatentWatch. Regulatory reference: FDA Quality Agreements Guidance; FDA ALCOA+ data integrity guidance. M&A reference: Alvarez & Marsal CDMO M&A Market analysis. Clinical pipeline: FDA NME approvals data 2024. All financial figures in USD unless stated.

This analysis is produced for informational purposes for pharmaceutical IP teams, R&D leads, and institutional investors. It does not constitute legal advice. For contract-specific legal guidance, consult qualified pharmaceutical transactional counsel.