The definitive guide to sildenafil IP strategy, authorized generics, evergreening tactics, and what the Viagra case teaches pharma teams about post-LOE revenue defense

1. The Patent Cliff Problem: What $200 Billion at Risk Actually Means

1.1 Defining Loss of Exclusivity (LOE) and Its Financial Mechanics

Patent expiration in pharmaceuticals is not a gradual process. It is a hard stop. When a small-molecule drug loses its last valid patent claim, the FDA can approve Abbreviated New Drug Applications (ANDAs) from generic manufacturers on day one, and the market typically sees 80-90% brand erosion within 12 months. Price erosion follows the same curve, often faster: brand prices fall 50% or more in the first year post-generic entry, and generic prices continue compressing toward API cost as additional filers receive approval.

The industry currently has roughly $200 billion in branded revenue exposed to patent expiration within a five-year window. That figure includes major assets across oncology, immunology, and metabolic disease, making LOE defense one of the highest-return activities a pharma IP or commercial team can pursue. A one-year extension of exclusivity on a drug generating $1.5 billion annually is worth more in risk-adjusted NPV than most mid-stage pipeline programs.

Pfizer learned this arithmetic with Viagra before most of the industry had a formal playbook for it. The result was a multi-instrument defense that kept sildenafil commercially relevant for over 15 years past its initial blockbuster period, across two separate branded indications, in markets ranging from the United States to South Korea.

1.2 Why Viagra Is the Right Case Study

Sildenafil’s story is not representative of every small-molecule LOE event. It is representative of the best-case outcome when a company executes IP, regulatory, commercial, and distribution strategy simultaneously. The compound had a discoverable second indication (pulmonary arterial hypertension), a strong cultural identity, a generics market entry that Pfizer could negotiate rather than merely suffer, and a consumer psychology that made brand premium sustainable. Most drugs have fewer of these levers available. But the analytical framework Pfizer applied, compound-level IP valuation rather than product-level, is broadly replicable. That is the lesson this article is structured to extract.

Key Takeaways – Section 1:

LOE events produce 80-90% brand erosion within 12 months under normal conditions; Pfizer achieved far better outcomes through active intervention.

The $200 billion in industry-wide patent exposure over the next five years makes LOE defense a high-priority capital allocation question, not just a legal one.

Sildenafil’s outcome reflects compound-centric lifecycle management, a methodology any pharma team with a mature small-molecule asset should model.

2. Sildenafil’s IP Architecture: A Compound-Centric Valuation Deep Dive

2.1 The Patent Estate That Protected $10+ Billion in Cumulative Revenue

Sildenafil’s commercial IP estate is best understood as a layered structure, not a single patent. At its core sat the composition-of-matter patent covering sildenafil citrate itself. Surrounding that were use patents (erectile dysfunction, pulmonary arterial hypertension), formulation patents, method-of-treatment patents, and ultimately the pediatric exclusivity extension that delayed generic entry in the United States past Pfizer’s original timeline.

The patent filed in 1994 specifically covering sildenafil’s use in treating ED defined the primary US market exclusivity window, which originally ran to October 2019 and was extended to April 2020 via the pediatric exclusivity program. The separate cardiovascular-use patent, filed in 1992 and covering what would become Revatio, expired in 2012. That staggered expiration is not accidental. It reflects deliberate prosecution strategy, filing use claims in a sequence that maximized total commercial coverage across both indications.

2.2 IP Valuation of the Sildenafil Estate

From a discounted cash flow perspective, Pfizer’s sildenafil patent estate was worth materially more than the revenue Viagra alone generated. The standard approach to pharmaceutical IP valuation applies a probability-adjusted NPV to each remaining year of exclusivity, discounted at a rate that reflects litigation risk, regulatory risk, and commercial execution risk.

For Viagra specifically, the US pediatric exclusivity extension covering December 2017 through April 2020, the period during which Teva paid royalties and no unrestricted generic entry occurred, had an estimated net present value of several hundred million dollars at the time the pediatric study was initiated. That is a return on a relatively modest clinical investment (pediatric pharmacokinetic studies are not expensive by Phase III standards), demonstrating that regulatory-pathway IP extensions generate some of the highest risk-adjusted returns available in pharmaceutical portfolio management.

The Revatio (sildenafil for PAH) patent estate ran separately and expired in 2012. Its commercial contribution was smaller than Viagra’s, but it established the principle that Pfizer was managing sildenafil as a compound asset rather than a single-indication product. By the time generic Revatio entered the market in 2012, Pfizer had already extracted years of PAH-market exclusivity revenue, and the generic PAH entry did not affect Viagra’s US exclusivity at all, because the two products sat under distinct use-patent claims.

2.3 Patent Thicket Construction Around Sildenafil

A full patent thicket around sildenafil included claims across at least four distinct layers: the active compound, specific crystalline salt forms, the oral dosage form and its pharmacokinetic profile, and the method of treatment in specific patient populations. This layering is the standard architecture for a mature small-molecule pharmaceutical IP strategy. Each layer creates a separate filing date, a separate expiration date, and a separate litigation target for generic challengers. Knocking out one layer does not automatically invalidate the others, which forces generic filers to run parallel Paragraph IV challenges against multiple claims simultaneously.

For Pfizer, this construction meant that a generic manufacturer filing an ANDA against Viagra was not simply challenging one patent. It was challenging a coordinated cluster of claims, each of which, if upheld in litigation, could delay market entry independently. This is why patent thicket construction is now standard practice for any small-molecule asset generating over $500 million annually, and why generic companies invest heavily in pre-filing patent landscape analysis before committing to ANDA programs.

Key Takeaways – Section 2:

Sildenafil’s IP estate was structured across at least four distinct patent layers, each with independent expiration dates and litigation targets.

The pediatric exclusivity extension on the Viagra ED use patent generated several hundred million dollars in risk-adjusted NPV for a modest clinical investment.

Pfizer’s separation of the ED and PAH patent estates allowed Revatio generics to enter in 2012 without disrupting Viagra’s US exclusivity.

3. Pfizer’s Patent Filing Chronology and the Pediatric Exclusivity Play

3.1 Full Timeline of Key IP Events

Understanding Pfizer’s strategy requires mapping the filing dates and expiration dates in sequence:

Event

Date

Sildenafil discovered in Pfizer labs

1989

Cardiovascular/PAH use patent filed

1992

ED use patent filed

1994

FDA approval of Viagra (ED)

March 1998

Revatio PAH patent expiration

2012

Generic sildenafil entry in Canada

2012

Generic sildenafil entry in UK/EU

June 2013

Pfizer-Teva settlement signed

December 2013

Teva authorized US market entry

December 11, 2017

Pfizer Greenstone AG launched

December 11, 2017

Original US Viagra patent expiration

October 2019

Final US Viagra patent expiration (pediatric extension)

April 2020

3.2 The Pediatric Exclusivity Mechanism

The Best Pharmaceuticals for Children Act (BPCA) grants six months of additional market exclusivity to drugs whose manufacturers conduct FDA-requested pediatric studies, regardless of whether the drug is actually used in pediatric populations or whether the studies show any pediatric benefit. For Viagra, Pfizer completed the required studies and received the six-month extension appended to the ED use patent’s October 2019 expiration, pushing the final date to April 2020.

The practical value of this extension was not primarily about Pfizer’s own brand revenue during that period. By December 2017, branded Viagra had already ceded significant market share to generic sildenafil and Pfizer’s own Greenstone authorized generic. The value was in the royalty income from Teva. Under the 2013 settlement terms, Teva was required to pay royalties to Pfizer through April 2020. Those royalty payments gave Pfizer a financial stake in Teva’s generic sildenafil revenue, transforming a competitive threat into a licensing relationship. The pediatric extension effectively extended that royalty obligation by six months beyond the original patent expiration.

3.3 Implications for Modern LOE Defense

The pediatric exclusivity play illustrates a broader principle: exclusivity extensions through regulatory pathways are systematically underexploited by pharma IP teams. The BPCA extension, the Hatch-Waxman Act’s five-year new chemical entity (NCE) exclusivity, the FDA’s Orphan Drug Designation exclusivity for rare disease indications, and the three-year exclusivity for new clinical investigations are all available tools. Combined with standard patent term restoration under 35 U.S.C. §156, which compensates for time lost during FDA review, a diligent team can routinely add three to five years of effective commercial exclusivity to a well-managed compound’s baseline patent life.

Key Takeaways – Section 3:

The pediatric exclusivity extension shifted Pfizer’s US final LOE date from October 2019 to April 2020, and its primary value was extending the royalty obligation in the Teva settlement, not brand revenue.

Hatch-Waxman’s suite of exclusivity pathways (NCE, pediatric, orphan drug, new clinical investigation) can add three to five years to effective market exclusivity when systematically pursued.

Pharma IP teams routinely leave regulatory exclusivity extensions on the table because they are managed separately from commercial and portfolio strategy.

4. The Paragraph IV Litigation Campaign and the Teva Settlement

4.1 How Paragraph IV Challenges Work Against Established Brands

Under the Hatch-Waxman Act, a generic manufacturer filing an ANDA against a patented drug must include one of four certifications. Paragraph IV is the most aggressive: it certifies that the listed patents are either invalid or will not be infringed by the generic product. Filing a Paragraph IV certification triggers a 30-month automatic stay on FDA approval while the patent holder litigates the challenge. If the innovator sues within 45 days of receiving notice, the stay activates.

For Viagra, multiple generic manufacturers filed Paragraph IV certifications targeting the ED use patent and related claims. Pfizer’s legal team pursued litigation against each filer. This is expensive, time-consuming litigation with uncertain outcomes, but it is almost always worth initiating for a drug generating over $1 billion annually. The 30-month stay alone is worth hundreds of millions in preserved exclusivity revenue, even if the innovator ultimately loses at trial.

4.2 The Teva Settlement: Engineering Generic Entry

By December 2013, Pfizer had negotiated a settlement with Teva Pharmaceuticals that permitted Teva to launch its generic sildenafil citrate on December 11, 2017, approximately two years before the original patent expiration in October 2019. The settlement required Teva to pay Pfizer royalties through April 2020.

From Pfizer’s perspective, this was a rational trade. Prolonged patent litigation against Teva carried the risk of an invalidation ruling that would have eliminated Pfizer’s exclusivity entirely, potentially opening the market to all ANDA filers simultaneously. A negotiated entry allowed Pfizer to control the timing, capture royalty income from Teva’s generic revenue, and prepare its authorized generic launch for the same day. It also gave Pfizer two additional years of fully branded Viagra sales at premium pricing, since Teva’s December 2017 launch came before the October 2019 original expiration but within a window Pfizer had planned for.

The settlement structure, a form of reverse payment where the innovator grants earlier entry in exchange for royalties rather than a cash payment to the generic filer, sits in a legally scrutinized zone following the FTC v. Actavis (2013) Supreme Court ruling. The Actavis decision held that reverse-payment settlements are subject to antitrust scrutiny under a rule-of-reason standard. Pfizer’s royalty-based arrangement with Teva post-dates Actavis and reflects the industry’s adaptation to that new legal environment: royalties paid to the innovator rather than cash paid to the generic manufacturer are generally viewed as more defensible under antitrust review, though each settlement structure requires independent legal analysis.

4.3 First-Filer Exclusivity and Its Strategic Implications

Under Hatch-Waxman, the first ANDA filer with a Paragraph IV certification earns 180 days of generic market exclusivity before other generic manufacturers can receive approval. This first-filer advantage is commercially valuable and shapes the settlement negotiation. Teva, as a first filer, had leverage: its 180-day exclusivity period meant that an agreed-upon early entry would give Teva a duopoly period with only Pfizer’s authorized generic as competition, rather than a crowded multi-filer generic market.

For Pfizer, this meant that its authorized generic (launched through Greenstone on December 11, 2017) would compete in a market with only one independent generic during Teva’s 180-day exclusivity window. That duopoly structure allowed Pfizer/Greenstone to capture a larger authorized generic market share during those first six months than would have been possible in a multi-filer environment.

Key Takeaways – Section 4:

Paragraph IV settlements post-Actavis require structuring as royalty arrangements rather than cash reverse payments to reduce antitrust exposure.

The Pfizer-Teva settlement gave Pfizer controlled timing, royalty income, and a duopoly period for its authorized generic during Teva’s 180-day first-filer exclusivity window.

For drugs over $1 billion in annual revenue, initiating Hatch-Waxman litigation is almost always NPV-positive based on the 30-month stay value alone, regardless of litigation outcome.

5. Evergreening in Practice: How Revatio Extended Sildenafil’s Commercial Life

5.1 What Evergreening Actually Is (And What It Is Not)

Evergreening refers to the practice of obtaining new patents on incremental innovations related to an existing compound, including new formulations, new dosing regimens, new patient subpopulations, new indications, new salt forms, or new delivery mechanisms, in order to extend effective market exclusivity beyond the original compound patent’s expiration.

Evergreening is legal. It is also controversial. From a patent theory perspective, each incremental innovation that meets the criteria for patentability (novelty, non-obviousness, utility) is entitled to its own protection. From a competition policy perspective, some evergreening strategies, particularly those targeting slightly modified formulations with no clinical improvement, are criticized for using the patent system to delay generic competition without generating patient benefit.

Pfizer’s sildenafil evergreening falls primarily in the defensible category because the PAH indication (Revatio) represents a genuinely distinct therapeutic application with separate clinical development, a separate NDA, and separate IP claims from the ED indication. It is not a reformulation of the same product; it is a different product in a different therapeutic area, even though the active ingredient is identical.

5.2 The Revatio (PAH) Indication: Technology Roadmap and IP Value

Sildenafil’s mechanism as a phosphodiesterase type 5 (PDE5) inhibitor produces vasodilation through increased cyclic GMP. In pulmonary arterial hypertension, this mechanism translates to reduced pulmonary vascular resistance, making it clinically relevant for a condition where excessive pulmonary vascular tone causes right heart failure.

The development path for Revatio required Phase III clinical trials demonstrating efficacy in PAH patients, a separate NDA, separate labeling, and separate patent filings covering the PAH-specific use claims. The PAH patent filed in 1992 predated the ED use patent, reflecting the original cardiovascular research focus of the sildenafil program. Revatio received FDA approval in 2005.

When the Revatio PAH patent expired in 2012, generic sildenafil for PAH entered the market. This did not affect Viagra’s US exclusivity because the two products operated under distinct use claims. The financial contribution of Revatio to Pfizer’s sildenafil revenue over its exclusivity period (2005-2012 in the US) represents pure uplift from compound-level lifecycle management. Without the Revatio development program, that revenue would not exist. With it, Pfizer captured at least several billion dollars in additional cumulative revenue from a compound whose primary indication exclusivity was already winding down.

5.3 The Compound-Level Lifecycle Management Roadmap

Sildenafil’s dual-indication history demonstrates a compound lifecycle model that modern pharma IP and R&D teams should apply systematically. The roadmap has four stages:

First, during the initial exclusivity period of a blockbuster indication, commission broad IP landscape analysis to identify additional therapeutic areas where the compound’s mechanism may have clinical relevance. For PDE5 inhibitors, that analysis correctly identified cardiovascular applications beyond ED.

Second, file IND applications and initiate Phase II proof-of-concept trials in the most promising secondary indications early, targeting completion before the primary patent’s peak revenue years end. Revatio’s development consumed resources during Viagra’s growth phase, but the clinical investment was modest relative to the incremental IP value created.

Third, pursue new use-patent filings contemporaneously with clinical development, ensuring that patent protection on secondary indications is established and defensible before generic challengers can mount Paragraph IV attacks.

Fourth, manage the two commercial programs as separate but coordinated IP estates, with independent patent expiration dates, independent litigation strategies, and independent authorized generic planning for each LOE event.

Key Takeaways – Section 5:

Revatio represents legitimate evergreening: a distinct therapeutic indication, separate NDA, and independent patent estate built on the same active compound.

The four-stage compound lifecycle management roadmap (landscape analysis, early-stage trials, parallel patent filing, coordinated estate management) is replicable for any small-molecule asset with broad mechanism-of-action applicability.

When the Revatio PAH patent expired in 2012, it had no effect on Viagra’s US LOE date, demonstrating the practical value of filing use claims under separate, independently defensible patent positions.

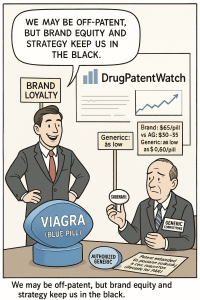

6. The Authorized Generic Weapon: Greenstone, Market Segmentation, and First-Day Cannibalization

6.1 How Authorized Generics Work

An authorized generic (AG) is a version of a brand-name drug that the brand-name manufacturer licenses or distributes through a subsidiary or partner, marketed under the generic drug’s nonproprietary name. Unlike ANDAs, authorized generics do not require a separate FDA approval; they operate under the brand’s existing NDA. They are chemically and biologically identical to the brand.

Because AGs bypass the ANDA process, the brand-name manufacturer can launch an AG on the same day the first generic filer receives ANDA approval, effectively entering the generic market through the front door on day one of competition. This is what Pfizer did through its subsidiary Greenstone LLC on December 11, 2017, the exact day Teva launched its sildenafil generic.

6.2 Pfizer’s Greenstone Strategy: Pricing, Positioning, and Revenue Impact

Greenstone launched sildenafil at $30-$35 per pill, approximately half the $65 list price of branded Viagra. Teva’s generic launched at a comparable price point. Within 18 months, other generic manufacturers (five distinct ANDA approvals in the US alone) drove prices down to $0.60 per pill for some dosage forms, and wholesale channels like Costco offered 20mg tablets at $4 per unit.

The Greenstone AG’s primary function was not to capture the low end of the market permanently. It was to prevent Teva from using the 180-day first-filer exclusivity period to establish sole generic dominance. By placing a Pfizer-affiliated product in the generic market on day one, at a comparable price, Pfizer divided the price-sensitive market segment rather than ceding it entirely to Teva.

The FTC has historically raised concerns about authorized generics reducing generic manufacturers’ incentives to file Paragraph IV challenges, since the first-filer’s 180-day exclusivity is diluted by AG competition. This tension is real and has influenced policy discussions, but from the innovator’s perspective, AGs remain a legitimate and often rational market defense tool.

6.3 The Dual-Product Portfolio: Brand + AG as a Segmentation Model

Pfizer’s simultaneous management of premium-priced Viagra and Greenstone’s generic sildenafil created a two-tier pricing architecture in a single therapeutic category. This is textbook second-degree price discrimination: offering the same underlying product at different price points to capture consumer surplus across willingness-to-pay segments.

The segment paying $65+ for branded Viagra consists primarily of consumers who associate the blue pill’s specific identity with reliability, those whose insurance coverage or co-pay cards make the brand cost-competitive, and prescribers following Dispense As Written (DAW) instructions tied to patient co-pay card programs. The segment paying $30-$35 for the Greenstone AG consists of price-aware consumers who accept generic labeling but prefer a Pfizer-affiliated product. The segment paying $0.60-$4 for unbranded generic sildenafil consists of cost-primary consumers, telemedicine platform users, and cash-pay patients.

By holding a product in all three price tiers, Pfizer minimized revenue loss across the full post-LOE market. The brand retained its margin-heavy premium segment. Greenstone captured mid-tier volume. Royalties from Teva gave Pfizer a stake in the competitive generic tier as well. Very few brand-name manufacturers execute all three simultaneously, and the Viagra case is among the clearest examples of this approach done well.

Key Takeaways – Section 6:

Greenstone’s same-day authorized generic launch diluted Teva’s 180-day first-filer exclusivity advantage and prevented Teva from achieving solo generic dominance during the duopoly window.

The three-tier pricing architecture (brand, AG, commodity generic) allowed Pfizer to retain revenue across all willingness-to-pay segments simultaneously.

The FTC’s concerns about AGs reducing Paragraph IV filing incentives for generic firms are real but do not affect the innovator’s cost-benefit analysis; from Pfizer’s position, the AG was NPV-positive regardless of the policy debate.

7. Pricing Mechanics: From $65 to $0.60, and the Premium Brand That Held

7.1 The Price Compression Curve Post-LOE

Sildenafil’s generic price trajectory followed the standard Hatch-Waxman compression pattern but compressed faster than most therapeutic categories because of the drug’s high commercial profile, large ANDA applicant pool, and strong consumer interest. Within 18 months of December 2017, generic sildenafil prices collapsed from $30-$35 (Teva first-filer pricing) to sub-$1 for some market segments.

The numbers in full: branded Viagra at approximately $65 per pill pre-LOE; Pfizer’s Greenstone AG at $30-$35 on launch day; Teva generic at comparable pricing; other generics within 18 months at $0.60-$4 depending on channel, dosage form, and quantity. Costco’s wholesale pharmacy offered 20mg tablets at $4 per unit. Telehealth platform Rex MD marketed sildenafil at $2 per dose for subscription members.

7.2 The Counter-Intuitive Branded Price Increase

In July 2018, approximately seven months after generic sildenafil flooded the US market, Pfizer raised the list price of branded Viagra. Post-generic list prices ranged from $90 to $139 per dose depending on channel. This move appears irrational at first read but makes sense within the brand’s co-pay card strategy.

When brand list prices are high, payer/PBM contracts push heavily toward generic substitution. But when brands deploy co-pay cards to offset patient out-of-pocket costs, the patient’s effective cost can equal or undercut the generic co-pay, making the brand commercially competitive at the pharmacy counter even at a $100+ list price. The higher list price primarily affects payers and PBMs rather than co-pay card users, and increasing the list price expands the margin available for co-pay card subsidies. This is the mechanism by which brands compete against generics not on net price but on patient-facing economics, while simultaneously extracting higher rebate negotiations from PBMs.

7.3 Insurance Coverage and Formulary Dynamics

Most Medicare Part D plans do not cover branded sildenafil for ED. This reflects CMS’s exclusion of drugs for sexual dysfunction from the Part D formulary categories that require coverage. The practical result is that Medicare beneficiaries who want sildenafil pay out-of-pocket, which pushes them strongly toward generic pricing, typically $0.60-$4 per pill through discount programs like GoodRx.

Commercial insurance coverage for branded Viagra varies by plan and employer. Many plans cover generic sildenafil at a Tier 1 or Tier 2 co-pay but place branded Viagra on Tier 3 or 4, or exclude it entirely. The DAW mechanism allows prescribers to block generic substitution at the pharmacy, but this is typically activated through Pfizer’s HCP co-pay card and patient assistance programs, creating a specific, targeted population of brand-adherent patients.

Key Takeaways – Section 7:

Generic sildenafil’s price collapsed from $65 to under $1 within 18 months of LOE in the US, consistent with multi-filer generic market dynamics.

Pfizer’s July 2018 brand price increase to $90-$139 per dose was a co-pay card economics move, not irrational pricing; higher list prices expand the margin available for patient-facing co-pay subsidies.

Medicare Part D’s ED drug coverage exclusion forces most government-insured patients into the generic market, segmenting the brand-responsive population toward commercial insurance and cash-pay consumers.

8. Brand Equity as a Moat: What Lifestyle Drugs Can Do That Specialty Drugs Cannot

8.1 Building the Brand Before the Patent Expires

Pfizer’s direct-to-consumer (DTC) investment in Viagra began immediately after its 1998 approval and ran continuously for over a decade. The campaign’s celebrity endorsers, Bob Dole and Pelé, were not chosen to reach existing ED patients. They were chosen to normalize the condition for men who did not yet identify as having ED but were experiencing symptoms they attributed to aging or stress. This was deliberate disease-state expansion: converting a condition primarily associated with illness or injury into a concern for healthy, active men.

Pfizer’s marketing also drew a direct connection between erectile capacity and masculine identity, framing Viagra not as a medical treatment but as a means of maintaining virile masculinity regardless of age. This framing, documented in academic literature on pharmaceutical advertising, turned a prescription drug into a lifestyle product with near-universal name recognition. By 2000, Viagra held 92% of the global prescribed ED drug market. That market share reflects not just clinical efficacy but brand penetration driven by a sustained, high-investment consumer marketing program.

8.2 The Behavioral Economics of Generic Resistance

A 2015 US national survey (n = approximately 1,000) found that 83% of respondents agreed physicians should prescribe generics when available, and 87% considered generics as effective as brand-name drugs. Yet 46% of the same respondents reported requesting a brand-name drug over a generic at some point in the past year.

This behavioral gap, between stated preferences and actual behavior, is particularly pronounced for lifestyle drugs where identity and psychology are embedded in the brand. Sildenafil’s generic version is bioequivalent to Viagra under FDA standards, meaning it reaches the same Cmax and AUC within 80-125% of the brand’s pharmacokinetic parameters. There is no clinical basis for expecting different efficacy. Yet a substantial population prefers the blue pill with the Pfizer name.

The practical explanation combines several factors. Some consumers distrust the manufacturing quality of generic facilities despite FDA equivalence standards. Some consumers attribute the brand-name product with a degree of reliability that anxiety about sexual performance specifically amplifies. Some consumers have never been offered a clear explanation of what bioequivalence means in practice. And some consumers have simply been told by their prescribers, through DAW instructions tied to co-pay card programs, to stay with the brand. The result is a segment of demand that is genuinely price-inelastic, willing to pay $65+ for an outcome that $4 generic sildenafil achieves at the same rate.

8.3 When Brand Equity Survives Generic Entry

The cases where branded drugs maintain meaningful share after LOE share several characteristics that the Viagra case exemplifies. The brand had extensive DTC investment before generic entry, creating deep consumer name recognition. The therapeutic category has a psychological or lifestyle dimension that amplifies brand attachment beyond clinical efficacy. The drug’s physical identity, Viagra’s color and shape specifically, is distinctive enough to become independently iconic. The company deployed a co-pay card and DAW program that made the brand cost-competitive at point of sale for a specific, targetable patient segment.

Not every drug has all of these characteristics. Specialty biologics compete differently, and the biosimilar interchangeability landscape operates under distinct regulatory standards. But for PDE5 inhibitors, diabetes medications, and several categories of cardiovascular drugs where DTC investment has been heavy, brand equity is a real asset that generates cash flow long past patent expiration.

Key Takeaways – Section 8:

Brand equity for lifestyle drugs generates quantifiable post-LOE cash flows; the behavioral gap between stated generic preference (87% say generics are equally effective) and actual brand-requesting behavior (46% do so) is the mechanism.

Pfizer’s DTC investment in disease-state expansion (converting aging symptoms into treatable ED) created demand beyond the existing patient population, multiplying the addressable market before generic entry.

DAW campaigns tied to co-pay card programs are the primary mechanism for converting brand equity into measurable prescription-level brand retention post-LOE.

9. OTC Reclassification as a Regulatory Arbitrage Tool

9.1 The UK OTC Approval and Its Strategic Logic

In November 2017, the UK Medicines and Healthcare products Regulatory Agency (MHRA) approved sildenafil 50mg (marketed as Viagra Connect) for over-the-counter sale without a prescription. This made the UK the first major market to offer prescription-free branded sildenafil, and the approval came the month before generic sildenafil flooded the US market.

The strategic logic is specific. OTC reclassification creates a distinct product category that operates outside the prescription generic substitution framework. A pharmacist dispensing a prescription for sildenafil will typically substitute to the cheapest generic. A consumer walking into a pharmacy and purchasing an OTC product specifically asks for Viagra Connect by name, making brand substitution far less automatic. The OTC channel essentially moves the product outside the formulary and DAW system entirely, placing the purchase decision back in the consumer’s hands.

9.2 What OTC Reclassification Does to IP Value

OTC approval extends a product’s commercial addressable market by reaching consumers who would not visit a physician for a prescription. For ED specifically, clinical estimates suggest that a large proportion of men with symptoms do not seek prescription treatment, citing stigma, inconvenience, or cost as barriers. OTC availability removes those barriers for the branded product while maintaining a price premium over prescription generics (which remain prescription-only in most markets).

From an IP and portfolio value perspective, OTC reclassification is best understood as a commercial exclusivity mechanism rather than a patent extension. It does not extend the patent term. It creates a consumer segment, self-treating OTC purchasers, in which the brand retains a structural advantage because no prescription-based generic substitution mechanism exists in that channel. The value of this advantage depends on the size of the untapped OTC consumer population, the marketing investment Pfizer makes in the OTC channel, and the price premium the brand can sustain against the fringe competition from prescription generics that determined consumers can still access.

9.3 Regulatory Pathway for OTC Reclassification

In the United States, OTC reclassification for a prescription drug requires either an NDA supplement supported by consumer labeling studies and OTC safety data, or a regulatory pathway through the FDA’s nonprescription drug review process. The FDA has not approved an OTC sildenafil product for the US market as of mid-2026. The UK approval provides a proof-of-concept regulatory dossier that could support a US filing, but the FDA’s OTC standards for ED drugs include specific requirements around consumer self-diagnosis capability and safety in the absence of physician oversight. Pfizer has not publicly disclosed a US OTC reclassification filing for sildenafil as of the date of this article.

Key Takeaways – Section 9:

UK OTC approval for Viagra Connect created a brand-controlled consumer purchasing channel outside the prescription generic substitution framework, protecting brand preference through self-selection.

OTC reclassification functions as a commercial exclusivity mechanism: it is not a patent extension but a channel strategy that removes the formulary and generic substitution infrastructure from the purchase decision.

The US OTC regulatory pathway for sildenafil remains unexercised as of 2026; the UK approval provides a precedent dossier that could support a US application.

10. Generic Entry Timelines by Region: US, EU, and South Korea

10.1 The US Timeline

US generic entry began on December 11, 2017, under the Pfizer-Teva settlement, not at patent expiration. Five generic sildenafil citrate approvals followed within 18 months. Price compression occurred rapidly, from $30-$35 per pill (Teva first-filer pricing) to $0.60-$4 depending on dosage and channel. Pfizer retained approximately 15% of the overall US sildenafil market post-generic flood. The US is notable for its complex branded strategy: co-pay cards, DAW programs, and the Greenstone AG running in parallel.

10.2 The European Timeline and Earlier Cliff

Generic sildenafil entered European markets in June 2013, approximately six years before US generic entry. The EU patent expiration reflected a different patent landscape, specifically the shorter EU data exclusivity periods and different patent term structures compared to Hatch-Waxman. In the UK, post-generic sildenafil prices fell to as low as 97p per tablet, representing a 95%+ price reduction from the original branded Viagra price.

European markets also moved more quickly toward OTC availability, culminating in the UK’s 2017 Viagra Connect approval. The faster generic entry and earlier OTC pathway in Europe gave Pfizer less runway for branded revenue extraction but also gave the company earlier data on DTC channel performance in an OTC sildenafil environment, data that informed its UK and global OTC strategy.

10.3 South Korea: A Case of Complete Market Reversal

South Korea represents the most extreme case of post-generic brand collapse in the sildenafil market. After generic sildenafil became publicly available in May 2012, Hanmi Pharmaceutical’s generic product ‘PalPal’ captured 86% of the Korean sildenafil market by 2017, while branded Viagra retained only 38% of PalPal’s sales volume in comparative terms. This reversal reflects several market-specific factors: the absence of US-style DTC advertising norms in South Korea, strong physician generic prescribing incentives, lower brand switching costs in the Korean pharmaceutical distribution system, and less effective co-pay card and DAW infrastructure for the Pfizer brand in that market.

The South Korean outcome is the baseline scenario, what happens to brand market share when the standard tools of brand defense (DTC, AG, co-pay card, DAW) are either unavailable or not deployed. It confirms that Pfizer’s US and UK brand retention was not the result of inherent consumer preference for the original product; it was the result of specific, intentional commercial and IP defense strategies.

Key Takeaways – Section 10:

The US achieved approximately 15% brand retention post-LOE through active defense; South Korea’s market flipped to 86% generic within five years with minimal defense deployed.

The EU’s earlier patent expiration (2013 vs 2020 in the US) gave Pfizer an earlier test of brand resilience under generic competition, informing its more aggressive US LOE strategy.

Regional LOE timelines differ substantially based on patent landscape, data exclusivity rules, and Hatch-Waxman equivalents; a compound-level global IP strategy must account for staggered generic entry by territory.

11. Market Share Data: What Actually Happened After LOE

11.1 Sildenafil Market Size and Growth

The global sildenafil market was approximately $3.5 billion in 2023 and is projected to reach $5.5 billion by 2032. The global ED drug market (which includes sildenafil/Viagra, tadalafil/Cialis, vardenafil/Levitra, and their respective generics) was $3.27 billion in 2023 and is forecast to reach $7.74 billion by 2033. Telehealth platform growth, at 12.22% CAGR, is a primary driver of the DTC generic segment’s expansion.

11.2 Pfizer’s Retained Share: Better Than Expected

Post-LOE market share data for Pfizer’s Viagra is counterintuitive. The drug’s peak global sales were $1.934 billion in 2008. After EU generic entry in 2013, global sales declined at an average of 35% year-on-year. By Q3 2020, global Viagra sales reached $121 million, a 29% increase from Q2 2020, likely reflecting pandemic-era telehealth demand. By 2023, the Viagra brand segment retained 37.3% of the overall ED drugs market and 45.35% revenue share in 2024. These figures reflect share of the full ED drug market (including Cialis, Levitra, and other branded competitors), not just the sildenafil generic market.

Within the sildenafil-specific segment, Pfizer’s retained share is approximately 15% of US prescriptions post-generic flood. That 15% retention rate is remarkably high relative to most small-molecule LOE events, where brand retention typically falls to 2-5% within three years. The Viagra brand retention rate of 15% reflects the full suite of defensive strategies described in this article: AG deployment, brand DTC investment, DAW and co-pay card programs, and OTC reclassification in select markets.

11.3 Competitor Dynamics: How Cialis and Levitra Changed the Picture

Viagra’s peak market share fell from 92% in 2000 to approximately 50% by 2007, not because of generic sildenafil (which did not enter most markets until 2012-2013) but because of competition from tadalafil (Cialis, Eli Lilly) and vardenafil (Levitra, Bayer/GlaxoSmithKline). Tadalafil’s longer half-life (up to 36 hours versus sildenafil’s four-to-six hours) created a clinically differentiated patient preference segment. By the time generic sildenafil entered the market, Viagra was already competing against these branded alternatives.

This matters for the market share analysis. Viagra’s continued 37-45% segment share in 2023-2024 is not purely a function of brand loyalty to sildenafil over generic sildenafil. It reflects brand loyalty in the broader PDE5 inhibitor category, including patient populations that have stayed with sildenafil rather than switching to tadalafil generics.

Key Takeaways – Section 11:

Pfizer’s 15% retained brand share in the US sildenafil market post-LOE is three to seven times higher than the typical brand retention rate for small-molecule drugs, attributable to active defense strategies.

Viagra’s 37-45% of the overall ED drug market in 2023-2024 includes competition against Cialis, Levitra, and their generics, reflecting category-level brand authority rather than sildenafil-specific loyalty alone.

The global sildenafil market is projected to grow to $5.5 billion by 2032, driven by telehealth DTC distribution growth at 12.22% CAGR.

12. Telemedicine, DTC Platforms, and the New Generic Distribution Infrastructure

12.1 How Telehealth Changed the ED Drug Market

The US telehealth platforms that entered the ED market, including Hims, Ro (Roman), Rex MD, Lemonaid, Optum Perks, and Amazon One Medical, collectively function as a new distribution infrastructure for generic sildenafil. They offer online consultation with licensed physicians, electronic prescription, and home delivery, removing the traditional barrier of an in-person physician visit for a condition many men find stigmatizing to discuss face-to-face.

Telehealth generic sildenafil pricing is dramatically lower than any brick-and-mortar channel: $2-$10 per dose depending on platform and subscription tier, compared to $0.60-$4 for generic sildenafil at wholesale pharmacies. The platform premium reflects convenience, privacy, and the bundled consultation cost, not the drug itself.

12.2 Pfizer’s Response: The Roman Supply Agreement

In January 2020, Pfizer entered into a supply agreement with Roman (now Ro), a direct-to-consumer telehealth men’s health platform, to provide a generic version of Viagra to Roman’s members. This is the most direct evidence that Pfizer explicitly recognized the telehealth channel as a strategic distribution pathway rather than a competitive threat.

By supplying Ro with authorized generic sildenafil, Pfizer captured a portion of the telehealth channel’s prescription volume as manufacturer revenue, even as branded Viagra remained unaffordable or uncovered for most telehealth users. The Ro agreement also gave Pfizer commercial intelligence on DTC platform demand patterns, pricing sensitivity, and demographic reach.

12.3 Implications for Future LOE Events

The telehealth infrastructure that matured around sildenafil has normalized DTC pharmaceutical distribution in ways that will affect every LOE event in categories with stigma, access barriers, or high cash-pay rates. Drugs for mental health, sexual health, weight management, and dermatology are particularly susceptible to telehealth channel disruption post-LOE, because the same access barriers that made in-person prescribing the primary channel are also the barriers telehealth eliminates.

For pharma IP and commercial teams planning LOE defense strategies, mapping the existing and emerging telehealth infrastructure in a drug’s therapeutic category is now a necessary analytical step. If a significant telehealth channel already exists pre-LOE, generic entry through those platforms will be faster and harder to intercept than through traditional pharmacy channels, and the brand’s co-pay card and DAW programs have limited reach in those channels.

Key Takeaways – Section 12:

Pfizer’s January 2020 supply agreement with Ro demonstrated that innovators can participate in telehealth generic distribution rather than only defend against it, capturing manufacturer revenue without brand dilution.

Telehealth generic sildenafil pricing ($2-$10 per dose) is determined by convenience and consultation bundle cost, not the drug’s commodity price, giving platforms a durable margin that does not compete directly with pharmacy generic economics.

LOE planning for any drug with access stigma or physician-visit friction must now include telehealth channel modeling; the sildenafil case is the reference template.

13. Consumer and Prescriber Behavior: The Bioequivalence Gap

13.1 What FDA Bioequivalence Standards Actually Guarantee

A generic drug approved under an ANDA meets the FDA’s bioequivalence standard when its pharmacokinetic parameters (Cmax, AUC, Tmax) fall within 80-125% of the reference listed drug’s parameters, tested in healthy volunteers under fasted and fed conditions. For sildenafil, this means generic formulations must demonstrate that the same dose delivers essentially the same amount of drug to the bloodstream at the same rate as branded Viagra.

The 80-125% confidence interval reflects statistical methodology in bioequivalence testing, not a meaningful clinical difference. Studies consistently show that the average generic is approximately 3-4% different from the brand in AUC, well within the range of normal pharmacokinetic variation between doses of the brand itself. For a drug like sildenafil, where the therapeutic window is wide and clinical response rates are similar across the sildenafil dose range, bioequivalence to the brand is clinically robust.

13.2 The Prescriber Dynamic: Generic Encouragement vs. Brand Promotion

Prescribers operate under two opposing pressures in the post-LOE sildenafil market. Payers and formulary guidelines push toward generic prescribing for cost containment. Pfizer’s HCP engagement programs, including DAW awareness campaigns and patient co-pay card programs, push toward brand prescribing. The DAW mechanism specifically allows a prescriber to write a prescription that a pharmacist cannot substitute generically, effectively locking in the brand fill.

Studies on prescriber behavior post-LOE consistently show that the default in the absence of active brand promotion is generic substitution. Pfizer’s investment in DAW campaigns targeted at HCPs who treat ED patients maintained a specific population of brand-adherent prescribers. The return on this investment is measurable at the prescription level: each successfully maintained brand fill at $65-$100 carries a substantially higher margin than the generic equivalent.

13.3 Insurance Architecture and the Out-of-Pocket Gap

Medicare Part D’s exclusion of ED drugs from required coverage is unique among common chronic condition treatments. The practical result is that Medicare-age men who want sildenafil pay entirely out-of-pocket, at which point generic discount programs like GoodRx typically deliver sub-$20 monthly costs for generic sildenafil. The brand receives essentially no Medicare-age consumer market for Viagra in the US.

Commercial insurance coverage varies widely. Plans that include ED coverage at all typically place branded sildenafil on Tier 3 or 4, where co-pays are $50-$100+ per fill. The brand co-pay card programs offset this for enrolled patients, but enrollment requires active HCP promotion of the program. This creates a situation where brand access is feasible but requires active steps that generic access does not, generating a systematic tilt toward generic use among less-engaged patients.

Key Takeaways – Section 13:

FDA bioequivalence standards require generic pharmacokinetics within 80-125% of the brand, and actual sildenafil generics typically fall within 3-4% of brand parameters, making clinical inferiority claims unsupported by data.

DAW campaigns are the primary HCP-facing brand defense tool post-LOE; without them, the prescriber default is generic substitution.

Medicare Part D’s ED drug coverage exclusion removes the largest age demographic from the branded Viagra market entirely, concentrating brand-defensible consumers in commercial insurance and cash-pay segments.

14. Investment Strategy: What Sildenafil Teaches Portfolio Managers About LOE Events

14.1 How Markets Price Patent Cliffs

Equity markets begin discounting patent expiration risk into pharmaceutical stock prices well before the LOE date. The typical pattern shows the first meaningful price impact four to five years pre-LOE as ANDA filers begin appearing in FDA Orange Book data, followed by accelerating discount as Paragraph IV certifications are filed and litigation begins. By the time generic entry actually occurs, most of the brand’s post-LOE revenue decline is already priced in.

Pfizer’s stock performance around Viagra’s LOE reflected this pattern. The market had been discounting Viagra’s declining contribution to Pfizer’s revenue for years, particularly after Eli Lilly’s Cialis gained market share through its extended-duration differentiation. By 2017, Viagra’s contribution to Pfizer’s overall revenue was small enough that the Teva settlement and authorized generic launch were non-events for Pfizer’s stock price. This is a general principle: for diversified large-cap pharma companies, individual product LOE events are often already fully priced by the time they occur.

14.2 The LOE Opportunity for Generics Investors

For investors in generic pharmaceutical companies, the Teva-sildenafil case offers a precise model. Teva’s first-filer advantage on sildenafil gave it the 180-day exclusivity period during which its generic competed only against Pfizer’s Greenstone AG. During that window, generic prices remained at $30-$35 per pill, generating substantially higher margins than the sub-$1 prices that followed multi-filer entry.

The investment thesis for generic first-filer positions is: identify Paragraph IV certifications filed by generic manufacturers against large-revenue branded drugs, assess the probability that the generic filer’s patent challenge will succeed, and size the position based on the expected 180-day exclusivity revenue stream discounted by litigation risk. The sildenafil case, where Teva’s negotiated entry gave it a duopoly period rather than a contested first-filer window, generated reliable returns relative to the litigation risk at time of settlement.

14.3 Branded Pharma: The LOE Defense Premium

For investors holding positions in branded pharmaceutical companies with upcoming LOE events, the Viagra case suggests that active LOE defense strategies are detectable in advance and are systematically mispriced. Specifically, markets tend to undervalue:

The authorized generic option, which is a known legal mechanism whose deployment is predictable for any company with an AG subsidiary like Greenstone. The royalty income from Paragraph IV settlements, which converts litigation risk into a known cash flow. The OTC reclassification pathway, which creates an incremental consumer market that is not captured in standard branded drug revenue forecasting models. The compound lifecycle extension through secondary indications, where IP estate analysis reveals the presence or absence of additional use claims that could support new indication development.

For a pharma IP team, conducting this analysis for your own portfolio is LOE preparation. For a portfolio manager, conducting the same analysis on competitor and target company assets is a source of investment edge.

Investment Strategy Note for Analysts:

The highest-conviction LOE defense signal is the combination of a large branded drug, a compound with demonstrated or plausible secondary indications, a first-filer Paragraph IV filed but unsettled, and an existing AG subsidiary. When all four conditions are present, the probability of a Pfizer-style managed LOE outcome is substantially higher than market consensus prices in. Track Orange Book ANDA filer data and patent certification deadlines for qualifying assets in your coverage universe.

Key Takeaways – Section 14:

Large-cap pharma LOE events are typically fully priced into equity values before generic entry; the alpha opportunity lies in correctly modeling the managed LOE outcome rather than the undefended baseline decline.

Generic first-filer investment theses should quantify the 180-day exclusivity revenue stream and discount by litigation risk; negotiated early-entry settlements with royalties, as in the Teva case, reduce litigation risk premium substantially.

The LOE defense premium for branded pharma is detectable in advance through IP estate analysis, Orange Book ANDA monitoring, AG subsidiary presence, and secondary indication development activity.

15. IP Valuation Framework: Pricing the Sildenafil Patent Estate

15.1 Components of the Sildenafil IP Valuation Model

Standard pharmaceutical IP valuation uses a probability-adjusted, risk-discounted NPV framework applied to the revenue attributable to each identifiable IP asset within a compound’s patent estate. For sildenafil, the estate components and their approximate valuation drivers were:

The Viagra ED use patent (expiring April 2020): valued based on peak Viagra revenues ($1.934 billion in 2008), discount rate reflecting litigation risk from multiple Paragraph IV filers, and expected terminal revenue decline post-LOE. The Teva settlement royalty stream converted a probabilistic future revenue component into a deterministic cash flow, reducing the discount rate for the post-2017 exclusivity period.

The Revatio PAH use patent (expiring 2012): valued based on Revatio revenue over its exclusivity period (FDA approval 2005, generic entry 2012), applying a lower discount rate given the distinct therapeutic area and smaller ANDA filer pool for a PAH-specific indication.

The pediatric exclusivity extension (six months appended to the ED use patent): valued at the marginal Teva royalty income generated during the extended period, minus the clinical study costs required to obtain the extension. This component’s value is deterministic and high-margin.

15.2 The Incremental Value of Each Lifecycle Management Layer

Working backward from Pfizer’s total sildenafil commercial history, each identifiable lifecycle management action added measurable incremental value:

The decision to develop Revatio as a distinct PAH indication created a separate, independently patented revenue stream that generated at least several billion dollars in cumulative Revatio sales during the 2005-2012 exclusivity period, plus the continuing Revatio generic revenue in which Pfizer retained no share but from which it had already extracted peak-value years.

The pediatric exclusivity study investment extended the Teva royalty obligation by six months. At Teva’s generic sildenafil revenue run rate, a six-month royalty extension was worth hundreds of millions in present value at the time of the pediatric study, against a clinical study cost of tens of millions of dollars at most.

The Greenstone AG deployment did not extend the IP term but captured market revenue that would otherwise have gone entirely to Teva and subsequent generic filers. Greenstone’s AG market share during the 180-day exclusivity window translated directly to retained Pfizer revenue at margins above commodity generic levels.

15.3 What This Framework Tells You About Your Own Portfolio

For pharma IP and portfolio teams conducting analogous valuations on current assets, the sildenafil estate analysis highlights four questions that should be standard in any LOE planning review: What secondary indications has the compound’s mechanism been tested in, and do any have Paragraph IV-defensible use patent claims? Is a pediatric indication study warranted, and has the timeline to obtain exclusivity been modeled against expected LOE timing? Does the company have an AG deployment infrastructure (subsidiary or partner) that can be activated on day one of generic entry? Has the OTC reclassification pathway been assessed for therapeutic areas where consumer self-treatment is medically appropriate?

If the answers to these questions are not on file in your IP strategy team, the Viagra case says you are likely leaving value on the table at the next LOE event.

Key Takeaways – Section 15:

Sildenafil’s IP estate generated value from at least four distinct components: the ED use patent, the PAH use patent, the pediatric exclusivity extension, and the AG deployment option.

The pediatric exclusivity study generated some of the highest risk-adjusted returns in the sildenafil IP estate: a clinical investment in the tens of millions generated a royalty extension worth hundreds of millions in NPV.

Standard LOE planning reviews should include four analytical questions: secondary indication pipeline, pediatric exclusivity timing, AG infrastructure readiness, and OTC reclassification feasibility.

16. Replicating the Playbook: Lifecycle Management Principles for Modern Pharma Teams

16.1 What the Viagra Case Generalizes To

Pfizer’s sildenafil strategy is not fully replicable for every drug. Several of its specific characteristics, a wide mechanism-of-action applicable to multiple therapeutic areas, a consumer-facing lifestyle positioning that supports DTC investment, and a patent estate with staggered expiration dates across distinct therapeutic claims, are unusual in combination. But the individual instruments Pfizer deployed are available to any pharma team managing a mature small-molecule asset.

The compound-centric lifecycle management philosophy is the most broadly applicable insight. Pfizer did not ask ‘how do we defend Viagra?’ It asked ‘what else can sildenafil do, and how do we patent and commercialize it?’ That question structure produces different answers than product-centric thinking, and it is the question that discovered Revatio’s PAH indication and generated years of additional exclusivity revenue.

16.2 The Lifecycle Management Roadmap for Small-Molecule Assets

A structured LOE preparation roadmap for a small-molecule drug generating over $500 million annually should include the following phases:

Years 8-10 of exclusivity: Commission comprehensive mechanism-of-action landscape analysis across therapeutic areas not covered by existing use patents. File IND applications for top-priority secondary indications. Assess eligibility for pediatric exclusivity study and model its NPV. Map all Hatch-Waxman ANDA filing triggers and expected timing.

Years 5-7 of exclusivity: Initiate Phase II trials in secondary indications. File use patent claims concurrent with clinical development milestones. Establish or confirm AG deployment capability through subsidiary or licensing partner. Conduct OTC reclassification feasibility review.

Years 3-4 of exclusivity: Finalize PAH or equivalent secondary indication NDA if clinically supported. Establish co-pay card and DAW program infrastructure for brand defense. Negotiate Paragraph IV settlements where favorable terms are achievable. Execute Hatch-Waxman 30-month stay strategy for remaining patent claims.

Year 1-2 before LOE: Confirm AG launch readiness through subsidiary or partner. Execute DTC brand investment in OTC-eligible markets. Finalize telehealth channel partnership agreements. Prepare tiered pricing architecture for post-LOE market segmentation.

16.3 What Changes in the Current Regulatory and Payer Environment

Several environmental conditions have shifted since Pfizer executed its sildenafil strategy. The Inflation Reduction Act (IRA) creates Medicare drug price negotiation provisions that will affect large-revenue branded drugs earlier in their commercial life, changing the NPV calculus for exclusivity extensions. The FTC’s increased scrutiny of Paragraph IV settlements under Actavis means that reverse-payment structures require more careful legal architecture than they did in 2013. Biosimilar interchangeability standards have matured rapidly for biologics, creating a parallel but distinct LOE framework for large-molecule assets.

The DTC telehealth channel did not exist in its current form when Pfizer launched Viagra. Today, any LOE strategy must include explicit telehealth distribution modeling and partnership analysis from the beginning of LOE planning, not as an afterthought when the generic market is already commoditized.

Despite these shifts, the core principles remain durable. Compound-level IP estate valuation. Layered patent thicket construction. Regulatory exclusivity pathway maximization. Authorized generic deployment. Brand equity investment pre-LOE. Tiered pricing architecture post-LOE. These are the instruments. The Viagra case is the best available execution template for how to deploy them simultaneously.

Key Takeaways – Section 16:

The compound-centric question (‘what else can this molecule do?’) produces more LOE value than the product-centric question (‘how do we defend this brand?’).

The four-phase LOE roadmap should begin in years 8-10 of exclusivity; teams that begin planning in years 3-4 have already foreclosed the secondary indication and pediatric exclusivity options.

IRA drug price negotiation provisions and the post-Actavis Paragraph IV settlement environment require updated legal and commercial modeling, but the core lifecycle management instruments remain valid.

Appendix: Key Data Tables

Table 1: Sildenafil Patent Estate Chronology (US)

Event

Date

Sildenafil discovered

1989

PAH/cardiovascular use patent filed

1992

ED use patent filed

1994

Viagra FDA approval

March 1998

Revatio (PAH) FDA approval

2005

Revatio PAH patent expiration

2012

Generic sildenafil entry (Canada)

2012

Generic sildenafil entry (UK/EU)

June 2013

Pfizer-Teva settlement signed

December 2013

Teva US generic launch

December 11, 2017

Greenstone AG launch (US)

December 11, 2017

Viagra Connect OTC approval (UK)

November 2017

Pfizer brand price increase

July 2018

Original US Viagra patent expiration

October 2019

Final US Viagra patent expiration (pediatric)

April 2020

Table 2: Sildenafil Pricing by Channel and Period

Product/Channel

Price (Approx.)

Period

Branded Viagra (retail)

$65/pill

Pre-AG launch

Greenstone AG

$30-$35/pill

December 2017 launch

Teva generic

$30/pill

Initial 2018 pricing

Multi-filer generic (commodity)

$0.60/pill

Post-2018

Generic sildenafil (Costco wholesale)

$4 per 20mg

Post-2018

Generic sildenafil (UK)

97p/tablet

Post-June 2013

Branded Viagra (post-price increase)

$90-$139/dose

Post-July 2018

Telehealth generic (Rex MD)

$2/dose

Subscription pricing

Telehealth generic (Hims, Ro)

$4-$10/dose

Platform pricing

Table 3: Market Share and Revenue Data

Metric

Value

Period/Context

Viagra global market share (peak)

92% of prescribed ED pills

2000

Viagra global market share (post-PDE5 competition)

~50%

2007

Viagra peak global sales

$1.934 billion

2008

Average annual Viagra sales decline

35% YoY

Post-EU LOE (2013+)

Pfizer retained US sildenafil market share

~15%

Post-US generic flood

Viagra Q3 2020 global sales

$121 million

Q3 2020

Viagra segment share (overall ED market)

37.3%

2023

Viagra revenue share (overall ED market)

45.35%

2024

Global sildenafil market size

~$3.5 billion

2023

Global sildenafil market forecast

~$5.5 billion

2032

Global ED drugs market size

$3.27 billion

2023

Global ED drugs market forecast

$7.74 billion

2033

Generic sildenafil US weekly prescriptions increase

")