A deep dive covering the ANDA pathway, EU MAA procedures, bioequivalence science, Paragraph IV litigation strategy, patent cliff analysis, evergreening roadmaps, and the IP valuation frameworks that institutional investors and generic manufacturers need to dominate post-patent markets.

I. The Generic Market at Scale: Economic Baseline and IP Value Drivers {#i}

A. Market Size, Growth Trajectory, and Prescription Volume

Generic drugs fill roughly 90% of all U.S. prescriptions while accounting for approximately 22% of total drug spending. That ratio is the product of deliberate legislative engineering, not market accident. At the global level, the generic drug market was valued at $435.3 billion in 2023 and is projected to reach $655.8 billion by 2028, a CAGR of 8.5%. A separate analysis from Precedence Research puts 2034 market size at $728.64 billion, implying a CAGR closer to 5% from a 2024 base of $445.62 billion. The divergence in CAGRs across analyst estimates reflects different assumptions about complex generic penetration and biosimilar market boundary definitions, not actual disagreement about volume trends.

The savings figure is more concrete. Generic drugs saved the U.S. healthcare system an estimated $253 billion in a single year during the mid-2010s, a figure the Association for Accessible Medicines has since updated to over $400 billion annually. The IRA (Inflation Reduction Act) provisions on drug price negotiation create an indirect tailwind for generics: as brand net prices compress on selected small-molecule drugs, the relative margin advantage of generics narrows, but the volume share continues to expand because formulary positioning for low-cost alternatives remains a payer priority.

The growth outlook rests on three structural pillars: patent expirations on high-revenue brand products, continued government procurement mandates favoring generics (particularly in lower-middle-income countries), and biosimilar market expansion as the regulatory pathway for biological products matures in both the U.S. and EU.

B. The IP Value of a Generic Drug Asset: Valuation Frameworks

For IP teams and institutional investors, a generic drug’s commercial value is not separable from its IP position. The core variables in any generic drug asset valuation are: time to market entry (driven by patent and exclusivity expiry analysis), probability of litigation success on Paragraph IV challenges, 180-day exclusivity status, API source qualification, and the number of anticipated generic entrants at launch.

A widely used methodology applies a risk-adjusted net present value (rNPV) framework. The model discounts expected cash flows from generic sales by: (1) a litigation risk factor derived from historical Paragraph IV challenge success rates (approximately 76% for first-to-file applicants), (2) a probability of technical failure at the bioequivalence stage (varies significantly by product class, roughly 15-30% for complex formulations), and (3) a market erosion curve calibrated to historical data on generic price decay as the number of manufacturers increases.

The HHS ASPE dataset is the most reliable public source for price erosion modeling. In markets with a single generic entrant, brand pricing typically decays by 20-30% in the first 12 months. With two generic entrants, the erosion reaches 50-60%. With five or more, prices often fall to 80-90% below original brand level within 24 months. These figures directly determine the profitability window for any Paragraph IV first-to-file position, which is why the 180-day exclusivity period is the most financially impactful single regulatory mechanism in the U.S. generic market.

IP valuation for brand-side assets follows a different calculus. The effective remaining patent life on a drug compound is typically shorter than the statutory 20-year term from filing because the patent is often filed years before FDA approval. By the time of NDA approval, the effective patent life may be only 7-10 years. Hatch-Waxman Section 156 provides a Patent Term Extension (PTE) of up to 5 years to compensate for regulatory review time, capped at a total remaining patent life of 14 years post-approval. That PTE calculation is a critical component of brand-side IP asset valuation and directly determines when a generic can file with a Paragraph III (patent not infringed, non-expiry) rather than a Paragraph IV certification.

C. The Patent Cliff: Identifying High-Value Targets

The ‘patent cliff’ describes the revenue discontinuity that occurs when a blockbuster drug loses market exclusivity. The cliff dynamic is steepest for high-revenue products with simple oral dosage forms, where multiple generic manufacturers can enter simultaneously at low technical risk.

Notable near-term patent cliffs include Eliquis (apixaban, BMS/Pfizer), whose U.S. composition-of-matter patents expire in the 2026-2028 timeframe, subject to ongoing litigation. Jardiance (empagliflozin, Boehringer Ingelheim/Eli Lilly) faces similar pressures in the same window. Dupixent (dupilumab), as a biologic, follows the biosimilar approval pathway rather than ANDA, but its exclusivity trajectory is equally tracked by competitive intelligence teams. For small-molecule generic manufacturers, apixaban is a particularly watched target given its annual brand revenues exceeding $10 billion globally.

Key Takeaways – Section I

The generic market’s $600+ billion trajectory is anchored by patent cliff dynamics and payer preference, not demand creation. Asset valuation requires integrating IP expiry analysis, litigation probability, price erosion modeling, and 180-day exclusivity status into a unified rNPV framework. Teams that treat these as separate workstreams leave money on the table.

Investment Strategy – Section I

Institutional investors screening generic pharmaceutical equities should weight companies with: first-to-file ANDA positions on high-revenue brand products with simple formulations, demonstrated Paragraph IV litigation track records, and diversified API supply chains not concentrated in a single geographic source. Concentration in complex generics (injectables, inhalers, topical semi-solids) offers higher margin protection against price erosion but requires longer development timelines and higher technical risk tolerance.

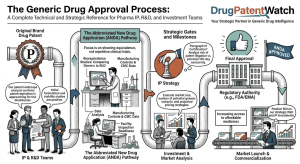

II. The Hatch-Waxman Architecture: Mechanism, Intent, and Strategic Exploitation {#ii}

A. The Legislative Bargain of 1984

The Drug Price Competition and Patent Term Restoration Act of 1984, universally known as Hatch-Waxman, created two systems in parallel. The ANDA pathway reduced the regulatory burden on generic manufacturers by allowing them to rely on the FDA’s prior safety and efficacy determination for the Reference Listed Drug (RLD), requiring only a demonstration of bioequivalence. Simultaneously, Section 156 of Title 35 created the Patent Term Extension mechanism, compensating brand manufacturers for time lost during FDA review.

The deliberate tension between these two systems is the engine that drives generic market competition. Hatch-Waxman did not eliminate patent protection; it created a structured pathway for challenging it. Generic manufacturers who understand that distinction operate at a fundamentally different strategic level than those who treat ANDA filing as a purely technical compliance exercise.

Before 1984, generic manufacturers in the U.S. faced a perverse requirement: they had to conduct full clinical trials to demonstrate the safety and efficacy of a copy of an already-approved drug. That barrier kept generic market penetration below 20% of prescriptions. Hatch-Waxman changed that by establishing the bioequivalence standard as a legal proxy for safety and efficacy equivalence.

B. The Four Patent Certification Categories

Every ANDA must include a certification with respect to each patent listed in the Orange Book for the RLD. The four certifications define the competitive strategy:

Paragraph I certifies that no patent information has been filed with the FDA for the listed drug. Paragraph II certifies that the patent has expired. Paragraph III certifies that the generic will not be launched until after the patent expires, effectively deferring competition. Paragraph IV, the strategically significant option, certifies that the listed patent is invalid, unenforceable, or will not be infringed by the manufacture, use, or sale of the proposed generic.

The choice among these certifications is not purely legal; it is a commercial decision with direct financial consequences. A Paragraph III certification guarantees a known entry date but forfeits any possibility of early market entry. A Paragraph IV certification creates litigation risk but is the only route to 180-day exclusivity and early entry if the patent challenge succeeds.

C. GDUFA: Fee Structure, Performance Goals, and Review Timelines

The Generic Drug User Fee Amendments (GDUFA), first enacted in 2012 and now in their third iteration (GDUFA III, covering fiscal years 2023-2027), fund the FDA’s Office of Generic Drugs (OGD) and govern review timelines. GDUFA III performance goals commit FDA to completing approximately 90% of standard ANDAs within 10 months and priority ANDAs within 8 months, measured from the date of receipt of a substantially complete application.

The fee structure is: a facility fee per manufacturing site (approximately $360,000 per active API facility and $228,000 per finished dosage form facility in FY2024), plus a per-application filing fee. These costs create a meaningful barrier for small generic manufacturers and explain why API-integrated generic companies, which can spread facility fees across a larger pipeline, carry a structural cost advantage.

GDUFA III also formalized the FDA’s Pre-ANDA Program, which allows manufacturers to seek formal meetings or written feedback on complex ANDA development questions before submission. Engaging this program for complex generics, particularly locally acting products or those requiring complex statistical models for bioequivalence, can prevent complete response letter cycles that add 12-18 months to approval timelines.

Key Takeaways – Section II

Hatch-Waxman is a strategic framework as much as a regulatory one. GDUFA III has compressed review timelines but elevated cost barriers. Companies not using the Pre-ANDA Program for complex submissions are leaving a risk-reduction tool unused.

III. The ANDA Submission Lifecycle: Technical Requirements and Submission Quality {#iii}

A. Pre-ANDA Development: Formulation, RLD Selection, and Regulatory History Review

The ANDA process begins with RLD selection. The RLD is the specific approved drug product to which the ANDA applicant submits their formulation for comparison, as listed in the Orange Book. For products where the FDA has designated a Reference Standard (RS) separate from the RLD, the RS is used for bioequivalence testing. Failing to distinguish between the RLD and RS at the outset of development is one of the most common and avoidable mistakes in ANDA preparation.

Formulation development for a generic must achieve pharmaceutical equivalence (same active ingredient, same dosage form, same route of administration, same strength) before bioequivalence can be assessed. Pharmaceutical equivalence is a necessary but not sufficient condition for bioequivalence. A formulation that meets pharmaceutical equivalence but uses different excipients can generate different dissolution and absorption profiles, producing bioequivalence failure.

The regulatory history review of the RLD includes analysis of any prior Citizen Petitions filed against the brand product, any REMS programs that restrict distribution, any prior ANDA approvals for the same product (which signal the regulatory precedent), and any active Orange Book litigation. Skipping a thorough regulatory history review at the pre-ANDA stage is how companies build products they cannot launch.

B. The eCTD Format and ANDA Content Requirements

ANDAs are submitted electronically to FDA’s Center for Drug Evaluation and Research (CDER) via the Electronic Submissions Gateway (ESG) in the electronic Common Technical Document (eCTD) format. The eCTD structure mirrors the ICH M4 guideline and organizes content into five modules: regional administrative information, summaries, quality (CMC), non-clinical, and clinical (which for an ANDA consists primarily of bioequivalence data).

The quality (Module 3) section is the technical core of the ANDA. It must contain complete Chemistry, Manufacturing, and Controls (CMC) information, including drug substance characterization, drug product formulation and manufacturing process description, container-closure system specifications, and stability data supporting the proposed shelf life. The stability program must follow ICH Q1A(R2) guidelines, with accelerated (40°C/75% RH, 6 months) and long-term (25°C/60% RH or 30°C/65% RH, depending on storage conditions) data. For products with photosensitivity concerns, ICH Q1B photostability data is required.

The proposed labeling must be identical to the RLD labeling, with the exception of specific permissible differences: the generic manufacturer’s name and address, the formulation differences for inactive ingredients when a biowaiver was granted, and any carve-outs for patented indications (known as ‘skinny labeling,’ a practice with significant legal implications discussed in Section VIII).

C. Information Requests, Discipline Review Letters, and Complete Response Letters

The FDA’s review process generates three types of formal communications. Information Requests (IRs) are the least serious: they ask for clarification or additional data on a specific point without placing the application in amendment status. Discipline Review Letters (DRLs) identify substantive deficiencies within a specific review discipline (chemistry, microbiology, labeling) and require a formal amendment that resets the review clock in some circumstances.

Complete Response Letters (CRLs) are issued when the FDA determines the application is not approvable in its current form. A CRL identifies all deficiencies that must be resolved before approval. Critically, a CRL does not constitute approval denial; it is a request for additional work. The applicant’s response to a CRL is a full resubmission, which the FDA has committed under GDUFA III to review within 6 months for a Class 1 resubmission (minor amendments) or 10 months for a Class 2 resubmission (major amendments including new bioequivalence studies).

The practical implication is that ANDA approval timelines are not fixed at 10 months; they reflect the number and severity of review cycles. An ANDA that generates two CRL cycles can easily take 3-4 years from initial submission to approval. The investment in high-quality submissions at the outset, including pre-submission consultation with FDA for complex products, is the most reliable way to compress this timeline.

Key Takeaways – Section III

RLD vs. Reference Standard confusion, incomplete stability packages, and inadequate CMC documentation are the three most common technical drivers of CRL cycles. GDUFA III Pre-ANDA meetings are underutilized for complex products. Every additional review cycle costs 12-18 months and compounds delay penalties in competitive markets.

IV. Bioequivalence Science: From TOST to BCS Classification and Narrow Therapeutic Index Drugs {#iv}

A. The Two One-Sided Test (TOST) and the 80-125% Criterion

Bioequivalence between a generic and its RLD is established statistically using the Two One-Sided Test (TOST) procedure applied to pharmacokinetic parameters. The two primary parameters are AUC (Area Under the Concentration-Time Curve, measuring total drug exposure) and Cmax (maximum plasma concentration, measuring peak exposure and absorption rate). For standard oral dosage forms, a generic is bioequivalent if the 90% confidence interval for the test/reference geometric mean ratio falls entirely within the 80.00-125.00% range for both AUC and Cmax.

The 80-125% criterion is derived from the log-normal distribution of pharmacokinetic parameters and regulatory consensus that differences in systemic exposure within this range are not clinically meaningful for most drugs. The criterion was not designed as an arbitrary ±20% band; the log-transformation means the window is asymmetric in absolute terms. A test/reference ratio of 1.25 represents a 25% increase, while a ratio of 0.80 represents only a 20% decrease.

The standard bioequivalence study design is a two-period, two-sequence, single-dose, crossover study in healthy adult volunteers. The crossover design controls for inter-individual pharmacokinetic variability by using each subject as their own control. Sample sizes typically range from 12-36 subjects for standard products, but can reach 50-100+ for highly variable drugs.

B. BCS Classification and Biowaivers

The Biopharmaceutics Classification System (BCS) divides drugs into four classes based on solubility and intestinal permeability. Class I drugs are highly soluble and highly permeable. Class II drugs are poorly soluble but highly permeable. Class III drugs are highly soluble but poorly permeable. Class IV drugs are poorly soluble and poorly permeable.

The FDA’s BCS-based biowaiver guidance allows applicants to request a waiver of in vivo bioequivalence testing for BCS Class I and Class III immediate-release (IR) solid oral dosage forms, provided additional criteria are met: the generic formulation must contain only excipients with established bioequivalence safety profiles, the dissolution profiles of the generic and RLD must match closely across three pH levels (1.2, 4.5, and 6.8), and the drug must not have a narrow therapeutic index.

ICH M9, finalized in 2021 and adopted by both FDA and EMA, provides the current harmonized framework for BCS-based biowaivers. ICH M9 extends BCS Class III biowaiver eligibility under certain conditions, recognizing that highly soluble, poorly permeable drugs are unlikely to show in vivo differences when the product dissolves rapidly. The FDA’s product-specific guidances (PSGs) identify which products are eligible for biowaivers and specify acceptable in vitro dissolution test methods.

The financial value of a BCS-based biowaiver is substantial. A standard in vivo bioequivalence study with a healthy volunteer crossover design costs $300,000-$800,000 and takes 6-12 months to complete, including analytical method validation, data analysis, and regulatory report preparation. A biowaiver supported by in vitro dissolution data costs an order of magnitude less and compresses the development timeline by 6-12 months.

C. Highly Variable Drugs (HVDs) and Reference-Scaled Average Bioequivalence (RSABE)

Highly Variable Drugs (HVDs) are defined as drugs where the intra-subject coefficient of variation (CV) for at least one pharmacokinetic parameter (typically Cmax) is 30% or greater. For HVDs, standard bioequivalence studies require impractically large sample sizes to demonstrate that the 90% CI falls within 80-125% with adequate statistical power.

The FDA and EMA permit a Reference-Scaled Average Bioequivalence (RSABE) approach for HVDs. RSABE scales the bioequivalence acceptance limits based on the observed within-subject variability of the reference product. In practice, if the reference product’s intra-subject CV for Cmax exceeds 30%, the acceptance limits can widen beyond 80-125%, potentially as wide as 69.84-143.19% at the extreme, though practical upper limits are narrower. The AUC criterion remains 80-125% regardless of variability.

The clinical justification for RSABE is that a highly variable drug’s concentration profile fluctuates widely within a single subject across administrations, so small differences between the generic and reference are clinically no more significant than the reference’s own day-to-day variability.

D. Narrow Therapeutic Index (NTI) Drugs

NTI drugs require special bioequivalence standards because small differences in drug exposure can produce clinically meaningful changes in efficacy or safety. Examples include warfarin (anticoagulant), phenytoin (anticonvulsant), lithium (mood stabilizer), cyclosporine (immunosuppressant), digoxin (cardiac glycoside), and levothyroxine (thyroid hormone replacement).

For NTI drugs, the FDA typically requires tighter bioequivalence acceptance criteria: the 90% CI must fall within 90.00-111.11% (rather than 80.00-125.00%) for both Cmax and AUC. This tighter standard is also applied to intra-subject switching studies for products like levothyroxine, where the FDA requires replicate crossover designs.

NTI drug ANDAs are among the most technically demanding in the generic approval pipeline. The tighter acceptance criteria require larger study populations to achieve adequate statistical power, and the clinical stakes of a failed bioequivalence study are high. For manufacturers with NTI ANDA positions, the technical barrier itself creates a competitive moat: fewer manufacturers can execute these studies competently, reducing the number of eventual market entrants and supporting higher post-launch prices.

E. Fed/Fasted Bioequivalence Studies

For oral solid dosage forms where food may affect absorption, FDA typically requires bioequivalence studies under both fed and fasted conditions. The fed condition study uses a high-fat, high-calorie meal (approximately 800-1,000 kcal, 50% from fat) and generally represents the worst-case scenario for food-drug interactions. Failing to design the fed study correctly, including meal composition and timing relative to dosing, is a common cause of bioequivalence failures that could have been avoided with better study design.

Key Takeaways – Section IV

BCS-based biowaivers are a structurally underutilized cost reduction tool for Class I and Class III IR products. NTI drugs carry higher technical risk but generate stronger competitive protection post-approval. RSABE for HVDs requires careful statistical planning; underpowering these studies is a direct path to bioequivalence failure and CRL cycle delays.

V. The EU Marketing Authorization Pathway: Article 10 Applications and Multi-Route Strategy {#v}

A. Article 10 Applications and the Regulatory Basis for EU Generics

In the EU, generic drug applications are submitted under Article 10 of Directive 2001/83/EC, which establishes the legal basis for abridged applications. The core Article 10(1) application (the ‘generic application’) requires the applicant to demonstrate that the product is a generic of a reference medicinal product authorized in the EU, that the reference product has been authorized for at least 8 years (data exclusivity period), and that the proposed generic is bioequivalent to the reference product.

Article 10(2) covers the ‘hybrid application,’ a category with significant strategic relevance. Hybrid applications apply when the proposed product cannot be classified as a pure generic because it differs from the reference in aspects such as changes in active substance, strength, pharmaceutical form, route of administration, or therapeutic indications. Hybrid applications require some additional pre-clinical or clinical data but still reference the existing dossier of the innovator, distinguishing them from full MAAs. The hybrid pathway is relevant for companies pursuing improved formulations or additional indications without conducting full Phase III trials.

Article 10(3) is the ‘bibliographic application’ pathway, applicable when a drug substance has been in well-established medicinal use within the Community for at least 10 years. This pathway allows applicants to use published scientific literature as a substitute for pre-clinical and clinical data.

B. The Centralized, Decentralized, MRP, and National Procedure Decision Matrix

The EU’s four authorization procedures serve different commercial objectives, and the optimal procedure selection depends on the product’s reference product authorization history, the applicant’s target market footprint, and resource constraints.

The Centralized Procedure (CP) results in a single marketing authorization valid in all 27 EU member states plus Iceland, Liechtenstein, and Norway. It is mandatory for certain product classes (biotechnology-derived products, ATMPs, orphan designated products) and voluntary for products meeting ‘significant therapeutic, scientific or technical innovation’ criteria. For a pure generic, CP is only available if the reference product was centrally authorized, or if the Company can demonstrate that Union authorization is in the interest of patients. Most pure generics do not qualify for CP; those that do benefit from a single dossier submission and pan-EU market access from day one.

The Decentralized Procedure (DCP) is the most commonly used pathway for new generic applications seeking authorization in multiple member states simultaneously. The applicant selects a Reference Member State (RMS) to lead the assessment and Concerned Member States (CMS) to participate. The assessment timetable is 210 days, with a consensus process when CMS raise objections. DCP is particularly efficient when the RMS has relevant scientific expertise for the product type.

The Mutual Recognition Procedure (MRP) applies when the applicant already holds a national marketing authorization in one member state and seeks to extend recognition to other member states. MRP is efficient for companies that pursued initial authorization through national procedure and now seek broader EU market access.

The National Procedure remains viable for products intended for a single market. Germany, France, and Italy, with their large population bases and distinct pricing frameworks, sometimes warrant standalone national applications.

C. Data Exclusivity (8+2+1) and Its Strategic Implications

The EU’s data exclusivity framework operates on an ‘8+2+1’ structure. Data exclusivity protects the reference product’s pre-clinical and clinical data for 8 years from initial authorization, during which no generic application referencing the data may be submitted. Market exclusivity then extends protection for an additional 2 years, prohibiting generic market entry regardless of ANDA or MAA approval status. A third year of additional market protection is available if, during the initial 8-year period, the marketing authorization holder obtains authorization for a new indication that provides a ‘significant clinical benefit’ compared to existing therapies.

The distinction between the 8-year data exclusivity and the 10 (or 11)-year market exclusivity is strategically critical for generic planning. A generic company may prepare and submit its MAA at the end of year 8, but cannot market the product until year 10 (or 11). The 2-year gap between submission eligibility and market entry creates a filing window during which the generic company is accumulating regulatory review time without yet incurring commercial launch costs.

Supplementary Protection Certificates (SPCs) extend patent protection for medicinal products by up to 5 years, compensating for time spent in regulatory review. SPCs operate independently of data and market exclusivity and are granted by national patent offices in each EU member state. An SPC’s expiry date is a critical milestone tracked by competitive intelligence teams, as it defines the legal boundary for generic market entry in each specific EU country. The EU Unitary SPC, authorized in 2023 under Regulation (EU) 2023/816, began taking effect in 2024 and will, for the first time, enable a single SPC valid across all participating EU member states, simplifying the IP landscape for both brand and generic companies.

Key Takeaways – Section V

Article 10(2) hybrid applications are a strategic middle ground for companies developing improved formulations without full Phase III investment. The 8+2+1 framework requires generic teams to build their submission timeline around year 8 as the filing trigger, not year 10. The EU Unitary SPC represents a structural change in European patent life management that IP teams need to model prospectively.

Investment Strategy – Section V

Companies with diversified EU approval portfolios across CP, DCP, and MRP procedures demonstrate more sophisticated regulatory capability than those relying on a single pathway. For deal evaluation, assess the pipeline composition: products with pending national authorizations in high-value markets (DE, FR, IT) awaiting MRP extension are lower-risk near-term launches than centralized applications still in initial assessment.

VI. Patent Protection, Orange Book Listings, and the Anatomy of a Patent Thicket {#vi}

A. Orange Book Listings: What Can and Cannot Be Listed

The Orange Book (formally, ‘Approved Drug Products with Therapeutic Equivalence Evaluations’) is not a passive registry. It is an active competitive tool, and both brand and generic manufacturers must understand its mechanics.

A brand company may list three categories of patents in the Orange Book for an approved drug: drug substance patents (claiming the active moiety), drug product patents (claiming the formulation, composition, or dosage form), and method-of-use patents (claiming approved therapeutic indications). Process patents, metabolite patents, and packaging patents cannot be listed in the Orange Book, regardless of their relevance to the product.

The 2020 CREATES Act and subsequent FDA rule (effective September 2023) tightened Orange Book listing requirements. The FDA now reviews listed patents for facially proper compliance with listing requirements and can delist patents that do not meet the statutory criteria. The FTC has also launched an Orange Book delisting challenge program, formally requesting FDA to remove patents that the FTC believes are improperly listed. These initiatives are direct responses to brand company practices of listing borderline-relevant patents to trigger 30-month stays against generic ANDAs.

Every new patent listed in the Orange Book after an NDA approval creates a potential 30-month stay opportunity for the brand company. This is why patent listing decisions are not purely legal; they are commercial decisions with direct financial implications for market exclusivity duration.

B. Patent Term Extension Under Hatch-Waxman Section 156

A patent covering an approved drug, medical device, food additive, or color additive may be eligible for Patent Term Extension (PTE) under 35 U.S.C. § 156. For pharmaceutical products, the PTE calculation compensates for time spent in FDA regulatory review following patent issuance. The maximum PTE is 5 years, and the total remaining patent life after the extension cannot exceed 14 years from the NDA approval date.

The PTE application must be filed within 60 days of NDA approval and requires documentation of the regulatory review period, including the time from IND submission to NDA submission (Phase I, II, III) and from NDA submission to NDA approval. The PTO (USPTO) reviews the application with input from FDA. Only one patent per approved drug product is eligible for PTE.

The practical importance of PTE for IP valuation is that it can add up to 5 years of brand exclusivity, during which no generic can receive final approval and market. For a $2 billion/year drug, 5 years of PTE represents up to $10 billion in protected revenue, less the cannibalization that authorized generics might generate.

C. Patent Thicket Construction: The IP Layering Roadmap

A patent thicket is a dense cluster of overlapping patents covering multiple aspects of a drug product, constructed to create a litigation barrier that generic challengers must navigate simultaneously. Building an effective thicket requires IP strategy that begins at the compound discovery stage and extends through post-approval lifecycle management.

The typical thicket construction sequence follows this architecture. The primary composition-of-matter patent, usually the first patent filed, covers the active moiety and its salts, esters, and polymorphs. This patent provides the broadest protection and is the most difficult to design around. The formulation patent layer covers the specific drug product: excipient combinations, controlled-release mechanisms, particle size specifications, and dosage form innovations. These patents often have narrower claims than the composition-of-matter patent but are sometimes easier to enforce because they are tied directly to the approved product.

The method-of-treatment patent layer covers specific therapeutic uses, dosing regimens, patient populations, or combination therapies. These patents are often filed later in the product lifecycle as clinical data accumulates from post-approval studies. Method patents are legally listable in the Orange Book as method-of-use patents and can trigger 30-month stays even if a generic seeks to market only for non-patented indications, a practice challenged in skinny labeling litigation discussed in Section VIII.

Polymorph patents target specific crystalline forms of the active substance and are frequently used as a secondary layer of protection after the primary composition-of-matter patent expires or faces challenge. Polymorphism is a property of most small-molecule drugs, and the crystalline form used in the commercial product can be patented if it exhibits unexpected properties (stability, solubility, bioavailability) compared to other known forms.

Metabolite patents cover active metabolites produced in vivo from the parent compound. These are particularly relevant when a prodrug strategy is used or when the metabolite itself has therapeutic activity. The enforceability of metabolite patents has been limited by obviousness challenges, as metabolites of known drugs are often considered foreseeable to skilled chemists.

Key Takeaways – Section VI

Orange Book listing strategy is a competitive weapon, not a compliance checklist. FTC and FDA delisting initiatives are actively narrowing the scope of permissible listings. Patent thicket durability depends on the strength of each individual layer, and a single successful invalidity challenge on the composition-of-matter patent can eliminate the primary exclusivity barrier even if the formulation and method patents remain.

VII. Regulatory Exclusivities: NCE, Orphan, Pediatric, and the 180-Day Economics {#vii}

A. New Chemical Entity (NCE) Exclusivity: Mechanics and the Four-Year Filing Rule

NCE exclusivity provides 5 years of market protection from NDA approval for drugs containing an active moiety not previously approved by the FDA. During the exclusivity period, FDA cannot accept or approve any ANDA or 505(b)(2) application referencing the NCE. The exclusivity blocks even the filing of a competing application, which distinguishes it from market exclusivity mechanisms that block approval but permit earlier submission.

The ‘NCE-1’ rule creates a critical filing opportunity for generic manufacturers. If a patent is listed in the Orange Book for an NCE-protected drug, a Paragraph IV-certified ANDA can be filed starting on the first day of the fifth year of NCE exclusivity (i.e., four years after NCE approval). The Paragraph IV filing at this juncture triggers a 30-month stay from the date of submission of the Paragraph IV notice letter to the NDA holder, potentially pushing final generic approval to year 7.5 post-brand approval. Understanding and executing on this timing precisely is one of the most financially consequential decisions a generic company makes.

B. Orphan Drug Exclusivity: Its Interaction with Patent Protection

Orphan Drug Exclusivity (ODE) provides 7 years of market protection for drugs approved for rare diseases affecting fewer than 200,000 U.S. patients. During ODE, FDA cannot approve a competing product for the same indication, though the exclusivity does not prevent approval for different indications or different patient populations.

ODE interacts with patent protection in complex ways. A drug with both patent protection and ODE benefits from both, but ODE runs concurrently with the patent term rather than extending it. When ODE outlasts patent protection, the ODE itself provides the market barrier. The inverse, where patent protection outlasts ODE, is less common but not rare for drugs with long effective patent lives due to PTE.

The strategic value of ODE for brand manufacturers depends on the competitive landscape for the orphan indication. If competing drugs exist that FDA could approve for overlapping patient populations, ODE’s protection is comprehensive. If the market is small enough that generic manufacturers find it uneconomical to develop, ODE functions primarily as a pricing enabler rather than a competition deterrent.

C. Pediatric Exclusivity: The 6-Month Extension Mechanism

Pediatric exclusivity provides an additional 6 months of market protection appended to any existing patents and regulatory exclusivities for a drug that is the subject of a Written Request from FDA to conduct pediatric studies. The 6-month extension applies to all formulations, dosage forms, and indications of the active moiety, making it more valuable than a single patent extension.

The economics of pediatric exclusivity are favorable for brand companies. A Written Request requires that the company conduct and submit pediatric studies within the specified timeframe. For a drug with $500 million/year in U.S. revenue, 6 months of additional exclusivity is worth $250 million in protected revenue (less generic erosion that would have occurred), far exceeding the cost of typical pediatric study programs ($5-30 million depending on indication complexity).

For generic manufacturers, pediatric exclusivity adds a deterministic 6-month delay to market entry beyond the patent expiry date. This delay is unlike patent litigation uncertainty because it is regulatory rather than legal. The only way to anticipate and plan for it is through systematic monitoring of the brand company’s pediatric study commitments and Written Request status, which are publicly disclosed in FDA’s pediatric database.

D. The 180-Day Exclusivity: Economics, Forfeiture, and Authorized Generics

The 180-day first-filer exclusivity is the single most valuable regulatory mechanism available to a generic manufacturer. First-filer status is conferred on the applicant (or group of applicants filing on the same day) that submits a substantially complete ANDA with a Paragraph IV certification first. During the 180-day exclusivity period, FDA cannot approve any subsequent ANDA for the same drug.

The financial value of 180-day exclusivity depends on the brand drug’s revenue and the price point the first filer maintains during exclusivity. Empirically, during 180-day exclusivity, the first filer typically prices at 15-30% below brand, capturing significant volume while maintaining margins far higher than the post-exclusivity market (where prices fall 80-90% below brand). For a $1 billion/year brand drug, 180-day exclusivity can generate $100-200 million in contribution margin for the first filer, depending on market share capture and pricing discipline.

Forfeiture is the primary risk to 180-day exclusivity value. There are six statutory grounds for forfeiture. Failure to market within 75 days of final FDA approval (or 30 months after ANDA submission, whichever is earlier) forfeits the exclusivity. Withdrawal of the ANDA forfeits it. A court decision finding the patent invalid or not infringed, followed by failure to market within 75 days, triggers forfeiture. An agreement between the first filer and brand manufacturer that delays market entry (the ‘pay-for-delay’ concern discussed below) can trigger FTC action. A failure-to-market forfeiture can be triggered even when the first filer intends to market, if regulatory delays (e.g., an import ban on the manufacturing facility) prevent timely launch.

Authorized generics are a brand company tactic that reduces but does not eliminate the value of 180-day exclusivity. An authorized generic is a brand product sold by the NDA holder (or a licensee) under the generic label at generic prices, without going through the ANDA process. The brand can launch an authorized generic simultaneously with the first filer’s launch, effectively creating a two-competitor market during the 180-day period and reducing the first filer’s market share capture. The authorized generic market share is typically 15-25% during the 180-day period, materially reducing the first filer’s contribution margin.

Key Takeaways – Section VII

NCE-1 timing, pediatric exclusivity monitoring, and first-filer status on high-revenue ANDA targets are the three most financially consequential regulatory exclusivity variables for generic portfolio management. Forfeiture risk is frequently underestimated; it requires proactive monitoring of all six statutory forfeiture triggers, not just the obvious market-failure scenarios.

Investment Strategy – Section VII

Companies with multiple first-filer ANDA positions across the $2B+ brand revenue tier warrant a valuation premium in generic pharma M&A. The key diligence question is not whether the position exists, but whether the manufacturing infrastructure is in place to launch within 75 days of approval without triggering a forfeiture.

VIII. Paragraph IV Litigation: Filing Strategy, Forfeiture, and the 30-Month Stay {#viii}

A. The Paragraph IV Notice Letter and the Artificial Act of Infringement

Filing an ANDA with a Paragraph IV certification is a statutory act of patent infringement under 35 U.S.C. § 271(e)(2), even though no product has been manufactured or sold. Congress designed this ‘artificial act of infringement’ to allow brand companies to litigate patent disputes before generic market entry, rather than forcing them to wait until the generic is actually on market. This design serves both parties: brand companies get early litigation resolution, and generic companies resolve the IP question before investing in commercial launch infrastructure.

The Paragraph IV notice letter must be sent to the NDA holder and the patent owner within 20 days of FDA notification that the ANDA has been filed. The notice must contain a ‘detailed statement of factual and legal basis’ for the generic’s belief that the patent is invalid, unenforceable, or will not be infringed. Courts have interpreted this requirement broadly; inadequate notice letters can have legal consequences but rarely doom an otherwise strong invalidity argument.

Upon receipt of the notice letter, the brand company has 45 days to file a patent infringement suit. If it files within 45 days, an automatic 30-month stay takes effect, preventing FDA from granting final approval to the ANDA. If the brand company does not file within 45 days, there is no stay, and FDA can grant final approval when the ANDA otherwise merits it.

B. The 30-Month Stay: Litigation Dynamics and Resolution Patterns

The 30-month stay runs from the date of receipt of the Paragraph IV notice letter by the NDA holder. It can be shortened if the court rules on the merits before 30 months expire. It can extend beyond 30 months if the court issues an order extending the stay. In practice, most pharmaceutical patent litigation takes 3-4 years to reach final judgment, meaning the stay often expires before the case is resolved, and generic market entry becomes contingent on the ongoing litigation outcome.

Empirical analysis of Paragraph IV litigation outcomes shows approximately 76% of first-to-file challenges eventually resulting in a favorable outcome for the generic company (either patent invalidity, unenforceability, or non-infringement). This success rate, however, masks significant variance by patent type. Composition-of-matter patents for small molecules are successfully challenged at lower rates than formulation or method-of-use patents, which are more susceptible to obviousness and double-patenting challenges.

The most common invalidity arguments in Paragraph IV litigation are obviousness (35 U.S.C. § 103), anticipation (prior art disclosure, § 102), and obviousness-type double patenting (when two related patents claim obvious variants of each other). Inequitable conduct claims (asserting that the patent was obtained through material misrepresentation to the USPTO) are less common since Therasense, Inc. v. Becton, Dickinson (Fed. Cir. 2011) raised the threshold for this defense.

C. Skinny Labeling Litigation: The GSK v. Teva and Beyond

Skinny labeling refers to the practice of omitting patented indications from generic drug labeling, enabling the generic to market for non-patented uses while the brand’s method-of-use patents for other indications remain in force. Under Hatch-Waxman, this practice is expressly permitted: a generic may carve out patented indications from its labeling without losing bioequivalence to the RLD.

The skinny labeling doctrine was significantly complicated by GSK v. Teva (Fed. Cir. 2020, 2021). In that case, GSK’s carvedilol (Coreg) carried a method-of-use patent for treating heart failure. Teva carved out the heart failure indication but marketed the product with materials that mentioned the heart failure use. The Federal Circuit held that induced infringement could still be found if the generic company’s promotional activities encouraged use of the product for the patented indication, even with the carved-out label. The case returned to district court for damages proceedings, creating significant uncertainty about skinny labeling risk.

For generic manufacturers, GSK v. Teva means skinny labeling is not a complete safe harbor if marketing materials, sales force communications, or even product promotion indirectly reference the carved-out indication. IP teams need to conduct marketing material reviews specifically for skinny-labeled products to avoid induced infringement exposure.

D. Pay-for-Delay (Reverse Payment) Settlements: FTC Scrutiny and Actavis

Pay-for-delay settlements, where a brand company compensates a generic company to delay market entry, were the subject of the Supreme Court’s FTC v. Actavis decision (2013). The Court held that reverse payment settlements are not presumptively lawful (rejecting the ‘scope of the patent’ test) and must be evaluated under the rule of reason standard for antitrust purposes.

Post-Actavis, the FTC has continued to challenge settlements that include large cash payments or other valuable transfers (authorized generic licenses, co-promotion agreements, side deals on other products) from brand to generic in conjunction with delayed entry. The FTC’s position is that these settlements reflect the economic value of eliminating the generic competition threat, which is an antitrust harm regardless of patent validity.

From a generic company’s perspective, pay-for-delay settlements can be commercially rational even under antitrust risk, because the expected value of the settlement (including the authorized generic license or cash payment) may exceed the expected value of at-risk launch and ongoing litigation. The legal risk, however, is that settlements found to violate the rule of reason can result in treble damages and disgorgement of profits.

Key Takeaways – Section VIII

The 76% historical success rate on Paragraph IV challenges overstates individual case probability; patent type, claim scope, and prior art availability are the actual predictive variables. Skinny labeling is no longer a risk-free approach after GSK v. Teva. Pay-for-delay settlements require antitrust counsel review as a mandatory component of any settlement negotiation.

IX. Evergreening Technology Roadmap: How Brand Companies Build and Defend IP Moats {#ix}

A. Primary Compound Protection to Secondary Patent Layering

Evergreening describes the suite of strategies brand companies use to extend effective market exclusivity beyond the expiration of the primary composition-of-matter patent. The term is pejorative in regulatory policy discussions, but from a brand company’s IP perspective, it is straightforward lifecycle management. Understanding the roadmap is essential for generic companies modeling entry timing.

The evergreening sequence typically follows this progression. During the primary patent’s protection window (typically years 1-12 post-approval), the brand company focuses on building the secondary patent layer through R&D on formulation improvements, new salt forms, new polymorph discoveries, and new delivery systems. Enantiomer patents (patenting the single active enantiomer of a racemic drug) have been widely used; AstraZeneca’s esomeprazole (Nexium) from omeprazole is the canonical example, with the strategy generating over $5 billion in annual revenues at peak despite the racemic omeprazole’s primary patents expiring.

Controlled-release formulations, when they offer genuine clinical benefit (reduced dosing frequency, improved tolerability), can generate strong secondary patents. OxyContin’s abuse-deterrent formulation patents, Concerta’s OROS technology, and Exelon Patch’s transdermal delivery patents are examples of formulation IP that extended market exclusivity substantially beyond the primary compound patent.

B. Product Hopping: Tactical Brand Withdrawal and Reformulation

Product hopping is a specific tactic where the brand company withdraws the original formulation from the market and replaces it with a new one, typically before generic entry for the original formulation. By pulling the original product, the brand forces prescribers to migrate to the new formulation, which has its own patent protection. The generic manufacturer whose ANDA references the now-withdrawn original product finds itself without a viable RLD and must either reformulate to reference the new product or navigate the regulatory complications of a withdrawn RLD.

A well-documented example involves the switch from Namenda IR (memantine immediate-release) to Namenda XR (memantine extended-release). Allergan, the brand manufacturer, announced the withdrawal of Namenda IR before generic entry for that formulation. The District Court and Second Circuit ultimately issued a preliminary injunction preventing Allergan from withdrawing Namenda IR, finding sufficient likelihood of an antitrust violation. The case illustrates both the tactic’s commercial logic and its legal vulnerability under antitrust law.

C. REMS as an Entry Barrier: The CREATES Act Framework

Risk Evaluation and Mitigation Strategies (REMS) are FDA-mandated safety programs for drugs with serious risk profiles. A REMS may include Elements to Assure Safe Use (ETASU), such as restricted distribution (only dispensed through certified pharmacies), prescriber certification requirements, or mandatory patient monitoring before dispensing. Drugs subject to ETASU include thalidomide analogs (lenalidomide, pomalidomide), isotretinoin, and sodium oxybate.

Before the CREATES Act (enacted December 2019), brand companies with REMS programs sometimes refused to provide samples of the RLD to generic manufacturers, citing REMS distribution restrictions. Without samples, generic manufacturers cannot conduct the bioequivalence studies required for ANDA submission. This sample denial strategy could delay generic entry indefinitely without any formal patent challenge, since the brand was not obligated to assist a competitor.

The CREATES Act created an express federal cause of action allowing generic (and biosimilar) manufacturers to sue brand companies for injunctive relief if they are denied sufficient quantities of the RLD or reference biological product for testing. The brand company’s defense is limited: it can show that the product is not covered by a REMS with ETASU, or that it has offered to provide the product under a ‘single, shared ETASU,’ or that the proposed testing would not comply with the ETASU.

Since CREATES Act enactment, several cases have been filed. The litigation precedents are still developing, but the Act has functionally ended the most egregious sample-denial practices. IP teams at generic companies should monitor CREATES Act litigation for defendants in their therapeutic area portfolios, as favorable precedent clarifies sample access rights.

Key Takeaways – Section IX

Brand evergreening follows a predictable IP layering sequence that generic intelligence teams can model prospectively. Product hopping carries antitrust risk but is not categorically illegal, creating uncertainty about entry timing for generics referencing a potentially-withdrawable RLD. The CREATES Act has materially improved sample access but is not yet settled law on all points.

X. Complex Generics: ANDA vs. 505(b)(2), Product-Specific Guidances, and Development Pathways {#x}

A. What Constitutes a Complex Generic Product

FDA’s 2017 guidance and subsequent policy statements define complex generic drug products as those involving complex active ingredients (biologics, peptides, polymeric mixtures, complex mixtures of active moieties), complex formulations (liposomal drugs, microsphere formulations), complex routes of delivery (locally acting drugs, drugs delivered via inhalation or nasal spray), or complex drug-device combination products.

The regulatory pathway for complex generics is ANDA, not NDA, but the evidentiary standard for demonstrating bioequivalence is significantly higher. For locally acting drugs, systemic pharmacokinetic studies do not establish local bioequivalence; FDA requires additional pharmacodynamic studies, clinical endpoint studies, or in vitro tests specific to the mechanism of local action. For inhaled products, device equivalence (same device or a device demonstrated to be equivalent in aerosol performance) is also required.

B. Inhaled Products: Nasal Sprays and MDIs

Complex inhaled generics are among the most technically challenging ANDA development programs. For nasal corticosteroids (fluticasone propionate nasal spray, mometasone furoate nasal spray), FDA requires a weight-of-evidence approach combining in vitro aerosol characterization (particle size distribution, spray pattern, droplet size), in vivo pharmacokinetic studies, and in vivo pharmacodynamic studies (often allergen challenge trials). The full development program for a nasal spray ANDA can cost $10-30 million and take 5-7 years.

Metered-dose inhalers (MDIs) for systemic diseases (albuterol sulfate HFA) require in vitro studies demonstrating aerosol equivalence (particle size distribution, dose uniformity, spray pattern) combined with pharmacokinetic studies. Dry powder inhalers (DPIs) require device equivalence assessment in addition to the aerosol characterization.

The commercial reward for complex inhaled generic products is commensurately higher than for simple oral solid dosage forms. Fewer manufacturers develop complex inhalers successfully, so post-launch price erosion is slower. Products with 3-5 manufacturer entries may settle at 40-60% below brand, compared to 80-90% for simple oral generics with 8-10 manufacturers.

C. Injectable Complex Generics: Liposomals, Microspheres, and Protein-Drug Conjugates

Injectable complex generics represent the highest-value and highest-risk segment of the generic pipeline. Liposomal formulations (liposomal doxorubicin, ABELCET amphotericin B lipid complex) require demonstration of physicochemical similarity (particle size, zeta potential, lipid composition, drug encapsulation efficiency) as well as pharmacokinetic equivalence. For some liposomal products, FDA has indicated that in vitro data alone may not suffice and that clinical endpoint studies may be required.

Microsphere products (injectable depot formulations such as leuprolide acetate for depot suspension, octreotide acetate for injectable suspension) present unique bioequivalence challenges due to their complex release kinetics. FDA has issued product-specific guidances for several microsphere products that outline a stepwise evidence approach including in vitro drug release testing, in vivo pharmacokinetic studies, and comparative clinical pharmacology.

D. The 505(b)(2) Pathway: When It Applies and When It Does Not

The 505(b)(2) NDA pathway allows an applicant to rely on studies they did not conduct and for which they have not obtained a right of reference, as part of the data package supporting approval. Unlike an ANDA, a 505(b)(2) can seek approval for a product that is not pharmaceutically equivalent to an RLD (different dose, different formulation, different indication). Unlike a full 505(b)(1) NDA, it can rely on published literature or FDA’s prior findings.

For complex generic developers, the 505(b)(2) pathway offers a route when the product cannot qualify as an ANDA due to differences from the RLD that FDA has not waived. The trade-off is that 505(b)(2) applications face the same Orange Book patent certification requirements as ANDAs (including the possibility of a 30-month stay) and do not qualify for 180-day first-filer exclusivity. The 505(b)(2) applicant also bears the full NDA user fee load rather than the lower ANDA user fee.

Key Takeaways – Section X

Complex generics offer higher margin protection but require substantially longer development timelines and higher investment. Product-specific guidances (PSGs) from FDA are the definitive technical reference for each complex generic program; companies that don’t design their development program around the relevant PSG from the start face predictable CRL cycles. The 505(b)(2) pathway is appropriate for complex products that cannot technically qualify as ANDAs, but it comes with a full NDA cost and timeline.

Investment Strategy – Section X

Complex generic pipeline depth is a quality-of-earnings signal in generic pharma equity analysis. Companies with 3+ complex ANDA positions (particularly inhaled or injectable) in late-stage development warrant pipeline premium multiples. The key diligence question is whether the bioequivalence study designs are consistent with the current PSG, which FDA updates periodically and which can invalidate earlier study designs.

XI. cGMP and Quality Systems: Warning Letter Trends, Data Integrity, and ICH Q7 Compliance {#xi}

A. FDA Warning Letter Trends in Generic Manufacturing

FDA Warning Letters to pharmaceutical manufacturing facilities have clustered around a consistent set of deficiency categories for the past decade. Data integrity violations (altered lab records, backdated data entries, deleted chromatography raw data), inadequate investigation of out-of-specification (OOS) results, and failures in aseptic processing controls account for the majority of Warning Letters with market access consequences.

Warning Letters differ from Import Alerts in their immediate commercial impact. A Warning Letter triggers a public disclosure and signals potential future enforcement but does not immediately halt product distribution. An Import Alert, issued under 21 CFR 312.110, blocks entry of products manufactured at the cited facility into the U.S. market. For generic manufacturers with a high proportion of U.S.-market products manufactured at a single overseas facility, an Import Alert is an existential commercial event.

Indian and Chinese API and finished dose manufacturers have received a disproportionate share of Warning Letters and Import Alerts, reflecting both the concentration of global generic manufacturing in these geographies and historical differences in quality culture and cGMP infrastructure investment. Sun Pharmaceutical, Ranbaxy (before its acquisition), Wockhardt, and multiple contract manufacturing organizations have experienced Import Alert-related disruptions. These events create market opportunities for competitors with clean cGMP records, since FDA’s drug shortage program can expedite ANDA approvals for products facing supply disruption.

B. Data Integrity: The 21 CFR Part 11 Framework and ALCOA+ Principles

21 CFR Part 11 establishes FDA requirements for electronic records and electronic signatures in pharmaceutical manufacturing. Compliance requires that electronic records be accurate, complete, reliable, and secure; that audit trails capture all data creation, modification, and deletion events; and that access controls prevent unauthorized data changes.

The industry standard for data integrity is the ALCOA+ framework: data must be Attributable, Legible, Contemporaneous, Original, and Accurate, with the extended ALCOA+ principles adding Complete, Consistent, Enduring, and Available. FDA’s 2018 guidance on data integrity explicitly states that the agency expects all data created during manufacturing and testing to adhere to ALCOA+ principles, whether in paper or electronic format.

The most common data integrity failures are not sophisticated fraud schemes; they are systemic process failures: disconnected chromatography systems not linked to audit-trail-enabled software, manual transcription of instrument data into master records without comparison to originals, and informal practices of re-running assays ‘off-system’ to avoid recording initial failures. These practices, when found during FDA inspection, result in Warning Letters regardless of whether the products themselves were actually defective, because FDA cannot trust the quality assurance data.

C. ICH Q7 and API Manufacturing Standards

ICH Q7 (‘Good Manufacturing Practice Guide for Active Pharmaceutical Ingredients’) defines cGMP requirements for API production, from starting materials through finished API. The standard covers quality management systems, personnel qualifications, facility and equipment qualification, materials management, production and in-process controls, packaging and labeling, storage and distribution, laboratory controls, and validation.

A critical concept in ICH Q7 is the ‘starting material’ designation: the point in the synthesis at which GMP requirements begin. API manufacturers and FDA have a longstanding tension over starting material designation, with manufacturers preferring to designate starting materials at later synthesis steps (which reduces the portion of the synthesis subject to GMP requirements) and FDA preferring earlier designation (which increases cGMP-compliant oversight). FDA’s 2019 draft guidance on starting material designation was never finalized, leaving the question partially unresolved and subject to case-by-case assessment during inspection.

D. EU GMP Non-Compliance: EMA Inspection Data

The EMA’s Annual Report for 2024 reported 10 GMP non-compliance statements issued by EEA authorities for manufacturing sites outside the EEA, with 5 originating from India. Non-compliance statements are published on the EMA website and result in marketing authorization holders being required to identify alternative API or finished product sources. For generic companies relying on a single-source API supplier that receives a GMP non-compliance statement, the disruption to production timelines can range from 6 months to 3 years, depending on the severity of the issues and the availability of alternative qualified suppliers.

Key Takeaways – Section XI

Data integrity is the top cGMP enforcement priority and the most common driver of Import Alerts for overseas manufacturers. ICH Q7 starting material designation creates ongoing regulatory ambiguity for API manufacturers. EMA’s published non-compliance statements are a publicly available signal for supply chain risk monitoring that generic IP and supply teams should track systematically.

XII. API Supply Chain: Geopolitical Risk, Multi-Sourcing, and the Drug Shortage Equation {#xii}

A. API Geographic Concentration and Geopolitical Risk

Over 70% of APIs used in drugs sold in the U.S. market originate from India or China. For certain drug classes, the concentration is even more extreme. Active pharmaceutical ingredients for antibiotics (including key penicillin and cephalosporin precursors), vitamin D3, and several cardiovascular generics come predominantly from a handful of Chinese manufacturers. Losartan valsartan API contamination (N-nitrosodimethylamine, NDMA) in 2018-2019 demonstrated the systemic risk of single-country API sourcing when a quality issue affects an entire manufacturing ecosystem.

U.S.-China trade tensions and potential tariff escalation on pharmaceutical imports have introduced new pricing and availability risks. Congressional proposals including the BIOSECURE Act (which, as of early 2026, has passed the House and is pending Senate action) would restrict U.S. government agencies from contracting with certain Chinese biotechnology companies, with potential spillover effects on pharmaceutical supply chains. Generic manufacturers heavily reliant on Chinese API sources need contingency planning for potential supply disruption that is no longer purely hypothetical.

B. Drug Shortage Dynamics and ANDA Prioritization

FDA prioritizes ANDA review for products in shortage. The Generic Drug User Fee Amendments created a formal mechanism: applications for products on FDA’s drug shortage list receive a 6-month review target (versus 10 months for standard ANDAs). This priority review mechanism creates a direct commercial incentive for manufacturers to file ANDAs for shortage products early.

Drug shortages tend to cluster in sterile injectables (oncology supportive care drugs, anesthetics, electrolytes) and older, low-margin generics. The economics of shortage products are instructive. When a product goes into shortage, market prices for the remaining supply increase, sometimes substantially. Manufacturers with ANDA approvals for shortage products who can scale up production quickly capture this market premium, which can be 5-10x the normal generic price during acute shortage periods.

C. Multi-Sourcing Strategy and Supplier Qualification

A multi-sourced API supply chain requires pre-qualification of secondary and tertiary API suppliers before primary supplier disruption occurs. Supplier qualification involves: analytical method validation against the primary supplier’s reference standards, stability studies confirming the drug product performs equivalently with API from each qualified source, and regulatory filings (annual product review updates or Prior Approval Supplements, depending on the nature of the API change) documenting the alternative source.

The time to qualify a new API supplier ranges from 12-24 months for a straightforward substitution to 3-5 years if the new supplier’s manufacturing process introduces impurity profile changes that require additional bioequivalence or clinical data. This timeline makes reactive multi-sourcing operationally inadequate; supply chain resilience must be built proactively, before the primary supplier faces regulatory action.

Key Takeaways – Section XII

BIOSECURE Act and tariff risk are creating structural pressure for U.S. and EU generic manufacturers to qualify additional API sources outside China. Drug shortage priority ANDA review is a commercially underutilized pathway. Multi-sourcing lead times of 12-24 months mean reactive supplier qualification is never adequate; proactive qualification programs are a competitive differentiator.

XIII. Pharmacovigilance Post-Approval: FAERS, Signal Detection, and Post-Market Obligations {#xiii}

A. FAERS and the Post-Market Safety Reporting Obligation

The FDA Adverse Event Reporting System (FAERS) is the primary post-market safety surveillance database. Generic manufacturers have the same post-market safety reporting obligations as brand manufacturers: they must report serious and unexpected adverse events to FDA within 15 days (expedited reports) and submit periodic reports for all adverse events on a quarterly basis for the first 3 years post-approval, then annually thereafter.

The pharmacovigilance obligation for a generic manufacturer is complicated by the fact that adverse event reports may not specify whether the patient received the brand or a specific generic manufacturer’s product. When a patient reports an adverse event after taking ‘metformin,’ attributing the event to a specific manufacturer is often impossible. This creates a collective reporting burden where individual generic manufacturers may systematically undercount their products’ adverse event contributions.

B. Signal Detection and Periodic Safety Update Reports

Signal detection from FAERS data uses disproportionality analysis methods including the Reporting Odds Ratio (ROR) and the Proportional Reporting Ratio (PRR). These statistics identify drug-event combinations reported more frequently than expected relative to all other drug-event combinations in the database, generating ‘signals’ that warrant further investigation.

Periodic Safety Update Reports (PSURs) in the EU (Periodic Benefit-Risk Evaluation Reports, PBRERs, under ICH E2C(R2)) and Periodic Adverse Drug Experience Reports (PADERs) in the U.S. are the scheduled reports that integrate signal data with benefit-risk assessment. For generic manufacturers, these reports tend to be simpler than for brand manufacturers because the safety profile of the reference product is well established, but they still require a dedicated pharmacovigilance infrastructure.

Key Takeaways – Section XIII

Pharmacovigilance infrastructure is a fixed cost that does not scale proportionally with product portfolio size; companies that build efficient, shared-platform pharmacovigilance systems have a structural cost advantage over those managing it product-by-product. Signal detection from FAERS provides early warning on safety issues that can affect the entire manufacturer class, including brand companies.

XIV. Competitive and Regulatory Intelligence: Patent Cliffs, White Space Analysis, and GDUFA III {#xiv}

A. Patent Cliff Monitoring: Tools, Methodologies, and Data Sources

Patent cliff analysis requires integrating three data streams: Orange Book patent expiries (for U.S. products), SPC expiry databases for EU jurisdictions, and ongoing Paragraph IV litigation status (which determines whether a listed patent’s expiry date is real or subject to challenge and extension).

The Orange Book is the authoritative source for U.S. patent and exclusivity data on approved drugs. It lists all patents an NDA holder has submitted, with expiry dates. However, the Orange Book is not a validated legal document; patent expiry dates are self-reported by NDA holders and may contain errors. IP teams should cross-reference Orange Book patent expiries against the USPTO Patent Full-Text and Image Database (PatFT) for accurate legal expiry dates including PTE calculations.

For EU SPC monitoring, national SPC databases vary significantly in accessibility and update frequency. EMA’s MRI Product Index provides a starting point for reference product authorization dates (which anchor data exclusivity calculations), but SPC expiry data requires country-by-country database monitoring. Specialized IP data platforms aggregate this multi-jurisdictional data.

DrugPatentWatch aggregates Orange Book data, Paragraph IV filings, ANDA approval status, tentative approvals, and litigation data into an integrated interface. Its primary value is not raw data access (all of which is theoretically publicly available) but aggregation, linkage across data types, and alert functionality that notifies users when relevant filings or approvals occur. For a generic manufacturer tracking 50-100 ANDA targets simultaneously, manual monitoring across multiple FDA databases is operationally infeasible; platform-aggregated monitoring is a practical necessity.

B. White Space Analysis: Identifying Low-Competition ANDA Opportunities

White space analysis in generic pharmaceutical development identifies drugs with large brand revenues, imminent or recent patent expiry, and a low count of pending or approved ANDAs. These products represent development opportunities where the post-launch competitive landscape is likely to be less crowded, supporting higher prices and better margins.

The data inputs for white space analysis are: FDA Orange Book data on approved ANDAs per product, FDA’s ANDA approval and tentative approval lists (updated weekly), GDUFA information reports (which disclose pending ANDA counts by product), and commercial prescription data (IMS/IQVIA or SYMPHONY). Cross-referencing these sources identifies products where the brand revenue is high, the patent expiry is near, and the count of pending ANDAs is low relative to the revenue opportunity.

Products with complex formulations, limited API source options, or required device components systematically appear in white space analysis because the development barrier reduces filer count. These products are also typically the most defensible from a margin perspective post-launch, because the same barrier that limited ANDA filings limits the eventual number of market entrants.

C. GDUFA III Performance Goals and Their Implications for Timeline Modeling

GDUFA III performance commitments include: completing approximately 90% of standard original ANDA submissions within 10 months of receipt, approximately 90% of priority original ANDAs (including shortage products) within 8 months, and approximately 90% of prior approval supplements within 10 months. These targets represent improvements over historical FDA performance and allow generic companies to build more reliable launch timeline models.

The performance goals also include commitments on meeting requests (FDA’s Pre-ANDA Program): approximately 90% of Type A meeting requests (urgent matters requiring rapid resolution) within 30 days, Type B meetings within 60 days. For complex generics with development questions that benefit from FDA scientific feedback, these meeting timelines allow structured pre-submission consultation without sacrificing significant calendar time.

Key Takeaways – Section XIV

Patent cliff monitoring requires multi-source data integration; Orange Book expiry dates alone are insufficient because they don’t reflect litigation dynamics or PTE calculations. White space analysis consistently identifies complex formulation products as the best-margin opportunities. GDUFA III meeting commitments make Pre-ANDA consultation a viable timeline management tool for complex programs.

XV. Advanced Manufacturing and AI Integration: The Next Competitive Moat {#xv}

A. Continuous Manufacturing: Regulatory Pathway and Adoption Status

Continuous manufacturing (CM) processes drug product continuously rather than in discrete batches, with integrated real-time quality monitoring and control. FDA has approved multiple NDA and ANDA products manufactured via continuous manufacturing platforms, including Prezista (darunavir) by Janssen, which was the first FDA-approved CM product (2016), and several generics subsequently.

The regulatory pathway for continuous manufacturing involves demonstrating that the process is validated, that real-time quality control (using Process Analytical Technology tools such as near-infrared spectroscopy for blend uniformity or dissolution prediction) is reliable, and that the process is capable of producing product that meets all quality specifications. FDA’s 2019 guidance on continuous manufacturing describes the agency’s expectations in detail.

The commercial case for continuous manufacturing is: reduced footprint (CM equipment is typically smaller than batch equipment for equivalent output), reduced batch failure risk (real-time monitoring detects deviations before they result in failed batches), and faster response to demand fluctuations (CM can be scaled by run time rather than requiring new equipment). The capital investment for CM implementation is substantial, but for high-volume products, the per-unit manufacturing cost advantage over batch processing is significant.

B. Process Analytical Technology (PAT) and Quality by Design Implementation

Process Analytical Technology (PAT) is the application of in-line or at-line analytical tools to monitor and control manufacturing processes in real time. FDA’s PAT guidance (2004) remains the foundational document, encouraging manufacturers to implement PAT as a component of Quality by Design.

Quality by Design (QbD) as defined in ICH Q8(R2) requires defining a Quality Target Product Profile (QTPP) first, then identifying Critical Quality Attributes (CQAs) that ensure the product meets the QTPP, then identifying Critical Process Parameters (CPPs) and Critical Material Attributes (CMAs) that affect CQAs. The resulting Design Space describes the range of inputs within which the process reliably produces quality product.

For generic manufacturers, implementing QbD from the outset of formulation development, rather than retrofitting it onto an already-developed product, produces a more robust design space and typically generates fewer CRL cycles during ANDA review because the CMC data package demonstrates a systematic understanding of the product and process. FDA reviewers respond favorably to QbD submissions because they reduce post-approval manufacturing risk and are more clearly linked to the quality evidence than traditional empirical formulation development reports.

C. AI and Machine Learning in Generic Drug Development

Machine learning applications in generic drug development cover three main areas: formulation prediction, bioequivalence outcome prediction, and regulatory document review automation.

Formulation prediction models use historical data from formulation databases to predict optimal excipient combinations, dissolution profiles, and stability outcomes for a new drug substance, reducing the number of formulation experiments required before identifying a viable lead formulation. Companies with large proprietary formulation databases (from years of generic development programs) can build proprietary models that constitute a competitive advantage not easily replicated by smaller entrants.

Bioequivalence outcome prediction models attempt to predict, from in vitro dissolution data and physicochemical properties, whether an in vivo bioequivalence study is likely to succeed. These models are primarily research-stage tools; their predictive accuracy is insufficient to substitute for in vivo studies, but they can prioritize formulation candidates and potentially reduce the number of clinical study failures.