In 2002, AbbVie launched adalimumab—a monoclonal antibody for rheumatoid arthritis sold under the brand name Humira—at a price of roughly $10,000 per year. By 2022, the annual list price had climbed above $84,000, and Humira had become the best-selling drug in pharmaceutical history, generating more than $200 billion in cumulative global revenue. The patent protecting the original molecule expired in the United States in 2016. Biosimilar competitors—cheaper copies of the drug manufactured by companies including Amgen, Sandoz, and Pfizer—had been ready to enter the market for years before they finally did, in January 2023.

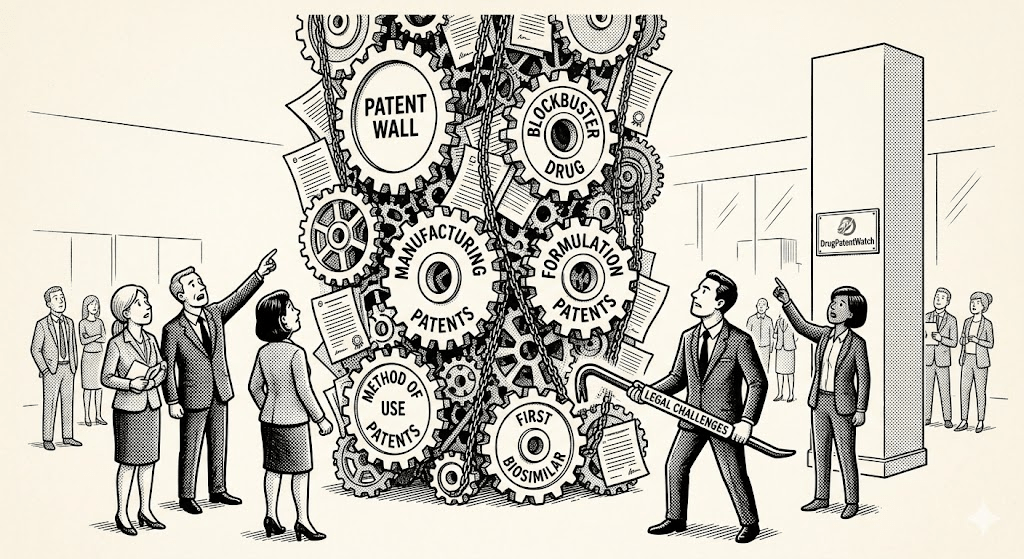

What kept them out for seven years was not better science, regulatory inertia, or manufacturing difficulty. It was a wall of patents: 136 of them, stacked around every conceivable variation of the original product, its formulation, its concentration, its manufacturing process, and the methods used to administer it. Independent analysis found that approximately 80% of those patents were duplicative—covering the same or nearly identical inventions linked together through a legal mechanism called terminal disclaimers to circumvent obviousness rejections at the U.S. Patent and Trademark Office [1]. The goal was never to win 136 patent lawsuits. The goal was to make it economically irrational for any competitor to try.

This is what a patent thicket looks like in practice. It is not a metaphor. It is a legal and commercial strategy, deliberately assembled over years, designed to convert a statutory 20-year monopoly into something closer to a perpetual one. And it works—not just for Humira, but across the biologic sector, where the combination of scientific complexity, a purpose-built litigation framework, and regulatory exclusivity provisions has produced some of the most aggressive intellectual property strategies ever deployed in any industry.

Understanding these strategies is no longer optional for anyone working in pharmaceutical investment, competitive intelligence, or drug development. The global biosimilar market is projected to grow from $34.8 billion in 2024 to $93.1 billion by 2030 [2]. More than $300 billion in pharmaceutical revenue faces patent expiration between 2024 and 2030 [3]. The firms that understand the mechanics of biologic IP—how thickets are built, where they are vulnerable, and what legal and regulatory tools exist to dismantle them—will be positioned to capture enormous value. The ones that treat patent expiration dates as simple cliffs will be wrong, repeatedly, and expensively.

This article dissects the mechanics of biologic patent strategy from first principles: the statutory framework that makes thickets possible, the layered tactics companies use to build them, the landmark cases that have tested their limits, and the emerging tools available to challengers. It draws on public patent records, court decisions, regulatory filings, and data from DrugPatentWatch, which tracks patent expirations, litigation timelines, and Orange Book listings across the pharmaceutical sector. The analysis runs from the DNA of the BPCIA to the specific battles playing out right now over Keytruda, Dupixent, and the next generation of biologic blockbusters.

Part I: Why Biologics Are Different—And Why That Matters for IP

The Scientific Gap Between Small Molecules and Biologics

To understand why biologic patent strategy is more complex than small-molecule drug strategy, you need to understand what a biologic actually is. A small-molecule drug—aspirin, metformin, atorvastatin—is a chemical compound with a defined molecular structure that can be precisely replicated through chemical synthesis. A generic version of atorvastatin is chemically identical to Lipitor. Same molecule, same effects, same pharmacokinetics. The regulatory standard for generic approval reflects this: demonstrate bioequivalence, and you are in.

A biologic is something else entirely. Monoclonal antibodies like adalimumab or pembrolizumab are large, complex proteins produced by living cell lines—typically Chinese hamster ovary cells engineered to express the desired protein. These molecules have molecular weights in the range of 150,000 daltons, compared to 180 daltons for aspirin. They contain hundreds of amino acids folded into precise three-dimensional structures. Their manufacturing involves fermentation, purification, and formulation steps that introduce variability at every stage. No two manufacturing runs produce molecules that are literally identical at the atomic level.

This biological complexity has two direct consequences for intellectual property. First, it generates more patentable layers. A small molecule has a structure, perhaps a polymorph or two, a synthesis route, and a method of use. A monoclonal antibody has all of that plus: the amino acid sequence of the heavy and light chains; the specific complementarity-determining regions (CDRs) that define binding specificity; the cell line used to produce it; the fermentation conditions; the purification protocol; the formulation (buffer, concentration, excipients); the device used to deliver it; the specific disease indications; the dosing regimen; the patient population; the co-administration with other drugs; and the manufacturing quality control methods. Each of these is a potential patent. An innovator company with a successful biologic has enormous incentive to patent as many of them as possible.

Second, the complexity means that a biosimilar—the biologic equivalent of a generic drug—requires a fundamentally different and more expensive development pathway than a small-molecule generic. A biosimilar applicant must conduct extensive analytical, functional, and often clinical studies to demonstrate that its product is “highly similar” to the reference biologic, even if not identical. The FDA’s totality-of-evidence standard for biosimilar approval under the Biologics Price Competition and Innovation Act (BPCIA) is far more demanding than the bioequivalence standard for small-molecule generics [4]. Development costs run from $100 million to $250 million per program, over seven to eight years [2]. That investment is at risk if the biosimilar cannot clear the patent thicket around the reference product.

The BPCIA: A Framework Built for Conflict

The BPCIA, passed in 2010 as part of the Affordable Care Act, created the regulatory pathway for biosimilar approval. It also created a patent litigation framework—the mechanism colloquially known as the “patent dance”—that is unlike anything in the generic drug space and that has directly enabled the construction of massive patent thickets.

Under the Hatch-Waxman Act, which governs generic small-molecule drugs, there are real constraints on how many patents a brand company can assert against a generic challenger. The Orange Book lists only patents covering the active ingredient, formulation, and method of use. Patent term extensions are capped at five years. The Act provides clear deadlines and litigation windows. The system is adversarial, but it operates within defined limits.

The BPCIA has no comparable constraint on the number of patents a reference product sponsor can assert. The statute requires the biosimilar applicant to share its abbreviated Biologics License Application (aBLA) with the reference product sponsor, who must then disclose all patents it believes are potentially infringed. The parties are supposed to negotiate a list of patents for the first wave of litigation. But there is no statutory cap on how many patents can end up on that list. AbbVie asserted as many as 63 patents against a single biosimilar challenger of Humira [1]. That is not a negotiation. It is a war of attrition by design.

The Supreme Court’s 2017 decision in Sandoz v. Amgen established that participation in the patent dance is not mandatory—a biosimilar applicant can opt out of the information exchange process [5]. But opting out does not eliminate litigation risk. It simply shifts the timing and gives the reference product sponsor the ability to seek immediate injunctive relief rather than waiting for the dance to complete. The decision transferred some procedural control to biosimilar applicants without fundamentally changing the economic math: facing dozens of patents, many of which are weak on the merits but expensive to challenge individually, the rational response for most biosimilar developers is a negotiated settlement with a delayed launch date rather than years of litigation.

This is the architecture that makes the patent thicket viable as a business strategy. It is not a bug in the BPCIA. It is, in the view of many critics, the predictable result of a statute that gave the pharmaceutical industry most of what it wanted during the legislative process.

“Patent thickets around reference biologics are purely designed to deter the entry of approved biosimilars.”— Former FDA Commissioner Scott Gottlieb [6]

Part II: The Anatomy of a Patent Thicket

Layer One: The Composition-of-Matter Core

Every biologic patent thicket starts with the same foundational asset: the composition-of-matter patent covering the primary active molecule. For Humira, this was U.S. Patent No. 6,090,382, covering the adalimumab antibody itself. For Keytruda (pembrolizumab), the core patents cover the pembrolizumab antibody and its CDR sequences. These patents are the ones that generate the most value and, correspondingly, the most defensible legal position—an innovator company that discovered and characterized a novel antibody has the strongest possible claim to the composition patent on that molecule.

The composition patent is also the one that expires first. The adalimumab composition patent expired in 2016. The core pembrolizumab patents are set to expire around 2028 [7]. These expiration dates represent the theoretical onset of biosimilar competition. In practice, they represent the moment when the rest of the thicket becomes load-bearing.

Layer Two: Formulation and Concentration Patents

The first line of defense after the composition patent expires is formulation patents: patents covering not the molecule itself but the specific preparation in which it is sold. AbbVie’s move from the original Humira formulation to a higher-concentration, citrate-free version was a textbook example of this strategy. The new formulation—which allows patients to inject a smaller volume, reducing injection-site pain—generated its own family of patents independent of the original molecule patents [8]. A biosimilar that matched the original Humira formulation but not the new citrate-free version faced a technically different product on pharmacy shelves. A biosimilar that matched the new formulation faced additional patents.

Merck has pursued the same tactic more openly with Keytruda. In September 2025, the FDA approved Keytruda Qlex, a subcutaneous injection formulation of pembrolizumab co-formulated with hyaluronidase, branded under the name Keytruda Qlex [9]. The subcutaneous formulation received approval across 38 solid tumor indications. Merck’s stated position, confirmed in communication with Bloomberg Law, is that the subcutaneous formulation patents will not block biosimilar entry for the IV formulation [10]. But that misses the commercial point. Merck’s goal is not to block biosimilar IV pembrolizumab—it knows it cannot do that. The goal is to convert the prescribing market to subcutaneous administration before 2028, so that when IV biosimilars arrive, physicians and payers are already committed to a new product that competitors cannot yet match.

Roche ran the same play with Herceptin. Genentech launched Herceptin Hylecta, a subcutaneous version of trastuzumab, in 2019—shortly before a wave of IV biosimilars entered the market [10]. The commercial logic is identical. You are not trying to block competition. You are trying to make the competing product irrelevant before it arrives.

Layer Three: Method-of-Use and Indication Patents

Method-of-use patents cover the specific clinical applications of a drug rather than the drug itself. A patent claiming the use of adalimumab for treating rheumatoid arthritis is different from a patent claiming the use of adalimumab for treating psoriasis, which is different from one claiming its use in Crohn’s disease. AbbVie prosecuted method-of-use patents across Humira’s expanding list of approved indications as each new indication was granted by the FDA. Because each new indication required clinical development and regulatory approval, AbbVie could argue that the underlying patent was being granted for a genuine innovation: the discovery that the drug worked in a new disease context.

The practical effect is patent protection that auto-extends as the drug succeeds clinically. Every new indication is a new patent family. Every new patient population—pediatric use, combination regimens—is another filing. Keytruda has more than 40 approved indications in the United States [7]. Merck has filed and continues to prosecute patents covering dosing regimens and combination use for many of them. Some of those patents are projected to extend protection into 2042, fourteen years beyond the expiration of the core composition patent [11].

The vulnerability of method-of-use patents, however, is greater than for composition patents. A biosimilar with a “skinny label”—an approved label that omits the patented indication—can in principle be marketed without infringing the method-of-use patent. The carve-out practice, well established in the Hatch-Waxman context, has been used in the biologic space too. But it creates commercial complexity: payers may default to biosimilars across all indications, and a brand company can allege induced infringement if the skinny-label biosimilar is effectively prescribed for the patented indication anyway.

Layer Four: Manufacturing Process Patents

The manufacturing of a monoclonal antibody involves a multi-step bioprocess: cell line development, upstream fermentation in bioreactors, downstream purification through a series of chromatography columns, viral inactivation, filtration, and formulation. Each of these steps can generate patentable innovations. Improvements to the cell culture medium, optimizations of the purification sequence, novel viral clearance steps, glycosylation profiles achieved under specific culture conditions—all are potential patent claims.

Manufacturing process patents create a particular problem for biosimilar developers because they are largely invisible until litigation begins. A biosimilar developer must independently develop its own manufacturing process; it cannot simply copy the reference product’s process because it has no access to proprietary process details. But if its independently developed process happens to overlap with a patented process step owned by the reference product sponsor, it may be infringing without knowing it. This is not theoretical. Process patent claims have featured in multiple biologic patent disputes, and they represent the layer of the thicket most resistant to prior art challenges because the innovations are genuinely novel and not duplicative in the way that formulation patents often are.

Layer Five: Device and Delivery Patents

Humira is administered using an autoinjector device. The device itself—its mechanical design, the needle configuration, the spring mechanism, the visual indicators—is separately patentable. AbbVie prosecuted device patents alongside the pharmaceutical patents. A biosimilar developer that wanted to launch a product in the same convenience format as Humira (rather than a prefilled syringe, which requires more manual dexterity) needed to either design around AbbVie’s device patents or negotiate a license. This added another layer of cost, complexity, and potential litigation exposure.

Device patents are often underestimated in competitive analysis of biologic exclusivity. Analysts focused on composition and formulation patents may fail to account for the commercial impact of forcing biosimilar competition into a less patient-friendly delivery format. In markets where patient convenience drives formulary decisions—specialty biologics for chronic conditions especially—a brand product with a proprietary autoinjector retains preference even when the drug itself is off patent.

The Terminal Disclaimer Problem

The mechanism that ties these layers together is the terminal disclaimer. When a patent applicant files multiple patents covering variations of the same basic invention, the USPTO will typically reject later patents as obvious over earlier ones. The applicant can overcome this rejection by filing a terminal disclaimer: a formal statement that the later patent will expire on the same date as the earlier one, preventing any unjust extension of the overall monopoly term.

The terminal disclaimer was intended as a quality control mechanism. In the biologic patent thicket context, it has become an enabling tool for the exact behavior it was supposed to prevent. AbbVie used terminal disclaimers to link together approximately 80% of Humira’s U.S. patent portfolio—duplicative patents that could not individually survive an obviousness challenge but that collectively created a web of litigation exposure [1]. Challenge one patent successfully, and it drags down others linked to it by terminal disclaimer. But to get to that result, a biosimilar developer must fight through years of litigation on each patent individually, bearing the full cost of that process.

A proposed USPTO rule in 2024 attempted to address this dynamic by restricting the use of terminal disclaimers in ways that would have significantly reduced the enforceability of thicket patents. Applied retrospectively to Humira’s portfolio, the analysis showed the rule would have reduced AbbVie’s assertable patents from 105 to 24 [4]. The rule generated substantial industry pushback and its implementation remains contested. But its formulation signals that regulators and lawmakers understand the mechanism and are beginning to address it directly.

Part III: The AbbVie Humira Playbook in Full

Building the Fortress

The timeline of AbbVie’s Humira IP strategy is worth reconstructing in detail because it is the template every pharmaceutical IP team now studies. Humira received FDA approval in 2002 for rheumatoid arthritis. The core composition patent, U.S. Patent No. 6,090,382, was set to expire in 2016. AbbVie had fourteen years from launch to build a patent portfolio that could survive the expiration of that foundational asset.

The strategy operated on two tracks simultaneously. The first was aggressive prosecution at the USPTO: filing new applications covering every formulation variant, every new indication as it was approved, every manufacturing improvement, every delivery device iteration. By the time biosimilar applicants began filing their aBLAs, AbbVie had assembled a portfolio of more than 130 issued patents. When pending applications are included, the filings numbered over 250 [6]. The portfolio was organized to ensure that no single patent covered an identical scope to any other—sufficient differentiation to survive direct invalidity challenges, but sufficient overlap to require biosimilar developers to clear each patent separately.

The second track was the litigation stance. AbbVie publicly stated that any biosimilar challenger would face four to five years of litigation [5]. This was not a bluff—it was an accurate description of the process a biosimilar developer would face under the BPCIA if it pursued the patent dance to conclusion without settling. When Amgen, Sandoz, Pfizer, Boehringer Ingelheim, Mylan, Samsung, and others filed their biosimilar applications, AbbVie asserted dozens of patents against each of them, triggering the full patent dance procedure.

The numbers from the resulting litigation are staggering. Against Alvotech, AbbVie listed 63 patents as potentially infringed. Against Amgen’s Amgevita, the first-wave litigation involved 10 patents drawn from 61 listed on AbbVie’s aBLA disclosure [1]. The cost of litigating even the first wave to conclusion runs into the tens of millions of dollars for each side. For a biosimilar program representing a total development investment of up to $250 million, the economics of continued litigation versus a negotiated settlement become unfavorable very quickly, particularly when the settlement offer is “you can launch in 2023 instead of 2034.”

The Settlement Machine

Every major Humira biosimilar challenger settled with AbbVie. Not one litigated the entire patent portfolio to a final judgment. The settlements generally provided for U.S. market entry in 2023—seven years after the composition patent expired—in exchange for commitments to pay royalties and to refrain from launching before the agreed date [12]. The specific financial terms remain confidential, but the pattern is consistent: early challengers negotiated somewhat better terms than late challengers, because the results of early litigation (even settled litigation) established precedents that informed subsequent negotiation. Later entrants—Samsung, Pfizer, Mylan—reached pre-litigation settlements, their negotiating positions already weakened by the experience of earlier challengers [3].

This dynamic, sometimes called the “free rider” problem in reverse, is a structural feature of the patent thicket strategy. The brand company benefits from each successive settlement: it establishes that the thicket can be enforced, discourages challengers from investing in full litigation, and creates settlement terms that subsequent entrants must accept as the market baseline. The biosimilar developer who fights hardest—bearing the highest legal costs—arguably creates value for its competitors who settle more cheaply based on the information produced in earlier proceedings.

The result for patients and payers was unambiguous. Humira’s annual list price exceeded $84,000 in the year before biosimilar entry. The price did not fall substantially until multiple biosimilars were on the market simultaneously in mid-2023—a process that required not just regulatory approval but the resolution of every patent dispute through settlement [13]. The seven-year delay in biosimilar entry cost the U.S. healthcare system an estimated $10 billion or more in excess drug spending, depending on the methodology used to calculate the counterfactual.

The Dupixent Comparison: A Different IP Architecture

AbbVie’s Humira strategy is instructive precisely because it represents the maximum expression of the patent thicket approach—the most patents, the most aggressive litigation stance, the greatest disparity between theoretical and actual exclusivity. But not every biologic blockbuster follows the same model. Understanding the variation is as important as understanding the archetype.

Dupixent (dupilumab), co-developed by Sanofi and Regeneron for atopic dermatitis and several other type 2 inflammatory conditions, had combined 2023 revenues exceeding $11 billion [14]. Its composition-of-matter patents provide a different exclusivity profile than Humira’s. The drug was approved in 2017 for atopic dermatitis, with subsequent approvals for asthma, chronic rhinosinusitis with nasal polyps, eosinophilic esophagitis, and prurigo nodularis expanding its clinical footprint. Unlike AbbVie, Sanofi and Regeneron have not been publicly identified as having pursued an aggressive patent accumulation strategy in the Humira mold. The 12-year regulatory exclusivity period under the BPCIA—which runs from the original 2017 approval—provides a hard floor preventing biosimilar approval before 2029 regardless of the patent picture.

This illustrates a point that competitive analysts sometimes miss: the two pillars of biologic exclusivity—patent protection and regulatory exclusivity—operate independently. A biologic with weak patents still cannot face a biosimilar within 12 years of its approval, because no aBLA can reference the brand’s clinical data for approval during that period. Patent thickets add time beyond the regulatory exclusivity period. They are most valuable for older biologics where the 12-year clock has already run out and composition patents are expiring.

Part IV: The Merck Keytruda Problem—$29.5 Billion and a Ticking Clock

The Scale of What Is at Stake

Keytruda generated $29.5 billion in global sales in 2024, representing approximately 56% of Merck’s total pharmaceutical revenue [9]. No drug in the history of oncology pharmacology has generated comparable annual revenue, and no pharmaceutical patent expiration in any sector carries a comparable revenue figure. The core pembrolizumab composition patents expire in the United States in 2028. Biosimilar developers including Amgen, Samsung Bioepis, and Bio-Thera Solutions are already in clinical development, with regulatory submissions potentially as early as 2026 or 2027 [15].

Without successful lifecycle management, Merck faces biosimilar-driven erosion of 70-80% of Keytruda’s IV formulation revenue within two to three years of competitive entry [16]. That is a revenue exposure of roughly $20-24 billion on a single product. The DCF implications for Merck’s equity valuation are equally stark: the present value of Keytruda’s post-2028 cash flows—discounted for the probability and timing of biosimilar entry and the rate of revenue erosion—represents a material fraction of Merck’s total enterprise value.

Merck’s patent portfolio around Keytruda has been extensively built out. The company has filed patents covering dosing regimens, specific combination use with chemotherapy regimens, patient selection biomarkers, and specific indication-by-indication uses across more than 40 approved cancer types. Some of these method-of-use patents carry projected lifespans extending into the 2030s and, for some combination regimens, into 2042 [11]. They will not prevent IV biosimilar entry in 2028. But they create a litigation landscape that biosimilar developers will need to navigate carefully, particularly for sales in indications where specific dosing or combination protocols are patented.

The Subcutaneous Gambit

The approval of Keytruda Qlex in September 2025—the subcutaneous pembrolizumab formulation co-formulated with hyaluronidase—is Merck’s most significant lifecycle management move, and one worth examining in operational detail.

The subcutaneous formulation carries its own patent protection covering the formulation, delivery device, and administration method [7]. Biosimilar manufacturers who develop IV pembrolizumab biosimilars will not be able to immediately substitute for Keytruda Qlex in patients who have converted to subcutaneous administration. Developing a biosimilar subcutaneous formulation requires a separate regulatory submission and clinical program—another round of development cost and regulatory delay. By the time IV pembrolizumab biosimilars arrive in 2028, Merck will have had at least three years to convert its prescribing base to a formulation that those biosimilars cannot directly compete with.

Bloomberg Law, citing a Merck spokesperson, noted the company’s carefully worded position: it “does not expect any patent protection specifically directed to SC pembrolizumab to impact the potential marketing of a biosimilar intravenous form of Keytruda” [10]. Read that sentence twice. Merck is not claiming the subcutaneous patents will block biosimilar IV pembrolizumab. It is simply noting, accurately, that the two formulations are legally distinct products. The commercial point—that the subcutaneous formulation will capture and protect market share that IV biosimilars cannot address—goes unspoken.

Congressional reaction has been pointed. Four members of Congress urged the USPTO in February 2023 to scrutinize Merck’s Keytruda patent portfolio, stating that applications appeared to reflect “anti-competitive business practices, such as patent thicketing and product hopping” [10]. Product hopping—the practice of switching a drug’s commercial format to a new, patent-protected version just as competition arrives for the original—is the specific allegation. Roche did it with Herceptin. Merck is doing it with Keytruda. The strategy is legal. Whether it is anti-competitive in a meaningful sense is a question that regulators and courts will continue to examine.

Method-of-Use as a Moat Around Oncology Indications

The breadth of Keytruda’s indication list creates a specific IP management challenge for biosimilar developers that does not exist for drugs with narrower clinical use. A biosimilar pembrolizumab can launch with a skinny label that omits specific patented indications, but Keytruda is approved for more than 40 tumor types across multiple biomarker-defined populations. Determining which indications are covered by independent method-of-use patents, which dosing regimens are patented, and which combination protocols create infringement exposure requires the kind of patent landscape analysis that tools like DrugPatentWatch are built to provide—mapping the full patent estate, tracking prosecution status at the USPTO, and monitoring litigation filings in real time.

For biosimilar pembrolizumab developers, the practical challenge is significant. A skinny label that omits the largest volume indications—first-line non-small cell lung cancer, for example—would eliminate the commercial value of the biosimilar program. But promoting the biosimilar for those indications while carrying a label that excludes them creates induced infringement risk. The legal resolution of this tension, in the pembrolizumab context, will define the commercial viability of biosimilar oncology development for the next decade.

Part V: Amgen v. Sanofi—The Supreme Court Redraws the Functional Claiming Map

The PCSK9 Fight and What Was Really at Stake

The most consequential biologic patent decision of the decade was not directly about patent thickets. It was about a more fundamental question: how broadly can a pharmaceutical company claim ownership of a class of antibodies? The Supreme Court’s unanimous May 2023 decision in Amgen Inc. v. Sanofi answered that question with precision, and the implications for the value of biologic patent portfolios have not yet been fully priced by markets or fully incorporated into IP prosecution strategy [17].

The dispute centered on PCSK9 inhibitors—a class of antibody drugs that reduce LDL cholesterol by blocking a protein that degrades the body’s LDL receptors. Both Amgen’s Repatha (evolocumab) and Sanofi/Regeneron’s Praluent (alirocumab) belong to this class. Amgen held patents that claimed, in broad functional terms, ownership of all antibodies that (1) bind to specific amino acid residues on PCSK9 and (2) block PCSK9 from impairing LDL clearance. The patents were not limited to any specific antibody structure or amino acid sequence. They were defined entirely by what the claimed antibodies did, not what they were [18].

The logic was appealing from an innovator’s perspective: we discovered this mechanism, we discovered this target epitope, therefore we should own all antibodies that work through this mechanism. If valid, these claims would have given Amgen a patent monopoly over the entire functional class of PCSK9-inhibiting antibodies—including Praluent, which Sanofi and Regeneron independently discovered and structurally characterize as a distinct molecule.

The Supreme Court, in an opinion authored by Justice Neil Gorsuch, applied the patent law’s enablement requirement: a patent specification must teach the public enough to make and use the full scope of what is claimed, without undue experimentation. Amgen’s specification described 26 specific antibody examples by their amino acid sequences and provided a two-step method (structure/screen) for identifying additional antibodies within the claimed genus. The Court found that this was not enough. The claimed genus potentially encompassed millions of distinct antibodies. The specification’s method for generating them was essentially trial-and-error screening. No “general quality” was identified that would allow a skilled scientist to reliably predict which candidate antibodies would have the claimed functional properties [19].

The Court’s conclusion was blunt: “if our cases teach anything, it is the more a party claims, the broader the monopoly it demands, the more it must enable.” Amgen’s functional genus claims were invalid for lack of enablement. The two patents at issue were struck down entirely [20].

The Baxalta Downstream: Functional Claims Keep Failing

The Amgen v. Sanofi decision was immediately applied by the Federal Circuit in Baxalta v. Genentech, where claims directed to antibodies that bind Factor IX or Factor IXa and increase pro-coagulant activity were invalidated on identical grounds [21]. The Federal Circuit found the facts “materially indistinguishable from those in Amgen.” Eleven antibody examples were not enough to enable a potentially vast genus defined purely by function. The result was swift and analytically brief—the Federal Circuit did not even conduct a detailed Wands factor analysis. It compared the facts to Amgen and applied the holding.

The downstream implications of these decisions are substantial. Any biologic patent portfolio built before May 2023 that includes functional genus claims—claims that define an antibody class by what it does rather than what it structurally is—carries material invalidity risk. DrugPatentWatch’s post-Amgen analysis recommends that analysts modeling biologic innovator companies identify specific patents in each portfolio that rely on functional rather than structural claim definitions, and discount or zero out NPV attributable to those claims pending a structural analysis of whether the specification discloses a “general quality” sufficient to satisfy the enablement standard [22].

The winning structure post-Amgen is sequence-defined claims: patents that claim an antibody by its specific CDR sequences, or by its precise binding interactions with a structurally characterized epitope. These are narrower than functional genus claims, but they are defensible. They protect what was actually invented. Regeneron, whose antibody platform generates sequence-defined intellectual property systematically, gained a structural competitive advantage from Amgen v. Sanofi that its competitors have only recently begun to fully understand and counteract [22].

What IP Teams Should Be Doing Right Now

The practical response to Amgen v. Sanofi for pharmaceutical IP teams operating within companies that hold pre-2023 antibody portfolios with functional genus claims is threefold. First, audit every pending application and issued patent that relies on functional definition rather than structural characterization—these need either structural claim limitations added (where prosecution history allows), or a realistic assessment of their invalidity risk if challenged. Second, for any patent asserted in BPCIA litigation, evaluate whether the opposing party could mount an enablement challenge under the Amgen standard and factor the probability of success into settlement negotiations. Third, ensure that future prosecution emphasizes structural claim definitions: CDR sequences, specific binding contacts with target residues, and structural features correlated with the functional property of interest.

For biosimilar developers and their counsel, the inverse applies: review the reference product sponsor’s patent estate for functional genus claims, identify any that fit the Amgen profile, and prepare IPR or declaratory judgment strategies that lead with enablement challenges. The Supreme Court gave the challenging party a very clear theory. It should be used.

Part VI: The Challenger’s Toolkit—Dismantling a Patent Thicket

Inter Partes Review as First Strike

The BPCIA patent dance allows a biosimilar developer to participate in a structured pre-litigation information exchange. It does not require waiting for the reference product sponsor to file suit before challenging patents. Inter partes review (IPR), the administrative validity challenge procedure before the Patent Trial and Appeal Board (PTAB), is available independently of the BPCIA process and can be used strategically to weaken a patent thicket before or during patent dance negotiations.

An IPR petition can be filed against any patent in the thicket that has survived for fewer than nine months from grant, or at any time after a litigation is filed, subject to estoppel rules. PTAB proceedings run on a twelve-to-eighteen month timeline, faster than district court litigation. If the PTAB institutes the petition and ultimately cancels the challenged claims, the patent is gone from the thicket. More importantly, a successfully instituted petition creates settlement leverage before the final decision: a reference product sponsor facing a high probability of losing a thicket patent in IPR has stronger incentives to negotiate a license or a delayed-entry agreement on favorable terms than it would have without that threat hanging over the portfolio.

The strategic sequencing matters. Filing IPR petitions against the weakest patents in the thicket—those most likely to be duplicative of prior art or to fail an Amgen-style enablement challenge—while using the patent dance to narrow the litigation list, is a coordinated approach that reduces the overall exposure without requiring full litigation on every patent. Several biosimilar developers have adopted this approach, and its effectiveness is visible in the compressed timelines for some post-Humira biologic patent settlements compared to the multi-year Humira proceedings.

The Terminal Disclaimer Chain Strategy

Terminal disclaimers create both a vulnerability and an opportunity. When a group of patents is linked by terminal disclaimers to a parent patent, successfully invalidating the parent creates downstream invalidity pressure on all the linked children. This is particularly effective against the type of duplicative patent accumulation that characterized Humira’s portfolio, where independent analysis found the 80% duplicative rate among patents linked by terminal disclaimers.

The proposed USPTO rule on terminal disclaimers—which would require that if any patent in a terminal disclaimer chain is held unenforceable, all linked patents are unenforceable—was specifically designed to deter this kind of portfolio construction going forward. Applied retroactively to Humira’s portfolio, it would have reduced the assertable patents from 105 to 24 [4]. The deterrence effect of such a rule, even if only prospective, fundamentally changes the economics of aggressive patent accumulation: a single successful invalidation challenge could detonate an entire chain of linked patents rather than requiring individual challenges to each one.

For biosimilar challengers facing thickets built on terminal disclaimer chains, identifying the parent patents in each chain—those whose invalidation would carry down the most children—is the highest-leverage analytical task in the patent landscape process. DrugPatentWatch’s tools for visualizing patent family relationships and prosecution history are directly applicable to this kind of chain analysis.

The ‘Skinny Label’ Defense and Its Limits

The skinny label strategy—launching a biosimilar with a label that excludes patented indications while including non-patented ones—provides a path to market entry even where method-of-use patents are asserted and cannot be immediately invalidated. The FDA permits biosimilar approval with a carve-out label that omits indications covered by unexpired patents listed in the Purple Book (the biologic equivalent of the Orange Book).

The practical value of the skinny label depends on the economic significance of the non-patented indications relative to the patented ones. For a drug where patented indications account for 90% of prescriptions, a skinny label biosimilar may not generate sufficient revenue to justify the development investment. For drugs where the largest indications are unpatented—or where the method-of-use patents are weak enough that a direct challenge is viable—the skinny label provides real commercial value.

The induced infringement risk remains significant. A brand company whose patented indication is being prescribed off-label for a skinny-label biosimilar can allege that the biosimilar manufacturer induced infringement through its marketing, physician education, and formulary positioning activities. The standard for induced infringement requires proof of knowledge and intent, but brand companies have been creative in identifying evidence of such intent in biosimilar marketing materials. The safer approach—and the more commercially constrained one—is to avoid any marketing activity that could be read as encouraging use in the patented indication, while accepting that payers and pharmacy benefit managers may substitute the biosimilar broadly regardless.

Declaratory Judgment Actions: Taking the Offensive

Nothing in the BPCIA requires a biosimilar developer to wait for the reference product sponsor to file suit. A biosimilar developer who opts out of the patent dance can file a declaratory judgment action affirmatively seeking a ruling that its product does not infringe, or that the asserted patents are invalid. This is not a commonly used approach—the defensive posture of the BPCIA process tends to push biosimilar developers into responding to brand company filings—but it is available and has been used strategically in circumstances where the biosimilar developer has strong prior art or invalidity arguments and wants to control timing and forum selection.

The choice of forum matters more in biologic patent litigation than in many other areas. The District of Delaware and the District of New Jersey handle the largest volume of BPCIA cases and have developed considerable expertise with the statute’s procedural requirements. But not every forum is equally favorable. Judge selection within those districts, case management philosophy, and the availability of specific discovery procedures all affect litigation dynamics in ways that a biosimilar developer filing first can partially control.

Part VII: The Regulatory Architecture—Exclusivity Beyond Patents

Twelve Years Is Not a Patent. It Is Something Harder to Challenge.

The most important non-patent exclusivity protection for biologics is the 12-year regulatory exclusivity period established by the BPCIA. During this period, the FDA will not approve an aBLA that relies on the reference biologic’s safety and efficacy data. No biosimilar can be approved before 12 years from the reference product’s licensure date, regardless of the patent landscape [23]. This is categorically different from patent protection in one crucial respect: it cannot be challenged, invalidated, or worked around through litigation or scientific differentiation. It is a statutory prohibition on regulatory approval, and it applies uniformly.

The 12-year exclusivity is also longer than any comparable protection in any other major pharmaceutical market. The European Union provides 10 years of data protection for biologics. Japan provides eight. The United States provision was the result of direct pharmaceutical industry lobbying during the BPCIA negotiations, where the industry successfully argued that a longer exclusivity period was necessary to justify the investment in biologic development. Critics have noted that this period substantially exceeds the investment recovery periods that even the most expensive biologic programs require, and that it functions as a guaranteed extension of market exclusivity that applies even when a drug’s commercial success means development costs were recovered years before the exclusivity expires.

For competitive analysts, the 12-year exclusivity creates a hard floor in biosimilar entry modeling. A biologic approved in 2015 cannot have a biosimilar approved before 2027 under any circumstances. A biologic approved in 2020 is protected through 2032. When analyzing the expected timing of biosimilar competition for any specific product, the first question is not “when do the patents expire?” but “when does the 12-year exclusivity expire?” If the exclusivity runs longer than the patent coverage, the patent thicket is irrelevant for entry timing—no biosimilar can enter anyway.

Pediatric Exclusivity and Orphan Drug Protections

Two additional exclusivity provisions extend biologic market protection in specific circumstances. Pediatric exclusivity—a six-month extension of existing exclusivity granted when a drug sponsor conducts FDA-requested pediatric studies—applies to biologics and can add six months to any patent or exclusivity period. For a biologic with $10 billion or more in annual revenue, a six-month pediatric exclusivity extension is worth $5 billion or more in protected revenue. The incentive to conduct pediatric studies is accordingly enormous, and brand companies managing biologic lifecycle often ensure that pediatric studies are conducted and completed in the years before primary exclusivity expiration.

Orphan drug exclusivity—seven years of marketing exclusivity granted for drugs developed to treat rare diseases affecting fewer than 200,000 patients—can also apply to biologics, particularly those developed for rare autoimmune or oncological conditions. The interaction between orphan exclusivity and the BPCIA’s 12-year exclusivity is complex and case-specific, but for drugs that qualify for orphan designation, the total exclusivity period may extend beyond the BPCIA baseline.

The Purple Book and the Information Infrastructure of Biologic Competition

The FDA’s Purple Book—formally the Biological Products: Lists of Licensed Biological Products with Reference Product Exclusivity and Biosimilarity or Interchangeability Evaluations—is the biologic equivalent of the Orange Book, listing reference biologics, their exclusivity expiration dates, and approved biosimilars with their interchangeability status. The Purple Book does not list specific patents the way the Orange Book does; patent information for biologics is disclosed through the BPCIA patent dance process rather than being prospectively listed in a government database.

This asymmetry creates a competitive intelligence challenge for biosimilar developers and investors. Identifying the full patent landscape around a reference biologic requires patent searching and analysis independent of any government registry, because there is no comprehensive official source. This is precisely the problem that tools like DrugPatentWatch address—aggregating patent data from the USPTO, PTAB, litigation records, and prosecution history files to provide a comprehensive view of the IP landscape around specific biologic products. For an analyst trying to model the realistic entry timeline for a biosimilar program, this kind of integrated data is the difference between an accurate forecast and a guess based on headline patent expiration dates alone.

Part VIII: The Economics of Thicket-Building—Who Profits and Who Pays

The Brand Manufacturer’s ROI Calculation

The economics of patent thicket construction are straightforward when you have access to the relevant numbers. Consider a biologic generating $10 billion in annual U.S. revenue. Its core composition patent expires in Year 0. Without a thicket, biosimilar entry might begin in Year 1 or Year 2, with revenue erosion of 70-80% within three years of first biosimilar entry. The revenue loss over a three-year erosion period, relative to pre-biosimilar levels, would represent approximately $20-24 billion in cumulative lost revenue (discounted to Year 0 present value).

A patent thicket that delays biosimilar entry for five years adds five years of uncontested $10 billion annual revenue—$50 billion gross, perhaps $30-35 billion present-value after capital costs and time value. The cost of building the thicket—additional patent prosecution, litigation costs, settlement payments—runs into the low billions at most for a major program. The ROI on thicket construction, for a drug with Humira’s or Keytruda’s revenue profile, is among the highest available to a pharmaceutical company on any capital deployment decision. This is why it happens. It is rational.

From the brand company’s perspective, patent accumulation is not even primarily a legal strategy—it is a financial strategy with legal tools as its instruments. The patents themselves may have varying degrees of legal validity. What matters is that each patent represents a litigation cost and uncertainty that a biosimilar developer must factor into its entry decision. The brand company does not need to win every patent dispute. It needs to make the aggregate cost of challenging the thicket exceed the expected commercial value of biosimilar entry, at which point rational challengers settle on the brand’s terms.

The Social Cost and the Policy Response

The social costs of biologic patent thickets are also straightforward, though the policy response has been slower than the problem warrants. Biologics represent approximately 2% of U.S. prescriptions but account for 37% of net drug spending [2]. The gap between those numbers represents the premium cost of biologic medications relative to small-molecule drugs, and patent thickets are a significant driver of that premium by preventing biosimilar competition that would otherwise reduce prices.

The policy response has involved three tracks. First, proposed changes to USPTO practice—including the terminal disclaimer rule discussed above and ongoing efforts to improve patent quality review for pharmaceutical applications. Second, legislative proposals in Congress to reform the BPCIA by capping the number of patents that can be asserted in Phase I litigation (one proposal would have reduced AbbVie’s assertable Humira patents from 105 to 24 [4]). Third, FTC scrutiny of reverse payment settlement agreements—deals in which a brand company pays a biosimilar challenger to delay launch—under antitrust law.

None of these tracks has yet produced a comprehensive resolution to the thicket problem. The USPTO rule on terminal disclaimers remained contested. Congressional reform proposals have repeatedly stalled. FTC enforcement of reverse payment agreements has been active but piecemeal. In the meantime, the Humira model has been studied, refined, and replicated by pharmaceutical IP teams across the industry.

Part IX: The Landscape in 2025 and Beyond—Dupixent, Enbrel, and the Next Wave

Enbrel and Amgen’s Thirty-Year Exclusivity Question

Humira is the most studied patent thicket, but it is not the only example worth examining. Amgen’s Enbrel (etanercept) has maintained approximately 30 years of exclusivity through a combination of patents and regulatory complexity [7]. The etanercept molecule itself received FDA approval in 1998. Its core patents have expired. Yet biosimilar competition in the United States has been effectively blocked not by a Humira-style litigation campaign but by a combination of manufacturing complexity, patient switching barriers, and a patent estate on manufacturing processes that proved resilient to challenge.

The Enbrel situation illustrates a dimension of biologic IP strategy that is less visible than the litigation-driven model: supply chain and manufacturing patents can be as effective as product patents in limiting competition, particularly for drugs with complex manufacturing requirements. Biosimilar etanercept is approved and marketed in Europe and other markets. It has not successfully penetrated the U.S. market at scale, and the reasons are structural rather than merely legal. The distinction matters for investors: a market position protected by manufacturing complexity and customer inertia may be more durable than one protected purely by litigation.

Keytruda’s Second Cliff: The 2028 Problem and the 2035 Question

Keytruda’s patent situation will define pharmaceutical IP strategy for the next decade more than any other single drug. The IV formulation’s core patents expire in 2028. The subcutaneous formulation (Keytruda Qlex) carries independent protection through the early 2030s. Method-of-use patents for specific indication-by-indication combination regimens extend into 2042 [11].

Merck faces a challenge that AbbVie did not face with Humira in the same acute form: its drug is the first-line standard of care in oncology across a vast range of tumor types, and its clinical community is deeply invested in the IV formulation’s pharmacokinetic profile and dosing flexibility. Converting patients to subcutaneous administration in oncology—where dosing precision and pharmacokinetic predictability are clinically significant—is not as straightforward as converting autoimmune patients to a more convenient injection format. Physicians and oncology pharmacists will have questions about subcutaneous pembrolizumab’s clinical comparability to IV in specific tumor contexts. Those questions create a window for IV biosimilar competition even after broad subcutaneous conversion begins.

Merck CEO Rob Davis has publicly described the subcutaneous transition as “turning the page” to a new commercial chapter for Keytruda [11]. Analysts at BioPharmCatalyst have characterized the lifecycle management strategy as potentially allowing Keytruda to “retain significant market share, albeit potentially at a lower rank” after biosimilar entry [9]. The market consensus, as of mid-2026, is that Keytruda’s revenue will not fall as precipitously as a simple patent cliff model would suggest—but that the compound effect of IV biosimilar price competition beginning in 2028 and the gradual market development of the subcutaneous formulation will produce a complex revenue trajectory that requires scenario modeling rather than a single decline curve.

Dupixent’s Coming Window and Sanofi’s Counter-Strategy

Dupixent’s 12-year BPCIA regulatory exclusivity expires in 2029, the first year that biosimilar development programs could theoretically receive FDA approval (assuming applications filed no later than 2027). The drug’s revenue trajectory—$11 billion in 2023, growing rapidly on the strength of expanding indications—makes it a target of comparable commercial importance to Keytruda for biosimilar developers looking at the post-2028 landscape.

Sanofi and Regeneron’s counter-strategy focuses on the clinical breadth of Dupixent’s indication portfolio—seven approved conditions across distinct type 2 inflammatory pathways—and the pipeline of additional indications in late-stage development. Each new indication approval generates a new set of method-of-use patents, extends the clinical differentiation of the branded product, and adds therapeutic area expertise that biosimilar manufacturers do not have. A biosimilar developer that matches dupilumab’s molecule in atopic dermatitis does not automatically have the data package to seek approval in chronic obstructive pulmonary disease or bullous pemphigoid. Indication-specific exclusivity fragmentation is a real commercial moat, even without composition patent coverage.

Part X: Tools and Information Infrastructure for the Competitive Intelligence Function

What Patent Data Actually Tells You (And What It Doesn’t)

The central challenge in pharmaceutical competitive intelligence is that patent data is abundant but often misread. A patent expiration date tells you when legal protection on a specific claim expires. It does not tell you when a biosimilar will actually enter the market. It does not account for regulatory exclusivity running longer than patent coverage. It does not reflect the litigation history that may have resulted in settlements extending the effective exclusivity period by years. It does not capture the commercial impact of formulation switching or indication-specific method-of-use patents that survive composition patent expiration.

The firms that get biosimilar entry timing right combine patent expiration data with four other data layers: regulatory exclusivity records (from the Purple Book and BPCIA filings), PTAB and district court litigation records (to determine which patents are under active challenge and what the probable outcomes are), settlement agreement terms (where publicly disclosed), and commercial intelligence on prescribing patterns and formulary positioning. DrugPatentWatch provides integrated access to patent, regulatory, and litigation data in a format designed for pharmaceutical analysts who need to model these scenarios—tracking not just when patents expire but what has happened in the courts and at the USPTO to the specific patents between grant and expiration.

Modeling Effective Exclusivity for Investment Analysis

For institutional investors, the key analytical construct is “effective exclusivity”—the period during which a branded biologic will face no meaningful price competition—as distinct from nominal patent expiration dates. Effective exclusivity reflects the actual market outcome that results from the interaction of patent coverage, regulatory exclusivity, litigation outcomes, settlement terms, and commercial lifecycle management strategies.

For Humira, the effective exclusivity period in the United States was approximately 21 years from approval—not the 14 years that a composition-patent-only analysis would have predicted, and substantially longer than the 12-year BPCIA exclusivity floor [7]. For Enbrel, the effective exclusivity period is approaching 30 years, a result that no patent-by-patent analysis of the etanercept IP portfolio would have predicted in 2000. For Keytruda, effective exclusivity in the IV formulation will likely end in 2028 or shortly thereafter, because the scale of biosimilar development programs and the commercial importance of the market make sustained litigation delay less viable than it was for Humira in 2016. But Keytruda’s subcutaneous formulation may sustain protected revenue for Merck well into the 2030s.

The investment implication is that branded biologic companies with strong lifecycle management capabilities—demonstrated capacity to execute formulation switches, indication expansions, and combination development—deserve a lower discount rate applied to their post-patent-cliff revenue forecasts than companies that rely solely on litigation-based exclusivity extension. AbbVie post-Humira has invested aggressively in next-generation immunology assets (Rinvoq, Skyrizi) precisely to reduce its dependence on the litigation model. The quality of that pipeline execution is what determines whether AbbVie grows or shrinks in a post-Humira-thicket world.

Part XI: The Future of Biologic IP Strategy

Post-Amgen Patent Prosecution—What Changes

The unanimous Supreme Court ruling in Amgen v. Sanofi has already changed biologic patent prosecution strategy, though the full downstream effect will take years to manifest in issued patents and litigated cases. The shift is from functional genus claims to structural claims—from “all antibodies that do X” to “the antibody with CDR sequences Y and Z that does X by binding to structural epitope Q.”

This is a narrowing of claim scope. An antibody defined by its specific CDR sequences covers one antibody, or a small family of closely related variants. An antibody defined by its function potentially covers millions. The Amgen ruling effectively required that innovators accept narrower claims in exchange for having defensible ones. This is not uniformly disadvantageous: a narrower, valid claim is worth more in litigation than a broad, invalid one. But it does mean that competitors can more easily design around structurally defined antibody claims than around functional genus claims, because designing around a specific CDR sequence is straightforward (generate a different sequence that achieves the same function) while designing around a claim to all antibodies achieving a function is practically impossible.

The implication for biosimilar strategy is significant. Pre-2023 functional genus claims represent litigation vulnerability for brand companies and invalidity opportunity for challengers. Post-2023 structural claims represent narrower but more defensible protection, and design-around freedom is correspondingly greater. The arms race continues—it has simply changed its character.

Artificial Intelligence and Patent Strategy

The pharmaceutical industry’s adoption of AI-driven drug discovery is beginning to intersect with patent strategy in ways that will define the next generation of biologic IP conflicts. Antibodies discovered through computational platforms—AI-designed sequences optimized for specific binding properties—generate structural IP that is both defensible under the post-Amgen standard (sequence-defined, not functional) and potentially more comprehensive (an AI that generates thousands of optimized antibody sequences provides a specification with far more examples than any conventional discovery program could).

Companies building AI discovery platforms—AbSci, Xencor, and Genentech’s internal computational biology group among them—are in a position to file patent applications with specification disclosure that would satisfy the enablement standard more robustly than traditional programs, while covering a structurally diverse set of antibody variants around a given target. This is, in effect, a technology-enabled response to the Amgen constraint: if you cannot claim a functional genus, you can still build a dense structural patent landscape around a target if you have the discovery capacity to generate and characterize sufficient examples.

For biosimilar developers, the AI-enabled patent landscape creates new complexity in freedom-to-operate analysis. Where a traditional antibody program might generate one or two structurally characterized antibodies against a given target, a computational program can generate thousands. Each variant is a potential patent. Designing around one structurally defined claim is easy; designing around hundreds of structurally defined claims covering the tractable epitope landscape of a given target is substantially harder.

Legislative and Regulatory Reform Trajectories

The three tracks of reform activity—USPTO procedural changes, BPCIA statutory amendments, and FTC antitrust enforcement—are all in motion, but none is close to producing a comprehensive resolution to the patent thicket problem.

The USPTO’s proposed terminal disclaimer rule, if finalized in substantially its proposed form, would represent the most significant single change to the thicket-building toolkit. Applied retroactively to existing portfolios, it would expose linked patent chains to chain-invalidation risk that does not currently exist. Applied prospectively, it would deter the accumulation of duplicative patents by dramatically increasing the legal risk associated with each terminal disclaimer filing. The pharmaceutical industry’s opposition to the rule has been intense, and its implementation timeline remains uncertain as of mid-2026.

Congressional proposals to amend the BPCIA directly—by capping the number of patents assertable in Phase I litigation, imposing disclosure requirements for the full patent estate in the Purple Book, or requiring independent invalidity assessment for patents asserted against biosimilar applicants—have bipartisan support in principle but have repeatedly been deprioritized relative to other legislative priorities. The political economy of pharmaceutical pricing reform makes BPCIA amendment genuinely difficult: any provision that reduces brand company exclusivity will be characterized as reducing innovation incentives, and that characterization resonates with legislators across both parties.

FTC enforcement of reverse payment settlements under the FTC v. Actavis standard has been active in the small-molecule context and is increasingly being applied to biologic patent settlements that include license fees or payments disguised as research collaborations. The challenge is evidentiary: proving that a settlement payment is large enough, and sufficiently unexplained by the value of the license obtained, to constitute an anticompetitive reverse payment requires detailed financial analysis of the patent litigation risk being resolved by the settlement. The FTC has the tools but the cases are complex and slow.

Part XII: Cross-Border Dimensions—Why the U.S. Thicket Problem Is Specifically American

The International Patent Divergence

One of the most revealing facts about biologic patent thickets is that they are largely an American phenomenon. The same drugs that are surrounded by 60-, 80-, and 130-patent fortresses in the United States face far smaller patent estates in Canada and the United Kingdom—and biosimilar competition in those markets arrived years earlier as a result. The Oxford Academic research that analyzed Humira’s patent assertions across three jurisdictions found a stark pattern: while AbbVie threatened U.S. biosimilar challengers with up to 63 patents, the same drugs faced far fewer patent assertions in Canada and the UK, and pre-litigation settlement rates were substantially lower in those markets precisely because the coercive power of the patent thicket was weaker [1].

The divergence has several causes. The first is the BPCIA’s statutory structure, which—as discussed—places no cap on the number of patents assertable in Phase I litigation. The Hatch-Waxman framework, which governs U.S. generic drug competition, creates implicit constraints through the Orange Book listing mechanism. The BPCIA equivalent, the Purple Book, lists biosimilars and interchangeability determinations but does not list specific patents. The patent dance disclosure process is confidential and does not create a public registry that would enable systematic tracking of which patents are being asserted and why. The opacity of the BPCIA patent process relative to the transparency of the Orange Book/Paragraph IV system is a structural feature that benefits brand companies by reducing the ability of later biosimilar challengers to free-ride on earlier patent analyses.

The second cause is the U.S. litigation cost structure. Patent litigation in the United States is vastly more expensive than in any comparable jurisdiction. A full BPCIA patent dance proceeding through trial can cost $50 million or more per side on a complex multi-patent case. European patent litigation—which proceeds through national courts with streamlined procedures and lower discovery costs—provides biosimilar challengers with a more level financial playing field. When the cost of litigation is lower, the coercive power of the thicket is weaker: if fighting is cheaper, the settlement terms necessary to buy off a challenger must be more favorable to that challenger.

The third cause is differences in patent examination quality and scope. The USPTO has historically granted broader patent claims than patent offices in Europe or Canada, with lower rates of obviousness rejection for pharmaceutical patents and more permissive treatment of terminal disclaimer-linked portfolios. European patent prosecution for pharmaceutical products tends to result in narrower, more defensible claims—which paradoxically means smaller but more legitimate patent portfolios rather than the large, duplicative thickets characteristic of the U.S. market.

What the European Experience Tells Us About Reform Feasibility

Biosimilar penetration in Europe consistently runs ahead of the United States for the same products. European markets achieved 40-60% biosimilar penetration for adalimumab within two years of first biosimilar entry; the U.S. market, despite having more biosimilar competitors available, had lower substitution rates because the BPCIA litigation settlements created an unusual situation where nine biosimilar products launched within a few months of each other in 2023, with no established pricing hierarchy and payer formulary decisions still in flux.

The European tender system—where national health services and hospital formulary committees conduct competitive bidding for biologic products—creates a different commercial dynamic than the U.S. payer contracting model. In a tender system, price is the primary competitive variable, and biosimilar entry produces rapid and large price reductions because payers can switch entire patient populations in a single formulary cycle. In the U.S. system, biosimilar entry produces more gradual market share gains because physicians and patients must be individually converted, branded rebate contracts create switching friction, and formulary tiers differentiate products in ways that maintain brand volume even at higher prices.

This commercial difference does not make U.S. patent reform irrelevant, but it does suggest that patent reform alone is not sufficient to produce European-level biosimilar penetration in the United States. Even if the patent thicket were fully dismantled—every terminal disclaimer chain invalidated, every formulation patent invalidated, every functional genus claim struck down—the commercial dynamics of the U.S. payer market would still produce slower and less complete biosimilar substitution than European tenders. Full reform requires both patent policy changes and payer market structure changes, and the latter is a harder political problem than the former.

The Pay-for-Delay Problem in the Biologic Context

The Supreme Court’s 2013 decision in FTC v. Actavis established that reverse payment settlements—agreements in which a brand drug company pays a generic challenger to delay its market entry—are subject to antitrust scrutiny under the rule of reason. The decision applied explicitly to small-molecule generic settlements under Hatch-Waxman. Its application to biologic patent settlements under the BPCIA is an open question that courts and the FTC are still resolving.

The challenge in the biologic context is that BPCIA settlements rarely take the form of naked cash payments. Instead, the brand company may license certain non-asserted patents to the biosimilar developer, offer a royalty-bearing license that reduces the biosimilar’s margin but enables launch before the patent expiration date, or enter into co-promotion or distribution arrangements with commercial value. These structures are designed to provide consideration for the delay commitment that is more defensible under Actavis than a cash payment—because Actavis held that a “large and unjustified” reverse payment suggests a settlement designed to maintain market power rather than to avoid litigation risk.

Whether license fees and commercial arrangements provided to biosimilar challengers in BPCIA settlements constitute “large and unjustified” reverse payments is fact-intensive and contested. The FTC has brought enforcement actions against several pharmaceutical settlement agreements under this theory, with mixed results. The complexity of biologic patent portfolios—where the brand company may genuinely be licensing technology of real commercial value rather than simply paying for delay—makes the antitrust analysis harder than in the small-molecule context, where the brand company often has little of commercial value to offer beyond delayed entry.

Part XIII: The Investor’s Framework—Valuing Biologic IP Correctly

The Discounted Cash Flow Trap

The most common error in biologic company valuation is applying a simple DCF model that discounts cash flows at the nominal patent expiration date. You build a revenue forecast, assume it continues to the composition patent expiration year, then apply an 80% haircut in Year 1 post-expiration and model down from there. This approach was wrong for Humira investors in 2016, when the composition patent expired but biosimilar entry was seven years away. It will be wrong for any analyst modeling Keytruda on the simple assumption that IV biosimilar competition arrives immediately in 2028.

The correct approach is to model the probability distribution of effective exclusivity—not a point estimate but a range of scenarios, each assigned a probability based on the specific legal and commercial factors at work. For Keytruda, the relevant scenarios span: (a) IV biosimilar entry in 2028 on the core composition patent expiration, with no significant litigation delay; (b) IV biosimilar entry in 2029-2030 after one or two years of BPCIA litigation on method-of-use and formulation patents; (c) substantial market conversion to subcutaneous Keytruda Qlex before IV biosimilars arrive, materially reducing the IV biosimilar market size and price erosion magnitude; (d) some combination of the above, differing by indication and geographic market.

Each of these scenarios has different revenue and margin implications for Merck, and the probability-weighted expected value of the Keytruda cash flow stream looks quite different depending on how you weight them. The patent landscape data—available through DrugPatentWatch for analysts tracking the evolution of Merck’s patent portfolio and the progress of biosimilar development programs in real time—is the primary input to scenario probability weighting. Analysts who lack access to that data will rely on published consensus estimates that lag reality by months, particularly in the period leading up to significant BPCIA litigation events.

How to Model the Subcutaneous Switch Premium

Valuing the Keytruda Qlex subcutaneous formulation requires modeling a commercial conversion process, not just a patent duration. The question is not “when does the subcutaneous patent expire?” but “what fraction of IV Keytruda volume will convert to subcutaneous before IV biosimilars arrive, and what is the price premium that Merck can maintain on the subcutaneous formulation after IV biosimilars are available?”

The relevant comparable is the Herceptin subcutaneous experience in Europe. Roche launched Herceptin SC (trastuzumab and hyaluronidase, co-formulated) as IV biosimilars entered the market. European data shows that subcutaneous Herceptin maintained a premium price and significant market share even after IV biosimilar entry, because the convenience advantage (5-minute injection vs 30-90 minute infusion) resonated with patients and oncology units managing throughput. U.S. market dynamics will differ—oncology reimbursement structures in the United States mean that infusion revenue matters to oncology practices in ways that European systems do not generate—but the directional analog applies: subcutaneous administration carries a real and defensible clinical preference that sustains market share at premium prices for some period after IV biosimilar entry.

The magnitude of the Keytruda Qlex premium will depend on payer decisions about coverage tiering, the speed of physician conversion to subcutaneous administration in specific tumor type contexts, and the ability of Merck’s commercial team to execute a coordinated formulary positioning strategy. These are commercial execution questions, not IP questions, but they feed directly into the IP value calculation: the longer the subcutaneous formulation’s independent patent protection lasts, the more time Merck has to lock in formulary positions that persist even after that protection expires.

Reading Patent Prosecution History for Valuation Signals

Sophisticated pharmaceutical analysts read patent prosecution histories—the records of communications between a patent applicant and the USPTO during the examination process—because those histories contain information about patent strength that does not appear on the face of the issued patent. Specifically, prosecution histories reveal: the prior art that the USPTO examiner considered; the claim rejections that were issued and the applicant’s responses to them; any claim amendments that narrowed scope in order to secure allowance; and any arguments made by the applicant that may limit the patent’s scope under the doctrine of prosecution history estoppel.

A patent that issued after multiple claim amendments to overcome obviousness rejections, combined with applicant arguments that specifically distinguish the claimed invention from a narrow set of prior art references, is a weaker patent than a patent that issued on first examination with no amendments. The former carries a narrower effective scope—the prosecution history limits what the patent owner can later claim it covers—and a more vulnerable validity profile, because the examiner identified and considered challenges that may resurface in IPR or litigation.

For biologic patent thickets, prosecution history analysis is particularly revealing for formulation and method-of-use patents, which are more likely than composition patents to have faced obviousness rejections during examination. A formulation patent that issued only after the applicant argued that its specific excipient combination produced an unexpected stability improvement is in a very different legal position than one that issued as filed. Tools that provide access to USPTO prosecution file histories—USPTO Patent Center provides this for free, while platforms like DrugPatentWatch integrate prosecution data with litigation and expiration tracking in a format that allows bulk analysis across a portfolio—are essential to this work.

Biosimilar Developer IPO and Capital Raise Analysis

Investment analysis of biosimilar developer companies requires a different set of patent-related inputs than analysis of branded biologic companies. The key questions for a biosimilar developer are: what is the expected timing of first commercial launch for each biosimilar in the pipeline, net of patent litigation risk? What litigation costs should be included in the development cost estimate? What is the probability of a pre-litigation settlement, and on what terms?

These questions require understanding the patent thicket around the reference product, not the biosimilar’s own intellectual property. A biosimilar developer may have no issued patents of its own and still be a valuable company if its development pipeline includes biosimilars targeting products where the patent thickets are demonstrably weak or where the Amgen v. Sanofi standard creates clear invalidity arguments against the asserted claims. Conversely, a biosimilar developer with a pipeline of products targeting drugs in the Humira mold—dense thickets of predominantly terminal disclaimer-linked patents—faces a more challenging commercial environment regardless of the quality of its manufacturing platform.