The executives who built careers navigating Hatch-Waxman—who internalized the 30-month stay, the Paragraph IV certification, the 180-day first-filer exclusivity—carry a set of mental models so deeply embedded they feel like physics. File early. Challenge the core compound patent. Win or settle. Launch and watch prices drop 80 percent. Collect your market share.

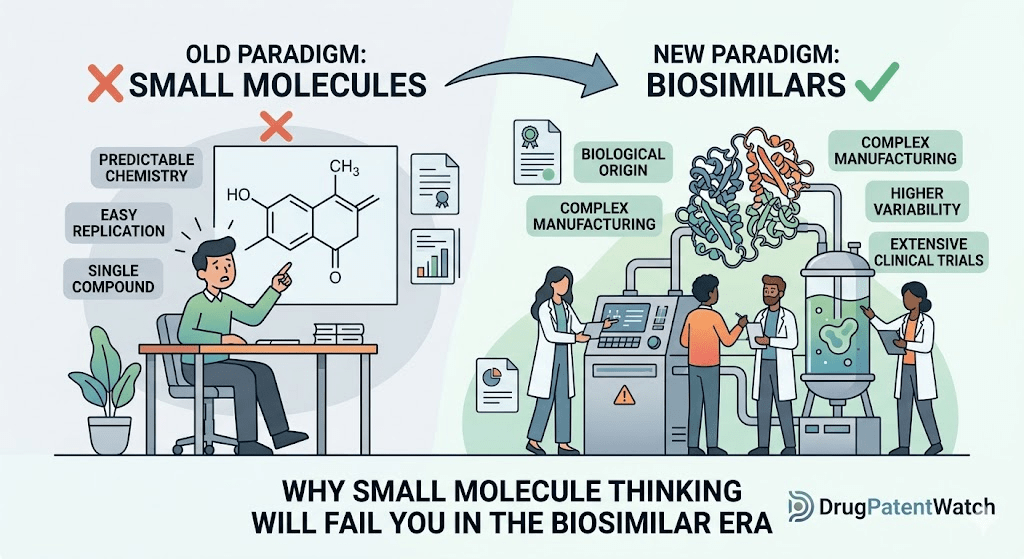

Those models built an industry. They also produce catastrophic miscalculations when applied to biologics.

The biosimilar space runs on different math, different litigation mechanics, different competitive dynamics, and a different commercial playbook. The regulatory pathway looks familiar from a distance—it was deliberately designed to echo Hatch-Waxman—but the resemblance is mostly aesthetic. Underneath, the rules are different enough that the generic drug playbook does not just underperform here. It actively misleads.

This piece maps exactly where small molecule thinking breaks down, what you should replace it with, and what the actual competitive dynamics look like across IP strategy, manufacturing, commercial launch, and pricing. It draws on the AbbVie-Humira litigation record, the adalimumab market entry data from 2023 and 2024, ustekinumab settlement structures, the Sandoz v. Amgen Supreme Court decision on patent dance optionality, and the FDA’s evolving interchangeability standards to give you a complete picture of what biosimilar strategy actually demands.

The Core Cognitive Error: Why Generic Drug Frameworks Mislead in Biologics

The Biologics Price Competition and Innovation Act of 2010 (BPCIA) was intentionally designed to evoke the Hatch-Waxman Act of 1984. Congress wanted people to understand the biosimilar pathway by analogy to the generic pathway. That political communication strategy created a durable misconception.

The analogy holds at the level of intent. Both laws create abbreviated approval pathways. Both establish exclusivity periods. Both set up frameworks for patent resolution without requiring biosimilar or generic applicants to run de novo clinical trials from scratch. That is roughly where the structural similarity ends.

The biosimilar framework runs on a fundamentally different information architecture, a different litigation timeline, different scientific evidentiary standards, a different commercial demand structure, and a different set of post-approval obligations. The most sophisticated IP teams in the generic space—firms that have run dozens of successful Paragraph IV campaigns—routinely misread biosimilar situations because they reach for tools that don’t fit.

The errors cluster into four categories. First, they underestimate the information asymmetry at the start of a biosimilar campaign. Second, they miscalculate the revenue erosion timeline after biosimilar entry, expecting the sharp, rapid curve that characterizes small molecule generics. Third, they underweight manufacturing competence as a durable competitive variable. Fourth, they treat physician adoption as a temporary friction rather than a structural market constraint.

Each of these errors is correctable. But correcting them requires understanding why biologics and small molecules occupy different regulatory and commercial universes, not just adjacent points on the same spectrum.

What ‘Highly Similar’ Means Legally vs. Scientifically

When the FDA approves a generic drug, it approves a molecule that is chemically identical to the reference product. The active ingredient is the same compound. The bioequivalence standard confirms that the generic delivers the same amount of drug to the same biological compartment over the same time window. No clinical endpoint data is required because the regulatory standard assumes that identical molecules in equivalent exposure will produce equivalent effects.

A biosimilar is not identical to its reference product. It cannot be. Biologics are produced in living cell systems—mammalian, yeast, or bacterial—and the manufacturing process determines critical quality attributes including glycosylation patterns, aggregation profiles, charge variants, and higher-order protein structure. Two batches from the same manufacturer are not identical. A biosimilar from a different manufacturing platform will not be identical to the reference product even if the primary amino acid sequence is exact.

The FDA does not require identity. It requires no clinically meaningful differences in safety, purity, and potency. That is a materially different evidentiary standard. It demands comparative analytical characterization, often pharmacokinetic studies, and sometimes clinical immunogenicity data. The agency uses a ‘totality of evidence’ standard that creates uncertainty at the margin and pushes development costs upward.

For IP strategists, this matters because it means the scientific basis of the regulatory dossier is partly opaque until manufacturing is well advanced. You commit hundreds of millions of dollars before you know whether your process generates a molecule that will survive FDA comparability review.

Orange Book vs. Purple Book: The Transparency Gap That Changes Everything

The Orange Book is a public database. It lists every patent a brand manufacturer claims covers an approved drug product, with expiration dates, patent numbers, and claim types. Generic manufacturers use it to structure litigation strategy before they ever file an ANDA. The information is mandatory—Hatch-Waxman requires disclosure as a condition of approval—and the FTC now actively challenges listings it considers improper.

The Purple Book is a different instrument entirely.

U.S. law requires that each application for approval of a small-molecule drug disclose the patents protecting the drug and mandates publication of that information in the Orange Book. U.S. law, however, imposes no patent-disclosure requirement on any application for approval of a large-molecule drug.

That single structural difference reshapes the entire competitive intelligence task for biosimilar developers. When you initiate a biosimilar program, you know the reference product’s approval date, its reference product exclusivity window, and whatever patents the originator has chosen to make public through other channels—press releases, litigation filings, analyst presentations. You do not know the full patent estate you will need to navigate until the BPCIA patent dance begins, which happens after you have filed your aBLA, which happens after you have spent several years and hundreds of millions on development.

The gap between developing a generic drug and a biosimilar is not regulatory paperwork. It is the difference between a $2 million chemistry project with a predictable litigation calendar and a $250 million biological manufacturing challenge conducted partly in the dark, against an innovator company holding hundreds of patents you won’t see until you’ve already committed years of capital.

DrugPatentWatch tracks patent estates across both Orange Book and Purple Book-adjacent sources, aggregating prosecution history, litigation dockets, PTAB filings, and public disclosures to build the most complete picture possible before a biosimilar developer commits to a program. Even with that intelligence infrastructure, the information asymmetry in biologics is structurally larger than in small molecules. You plan around uncertainty rather than certainty.

Purple Book Exclusivity Dates: What They Tell You and What They Don’t

The BPCIA’s 12-year reference product exclusivity period runs from the date of first FDA approval and prevents any biosimilar applicant from relying on the innovator’s data to support a 351(k) application during that window. This is categorically different from the Hatch-Waxman NCE exclusivity: it cannot be circumvented by a biosimilar developer who independently generates equivalent safety and efficacy data, because the exclusivity protection attaches to the reference product’s regulatory status, not to the underlying clinical data.

The Purple Book exclusivity date is a planning anchor, not a launch date. It tells you the earliest point at which you could theoretically receive FDA acceptance of a biosimilar aBLA. It does not tell you when you will actually be allowed to launch, because patent litigation under the BPCIA framework can run independently of and beyond the exclusivity window. AbbVie’s Humira patents extend to 2034 and beyond on certain formulation and manufacturing claims. The 12-year exclusivity window for adalimumab expired in 2014. Biosimilars did not launch in the U.S. until 2023—nine years after exclusivity ended—because of the patent estate that followed.

What the FDA’s 2023 BPPT Provision Changes for Patent Transparency

As of 2023, a new requirement—the Biological Product Patent Transparency (BPPT) provision—requires originators to publish patent lists, which may eventually feed into Purple Book entries. The provision moves the disclosure timeline earlier and gives biosimilar developers at least partial visibility into the patent landscape before they have committed maximum capital. Early analysis suggests the BPPT lists are incomplete relative to what emerges in litigation, but they represent a structural improvement over the prior near-total opacity.

For biosimilar developers currently building programs around assets that fall under BPPT requirements, the calculus has shifted. More pre-filing intelligence is available. The remaining question is whether originators list their strategically threatening patents or manage disclosure to stay technically compliant while preserving tactical surprise. The FTC’s Orange Book enforcement campaign provides a template for challenging improper or strategically unhelpful listings—but the enforcement apparatus has not yet been fully applied to BPPT compliance.

Paragraph IV vs. Patent Dance: How Litigation Mechanics Diverge

In the Hatch-Waxman world, a generic manufacturer’s litigation strategy begins with a decision: certify against the patent, pay to design around it, or wait it out. A Paragraph IV certification is a legal declaration that the listed patent is either invalid or not infringed by the proposed generic product. Filing that certification is treated under the statute as an act of patent infringement, which triggers the brand manufacturer’s right to sue within 45 days and activates a 30-month stay on FDA approval.

The system is transparent, structured, and relatively predictable. The patents at issue are listed in the Orange Book. The legal event that triggers litigation is defined by statute. The 30-month clock is finite. The first generic filer earns 180 days of exclusivity—the dominant commercial incentive structuring the entire race to file.

The BPCIA patent dance operates on a different structural logic entirely.

How the BPCIA Patent Dance Works: The Structured Exchange Phase by Phase

The ‘patent dance’ under the BPCIA is the biosimilar analog of the Hatch-Waxman paragraph certification process, but substantially more complex. The biosimilar applicant and the reference product sponsor exchange lists of potentially relevant patents, engage in a defined negotiation process about which patents to litigate, and then proceed through a structured two-phase litigation framework. The first phase covers a negotiated list of patents, and a second phase covers patents not included in the first. This process can take years and involves significantly more potential IP claims than a typical Hatch-Waxman paragraph certification proceeding.

The mechanics run as follows. After the FDA accepts a biosimilar aBLA for review, the applicant provides the reference product sponsor with confidential information about its manufacturing process—the aBLA itself plus a detailed description of the manufacturing process. The reference product sponsor then has 60 days to provide a list of patents it believes could reasonably be asserted against the biosimilar. The applicant responds with its contentions—infringement positions on each listed patent and invalidity arguments. The parties negotiate a subset of patents for first-phase litigation, subject to statutory limits. Litigation on the agreed list proceeds, followed by a second phase covering patents not included in the first.

Notice to commercialize—a separate statutory requirement giving the reference product sponsor 180 days’ notice before launch—triggers a second wave of potential litigation. In Sandoz v. Amgen (2017), the Supreme Court held that the patent dance is optional, not mandatory, for biosimilar applicants. But the downstream consequences of skipping the dance—particularly accelerating litigation timelines and notice-to-commercialize complexity—mean the decision is genuinely strategic rather than obviously preferable in either direction.

Is the Patent Dance Mandatory? What Sandoz v. Amgen Actually Decided

The BPCIA operates under a ‘Patent Dance,’ which is a private exchange of information between the biosimilar applicant and the reference product sponsor. This exchange became optional following the 2017 Supreme Court decision in Sandoz v. Amgen. What the decision did not resolve was whether skipping the dance creates consequences under state law in certain jurisdictions—an open question that litigation teams navigating early biosimilar launches had to manage carefully in 2018 through 2022.

For practical IP strategy, the optionality matters in two scenarios. First, when the reference product sponsor’s patent estate is well-understood from public litigation records and the biosimilar developer wants to accelerate to litigation rather than exchange information that helps the originator sharpen its patent assertions. Second, when the patent estate is genuinely uncertain and the biosimilar developer values the information exchange in spite of its costs. The decision calculus differs by program and by company. No single rule applies across the industry.

The 30-Month Stay Equivalent in Biosimilars: Why There Isn’t One

The Hatch-Waxman 30-month stay is a regulatory mechanism: if the brand sues within 45 days of receiving Paragraph IV notice, the FDA cannot approve the ANDA until the earlier of 30 months from notice or a court decision clearing the patent. The stay is automatic and gives the brand a defined litigation runway before facing market entry.

The BPCIA has no structural equivalent. There is no automatic stay on FDA approval of a biosimilar aBLA triggered by the reference product sponsor’s decision to litigate. Injunctions are available through court order, but they require the standard four-factor test for preliminary injunctive relief—likelihood of success on the merits, irreparable harm, balance of equities, public interest—rather than an automatic statutory mechanism. Originators who want to block biosimilar launches pending patent resolution must earn injunctive relief rather than receive it by statute.

That asymmetry is one reason biosimilar litigation is structurally less predictable than Hatch-Waxman litigation. The regulatory clock and the legal clock run independently. A biosimilar can receive FDA approval while patent litigation is ongoing, and the launch timing becomes a strategic decision weighted against litigation risk rather than a statutory outcome.

Patent Thickets in Biologics vs. Small Molecules: The Humira Archetype

‘A drug patent thicket is not a set of strong patents protecting a revolutionary molecule. It is a dense, overlapping array of secondary patents—formulation, manufacturing process, delivery device, dosing regimen—designed to create litigation cost and risk that makes any challenge economically unattractive, regardless of the individual merit of each patent.’

— DrugPatentWatch, The Thicket Maze: A Strategic Guide to Navigating and Dismantling Drug Patent Fortresses (2025)

Patent thickets exist in small molecules too. AstraZeneca’s Prilosec, Sanofi’s Plavix, and Bristol-Myers Squibb’s Taxol all generated formulation and method patent litigation that extended exclusivity beyond core compound expiration. But the thickets in small molecules operate within a bounded information environment—every listed patent is in the Orange Book, the FTC is actively challenging improper listings, and the litigation timeline is anchored by the 30-month stay mechanism.

In biologics, thickets are structurally larger, less transparent, and face fewer procedural constraints. Unlike Hatch-Waxman, the BPCIA places no statutory limit on the total number of patents that a brand company can assert against a biosimilar competitor in litigation. This seemingly minor detail is arguably the single biggest reason why patent thickets have become exceptionally dense and problematic in the biologics space. The Humira case is the prime example: AbbVie was able to assert over 60 patents against a single biosimilar challenger.

How AbbVie Built 132 Patents on One Drug: The Adalimumab Patent Portfolio Anatomy

Before the 2016 expiration of the original ‘382 patent for the Humira antibody (adalimumab), AbbVie applied for and obtained 132 patents relating to the formulation and methods of manufacture for Humira with expiration dates extending well past 2016. Within this ‘patent thicket,’ 90% of the patents were issued in 2014 or later, despite Humira first being marketed in 2002.

The patent family anatomy tells the strategic story clearly. The core ‘382 compound patent claiming the adalimumab antibody itself expired in 2016. The subsequent portfolio covers:

High-concentration formulation patents protecting the citrate-free 100mg/mL formulation that became the standard of care (extending into the late 2020s)

Manufacturing process patents covering cell line engineering, purification sequences, and glycosylation control (extending to 2028–2034)

Method-of-use patents for specific dosing regimens in rheumatoid arthritis, psoriasis, and Crohn’s disease

Device patents covering the autoinjector and prefilled syringe systems that most patients actually use

AbbVie applied for approximately 247 patents, of which 132 were granted, creating a ‘patent thicket’ protecting Humira from competition until 2037, when the last patent expires.

No small molecule drug in the history of the Orange Book has a comparable portfolio. The closest analogues—Nexium’s formulation patents, Lipitor’s crystalline form patents—were challenged and largely invalidated on Paragraph IV certification. The Humira estate was large enough that most biosimilar challengers concluded litigation to full resolution was economically irrational and settled instead.

What AbbVie’s Antitrust Exposure Actually Revealed About Thicket Strategy Limits

The antitrust litigation over Humira ran from 2019 through the Seventh Circuit’s 2022 decision. Indirect purchasers argued that AbbVie’s patent thicket, combined with settlement agreements that kept biosimilars out of the U.S. market while permitting European entry, constituted monopolization under Section 2 of the Sherman Act and illegal market allocation under Section 1.

The Seventh Circuit was unpersuaded, viewing the U.S. and EU settlements as ‘traditional resolutions of patent litigation.’ The court concluded that on each continent AbbVie surrendered its monopoly before all of its patents expired, and the rivals were not paid for delay.

The practical lesson from that outcome is not that aggressive biologic patent strategies are legally safe. It is that the legal boundary between legitimate patent settlement and anticompetitive delay is contested, jurisdiction-dependent, and unlikely to be resolved by courts in ways that give biosimilar developers reliable guidance before they commit capital. The Humira thicket survived antitrust challenge in the Seventh Circuit. Different facts, different geography, or different settlements structure could produce different outcomes.

Biologic Thicket vs. Small Molecule Thicket: The Key Structural Differences

Three structural differences separate biologic patent thickets from their small molecule counterparts and explain why generic-trained IP teams systematically underestimate them.

First, the manufacturing process is itself patentable in biologics in ways it rarely is for small molecules. A synthetic route to a small molecule is protectable but relatively constrained—the molecule is what it is, and process modifications are limited by chemistry. A biologic manufacturing process involves cell line selection, growth media composition, fermentation conditions, purification sequences, formulation chemistry, and dozens of other variables, each of which can be independently patented. A biosimilar developer who designs an analytically comparable molecule but uses a different process to get there can still infringe manufacturing patents the originator holds.

Second, the formulation space for biologics is substantially larger. Protein therapeutics are physically unstable—they aggregate, oxidize, deamidate, and degrade through mechanisms that depend sensitively on pH, ionic strength, surfactant type, and container materials. Optimizing a stable, patient-acceptable formulation requires extensive experimentation, and the resulting formulation parameters are patentable. The originator who has already done that work can hold formulation patents that cover the parameter space a biosimilar developer is most likely to inhabit.

Third, biologic patents are harder to challenge analytically. Patents involving the composition of a molecule are often more challenging to litigate compared to manufacturing patents because manufacturing technology is less restrictive. For a Paragraph IV challenger attacking a small molecule polymorph patent, the invalidity argument typically turns on prior art chemical synthesis records. For a biosimilar challenger attacking a biologic manufacturing patent, the invalidity argument requires deep process chemistry expertise and is inherently less certain.

Why the 12-Year Reference Product Exclusivity Period Is Not a Longer Version of NCE Exclusivity

New Chemical Entity exclusivity under Hatch-Waxman runs five years from approval. It prevents the FDA from accepting an ANDA for any drug that contains the same active moiety for that period. The practical consequence is that generic manufacturers cannot even file a Paragraph IV certification during the NCE window—the litigation clock cannot start. Generic entry is effectively blocked for five years regardless of patent position.

The 12-year BPCIA exclusivity works similarly in one sense: it blocks FDA acceptance of a biosimilar aBLA that relies on the reference product’s data. But three structural distinctions make it a categorically different competitive tool.

First, 12 years is long enough that the exclusivity period and the core biologic patent typically expire in the same general timeframe, rather than leaving the patent as the primary post-exclusivity barrier as happens with many small molecules after NCE expiration. For small molecules, the five-year NCE window ends and the core patent often still has a decade to run. For biologics, the 12-year exclusivity window and the core biologic sequence patents tend to co-expire, which means biosimilar developers who invest in development during the exclusivity window are betting on being ready to launch as multiple barriers simultaneously fall.

Second, the 12-year period does not interact with the patent litigation system the way NCE exclusivity does. A biosimilar applicant who waits until Year 12 to file still faces the full patent dance process after filing. They have not used the exclusivity period to position their litigation strategy. The Hatch-Waxman analog would be a generic manufacturer who cannot file a Paragraph IV certification until five years post-approval but then immediately runs the standard litigation calendar. Biosimilar developers do not get that clean sequential structure.

Third, the four-year early-filing provision under the BPCIA allows a biosimilar applicant to file at Year 8 rather than Year 12, at the cost of the FDA not acting on the application until Year 12. This provision enables biosimilar developers to get the regulatory process started while the exclusivity period is still running—a useful tool for compressing timelines but one that requires capital commitment four years before any approved launch is possible.

How the Four-Year Early Filing Window Shapes Biosimilar Development Timelines

The strategic use of the Year 8 filing window is one of the clearest differentiators between sophisticated biosimilar developers and those applying small molecule timing instincts. A generic manufacturer optimizes its ANDA filing to coincide roughly with the end of NCE exclusivity, calibrating development work to be complete as the legal barriers fall. A biosimilar developer who follows that instinct and waits until Year 10 or 11 to begin the aBLA process will consistently be late to market relative to competitors who started at Year 5 or 6 of the reference product’s lifecycle.

The development timeline for a biosimilar is approximately eight to twelve years from program initiation to approval. That is longer than many reference product exclusivity periods, which means biosimilar development for a newly approved biologic must start essentially immediately after the reference product reaches market—well before most commercial-stage IP and market data about the reference product’s performance is available.

Generic manufacturers who try to apply small molecule pipeline logic—wait for proof of commercial success, then file—routinely find themselves developing into a competitive market that is already populated by developers who started earlier. The earliest-starting developers have lower capital efficiency but higher probability of first-to-market premium capture.

Development Cost Asymmetry: $5 Million vs. $375 Million and What It Means for Pipeline Economics

The Pharmaceutical Research and Manufacturers of America estimate it costs in the region of $1.2 billion to develop a new biologic, compared with approximately $375 million and $1.5–4 million for a biosimilar and small molecule generic, respectively.

That cost differential—roughly $375 million for a biosimilar versus $5 million for a small molecule generic—reshapes every pipeline economics calculation. In the generic business, a company can run dozens of development programs simultaneously, spreading risk across a broad portfolio, because the per-program capital requirement is low enough to permit diversification. A failure costs a few million dollars and a couple of years of regulatory work. The portfolio approach was always the rational strategy.

In biosimilars, the per-program capital requirement forces concentration. A company with $1 billion in biosimilar development capital can run two or three programs simultaneously, not twenty. Each program selection decision is a major capital allocation choice, not a probabilistic portfolio bet. The cost structure demands a fundamentally different approach to target selection, competitive intelligence, and risk assessment.

Why Biosimilar NPV Calculations Break Differently Than Generic Drug NPV Calculations

A standard generic drug NPV model discounts cash flows against patent expiration probability, 180-day exclusivity eligibility, and first-to-file race timing. The model is relatively tractable because the key variables are largely knowable from Orange Book data and litigation history before significant capital is deployed.

A biosimilar NPV model requires discounting against variables that are substantially less knowable at investment decision time: the full patent estate (not fully disclosed), the probability of achieving biosimilarity in analytical characterization (depends on manufacturing platform choices not yet finalized), the regulatory pathway to interchangeability (FDA guidance evolves), physician adoption rates (highly indication-dependent), and PBM formulary decisions (subject to rebate negotiations that happen post-launch). The model is correspondingly less reliable, and the error bars around financial projections are wider.

Biosimilars require substantial investments and the NPV framework must incorporate a comprehensive risk assessment through a sensitivity analysis of critical variables such as development timelines, manufacturing costs, and market penetration rates. What this means practically is that biosimilar investment committees need a different analytical framework than generic investment committees—one that explicitly models the range of commercial outcomes rather than treating the binary win/settle/lose structure of Hatch-Waxman litigation as the primary value driver.

Capital Requirements, Clinical Trial Obligations, and How Biosimilar Development Costs Are Allocated

The $375 million biosimilar development cost is distributed across several categories that small molecule developers do not encounter. Cell line development and selection—the process of engineering a host cell that expresses the target protein with acceptable critical quality attributes—can take two to four years and consume $20–50 million before any regulatory-grade material is produced. This has no generic analog. A generic developer chooses a synthetic route and optimizes it; there is no biological engineering phase.

Analytical characterization of biosimilarity is the second major cost center. Demonstrating that a biosimilar is ‘highly similar’ to the reference product across dozens of physicochemical and functional attributes requires state-of-the-art analytical instrumentation and extensive method development. The FDA expects a comprehensive analytical package that can take years to build and cost $50–100 million in well-equipped biosimilar organizations.

Clinical pharmacokinetic studies and, in many programs, phase 3 immunogenicity studies constitute the third major cost category. Generic developers do not run clinical trials. Biosimilar developers typically run at least one PK/PD bridging study and sometimes a full phase 3 program depending on FDA guidance for the reference product’s indication class and the analytical package’s persuasiveness. As FDA science has progressed, some programs have received approval without phase 3 data, but this remains program-specific.

Manufacturing as Competitive Moat: The CMC Reality Generic Developers Underestimate

In small molecule generics, manufacturing is a commodity function. The molecules are synthesized through defined chemical routes, quality is verified through analytical chemistry, and the regulatory barrier is meeting Good Manufacturing Practice standards that most contract manufacturers can satisfy. Manufacturing expertise provides limited differentiation because the science is largely standardized.

In biosimilars, manufacturing is the competitive moat. The biologic product is inextricably defined by the process that produces it. The FDA explicitly states that ‘the process is the product’ for biologics—meaning that two companies producing nominally the same protein through different cell lines, growth conditions, and purification processes will produce biologics that may be analytically distinct even if both are highly similar to the reference product.

Companies with experience in manufacturing, especially in manufacturing biologics, such as Amgen and Biogen, will have a considerable advantage over new companies with no such manufacturing experience. Therefore, experienced companies should dominate the market, which is one reason for the various alliances that enable these companies to be stronger competitors.

Cell Line Development, Glycosylation Control, and Why Manufacturing Failures Kill Biosimilar Programs

The most common technical failure mode in biosimilar development is an inability to control critical quality attributes at manufacturing scale. A biosimilar developer can generate a protein that passes bench-scale characterization and looks analytically similar to the reference product during early development, then discover at process scale that glycosylation patterns shift, aggregation increases, or charge variant profiles drift outside the acceptable range. By that point, years of development work and hundreds of millions of dollars are at risk.

Glycosylation is the primary culprit. Most therapeutic monoclonal antibodies are glycosylated—sugar structures are attached to specific amino acid positions, and those sugars influence the protein’s effector function, half-life, and immunogenicity. The glycan patterns depend on the host cell type, the culture media composition, the dissolved oxygen level, the temperature, and dozens of other process parameters. Controlling glycosylation to match the reference product’s profile requires extensive process development and ongoing manufacturing monitoring. It is not a solved problem that a competent chemistry operation can execute without biological engineering expertise.

What a Strong CMC Package Means for Biosimilar Regulatory Approval Timelines

The FDA’s review of a biosimilar aBLA focuses heavily on the analytical comparability package—the body of data demonstrating structural and functional similarity. A strong package reduces the agency’s residual uncertainty and decreases the probability of a Request for Information or Complete Response Letter that resets the review clock. A weak package—one with unexplained differences in functional assays, high levels of process-related impurities, or limited characterization of post-translational modifications—extends review and may require additional clinical data before approval.

Generic drug approvals rarely require clinical data. The bioequivalence standard is either met or not met, and the agency can typically resolve deficiencies through analytical or pharmacokinetic data. Biosimilar CMC deficiencies sometimes require clinical resolution—additional immunogenicity studies, extended PK comparisons, or phase 3 data in specific indications. The regulatory timeline uncertainty in biosimilars is structurally higher than in generics, even for programs where the science is sound.

Why Revenue Erosion After LOE Looks Nothing Like a Small Molecule Cliff

The small molecule patent cliff is empirically well-documented. Once a generic enters an off-patent small molecule market, brand prices drop sharply as generic pricing undercuts by 80–90 percent, and generic volume share reaches 80–90 percent within 12–18 months. The brand retains a small loyalty segment—typically patients on assistance programs, institutional contracts, or inertial prescribing—but the revenue trajectory is essentially vertical downward.

Where generic entry typically destroys 80–90% of a branded small molecule’s revenue within 18 months, biosimilar competition erodes revenue by only 30–50% over 3–5 years. This difference is not academic; it is the single most important factor in explaining why biologic assets command premium valuations and why acquirers pay more for biologic pipeline programs than for equivalent small molecule programs.

The difference is structural, not temporary. It reflects five distinct factors that do not apply to small molecules.

Five Structural Reasons Biologic Revenue Erosion Is Slower Than Generic Erosion

First, biosimilars are not automatically substitutable. A pharmacist cannot swap a biosimilar for a reference biologic at the dispensing counter without physician authorization unless the biosimilar has received FDA interchangeability designation and the applicable state law permits substitution. Physician prescribing habits are sticky. Switching a stable patient to a new biologic formulation carries perceived clinical risk that has no analog in switching a stable patient from brand-name atorvastatin to generic atorvastatin.

Second, the pricing dynamics are fundamentally different. Generic manufacturers compete on price because the product is identical and the only differentiation is cost. Biosimilar manufacturers compete on formulation attributes, interchangeability designation, patient support infrastructure, and rebate structures negotiated with PBMs. The floor price for a biosimilar is higher than for a generic because development costs are higher and the competitive differentiation extends beyond pure price.

Third, originator biologics are often the anchor of complex PBM rebate arrangements that create formulary protection. AbbVie’s sustained Humira pricing well above biosimilar levels through 2023 and into 2024 reflected rebate architectures that made Humira’s net price competitive with biosimilars’ list prices in many payer contracts. The originator’s rebate leverage depends on volume, which requires maintaining a large prescribing base even as biosimilars enter.

Fourth, patient advocacy and patient support programs create prescribing inertia that generic manufacturers never need to counter. Biologic patients are often on long-term therapy for chronic conditions, and their physicians are cautious about switching biologics that are producing stable disease control. The clinical conservatism is rational and adds structural friction to biosimilar penetration.

Fifth, post-marketing safety surveillance requirements for biosimilars create a pharmacovigilance burden that generics do not carry. Physicians who are uncertain about long-term immunogenicity profiles for new biosimilars sometimes prefer to maintain established patients on reference products until the real-world safety record builds. That preference erodes over time as biosimilar post-marketing data accumulates, but the timeline is three to five years, not three to five months.

Equity analysts covering branded pharmaceutical companies have repeatedly over-penalized biologic LOE events using small molecule cliff assumptions. The error typically manifests as consensus revenue estimates that show a sharp decline in year one of biosimilar competition and a recovery that never materializes because the analysts assumed the originator would lose market share faster than it actually does.

The systematic forecasting error reflects the cognitive anchoring described at the outset of this piece: analysts trained on small molecule patent cliffs apply those patterns to biologic LOE events without adjusting for the structural differences in substitution mechanics, pricing dynamics, and physician prescribing behavior.

More accurate biologic LOE models use indication-specific adoption curves based on comparable prior launches, segment the patient population by payer type (commercial, Medicare Part B, Medicare Part D, Medicaid), model formulary tier assignment probability for biosimilar entrants, and explicitly account for rebate erosion on the originator product rather than assuming the originator’s net price holds while list price competition intensifies.

The Interchangeability Designation: What It Is, What It Isn’t, and Why It Determines Market Share

The FDA’s interchangeability designation is the biosimilar world’s closest analog to the automatic substitution that makes generic drugs commercially dominant. An interchangeable biosimilar can be substituted by a pharmacist without physician intervention, subject to state law substitution requirements. It is the designation that converts a biosimilar from a physician-chosen alternative into a pharmacy-driven default.

The practical effect of interchangeability is that it moves the biosimilar into the same competitive dynamic as a small-molecule generic: pharmacy dispensing decisions drive substitution rather than physician prescribing decisions alone. For high-volume self-injectable products like insulin analogs and adalimumab, interchangeability is the difference between 10% and 40% market share within 24 months of launch.

That 30-percentage-point difference in market share is a commercial consequence of a single regulatory designation. It is the most important regulatory variable in biosimilar commercial planning, and it is one that generic-trained executives frequently underweight because it has no equivalent in small molecule strategy.

FDA Interchangeability Switching Study Requirements and What the June 2024 Policy Reversal Means

Until 2024, FDA guidance required that biosimilars seeking interchangeability designation demonstrate safety and efficacy in multiple switching studies—clinical trials specifically designed to show that patients could alternate between the biosimilar and the reference product without adverse outcomes. These studies added cost, time, and regulatory risk to the interchangeability pathway.

The FDA’s June 2024 reversal on interchangeability switching studies revised this requirement, accepting analytical and clinical data from the biosimilar approval package as sufficient for interchangeability in many cases without dedicated switching studies. The practical consequence is a lower-cost, faster path to interchangeability for biosimilars that have strong analytical comparability packages—a structural improvement in the economics of targeting interchangeability designation from program initiation.

For biosimilar developers making program investment decisions today, the June 2024 guidance change shifts the optimal development strategy. Interchangeability is now more achievable and should be built into initial program design rather than pursued as a post-approval upgrade. Programs that were designed before the guidance change, targeting the old switching study standard, should be reviewed to determine whether the regulatory investment can be redirected.

State Law Substitution Requirements: All 50 States Have Biosimilar Laws, But Variance Persists

As of 2025, all 50 states have enacted biosimilar substitution laws, but they vary in notification requirements. The variation matters commercially. Some states require pharmacist notification to the prescribing physician before substituting an interchangeable biosimilar. Others require patient consent. Some allow substitution with retrospective notification. The operational complexity of navigating fifty different substitution regimes is a real administrative burden for biosimilar manufacturers building distribution infrastructure.

The practical implication for market entry planning is that interchangeability designation does not produce uniform commercial benefit across the U.S. market. A biosimilar with interchangeability designation will see faster pharmacy-driven substitution in states with permissive notification requirements than in states requiring pre-substitution physician authorization. Commercial teams who model interchangeability benefit as a single national rate will consistently misestimate state-level market dynamics.

PBM and Formulary Strategy: How Payer Architecture Replaces Pharmacy Substitution Logic

In the small molecule generic world, the commercial outcome at patent expiration is largely determined by price. Generic manufacturers set list prices at 80–90 percent below brand, pharmacies substitute automatically, and market share follows volume. PBM formulary decisions matter at the margin—preferred generic status can provide incremental volume—but the core commercial outcome is driven by price and automatic substitution.

In the biosimilar world, formulary architecture is the primary commercial lever. A biosimilar without preferred formulary placement can lose to a reference biologic even when priced 30–40 percent below brand list price, because the rebates the originator pays the PBM to maintain formulary preference can make the originator’s net cost competitive with the biosimilar’s lower list price. The commercial team that leads with list price as its primary biosimilar positioning strategy is applying small molecule logic to a market where it doesn’t work.

Rebate Architecture and Biosimilar Formulary Exclusion: What the Humira 2023 Launch Proved

When adalimumab biosimilars launched in January 2023—nine biosimilars entered the U.S. market within weeks of each other—the commercial dynamics were initially more favorable to AbbVie than many analysts predicted. AbbVie had spent years building rebate arrangements with major PBMs that made Humira’s net cost competitive with biosimilar prices at launch. Several major commercial formularies initially excluded adalimumab biosimilars or placed them on non-preferred tiers where high cost-sharing reduced patient demand.

Adalimumab biosimilars gained momentum in 2024 as PBMs reshaped formularies—a trend now extending to ustekinumab. The 2024 formulary restructuring reflected PBMs recalculating whether AbbVie’s rebates still justified Humira’s preferred status as the biosimilar competitive set expanded and biosimilar pricing evolved. The commercial outcome—a gradual rather than sudden shift of volume to biosimilars—is precisely what the structural differences predict.

Adalimumab biosimilars captured 22% U.S. market share within nine months of launch, a pace that would have been implausible a decade earlier. That is a genuinely strong adoption rate for the U.S. biosimilar market historically. It is also substantially slower than the 80–90 percent share capture that characterizes small molecule generic entry in twelve months.

Medicare Part B vs. Part D Biosimilar Incentives: Why the Reimbursement Channel Determines Strategy

Medicare Part B covers biologics administered in a physician’s office—typically infused products like bevacizumab, trastuzumab, and rituximab. Part D covers self-administered biologics dispensed through specialty pharmacy—including adalimumab, etanercept, and ustekinumab. The reimbursement mechanics under each benefit differ substantially, and biosimilar competitive dynamics differ accordingly.

Under Part B, providers are reimbursed at average sales price plus a percentage markup. A biosimilar reimbursed at a lower ASP than the reference product creates a smaller markup for the physician practice, which reduces the financial incentive to prescribe the biosimilar over the reference product. This dynamic—known as the Part B biosimilar payment differential problem—has persistently slowed biosimilar adoption in infused oncology products despite lower list prices.

The Inflation Reduction Act introduced a temporary ASP add-on bonus for qualifying biosimilars under Part B, specifically to address this incentive misalignment. The long-term trajectory of that policy incentive is subject to federal budget discussions and may not provide permanent commercial certainty. Biosimilar manufacturers planning Part B programs need to model the reimbursement incentive scenarios explicitly rather than assuming parity with reference product reimbursement dynamics.

Biosimilar Pricing Strategy: Why Discounting 80 Percent Is Not the Play

Generic drug pricing strategy in the period immediately following patent expiration follows a simple rule: price to win volume. Prices drop sharply, margins are thin, and the companies that survive are those with the lowest cost structures and highest manufacturing efficiency. The competitive moat in generic drugs is operational, not scientific.

Biosimilar pricing strategy cannot follow that model for four structural reasons.

First, development and manufacturing costs are high enough that 80 percent discounts relative to reference biologic prices are not economically viable for most biosimilar programs. A biosimilar developer who spent $300–400 million developing a product needs to recover that investment and earn a return over a market share trajectory that unfolds over years, not months. The pricing floor is fundamentally higher.

Second, deep discounts can paradoxically signal lower quality to prescribing physicians who are already uncertain about biosimilar clinical equivalence. In small molecules, identical chemistry makes price the rational selection criterion. In biologics, where ‘highly similar’ leaves room for clinical conservatism, physicians sometimes interpret aggressive discounting as evidence of a product that needs to compete on price because it cannot compete on clinical confidence.

Third, PBM rebate negotiations require a high list price as a starting point. A biosimilar that launches at 40 percent of Humira’s list price has limited capacity to offer PBMs the rebates needed to secure preferred formulary placement, because the absolute dollar rebate that a 40 percent list price can accommodate is smaller than the rebate a 70 percent list price can accommodate. Formulary placement decisions by PBMs are made on net cost, not list price, and the originator’s rebate machine—built over years at premium list prices—gives it structural negotiating leverage that a deeply discounted biosimilar cannot easily replicate.

Fourth, specialty pharmacy distribution economics favor products with higher per-unit margins. Specialty pharmacies earn spreads, dispensing fees, and performance fees that depend on the product’s reimbursement. Low list price biosimilars generate lower specialty pharmacy economics and may receive less proactive distribution support as a result.

The Right Biosimilar Pricing Framework: Net Cost Parity, Not List Price Discounting

Sophisticated biosimilar commercial strategies target net cost parity with the reference biologic rather than list price discounting. The goal is to make the biosimilar’s net cost to payers equal to or below the reference biologic’s net cost after rebates, while maintaining a list price high enough to support the rebate economics PBMs expect.

This strategy requires detailed intelligence on the originator’s rebate structures with key payers—information that is not public and must be assembled from PBM contracting relationships, analyst commentary, and historical price-volume data. Generic drug commercial teams who have never operated in a rebate-intensive competitive environment frequently lack the organizational capability to execute this strategy, which is one reason biosimilar commercial launches have frequently underperformed projections made by organizations applying generic market entry logic.

PTAB Challenges in Biosimilars: Pre-Approval IPR as Market Entry Acceleration

Inter Partes Review (IPR) petitions at the Patent Trial and Appeal Board provide a route to patent invalidation that runs outside the court system on a faster timeline and with a lower evidentiary burden than district court litigation. Generic manufacturers have used IPR extensively to challenge Orange Book-listed patents—particularly formulation and method patents—and invalidate claims that would otherwise require expensive Hatch-Waxman litigation to overcome.

Biosimilar developers have adopted PTAB more slowly, in part because the absence of Orange Book disclosure means identifying the most valuable targets for IPR challenge requires more intelligence gathering. As biologic patent thickets have become better documented through the BPPT provision, litigation dockets, and commercial intelligence tools like DrugPatentWatch, PTAB strategy has become a more central element of biosimilar entry planning.

One study found that launching patent challenges during Phase 3 (pre-approval) can slash market-entry delay by approximately 4.8x compared to waiting for post-approval fights. That finding reflects the PTAB’s twelve-to-eighteen-month review timeline: an IPR petition filed during biosimilar clinical development can receive a final written decision before the biosimilar aBLA is even under FDA review, clearing patent claims that would otherwise require resolution through the patent dance litigation process.

When to File IPR Petitions vs. Engage the Patent Dance: The Strategic Decision Framework

The decision between PTAB IPR and patent dance litigation is not an either/or choice—both tools can be deployed simultaneously on different patents in the same estate. The relevant strategic question is which patents are most vulnerable to PTAB challenge and which are better addressed through dance litigation, and how to sequence those actions optimally.

Patents with strong prior art bases are PTAB candidates. Manufacturing process patents based on techniques that were known in the literature before the patent filing date, formulation patents covering pH and excipient combinations already disclosed in biophysics literature, and antibody engineering patents claiming approaches described in academic research are all potential IPR targets. The PTAB’s invalidity standard—preponderance of the evidence—is lower than the clear and convincing evidence standard in district court.

Patents with claim scope that depends on interpreting functional claim language, claim construction disputes, or infringement analysis tied to the specific molecular characteristics of the biosimilar under development are often better addressed in dance litigation or district court, where claim construction is more flexible and the factual development of infringement positions is more fully supported.

PTAB Success Rates for Biologic Manufacturing Process Patents vs. Compound Patents

The PTAB has historically shown higher invalidation rates for manufacturing process claims than for core biologic compound claims. Process patents are more vulnerable to prior art arguments because manufacturing techniques evolve through a published scientific literature that provides readily accessible invalidating disclosure. Compound patents claiming novel protein sequences or antibody binding domains face higher PTAB scrutiny on written description and enablement grounds but are less susceptible to prior art invalidity when the molecule is genuinely novel.

For biosimilar developers constructing a PTAB strategy, this pattern suggests prioritizing process and formulation patent challenges while addressing compound claims through dance litigation or settlement. The combination strategy—PTAB for the technically invalidable peripheral claims, dance litigation for the core claims where settlement is probable—is increasingly standard among sophisticated biosimilar market entry teams.

Biosimilar Settlement Structures: How They Differ from Hatch-Waxman Pay-for-Delay

The Federal Trade Commission has aggressively pursued pay-for-delay settlements in the Hatch-Waxman context since the Supreme Court’s 2013 Actavis decision held that large reverse payments to generic challengers can constitute antitrust violations. The enforcement framework gives brands and generics clear parameters: reverse payments above the value of avoided litigation costs face antitrust scrutiny.

Biosimilar settlements operate in a different legal environment. The BPCIA does not create a 180-day first-filer exclusivity period, so the settlement currency that dominates Hatch-Waxman negotiations—sharing the value of 180-day exclusivity with a generic challenger—does not exist. Biosimilar settlements instead typically involve royalty-bearing licenses for early entry, geographic market division (U.S. launch date versus European launch date, as in the Humira settlements), or agreement to launch at defined future dates in exchange for dismissal of patent claims.

Biosimilar manufacturers were able to expedite their launches to 2023—11 years prior to brand patent expiration—due to patent settlements. Without settlements, biosimilar manufacturers simply could not have navigated the 136-patent estate owned by AbbVie and ‘batted one thousand.’

The settlement outcome for adalimumab—nine biosimilar entrants agreeing to royalty-bearing 2023 launches in exchange for not pursuing full patent challenges—was commercially rational for both sides. AbbVie preserved royalty revenue and avoided the risk of patent invalidation on its most commercially critical manufacturing claims. Biosimilar developers secured a defined launch date against a patent estate that would have taken years to litigate to resolution.

Are Biologic Settlements Pay-for-Delay? The Seventh Circuit’s Humira Analysis and Its Limits

Biosimilar manufacturers ultimately dropped their patent cases and negotiated individual settlement agreements with AbbVie, in which they agreed not to contest AbbVie’s patents in the United States and to delay U.S. biosimilar adalimumab entry to 2023 in exchange for AbbVie agreeing not to fight entry of adalimumab biosimilars in the European Union.

The Seventh Circuit found these settlements to be traditional patent litigation resolutions rather than illegal reverse payment arrangements. Legal scholars and FTC economists have contested that characterization—arguing that the European market access AbbVie granted constituted a form of payment with calculable value. The doctrinal status of biologic settlement antitrust exposure remains unsettled, and biosimilar developers negotiating settlements with reference product sponsors in 2025 and beyond should model regulatory challenge risk as a scenario even where prior court outcomes have been favorable to originators.

Physician Adoption as a Commercial Barrier: The Variable That Generic Developers Ignore

Generic drug success requires no physician behavioral change. The pharmacist substitutes the generic. The physician’s prescribing pattern is unchanged. Market share flows to the generic automatically through the dispensing system.

Biosimilar success, for products that lack interchangeability designation, requires physician behavior change. The physician must actively choose to prescribe the biosimilar, either for new patients initiating therapy or, more slowly, for established patients being transitioned. That behavioral change has to be earned through education, clinical evidence communication, patient support services, and in some cases financial incentives through managed care contracting.

The commercial infrastructure required to drive physician adoption—medical affairs teams, clinical liaisons, speaker programs, real-world evidence publication—is expensive, relationship-intensive, and entirely absent from the generic drug commercial model. Generic manufacturers who enter biosimilars without building this infrastructure consistently underperform their market share projections because they have no mechanism to convert physician familiarity into prescribing decisions.

How Indication Mix Affects Physician Adoption Rates Across Biosimilar Programs

Physician adoption rates for biosimilars vary substantially by indication and patient population. Oncology biologics—bevacizumab biosimilars in non-small cell lung cancer, trastuzumab biosimilars in breast cancer, rituximab biosimilars in non-Hodgkin’s lymphoma—have achieved high adoption rates in part because oncologists are accustomed to managing drug-related toxicity risk and have become increasingly confident in the clinical equivalence of well-characterized biosimilars. Biosimilar penetration in oncology indications has in some segments exceeded 80 percent.

Autoimmune biologics—adalimumab, etanercept, ustekinumab—show slower adoption patterns because the treating physicians (rheumatologists, dermatologists, gastroenterologists) are managing patients on long-term therapy for chronic conditions where stability is highly valued and transitions are perceived as risk events. These specialties require more extensive clinical evidence communication and are more influenced by payer mandate than by proactive prescriber choice.

Endocrine and metabolic biologics—insulin analogs, growth hormone products—occupy a middle position where patient experience and device usability factors substantially influence adoption alongside clinical confidence and payer decision-making.

What 22% Market Share in Nine Months Tells You About the Adalimumab Commercial Dynamics

Adalimumab biosimilars captured 22% U.S. market share within nine months of launch. That figure deserves careful interpretation. It represents aggregate share across nine biosimilar products from different manufacturers with different formulation profiles, different interchangeability designations, and different commercial organizations. The aggregate obscures substantial variation at the product level—some biosimilars achieved strong early penetration in specific segments while others captured minimal share.

The products that achieved faster share capture had three characteristics in common: interchangeability designation enabling pharmacy substitution, citrate-free high-concentration formulation matching the preferred Humira administration profile, and either strong PBM formulary placement or preferred status on major commercial plans. Products lacking any of these three attributes typically captured negligible share in the early launch period regardless of their clinical data package or price point.

For biosimilar developers planning programs that will enter competitive markets between 2026 and 2030, the adalimumab launch data provides a clear commercial template: interchangeability, formulation parity with the reference product, and formulary architecture are the variables that determine commercial success. Price is a hygiene factor, not a differentiation strategy.

Ustekinumab Biosimilars: The Next Patent Cliff and What It Tells You About Settlement Architecture

Ustekinumab—sold by Johnson and Johnson as Stelara—is the IL-12/IL-23 biologic indicated for plaque psoriasis, psoriatic arthritis, Crohn’s disease, and ulcerative colitis. Ustekinumab lost its core U.S. patent exclusivity in late 2023. Multiple biosimilars launched in 2025 following settlement agreements that established royalty-bearing access. J&J reported Stelara revenue declining sharply through 2024–2025 as biosimilar competition materialized.

The ustekinumab situation illustrates a different settlement architecture than Humira. The Stelara patent estate is smaller—J&J did not build a 132-patent thicket comparable to AbbVie’s—and biosimilar settlements focused on negotiating launch dates and royalty structures without the geographic market division that characterized the Humira deals. Biosimilar developers including Amgen, Samsung Bioepis, Fresenius Kabi, and others negotiated entry at or near the core patent expiration rather than years after it.

The commercial result is earlier and steeper revenue erosion for J&J than AbbVie experienced in 2023. Without a multi-year settlement buffer, the originator faces competition sooner and has less time to rebuild its rebate structures to defend volume. The ustekinumab market is forecasted to show more rapid biosimilar penetration than adalimumab, in part because the market structure is less defended and the entry cohort includes biosimilars with interchangeability designation from launch.

What Biosimilar Stelara vs. Humira Market Dynamics Reveal About Patent Estate Strategy

Comparing adalimumab and ustekinumab biosimilar market entry dynamics provides a natural experiment in the commercial consequences of different patent estate architectures. AbbVie’s aggressive patent filing strategy bought years of effectively protected U.S. market position beyond core compound exclusivity—at the cost of ongoing patent thicket maintenance expenses, antitrust litigation defense costs, and reputational exposure that contributed to Congressional interest in pharmaceutical IP reform. J&J’s less aggressive approach produced earlier biosimilar entry and more rapid revenue erosion but lower ongoing IP defense costs and significantly less antitrust risk.

The comparison does not yield a simple answer about which strategy is superior because the decision depends on factors specific to each product—the magnitude of patent thicket maintenance economics relative to protected revenue, the probability of antitrust enforcement success, and the scale of the revenue base being protected. What it demonstrates clearly is that the commercial outcomes from biosimilar entry are substantially shaped by patent estate strategy decisions made years before launch, not by the post-patent-expiration commercial execution of either the originator or the biosimilar entrant.

Supply Chain and Cold Chain: The Infrastructure Requirement That Small Molecule Players Underestimate

Small molecule generics ship at room temperature in standard pharmaceutical-grade packaging. The cold chain—refrigerated storage and transport infrastructure—is not a competitive factor in generic drug distribution. A generic can be stored at any licensed pharmacy, shipped through standard drug distribution networks, and held in standard medication storage without special equipment.

Biologics require cold chain infrastructure from manufacturing through administration. Monoclonal antibodies, fusion proteins, and other large molecule therapeutics are protein-based and susceptible to irreversible denaturation or aggregation if exposed to temperatures outside their specified range. Cold chain failures—temperature excursions during storage or transport—produce product that is potentially immunogenic or inactive, and detecting those failures reliably requires continuous temperature monitoring rather than spot checks.

Biosimilars have to overcome the particular barriers that are associated with manufacturing, marketing, storage (cold) and other distribution issues, delivery devices, immunogenicity, and special requirements for pharmacovigilance.

The cold chain requirement adds distribution cost and complexity. It restricts the universe of distribution partners capable of handling biosimilar products to specialty distributors and specialty pharmacies with validated cold chain operations. It creates regulatory documentation obligations—excursion records, temperature maps, stability testing—that small molecule generic companies rarely encounter. It is also a point of competitive differentiation: biosimilar manufacturers with strong cold chain quality systems are less likely to experience distribution-related product failures that generate adverse event reports and physician loss of confidence.

Device Strategy: Auto-Injectors, Pre-Filled Syringes, and the Patient Experience Competitive Dimension

Self-administered biologics are typically delivered via auto-injector or pre-filled syringe. The physical device—its ergonomics, injection force, needle length, reconstitution requirements, and the subjective experience of the injection—materially influences patient adherence and physician choice. Humira’s transition from a high-concentration citrate-containing formulation (which caused injection site pain) to a citrate-free high-concentration formulation was itself a strategic move designed to improve patient experience and create new patent coverage simultaneously.

Biosimilar developers who match the reference product’s formulation but use a different delivery device introduce a clinical and commercial variable that physicians and patients can cite as a reason for product choice. A biosimilar with a less patient-friendly device can lose market share to a biosimilar with equivalent clinical data but better injection experience, independent of price or interchangeability status.

Device strategy for biosimilars is therefore a commercial function, not merely an engineering convenience. It requires understanding the reference product’s device pain points, designing to address them, and potentially developing proprietary device designs that serve as differentiation from both the originator and competing biosimilars. It is a dimension of biosimilar competition entirely absent from the small molecule generic playbook.

What Happens When a Biosimilar Fails the Patent Dance? Litigation Scenarios and Injunctive Relief

A biosimilar developer who skips the patent dance, mis-sequences notice obligations, or launches at-risk without patent dance completion faces the prospect of preliminary injunctive relief halting commercial launch while litigation proceeds. In the Hatch-Waxman system, this scenario is relatively rare because the 30-month stay provides a defined litigation runway before any approved generic can launch. In the BPCIA system, where FDA approval and launch authorization are legally separable and the patent dance can be skipped, the risk of at-risk launch and subsequent injunction is more directly managed by the biosimilar developer’s choice of litigation strategy.

The injunction standard in BPCIA litigation requires the reference product sponsor to show likelihood of success on patent infringement claims, which in practice means demonstrating that the biosimilar’s manufacturing process or formulation infringes valid claims. Early-stage injunctions—before the full merits have been litigated—are difficult to obtain in patent cases, but the threat of an injunction during the commercially critical launch period imposes settlement leverage on biosimilar developers even when the underlying patent claims may not be strong.

At-Risk Launch Decisions in Biosimilars vs. Small Molecules: Risk-Reward Calculation Differences

Generic manufacturers routinely launch at-risk after Paragraph IV victories at the district court level while appeals are pending, accepting the possibility of damages liability in exchange for capturing market share during the appeal period. The damages exposure in a small molecule at-risk launch is quantified in terms of the brand manufacturer’s lost profits on sales diverted to the generic—typically a defined, calculable number based on the brand’s post-generic sales volume.

At-risk launch in biosimilars faces a different damages calculation. A reference product sponsor asserting manufacturing process patent infringement can seek a royalty on every biosimilar unit sold during the infringing period, plus potentially enhanced damages for willful infringement if the biosimilar developer proceeded with knowledge of the patent. The magnitude of potential damages can be larger relative to the at-risk sales volume than in small molecule cases because biologic product unit economics generate higher revenue per unit and royalty rates in biologic patent licenses are typically higher than in small molecule settlements.

Biosimilar developers who apply generic at-risk launch logic without adjusting for these differences in damages exposure and injunction probability can significantly underestimate the litigation risk associated with early commercial entry.

The pattern is consistent enough to qualify as a systematic bias. Equity research analysts covering branded pharmaceutical companies with major biologic franchises approaching LOE events consistently overestimate the speed and depth of revenue erosion in the first two to three years of biosimilar competition. The overestimation leads to excessive share price discounting in the pre-LOE period and subsequent share price recovery when the originator beats consensus revenue expectations by maintaining higher market share and pricing than analysts modeled.

The bias traces directly to small molecule cliff assumptions applied to a market that does not behave like a small molecule cliff. Analysts who covered the generic drug industry built intuitions about LOE dynamics that informed their biologic LOE forecasts, and those intuitions are consistently wrong in the direction of overstating competitive erosion speed.

Three specific modeling errors account for most of the forecasting gap. First, analysts typically model a single blended market share erosion curve rather than segmenting the patient population by payer type and formulary tier. Commercial patients on employer-sponsored insurance experience different biosimilar adoption rates than Medicare Part D patients because the formulary management practices differ. Blending these populations understates originator persistence in the Medicare channel and overstates it in commercial managed care.

Second, analysts frequently undermodel the originator’s ability to defend net price through rebate increases. When biosimilars enter at list prices 20–40 percent below the originator’s list price, the originator can increase its rebate offer to PBMs to maintain net cost parity—maintaining formulary preference at the cost of reduced gross margin. This dynamic preserves originator volume at the expense of originator realized price, producing revenue outcomes different from both the originator’s list price trajectory and the biosimilar’s gross-to-net math.

Third, analysts undermodel the time required to build interchangeability-driven pharmacy substitution volume. When a biosimilar receives interchangeability designation, analysts sometimes model rapid volume ramp assuming the designation immediately produces generic-like substitution rates. The reality is that state law variation, pharmacy system programming, specialty pharmacy contracting, and PBM formulary decisions all create friction that delays interchangeability benefit even after FDA designation.

The Correct Biosimilar LOE Financial Model: A Framework for Investor Analysis

A complete biosimilar LOE financial model requires eight distinct components that generic drug LOE models do not need.

The first is a payer segment map: quantify the patient population by commercial, Medicare Part D, Medicare Part B, Medicaid, and cash-pay segments, with separate market dynamics modeled for each. The second is a formulary scenario model: project preferred, non-preferred, and excluded tier placement probability for biosimilars across major payer plans, weighted by covered lives. The third is a rebate erosion model: estimate the originator’s rebate trajectory as competitive pressure forces margin concession to defend formulary placement. The fourth is an interchangeability timing model: map the expected state-by-state adoption ramp following FDA interchangeability designation. The fifth is a physician adoption curve by specialty: model rheumatology, oncology, and gastroenterology adoption separately given their structurally different switching propensities. The sixth is a competitive entry sequencing model: project which biosimilar entrants achieve commercial scale and which struggle, and how the competitive set consolidates over time. The seventh is a manufacturing capacity constraint model: assess whether sufficient biosimilar manufacturing capacity exists to supply the market even if demand shifts quickly. The eighth is a post-marketing commitment risk model: account for the possibility that FDA requires additional safety or immunogenicity data that could restrict one or more biosimilar entrants.

The Strategic Investor’s Checklist for Biosimilar Pipeline Assets

Investors evaluating biosimilar pipeline assets—whether in public company equity analysis, venture capital due diligence, or acquisition target assessment—need a distinct analytical framework that does not map onto generic drug pipeline valuation.

The checklist starts with manufacturing platform maturity. Does the developer have a validated manufacturing process for the specific product class? Large-scale monoclonal antibody manufacturing, ADC production, and fusion protein manufacturing each have different equipment and process control requirements. A developer with a validated platform for one class does not automatically have the competencies required for another. Platform maturity is the single variable most predictive of development timeline risk.

The second element is analytical characterization depth. Does the biosimilar’s analytical package demonstrate high similarity across the critical quality attributes most likely to create FDA concerns for the specific reference product? For an antibody with a complex glycosylation profile, does the developer have the analytical methodology to characterize and control that profile? For a protein with documented immunogenicity concerns, does the developer have robust immunogenicity assays?

Third, assess patent landscape intelligence completeness. Has the developer used tools like DrugPatentWatch to build a comprehensive picture of the reference product’s patent estate, including not only filed patents but prosecution history, continuation applications pending, and patents held by third-party licensors? Incomplete patent landscape intelligence is one of the most common sources of biosimilar program disruption, producing unexpected litigation that delays or blocks launch.

Fourth, evaluate commercial organization capability. Does the developer have the medical affairs, managed markets, and payer contracting infrastructure required to support a biosimilar launch? Specifically, does it have relationships with the major PBMs and experience negotiating biosimilar formulary placement? Organizations that lack this infrastructure will either underperform market share projections or face acquisition by commercial-stage companies at unfavorable valuations.

Fifth, confirm interchangeability pathway planning. Is the development program designed to achieve interchangeability designation under the post-2024 FDA guidance, and has the analytical and clinical work required for that designation been incorporated into the aBLA strategy? Programs that did not plan for interchangeability from initiation may require costly protocol amendments or additional studies.

Key Takeaways

The BPCIA and Hatch-Waxman look similar by legislative design but operate on fundamentally different legal, scientific, and commercial mechanics. Applying generic drug logic to biosimilar strategy produces systematic errors across IP, commercial, and financial planning.

The Orange Book’s patent transparency requirement has no equivalent in the biosimilar world. The Purple Book lists exclusivity dates but not patent estates. Biosimilar developers commit capital in partial informational darkness and must build intelligence from litigation records, prosecution history, and tools like DrugPatentWatch rather than regulatory disclosure.

The BPCIA patent dance is optional after Sandoz v. Amgen but the decision to skip it has consequences for litigation timeline and notice-to-commercialize obligations. Neither engagement nor avoidance is universally correct—the decision is program-specific and requires genuine strategic analysis.

AbbVie’s 132-patent Humira estate is the archetype of biologic patent thicket strategy. The estate survived antitrust challenge in the Seventh Circuit, but the doctrinal status of biologic settlement arrangements under federal antitrust law is not fully settled.

The 12-year BPCIA reference product exclusivity is structurally different from Hatch-Waxman NCE exclusivity. It does not interact with the patent dance the same way, and it does not provide the same clean sequential structure between exclusivity expiration and litigation commencement.

Biosimilar development costs average $300–400 million per program, roughly 80–100 times the cost of a small molecule generic program. This changes pipeline portfolio strategy from diversification to concentration.