A forensic guide to pharmaceutical life cycle extension: the IP strategies, regulatory mechanics, and commercial execution frameworks that separate drugs with ten-year franchises from ones that collapse overnight.

The day a pharmaceutical blockbuster loses patent protection is not a single event. It is the culmination of decisions made, or not made, five to ten years earlier. When generic manufacturers flood the market after a brand drug loses exclusivity, the revenue drop is not gradual. FDA data consistently shows that a branded drug loses 80% to 90% of its prescription volume within twelve months of generic entry when multiple competitors enter simultaneously. For a drug generating $3 billion in annual U.S. sales, that means $2.4 billion in revenue disappears within a year.

The companies that absorb that loss as an unmanageable shock are the ones that treated life cycle extension as a last-minute defensive exercise. The ones that navigate it profitably are the ones that built a structured franchise around the original molecule years before the primary patent expired, layering additional IP, pursuing regulatory exclusivities the statute explicitly created for them, and executing commercial strategies designed to migrate the patient base before generic substitution became a market reality.

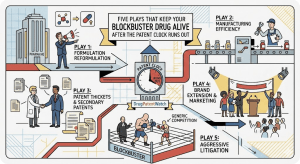

This article covers the five strategic plays that pharmaceutical companies use to extend the commercial life of their blockbusters. It covers the legal basis for each strategy, the mechanics of execution, the data on financial returns, and the real-world case studies that reveal what actually works versus what looks good in a boardroom presentation. Where relevant, it draws on the kind of patent landscape intelligence that platforms like DrugPatentWatch make accessible, because none of these strategies can be executed without knowing exactly where your patent protection stands, where the vulnerabilities are, and what your competitors are planning.

The five plays are not equally available to every product. Some require the right molecular characteristics. Some require specific clinical data. Some require organizational capabilities that not every pharmaceutical company has built. But understanding all five, and knowing when each one applies, is the foundational competency for anyone responsible for managing the commercial lifecycle of a high-revenue pharmaceutical product.

Play One: The Formulation Fortress

Building a Secondary Patent Portfolio That Generic Companies Cannot Walk Around

The composition-of-matter patent is the most powerful IP asset in pharmaceutical development. It covers the active ingredient itself, not any particular form of it, meaning any product containing the molecule infringes the patent regardless of how it is formulated, what indication it targets, or how it is packaged. When a composition-of-matter patent expires, the door to generic competition opens fully and immediately. The brand company’s response to that expiry, ideally executed three to five years before it happens, is the formulation fortress.

The formulation fortress strategy involves systematically developing new formulations of the approved molecule that offer genuine clinical utility and generating patents on those formulations that qualify for Orange Book listing. The objective is to have, by the time the composition patent expires, a reformulated product already on the market with its own protected intellectual property, a migrated patient base, and a set of Orange Book-listed patents that any subsequent ANDA filer must either challenge through Paragraph IV certification or wait out.

The strategy rests on a specific legal architecture. Orange Book-listed patents covering drug formulations are fully eligible for the Hatch-Waxman 30-month automatic stay when challenged by a Paragraph IV certification. An ANDA applicant who files against a formulation-patented product faces the same litigation clock, the same 30-month delay risk, and the same cost of patent litigation as one challenging a composition-of-matter patent. The only difference is that formulation patents are typically narrower and therefore more vulnerable to design-around strategies, which means the fortress must be built with enough walls that no single design-around defeats the entire structure.

What Qualifies as a Defensible Formulation Patent

Not every change to a drug product generates a defensible patent. The most common formulation innovation categories that produce Orange Book-listable patents with genuine claim scope include extended-release or controlled-release mechanisms, abuse-deterrent delivery systems, new salt or polymorph forms with distinct physical properties, prodrug conversions that improve bioavailability or tolerability, particle size or nanotechnology modifications that change pharmacokinetic profiles, and combination products that pair the original molecule with a complementary agent.

The quality of the formulation patent matters enormously. A broad, well-written formulation patent that covers a range of polymer compositions capable of achieving the desired release profile is far more defensible than a narrow patent claiming a specific percentage of a specific polymer. Generic formulators are skilled at modifying their formulations to avoid specific claim language while achieving the same functional result. The only way to build formulation IP that actually holds is to work with patent counsel who understand both the formulation science and the patent prosecution strategy from the earliest stages of formulation development.

The structural requirement that makes formulation patents enforceable is the connection to actual clinical differentiation. Courts have been increasingly skeptical of obviousness defenses to formulation patents when the brand company can demonstrate that the specific formulation choice was not obvious to a skilled formulator at the time of invention and that the resulting formulation produces unexpected results. A once-daily extended-release formulation that achieves the same efficacy with demonstrably better adherence than twice-daily dosing, supported by pharmacokinetic data showing the specific technical challenges overcome to achieve the profile, presents a stronger obviousness defense than a formulation that merely changes the polymer blend without demonstrable consequence.

The Patient Migration Imperative

A formulation fortress only functions commercially if the patient base migrates from the original formulation to the new, protected one before generic versions of the original product arrive. This is the product hop, and it is the execution challenge that determines whether the fortress delivers its financial promise.

The product hop requires coordinated execution across regulatory, commercial, and medical affairs functions. The regulatory team needs to obtain approval of the new formulation with a label that physicians and payers can adopt. Medical affairs needs to generate the clinical data and publications that support formulary placement and prescribing preference. Commercial needs to execute an active promotion campaign that shifts prescribers from the original formulation to the new one, and managed care needs to negotiate formulary positioning for the new product that maintains or improves reimbursement before the generics arrive.

The legal boundaries on product hops have been tested in multiple court cases. The most instructive is the Namenda XR litigation, where Forest Laboratories sought to withdraw Namenda immediate-release from the market to force prescribers onto the extended-release formulation before generic IR became available. A court order in New York blocked the withdrawal, finding that it constituted anticompetitive conduct designed to forestall competition rather than serve patient interests [1]. The decision established that a hard withdrawal of the original product to coerce migration is legally vulnerable; a soft migration, where the brand continues promoting the new formulation while leaving the original available, is much more defensible.

The commercial data on patient migration success is mixed and product-specific. Forest’s Namenda XR program, despite the legal challenge to the hard switch attempt, ultimately succeeded in migrating a significant portion of the Namenda patient base to the extended-release formulation. By the time Namenda IR generics entered the market, the XR formulation controlled approximately 75% of memantine prescriptions in the U.S., significantly dampening the revenue impact of generic IR entry [2]. That outcome, achieved largely through commercial execution rather than the attempted hard switch, demonstrates that migration can work even under legal pressure.

Case Study: Purdue’s OxyContin Reformulation

Purdue Pharma’s reformulation of OxyContin from a tamper-susceptible extended-release formulation to an abuse-deterrent extended-release product is the most widely analyzed formulation fortress execution in pharmaceutical history, though its ultimate legacy is inseparable from the broader opioid crisis that followed.

From a pure IP and regulatory mechanics perspective, Purdue’s strategy was precise. The company developed a new polyethylene oxide-based matrix formulation that converted to a viscous gel when tampered with, resisting crushing and injection. Purdue filed 505(b)(2) applications for the new formulation and generated multiple Orange Book-listed patents covering the abuse-deterrent matrix technology. The FDA approved the reformulation in 2010 and in 2013 determined that the original OxyContin formulation should be withdrawn and that the new formulation warranted labeling stating that it had abuse-deterrent properties [3].

The IP and regulatory execution worked as designed. When generic manufacturers filed ANDAs referencing the original OxyContin formulation, the FDA was able to decline those applications on grounds that the reference listed drug had been withdrawn for reasons of safety or effectiveness, while ANDA filers challenging the new formulation’s patents faced both litigation costs and the FDA’s specific requirements for demonstrating abuse-deterrence in generic products. The formulation fortress effectively closed the generic entry path for the standard opioid format while the new formulation maintained brand exclusivity.

The case illustrates both the commercial power of the formulation fortress strategy and the policy complications it can generate. The FDA’s guidance on abuse-deterrent opioids, specifically designed to incentivize reformulation investments like Purdue’s, has since become the subject of significant public health debate. But the regulatory and IP mechanics of the strategy operated exactly as designed.

Play Two: Indication Expansion

Why New Clinical Data on Old Molecules Is One of the Best Returns in Drug Development

New drug indications are approved through the same 505(b)(2) pathway that covers formulation changes, and they carry a distinct financial logic: the safety foundation of an approved molecule is already established, meaning Phase I trials can be abbreviated or eliminated and the clinical development program focuses exclusively on proving efficacy and safety in the new patient population. That reduces development cost, development time, and clinical risk relative to a novel compound targeting the same indication.

The return structure for indication expansion depends primarily on three variables: the size and value of the new indication, the exclusivity available to protect the new use, and whether the new indication’s label language can be protected from generic carve-out strategies through method-of-treatment patents.

On exclusivity, a new indication supported by new clinical investigations qualifies for three-year new clinical investigations exclusivity. That exclusivity is not broad, it protects only the specific new condition of use approved based on the new data, and an ANDA filer can avoid it by carving the new indication out of their proposed labeling. But three years of exclusivity on a large indication, combined with method-of-treatment patents covering the new use, can be commercially significant if the indication attracts premium pricing.

The orphan drug pathway creates the most valuable indication expansion economics. Seven years of market exclusivity for an orphan indication, defined as affecting fewer than 200,000 U.S. patients, cannot be circumvented by a generic carve-out. A generic cannot be approved for the same drug in the same orphan condition for seven years from the date of brand approval. For a well-established molecule with a new orphan application, that seven-year window at orphan drug pricing represents returns that can dwarf the economics of the original indication.

The Method-of-Treatment Patent Layer

The most durable protection for a new indication is a method-of-treatment patent that covers administering the drug for the specific new purpose. Method-of-treatment patents are Orange Book-listable if they cover a method of using the drug as approved, and they require Paragraph IV certification from any ANDA applicant who wants to include the patented indication in their labeling.

The complexity in method-of-treatment patent protection is the skinny label carve-out. Under Hatch-Waxman, an ANDA applicant can propose labeling that omits the patented indication, stating only the non-patented indications for which it seeks approval. If the FDA accepts the carved-out labeling as scientifically coherent (meaning the drug can be safely prescribed without reference to the patented indication), the ANDA can be approved without infringing the method patent.

Whether the carve-out actually protects the generic company from infringement liability is a contested question. The Federal Circuit’s decision in GlaxoSmithKline v. Teva established that a generic manufacturer can be held liable for induced infringement of a method-of-treatment patent even with a labeled carve-out, if the evidence shows that the generic product would inevitably be prescribed for the patented indication [4]. That decision created substantial uncertainty about the reliability of skinny labels as a safe harbor and has led some generic companies to either avoid challenging method-of-treatment patents entirely or to accept the litigation risk as part of their business model.

Brand companies seeking maximum protection for new indications should work proactively with patent counsel to draft method-of-treatment patent claims that are difficult to avoid through carve-outs. Claims that cover the core treatment mechanism rather than only secondary aspects of the indication create carve-out challenges because the patented use may be the primary use of the drug. The more the patented indication represents a dominant use of the drug, the more difficult the carve-out strategy becomes for generic applicants.

Pediatric Indication Development: Six Months That Changes the Math

The six-month pediatric exclusivity extension available under the Best Pharmaceuticals for Children Act is, from a pure return-on-investment perspective, one of the most efficient capital deployments in pharmaceutical development. The FDA issues a Written Request specifying the studies it wants the company to conduct in pediatric patients; if the company conducts those studies and submits the results whether or not they demonstrate efficacy in the pediatric population the FDA grants six months of additional exclusivity that attaches to every unexpired patent and regulatory exclusivity for the drug.

The extension applies not just to the pediatric indication but to all uses of the drug covered by unexpired Orange Book patents. A drug with $2 billion in annual adult indication sales generating six months of additional exclusivity from a pediatric study program earns approximately $1 billion in incremental revenue. The pediatric study program itself might cost $50 million to $100 million. No other research investment in pharmaceutical development generates comparable returns with comparable reliability.

The mechanics require attention. The FDA issues Written Requests selectively, prioritizing pediatric populations with unmet medical needs and drugs that are actually likely to be used in children. A company seeking a Written Request must affirmatively engage with the FDA’s pediatric office, often through a Pediatric Study Plan submission, to make the case that their product merits a request. The FDA’s Office of Pediatric Therapeutics and PREA requirements for drugs likely to be used in pediatric populations create both mandatory and voluntary pathways to pediatric exclusivity.

The six-month extension also applies at the FDA’s discretion to drug products currently protected only by regulatory exclusivity with no remaining patent coverage. That provision creates pediatric exclusivity opportunities even for drugs whose composition-of-matter patents have already expired, as long as some form of data exclusivity or Orange Book patent is still running. Pharmaceutical companies with products approaching exclusivity cliffs should review Written Request eligibility as part of their standard lifecycle planning process.

Case Study: Jazz Pharmaceuticals and Xyrem

Jazz Pharmaceuticals’ management of the Xyrem (sodium oxybate) franchise provides a detailed case study in indication expansion executed with both regulatory precision and commercial sophistication.

Xyrem was originally approved for cataplexy in narcolepsy patients, an orphan indication that provided seven years of market exclusivity. Jazz pursued an additional indication for excessive daytime sleepiness in narcolepsy, which generated additional three-year exclusivity on that specific use. Jazz subsequently developed Xywav, a lower-sodium formulation of sodium oxybate for the same indications, filed as a 505(b)(2) and approved in 2020. The lower-sodium profile provided a clinical differentiation claim relevant to the cardiovascular risk profiles of the narcolepsy patient population.

The indication expansion strategy continued beyond narcolepsy. Jazz conducted clinical trials in idiopathic hypersomnia, a condition affecting a different but overlapping patient population, and obtained FDA approval for Xywav in idiopathic hypersomnia in 2021, the first drug approved for that condition [5]. The idiopathic hypersomnia indication carried orphan drug designation and seven years of orphan exclusivity, effectively extending the protected commercial period for the franchise well beyond what the original narcolepsy indication’s patents and exclusivities would have provided.

The Jazz/Xyrem case also illustrates the commercial and policy complications of LCE strategies. Xyrem’s classification as a Schedule III controlled substance, its REMS distribution restrictions, and its pricing generated Congressional scrutiny and antitrust litigation focused on the company’s agreements with potential generic and 505(b)(2) competitors. The FTC sued Jazz in 2023, alleging that its agreements with potential challengers constituted an anticompetitive scheme to maintain monopoly pricing [6]. The litigation does not invalidate the underlying regulatory strategy but serves as a reminder that LCE execution in high-profile, high-priced products invites antitrust scrutiny proportional to the commercial stakes.

Play Three: The Combination Product Strategy

Two Molecules, One New Protected Franchise

Combining an established molecule with a complementary agent in a single drug product is one of the most commercially productive LCE strategies available. Fixed-dose combinations offer genuine clinical convenience benefits when both components are genuinely complementary, reduce pill burden, may improve adherence, and can generate a new NDA or 505(b)(2) application with its own Orange Book-listed patents and data exclusivities, independent of the original components’ IP status.

The combination product strategy works particularly well in therapeutic categories where polypharmacy is common and where adherence to multi-drug regimens is a recognized clinical problem. Cardiovascular medicine, HIV treatment, diabetes management, and respiratory disease are the categories where fixed-dose combinations have generated the most significant commercial successes.

The regulatory pathway for most combination products is 505(b)(2). The applicant relies on the existing safety and efficacy data for each component while conducting bridging studies to support the combination and, where needed, clinical trials to establish efficacy of the combination. If both components are already approved, the FDA’s evidentiary requirements focus primarily on whether the combination is appropriate (no adverse interactions, no pharmacokinetic interference between components) and whether the fixed-dose ratio is clinically justified.

The IP Architecture of Fixed-Dose Combinations

Fixed-dose combination products generate patentable intellectual property at several levels. The combination itself, two specific molecules in a specific ratio or form, may be novel and non-obvious if the combination produces synergistic effects or unexpected clinical advantages over either component alone. The formulation technology required to combine the components in a single stable dosage form may generate separate formulation patents. Method-of-treatment patents covering administration of the combination for specific indications are Orange Book-listable.

The layering of combination patents on top of individual component patents creates multiple barriers to generic competition. A generic manufacturer seeking to market a copy of a fixed-dose combination must either demonstrate bioequivalence to the combination product (and navigate any bioequivalence challenges specific to the combination) or challenge each Orange Book-listed patent through Paragraph IV certifications. Patents covering the combination product cannot be circumvented by demonstrating that the individual components are bioequivalent to their individual references; the generic must show bioequivalence to the combination itself.

The combination strategy also defends against reference-listed drug substitution risks. When a fixed-dose combination is the only approved product containing the specific combination, pharmacists cannot substitute a generic for one component only. The substitution rules require therapeutic equivalence to the reference, which in this case is the combination product.

Case Study: AstraZeneca’s Symbicort and Respiratory Combinations

The respiratory inhaler category demonstrates how combination product strategy and formulation innovation can operate simultaneously to create durable franchise protection. AstraZeneca’s Symbicort, a combination of budesonide (an inhaled corticosteroid) and formoterol (a long-acting beta-agonist) in a metered-dose inhaler, represented a genuine advance over sequential administration of the two agents. The combination allowed a single inhaler device to deliver both components in fixed ratio, reducing device burden and potentially improving adherence in asthma and COPD patients.

The combination patent strategy for Symbicort covered the specific ratio of budesonide to formoterol, the formulation characteristics enabling co-delivery, and the delivery device technology. Each patent layer required separate Paragraph IV challenge from any ANDA applicant seeking to market a generic combination inhaler. The device technology patents, covering the Turbuhaler dry powder inhaler system in some markets and the pressurized metered-dose device in others, created an additional layer of IP protection beyond the pharmaceutical combination itself.

Generic inhalers face a particular challenge because the bioequivalence assessment for orally inhaled products is substantially more complex than for oral immediate-release products. The FDA requires demonstration of bioequivalence at both the systemic (PK-based) and local (lung deposition-based) levels, using a combination of pharmacokinetic studies and in vitro testing of aerodynamic particle size distribution. That complexity means ANDA applicants for respiratory combinations face higher development costs, longer review times, and more uncertain approval outcomes than standard oral generics [7]. The combination of pharmaceutical IP, device IP, and bioequivalence complexity creates a substantially higher barrier to generic entry than any single element alone.

The Antihypertensive Combination Template

The antihypertensive category has generated the most commercially prolific use of the combination product strategy, with pharmaceutical companies combining established agents in ways that provided clinical convenience and extended patent-protected revenue beyond what either component’s individual IP would have supported.

The ACE inhibitor/calcium channel blocker combinations, the ARB/diuretic combinations, and the triple-therapy combinations that followed all followed the same strategic logic: take two components whose individual use in hypertension management is well-established, develop a clinically rational fixed-dose combination, file a 505(b)(2) application relying on the individual components’ clinical databases, and generate combination patents that create a new exclusivity period for the combined product. When the individual component patents expire and generic monotherapy becomes available, prescribers who have shifted to the combination product face no immediately available generic combination substitute.

Novartis’s Exforge (amlodipine/valsartan), Daiichi Sankyo’s Azor (amlodipine/olmesartan), and the triple combination Tribenzor (amlodipine/olmesartan/hydrochlorothiazide) all executed this template with commercial success. Each combination generated Orange Book-listed patents that required separate challenge from ANDA applicants, even though each component was individually available as a generic. The strategic value of the combination was that it created a protected product category where none of the components’ expiring IP could be used to manufacture a direct generic substitute.

Play Four: Pediatric and Orphan Drug Repositioning

The Regulatory Exclusivity Strategies That Patent Law Cannot Block

Some of the most durable LCE strategies depend not on patents at all, but on statutory exclusivities that the FDA grants independently of any IP considerations. Pediatric exclusivity, orphan drug exclusivity, and the data exclusivities associated with new clinical investigations are granted by the FDA based on regulatory criteria, and they block generic entry regardless of patent status. A drug can be completely off-patent, with every composition and formulation patent expired, and still be protected from generic competition by a valid regulatory exclusivity.

This distinction matters in LCE planning because regulatory exclusivity is qualitatively different from patent protection in terms of how it can be challenged. ANDA applicants can file Paragraph IV certifications challenging patent validity or non-infringement, and they can win. They can design around narrow formulation patents. They can carve out patented indications from their labels. Regulatory exclusivity has no equivalent challenge mechanism: an ANDA applicant cannot argue that the FDA’s grant of three-year new clinical investigations exclusivity was incorrect. They can only wait for it to expire.

The strategic implications are clear. Pharmaceutical companies approaching the end of their primary patent protection should identify every regulatory exclusivity that remains available for their product and pursue those exclusivities as part of a coordinated LCE program. Missing a pediatric exclusivity opportunity because the company failed to engage with the FDA’s Written Request process is a recoverable mistake in year three of exclusivity but not in year seven.

Orphan Drug Designation: The Seven-Year Shield

Orphan drug designation under the Orphan Drug Act requires a disease affecting fewer than 200,000 U.S. patients and a plausible scientific rationale for the drug’s activity in that disease. It does not require that the drug be the only potential treatment; it does not require that the company have previously investigated the orphan application; and it does not require that the orphan indication have any relationship to the drug’s previously approved indications.

For LCE purposes, the key question is whether an approved molecule has mechanistic activity that could translate into clinical benefit for a qualifying rare disease population. Given the breadth of biological mechanisms involved in rare diseases, the answer is yes for a larger fraction of approved molecules than most pharmaceutical companies have systematically explored.

The commercial economics of orphan repositioning are particularly attractive when the small patient population supports premium pricing under orphan drug commercial conventions. Orphan drugs routinely achieve annual per-patient pricing in the range of $50,000 to $500,000 or more, reflecting the limited patient population, the clinical need, and the payer acceptance of premium pricing for rare disease treatments. For a molecule with established safety and a new orphan indication, the combination of seven-year exclusivity and orphan drug pricing creates revenue potential that can generate significant returns even from a relatively small patient population.

The regulatory pathway for orphan repositioning is almost always 505(b)(2). The existing safety database for the approved drug informs the orphan indication development program, often eliminating the need for a full Phase I safety program. The development investment concentrates in Phase II/III efficacy studies in the rare disease population. Total development costs for orphan repositioning programs typically run $30 million to $100 million, producing seven-year protected franchises in premium-priced categories.

Case Study: Thalidomide’s Extraordinary Repositioning

Thalidomide’s repositioning from one of medicine’s most notorious withdrawn drugs to an approved orphan oncology treatment is the most striking demonstration that regulatory exclusivity and clinical repositioning can transform a product’s commercial and scientific profile completely.

Thalidomide was withdrawn from most markets in the 1960s due to its severe teratogenic effects. Celgene (later acquired by Bristol-Myers Squibb) pursued clinical development of thalidomide for multiple myeloma and erythema nodosum leprosum (ENL), both orphan conditions. The FDA approved thalidomide for ENL in 1998 under a restricted distribution REMS program designed to prevent fetal exposure, and for multiple myeloma in 2006. Each orphan approval generated seven years of market exclusivity for the specific condition.

Celgene subsequently developed lenalidomide, a structural analog of thalidomide with improved efficacy and a modified safety profile, and pursued 505(b)(2) applications for multiple myeloma and other hematologic malignancies. Lenalidomide became Revlimid, which at peak generated over $12 billion in global annual revenue [8]. The thalidomide/lenalidomide franchise demonstrated that systematic chemical modification of a molecule with established biological activity in a rare disease, combined with rigorous orphan drug strategy, can generate pharmaceutical franchises worth tens of billions in market value from molecules that the original developer had abandoned.

The Celgene/Revlimid case also generated the most significant patent settlement scrutiny in recent pharmaceutical history, with multiple challenges to Celgene’s agreement with generic manufacturers that delayed lenalidomide generic entry. The FTC and private plaintiffs challenged those agreements as anticompetitive. Bristol-Myers Squibb, which acquired Celgene in 2019 for $74 billion, ultimately saw generic lenalidomide enter the U.S. market in 2022 when the settlement-delayed entry timeline expired [9]. The litigation outcome illustrates that even the most commercially successful orphan drug franchises attract sustained competitive and regulatory scrutiny when their pricing and exclusivity management generates market-wide cost implications.

Rare Pediatric Disease Designation and Priority Review Vouchers

The Rare Pediatric Disease (RPD) priority review voucher program creates an additional financial incentive for pursuing orphan drug strategies in pediatric rare diseases. A company that obtains approval for a treatment for a rare pediatric disease receives a priority review voucher that can be used to obtain six-month priority review for any subsequent FDA application, or sold to another company.

The market value of priority review vouchers has ranged from approximately $100 million to over $350 million, depending on market conditions and the regulatory calendar pressures facing potential buyers. For a company developing an LCE program around an orphan pediatric indication for an approved molecule, the RPD voucher represents a material financial asset in addition to the seven-year orphan exclusivity and the pediatric exclusivity extension.

The strategic value of the RPD pathway in LCE planning has been underexplored by most large pharmaceutical companies, which focus their rare pediatric programs on novel compounds rather than repositioning approved molecules. Smaller specialty pharmaceutical companies and biotechs have been more aggressive in identifying approved molecule repositioning opportunities in rare pediatric diseases, generating both orphan exclusivity and voucher value from clinical programs that leverage existing safety databases.

Play Five: The Authorized Generic and Managed Genericization Strategy

When You Cannot Stop Generic Entry, Control It

The four preceding strategies aim to extend the period of protected, premium-priced exclusivity. This fifth play acknowledges a reality that every pharmaceutical brand eventually faces: generic entry is coming, the composition patent will expire, and the formulation fortress, combination strategy, and indication expansions will delay but not permanently prevent genericization. The question then becomes not how to stop generic entry, but how to manage it in a way that preserves the maximum share of the market’s total value for the brand company.

The authorized generic is the primary instrument for managed genericization. An authorized generic is a copy of a brand drug product, using the brand’s approved NDA, that the brand company (or its authorized partner) launches in the generic market segment alongside or immediately after generic entry. Because it uses the brand’s NDA rather than a separate ANDA, it does not trigger the 30-month stay provisions and is not subject to the same Paragraph IV litigation risk. Because it is manufactured to brand specifications under the brand’s quality systems, it typically commands a modest premium over commodity generic prices.

The 180-Day Exclusivity Interaction

The authorized generic strategy has a specific and consequential interaction with the 180-day first-filer generic exclusivity. The statute grants 180 days of exclusivity to the first ANDA filer with a Paragraph IV certification, during which the FDA cannot approve any other ANDA for the same drug. The statute says nothing about authorized generics. An authorized generic launched by the brand company during the first-filer’s 180-day exclusivity period competes directly with the first-filer without any statutory bar, because it is not an ANDA.

The competitive effect of an authorized generic launch during 180-day exclusivity is substantial. Without an authorized generic, the first ANDA filer typically operates as a near-monopolist during the exclusivity period, capturing high market share at pricing that is discounted from the brand price but substantially above commodity generic levels. Industry data show that during 180-day exclusivity periods with an authorized generic present, the first-filer’s market share drops significantly and its pricing power is materially reduced [10]. Generic companies have challenged authorized generic practices on antitrust grounds, arguing that a brand company’s decision to launch an authorized generic is anticompetitive when made in response to a Paragraph IV challenge. Those challenges have been largely unsuccessful in court, but the policy debate continues.

For brand companies, the decision to launch an authorized generic involves balancing internal revenue capture against the deterrence effect on future Paragraph IV filers. If generic companies anticipate that every Paragraph IV challenge will be met with an authorized generic that eliminates the economic case for 180-day exclusivity, they may be less willing to file Paragraph IV certifications in the first place, reducing the competitive pressure on the brand. That deterrence logic argues for a consistent policy of authorized generic launches that is known to the market, not a case-by-case decision.

Licensing Strategies and the Controlled Entry Framework

The managed genericization strategy extends beyond authorized generics to structured licensing arrangements with select generic manufacturers. A brand company approaching the end of exclusivity can negotiate licenses with one or two generic manufacturers, granting them rights to market generic versions of the product in exchange for royalties. The license grants controlled entry, preserving the brand company’s participation in the generic revenue stream while potentially limiting the number of generic competitors below what an unconstrained market entry would produce.

Controlled entry licensing strategies require careful antitrust structuring. Agreements that effectively limit generic competition by reducing the number of market entrants can attract FTC scrutiny under pay-for-delay or market allocation theories, even when structured as royalty-bearing licenses rather than payment-for-delay arrangements. The key legal test under FTC v. Actavis is whether the agreement includes a large, unjustified payment from the brand to the generic; a royalty-bearing license where the generic pays the brand does not trigger that test in the same way, but can still attract scrutiny if the effect is to restrict competition materially.

The most defensible controlled entry licenses are those structured around genuine IP rights, where the generic company is paying a royalty for use of a valid patent that the generic would need to design around or challenge absent the license. A royalty-bearing license on a formulation patent that the generic company genuinely needed for its product is a straightforward commercial arrangement. A license designed to delay generic entry in exchange for a payment structured to appear as a royalty will face FTC analysis that looks through the structure to the economic effect.

Case Study: Pfizer’s Lipitor Strategy

Pfizer’s management of the Lipitor (atorvastatin) franchise through the period of generic entry demonstrates both the commercial scale of managed genericization and the importance of early LCE preparation.

Lipitor was the world’s best-selling drug, generating approximately $13 billion in global sales and $5 billion in U.S. sales in its peak year. The primary composition-of-matter patent expired in November 2011, and Teva Pharmaceutical received 180-day first-filer exclusivity for generic atorvastatin. Pfizer launched an authorized generic version of Lipitor on the same day as Teva’s generic entry, limiting Teva’s near-monopolist pricing power during the exclusivity period.

Pfizer’s LCE strategy for Lipitor also included developing and launching Liptruzet (atorvastatin/ezetimibe combination) as a new 505(b)(2) product, attempting to capture patients requiring combination statin/cholesterol absorption inhibitor therapy in a single formulation. The commercial success of that combination was limited by the availability of Vytorin (simvastatin/ezetimibe) from Merck, but the strategy demonstrated the combination product approach in a commodity statin environment [11].

The Lipitor generic entry is the benchmark case for measuring the revenue cliff that managed genericization aims to soften. Pfizer’s global atorvastatin revenues fell from approximately $9.6 billion in 2011 to $3.9 billion in 2012, a decline of nearly 60% in a single year [12]. The authorized generic captured some of that revenue loss, but the primary lesson from Lipitor is that no amount of managed genericization can fully offset the revenue impact when a patent expires on a drug generating that level of sales. Early LCE investment, executed years before expiry, is what determines whether the franchise survives the cliff with meaningful revenue or enters a terminal decline.

Part Six: The Patent Intelligence Infrastructure

Building the Data Capabilities That Make LCE Strategies Work

Every LCE strategy depends on a precise understanding of the patent and exclusivity landscape. The formulation fortress requires knowing exactly which patents are already listed in the Orange Book and when they expire, so the new formulation patent program can be designed to extend beyond them. Indication expansion requires knowing whether method-of-treatment patents are available for new uses and whether existing patents on the original indication will support the listing requirements. Combination product strategy requires mapping the IP of both components before committing to development. Orphan repositioning requires assessing freedom to operate in the orphan indication space. Managed genericization requires tracking the Paragraph IV filing activity that signals imminent generic competition.

The Orange Book provides the foundational data: patent listings, expiry dates, use codes for method-of-treatment patents, and exclusivity periods. But the Orange Book alone is insufficient for serious LCE planning. The database shows nominal patent expiry dates but does not reflect patent term adjustments, patent term extensions under 35 U.S.C. § 156, or the litigation status of patents currently being challenged. It does not show pending ANDA applications, the names of applicants who have filed Paragraph IV certifications, or the specific grounds being argued in current patent litigation.

DrugPatentWatch addresses those gaps by aggregating Orange Book data with USPTO patent records, FDA ANDA filing data, Paragraph IV certification records, and court docket information into a unified intelligence platform. For LCE planning purposes, the platform allows a company to see the full competitive picture: which ANDAs have been filed against any of their Orange Book-listed patents, which applicants are in the queue, whether any 30-month stays are currently running, and what the litigation history suggests about the vulnerability of specific patents. That synthesis of FDA, USPTO, and court data into a single queryable system represents the kind of intelligence infrastructure that serious LCE planning requires.

The Patent Expiry Calendar as a Strategic Asset

Systematic LCE planning begins with a patent expiry calendar that covers not just the company’s own products but the competitive landscape for molecules in their therapeutic focus areas. Every blockbuster approaching patent expiry is a potential LCE opportunity for competitors as well as a defensive planning requirement for the brand holder. Understanding when competitors’ molecules will enter generic competition, and what combination or reformulation opportunities those molecules present, is as important as defending your own franchise.

A rolling five-year patent expiry calendar, updated continuously with new Orange Book listings, litigation outcomes, and regulatory exclusivity changes, is the foundational tool for pharmaceutical business development. Companies that build and maintain this calendar, using platforms like DrugPatentWatch to ensure completeness and accuracy, identify business development and in-licensing opportunities earlier than competitors who rely on ad hoc research.

The calendar has specific tactical uses in Paragraph IV litigation. When a brand company receives a Paragraph IV notice letter, they have 45 days to file suit to trigger the 30-month stay. That decision requires knowing not just whether the suit is winnable, but what the strategic value of the 30-month delay is relative to the cost of litigation. A product generating $1 billion per year where a 30-month stay preserves $2.5 billion in revenue warrants more aggressive litigation investment than one generating $100 million per year. Making that calculation quickly and accurately depends on having current patent and market data integrated and accessible.

Monitoring Competitor ANDA and 505(b)(2) Filings

The FDA publishes information on pending ANDA and 505(b)(2) applications through its various databases, and Paragraph IV certifications generate public filing records when litigation is initiated. But the most actionable intelligence often comes from tracking the full pattern of competitor activity across multiple products simultaneously, not just monitoring notifications for a single drug.

A generic company that files Paragraph IV certifications across a brand company’s entire portfolio is signaling more than individual product challenges. It is revealing its technical capabilities, its litigation appetite, and potentially its commercial strategy for the category. A specialty pharmaceutical company filing multiple 505(b)(2) applications for new formulations in a therapeutic category is advertising its investment priorities and potentially competing for the same reformulation opportunities the brand company itself is pursuing.

Competitive intelligence on ANDA and 505(b)(2) filing activity is valuable for prioritizing patent prosecution investment. If multiple ANDA filers are already in the queue for a product, the brand company’s patent prosecution team should be reviewing Orange Book listings for any additional formulation or method-of-use patents that could be listed, and should be evaluating whether patent prosecution in related areas could generate claims that would be infringed by likely generic formulations.

Part Seven: The Regulatory Execution Framework

FDA Engagement Strategies That Determine LCE Success

LCE programs are not purely legal and commercial exercises. They depend on FDA approval of new applications, and the quality of a company’s FDA relationship, the depth of its regulatory expertise, and the design of its clinical programs determine whether those approvals come on the first submission or after costly deficiency cycles.

The most important single pre-submission activity for any LCE application, whether a 505(b)(2) for a new formulation, a new indication filing, or a combination product application, is a Type B meeting with the relevant FDA review division. These meetings, requested and held before the NDA is filed, allow the company to confirm the data package required for approval. The cost of a Type B meeting is several months of preparation time and regulatory consulting fees. The cost of a Complete Response Letter requiring additional Phase III clinical trials is typically $20 million to $100 million and 12 to 24 months of delay. The arithmetic argues for exhaustive pre-submission engagement in every case.

For orphan drug programs, the FDA’s Office of Orphan Products Development is a separate engagement channel. OOPD reviews orphan drug designation requests, which can be filed before any clinical work begins, and provides guidance on clinical development programs for rare disease indications. Early designation not only locks in the exclusivity claim but signals to payers and investors that the program has regulatory substance. Companies that file for orphan designation early in development, rather than waiting until a clinical program is substantially complete, gain both the designation’s commercial signaling value and the procedural advantages that come with FDA familiarity before the NDA review begins.

The PDUFA Priority Review Decision

Priority review designation, granted to drugs that address serious conditions and offer a potential improvement over available therapy, accelerates FDA review from 12 months to 6 months. For LCE programs with significant commercial timelines, the 6-month difference in review time can be material. A formulation or indication that would generate $150 million in quarterly revenue enters the market two quarters earlier with priority review, representing $300 million in additional revenue that would otherwise be lost to a slower standard review.

Priority review eligibility for LCE programs requires meeting the “serious condition” threshold and demonstrating clinical improvement. A new formulation that reduces pill burden for a seriously ill patient population, a new indication in a disease with inadequate existing therapies, or a combination product that eliminates drug-drug interactions with safety implications can qualify. The FDA’s guidance on priority review criteria makes clear that marginal improvements in convenience for well-managed conditions will not qualify, but genuine clinical advances in serious diseases can.

The Breakthrough Therapy designation, available for drugs targeting serious conditions where preliminary clinical evidence indicates substantial improvement over available therapy, offers even more intensive FDA engagement than standard priority review. Breakthrough designation is available for LCE applications where the new indication targets a serious disease and the early clinical data are compelling. The designation provides frequent FDA interaction during development, rolling review of application sections as they are completed, and intensive guidance to maximize the efficiency of the development program. Several 505(b)(2) applications for new indications of approved molecules have received Breakthrough designation, particularly in oncology and rare disease categories.

REMS as Both Barrier and Opportunity

A Risk Evaluation and Mitigation Strategy (REMS) required by the FDA for a product with significant safety risks can function as both a regulatory burden and a competitive barrier. The brand company managing an approved REMS program controls access to the proprietary safety information, patient monitoring protocols, and distribution systems that the REMS requires. Generic applicants seeking to reference the brand’s REMS program for their own ANDA must either demonstrate that their product shares the REMS or develop an equivalent system.

Brand companies have used REMS programs as barriers to generic entry in several cases, most notably in the context of shared REMS requirements. The FDA’s position is that brand companies must share REMS systems with generic applicants on commercially reasonable terms, and the agency has issued guidance emphasizing that REMS programs cannot be used to foreclose generic entry. Despite that guidance, REMS-based delays in generic access have been documented and have attracted FTC enforcement attention.

For LCE purposes, the most legitimate use of a REMS is in support of a new, genuinely dangerous formulation or indication where safety monitoring adds clinical value. A 505(b)(2) application for an abuse-deterrent formulation with a REMS covering prescription drug monitoring program reporting, a new indication with a serious teratogenic or hepatotoxic risk requiring monitoring, or a combination product with drug interaction risks requiring baseline testing can build REMS requirements into the product profile that are clinically justified and that create genuine competitive differentiation for the brand versus a stripped-down generic substitute.

Part Eight: The Financial Architecture of LCE

Modeling the Value of Each Strategic Play

The financial case for LCE investment cannot be made in the abstract. It requires product-specific analysis of expected revenue under an LCE scenario versus a base case of unmanaged genericization. The key variables in that model are current product revenues, revenue trajectory under the base case, timing and cost of LCE development programs, probability of approval for each program, incremental exclusivity duration generated by each strategy, and the competitive response to each initiative.

The model structure for a formulation extension starts with the new formulation’s development cost (typically $20 million to $80 million), the probability of regulatory approval (typically 70% to 85% for straightforward extended-release reformulations of established molecules), the timeline from program initiation to launch, and the expected market adoption rate for the new formulation. The incremental value is the revenue generated during the new formulation’s exclusivity period that would not otherwise be earned, discounted for the probability of failure and time value of capital.

A pharmaceutical company with a product generating $1.5 billion in annual U.S. revenues and a composition patent expiring in four years faces a different financial calculus than one with two years of remaining exclusivity. With four years, a well-executed formulation program can be completed and launched, a new indication program can be initiated (though may not complete before composition expiry), and a pediatric exclusivity program can almost certainly be executed. With two years, only the fastest development programs are viable, and the financial model needs to be more conservative about what can realistically be accomplished.

For indication expansion programs, the model incorporates the expected revenue from the new indication as a separate revenue stream, with its own exclusivity period and pricing dynamics. A new orphan indication generating $50 million in annual revenues under seven-year orphan exclusivity has a present value of approximately $250 million to $300 million at typical pharmaceutical discount rates, net of development costs. For a product at risk of losing $1.5 billion in branded revenues to generic competition, that incremental orphan franchise is meaningful but not transformative on its own. In combination with a formulation extension and pediatric exclusivity, the total LCE value can approach $500 million to $700 million in incremental franchise value, which is significant when measured against total development investment of perhaps $100 million to $150 million.

The Capital Allocation Competition

LCE programs compete for capital with novel drug development programs in every large pharmaceutical company’s budget process. The argument for novel drugs is straightforward: successful novel drugs generate larger peak revenues than LCE programs and create entirely new therapeutic franchises. The argument for LCE is equally straightforward: LCE programs have lower development costs, shorter development timelines, higher probability of regulatory approval, and predictable revenue bases because they leverage existing products with established markets.

The historical data on capital allocation between novel and LCE programs shows that pharmaceutical companies chronically underinvest in LCE relative to the risk-adjusted return differential. The probability of a novel drug succeeding from Phase I to approval is approximately 12% to 14%, with typical Phase I-to-approval timelines of 10 to 15 years and total development costs of $500 million to $2 billion [13]. The probability of a well-designed 505(b)(2) formulation extension succeeding is 70% to 85%, with development timelines of 3 to 6 years and development costs of $20 million to $80 million.

On a risk-adjusted basis, LCE programs generate returns that compare favorably with novel drug development across most therapeutic categories. The persistent underinvestment in LCE reflects a combination of scientific bias toward novel biology, commercial bias toward large peak-sales potential rather than probability-weighted expected value, and organizational dynamics in large pharmaceutical companies that reward novel drug pipeline programs with more visibility and career advancement than LCE management.

The companies that have built systematic LCE capabilities, including Jazz Pharmaceuticals, Supernus Pharmaceuticals, Teva’s specialty division before its debt crisis, and Assertio Therapeutics, have generally delivered better risk-adjusted returns from their development investment than large pharmaceutical companies managing LCE reactively. The competitive advantage of building LCE as an institutional capability rather than an episodic defensive reaction is captured in the consistency of the development pipeline and the predictability of the resulting exclusivity cash flows.

The Cost of LCE Failure

The financial model for LCE needs to account not just for the value of successful programs but for the cost of inadequate LCE execution. When a brand company fails to execute a formulation fortress and is left with only the original composition-of-matter patent expiring with no successor products in the market, the revenue cliff is steep and the recovery is slow. The brand drug typically loses 80% to 90% of prescription volume within 12 months of generic entry [14]. The brand maintains a residual share among patients who prefer the original product for reasons of familiarity, perceived quality, or formulary placement, but that residual share typically represents 5% to 15% of the original volume at brand pricing.

The aggregate revenue impact of inadequate LCE planning is captured in what the industry calls the “patent cliff,” the period of accelerated revenue decline when multiple large products lose exclusivity simultaneously without adequate replacement. The industry-wide patent cliff of 2011 to 2015 generated estimated global revenue losses of over $200 billion as drugs including Lipitor, Plavix, Seroquel, Actos, and others lost exclusivity within a short period [15]. Companies that had invested in LCE programs for some of those products, and had filled their development pipelines with successor products, navigated that period with acceptable financial outcomes. Companies that had relied on the original products’ revenue without investing in successors faced the full impact of the cliff.

Part Nine: Antitrust Boundaries

Where LCE Strategy Ends and Anticompetitive Conduct Begins

LCE strategies operate within a legal framework that the FTC and Department of Justice monitor actively. The line between legitimate IP management and anticompetitive exclusionary conduct is not always bright, and pharmaceutical companies have crossed it in ways that generated substantial enforcement action, litigation exposure, and in some cases, criminal liability.

The primary antitrust risk areas for LCE strategies are reverse payment settlements (where a brand pays a generic to delay entry), product hops combined with hard withdrawal of original products (where the brand forces migration by eliminating the generic reference), REMS manipulation (where the brand denies generic access to the safety system required for generic development), and sham citizen petitions (where the brand files petitions with the FDA not to raise legitimate safety concerns but to delay generic approval).

Reverse payment settlements, sometimes called pay-for-delay, attracted the most significant legal attention in the decade following FTC v. Actavis. The Supreme Court’s 2013 ruling that reverse payment settlements are subject to antitrust rule-of-reason analysis rather than per se legality created a framework in which large, unexplained payments from brand to generic in connection with patent settlements are presumptively anticompetitive. Several major settlements, including those involving AndroGel (testosterone gel), Nexium (esomeprazole), and Lamictal (lamotrigine), were challenged under Actavis, generating significant litigation and in some cases substantial settlements or adverse judgments [16].

The product hop cases, including the Namenda litigation discussed earlier, established that hard withdrawal of an original product to force migration to a protected successor is actionable monopolization under Section 2 of the Sherman Act when it has no legitimate business justification other than forestalling generic competition. Soft transitions, where the brand continues selling the original product while promoting the successor, are generally defensible.

For companies building LCE programs, the antitrust compliance framework needs to be integrated into the strategy design from the beginning, not applied as a review layer after the strategy is set. Each element of an LCE program should have a documented clinical or business rationale that is independent of its competitive effect on generic entry. The formulation improvement should have genuine clinical utility. The pediatric program should serve genuine pediatric patient needs. The combination product should offer genuine clinical convenience beyond what sequential monotherapy provides. Where those clinical rationales exist and are documented contemporaneously, the LCE strategy is defensible. Where they appear to be pretextual, the antitrust exposure is real.

Part Ten: Building Organizational LCE Capability

The Internal Structure That Makes LCE Happen

The most sophisticated LCE strategies fail when the organizational capability to execute them does not exist. LCE requires coordination across patent prosecution, regulatory affairs, clinical development, medical affairs, commercial, and government affairs functions in ways that most pharmaceutical organizational structures are not designed to support efficiently.

The core organizational requirement is a cross-functional LCE team with direct access to senior leadership and a mandate that spans both the defensive (protecting existing products) and offensive (building new exclusivities) dimensions of lifecycle management. Companies that assign LCE responsibility to a regulatory affairs team operating in isolation from commercial strategy, or to a commercial team operating without patent prosecution input, consistently underperform relative to their portfolio’s potential.

The timing requirement for LCE initiation is the most common failure point. Companies that begin LCE planning when a product is already three to four years from patent expiry are generally too late to execute a full formulation fortress strategy, may be too late to initiate the clinical programs required for new indication exclusivities, and may find that competitive 505(b)(2) filers have already staked claims to the most obvious formulation opportunities. LCE planning for a product with five to ten years of remaining exclusivity is not premature; it is the operational requirement for comprehensive franchise protection.

The organizational roles that matter most are the patent counsel coordinating Orange Book listing strategy, the regulatory strategist responsible for FDA engagement planning, the clinical development lead identifying the data programs required for new exclusivities, and the commercial strategist who connects the clinical differentiation story to the market execution plan. Those four roles need to be coordinated through a governance structure that makes clear who owns the LCE program and how decisions are made when the commercial calendar and the development timeline create tradeoffs.

The Make vs. Partner Decision

Many pharmaceutical companies, particularly those without fully integrated formulation and clinical development capabilities, execute LCE programs through partnerships. A branded pharmaceutical company with a high-revenue product and approaching patent expiry can partner with a contract development organization for formulation work, with a clinical research organization for clinical studies, and with a specialty pharmaceutical partner for commercial execution of a new indication in a therapeutic category outside its core expertise.

The partnership model accelerates LCE development by accessing specialized capabilities without building them in-house, but introduces coordination complexity and requires careful IP structuring to ensure that the brand company retains appropriate rights to the resulting products and patents. Partnership agreements for LCE programs need to address patent ownership (any formulation innovation generated by the CDMO partner should revert to the brand company or be jointly owned with clear licensing terms), data rights (all clinical data generated in the program should be owned by or licensed to the NDA holder), and exclusivity (the partnership should not create obligations that prevent the brand company from managing its own product’s competitive environment).

In-licensing LCE opportunities is an increasingly common strategy for companies that want to build specialty franchises without full development programs. A company can acquire rights to a 505(b)(2) program that a smaller developer has already completed, paying a development premium in exchange for receiving an FDA-approved product with an established patent portfolio and exclusivity profile. That approach compresses the time from investment to commercial launch but requires disciplined valuation of the acquired asset, including thorough patent due diligence on the Orange Book listings, litigation status, and exclusivity duration.

Key Takeaways

Pharmaceutical life cycle extension is a capital allocation discipline, not a legal formality. The five strategies covered here, formulation fortresses, indication expansion, combination products, orphan and pediatric repositioning, and managed genericization, all require investment, organizational capability, and execution discipline years before the patent cliff arrives. Companies that treat LCE as a last-minute defensive measure absorb the full revenue impact of generic entry. Companies that build LCE as an institutional capability consistently generate incremental franchise value that exceeds their development investment on a risk-adjusted basis.

The formulation fortress is the most widely applicable LCE strategy, but its commercial success depends entirely on genuine clinical differentiation and patient migration. A reformulated product that payers and prescribers do not prefer will not maintain brand pricing against generic substitution, regardless of how well the patent portfolio is constructed. Clinical utility is not optional; it is the foundation of the commercial model.

Regulatory exclusivity, particularly orphan drug and pediatric exclusivity, provides protections that no patent challenge can overcome. These exclusivities are underutilized by large pharmaceutical companies relative to their financial returns. A systematic review of every approved molecule in a company’s portfolio for orphan indication potential and pediatric Written Request eligibility is a standard component of LCE planning, not an exceptional opportunity.

Patent intelligence is the operational foundation for all five strategies. Understanding exactly which patents protect your product, when they expire, which competitors have filed Paragraph IV certifications, and what the litigation history suggests about patent vulnerability requires the kind of integrated FDA and USPTO data that platforms like DrugPatentWatch provide. LCE planning that relies on static Orange Book reviews conducted annually will miss the real-time competitive signals that determine whether a Paragraph IV challenge requires immediate litigation response or can be managed through settlement discussions.

The antitrust boundaries on LCE strategy are real and actively enforced. Every element of an LCE program should have a documented clinical or business rationale that is independent of its competitive effect on generic entry. The line between legitimate franchise management and anticompetitive exclusionary conduct is tested by the quality of that rationale, and courts will examine it carefully.

The financial case for early, systematic LCE investment is compelling when measured against the alternative. A patent cliff without a succession plan is a company-defining event for any pharmaceutical business whose revenues concentrate in a blockbuster franchise. The tools to manage it are available, the regulatory framework supports it, and the companies that execute it consistently demonstrate that the investment earns returns.

FAQ

Q1: At what point in a drug’s lifecycle should a company begin LCE planning, and what are the specific triggers that indicate planning has started too late?

A. LCE planning should begin no later than five years before primary composition-of-matter patent expiry, and for large franchises, the ideal initiation point is seven to ten years out. The reason for that timeline is that each LCE strategy has a minimum development and regulatory review period. A formulation fortress program takes three to five years from initiation to approval and commercial launch. A new indication clinical program takes three to six years depending on indication complexity. A pediatric program requires time to engage the FDA on a Written Request, conduct the studies, and submit the results, typically two to four years total. Planning that begins three years before composition patent expiry is too late for most substantive LCE programs; it leaves only managed genericization and authorized generic strategies as viable options. The operational trigger for beginning LCE planning should be set internally at five years before primary patent expiry for all products with annual revenues exceeding a defined threshold, typically $300 million or more for large pharmaceutical companies.

Q2: How should a pharmaceutical company evaluate whether a potential new indication for an approved drug is financially viable for LCE purposes, considering the cost of clinical development against the expected exclusivity value?

A. The evaluation framework has four components that must all be positive for a new indication LCE program to be financially justified. First, the indication must be of sufficient size and value to generate revenue that exceeds development cost within the exclusivity period, discounted for development risk. A primary care indication affecting millions of patients at generic pricing generates different economics than an orphan indication affecting 10,000 patients at $200,000 per patient per year. Second, the exclusivity available must be sufficient to generate a return. Three-year new clinical investigations exclusivity for a large primary care indication in a commodity category will likely be insufficient; seven-year orphan exclusivity for a rare disease is typically sufficient. Third, the indication must be defensible from generic carve-out, either through method-of-treatment patents with broad claims or through the nature of the disease and labeling. Fourth, the company must have or be able to build the commercial capability to market in the new indication category. A cardiovascular company pursuing a CNS orphan indication needs either internal CNS commercial capability or a partnership to commercialize the product. Running the model with realistic assumptions about market penetration, pricing, development costs, and discount rates will identify programs with positive expected value and those that look attractive until the numbers are examined.

Q3: What are the most common formulation fortress patent vulnerabilities that generic companies successfully exploit in Paragraph IV litigation, and how should brand companies design their formulation IP to minimize those vulnerabilities?

A. The most common successful attacks on formulation patents fall into four categories. Obviousness based on prior art formulation technologies is the most frequent: if the specific polymer system, release mechanism, or delivery technology in the patent was already described in the scientific or patent literature at the time of filing, the formulation patent is vulnerable to obviousness attack regardless of whether the specific application to the brand drug was novel. Companies should conduct thorough prior art searches before drafting formulation patent claims and should draft claims that focus on the specific technical result achieved rather than the general technique used. Written description and enablement challenges succeed when the patent claims a broader range of formulations than the inventor actually made and tested; the specification must provide sufficient detail to enable a skilled formulator to reproduce the claimed invention across the full claimed range. Non-infringement arguments succeed when the generic manufacturer’s formulation differs from the brand’s in a way that avoids the specific claim language; companies should draft claims with functional language covering what the formulation achieves, not just structural language describing what it contains, to make design-arounds more difficult. Finally, double-patenting rejections during prosecution, and corresponding obviousness-type double-patenting invalidity arguments in litigation, can threaten formulation patents that too closely resemble the composition-of-matter patent. Filing terminal disclaimers to address double-patenting during prosecution is the standard solution, but it ties the formulation patent’s expiry to the composition patent’s expiry, reducing the extension benefit.

Q4: How does the FDA evaluate whether a 505(b)(2) LCE product offers sufficient clinical differentiation to support priority review designation, and what level of clinical evidence is typically required to meet that threshold?

A. Priority review designation under PDUFA requires that the drug, compared to available therapy, “may provide a therapy where none exists or may be superior to available therapy in one or more of the following ways”: greater effectiveness, elimination or substantial reduction of a treatment-limiting adverse effect, or documented enhancement of patient compliance expected to lead to an improvement in serious outcomes. For LCE programs, the differentiation claim must be clinically substantiated, not merely theoretical. An extended-release formulation claiming priority review on the basis of improved adherence needs preliminary clinical or epidemiological data showing that adherence to the immediate-release formulation is a documented clinical problem, that the once-daily dosing profile would plausibly improve adherence in the target population, and that improved adherence translates into improved clinical outcomes in serious disease contexts. An abuse-deterrent formulation claiming priority review in a high-abuse-potential opioid context needs epidemiological data on the scale of misuse of the immediate-release formulation and evidence that the abuse-deterrent mechanism addresses the primary routes of misuse. The FDA’s priority review designation decisions are not publicly reasoned in detail, so companies assessing eligibility should engage with the relevant review division through pre-submission meetings to get the agency’s preliminary view before committing to the priority review request in the NDA cover letter.

Q5: What practical steps should a pharmaceutical company take when it receives its first Paragraph IV certification notice letter against an LCE product’s Orange Book-listed patents, and how does that process differ from receiving a notice letter against the original product’s patents?

A. The first step on receiving a Paragraph IV notice letter is to confirm the date of receipt precisely, because the 45-day clock for filing suit to trigger the 30-month automatic stay begins running from receipt, not from the date of the notice letter. The legal team should immediately secure that date with documented evidence and calendar the 45-day deadline with internal alerts. The second step is to analyze the notice letter’s detailed statement of the bases for invalidity or non-infringement, which the statute requires the applicant to provide. That detailed statement reveals the generic company’s legal theory, their formulation approach (to the extent it is revealed by their non-infringement arguments), and the specific prior art they are relying on for invalidity contentions. For an LCE formulation patent, the analysis differs from a composition-of-matter patent challenge primarily in that the technical facts are different: the relevant prior art is formulation science rather than synthetic chemistry, the non-infringement arguments typically focus on differences in polymer composition or structural features of the formulation rather than molecular structure, and the claim construction questions that will drive litigation outcomes center on formulation terminology rather than chemical terminology. The brand company should immediately engage IP litigation counsel with expertise in formulation patent cases (a specific subspecialty of pharmaceutical patent litigation) and should brief that counsel on the formulation development history, the prosecution history of the challenged patent, and any prior litigation involving the same patent or patent family. The decision to sue, which must be made within 45 days, should be driven by a rapid but thorough assessment of the patent’s strength on the specific grounds raised in the notice letter, not by the commercial value of the 30-month stay alone.

Sources

[1] New York v. Actavis, PLC, 787 F.3d 638 (2d Cir. 2015).

[3] U.S. Food and Drug Administration. (2013). FDA approves abuse-deterrent labeling for reformulated OxyContin. FDA News Release. https://www.fda.gov/news-events/press-announcements/fda-approves-abuse-deterrent-labeling-reformulated-oxycontin

[4] GlaxoSmithKline LLC v. Teva Pharmaceuticals USA, Inc., 7 F.4th 1320 (Fed. Cir. 2021).

[5] Jazz Pharmaceuticals PLC. (2021). FDA Approves Xywav (calcium, magnesium, potassium, and sodium oxybates) for Idiopathic Hypersomnia in Adults. Jazz Pharmaceuticals Press Release. https://www.jazzpharma.com/press-releases

[6] Federal Trade Commission. (2023). FTC Sues Jazz Pharmaceuticals for Illegally Blocking Competition to Billion-Dollar Sleep Drug. FTC Press Release. https://www.ftc.gov/news-events/news/press-releases/2023/01/ftc-sues-jazz-pharmaceuticals

[7] U.S. Food and Drug Administration, Office of Generic Drugs. (2022). Product-Specific Guidance for Budesonide; Formoterol Fumarate Dihydrate Inhalation Aerosol. FDA. https://www.fda.gov/drugs/guidances-drugs/product-specific-guidances-orally-inhaled-and-nasal-drug-products

[9] In re Revlimid (Lenalidomide) Antitrust Litigation, Case No. 3:19-md-02979 (D.N.J. 2019-2022).

[10] Hollis, A. (2003). The importance of being first: Evidence from Canadian generic drug markets. Health Economics, 12(9), 723-734. https://doi.org/10.1002/hec.805