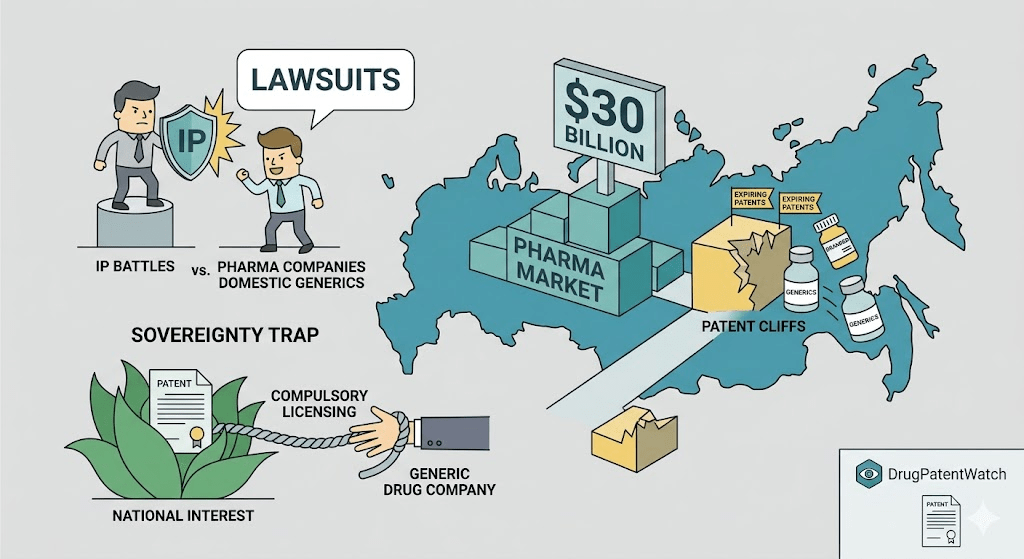

The Russian pharmaceutical market generated 2.85 trillion roubles in 2024 — but every dollar of that growth evaporated in currency translation. In US terms, the market held flat at $30.9 billion. In euros, it contracted. What looks like a 10% growth story in local currency is, for any company repatriating profits, a zero-growth market with rising operational risk. That structural tension between rouble-denominated scale and hard-currency reality defines every IP, licensing, procurement, and market-entry decision in this sector.

This analysis covers the full stack: patent term extension mechanics at Rospatent, the Osimertinib FAS dispute and what it means for IP enforcement strategy, the Pharma 2030 targets that are actively reshaping procurement rules, data exclusivity case law that flipped twice in eight years, biosimilar competition from BIOCAD and R-Pharm, API dependency risk, and the EAEU regulatory pathway that now governs all new drug registrations across five countries.

Why Russia’s Pharma Market Is Structurally Different From Every Other Emerging Market

Most emerging pharmaceutical markets reward a simple playbook: register the drug, price above local generics, find a distributor, grow volume. Russia does not work that way. The state is not a background regulator here — it controls roughly 33% of drug purchasing directly through state procurement programs, sets preferred supplier lists that exclude non-localized foreign companies by rule, and has an explicit government strategy (Pharma 2030) that targets 70% domestic market share by value.

That combination of state procurement power and industrial policy creates a market where IP rights, localization decisions, and regulatory positioning are inseparable commercial variables. A patent that would generate seven years of exclusivity in Germany may generate three in Russia if a domestic manufacturer files a parallel application, challenges the data exclusivity period, or receives a compulsory license referral. Understanding that risk is not optional for any licensing deal, royalty structure, or market-entry valuation.

From Soviet Command Economy to State Capitalism: Why Pharma 2030 Was Inevitable

How the Soviet Drug Industry’s Collapse Explains Every Modern Protectionist Policy

The Soviet pharmaceutical system nationalized all production after 1917 and built a network of state research institutes — the Gamaleya Institute being the best-known — designed around supply security rather than commercial efficiency. By the 1980s, the system produced adequate volumes of essential medicines but was structurally incapable of innovation. Quality control was inconsistent, API production lagged Western standards, and the incentive structure rewarded volume over efficacy.

When the Soviet Union dissolved in 1991, the domestic industry went with it. Russian “shock therapy” opened the market to foreign imports. By the late 1990s, imported drugs accounted for 75-80% of the market in value. Active Pharmaceutical Ingredient (API) production collapsed by roughly 80% between 1991 and 1999 — a figure that still drives policy today. The policymakers running Pharma 2030 came of age watching that collapse. Their response is not economic nationalism for its own sake; it is a direct attempt to prevent a repeat.

What Pharma 2020 Actually Achieved — and Where It Fell Short

Pharma 2020, Russia’s first post-Soviet industrial strategy for the sector, aimed to bring 90% of the Vital and Essential Drug List (EDL) into domestic production and raise the local market share to 75% in value by 2020. Those targets were not met. The Russian Association of International Pharmaceutical Manufacturers (AIMP) estimated foreign companies invested approximately 1 trillion roubles (around $17 billion at the time) in localization projects over the decade following Pharma 2020’s launch.

What actually shifted was the commercial model for multinational corporations. Importation became progressively harder to defend against the “Third Wheel” procurement rule, which automatically disqualifies foreign bids when two or more EAEU-based competitors have submitted offers. Companies that refused to localize found themselves excluded from the state segment entirely.

The Two Competing Visions Inside Pharma 2030

Pharma 2030, approved as the successor strategy, contains an internal contradiction that matters for market forecasting. One set of documents targets a domestic market share of 43% in value by 2030 — essentially a generics substitution goal. A competing set targets 70%, which would require Russia to produce not just copies of off-patent drugs but competitive biologics, biosimilars, and eventually original innovative compounds.

Andrey Ivashchenko at the ChemRar High Tech Center has publicly called the 43% target “outdated,” arguing it locks Russia into a generic factory model that will never generate the export revenue or innovation capacity the strategy claims to seek. His argument is commercially important for foreign companies: a generic factory model maximizes price competition and procurement exclusion, while an innovation hub model requires technology transfer partnerships, R&D collaboration, and a more functional IP environment.

The outcome of that internal debate will determine whether Russia is a market where foreign IP generates licensing royalties or one where it gets replicated under preferential rules.

The Market’s Dual Structure: Commercial Retail vs. State Procurement

How the 13.8% Commercial Growth Rate Misleads Multinational Revenue Forecasts

The commercial pharmacy segment grew to 1.635 trillion roubles in 2024, up 13.8% from the prior year. That number requires context. The drug inflation rate ran at 7.8% for the year. Strip out inflation, and real volume growth is modest. Strip out currency depreciation, and the gain in dollar terms is effectively zero. The segment’s apparent strength is a function of price increases on imported brands, not volume expansion or new patient penetration.

Within commercial retail, generics hold 68.4% of prescription sales by volume — a figure driven by both government incentives and consumer price sensitivity at a population level. Prescription drugs represent 63.3% of commercial segment value. The e-commerce sub-segment reached 283 billion roubles (14% of the pharmacy market) in 2024, with Apteka.ru controlling 32% of that digital channel.

Why State Procurement Concentration Creates IP and Pricing Risk

The state segment shrank from 42% of the market in 2021 to 33% by end-2024, partly because large COVID-19 procurement unwound. But the shrinking headline number obscures a structural shift in how state purchasing works. A total of 86.4% of contracts for essential medicines are awarded to a single supplier. This is not a competitive tender outcome — it is a deliberate consolidation around state-preferred domestic producers.

For an innovative multinational with a patented product on the EDL, the practical implication is stark: even with valid patent protection, a domestic manufacturer with state backing may receive the procurement contract if it has achieved localization. The patent protects against commercial market infringement but does not prevent a state-directed alternative from capturing the institutional channel.

Top-Selling Drugs in Russia and What the Revenue Data Says About IP Exposure

Why Xarelto and Eliquis Lead the Market — and How Long They Stay There

Bayer’s rivaroxaban (Xarelto) and Pfizer/Bristol-Myers Squibb’s apixaban (Eliquis, sold as Elikvis in Russia) topped the market in 2024 at 18.08 billion roubles and 18.02 billion roubles respectively, with Eliquis growing 29% year-over-year. Both are direct oral anticoagulants (DOACs) with compound patent protection that is eroding globally.

Rivaroxaban’s core compound patent expired in the EU in 2024 and faces pressure in multiple markets. In Russia, the patent situation involves both the active compound and formulation claims. Domestic manufacturers have been filing bioequivalence studies and generic registrations. Once a credible generic enters the commercial channel at 30-40% lower price, the volume erosion on branded Xarelto is typically rapid. Bayer’s localization investment — it manufactures in Russia and holds the top commercial market position — provides some structural protection in the state segment, but generic entry in the pharmacy channel is an immediate margin risk.

Apixaban holds stronger patent protection in key markets through 2026-2028 depending on jurisdiction, with Bristol-Myers Squibb having defended against multiple Paragraph IV-equivalent challenges in the US. Russia does not have a direct Paragraph IV analogue, but Rospatent post-grant challenges and data exclusivity disputes serve a functionally similar purpose.

How Russian Domestic Brands Pentalgin and Mexidol Compete Without Patent Moats

Pharmstandard’s Pentalgin (analgesic combination) and Pharmasoft’s Mexidol (ethylmethylhydroxypyridine succinate, an antioxidant-nootropic) each generate approximately 9-10 billion roubles annually, ranking alongside globally recognized specialty drugs. Neither has a meaningful patent moat in the Western sense. Their competitive position rests on brand recognition, established distribution relationships, and consumer familiarity — assets that are hard to dislodge in OTC categories.

Mexidol is worth particular note for competitive intelligence purposes: it is not approved by the FDA or EMA, has a mechanism of action that remains contested in Western clinical literature, and yet generates top-10 commercial sales in the world’s eighth-largest pharmaceutical market. This illustrates the epistemological gap between Russian regulatory standards and Western approval thresholds — relevant for any MNC considering reciprocal market entry or licensing arrangements.

Table 1: Top 10 Drugs in Russia by 2024 Sales and IP Risk Profile

Patent intact to ~2026-2028; data exclusivity contested

3

Nurofen (ibuprofen)

Reckitt Benckiser

10.86

+14%

Off-patent; brand competition only

4

Edarbi (azilsartan)

Takeda

10.76

N/A

Expiring compound patent; generic threat emerging

5

Detralex (diosmin/hesperidin)

Servier

10.44

N/A

Off-patent; brand/formulation only

6

Heptral (ademetionine)

Abbott

9.62

N/A

Off-patent; brand differentiation

7

Pentalgin

Pharmstandard

9.58

+11%

No patent moat; OTC brand position

8

Teraflu

GSK

9.39

N/A

Off-patent OTC

9

Forxiga (dapagliflozin)

AstraZeneca

9.27

N/A

SGLT2 class; biosimilar pressure emerging

10

Mexidol

Pharmasoft

8.63

+10%

Domestic-only compound; no Western approval

The Russian Patent System: What Rospatent Actually Grants and What It Doesn’t

How Patent Term Extensions Work in Russia Under Article 1362

Russia provides a 20-year patent term from filing date, consistent with TRIPS obligations. Patent Term Extensions (PTEs) are available under Article 1362(2) of the Civil Code of the Russian Federation, compensating for regulatory review time in a manner structurally similar to Supplementary Protection Certificates (SPCs) in the EU.

The key mechanics: the PTE applicant must file with Rospatent within six months of either the first marketing authorization date or the patent grant date, whichever falls later. The maximum extension is five years. Russia has no pediatric extension equivalent to the EU’s additional six-month SPC extension under Regulation (EC) 1901/2006.

Since 2015, Rospatent has applied a considerably stricter approach to claim scope in PTE grants. Before that policy shift, extensions often covered the full breadth of original patent claims. Now, Rospatent issues a supplementary patent with claims restricted to the specific approved product — the precise active ingredient, indication, and form covered by the marketing authorization. This matters commercially: a product claim covering a free base compound will not automatically protect the hydrochloride salt form, a specific polymorphic form, or a pediatric formulation under the supplementary patent. Generic manufacturers have used this narrow scope to design around PTEs that would have been blocking under pre-2015 practice.

The practical consequence for lifecycle management: IP teams filing for Russian PTEs must construct the marketing authorization and the original patent claims in tight coordination. A broad compound claim with a narrow authorization creates a narrow supplementary patent. The extension covers only what is literally authorized — not what the compound claim might otherwise reach.

Table 2: Russian PTE vs. EU SPC — Key Structural Differences

Feature

Russia (PTE via Article 1362)

EU (SPC via Reg. 469/2009)

Governing law

Article 1362(2), Civil Code RF

Regulation (EC) No 469/2009

Max extension

5 years

5 years

Pediatric extension

None

+6 months

Filing deadline

6 months from MA or patent grant

6 months from MA or patent grant

Claim scope

Restricted to authorized product

Covers active ingredient per granted claims

Extension mechanism

Supplementary patent (separate grant)

SPC certificate (layered on base patent)

Challenge mechanism

Rospatent post-grant + civil court

National IP offices + CJEU referrals

Why Claim Drafting Strategy for Russian Filings Differs From US and EU Practice

US practitioners building patent families for global coverage routinely draft broad compound claims intended to hold through Paragraph IV challenges and PTAB IPR proceedings. That approach requires adjustment for Russia. At Rospatent, examination of pharmaceutical claims involves a more literal reading of experimental data support than in some Western offices. Claims unsupported by specific experimental data in the Russian application — even if supported in the PCT or priority application — may be narrowed or rejected.

The result: a patent that protects a full compound class at the USPTO may be granted only as a specific compound claim at Rospatent. Generic manufacturers tracking this divergence know exactly where the gaps are. Any IP team running a global prosecution strategy for a major asset should treat Russia as a separate, data-intensive prosecution environment, not a routine national phase entry.

Data Exclusivity in Russia: Eight Years of Contested Case Law

How the Novartis v. Biointegrator Decision Gutted Exclusivity Rights

Russian law provides six years of data exclusivity for reference medicines, split into a four-year registration exclusivity period (during which a generic cannot file) and a two-year market exclusivity period (during which a filed generic cannot receive approval). On paper, this is a standard TRIPS-compliant protection period.

In practice, the Novartis v. Biointegrator litigation in 2015-2016 created a carve-out that effectively nullified the protection for most products. The court ruled that data exclusivity applied only to non-public, undisclosed clinical data. Because the clinical trial results supporting most drug approvals are published in peer-reviewed journals — as required by international transparency standards and increasingly by law — the court found that generic manufacturers could legally reference publicly available data to support their applications without triggering the exclusivity bar.

For any branded company relying on Russian data exclusivity as a component of its IP defense strategy, that ruling meant the exclusivity clock was running, but the door it was supposed to keep locked was already open. Generic applications proceeded on the basis of published literature. The protection existed as a legal entitlement but had no operational effect.

Why the 2023 Pharmnovations Decision Changes the Data Exclusivity Calculus

In 2023, Russia’s Court of Appeal issued a ruling in a case involving Pharmnovations that inverted the Novartis-era logic. The court ordered the Ministry of Health to annul a competitor’s generic registration specifically because the application had been submitted during the four-year registration exclusivity period. The decision did not engage with the question of whether the underlying data was public — it treated the exclusivity period as a procedural bar to filing, regardless of what data the generic application relied on.

That distinction matters. If the Pharmnovations logic holds and is applied consistently, data exclusivity in Russia becomes a filing bar during the first four years, not a data-protection right contingent on the information’s confidentiality. That is closer to how the EU data exclusivity system functions under Directive 2004/27/EC’s 8+2+1 framework than the pre-2023 Russian practice.

The two rulings are not formally reconciled. Russian courts do not follow strict precedent in the common law sense, so both outcomes remain available depending on the facts and the forum. IP teams should treat data exclusivity in Russia as a contested, jurisdiction-specific right that requires active litigation to enforce — not a passive protection that runs automatically.

The Osimertinib Patent Dispute: How AstraZeneca vs. Axelpharm Defines the New IP Battlefield

Why This Case Matters Beyond a Single Drug

AstraZeneca’s osimertinib (Tagrisso) is a third-generation EGFR tyrosine kinase inhibitor approved for non-small cell lung cancer with T790M mutations. It generated approximately $5.7 billion globally in 2023. In Russia, Tagrisso holds significant oncology market share in a therapeutic category that the state prioritizes in procurement programs.

When Russian generic manufacturer Axelpharm registered a domestic osimertinib generic and launched, AstraZeneca responded with both a standard patent infringement action and a complaint to the Federal Antimonopoly Service (FAS), framing the at-risk launch as an act of unfair competition under Russian competition law. The FAS accepted the framing, investigated, and in November 2024 ruled in AstraZeneca’s favor — fining Axelpharm and ordering it to cease sales.

How the Moscow Arbitration Court Reversed the FAS Decision

In May 2025, the Arbitration Court of Moscow overturned the FAS ruling. The court found that the antimonopoly service had failed to prove actual patent infringement by its own investigative standards, had not properly established that AstraZeneca and Axelpharm were engaged in direct competitive conduct as required for an unfair competition finding, and had misapplied the underlying competition law framework.

The reversal does not mean FAS intervention in pharma IP disputes is dead — it means the evidentiary threshold for sustaining such an intervention is higher than the initial ruling suggested. AstraZeneca’s strategy of using competition law as a parallel IP enforcement tool is now established as available even if its first application failed on procedural grounds.

For IP strategists: the osimertinib case establishes that patent disputes in Russia now have at least three simultaneous venues: patent court (Rospatent or commercial court), FAS administrative complaint, and potential compulsory licensing proceedings. Each venue has different evidentiary standards and decision timelines. A comprehensive patent defense strategy requires resources across all three, not a sequential escalation.

What Compulsory Licensing Risk Looks Like for Patented Oncology Drugs in Russia

Russia’s Civil Code permits compulsory licensing for patented inventions in cases of national defense, national security, or “other vital state interests.” Since 2022, the government has also enacted measures allowing the use of patents owned by entities from “unfriendly countries” without consent, in exchange for compensation set at a level the Russian government determines to be “equitable.” This is not a hypothetical: the mechanism has been invoked in other IP categories since 2022.

For oncology drugs — a category the state explicitly targets in Pharma 2030 as a priority for domestic production — the combination of compulsory licensing authority and the “unfriendly countries” regime creates a two-pronged expropriation risk. A patented oncology drug owned by a US, EU, or UK company could face compulsory licensing on national security grounds, with the compensation rate set unilaterally. No WTO dispute settlement mechanism is currently available to contest that through normal channels given the geopolitical context.

Investors and licensing teams should model this as a binary tail risk rather than a gradual erosion scenario. The drug either retains commercial protection or it doesn’t, and the switch can happen administratively with minimal notice.

Russia’s Biosimilar Ambitions: BIOCAD’s Pipeline and the Regulatory Pathway

How BIOCAD Is Building a Global Biosimilar Position From a Russian Base

BIOCAD is Russia’s most technically sophisticated biopharma company. Its pipeline targets high-value biologics in oncology (pembrolizumab biosimilar, rituximab, trastuzumab), autoimmune disease (adalimumab, ustekinumab biosimilars), and ophthalmology (bevacizumab). The company has received regulatory approval in multiple CIS and Asian markets for biosimilar products and is explicitly targeting export revenue as a component of its growth strategy.

BIOCAD’s competitive relevance for Western originators is direct: it is developing biosimilars of drugs that are either approaching loss of exclusivity or whose patents have already expired in Russia while remaining in force in the US and EU. A BIOCAD biosimilar approved in Russia can enter CIS and EAEU markets immediately upon Russian approval. The EAEU’s centralized procedure creates a five-country approval from a single Russian dossier. For a drug like adalimumab (where AbbVie’s Humira lost exclusivity in the US in 2023), BIOCAD’s version competes in markets where AbbVie has maintained revenue — particularly in countries where it has not yet established a biosimilar-friendly reimbursement position.

Why Biosimilar Interchangeability Standards in Russia Are Less Stringent Than FDA Requirements

The Russian framework for biosimilar approval does not require the same level of clinical comparative data as the FDA’s 351(k) pathway or the EMA’s similar biological medicinal products guideline. Russian biosimilar approvals historically relied more heavily on physicochemical comparability and in vitro functional data, with reduced emphasis on clinical pharmacokinetics and immunogenicity studies. This allows domestic biosimilar developers to bring products to market faster and at lower development cost than is possible under Western regulatory standards.

The commercial implication for originator companies is that biosimilar competition in Russia arrives earlier and at steeper price discounts than in the US or EU. A biologic that might maintain 70% market share for three years after Western biosimilar entry may face 50%+ volume erosion in Russia within 18 months. Procurement programs favor the cheapest biosimilar regardless of clinical data package depth, because Minzdrav’s EDL procurement criteria weight price heavily for products with demonstrated category interchangeability.

R-Pharm’s Strategy: State Procurement Dominance Through Contract Manufacturing

R-Pharm occupies a different strategic position than BIOCAD. While BIOCAD emphasizes original R&D and biosimilar innovation, R-Pharm built its position through contract manufacturing relationships with multinational companies, state procurement alignment, and therapeutic area focus in oncology, antiviral therapies, and autoimmune disease.

R-Pharm serves as a contract manufacturer for AstraZeneca, GlaxoSmithKline, and other MNCs, producing drugs locally to satisfy the Pharma 2030 localization requirements that unlock state procurement access. This positions R-Pharm simultaneously as a supplier to foreign companies and a competitor to them in the procurement channel. The dual role is not accidental — it reflects the Russian government’s deliberate strategy to build domestic manufacturing capacity through technology transfer embedded in contract arrangements.

For foreign companies, the R-Pharm partnership model carries the same tension as any localization strategy: the infrastructure and know-how transferred to meet today’s procurement requirements may fund tomorrow’s domestic competitor.

The EAEU Regulatory Pathway: What the Mandatory Centralized Procedure Means for Market Entry Timing

How the January 2022 Shift to EAEU Mandatory Registration Changed Filing Strategy

Since January 1, 2022, all new drug registrations in Russia must proceed through the Eurasian Economic Union centralized procedure, covering Russia, Belarus, Kazakhstan, Armenia, and Kyrgyzstan as a unified regulatory bloc. A successful application produces marketing authorization valid across all five member states.

The technical requirement is a Common Technical Document (CTD) dossier in ICH format, but Module 1 — administrative, labeling, and country-specific information — must be submitted in Russian for all five countries. Foreign manufacturers must appoint a local representative resident in at least one EAEU member state.

The procedural timeline under the national system runs to 160 business days as a nominal clock, but query periods (up to 90 business days of clock-stopping) and GMP certificate requirements mean the practical approval timeline for a site-specific application is routinely 12-18 months. For a new molecular entity seeking market entry in Russia, the combined timeline from first EAEU filing to commercial launch — accounting for registration, GMP certification by Roszdravnadzor, and distribution channel setup — is typically 24-36 months.

Why GMP Certification by Roszdravnadzor Creates a Non-Tariff Barrier

Every production site and dosage form requires a separate GMP certificate issued by Roszdravnadzor (the Federal Service for Surveillance in Healthcare). The inspection process involves on-site audits by Russian inspectors, conducted on Russian inspection timelines that have limited alignment with EMA or FDA inspection scheduling. A site that holds both FDA and EMA GMP compliance will not automatically satisfy Roszdravnadzor requirements — Russia conducts its own inspections and issues its own certificates.

For foreign manufacturers choosing between direct importation and local contract manufacturing to satisfy localization requirements, the GMP certification timeline is a critical commercial variable. A contract manufacturing arrangement with R-Pharm or Pharmstandard transfers the GMP burden to a domestically certified site, accelerating state procurement eligibility. An owned-and-operated foreign plant must pass Russian GMP inspection before any product can be sold in state procurement channels, regardless of how many other regulatory bodies have cleared it.

Russia’s API Dependency: The 95% Import Problem That Undermines Every Self-Sufficiency Goal

Why Russian Pharma 2030’s Central Vulnerability Is Its API Supply Chain

Approximately 95% of Active Pharmaceutical Ingredients used in Russian drug manufacturing are imported, primarily from China and India. This figure appears in multiple government documents as an acknowledged strategic vulnerability. The Pharma 2030 strategy includes API localization as a stated goal, but the gap between stating the goal and closing it is substantial.

Building a domestic API industry requires chemical synthesis capacity, purification infrastructure, analytical testing capability, regulatory compliance systems, and a trained workforce. Most of this was dismantled in the 1991-1999 period and has not been rebuilt. The Russian government has allocated funding to early-stage API production initiatives and has provided subsidies to small-scale chemical producers. But the economics of API production are global-scale economics — Indian and Chinese manufacturers operate at volumes that produce unit costs Russian domestic producers cannot match without sustained, multi-decade subsidy.

The strategic risk for the domestic industry is a single-point supply chain: a disruption to Chinese API supply for a specific compound — whether from export restrictions, production incidents, or geopolitical pressure — has no domestic backstop. Russia discovered this in mild form during COVID-19 supply chain disruptions and responded with emergency procurement from India. The 2022 sanctions environment has added financial complexity to these transactions, making API procurement more expensive and administratively burdensome even when physical supply is available.

How Indian Generics Producers Are Navigating the Russia Sanctions Environment

India has maintained a commercial relationship with Russia throughout the post-2022 sanctions period, with Indian generic manufacturers continuing to supply both finished drugs and APIs to Russian buyers. Sun Pharma, Dr. Reddy’s, Cipla, and Glenmark all maintained or increased their Russian market presence during 2022-2024. The EAEU’s regulatory harmonization makes India an attractive supply partner — Indian manufacturers with WHO-GMP certification can often satisfy Roszdravnadzor requirements more easily than Western manufacturers, and the pricing differential over European API sources is substantial.

For Indian generic manufacturers, the Russian market post-2022 opened competitive space vacated by Western companies that suspended investment or reduced promotional activity. Companies that maintained supply chains and distributor relationships captured volume that had been held by multinationals. The medium-term risk for Indian players is reputational exposure in Western markets if their Russian revenue becomes a compliance or secondary-sanctions concern.

The Competitive Hierarchy: Multinationals Under Pressure, Domestic Champions Rising

How Bayer, Novartis, and Sanofi Held the Top Three Slots While Pulling Back Investment

The top positions in the Russian market remain held by foreign multinationals. Bayer led with 77.1 billion roubles in 2023 revenue, driven largely by Xarelto. Novartis followed at 76.4 billion roubles, and Sanofi at 67.7 billion roubles. All three have announced suspension of new capital investment in Russia and reduced non-essential promotional activities since 2022.

Holding revenue while reducing investment produces exactly what it looks like: a short-term maintenance of position funded by existing market presence, with long-term erosion as the pipeline of new product launches dries up. For companies that have localized production — Bayer, Sanofi, AstraZeneca, Takeda — that localization provides some insulation against immediate market loss, but it does not substitute for a functioning new product launch strategy.

AstraZeneca’s Russian revenues in 2023 were 65.7 billion roubles. Its local pipeline includes both oncology products (Tagrisso, Imfinzi, Calquence) and cardiovascular drugs (Forxiga, Brilinta). The Tagrisso patent dispute described above is the most visible IP conflict, but AstraZeneca also faces biosimilar pressure on its monoclonal antibodies as BIOCAD and Pharmasyntez advance comparable programs.

Table 3: Top 10 Pharmaceutical Companies in Russia by 2023 Revenue

Rank

Company

Country

2023 Revenue (bn RUB)

Market Share

1

Bayer

Germany

77.1

3.5%

2

Novartis

Switzerland

76.4

3.4%

3

Sanofi

France

67.7

3.0%

4

AstraZeneca

UK/Sweden

65.7

2.9%

5

Roche

Switzerland

61.9

2.8%

6

Johnson & Johnson

USA

58.0

2.6%

7

Stada

Germany

56.1

2.5%

8

Abbott

USA

46.6

2.1%

9

OTCPharm

Russia

45.6

2.0%

10

Servier

France

~45.0

~2.0%

Pharmstandard’s Competitive Moat: Scale, Breadth, and State Alignment

Pharmstandard is Russia’s largest domestic drug manufacturer by sales volume, with over 400 pharmaceutical products across cardiology, diabetes, neurology, and oncology. Its annual production capacity exceeds 1.7 billion packages. The company’s competitive position is not built on patent-protected innovation — it is built on manufacturing scale, established distributor relationships, and a product portfolio that maps closely to the EDL priorities the state procurement system favors.

For foreign companies assessing competitive risk, Pharmstandard is the baseline threat in generics. It can produce most small-molecule off-patent drugs at costs that undercut imports, has existing relationships with Protek, Pulse, and Katren (the distribution oligopoly), and has state procurement contracts that provide revenue floor stability. Its expansion into the OTC analgesic category with Pentalgin demonstrates the company’s capacity to build consumer brands alongside its institutional channel presence.

How Pharmstandard’s Acquisition History Shapes Its Competitive Position

Pharmstandard has pursued strategic acquisitions of smaller Russian manufacturers and distribution-adjacent assets since the mid-2000s. Its ownership structure connects to Victor Kharitonin and Egor Kulkov through holding structures that have occasionally attracted scrutiny in corporate governance analyses. The company’s close alignment with government health priorities has been interpreted by some analysts as a structural advantage in procurement allocation, not merely competitive merit.

For a foreign company seeking a Russian contract manufacturer or local partner, Pharmstandard’s market position means any competitor that partners with it is lending credibility to an entity that will ultimately compete against them in off-patent categories.

The Distribution Oligopoly: How Protek, Pulse, and Katren Control Market Access

Why Getting Past the Top Three Distributors Is the Real Market Entry Barrier

Russia’s pharmaceutical distribution landscape is more concentrated than its manufacturing sector. In Q1 2025, the top ten distributors controlled 80.4% of the market. The top three — Protek, Pulse, and Katren — collectively hold over 36% of the total market. These companies are not passive logistics operators; they are active commercial agents with pricing influence, promotional leverage, and preferential shelf placement capacity across 50,000-plus pharmacy outlets spanning Russia’s eleven time zones.

For any company entering the Russian market — multinational or generic player — distribution terms with these three companies determine commercial viability. Protek operates its own pharmacy chain (Rigla, one of Russia’s largest) in addition to wholesale distribution, creating vertical integration that gives it both procurement and retail leverage. Katren similarly operates pharmacy chains alongside its wholesale business.

The negotiating dynamics favor the distributors. A foreign manufacturer with one or two products cannot credibly threaten to withdraw from a major distributor’s network without writing off a substantial portion of its Russian revenue. The distributors know this and set commercial terms accordingly — typically higher margins than are standard in Western European markets, longer payment cycles, and promotional contribution requirements that increase fixed commercial costs.

Investor Implications: What Russia’s Pharma IP Dynamics Mean for MNC Valuations

How to Model Russian Revenue Risk for Pharma Companies With Significant Exposure

For companies where Russia represents a meaningful revenue line — historically 2-4% of global revenue for mid-tier European specialty pharma firms — the valuation question is whether to apply a geopolitical risk discount, a currency risk discount, or both. The answer is both, but at different time horizons.

The currency risk is immediate and quantifiable: 2.85 trillion roubles in market size at today’s exchange rates translates to approximately $30.9 billion. If the rouble depreciates another 20% (a realistic scenario given fiscal pressure and energy price volatility), the dollar-equivalent market shrinks to roughly $24.7 billion with no change in rouble-denominated volumes. Companies that manufacture locally have partial natural hedges; pure importers do not.

The geopolitical risk is event-driven and binary at the tail. For innovative drugs owned by companies headquartered in “unfriendly countries,” the compulsory licensing and patent suspension mechanisms enacted since 2022 create a scenario where IP protection is withdrawn by government decree. The expected value impact on a 10-year DCF is modest if the probability is low, but the scenario matters for portfolio managers running concentration risk in emerging market pharma.

What Investors Are Watching: Key Variables for Russian Pharma Exposure

The variables that matter for investment analysis are: (1) localization status — is the company manufacturing in Russia or importing; (2) EDL inclusion — is the relevant drug on the Essential Drug List, which determines state procurement eligibility; (3) patent expiry timeline — when do core patents expire, and have domestic manufacturers already filed registrations; (4) compulsory licensing risk — is the drug in a therapeutic category the state has targeted for domestic production; and (5) distributor contract terms — what are the payment terms and margin structures with Protek, Pulse, and Katren.

A company that manufactures locally, holds drugs on the EDL, has patents expiring in the 2028-2032 window, and has established distributor relationships is in a defensible commercial position. A company that imports, holds no manufacturing presence, and has core patents expiring before 2027 is likely facing accelerating revenue erosion in Russia regardless of the formal IP environment.

How Russia’s Clinical Trial Infrastructure Is Being Disrupted by MNC Withdrawals

What Happens to the 1,300 Western-Sponsored Trials That Drive Russian Innovation

Of Russia’s approximately 2,100 active clinical trials, over 1,300 have historically been sponsored by US and Western European companies. These trials provided Russian patients with access to experimental therapies, generated Russian clinical data supporting global registrations, and funded the clinical research organization infrastructure that supports Roszdravnadzor submissions.

Since 2022, many multinationals have halted new trial initiations in Russia. Existing trials have continued in most cases — abandoning enrolled patients mid-trial raises serious ethical and regulatory issues — but the pipeline of new Phase 2 and Phase 3 trials sponsored by Western companies has effectively stopped. CROs like IQVIA, which operated more than 500 trials in Russia over the preceding decade, have reduced Russian activities in line with client decisions.

The long-term consequence is a shrinkage in the Russian clinical database that cannot be compensated by domestic sponsors quickly. Russian companies’ internally sponsored trials predominantly target bioequivalence for generics (about 50% of domestically sponsored trials) and only 25% address critical disease areas like oncology or cardiovascular disease. Original drug development requires a type and scale of clinical evidence that takes a decade to build and cannot be accelerated through policy mandates alone.

Common Questions From Pharma IP and Commercial Teams

Does Russia’s six-year data exclusivity period provide meaningful protection post-2023?

The 2023 Pharmnovations ruling restored some procedural force to the four-year registration exclusivity bar, but the underlying question of whether publicly available clinical data can be referenced remains unresolved by a definitive Supreme Court ruling. Treat data exclusivity as worth asserting aggressively, not as a reliable passive protection.

How does Russia’s Paragraph IV equivalent work for generic challenges?

Russia has no formal Paragraph IV filing mechanism equivalent to the US Hatch-Waxman framework. Generic manufacturers do not certify against listed patents before filing. Instead, generic registration proceeds independently, and patent disputes arise post-registration or post-launch. The result is more at-risk launches and less pre-launch IP dispute resolution than in the US system.

Can a US company use US court orders to block Russian generic sales?

No. Russian courts apply Russian law and do not enforce foreign injunctions. A US district court ruling against a Russian generic manufacturer has no operative effect in Russia. IP enforcement must occur through Russian civil courts, Rospatent proceedings, or FAS administrative complaints — each under Russian procedural rules.

What is the “Third Wheel” rule and does it apply to all state procurement?

The “Third Wheel” rule (sometimes called the “Two from EAEU” rule) applies specifically to state procurement tenders governed by Federal Law No. 44-FZ. When at least two compliant bids from EAEU-based manufacturers are submitted, all bids from manufacturers outside the EAEU are automatically disqualified. This applies to purchases of drugs on the Vital and Essential Drug List through state tender processes, which represent the majority of hospital and subsidized procurement.

How long does EAEU drug registration take in practice?

The nominal clock is 160 business days plus query response periods of up to 90 business days. In practice, first-time filers without established relationships with Minzdrav should budget 18-24 months from initial submission to receiving marketing authorization. Site-specific GMP certification adds additional time if the manufacturing site has not previously been certified by Roszdravnadzor.

Which Russian domestic companies are most likely to challenge MNC patents?

The companies with both the technical capacity and commercial incentive to challenge MNC patents are BIOCAD (biologics/biosimilars), R-Pharm (contract manufacturer that has developed originator capabilities), Pharmstandard (generic small molecules), Pharmasyntez (generic oncology drugs), and Geropharm (insulin and biosimilars in endocrinology). Pharmasyntez has been particularly active in oncology generics and has registered generic versions of patented cancer drugs that were subsequently contested.

Investment Strategy

For Innovative MNCs Assessing Russian Exposure

Companies with patented drugs generating more than 2% of global revenue in Russia face a portfolio decision: invest in localization to protect state procurement access and currency hedge, or manage the Russian business as a declining asset while preserving optionality for eventual re-entry.

The localization investment required to satisfy Pharma 2030 requirements — manufacturing, GMP certification, distribution infrastructure — typically runs to $50-150 million for a single drug category. The payback period on that investment, given the currency environment and IP risk, is longer than in most other emerging markets. Companies with broad portfolios in Russia (five or more major products) can spread the localization cost across a larger revenue base and achieve better economics. Single-product companies face a structurally unfavorable cost-to-benefit ratio.

For drugs with fewer than three years of remaining patent protection and active domestic generic registration activity, the investment case for deep localization is very weak. For biologics and complex drugs with patent protection extending past 2030, the case is stronger — but only if the IP enforcement environment continues to improve from its post-2016 low point.

For Biosimilar and Generic Developers Targeting Russia and the EAEU

The EAEU’s five-country centralized registration system makes Russia the gateway to a combined pharmaceutical market of roughly 180 million people. A company that achieves Russian registration and meets GMP standards automatically has the regulatory foundation for Kazakhstan, Belarus, Armenia, and Kyrgyzstan.

For biosimilar developers targeting specific EAEU markets, the strategic calculus involves timing: entering before BIOCAD or other domestic champions have achieved dominant market position in a given therapeutic category. In categories where BIOCAD already holds state procurement contracts (certain oncology biosimilars, adalimumab), a new entrant faces both a domestic incumbent with government alignment and the administrative burden of displacing an established contract. Entering underserved categories — rare disease biologics, specialty ophthalmology, some neurology biosimilars — offers better first-mover economics.

API security is the operational priority. Any biosimilar or generic company building a Russia/EAEU strategy must establish reliable API supply from Indian or Chinese manufacturers through commercial arrangements that are not dependent on single suppliers or single logistics routes. Secondary sourcing and safety stock policies that assume a 90-day supply disruption are minimum risk management standards in the current environment.

Key Takeaways

Russia’s pharmaceutical market generates 2.85 trillion roubles and is holding flat in dollar terms at $30.9 billion. Currency depreciation and drug inflation are both running simultaneously, producing the appearance of growth that does not translate to hard-currency revenue.

The Pharma 2030 strategy is the single most consequential factor in Russian pharmaceutical commercialization. Its “Third Wheel” procurement rule, EDL localization requirements, and API substitution targets are not aspirational — they are operative rules already reshaping competitive dynamics. The internal debate between the 43% generic factory target and the 70% innovation hub target has not been resolved. Both versions of the strategy are bad for pure importers and potentially good for companies willing to manufacture locally and transfer technology.

Data exclusivity exists on paper and was operationally dead after 2016, but the 2023 Pharmnovations ruling has reopened the question. The enforcement environment for IP rights in Russia is more active than it was three years ago, and the FAS’s involvement in the Osimertinib case confirms that administrative routes — not just patent courts — are available and worth using.

The distribution oligopoly (Protek, Pulse, Katren) controls 36%+ of the market. No commercial strategy succeeds without addressing distributor terms as a primary commercial variable, not an afterthought.

BIOCAD and R-Pharm are serious competitors, not local substitutes. Their biosimilar pipelines target the same drugs that MNCs are defending globally. Regulatory approvals in Russia and the EAEU translate directly to market access for drugs still under patent in Western markets.

The 95% API import dependency remains Pharma 2030’s structural vulnerability. Supply chain disruptions affecting Indian or Chinese API supply have no domestic backup and will affect both domestic generics producers and multinational localized facilities.

All revenue figures are sourced from Russian pharmacy data providers and company filings. Patent timeline analysis reflects publicly available Rospatent records and court decisions. This analysis does not constitute investment advice.

")