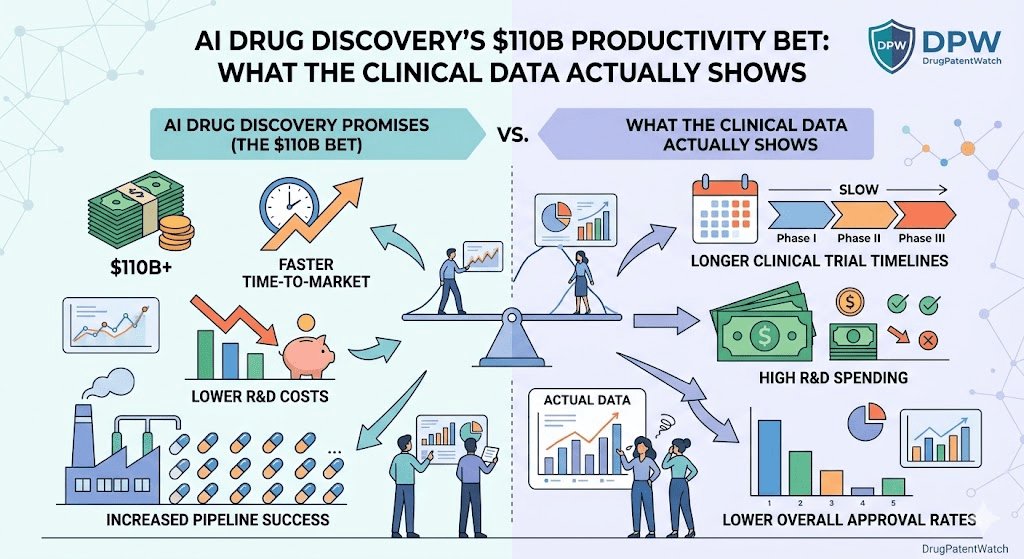

The cost of bringing a drug to market has crossed $2 billion. The Phase 2 failure rate sits near 60%. And for the past 70 years, Eroom’s Law has tracked the industry’s declining R&D productivity with the regularity of a bad earnings report. Into this structural problem, the industry has placed a very large wager on artificial intelligence.

This is not a technology story. It is an economics story about whether a new class of computational tools can invert the risk profile of pharmaceutical R&D before the patent cliff swallows the revenue base of the companies paying for it.

The answer, as of mid-2025, is: partially. AI has demonstrably improved preclinical success rates. It has not yet cracked late-stage efficacy. The gap between those two statements contains most of what matters for investors, IP teams, and pipeline strategists.

Why Eroom’s Law Makes AI Adoption Commercially Inevitable

The pharmaceutical industry has a structural productivity problem that predates AI by decades. The number of new drugs approved per billion dollars of R&D spending has halved approximately every nine years since 1950. Inflation-adjusted, that means the industry is producing fewer approved drugs per dollar today than it was in the 1960s, despite vastly superior chemistry tools, genomic databases, and computing power.

This dynamic is why AI is not optional. When a single Phase 3 failure can erase $500 million in sunk cost, any tool that improves early-stage prediction of clinical failure has compounding value. The NPV math is straightforward: reducing preclinical time from five years to eighteen months adds years of patent-protected market exclusivity on the backend. One additional year of Keytruda-level revenue, currently running above $25 billion annually, exceeds the entire annual AI drug discovery investment market.

The economic pressure is also structural. Major biopharma companies collectively face a patent cliff that will expose well over $200 billion in annual revenue to generic and biosimilar competition between 2025 and 2030. AbbVie’s Humira is already in full erosion. Merck’s Keytruda (pembrolizumab) faces its first composition-of-matter expiry around 2028. Bristol Myers Squibb’s Eliquis (apixaban) and Opdivo (nivolumab) are close behind. The companies funding AI drug discovery programs are not doing it out of scientific curiosity. They are doing it to replace that revenue before it disappears.

The Phase 1 vs. Phase 2 Divergence: Where AI Actually Works

The most cited statistic in AI drug discovery is that AI-discovered molecules clear Phase 1 trials at a rate of 80-90%, compared to the historical industry average of 40-65%. This figure is accurate but requires precise interpretation.

Phase 1 trials test safety and pharmacokinetics. They ask: does this molecule move through the human body in a predictable way, and does it kill people at the intended dose? AI is exceptionally good at solving these problems computationally. Optimizing for ADMET properties, which include absorption, distribution, metabolism, excretion, and toxicity, is fundamentally a pattern-recognition problem across large chemical datasets. Models trained on ChEMBL and proprietary synthesis databases can predict metabolic liability, hERG channel toxicity, and solubility with accuracy that consistently outperforms traditional medicinal chemistry intuition for well-characterized chemical space.

Phase 2 is different. Phase 2 asks whether the molecule actually does something useful to the disease. It tests a biological hypothesis, not a chemical property. And here the AI advantage narrows considerably. Phase 2 success rates for AI-derived molecules currently track near the historical 40% benchmark, which means that while AI has effectively solved the “make a good molecule” problem, predicting whether that molecule will modulate a complex human disease remains largely unsolved.

The practical implication for portfolio managers: early-stage AI programs deserve a higher probability of technical success (PoTS) adjustment for Phase 1, but not for Phase 2 unless the company can demonstrate that its target identification process has been validated in human data, not just cellular assays.

Insilico Medicine’s ISM001-055: What the IPF Phase 2a Data Actually Proves

In November 2024, Insilico Medicine announced positive topline Phase 2a results for ISM001-055, a TNIK inhibitor for idiopathic pulmonary fibrosis. The trial enrolled 71 patients across 21 Chinese sites, and the drug showed a dose-dependent improvement in Forced Vital Capacity. Patients on the highest dose, 60 mg once daily, gained a mean of 98.4 mL from baseline at 12 weeks, against a decline of 62.3 mL in the placebo arm.

Two things make this result matter for the broader field. First, the target. TNIK (Traf2- and NCK-interacting kinase) was identified by Insilico’s PandaOmics platform as fibrosis-relevant before any medicinal chemist had worked on it. The molecule was designed by Chemistry42, a generative chemistry engine. This was not a repurposed compound or a known scaffold in a new indication. It was a novel target and a novel molecule, both originating from AI computation.

Second, the timeline. Target identification to preclinical candidate took 18 months. Entry into Phase 1 happened within 30 months. The industry average for equivalent programs is 5-6 years. That compression has direct IP implications: earlier IND filings mean earlier patent priority dates, which affects the eventual exclusivity window when calculating loss of exclusivity for competitive intelligence purposes.

What the data does not prove is scalability across therapeutic areas. IPF has reasonably well-characterized fibrotic pathways. The same platform approach applied to a heterogeneous disease like schizophrenia or treatment-resistant depression, where target biology is substantially less understood, would face entirely different challenges.

Why Recursion’s REC-994 Failure Is More Instructive Than Insilico’s Success

Recursion Pharmaceuticals discontinued REC-994, its superoxide scavenger for Cerebral Cavernous Malformation, in May 2025 after long-term extension data from the SYCAMORE trial failed to sustain the efficacy signals seen at the 12-month mark. Lesion volume reduction on MRI, which had shown encouraging trends, did not hold through the extension period. Functional outcomes were also inconclusive.

The mechanism failure here is analytically important. Recursion’s phenomics platform identifies drugs by their effect on cellular morphology, specifically by detecting whether a compound reverses the abnormal cell shape associated with a disease state. The platform correctly identified that REC-994 altered the CCM phenotype in cells. It did not capture whether that cellular signal would translate to clinical benefit in a disease that manifests in brain vasculature, involves immune crosstalk, and shows high inter-patient heterogeneity.

This is the translation gap. A cellular phenotype is not a disease. An animal model is not a patient. The AI correctly solved for the cell; it could not solve for the system. For investors evaluating phenomics-based discovery platforms, this failure argues for discounting Phase 2 probability of success estimates relative to companies with mechanistic target validation in human genetic data, such as loss-of-function variants from large-scale biobank studies.

The REC-994 failure also accelerated Recursion’s strategic rationale for acquiring Exscientia. Phenomics-derived targets need precision chemistry. Exscientia’s platform, which uses multi-parameter optimization to design molecules for specific binding profiles, addresses exactly the gap that phenomics alone cannot fill.

How the Recursion-Exscientia Merger Reshapes TechBio Competitive Dynamics

The combination of Recursion and Exscientia is the most consequential M&A event in AI drug discovery since the sector emerged. Recursion brought industrial-scale biological data generation, with a platform capable of running millions of cellular experiments per week. Exscientia brought precision medicinal chemistry and the credibility of having put multiple AI-designed molecules into clinical trials, including DSP-1181 (a D1/5 receptor agonist developed with Sumitomo Dainippon Pharma) and EXS-21546 (an A2A antagonist, subsequently discontinued).

The combined entity aims to be vertically integrated from target identification through IND filing, with no outsourced discovery steps that could compromise data proprietary. This matters for IP strategy: when a company’s discovery platform generates the target hypothesis, synthesizes and screens molecules, and owns all associated data, the patent claims covering the resulting asset have a cleaner provenance trail than programs where the target came from an academic collaboration and the chemistry from a CRO.

For competing platforms, the merger sets a competitive bar. Standalone AI chemistry companies now face pressure to either demonstrate Phase 2 efficacy or find a strategic partner with biological data generation capabilities. Exscientia-equivalent platforms without a Recursion-equivalent biology engine are likely acquisition targets through 2027.

AlphaFold 3’s Commercial Impact Beyond the Academic Press Release

AlphaFold 2 transformed structural biology by predicting static protein structures. AlphaFold 3, released by Google DeepMind and Isomorphic Labs, predicts the interactions of proteins with small molecule ligands, DNA, and RNA. The architectural shift from Evoformer to Pairformer, combined with a diffusion-based coordinate prediction system, allows the model to predict how a drug candidate physically docks into a binding site with accuracy that reportedly exceeds previous methods by at least 50% on standard benchmarks.

The commercial implication for drug discovery is not just better docking predictions. It is the compression of the hit-to-lead phase. Traditionally, identifying which chemical scaffold binds a target requires high-throughput screening of large compound libraries, a process that costs millions of dollars and takes months. With AlphaFold 3 quality docking predictions, computational screening of virtual libraries with hundreds of millions of compounds becomes the first-line approach, with physical synthesis reserved for the top-scoring candidates. This changes the cost structure of early-stage programs and, by reducing the number of compounds that need to be synthesized and tested, reduces dependence on outsourced chemistry capacity, including the Chinese CRO infrastructure threatened by the BIOSECURE Act.

Isomorphic Labs, the commercial arm of this effort, signed discovery partnerships with Eli Lilly and Novartis in early 2024 worth up to $3 billion in combined milestone payments. The deal economics, which front-load Isomorphic’s cash while back-loading risk to milestone achievement, reflect the industry’s current uncertainty about where AI-assisted structural biology stops and drug optimization begins.

Diffusion Models in Molecular Design: Why DiffDock Changes the Target-Drug Matching Problem

Generative image models like Stable Diffusion work by learning to remove noise from images iteratively, beginning with random static and refining to coherent output. Molecular diffusion models apply the same principle to 3D chemical space. DiffDock, developed at MIT, treats ligand docking as a diffusion process over the space of ligand poses and conformations, generating distributions of likely binding configurations rather than a single “best” answer.

This probabilistic output is practically valuable. Traditional docking software gives a single predicted binding mode and a score. DiffDock gives a distribution of modes, allowing chemists to identify not just the most likely binding configuration but the range of configurations that satisfy the binding energy threshold, which informs which parts of the molecule can be chemically modified without disrupting the binding interaction. This improves the efficiency of the lead optimization phase, which historically consumes two to three years between a confirmed hit and an IND-ready candidate.

The patent implications are indirect but real. Faster lead optimization reduces the time from patent filing to IND filing, which affects the effective patent life remaining when a drug eventually reaches market. A drug that takes six years from first patent filing to NDA approval has approximately 14 years of patent-protected market life (assuming a 20-year term from filing). A drug that takes four years has 16 years. At peak sales of a blockbuster-class drug, those two additional years are worth billions in discounted cash flow.

What the FDA’s January 2025 AI Guidance Actually Requires From Sponsors

The FDA’s January 2025 draft guidance on AI in regulatory submissions does not prohibit black-box algorithms from NDA packages. It requires that sponsors document why their model is credible for its specific context of use, what data it was trained on, and how they will monitor it for performance degradation after deployment. This is substantially more demanding than simply asserting that an algorithm worked in internal validation.

The credibility assessment framework follows a seven-step process. Sponsors must define the question the model answers, the data used to train and validate it, the metrics used to evaluate performance, the conditions under which it fails, and the plan for ongoing monitoring. For AI tools used to support efficacy claims (e.g., digital biomarker endpoints, AI-read imaging studies), the bar is high. For AI tools used in back-office functions like site selection or supply chain optimization, the oversight requirements are lighter.

The practical bottleneck for most sponsors is documentation. Most pharma companies have been using AI internally for years, often building models without the systematic audit trails that regulatory credibility assessment now requires. This creates a remediation problem for legacy tools and a quality-by-design imperative for new programs. Companies that have not already implemented model cards, data lineage tracking, and drift monitoring protocols face significant regulatory preparation costs before their AI-supported submissions can withstand FDA scrutiny.

The European Medicines Agency is aligned on the broad framework, with additional emphasis on algorithmic bias and demographic representativeness of training datasets. The convergence of FDA and EMA expectations reduces the complexity of global submission strategies but does not eliminate it.

Freedom to Operate by Design: How AI Generative Chemistry Creates Patent Risk at Scale

Generative chemistry models produce novel molecular structures at a rate that far exceeds the capacity of IP teams to manually assess patentability and freedom to operate. A single generative run can produce thousands of candidate structures in hours. Without systematic IP screening integrated into that process, a company can spend two years developing a molecule that turns out to fall within a competitor’s Markush claim, a broad patent structure that covers entire chemical families rather than specific compounds.

Markush claims are the primary IP weapon of branded pharma companies protecting their small molecule franchises. When Pfizer filed patents on tofacitinib (Xeljanz), the Markush structures in those filings covered tens of thousands of JAK inhibitors that Pfizer had never synthesized. Any generative AI platform designing JAK inhibitors without ingesting those claims as constraints will produce molecules that infringe.

The solution is integrating patent data directly into the generation process rather than checking freedom to operate after a lead series is identified. Platforms that incorporate structured patent databases, covering not just granted patents but pending applications, Orange Book listings, patent term extensions, and litigation status, can penalize the generative model for producing structures that fall within active claims and reward it for exploring chemical space where IP is available or expired.

This is the practical application DrugPatentWatch supports in AI programs: the patent data becomes a constraint in the objective function during generation, not a legal checkpoint months later. The distinction matters enormously for capital efficiency, because a freedom-to-operate failure discovered at lead optimization costs far less to address than one discovered at NDA submission.

How AI Patent Prediction Models Are Changing Generic Entry Forecasting

The conventional approach to estimating generic entry timing uses the last patent expiry date from the FDA’s Orange Book. This approach is systematically wrong for two reasons. First, branded companies routinely list additional patents after initial approval, extending the Orange Book filing date well beyond the original composition-of-matter expiry. Second, litigation settlement agreements, particularly those under Hatch-Waxman paragraph IV procedures, typically define entry dates that are earlier than patent expiry but later than the challenger’s intended launch, through authorized generic provisions, revenue-sharing terms, and market exclusivity windows.

Machine learning models trained on historical litigation outcomes, settlement terms, and patent portfolio characteristics can predict actual generic entry dates with substantially higher accuracy than simple Orange Book analysis. The predictive features include: the breadth of Markush claims in the asserted patents, the litigation history of the brand’s IP counsel, the capitalization and pipeline depth of the ANDA filer, whether the case settled in the 30-month stay window, and the presence of any regulatory exclusivity (such as pediatric exclusivity or new chemical entity exclusivity) that would extend market protection beyond patent term.

For portfolio managers holding branded pharma equity, this matters because consensus models consistently underestimate how long loss of exclusivity can be delayed through litigation and settlement. Humira’s adalimumab franchise is the canonical example: composition-of-matter patents expired years before biosimilars reached US patients, because AbbVie’s formulation and dosing device patents, combined with settlement agreements that granted delayed entry dates, extended effective exclusivity well past what a simple patent analysis would suggest.

The BIOSECURE Act’s Specific Impact on AI-First Virtual Biotechs

AI drug discovery companies with lean internal teams and large outsourcing footprints face a specific version of the BIOSECURE Act risk that asset-heavy pharma companies do not. A company like Recursion has substantial internal biology infrastructure. A typical Series B virtual AI biotech has two dozen employees, a generative chemistry platform, and contracts with Chinese CROs for synthesis, screening, and DMPK studies.

WuXi AppTec and WuXi Biologics together account for manufacturing and testing services embedded in an estimated 25% of US drug supply chains. Their pricing has historically been 30-50% below equivalent US or European CRO capacity, a gap that reflects labor cost arbitrage and Chinese government industrial policy subsidies. If the BIOSECURE Act passes in its current form and virtual biotechs must transition to alternative CROs, two-year transition timelines and 30-40% cost increases are the baseline scenario.

For AI drug discovery companies, this shifts the economic thesis. The cost savings from AI-accelerated preclinical work, which the industry has projected at 25-50% reductions in discovery costs, are partially offset by increased synthesis and testing costs if Chinese CRO access is eliminated. The companies best positioned are those building or contracting domestic automated synthesis capabilities, which reduces per-compound costs through robotics rather than labor arbitrage.

India-based CROs (Syngene, Divi’s Laboratories, Piramal) are the primary beneficiaries of this dynamic and have been actively expanding capacity in anticipation of BIOSECURE-driven demand shifts since 2023.

Why Novartis CEO Vas Narasimhan’s ‘Grounded’ AI Position Reflects Rational Capital Allocation

Novartis has been measured in its AI drug discovery claims relative to peers. CEO Vas Narasimhan has publicly stated that while AI is improving R&D productivity, the “big gains” in discovery are likely five or more years away. Novartis is focused on targeted applications: AI-assisted patient stratification, protocol optimization, and specific chemistry tasks, rather than wholesale platform replacement of discovery teams.

This position reflects a rational analysis of the current state of the technology. Novartis has a deep pipeline with multiple late-stage assets that will generate revenue through the end of the decade regardless of AI productivity gains. The company does not have the same urgency to collapse timelines that a small biotech with a single lead asset does. Paying for a transformational AI platform before efficacy data validates the approach is a capital allocation decision, not just a scientific one.

By contrast, Sanofi’s “all-in” AI strategy, which includes partnerships with Recursion, Formation Bio, and OpenAI, reflects a different competitive position. Sanofi’s pipeline has faced more volatility, and the company is under greater pressure to demonstrate pipeline replacement velocity. The different AI stances of Novartis and Sanofi are not scientific disagreements about whether AI works; they are portfolio management decisions driven by different balance sheet dynamics and competitive timelines.

Key Pipeline Candidates Investors Are Watching Through 2027

Several AI-generated or AI-assisted programs have reached clinical stages that will generate binary events in the next 24 months.

Schrödinger’s SGR-1505, a MALT1 inhibitor for B-cell malignancies including Waldenstrom macroglobulinemia, received FDA Fast Track designation in mid-2025 after initial Phase 1 data showed acceptable safety and preliminary activity. Phase 1 dose escalation is ongoing, with potential Phase 2 initiation in late 2025 or early 2026. Schrödinger designs its molecules using a physics-based free energy perturbation engine combined with machine learning, a hybrid approach that differs from pure deep learning generative models.

Relay Therapeutics’ RLY-2608 is a pan-mutant-selective PI3K alpha inhibitor designed on the Dynamo platform, which integrates AI with molecular dynamics simulations to target conformational flexibility in oncoproteins. RLY-2608 is advancing toward Phase 3 in breast cancer, making it one of the most clinically advanced AI-enabled molecules in oncology. A Phase 3 data readout would represent a decisive test of whether AI-assisted rational design translates to registrational-quality efficacy.

Verge Genomics’ VRG50635 for ALS is notable for a methodological innovation beyond the molecule itself. Verge is using AI-derived digital biomarkers (voice analysis, mobility metrics) as earlier efficacy signals, attempting to detect clinical benefit before traditional endpoint timelines. If validated, this approach could compress Phase 2 decision windows from 24 months to 12, which has direct implications for capital efficiency in rare disease programs.

What Happens to Drug Pricing After AI Compresses Discovery Costs

The standard economic argument that lower R&D costs should reduce drug prices assumes that pharmaceutical pricing is cost-plus. It is not. Drug pricing reflects the value delivered to patients and payers, measured in quality-adjusted life years, cost-effectiveness thresholds, and competitive alternatives, not manufacturing and development costs.

The implication: AI-driven discovery cost reductions will not lower prices for new drugs. They will increase margins for companies that capture the productivity gains and return those gains to shareholders rather than reinvesting them in additional programs. The most likely scenario is that companies use AI savings to run more programs at equivalent per-program cost, increasing shots on goal rather than reducing the price of successful ones.

Where AI does exert downward pressure on drug prices is indirectly, through accelerating the timeline to generic competition. If AI allows generic developers to design around the patent thicket surrounding a branded drug more efficiently, the time from loss of exclusivity to meaningful generic penetration shortens. The same patent landscape analytics that branded companies use to extend exclusivity are available to ANDA filers and Paragraph IV challengers who use them to identify invalidation strategies and design-around chemistry.

How the US-China Biotech Data Race Creates Long-Term IP Risk

China’s position in AI drug discovery is not simply as a CRO services provider. Chinese companies have filed more AI-related drug discovery patents per year than any other country since 2021, according to patent database analyses. State-backed programs have prioritized AI-enabled pharmaceutical innovation as a national technology objective, funding academic centers and commercial programs at a scale that reflects long-term industrial policy rather than near-term commercial returns.

The data sovereignty dimension creates a structural risk for Western pharma companies. If Chinese health data, which covers 1.4 billion patients across a healthcare system that digitized records earlier than many Western countries, becomes available only to Chinese AI drug discovery programs, it creates an asymmetric training data advantage. Models trained on globally diverse patient populations will outperform those trained on primarily Western datasets for predicting drug response in Asian populations, which is already a problem for clinical trial design and drug labeling.

The eventual bifurcation of AI drug discovery technology stacks, with US-aligned companies using US and European models and data sources and Chinese companies using domestic alternatives, will increase development costs for globally registered drugs and potentially slow convergence on best-in-class candidates across therapeutic areas.

Revenue at Risk: The Patent Cliff Math for 2025-2030

The aggregate revenue exposure from major patent expirations over the next five years is the primary commercial context in which every AI drug discovery investment decision sits.

Merck’s Keytruda (pembrolizumab) generated approximately $25 billion in 2024 revenue. Its composition-of-matter patent expires around 2028, with subsequent challenges likely as multiple biosimilar developers including Samsung Bioepis, Celltrion, and Teva have been publicly identified as potential entrants. Merck’s ability to replace Keytruda-scale revenue from internal pipeline programs, several of which are being designed with AI assistance, is the central question in every institutional investor’s Merck model.

Bristol Myers Squibb faces Opdivo (nivolumab) exclusivity pressure on a similar timeline, compounded by the Revlimid (lenalidomide) generic erosion that has already been occurring since 2022. BMS has been aggressive in using AI for next-generation checkpoint inhibitor design, particularly in combination therapy optimization where clinical trial design complexity makes AI-assisted patient stratification commercially valuable.

AstraZeneca’s Imfinzi (durvalumab) and AbbVie’s post-Humira pipeline are in similar positions. The aggregate exposure is in the $150-200 billion range of annual revenue facing generic or biosimilar competition by 2030. Against this backdrop, the AI drug discovery market at $2.6 billion in 2025 is not a large bet. It is an asymmetric hedge.

Why Proprietary Data, Not Algorithms, Is the Actual Competitive Moat

Every major AI drug discovery company uses versions of the same publicly available model architectures. AlphaFold 3 is available to academic researchers. Diffusion models for molecular generation are published in peer-reviewed journals and open-source repositories. The large language model architectures underlying protein sequence analysis are derivations of publicly available transformer models.

What is not available publicly is clean, standardized, proprietary wet-lab data collected at scale under controlled conditions. Recursion’s value proposition is not its algorithms; it is the billions of cellular images it has generated through its automated laboratory infrastructure, each annotated with compound identity, dose, time, and cell type. No competitor can replicate that dataset without building the same physical infrastructure and running it for years.

This data scarcity dynamic also explains why Big Pharma’s historical clinical data vaults have become strategically valuable in ways they were not five years ago. Pfizer’s 30 years of Phase 2 and 3 clinical trial patient-level data is an asset that no AI-native startup can acquire through fundraising. It contains human-biology signals on drug response, biomarker correlation, and toxicity that would cost billions of dollars to regenerate in new trials. The companies that learn to extract prediction value from these vaults will have a durable advantage over startups trained primarily on public databases.

Most Important Ongoing Litigation in AI Drug Discovery IP

The inventorship question is the most active legal frontier in AI pharma IP. The USPTO’s 2024 guidance, affirmed in Federal Circuit decisions, states that AI cannot be a named inventor. This has produced a growing category of patent disputes where the degree of human creative contribution to an AI-assisted drug design is contested.

The practical challenge is that modern generative chemistry workflows blur the line between human direction and algorithmic output. A medicinal chemist who defines the target pocket parameters and selects the top 10 candidates from 10,000 generated structures has clearly contributed inventive activity. A scientist who types “design a TNIK inhibitor” into a generative model and approves the first output has a much weaker inventorship claim. The courts have not yet drawn a bright line between these extremes, and contested patents from AI-first drug discovery programs are beginning to accumulate in PTAB proceedings.

Separately, several major pharma companies have filed patent applications for novel molecules that AI systems generated, naming only human researchers as inventors with varying levels of documented contribution. As these patents move toward potential litigation or IPR challenges, the documentation practices used during the generative design process will determine whether the patents survive. Companies using platforms with comprehensive experiment logging and decision audit trails are better positioned than those relying on informal workflows.

Common Investor Questions

Does AI actually shorten clinical development timelines, or just preclinical?

The demonstrated gains are concentrated in preclinical. Target identification, hit generation, and lead optimization are all faster. Clinical trial design, patient recruitment, and protocol execution are improving but not yet dramatically faster. The FDA and ICH still require the same safety pharmacology studies, toxicology packages, and GMP manufacturing scale-up timelines regardless of how quickly the molecule was designed.

Which therapeutic area benefits most from AI drug discovery?

Oncology, infectious disease, and CNS each offer different profiles. Oncology has the most human genetic validation data, the clearest biomarker infrastructure, and FDA pathways (accelerated approval, breakthrough designation) that allow smaller, faster trials. This makes oncology the highest-probability area for near-term AI drug approvals. CNS is where AI is most needed (the biology is least understood) but also where translation failure risk is highest.

How does AI drug discovery affect generic pharma strategy?

Generic pharma companies use AI for two purposes: designing around branded company patents (to enable earlier ANDA filings or Paragraph IV challenges) and optimizing their own manufacturing processes. The IP design-around use case is growing and directly threatens the ability of branded companies to maintain patent thickets through iterative formulation and device patents.

What is the signal that an AI drug discovery platform is genuinely differentiated vs. marketing?

The most reliable signal is proprietary data generation capacity, not algorithmic claims. A platform that generates its own experimental data at scale, maintains full data lineage from experiment to model training, and has published or presented reproducible validation benchmarks is more credible than one that claims superior algorithms without a clear data advantage.

Does Phase 2a success from a single AI-designed drug validate the entire sector?

No. Insilico’s ISM001-055 Phase 2a result is a genuine milestone. It is one molecule, in one indication, in a trial powered to detect a signal rather than confirm registration-quality efficacy. Phase 3 results across multiple AI-derived molecules in multiple therapeutic areas are required to establish that AI-assisted design systematically improves efficacy prediction.

Key Patent Expiry Dates Relevant to AI-Driven Pipeline Replacement

The following drugs represent primary revenue exposure targets driving AI discovery investment:

Keytruda (pembrolizumab, Merck): Core composition-of-matter patents expire approximately 2028; formulation and combination-use patents may extend effective exclusivity. Multiple Paragraph IV filings anticipated from 2026 onward.

Opdivo (nivolumab, Bristol Myers Squibb): Composition-of-matter expiry approximately 2027-2028 depending on jurisdiction. BMS has filed substantial secondary patents on dosing regimens and combination therapies that will be litigated by biosimilar entrants.

Eliquis (apixaban, BMS/Pfizer): Core US patents expired in 2026 after settlement terms granted Bristol Myers and Pfizer several additional years of market exclusivity from the original expiry date. Generic entry is actively occurring.

Imbruvica (ibrutinib, AbbVie/J&J): Facing both generic competition for the small molecule and a complex patent estate covering multiple cancer indications at different stages of exclusivity.

Dupixent (dupilumab, Regeneron/Sanofi): Biologic; composition-of-matter expiry approximately 2031-2033 depending on patent, with biosimilar development timelines suggesting 2033-2035 market entry at the earliest in the US.

Investment Strategy: How to Position Around AI Drug Discovery’s Current Limitations

The risk-adjusted investment thesis in AI drug discovery requires separating three distinct asset classes that are often conflated in analyst coverage.

The first is pure-play AI platform companies (Recursion, Schrödinger, Relay, Verge). These are effectively pre-revenue biotech companies whose valuation is driven by pipeline probability-of-success assumptions, platform differentiation claims, and cash runway relative to Phase 2 data timelines. They carry binary risk concentrated in Phase 2 efficacy readouts. Investors should model platform value separately from pipeline value, applying significant discount rates to both given the translation gap documented in the REC-994 failure.

The second is Big Pharma companies using AI to improve R&D productivity (Pfizer, Sanofi, Novartis, AstraZeneca). AI adoption within these companies is a margin and pipeline quality story, not a separate asset to value. The relevant metric is whether AI investment is measurable in phase transition success rates or cycle time compression, not in press release partnership announcements.

The third is picks-and-shovels infrastructure plays: computational chemistry software (Schrödinger’s software segment, Certara), data platforms (DrugPatentWatch, Komodo Health), and CRO/CDMO capacity serving AI program synthesis needs (Lonza, Samsung Biologics, LabCorp Drug Development). These carry lower binary event risk than pure-play AI biotechs while capturing sector growth.

The most defensible position currently is overweighting infrastructure and data platforms, maintaining selective exposure to late-stage AI-derived pipeline programs with Phase 2 data due within 12-18 months, and being cautious about platforms with only preclinical validation in complex CNS or inflammatory indications where the translation gap is widest.

Key Takeaways

AI drug discovery has produced its first Phase 2a efficacy validation in a complex chronic disease (Insilico’s ISM001-055 in IPF) and its first high-profile Phase 2 failure (Recursion’s REC-994 in CCM). Both events are informative. The success validates AI’s ability to identify novel targets and design active molecules. The failure defines the boundary of that capability: cellular phenotype prediction does not reliably predict clinical efficacy in heterogeneous human diseases.

The FDA’s January 2025 AI guidance removes regulatory ambiguity but creates documentation requirements that many companies are not currently meeting. Methodological transparency is now a compliance obligation, not a competitive differentiator.

Freedom to operate by design, using patent data as a constraint during molecular generation rather than a checkpoint at lead selection, is the IP management practice that separates operationally sophisticated AI programs from those carrying latent infringement risk.

The BIOSECURE Act creates a material cost and timeline risk for virtual AI biotechs dependent on Chinese CRO infrastructure, with India-based alternatives as the primary transition pathway.

Proprietary data, not algorithms, is where sustainable competitive advantage in AI drug discovery resides. The companies that will lead by 2030 are those currently generating the most informative experimental data, not those with the most sophisticated generative models.

For patent expiry tracking, litigation status monitoring, and AI-compatible patent database access across the global pharmaceutical IP landscape, DrugPatentWatch provides structured data infrastructure for discovery teams, IP counsel, and investment analysts.