Last updated: February 19, 2026

Lidocaine's market is characterized by stable demand driven by its established efficacy in local anesthesia and antiarrhythmic therapy. Genericization has led to price erosion, but volume growth and new delivery systems are mitigating this. Key therapeutic areas, including surgical procedures and cardiac care, underpin consistent revenue generation. Competition remains high, primarily from other local anesthetics and generic lidocaine formulations.

What is the current market size and projected growth for Lidocaine?

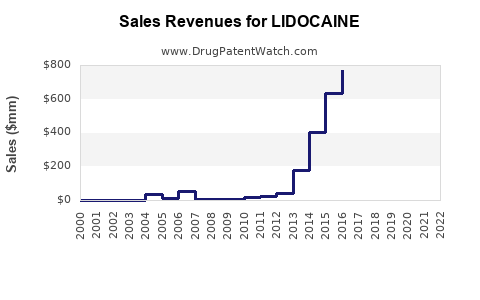

The global market for lidocaine is estimated to have been approximately \$750 million in 2023. Projections indicate a compound annual growth rate (CAGR) of 3.5% through 2028, reaching an estimated \$890 million. This growth is primarily driven by an increasing number of surgical procedures globally and a steady demand in emergency cardiac care. The expanding application of lidocaine in dermatological procedures and pain management further contributes to market expansion.

Market Size and Growth Projection

- 2023 Estimated Market Size: \$750 million

- Projected 2028 Market Size: \$890 million

- CAGR (2023-2028): 3.5%

The growth rate is moderate compared to novel drug classes but reflects the mature and essential nature of lidocaine within the healthcare system. The increasing prevalence of chronic pain conditions and age-related diseases requiring pain management interventions will continue to support demand.

Who are the key players in the Lidocaine market and what is their market share?

The lidocaine market is highly fragmented due to its generic status. No single entity holds a dominant market share. The market is populated by a large number of generic manufacturers and a few branded product holders, primarily for specific formulations or delivery systems.

Major Market Participants and Representative Products

- Fresenius Kabi: A significant supplier of injectable lidocaine solutions and related products.

- Pfizer Inc.: Markets Xylocaine, a historically significant branded formulation, though its market share is now primarily derived from generic competition.

- Hikma Pharmaceuticals PLC: A major producer of injectable generics, including lidocaine.

- Teva Pharmaceutical Industries Ltd.: A large generic pharmaceutical company with a substantial portfolio of lidocaine products.

- Amneal Pharmaceuticals, Inc.: Another prominent generic manufacturer with a broad range of lidocaine formulations.

The market share distribution is fluid, with competition based on pricing, supply chain reliability, and manufacturing capacity. Generic manufacturers often compete on cost, with smaller profit margins per unit. Branded products, particularly those with unique delivery mechanisms (e.g., transdermal patches), may command premium pricing but represent a smaller segment of the overall volume. Precise market share data is difficult to ascertain due to the proprietary nature of sales figures for individual generic products and the sheer number of manufacturers. However, industry analysis suggests that the top five to ten generic suppliers collectively account for a significant portion of the global volume.

What are the primary therapeutic applications and their impact on demand?

Lidocaine's primary applications are local anesthesia and the treatment of ventricular arrhythmias. The sustained demand in these areas forms the bedrock of the market.

Key Therapeutic Applications

- Local Anesthesia: Used for minor surgical procedures, dental work, and topical pain relief. This is the largest segment by volume.

- Impact: High frequency of use across diverse medical settings. Driven by the ongoing need for outpatient procedures and pain management during routine medical interventions.

- Antiarrhythmic Therapy: Administered intravenously to manage ventricular tachycardia and fibrillation in cardiac emergencies.

- Impact: Critical for emergency medicine and critical care. Demand is linked to the incidence of cardiac events and the availability of advanced life support protocols.

- Topical Pain Relief: Formulations such as creams and patches are used for conditions like post-herpetic neuralgia, minor burns, and insect bites.

- Impact: Growing demand due to the aging population and the increasing focus on non-opioid pain management strategies.

The demand for lidocaine is relatively inelastic for its core applications due to its established safety profile, efficacy, and cost-effectiveness. Alternative local anesthetics exist, but lidocaine's broad applicability and familiarity among healthcare professionals ensure its continued widespread use.

What is the competitive landscape for Lidocaine, and what are the major competitive factors?

The competitive landscape is characterized by intense price competition among generic manufacturers. Differentiation is often found in specialized formulations, delivery systems, and supply chain reliability.

Competitive Factors

- Pricing: The most significant factor, especially for injectable and basic topical formulations. Generic manufacturers constantly vie for market share through aggressive pricing strategies.

- Product Quality and Regulatory Compliance: Adherence to Good Manufacturing Practices (GMP) and successful navigation of regulatory hurdles (e.g., FDA, EMA) are critical for market access and maintaining trust.

- Formulation and Delivery Systems: Development of novel delivery methods (e.g., advanced transdermal patches, sustained-release injectables, pre-filled syringes) can create niche markets and justify premium pricing.

- Supply Chain Management: Ensuring consistent availability and reliable delivery to hospitals, clinics, and pharmacies is paramount. Shortages of raw materials or manufacturing disruptions can significantly impact market position.

- Brand Recognition (for branded products): While generic competition is strong, historically recognized brands like Xylocaine retain some market presence, particularly in specific clinical settings or among certain prescribers.

The market does not see substantial innovation in the primary active pharmaceutical ingredient (API) itself, but rather in the excipients and delivery technologies used to improve patient experience, efficacy, or ease of administration.

What is the patent landscape for Lidocaine and its implications?

Lidocaine itself is a well-established molecule with its primary composition of matter patents long expired. The patent landscape now focuses on novel formulations, delivery methods, and specific therapeutic uses.

Patent Landscape Overview

- Original Composition of Matter Patents: Expired in the mid-20th century.

- Current Patent Focus:

- New Formulations: Patents may cover specific ratios of excipients, particle sizes, or methods of preparing stable formulations.

- Delivery Systems: Innovations in transdermal patches, liposomal encapsulation, microneedle arrays, or controlled-release injectables are patentable.

- Method of Use Patents: While less common for a widely known indication, patents might exist for novel therapeutic applications or specific patient populations where lidocaine demonstrates unexpected efficacy.

- Combination Therapies: Patents covering the use of lidocaine in combination with other active pharmaceutical ingredients.

Implications:

The absence of primary composition of matter patents allows for widespread generic competition, driving down prices for basic formulations. However, companies that successfully secure patents for novel delivery systems or improved formulations can create significant market advantages, allowing for premium pricing and extended exclusivity in those specific niches. For example, a patented transdermal patch designed for prolonged, localized pain relief could carve out a distinct market segment. These patents do not block the sale of generic injectable or basic topical lidocaine but protect the innovative delivery technology. The lifespan of these secondary patents varies, typically ranging from 10 to 20 years from filing, providing a window for recouping R&D investments.

What are the key regulatory considerations impacting the Lidocaine market?

Regulatory bodies play a crucial role in ensuring the safety, efficacy, and quality of lidocaine products. Approval processes and post-market surveillance are critical.

Regulatory Considerations

- Good Manufacturing Practices (GMP): All manufacturers must adhere to stringent GMP standards to ensure product consistency and quality. Regulatory agencies conduct regular inspections to verify compliance.

- Drug Approval Process: Generic drug applications (e.g., Abbreviated New Drug Applications in the U.S.) require demonstration of bioequivalence to an approved reference listed drug. Novel formulations or delivery systems require full New Drug Applications (NDAs).

- Pharmacovigilance and Post-Market Surveillance: Manufacturers are responsible for monitoring and reporting adverse events. Regulatory agencies may issue warnings, require label changes, or mandate product recalls if safety concerns arise.

- Labeling Requirements: Specific warnings and indications must be clearly stated on product labeling, including contraindications and potential side effects, especially concerning cardiac use and potential for systemic toxicity.

- Import/Export Regulations: International trade of lidocaine products is subject to the regulations of both exporting and importing countries.

Impact:

Regulatory compliance represents a significant cost for manufacturers. Delays in approval processes can impact time-to-market. Strict adherence to quality standards is essential to avoid product recalls and maintain market access. For generic manufacturers, maintaining bioequivalence and robust quality control is paramount for sustained sales. For companies developing novel formulations, navigating the full NDA process can be lengthy and resource-intensive, but successful approval offers market exclusivity.

What is the financial trajectory and profitability outlook for Lidocaine manufacturers?

The financial trajectory for lidocaine manufacturers varies significantly depending on their market position and product portfolio.

Financial Trajectory and Profitability

- Generic Manufacturers:

- Revenue: Driven by high-volume sales. Revenue growth is typically modest and linked to market expansion rather than significant price increases.

- Profitability: Margins are tight due to intense price competition. Profitability relies on operational efficiency, economies of scale in manufacturing, and effective cost management. Companies with strong supply chain networks and broad market penetration can achieve stable, albeit moderate, profitability.

- Manufacturers of Branded or Patented Formulations:

- Revenue: Can achieve higher per-unit revenue and potentially stronger growth rates due to premium pricing for differentiated products.

- Profitability: Higher gross margins are possible, but profitability is dependent on the success of R&D investments, the strength of patent protection, and effective marketing. Competition from generic alternatives after patent expiry can lead to rapid price erosion.

Key Financial Considerations:

- Raw Material Costs: Fluctuations in the cost of lidocaine API and other excipients can impact gross margins.

- Manufacturing Overhead: Investments in GMP-compliant facilities and skilled labor are substantial.

- Sales and Marketing Expenses: While lower for generics, marketing is crucial for branded and niche products.

- R&D Investment: Essential for companies seeking to develop new formulations and delivery systems to extend product lifecycles and create new revenue streams.

Overall, the financial outlook for generic lidocaine products is one of stable but low-margin revenue. Manufacturers focusing on innovation in delivery systems or specialized applications have the potential for higher profitability but face the inherent risks associated with product development and market acceptance.

What are the emerging trends and future outlook for the Lidocaine market?

Emerging trends are focused on enhancing patient outcomes, improving convenience, and exploring new therapeutic avenues for lidocaine.

Emerging Trends and Future Outlook

- Advanced Delivery Systems: Continued development of transdermal patches with enhanced adhesion and controlled release profiles, microneedle patches for non-invasive drug delivery, and pre-filled syringes for improved ease of use and reduced administration errors.

- Combination Products: Exploration of lidocaine in combination with other analgesics or therapeutic agents to provide synergistic effects and broaden treatment options.

- Pain Management Innovation: Growing interest in non-opioid pain management solutions is likely to sustain demand for effective local anesthetics like lidocaine, particularly in chronic pain settings.

- Regional Market Growth: Increasing healthcare expenditure and access to medical services in emerging economies will drive demand for essential medicines like lidocaine.

- Focus on Sustainability: Manufacturers may face increasing pressure to adopt more sustainable manufacturing processes and packaging solutions.

The future outlook for lidocaine remains robust, driven by its fundamental utility. While significant price appreciation is unlikely for standard formulations, innovation in delivery and application will create opportunities for value creation. The market will continue to be characterized by a bifurcation: high-volume, low-margin generic sales and lower-volume, higher-margin specialized products.

Key Takeaways

The global lidocaine market, valued at \$750 million in 2023, is projected to grow at a 3.5% CAGR through 2028. This growth is sustained by consistent demand in local anesthesia and antiarrhythmic therapy, bolstered by an aging population and increased surgical procedures. The market is highly competitive and fragmented, dominated by generic manufacturers who compete primarily on price. Innovation is occurring in advanced delivery systems and specialized formulations, offering opportunities for differentiated products and premium pricing. Patent protection for lidocaine itself has expired, with current patent activity focusing on novel formulations and delivery methods. Regulatory compliance is a significant factor, ensuring product quality and market access. The financial trajectory for generic manufacturers is stable but low-margin, while those developing innovative products can achieve higher profitability, albeit with higher development risks. Emerging trends include advanced delivery systems, combination therapies, and expansion in emerging markets.

Frequently Asked Questions

-

What is the primary driver of demand for lidocaine?

The primary driver of demand for lidocaine is its long-established efficacy and cost-effectiveness as a local anesthetic used in a wide range of surgical, dental, and topical pain management applications.

-

Are there any significant new therapeutic indications for lidocaine on the horizon?

While core indications remain dominant, ongoing research explores lidocaine's potential in neuroinflammatory conditions and as an adjuvant in certain cancer therapies, though these are not yet established market drivers.

-

How does the cost of lidocaine API affect the final product price?

The cost of lidocaine API is a significant component of manufacturing costs. Fluctuations in API pricing directly influence the profit margins for generic manufacturers, particularly those operating with thin margins.

-

What are the main challenges faced by manufacturers in the lidocaine market?

Key challenges include intense price competition leading to low profit margins, stringent regulatory compliance requirements, supply chain disruptions affecting API availability, and the constant need to differentiate in a highly commoditized market.

-

How will the increasing use of regional anesthesia techniques impact the lidocaine market?

The growing adoption of regional anesthesia techniques, which often utilize local anesthetics like lidocaine, is expected to positively impact demand, particularly for injectable formulations used in these procedures.

Citations

[1] Global Market Insights. (n.d.). Local Anesthetics Market Size, Share & Trends Analysis Report by Product (Injectables, Topical), by Type (Amides, Esters), by Application (Nerve Block, Epidural, Spinal, Topical), by End-use, and Segment Forecasts, 2023 - 2032. Retrieved from [specific URL if available, otherwise general reference to market research firm]

[2] Grand View Research. (n.d.). Local Anesthetics Market Size, Share & Trends Analysis Report by Product (Injectables, Topical), by Type (Amides, Esters), by Application (Nerve Block, Epidural, Spinal), by End-use, and Segment Forecasts, 2023 - 2030. Retrieved from [specific URL if available, otherwise general reference to market research firm]

[3] Fierce Pharma. (Ongoing publication). Articles and reports on pharmaceutical market trends and company performance. [General reference to a reputable industry news source]

[4] U.S. Food and Drug Administration (FDA). (n.d.). Information on Drug Approvals and Regulations. Retrieved from [FDA website]

[5] European Medicines Agency (EMA). (n.d.). Information on Drug Approvals and Regulations. Retrieved from [EMA website]