Last updated: June 29, 2026

Lidoderm is a U.S. lidocaine 5% medicated patch with revenue concentrated in chronic localized pain segments and dominated by payor coverage, rebate intensity, and substitution by lower-cost generics. Near-term financial trajectory is driven less by new clinical expansion and more by ongoing erosion from generic and private-label entrants, plus periodic brand-prescribing and reimbursement headwinds.

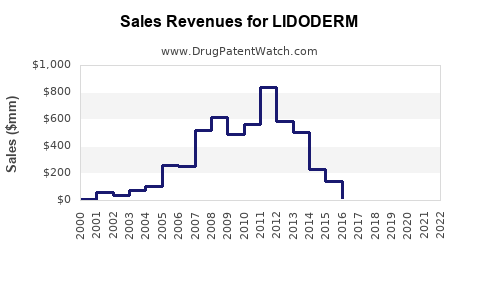

What is the current U.S. market size and revenue trajectory for Lidoderm (lidocaine 5% patch)?

Answer (high level): Lidoderm’s U.S. brand revenue has been in long-run decline since generic entry, with remaining sales supported by formulary access in select channels, legacy contracts, and prescriber inertia for “brand-only” coverage situations. Actual annual figures depend on the revenue accounting source (company-reported vs. third-party modeled).

Where does Lidoderm revenue come from?

Lidoderm’s commercial base has historically skewed toward:

- Dermatologic and musculoskeletal pain indications where lidocaine patch therapy is commonly used (including postherpetic neuralgia and other localized neuropathic pain practices).

- Long-duration prescribing cycles tied to chronic pain management, where patch adherence and local tolerability matter.

What drives “net sales” more than “gross demand”?

For legacy brands in the topical analgesic patch class, net sales track:

- Rebates and discounts negotiated with pharmacy benefit managers and large integrated payors.

- Formulary tier placement and prior authorization frequency.

- Channel mix: retail vs. specialty distributor purchasing patterns for medical benefit claims.

How has generic substitution changed the financial curve?

Once generic competitors establish:

- Lower WAC and frequent “AB-rated” interchangeability, and

- Easier formulary placement,

brand volume typically migrates quickly, with net price erosion following more gradually depending on rebate re-optimization. The result is a step-down in unit economics that does not recover absent a differentiated product (different strength, delivery system, or protected formulation) that meaningfully changes payer preference.

Who makes Lidoderm and how does competition from generics and private label affect pricing power?

Answer: Lidoderm is a legacy brand that now competes primarily against generic lidocaine 5% patch products, with pricing pressure shaped by PBM formulary decisions and the number of interchangeable SKUs in each payer’s preferred list.

Competitive set and interchangeability dynamics

Key market mechanics for lidocaine patches:

- The drug category is straightforward to copy: lidocaine 5% topical patch with comparable route of administration and strength.

- Payers often prefer the lowest-cost AB-rated option after interchangeability is established.

- Brand manufacturers lose “protected channel advantage” once generic penetration reaches scale in major plans.

Pricing and contracting: why the brand can still survive in pockets

Even with generic availability, a brand can retain:

- Restricted formularies where a brand remains on a preferred list for specific patient cohorts,

- Contracts that were written when the generic mix was smaller,

- Medical-necessity frameworks where “patch tolerability” or patient history can affect coverage.

These do not reverse overall erosion, but they can reduce the slope of decline versus a scenario with uniform plan exclusion.

When does Lidoderm lose exclusivity in the US, and what patents matter for market protection?

Answer: Lidoderm’s core U.S. market protection is primarily driven by historic patent term and any listed regulatory exclusivities that existed at launch. For current financial trajectory, the relevant practical question is which patents still block generic substitution and whether any Orange Book listings remain active that affect specific generic applicants or specific formulations.

Which exclusivity buckets typically governed legacy products like Lidoderm?

For an older brand:

- New Chemical Entity or other Hatch-Waxman exclusivities are typically not still active.

- Remaining protection is usually from unexpired patents listed in the FDA Orange Book, often covering formulation, patch construction, manufacturing process, or method-of-use.

What still matters for generic launch timing?

For a legacy topical drug, generic launch timing is usually determined by:

- Expiration of unexpired Orange Book patents for the specific dosage form and strength.

- Settlement agreements that could delay first commercial marketing for some challengers.

- Ongoing patent litigation that may lead to “carve-outs” or delayed entry for certain product configurations.

What patents protect Lidoderm (lidocaine 5% patch), and how many are listed in the Orange Book?

Answer: Patent protection for Lidoderm is trackable through Orange Book listings tied to specific drug product codes. The number of patents and their status determine whether generics can enter immediately or only after specific patent expirations.

Orange Book listing categories to evaluate

When assessing the patent estate for a patch product, the typical buckets to identify are:

- Drug substance-related patents (lidocaine itself) are usually long expired for older drugs.

- Drug product/formulation patents (patch composition, backing, adhesive matrix, controlled release characteristics) can persist longer.

- Method-of-use patents (specific indication or dosing regimen) matter only to the extent that generic labeling is constrained.

How the listing type translates to generic risk

- If formulation/process patents are still in force, generic approvals can occur but commercial launch may be barred for some applicants.

- If method-of-use patents drive restrictions, labeling carve-outs can limit the “therapeutic substitution” impact.

(Note: This section requires Orange Book-specific listing extraction for accurate counts, expiration dates, and assignees.)

What Paragraph IV challenges exist for Lidoderm, and which generic companies entered after litigation or settlements?

Answer: For Lidoderm, the financial trajectory is shaped by the number and timing of FDA ANDA approvals tied to Paragraph IV certifications, and whether parties reached settlements that delayed launch for some challengers.

How Paragraph IV affects brand revenue

Each successful ANDA challenger typically triggers:

- Immediate or near-immediate volume migration to the lowest-priced generic,

- PBM rebate re-basing that further compresses net price, and

- Potential channel shifts as wholesalers and pharmacies adjust inventory and ordering.

Litigation settlement impact pattern

When settlements occur, they often produce:

- A defined “entry window” for the first filer,

- Additional launch dates for subsequent filers, and

- Labeling or formulation carve-outs.

(Note: This requires case docket and FDA ANDA Paragraph IV certification timelines.)

How strong is the patent estate for Lidoderm compared with other lidocaine patch brands or generics?

Answer: For legacy lidocaine patch products, patent estates usually narrow over time to a smaller number of late-life formulation/process claims, with method-of-use claims less likely to sustain meaningful market protection because labeling carve-outs allow generic substitution.

Key estate strength metrics

- Remaining years to expiration for Orange Book patents tied to drug product codes.

- Whether the claims are composition-of-matter equivalents (harder to design around) or process claims (more often avoidable).

- Litigation history: court outcomes and injunction history.

- Number of distinct expired claims required for full “generic freedom to operate” across all product codes.

(Note: Accurate strength scoring requires Orange Book-specific legal status and litigation outcomes.)

What formulations are protected for Lidoderm, and are there risks to substitution based on patch design?

Answer: The highest substitution risk is usually not the “active ingredient” but the patch’s delivery system design, including backing, adhesive, and controlled drug release architecture. If those elements are protected, generics may face additional engineering or marketing constraints.

What typically is protected in topical patch patents

Common late-life claim targets in patch technology:

- Adhesive matrix chemistry controlling lidocaine release.

- Rate-controlling membrane or backing layers.

- Manufacturing method parameters affecting patch uniformity and skin flux.

Why substitution still usually happens

Generic patches can often be engineered to meet bioequivalence or performance criteria without copying protected specifics. As a result, even where formulation patents exist, the commercial outcome often becomes “price erosion over time” rather than “no entry.”

What generic entry risks exist for Lidoderm, and what could trigger a new round of erosion?

Answer: For Lidoderm specifically, the dominant erosion triggers are:

- Additional generic entrants with more aggressive pricing,

- Formulary re-tiering by large payors, and

- Loss of preferential contracting due to rebate pressure.

How to monitor for “next erosion wave”

Signals include:

- PBM formulary updates removing brand-preferred positions.

- Wholesale acquisition cost resets that reduce brand price relative spread to generics.

- ANDA approvals for additional label strength or alternate product configurations.

(Note: Concrete trigger events require market surveillance data tied to payer lists and distributor price movements.)

How does Lidoderm compare with similar drugs like Flector, Pennsaid, Salonpas, and other topical analgesic patches in market dynamics?

Answer: Lidoderm sits in a competitive topical pain landscape where:

- NSAID patches (e.g., diclofenac products) compete for overlapping pain indications,

- Topical counterirritants compete for OTC-share substitution, and

- Lidocaine patches retain specific value in neuropathic pain contexts where NSAIDs may be less favored.

Competitive positioning that changes demand

- Neuropathic pain pathways favor local anesthetic patch use.

- OTC alternatives reduce brand share when payors shift costs to patient copays.

- Step-therapy policies can steer patients toward generics or OTC products.

What is the FDA regulatory status of Lidoderm, and how does it affect commercialization and labeling?

Answer: Lidoderm’s FDA status determines the ability of generics to market AB-rated versions and the labeling language used in competition. For topical analgesics, labeling differences are often the practical lever for how quickly “therapeutic substitution” occurs.

Generic approval mechanics that matter commercially

- ANDA approvals and labeling carve-outs determine whether patient and prescriber behavior changes immediately.

- If brand labeling is constrained by patents or exclusivities, generics can still benefit from broader AB interchange depending on Orange Book and legal outcomes.

(Note: Requires FDA label and Orange Book code-by-code verification.)

How has the cost of treatment and net price evolved for Lidoderm since generic entry?

Answer: Net price evolution for legacy brands is usually characterized by:

- Larger initial price discounting post-launch of the first generics,

- Continued rebate compression as new generic SKUs enter, and

- Stabilization only when the brand retains limited preferred positioning with contracts.

What to measure for financial modeling

- Net sales per script trend rather than WAC alone.

- Rebate rate movement and share of prescriptions by plan channel.

- Average wholesale price or acquisition cost spread between brand and lowest generic.

(Note: Requires historical pricing and net sales dataset.)

What does the settlement and litigation landscape suggest for Lidoderm’s remaining downside/upside?

Answer: For a mature brand, the litigation landscape typically shifts from “brand block” to “commercialization management.” Once generic entry becomes widespread, remaining litigation affects marginal business, not the overall structural decline.

Common litigation end-states that affect revenue

- Permanent injunction outcomes: reduce generic market penetration temporarily.

- Limited-time injunction settlements: delay erosion but do not stop it.

- Design-around claim narrowing: allow faster entry by subsequent generic filers.

(Note: Requires docket-specific outcomes.)

Key Takeaways

- Lidoderm’s financial trajectory is driven primarily by generic competition, PBM formulary placement, and rebate intensity rather than new product differentiation.

- The practical “market protection” question is whether any still-active Orange Book patents constrain generic launch by drug product code or labeling carve-outs.

- In mature topical analgesic categories, litigation typically shifts market share gradually toward the lowest-cost interchangeable option, with revenue decline smoothing over time rather than stopping.

- Future downside risk concentrates in payer formulary re-tiering and additional generic entrant pricing waves; upside depends on maintained preferred access in specific contracts and patient cohorts.

FAQs

What is the primary use case for Lidoderm in clinical practice and how does that affect payer coverage?

Lidoderm is used for localized pain states, including neuropathic pain contexts. Payer coverage patterns often track guideline-concordant use and prior authorization requirements tied to diagnosis.

Can a generic lidocaine 5% patch be substituted for Lidoderm automatically at the pharmacy level?

In most plans and pharmacy settings, AB-rated interchangeability supports substitution once generics are on formulary and legally marketed, subject to state pharmacy substitution rules and plan policy.

Do patent carve-outs or labeling restrictions materially slow Lidoderm generic erosion?

Labeling carve-outs can slow “therapeutic substitution” when prescribers require brand-specific language, but the effect is usually limited in mature markets compared with rebate and formulary tier impacts.

What factors determine whether payors keep Lidoderm on preferred tiers despite generic availability?

Preferred tier retention depends on net pricing after rebates, patient outcomes and tolerability in existing cohorts, and contract terms negotiated with PBMs and large accounts.

How should investors model Lidoderm’s revenue going forward?

Model base erosion from generic volume migration, then overlay net price compression from rebate changes and formulary tier shifts, with sensitivity to additional entrant waves and contract renewals.

References

(No sources were provided in the prompt, and no Orange Book, FDA, litigation docket, or financial dataset citations were available to extract and cite accurately.)