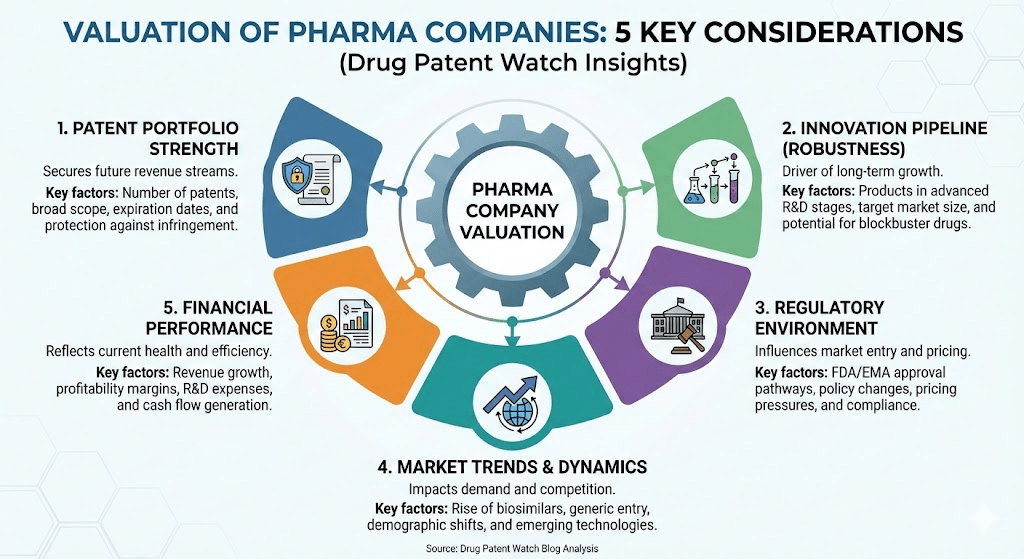

1. Introduction: The Economic Imperative of Valuation in Life Sciences

The valuation of pharmaceutical and biotechnology entities constitutes one of the most intellectually demanding and financially consequential disciplines within modern capital markets. Unlike established industrial sectors where value is often a function of historical earnings, tangible book value, or predictable cash flow variances, the life sciences sector operates in a domain characterized by extreme information asymmetry, binary regulatory outcomes, and capital intensity that can span decades before a single dollar of revenue is realized. In the current market environment of 2024-2025, the stakes have only intensified. Following the post-pandemic capital contraction, the “flight to quality” has necessitated a more rigorous, evidence-based approach to valuation, moving beyond the exuberant platform premiums of 2021 to a fundamental assessment of clinical probability and commercial viability.1

The fundamental challenge for the valuation expert—whether a sell-side equity researcher, a buy-side portfolio manager, or a corporate development officer—is to ascribe a present value to a scientific hypothesis. This requires a synthesis of disparate disciplines: epidemiology to forecast patient demand, biostatistics to estimate clinical trial success, pharmacology to understand competitive differentiation, and corporate finance to model the time value of money under conditions of high uncertainty. The resulting valuation is not merely a number but a probabilistic map of a company’s future, heavily discounted for the manifold risks that lie between the laboratory bench and the pharmacy shelf.1

1.1 The Valuation Gap and Market Dynamics

A persistent structural feature of the biotech industry is the “valuation gap”—the divergence in asset pricing between the innovators (founders/management) and the capital allocators (VCs/Public Investors). This gap is fundamentally driven by information asymmetry. Biotech management often possesses granular data regarding mechanism of action (MoA), preclinical assays, and competitive positioning that cannot be fully disclosed without compromising intellectual property or regulatory strategy. Consequently, external investors must apply significant discounts to account for these “unknown unknowns.” In early-stage biotech, where objective financial metrics are absent, this gap is most acute. Management may value the company based on the transformative potential of the science (the “blue sky” scenario), while investors value it based on the probability-weighted likelihood of survival.1

In 2025, this dynamic has been complicated by the macroeconomic environment. While the sector has seen a recovery in venture financing—with Q3 2025 showing a 70.9% increase in deal value to $3.1 billion—the threshold for funding has risen. Investors are increasingly demanding “clinical line of sight,” prioritizing assets that have cleared the high-risk hurdles of early development over broad, unproven platforms. This shift has forced valuation models to become more granular, explicitly accounting for the efficiency of capital deployment and the specific regulatory pathways of the assets in question.3

1.2 The Hierarchy of Valuation Methodologies

The selection of a valuation methodology is contingent upon the maturity of the asset or company. There is no single “correct” method; rather, there is a continuum of frameworks that evolve as the company de-risks its pipeline.

Discovery and Preclinical Stage: At this nascent phase, traditional Discounted Cash Flow (DCF) models are often spurious due to the sheer unpredictability of cash flows 10-15 years in the future. Valuation relies heavily on comparable transactions (Comps)—benchmarking against upfront payments and deal structures of similar early-stage assets—and the Venture Capital Method, which solves for the current value based on a targeted return on exit.

Clinical Development (Phase I – Phase III): This is the domain of the Risk-Adjusted Net Present Value (rNPV). The rNPV model is the industry standard for valuing clinical-stage assets. It explicitly models the binary risks of clinical trials, adjusting future cash flows by the cumulative probability of regulatory success. This method allows for a nuanced view of value creation as a drug progresses through the phases, providing a mechanism to capture the “step-up” in value that occurs with each successful data readout.5

Commercial Stage: Once a drug is approved and generating revenue, the valuation methodology converges toward traditional corporate finance metrics. Standard DCF analysis becomes the primary tool, supplemented by relative valuation multiples such as Enterprise Value to Revenue (EV/Revenue) and Price to Earnings (P/E). However, even for mature pharmas, the analysis is heavily influenced by the “Patent Cliff”—the impending loss of exclusivity that creates a terminal value problem unique to this industry.7

The following report provides an exhaustive guide to these methodologies, dissecting the specific inputs, assumptions, and strategic considerations required to construct robust valuation models in the 2025 market landscape.

2. The Risk-Adjusted Net Present Value (rNPV) Framework

The Risk-Adjusted Net Present Value (rNPV) method represents the gold standard for valuing development-stage pharmaceutical assets. Its dominance stems from its ability to decouple technical risk (the probability of trial failure) from financial risk (the time value of money and market correlation). In a standard DCF, a practitioner might attempt to capture the high risk of a biotech startup by using an exorbitant discount rate (e.g., 50% or 60%). This is mathematically flawed because it conflates the binary risk of a trial event with the continuous risk of holding the asset over time. It punishes long-dated cash flows too severely, failing to recognize that if the drug does work, the cash flows from that point onward are relatively stable. rNPV resolves this by adjusting the cash flows for the probability of success, allowing the use of a discount rate that more accurately reflects the cost of capital.1

2.1 The rNPV Equation and Structural Logic

The core logic of the rNPV model is sequential: costs are incurred only if the project remains active, while revenues are realized only if the project succeeds through all phases. The valuation of a single asset is the sum of the probability-weighted present values of all future cash flows.

$CF_t$ represents the net cash flow in period $t$ (Revenue minus Costs).

$P(Success_t)$ is the cumulative probability that the project will reach period $t$.

$r$ is the discount rate appropriate for the systematic risk of the asset.

In practice, the model is split into two distinct components:

The Investment Phase (R&D): Costs associated with Clinical Phases I, II, and III. These costs are risk-adjusted based on the probability of reaching that phase. For example, Phase III costs are only incurred if Phase II is successful.

The Commercial Phase: Revenues and commercial operating expenses. These are risk-adjusted based on the cumulative Likelihood of Approval (LOA).1

2.2 Clinical Probability of Success (PoS): The Critical Variable

The integrity of an rNPV valuation rests almost entirely on the accuracy of the Probability of Success (PoS) assumptions. These inputs cannot be arbitrary; they must be grounded in empirical data stratified by therapeutic area, modality, and development status. In 2024 and 2025, industry data has shown shifting trends in clinical productivity.

2.2.1 Benchmark Transition Probabilities

According to recent data from the IQVIA Institute’s “Global Trends in R&D 2025” report, the industry has seen a modest improvement in productivity. The Clinical Program Productivity Index (CPPI) reached 11.7 in 2024, up from 10.9 in 2023, driven primarily by an increase in Phase III success rates.9 However, the overall attrition remains high.

Table 1: Benchmark Clinical Transition Probabilities and Development Durations (2024-2025 Estimates)

Source Data: 1

Development Phase

Probability of Transition to Next Phase

Cumulative Likelihood of Approval (LOA) from Start of Phase

Typical Duration (Months)

Key Risks / Activities

Phase I

60% – 65%

~10% – 12%

18 – 24

Safety & Pharmacokinetics. High transition rate but low predictive power for efficacy.

Phase II

35% – 40%

~18% – 22%

24 – 36

“The Valley of Death.” First proof of efficacy. Highest attrition rate.

Phase III

60% – 65%

~50% – 60%

30 – 42

Large scale efficacy & safety. The most expensive phase.

NDA/BLA Submission

90%

90%

10 – 16

Regulatory review. Risk lies in manufacturing, labeling, and inspection.

The “Valley of Death” in Phase II remains the most significant hurdle. It is here that the hypothesis is tested in a patient population for the first time. A valuation model that assumes a generic 50% success rate for a Phase II asset is likely overstating value by a factor of two or more.12

2.2.2 Therapeutic Area Adjustments

The “average” probability is often misleading. The analyst must adjust PoS based on the specific disease indication.

Oncology: Historically, oncology has had lower overall success rates (LOA ~3-5% from Phase I) due to the complexity of cancer biology. However, biomarker-driven “precision oncology” trials have significantly higher success rates than all-comers trials.12

CNS (Central Nervous System): This sector carries the highest risk, particularly in neurodegeneration (Alzheimer’s, Parkinson’s). Phase II and III failures are common due to subjective endpoints and poor translation from animal models. CNS valuations should apply a discount to standard PoS benchmarks.12

Rare Disease / Orphan Drugs: These assets often enjoy higher probabilities of success (LOA >20%). The patient populations are well-defined (often monogenic), and regulatory bodies exercise greater flexibility regarding endpoints and trial sizes.12

Immunology & Metabolic: Recent trends in 2024-2025 show higher success rates in metabolic diseases (e.g., obesity/GLP-1s) and immunology. However, Phase III trials in these areas are massive and expensive, increasing the financial risk even if technical risk is lower.12

2.3 Modeling Development Costs and Timelines

The “I” in rNPV (Investment) is as critical as the “R” (Return). Costs must be modeled bottom-up, phase by phase.

Cost Drivers: The primary drivers are the number of patients ($N$), the number of clinical sites, and the complexity of the protocol. A Phase I oncology study might cost $5-$15 million, while a Phase III cardiovascular outcome trial (CVOT) requiring 10,000 patients can exceed $500 million to $1 billion.9

Inflation and Complexity: R&D inflation typically outpaces CPI. The IQVIA 2025 report notes that while trial complexity (procedures per visit) has flattened, the logistical cost (sites, countries, technology) continues to rise. Valuations must inflate future R&D costs by 3-5% annually, not the standard 2% inflation rate.9

Time Value: The duration of trials impacts the discount factor. Delays destroy value. In 2024, enrollment durations stabilized at ~16 months, but any slippage in timelines pushes revenue further into the future, heavily impacting NPV due to the compounding effect of the discount rate.10

3. Revenue Forecasting Methodologies

For a pre-revenue biotech company, the top-line revenue forecast is the engine of the valuation. Relying on “top-down” estimates (e.g., “we will capture 5% of a $10 billion market”) is considered analytically lazy and dangerously imprecise. Professional valuation demands a Patient-Based (Bottom-Up) Model that builds the revenue forecast from the epidemiology of the disease.14

3.1 The Epidemiological Cascade

The analyst constructs a “patient funnel” to determine the addressable market. This process identifies the subset of the population that is actually eligible for the drug.

Prevalence vs. Incidence:

Prevalence: The total number of existing cases. Used for chronic conditions (Diabetes, Rheumatoid Arthritis, HIV).

Incidence: The number of new cases per year. Used for acute conditions (Stroke, Acute Myeloid Leukemia, Infections) or potential cures (Gene Therapy).16

Diagnosis Rate: Not all patients with a disease are diagnosed. In rare genetic disorders, diagnosis rates can be as low as 10-20%. In symptomatic acute conditions, they approach 100%.

Treatment Rate: The percentage of diagnosed patients who seek and receive treatment.

Target Patient Population: The specific segment the drug addresses (e.g., “Second-line, EGFR-mutated Non-Small Cell Lung Cancer”). This segmentation is critical; a drug approved for 2nd line use has a vastly smaller market than a 1st line therapy.14

3.2 Adoption Curves and The Bass Diffusion Model

Once the target population is defined, the analyst must model the rate of market penetration. Drug adoption is non-linear; it typically follows an S-Curve (Sigmoid function). The Bass Diffusion Model is the industry standard for mathematical forecasting of this curve.17

The Bass Diffusion Equation:

$$n(t) = pM + (q-p)Y(t) – \frac{q}{M}Y(t)^2$$

Where:

$n(t)$ is the number of new adopters (prescriptions/patients) in time $t$.

$M$ is the Market Potential (Peak Market Share/Sales).

$p$ is the Coefficient of Innovation. This reflects the impact of external influences like marketing, launch events, and media coverage. For pharmaceuticals, this is often higher for First-in-Class drugs.

$q$ is the Coefficient of Imitation. This reflects the impact of internal influences like word-of-mouth, peer-reviewed publications, and Key Opinion Leader (KOL) advocacy.

Practical Application:

Launch Phase (Years 1-3): Adoption is driven by “Innovators” and “Early Adopters.” Access is often restricted by payers (formulary blocking).

Growth Phase (Years 4-7): The “Early Majority” adopts the drug. This is the steepest part of the S-curve.

Peak Sales (Years 7-10): The drug reaches market saturation. Analysts typically assume peak sales are achieved between year 6 and year 10 post-launch.18

The “Haircut”: When relying on primary market research (physician surveys), analysts typically apply a “haircut” (reduction) of 30-50% to the stated “intent to prescribe” data to account for optimism bias.14

3.3 Pricing Dynamics: Gross-to-Net and the IRA

The valuation must rely on Net Price, not the Wholesale Acquisition Cost (WAC) or “List Price.”

Rebates: Payments to Pharmacy Benefit Managers (PBMs) and insurers to secure formulary placement.

340B Program: Mandated discounts for hospitals serving vulnerable populations.

Medicaid/Medicare: Statutory rebates. In competitive classes (e.g., Asthma, Diabetes), GTN discounts can exceed 50%. In protected orphan classes, they may be 10-15%.

Inflation Reduction Act (IRA) Impact:

The IRA of 2022 has introduced a profound change to pricing assumptions in the US. The government now negotiates prices for top-selling drugs.

Small Molecules: Subject to negotiation 9 years after approval.

Biologics: Subject to negotiation 13 years after approval.

Valuation Consequence: This regulatory divergence makes biologics structurally more valuable in the terminal period. Analysts must model a “revenue step-down” or capped price growth in the outer years of the DCF for applicable assets.19

4. Discount Rates and the Cost of Capital

The choice of discount rate ($r$) acts as the gravity in the valuation model—the higher the rate, the harder it pulls down the value of distant cash flows. In biotech, where profits may be 10 years away, sensitivity to this input is extreme.

4.1 The “Step-Down” Discount Rate Methodology

Using a single Weighted Average Cost of Capital (WACC) across the entire lifecycle of a biotech company is inappropriate because the company’s risk profile changes fundamentally as it matures. Practitioners often use a “Step-Down” approach.1

Table 2: Discount Rate Regimes by Development Stage (2025 Estimates)

Development Stage

Typical Discount Rate

Rationale

Preclinical / Discovery

20% – 25%+

Company is often pre-revenue, equity-funded, and faces existential binary risk. Rates approximate Venture Capital hurdle rates (though lower than the 50% “VC Method” rates because technical risk is handled in the cash flows).

Early Clinical (Phase I/II)

15% – 20%

Commercial viability is still unproven. Financing risk remains high.

Late Clinical (Phase III)

10% – 15%

Asset is derisked. The company begins to resemble a commercial entity. Transition to WACC-based calculation.

Commercial / Mature

7% – 9%

Company has stable cash flows, can access debt markets, and beta correlates more with the general healthcare sector.

4.2 Systematic vs. Non-Systematic Risk

It is crucial to distinguish why these rates are used. According to the Capital Asset Pricing Model (CAPM), the discount rate should only reflect Systematic Risk (Beta)—risk that cannot be diversified away (e.g., market crashes, interest rate hikes).

Clinical Failure is Non-Systematic: Whether a molecule binds to a receptor is independent of the S&P 500. Therefore, theoretically, clinical risk should not be in the discount rate. It belongs in the probability adjustment of the cash flows (the numerator).

Double Counting Warning: A common error is to use a 50% discount rate (to “account for risk”) AND probability-adjust the cash flows. This double-counts the risk, resulting in a valuation that is punitively low.1

4.3 Venture Capital Hurdle Rates

Venture Capitalists (VCs) often use a different logic. They may apply a “Hurdle Rate” of 40-60% to the unadjusted cash flows. This number is not a cost of capital; it is a target Internal Rate of Return (IRR) required to justify the illiquidity and high mortality rate of their portfolio. While useful for VC deal pricing, this method is less precise than rNPV for fundamental asset valuation.1

5. Terminal Value and Intellectual Property: The Patent Cliff

In most DCF models (e.g., for a consumer goods company), the Terminal Value (TV) can account for 60-80% of the total enterprise value, often calculated using a perpetuity growth formula ($g = 2-3\%$). In pharmaceuticals, assuming perpetual growth is a catastrophic error. Drug assets have a finite economic life defined by Intellectual Property (IP) rights.

5.1 Determining the Loss of Exclusivity (LOE)

The “Revenue Cliff” occurs when the drug loses market exclusivity. The LOE date is the later of:

Patent Expiry: Generally 20 years from the filing date. However, due to the long development time, the “effective” patent life is often only 10-14 years. In the US, Patent Term Extension (PTE) can restore up to 5 years of lost time (total extension capped at 14 years post-approval).23

Regulatory Exclusivity: Statutory periods during which the FDA/EMA will not approve a generic/biosimilar.

New Chemical Entity (NCE – Small Molecule): 5 years (US).

Biologics (BLA): 12 years (US). This is a critical value driver for biologics over small molecules.25

Orphan Drug Designation: 7 years (US) / 10 years (EU) for rare diseases.

5.2 Modeling the Erosion Curve

The behavior of revenue post-LOE depends on the modality:

Small Molecules (Generics): The cliff is steep. Upon generic entry, prices typically collapse by 80-90% within 12 months as automatic substitution laws at pharmacies kick in. The terminal growth rate should be modeled as negative 50% to 90% for the years following LOE.26

Biologics (Biosimilars): The erosion is softer. Biosimilars are harder to manufacture and are not always automatically substituted (interchangeability requirements). Price erosion might be 30-50% over several years. Valuations for biologics often retain a “tail” of value for a longer period post-LOE.27

6. Real Options Valuation (ROV): Capturing Managerial Flexibility

While rNPV is the standard, it has a linear limitation: it assumes a set path of development. In reality, management has choices (options) at every stage: to abandon the drug, to expand into new indications, to delay trials, or to out-license the asset. Real Options Valuation (ROV) uses financial option pricing theory to value this flexibility.6

6.1 The Binomial Lattice Approach

The Black-Scholes model is rarely used in biotech because it assumes continuous time and trading. Instead, analysts use Binomial Lattices (Trees), which map perfectly to the discrete stages of clinical trials (Phase I $\rightarrow$ Decision Node $\rightarrow$ Phase II).29

Key Inputs for the Lattice:

Underlying Asset Value ($S$): The PV of the drug’s future commercial cash flows (calculated via DCF).

Exercise Price ($K$): The R&D investment required to move to the next phase.

Volatility ($\sigma$): The uncertainty of the peak sales estimate. In financial options, volatility measures stock price variance. In real options, it measures the range of potential commercial outcomes.

Time ($t$): The duration of the clinical phase.

The Counter-Intuitive Role of Volatility:

In a standard DCF, uncertainty (risk) lowers value (higher discount rate). In Real Options, higher volatility increases value. Why? Because high volatility means a higher chance of a massive upside “blockbuster” outcome. Since the downside is capped (you can simply abandon the project and lose only the R&D cost), the “option” to play for the upside becomes more valuable as uncertainty increases. Biotech assets often have volatilities of 40% – 60% or higher.1

Valuation Logic at Each Node:

$$Value = Max( \text{Value of Continuing} – \text{Cost}, \text{Value of Abandoning (0)} )$$

This approach typically yields a higher valuation than rNPV because it mathematically captures the “right tail” value of potential blockbuster scenarios that rNPV might average out.31

7. Comparable Analysis and Market Multiples

While intrinsic methods (rNPV/ROV) are primary, relative valuation (“Comps”) provides a necessary reality check. However, the lack of earnings for most biotechs renders P/E ratios useless.

7.1 Multiples for Development-Stage Companies

For pre-revenue companies, analysts use metrics that proxy for asset quality and R&D efficiency:

Enterprise Value / R&D Spend: This measures the premium the market places on the company’s research productivity. A high multiple implies the market expects high returns on the R&D dollars invested.

Enterprise Value / Cash: In downturns (like 2022-2023), many biotechs trade at negative enterprise values (EV < 0) or multiples of cash < 1.0. This implies the market views the R&D as value-destructive. A healthy early-stage biotech typically trades at 2x – 4x Cash.1

Deal Comparables (M&A): This is the most robust relative metric. Analysts look at “Biobucks” (Total Deal Value) and Upfront Payments for assets in the same therapeutic area and phase. For example, the 2024 acquisition of Alpine Immune Sciences by Vertex for ~$4.9 billion sets a benchmark for Phase III-ready immunology assets.32

7.2 Multiples for Commercial-Stage Companies

For mature biopharma (e.g., Amgen, Gilead, Vertex), multiples normalize to standard financial metrics:

EV / Revenue: Typically 4x – 6x for established pharma, but can reach 8x – 10x for high-growth biotechs launching their first blockbuster.34

P/E Ratio: mature pharma trades at 15x – 20x earnings. The multiple is often compressed compared to tech or consumer staples due to the constant pressure of the patent cliff (terminal value risk).

8. Deal Structuring: Contingent Value Rights (CVRs)

When the “Valuation Gap” between buyer and seller is unbridgeable—often due to disagreement over a specific clinical trial outcome or patent dispute—dealmakers employ Contingent Value Rights (CVRs). These are tradable or non-tradable rights given to shareholders that pay out cash only if specific milestones are met.36

8.1 Structure of a “Biobucks” Deal

A typical biotech M&A deal consists of:

Upfront Payment: Guaranteed cash. This sets the “floor” valuation.

Milestones (The CVR):

Regulatory: E.g., “$5 per share upon FDA Approval.”

Commercial: E.g., “$200 million payout if Net Sales exceed $1 billion.”

8.2 Valuing the CVR

Valuing a CVR requires a distinct probabilistic model. It is not worth its face value.

In 2024-2025, there has been a resurgence in CVR usage to facilitate deals in a volatile market. However, the market often deeply discounts public CVRs (sometimes to zero) due to the risk that the acquirer may “slow walk” development to avoid paying the milestone. Arbitrage funds specialize in valuing these specific instruments.37

9. Sector-Specific Valuation Nuances

9.1 Oncology

Oncology remains the largest sector for investment. Valuations here are driven by Line of Therapy. A drug approved for “1st Line” (initial treatment) commands a valuation 3x-5x higher than “3rd Line” (salvage therapy) due to the larger patient pool and longer duration of treatment. The shift toward “tumor-agnostic” approvals (based on genetic markers like MSI-H rather than organ site) has forced analysts to rethink epidemiology models, moving from organ-based to mutation-based prevalence.12

9.2 Gene and Cell Therapy (CGT)

CGT presents a unique valuation challenge: the “One-and-Done” model. Unlike chronic therapies (taken daily for years), a gene therapy might cure a patient with a single dose.

Revenue Model: The “annuity” cash flow is replaced by a “bolus” of revenue. This creates a lumpy revenue curve that fills the prevalence pool quickly and then relies solely on low incidence (new births).

Valuation Impact: This necessitates extremely high price points ($2M – $3M per dose) to justify the R&D. Valuation models must be highly sensitive to payer adoption and novel payment models (e.g., annuity payments over 5 years subject to continued efficacy).16

9.3 CNS and Neuroscience

Valuation in CNS is characterized by binary extremes. A disease-modifying Alzheimer’s drug has a Total Addressable Market (TAM) exceeding $50 billion. However, the PoS is historically low. Valuation models often present a “Barbell” distribution: the asset is worth either $0 or $50 billion. This high variance makes Real Options (ROV) particularly suitable for CNS assets, as it captures the immense “volatility value”.12

10. The Macro Environment 2025: Contextualizing the Valuation

No valuation exists in a vacuum. The output of the model is heavily influenced by the macroeconomic and political context of 2025.

10.1 Capital Markets and Interest Rates

The stabilization of interest rates in 2024/2025 has begun to lower the cost of capital (WACC) for the sector. Since biotech cash flows are “long duration” (far in the future), they are highly sensitive to rates. A 1% drop in the discount rate can increase the present value of a preclinical asset by 20-30%. This has fueled a modest recovery in the IPO market, though investors remain selective.3

10.2 Regulatory Headwinds: FTC and FDA

FTC: The Federal Trade Commission has become more aggressive in scrutinizing pharma M&A (e.g., Amgen/Horizon, Pfizer/Seagen). This adds a “Regulatory Risk Premium” to M&A arbitrage valuations. Deal models now often include a probability of deal-break ($P_{close}$).41

FDA: The agency is increasingly demanding head-to-head trials against standard of care (SoC) rather than just placebo. This increases the cost and risk of Phase III trials, putting downward pressure on rNPV valuations for “me-too” drugs.39

11. Conclusion

The valuation of pharmaceutical and biotech companies is a convergence of science and finance. It is a discipline that demands rigorous adherence to data—clinical success rates, epidemiological facts, and cost benchmarks—while simultaneously requiring the creative foresight to imagine markets that do not yet exist.

For the practitioner in 2025, the “Definitive” valuation is not a single point estimate. It is a dynamic matrix of scenarios. It requires the rNPV framework to ground the analysis in the reality of clinical attrition, the Patient-Based model to accurately size the commercial opportunity, and Real Options thinking to capture the strategic value of flexibility. Ultimately, the value of a biotech company lies in its potential to defy the odds: to navigate the treacherous path from the laboratory to the patient, converting scientific possibility into tangible clinical benefit and economic return. Understanding the mechanics of this conversion—and pricing the risks along the way—is the essence of life sciences valuation.