Pharma IP teams, hedge funds, and biosimilar developers treat a Paragraph IV filing as a legal event. It is not. It is the opening move of a multi-front capital war, and the companies that treat it as anything less tend to lose it in ways they never anticipated.

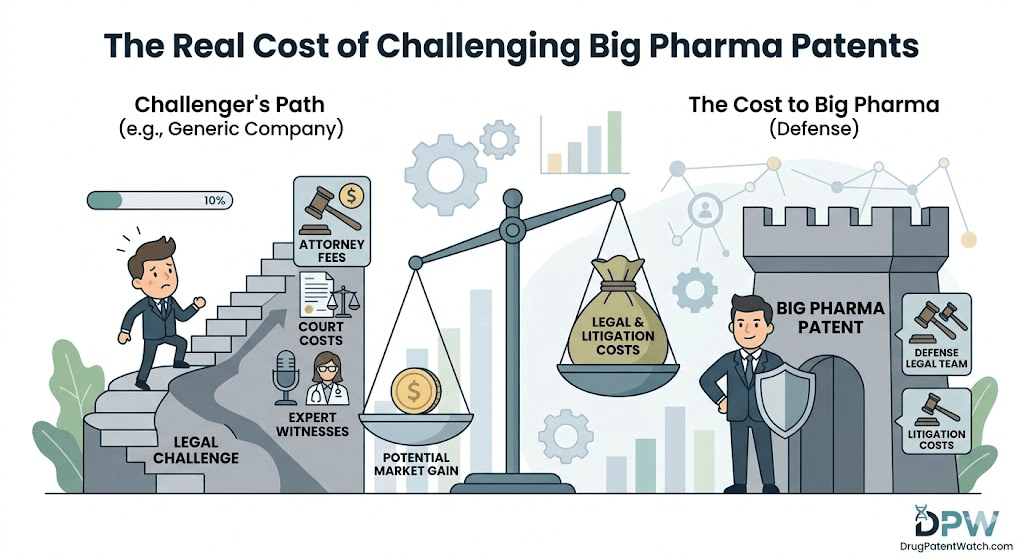

The asymmetry is brutal. The average brand-name company’s financial stake in a PIV case runs to approximately $4.3 billion in revenue it is defending. The average generic challenger’s upside is roughly $204.3 million. That ratio explains nearly every strategic decision an incumbent makes: the nine-figure legal budgets, the 100-patent thickets, the authorized generic threats deployed at the moment of maximum pain. The brand is not litigating to win in court. It is litigating to make winning unprofitable.

This article maps the full risk architecture of a pharmaceutical patent challenge: the Hatch-Waxman mechanics that set the battlefield geometry, the direct and indirect financial exposures, the incumbent’s operational retaliation playbook, the antitrust minefield embedded in settlement, and the competitive intelligence infrastructure required to survive all of it.

How the Hatch-Waxman Framework Creates the Battle Lines

Why the 1984 Compromise Still Drives Modern Patent Wars

The Drug Price Competition and Patent Term Restoration Act of 1984 was built around a deliberate tension. Congress wanted lower-cost generics on the market faster. It also wanted to preserve the financial logic of drug development, where a single approved compound must recoup the cost of the thousands that failed before it. The Abbreviated New Drug Application pathway resolved the first goal. Patent Term Extension and regulatory exclusivity addressed the second. The collision between them is where modern pharma IP litigation lives.

The ANDA mechanism eliminated the requirement that generic manufacturers run their own clinical trials. A generic applicant need only prove bioequivalence to the reference listed drug (RLD) and satisfy the relevant patent certifications. The safe harbor at 35 U.S.C. § 271(e)(1) protects the bioequivalence testing work itself from infringement claims, which is the legal foundation that makes the entire generic development enterprise possible.

What Congress did not fully anticipate was how efficiently pharmaceutical companies would use the patent system’s flexibility to extend commercial exclusivity far beyond the original patent term. Patent Term Extension restores some of the regulatory review period, but the more commercially powerful tools are the secondary patents layered around a molecule after its original exclusivity has expired or is approaching expiration.

What Orange Book Listings Actually Mean for Challengers

The FDA’s Orange Book is the official catalog of patents that a brand-name NDA holder believes covers its drug product. Every Orange Book listing is, in effect, a formal declaration of what must be litigated before a generic can reach the market. A brand with 40 Orange Book patents for a single product has not necessarily invented 40 distinct things. Many of those listings will cover minor formulation variations, delivery mechanisms, or metabolite forms that a skilled formulation chemist could design around. But litigating each one costs money and time.

The FDA’s current Orange Book reform posture is relevant here. The FTC has filed administrative challenges to dozens of listings it considers improper, including patents on devices like inhalers that do not cover the drug substance itself. As of mid-2026, those challenges have produced some delisting decisions but have not yet fundamentally changed the volume-listing strategy most large incumbents use. Challengers need to factor in the realistic timeline for any FTC-driven delisting when modeling their entry scenarios.

The Paragraph IV Filing: When a Certification Becomes a Lawsuit

A Paragraph IV certification declares that a listed patent is invalid, unenforceable, or will not be infringed by the generic product. Under Hatch-Waxman, this certification is deemed an act of patent infringement, which is what allows the parties to litigate before any product reaches the market and causes commercial injury.

The 45-day window after the brand receives the PIV notice letter is the most consequential short period in pharmaceutical IP. If the brand files suit within those 45 days, it triggers an automatic 30-month stay of FDA approval for the ANDA. That stay requires no showing of merit. It runs automatically, providing the brand with up to two and a half years of continued exclusivity regardless of how weak the asserted patents may be. The stay is the single most powerful structural asymmetry in the entire Hatch-Waxman framework, and it is why brands with large Orange Book listings file on receipt of virtually every PIV notice, even for patents they privately believe are vulnerable.

The 180-day exclusivity period awarded to the first ANDA filer is the financial prize that drives most challenges against high-revenue drugs. This exclusivity cannot be shared with subsequent ANDA filers during the initial 180 days, creating a temporary duopoly between the brand and the first generic. The pricing dynamics in that window are significantly more favorable than the competitive environment after multiple generics enter. First-filer exclusivity has historically generated enough revenue to justify the cost of litigation even when the total period of market exclusivity is relatively short. That calculus changes, however, once the brand deploys an authorized generic into that same window.

Published litigation cost estimates for pharmaceutical patent cases typically capture direct legal fees, expert witnesses, and e-discovery costs. They do not capture the full cost. A high-stakes Hatch-Waxman case involving a drug with more than $25 million at risk carries median total costs through trial and appeal of approximately $4 million according to AIPLA data. That number is often cited in board presentations. What is less often cited is that the median is not the maximum, and that high-revenue drugs attract the most aggressive defense, pushing costs well above median.

The cost structure for the challenger is more exposed than for the brand in one critical respect: the brand’s litigation expenses are tax-deductible as ordinary business expenses, a treatment the Federal Circuit affirmed in the context of Hatch-Waxman litigation. The generic challenger’s costs carry the same treatment, but the brand is typically amortizing legal spend against a much larger revenue base, which means its effective cost per dollar of revenue protected is far lower.

Expert witness fees deserve separate attention. In cases involving biologic patents, mechanism-of-action disputes, or complex formulation chemistry, the technical experts who can credibly testify at the POSITA standard are a small community. The same professors and industry scientists who serve as defense experts for brand companies are often unavailable to challengers for obvious conflict reasons. Finding qualified, credible technical experts who are not already committed to the other side is a genuine operational constraint that adds cost and sometimes delays.

Revenue at Risk

Median Cost Through Discovery and Claim Construction

Median Total Cost Through Trial and Appeal

$1M – $10M

$600,000

$1,500,000

$10M – $25M

$1,225,000

$2,700,000

Over $25M

$2,375,000

$4,000,000+

Source: American Intellectual Property Law Association data, adapted

How an At-Risk Launch Becomes a Bet-the-Company Decision

An at-risk launch, where a generic company begins commercial sales after the 30-month stay expires but before all patent appeals are exhausted, is the highest-variance decision available in pharmaceutical IP strategy. The upside is early market entry and first-mover pricing power. The downside is damages calculated on the brand’s lost profits at monopoly prices, not on the generic’s actual revenues.

The damages math in a failed at-risk launch is structurally punishing. Lost profits damages require the brand to show: it would have made the sales the generic captured, it had the manufacturing capacity to make those sales, there was no non-infringing substitute available to customers, and a quantifiable profit margin. In practice, for large-market drugs, courts have consistently found that all four factors point toward maximum exposure for the infringer. The result is damages that can equal or exceed the generic’s entire revenue from the product, sometimes by a wide margin.

If a court finds willful infringement, which it may when a company launches after losing an initial district court decision, enhanced damages of up to three times the actual amount are available under 35 U.S.C. § 284. The Federal Circuit has applied this multiplier in pharmaceutical cases, and the possibility of enhanced damages should be a mandatory input in any at-risk launch financial model.

Teva and Protonix: The $2.15 Billion Cautionary Case

Teva Pharmaceutical and Sun Pharmaceutical launched generic pantoprazole (Protonix) in late 2007 while patent litigation with Wyeth was ongoing. Their internal analysis concluded that the core Wyeth patent was likely invalid. They were wrong. A federal jury upheld the patent in April 2010, and after extended damages proceedings, the parties settled in June 2013 with Teva and Sun agreeing to pay a combined $2.15 billion to Pfizer and Takeda, Wyeth’s successors.

The settlement required both companies to formally admit their sales constituted infringement of a valid patent. That admission has ongoing IP relevance beyond the settlement itself. The Protonix case is instructive not because at-risk launches always fail, but because it illustrates that even a well-reasoned internal patent assessment can be wrong, and that the damages consequences of being wrong are potentially existential. Any at-risk launch decision should assign a non-trivial probability to an adverse outcome and model the damages exposure explicitly under that scenario.

What Investors Are Watching: How Litigation News Moves Stock Price

Pharmaceutical patent litigation is priced into equities in real time. Event-study research on PIV case outcomes shows that when a brand-name company wins a district court decision, its stock rises by roughly 2.1% on average, and the challenging generic’s stock falls by roughly 1.6%. When the brand loses, the brand’s stock drops approximately 2.4% and the challenger’s rises approximately 3.1%. Those are average movements across a population of cases. For individual companies with concentrated revenue exposure, the moves can be multiples larger.

The market reaction creates a feedback loop that disadvantages challengers. A negative ruling in the district court hits the challenger’s stock price, potentially impairing the company’s ability to raise capital for the appeal or for other R&D programs. The brand, defending a large revenue stream across a diversified portfolio, can absorb a negative ruling with less proportional impact on its overall market capitalization. A challenger whose litigation is the single most important item in its commercial pipeline has no such diversification buffer.

Short sellers track patent litigation calendars actively. Claim construction hearing dates, trial dates, and appeal argument schedules are all public information. A sophisticated short position against a challenger can be established before an expected adverse ruling and covered after the stock decline. Managing this dynamic requires investor relations attention that adds operational cost and distraction to the litigation itself.

The Incumbent’s Retaliation Playbook

How Patent Thickets Work and Why They Are Getting Larger

A patent thicket is not a single defensive strategy. It is the cumulative result of systematic filing across every patentable dimension of a drug’s commercial life: new formulations, method-of-use claims for specific patient populations, dosing regimens, metabolites, polymorphs, combination therapies, delivery devices, and manufacturing processes. Each continuation application extends the patent family without necessarily claiming anything that a skilled chemist would consider inventive over the prior art.

The strategic value of a thicket lies in arithmetic, not in any individual patent’s validity. If a challenger must litigate 40 patents, and each individual case costs $3-4 million and takes 30 months to resolve, the total cost of clearing the thicket through litigation alone can exceed $150 million. Many of those patents will ultimately be invalidated. But the litigation timeline means that even weak patents provide years of market exclusivity simply because no one can afford to fight them all simultaneously.

AbbVie’s Humira patent estate is the most-studied example of this strategy operating at industrial scale. AbbVie filed over 100 patents around adalimumab covering formulation, dosing, and manufacturing. The core patent on the molecule expired in 2016. Biosimilar competition in the United States did not begin until January 2023, seven years later. The thicket did not prevent eventual biosimilar entry. It delayed that entry by seven years, during which AbbVie generated tens of billions in Humira revenue that would otherwise have been competed away. The thicket functioned exactly as designed: not as an impenetrable wall but as an expensive and time-consuming obstacle.

AbbVie eventually settled with all major biosimilar developers, granting licenses with entry dates ranging from 2023 to 2024 depending on the agreement. The financial terms of those settlements are not fully public, but the pattern of negotiated entry dates followed by settlement royalty structures is now standard in the biologics space. The thicket’s commercial purpose is to extend the period during which settlement negotiations occur on terms favorable to the brand.

Why AbbVie’s Humira Exclusivity Extended to 2023 Despite a 2016 Patent Expiry

The gap between Humira’s core patent expiration and actual U.S. biosimilar entry reflects both the patent thicket and the specific challenges of biosimilar interchangeability designation. FDA approval of a biosimilar requires demonstrating that it has no clinically meaningful differences from the reference product. Interchangeability designation, which allows pharmacists to substitute without prescriber intervention, requires additional switching studies showing the patient does not experience greater risk from alternating between the biosimilar and the reference biologic.

The interchangeability pathway is more demanding for complex biologics than for small-molecule generics, and the Biologics Price Competition and Innovation Act (BPCIA) provides a 12-year period of regulatory exclusivity for reference biologics, entirely separate from patent protection. A biosimilar developer must navigate both the 12-year exclusivity period and the patent thicket before commercial launch. This dual barrier is structurally more formidable for biologics than the comparable Hatch-Waxman framework for small molecules.

How Authorized Generics Destroy the First-Filer’s Reward

An authorized generic is the brand’s own product, or a licensed version of it, sold under a generic label. Because it is covered by the original NDA, the brand does not need to file an ANDA. It can launch an authorized generic at any time, including during the first-filing generic’s 180-day exclusivity period.

The FTC’s 2011 study on authorized generics documented that their presence during the 180-day exclusivity period reduces the first-filing generic’s revenues by 40% to 52% on average. That revenue reduction does not affect the first-filer’s cost structure. The legal fees, expert witness costs, and management time already expended cannot be recovered by earning less from the exclusivity window. The authorized generic converts a lucrative duopoly into a three-player market earlier than anticipated.

Brand companies use authorized generic threats strategically in settlement negotiations. The threat of an authorized generic launch can be more valuable than the launch itself, because it creates a negotiating lever: settle on our terms for a specific entry date, or we will launch an authorized generic and compress your exclusivity economics. Generic companies that have not modeled the authorized generic scenario quantitatively going into settlement talks tend to concede more than they should.

The 2025 RAPS analysis of authorized generic trends suggests that explicit no-AG commitments in settlement agreements have become less common following FTC scrutiny, replaced by more nuanced arrangements. The FTC has characterized no-AG commitments as a form of reverse payment under the FTC v. Actavis framework, meaning that brands are increasingly using authorized generics as commercial tools rather than settlement chips.

How Product Hopping at Eli Lilly and Warner Chilcott Shifted Market Access

Product hopping occurs when a brand transitions its patient base from a formulation whose patent is expiring to a marginally modified formulation covered by new patents, before the generic version of the original can reach the market. The modification typically involves a change in dosage form, release mechanism, or dosing interval that does not represent a meaningful clinical advance.

Warner Chilcott’s transition of Doryx (doxycycline hyclate) from 75mg and 100mg tablets to 150mg tablets was examined by the Second Circuit in a case brought by generic manufacturers. The court found that the product reformulation, combined with Warner Chilcott’s market withdrawal of the original tablets, constituted actionable conduct under antitrust law when it effectively eliminated the market for the generic’s approved product. The case established that product hopping can cross the line from legitimate product development into anticompetitive market manipulation.

Eli Lilly’s transition from Prozac (fluoxetine) to Sarafem and later to the weekly formulation is an earlier example of the same commercial logic applied before the antitrust doctrine was well developed. The pharmaceutical industry has refined these strategies considerably since then. The legal risk of an antitrust claim for product hopping now depends heavily on whether the brand withdraws the original product or simply stops promoting it, since courts have distinguished between product withdrawals that destroy the generic market and competitive transitions that leave the original product available.

The PTAB as a Second Front: Inter Partes Review Strategy

Why the PTAB Burden of Proof Matters More Than People Think

In U.S. district court, an issued patent carries a presumption of validity. A challenger must prove invalidity by clear and convincing evidence. At the Patent Trial and Appeal Board, there is no presumption of validity, and invalidity requires only a preponderance of the evidence. That difference in legal standard, holding everything else constant, makes the same prior art more likely to succeed as an IPR argument than as a district court argument.

The practical impact is that challengers who lose invalidity arguments at the district court level have not necessarily exhausted their options. An IPR petition can advance prior art that the district court considered but did not find convincing under the higher standard. The Federal Circuit has confirmed that issue preclusion principles do not automatically bar an IPR petition following a district court loss, though the specific facts of each case matter. This creates a genuine asymmetry that brands must manage and challengers can exploit.

The PTAB’s administrative patent judges are technically trained. They are more likely than a lay jury to understand the mechanistic significance of a prior art reference, and they are more likely to credit a chemist’s testimony about whether a claimed compound would have been obvious to formulate given the prior art. In fields like biologics, where the difference between a patentable antibody and an obvious variant depends on understanding molecular biology at a granular level, PTAB proceedings can produce more technically accurate outcomes than jury trials.

How IPR Timing Interacts with the 30-Month Stay

An IPR petition filed after a district court lawsuit has been initiated creates a procedurally complex situation. The PTAB must issue a final written decision within one year of institution, with a possible six-month extension. That 18-month maximum timeline from petition to decision is typically shorter than the 30-month stay period, meaning an IPR can potentially produce a patent invalidity ruling before the stay expires and FDA approval issues.

The district court has discretion to stay the infringement case pending the IPR outcome, which would conserve litigation resources if the IPR results in invalidity. Courts in the District of Delaware and Northern District of California, where most Hatch-Waxman cases are filed, have been inconsistent in granting such stays. Some judges view the PTAB process as complementary to district court review and will stay the case; others view the parallel proceedings as creating scheduling inefficiency and decline to stay. This uncertainty means challengers cannot rely on an IPR stay to compress the district court timeline, but they can use the IPR as genuine dual-front pressure on the brand’s patent portfolio.

What Amgen v. Sanofi Changed About Biologic Patent Strategy

The Supreme Court’s unanimous 2023 ruling in Amgen Inc. v. Sanofi invalidated Amgen’s patents on anti-PCSK9 antibodies under the enablement doctrine. The patents claimed an entire functional genus of antibodies that could bind PCSK9 and reduce LDL cholesterol, but they only described the amino acid sequences for 26 specific antibodies. The Court held that claiming millions of functional variants while enabling only a handful violates the requirement that a patent specification enable the full scope of the claimed invention without undue experimentation.

The commercial implications extend well beyond PCSK9 antibodies and Amgen’s commercial dispute with Sanofi and Regeneron. The decision has materially increased the vulnerability of broad, functionally defined biologic claims across the entire biologics patent landscape. Any patent claiming a functional class of antibodies, receptors, or other large molecules without providing a comprehensive roadmap for producing that entire class is now more susceptible to an invalidity challenge than it was before the decision. Biosimilar developers and generic challengers working in the monoclonal antibody space should assess enablement as a primary invalidity angle, not a secondary one.

Revenue at Risk: Key Patent Expiry Dates and Loss of Exclusivity Forecasts

Which Drugs Face the Largest Revenue Cliffs Through 2030

The pattern of pharmaceutical patent expiry over the next four years concentrates revenue exposure in a handful of therapeutic areas: oncology (particularly PD-1/PD-L1 checkpoint inhibitors), diabetes and obesity (GLP-1 receptor agonists), and immunology (JAK inhibitors and IL-targeting biologics). The aggregate revenue at risk from loss of exclusivity events between 2026 and 2030 has been estimated by Boston Consulting Group at over $200 billion across the industry.

Merck’s Keytruda (pembrolizumab) holds the single largest individual revenue exposure. Keytruda generated approximately $25 billion in 2024 sales and faces biosimilar entry risk beginning around 2028 when its core patents expire, though Merck has filed continuation patents that could delay that entry. The question of whether those continuation patents represent genuine innovation or thicket-building will be one of the most consequential patent disputes of the next decade.

Bristol Myers Squibb’s Opdivo (nivolumab) similarly faces PD-1 patent expiry questions. BMS and Ono Pharmaceutical have defended their PD-1 patents against challenges from other checkpoint inhibitor developers, including the landmark litigation with Keytruda’s intellectual history. The eventual resolution of the fundamental PD-1 patent questions will determine whether both drugs face simultaneous biosimilar entry or staggered competition.

Novo Nordisk’s semaglutide (Ozempic, Wegovy) and Eli Lilly’s tirzepatide (Mounjaro, Zepbound) are the most commercially consequential GLP-1 patents currently in force. Both companies have filed aggressive continuation patent strategies around formulation, dosing regimen, and delivery device. The manufacturing complexity of GLP-1 peptides creates an additional barrier to biosimilar entry that exists independently of the patent position, but the patent thicket is being built regardless.

Why Keytruda’s Patent Expiry Matters for Merck Investors

Keytruda represents approximately 40% of Merck’s total revenue. The loss of exclusivity event, whenever it occurs, will be the most significant single financial event in Merck’s modern commercial history. Merck’s pipeline investments in oncology, including co-stimulatory bispecific antibodies and ADC partnerships, are explicitly positioned as Keytruda successors. The adequacy of that pipeline to replace Keytruda’s revenue contribution is the central question for Merck investors from now through 2030.

The biosimilar development timeline for a monoclonal antibody as complex as pembrolizumab is typically five to seven years from the start of development to a regulatory filing. Companies that have not begun biosimilar pembrolizumab development programs are effectively out of the first wave of competition. The first wave of biosimilar entrants will face the Merck thicket in its entirety; companies that enter the market in the second or third wave may benefit from invalidity decisions obtained by earlier entrants without having incurred those litigation costs.

How Bristol Myers Squibb Defended Opdivo Against PD-1 Patent Challenges

BMS’s PD-1 patent position on nivolumab has faced challenges on multiple fronts. The foundational PD-1 and PD-L1 work comes from academic research conducted at multiple institutions, and the question of who invented what first generated extensive interference proceedings and subsequent litigation. BMS settled with multiple parties, including Ono Pharmaceutical and others, to consolidate its patent position.

The key lesson from the Opdivo patent history is that complex biologics with multiple institutional inventors and overlapping patent families create invalidity vulnerabilities that well-capitalized challengers can exploit. Each settlement that resolves one prong of the patent family tends to create transparency about which claims have been quietly conceded, which can be used to model vulnerability in the remaining claims.

The Settlement Paradox: How a Negotiated Peace Becomes an Antitrust Target

Why 40% of Patent Cases Settle Before Trial and What That Statistic Hides

Settlement data from 2023 shows that 40% of patent litigation cases resolved before trial. In pharmaceutical patent litigation, the settlement rate is higher because the economics of the case structure drive both parties toward negotiated outcomes. The brand wants a predictable exclusivity end date to manage investor guidance. The generic wants a certain entry date and a guaranteed period of revenue. The litigation itself generates only unpredictable binary outcomes, which neither party can perfectly plan around.

What the headline settlement rate does not show is the distribution of settlement terms and what challengers typically give up to get them. In a world where both parties are rational, the settlement value should approximate the expected outcome of the litigation. In practice, challengers with weaker balance sheets settle earlier and on less favorable terms because they cannot afford to litigate to the most favorable outcome. Adequately capitalized challengers that can credibly threaten to litigate through trial and appeal consistently achieve earlier entry dates and better financial terms than undercapitalized challengers who signal settlement pressure.

FTC v. Actavis and the Rule of Reason: What Changed in 2013

Prior to the Supreme Court’s 2013 ruling in FTC v. Actavis, many circuit courts evaluated pharmaceutical patent settlements under the “scope of the patent” test. Under that standard, any settlement that restricted competition only to the extent the underlying patent claims justified was presumptively lawful. In practice, this meant that explicit cash payments from brand to generic in exchange for a delayed entry date were generally not actionable under antitrust law.

Actavis rejected that framework. The Court held that a large unexplained reverse payment is a strong indicator that the parties are sharing monopoly profits rather than settling a genuine dispute about patent validity or infringement. It applied the antitrust rule of reason, which requires a substantive analysis of competitive effects, to evaluate these settlements. The practical effect was to make explicit “pay-for-delay” arrangements substantially riskier and to shift the industry toward more complex settlement structures.

The FTC’s most recent annual MMA report, covering fiscal year 2024, documents the continued evolution of settlement terms. Explicit cash payments now account for a small fraction of total agreements. The dominant forms of possible compensation in current filings are: no-AG commitments (the brand agrees not to launch an authorized generic during the first-filer’s exclusivity period), quantity restriction agreements (the generic commits not to sell more than a specified volume during a defined period), and ancillary business arrangements (supply agreements, licensing deals, or co-promotion arrangements at terms that are not commercially arms-length).

What Quantity Restriction Agreements Mean for Generic Market Entry

Quantity restrictions are the FTC’s current area of sharpest investigative focus. These provisions limit how much of a product a settling generic can sell for a period after its launch. From a competitive standpoint, they function like market allocation arrangements: the brand and generic agree to divide the market by volume rather than competing on price, which preserves a higher price level for both at the expense of patients and payers.

The legal status of quantity restrictions under the rule of reason is not fully settled. The FTC has expressed its view that these arrangements are anticompetitive and has pursued enforcement actions, but the case law is still developing. Challengers who are considering accepting quantity restriction terms as part of a settlement should treat them as a source of long-tail antitrust liability, not as a resolved commercial arrangement.

No-AG Agreements After Actavis: What the FTC Is Actually Monitoring

A no-AG commitment from a brand-name company to a settling first-filer generic preserves the economic value of the 180-day exclusivity period by eliminating the authorized generic threat that would otherwise compress it. The FTC’s position is that this commitment is a transfer of economic value from the brand to the generic and can constitute an unlawful reverse payment under Actavis.

The FTC’s enforcement posture on no-AG agreements has been inconsistent across administrations. The Biden-era FTC pursued these aggressively. The current regulatory environment under a new commission configuration is somewhat less predictable, but the legal risk does not depend on enforcement posture alone. Private plaintiffs, including payers, PBMs, and state attorneys general, can bring their own rule-of-reason challenges to settlements they believe harmed competition. The FTC losing interest in a particular settlement does not eliminate private plaintiff exposure.

How Biosimilar Entry Timing Works in Practice

What Actually Happens at Loss of Exclusivity for a Biologic

The mechanics of biosimilar market entry differ materially from small-molecule generic entry. When a small-molecule drug loses exclusivity, the generic market can achieve high substitution rates quickly because pharmacists can substitute bioequivalent generics without prescriber intervention. Biosimilars are not automatically interchangeable without the FDA’s specific interchangeability designation, which requires additional switching studies.

A biosimilar without interchangeability designation still competes commercially, but it requires prescriber action rather than pharmacist substitution. Hospital formularies and GPO contracts drive institutional adoption. Payer formulary decisions are the primary lever in the commercial market. The transition from brand to biosimilar is therefore slower and more expensive than small-molecule LOE, and the revenue erosion curve is less steep in the first one to two years after biosimilar entry.

The entry of multiple biosimilars accelerates price competition significantly. Humira biosimilar pricing in the first 18 months of U.S. competition demonstrated this dynamic. AbbVie maintained a high-list/high-rebate formulary strategy for Humira while biosimilar entrants competed on net price. The coexistence of two pricing strategies in the same therapeutic category, one oriented toward formulary rebates and one oriented toward list price discounts, created a fragmented market that sustained AbbVie’s commercial revenues longer than many forecasters anticipated.

Which Competitors Benefit When a Blockbuster Loses Exclusivity

The immediate beneficiaries of a branded drug’s loss of exclusivity are the first-filing generics (for small molecules) or the first approved biosimilars (for biologics). The less obvious beneficiaries are the brand’s therapeutic competitors, who can reprice their products, shift promotional messaging, or expand formulary access as the brand’s market share erodes.

When Revlimid (lenalidomide) faced generic entry in 2022 following Bristol Myers Squibb’s structured settlement with multiple generic manufacturers, competitors in the multiple myeloma space recalibrated their commercial strategies. The eventual revenue erosion of Revlimid created opening for BMS’s own Pomalyst (pomalidomide) to compete on different clinical grounds, a dynamic BMS anticipated in its pipeline planning. Companies with therapeutic franchise exposure to a patent cliff should model both the revenue erosion on the at-risk product and the competitive dynamics in adjacent indications.

Why Manufacturing Complexity Matters for Biosimilar Entry

How GLP-1 Manufacturing Difficulty Creates a Non-Patent Barrier

GLP-1 receptor agonist peptides require demanding manufacturing processes. Semaglutide and tirzepatide are both synthetic peptides produced through solid-phase peptide synthesis followed by complex purification and formulation steps. The scale required to supply commercial volumes of these molecules at competitive cost is not achievable by most API manufacturers without substantial capital investment and process development.

This manufacturing complexity creates a barrier to biosimilar entry that exists entirely outside the patent system. A company that has cleared every Novo Nordisk patent on semaglutide still cannot enter the market without a reproducible and cost-effective manufacturing process, regulatory-grade analytical methods, and sufficient manufacturing scale. The companies best positioned to challenge GLP-1 patents are those that have invested in parallel manufacturing development, not those that have optimized solely for legal strategy.

The FDA’s approval of an authorized biosimilar peptide also requires demonstrating analytical comparability to the reference product, which is technically demanding for a molecule as structurally complex as semaglutide. The regulatory science for GLP-1 peptide comparability is still maturing, and early biosimilar filers should expect more intensive FDA review than would apply to a simpler small-molecule generic.

What Makes Biologic Manufacturing Difficult for Generic Entrants

Manufacturing complexity is the dimension of biologic competition that most non-specialist investors underestimate. A monoclonal antibody produced in a CHO cell line is not the same product if produced in a different cell line, and it is not the same product if the purification process differs even slightly. Post-translational modifications, glycosylation patterns, and aggregation profiles can all differ between the reference biologic and a biosimilar even if the primary amino acid sequence is identical. The FDA’s totality-of-evidence approach to biosimilar approval requires demonstrating similarity across all of these dimensions, which requires extensive analytical and clinical work.

The capital cost of building a biologic manufacturing facility capable of GMP-compliant production at commercial scale is typically $200 million to $500 million or more. Few generic companies have that manufacturing infrastructure. The competitive landscape for biosimilar biologics is therefore far more concentrated among large, vertically integrated pharmaceutical and contract manufacturing organizations than the generic small-molecule market is. This concentration reduces the number of credible challengers, which reduces competitive pressure on brands, and it gives incumbents a more manageable litigation adversary pool.

Operational Risk: How Litigation Drains the R&D Pipeline

Why a Patent Challenge Costs More Than the Legal Budget Suggests

The hidden operational cost of a major patent challenge is the diversion of scientific and executive talent from revenue-generating activities to litigation support. Depositions, claim construction briefing, and trial preparation require sustained involvement from the company’s formulators, analytical chemists, and pharmacologists. These are not fungible employees who can be replaced during the litigation period with temporary hires. They are the people on whom the company’s pipeline depends.

A formulation chemist spending 30% of their time on litigation support for 18 months is not developing the next difficult-to-formulate generic product for 30% of their productive capacity for 18 months. The opportunity cost of that lost development time compounds forward: a product that would have been filed in 18 months may now be filed in 24 months, losing first-filer status or narrowing the competitive window. The loss does not appear on the income statement. It appears two to three years later as a weaker pipeline than the company would otherwise have had.

Senior executives face the same dynamic. A CEO and general counsel who are deeply involved in managing major patent litigation are allocating strategic attention that would otherwise go to product portfolio development, licensing negotiations, and commercial planning. This attention cost is highest in the middle stages of litigation, when case strategy is most fluid and decisions most consequential.

How Patent Thicket Litigation Starves Small Generic Companies’ Pipelines

For smaller generic manufacturers, the pipeline diversion risk from a single major litigation is existential in a way it is not for Teva or Sandoz. A company with 50 scientists cannot absorb the litigation support demands of a major Hatch-Waxman case without materially compromising its other development programs. Large generic companies have this scale advantage over smaller challengers, which is part of why patent challenges against blockbuster drugs are dominated by a small number of large players.

The concentration of Hatch-Waxman litigation among large generic companies creates a structural problem for competition policy. The drugs most worth challenging, those with the highest revenue and the most patients on therapy, are also the drugs with the most aggressive patent thickets and the largest incumbent litigation budgets. The barrier to challenging them is highest precisely where the social benefit of successful challenge is greatest.

Common Investor Questions

What is the single most important financial number to understand in a PIV challenge?

The financial stake asymmetry. The brand’s average revenue at risk is roughly $4.3 billion per PIV case. The challenger’s average upside is roughly $204 million. Understanding that ratio explains the brand’s willingness to spend aggressively on defense and helps calibrate the challenger’s risk tolerance.

How should investors interpret a Paragraph IV filing against a portfolio company’s drug?

As a material event requiring immediate cash flow modeling, not just a legal event to be monitored. The relevant questions are: how many patents are listed in the Orange Book for this drug, how many of those are in the primary coverage claims versus secondary/formulation claims, is there a 30-month stay in effect, and what is the FDA exclusivity status independent of patent protection? The stock price reaction at filing tends to underestimate the long-term revenue risk if the filing leads to eventual generic entry.

How do authorized generics affect the investment case for first-filer generic companies?

Materially. If a brand launches an authorized generic during the 180-day exclusivity period, the first filer’s revenue from that period is reduced by 40% to 52% on average. If an authorized generic launch was not in the financial model for the challenger, the stock reaction to an AG announcement during the exclusivity period can be severe.

What does FTC v. Actavis mean for evaluating pharmaceutical settlement agreements?

Any settlement involving a transfer of value from brand to generic, whether in cash or in other forms like no-AG commitments or volume restrictions, is subject to antitrust review under the rule of reason. Investors in companies that are parties to such settlements should treat the antitrust exposure as a real liability until the statute of limitations has run and no enforcement action has been initiated.

Why do biosimilar timelines consistently slip from original forecasts?

Three reasons account for most of the slippage: patent thicket litigation takes longer than expected, manufacturing development and scale-up takes longer than expected, and FDA analytical comparability review is more intensive than expected for complex biologics. The interchangeability designation process adds additional time beyond basic biosimilar approval. Investors should apply a systematic delay buffer to any commercial biosimilar launch forecast.

Investment Strategy: Positioning Around Pharma Patent Events

How to Build a Pharma IP Event Calendar for Portfolio Management

The Orange Book contains structured data on every patent protecting every FDA-approved drug. Regulatory exclusivity expiration dates are separately tracked by the FDA’s Drugs@FDA database. Cross-referencing these two sources against revenue data from company filings and third-party market research creates a prospective event calendar that can identify approaching loss-of-exclusivity events years in advance.

The most actionable LOE events for portfolio management are those where: the primary patent is within three years of expiration, at least one Paragraph IV challenge has already been filed, and the drug’s revenue contribution to the brand company’s total revenues is large enough to be material. These events are visible enough to track but complex enough that most investors are not modeling them precisely.

Platform analytics tools, including DrugPatentWatch, consolidate this data and enable systematic screening across the full approved drug universe. The competitive intelligence value is not just in identifying upcoming LOE events but in tracking the litigation status of current PIV cases in real time, which provides earlier signals about likely generic entry timing than waiting for official settlement announcements.

How Patent Expiry Events Create Both Long and Short Opportunities

The brand-side position heading into a major LOE event is typically a slow deterioration of valuation multiples rather than a sudden collapse, unless the patent is invalidated unexpectedly before its expiration date. Brands with large LOE events on the horizon trade at compressed multiples relative to their near-term earnings because investors discount for the eventual revenue erosion. Companies that manage LOE transitions well, through pipeline launches that replace expiring revenue, recapture multiple expansion. Companies that manage them poorly trade down.

The challenger-side position is the inverse. A successful Paragraph IV challenge can be a catalyst for significant stock appreciation in a generic or biosimilar company, particularly if first-filer status and 180-day exclusivity are in play. The most concentrated opportunities arise in the 30 to 90 days before a district court decision is expected on a PIV case involving a high-revenue drug, when the binary outcome probability is most relevant to valuation.

Key Takeaways

Pharmaceutical patent litigation is fundamentally asymmetric. The brand is defending a known and quantified revenue stream against challengers whose reward, though meaningful, is a fraction of what the brand stands to lose. That asymmetry drives every aspect of the brand’s strategy: the patent thicket, the authorized generic threat, the aggressive 45-day lawsuit trigger, and the willingness to litigate through appeal even after losing in the district court.

At-risk launches carry catastrophic downside risk. The Protonix settlement at $2.15 billion is the headline case, but the structural problem is the damages calculation methodology, where infringer liability is measured against the brand’s lost monopoly profits, not the generic’s actual revenues. Any at-risk launch model that does not explicitly assign a probability to adverse outcome and model the resulting damages exposure is incomplete.

The PTAB creates a genuine second front that challengers can use to pressure patent portfolios at lower cost and under more favorable standards than district court. The preponderance-of-evidence standard and the technical expertise of APJs make it the correct first choice for challenging secondary formulation patents in a patent thicket, where the invalidity arguments are strong but the individual patent’s commercial value may not justify full district court litigation.

FTC v. Actavis has not eliminated anticompetitive settlements. It has replaced them with more complex ones. Quantity restrictions and no-AG commitments carry antitrust exposure that persists for years after the settlement is signed. Companies accepting these terms should model the liability alongside the commercial benefit.

Manufacturing complexity is an underappreciated variable in biosimilar competition. Patent clearance alone is not sufficient to enter the market for complex biologics. Capital investment in manufacturing infrastructure, process development, and analytical comparability work must proceed in parallel with the legal strategy for biosimilar entry to be commercially viable when patents expire.

Competitive intelligence infrastructure is not optional. The companies that consistently achieve profitable patent challenges operate with real-time visibility into the full patent landscape, regulatory exclusivity status, litigation history, and competitor filing activity. Building this infrastructure is a cost of competing in this market.

Frequently Asked Questions

What is a Paragraph IV certification and why does it constitute infringement?

A Paragraph IV certification is a statement by an ANDA filer that a patent listed in the Orange Book for the reference drug is invalid, unenforceable, or will not be infringed by the generic product. Under the Hatch-Waxman framework, this filing is deemed a technical act of patent infringement. Congress designed this legal fiction to allow patent disputes to be litigated and resolved before generic market entry, avoiding the harm of an actual infringing launch. Without this mechanism, generics would need to launch commercially before any infringement claim could be adjudicated, which would expose them to much larger damages.

How does the 30-month automatic stay work in practice?

If the brand files a patent infringement lawsuit within 45 days of receiving the PIV notice letter, FDA approval of the ANDA is automatically stayed for 30 months from the date the brand received the PIV notice. The stay requires no showing of merit. It runs automatically regardless of the strength of the asserted patents. After 30 months, FDA can approve the ANDA if it is otherwise approvable, even if litigation is ongoing. This is typically when at-risk launch decisions become live.

What is the difference between patent exclusivity and regulatory exclusivity?

Patent exclusivity flows from the patent system: it lasts for the patent’s term (20 years from filing, subject to PTE) and can be challenged in litigation. Regulatory exclusivity is a separate statutory grant from FDA: New Chemical Entity exclusivity lasts five years and cannot be challenged through the patent system. Orphan Drug exclusivity lasts seven years. These exclusivities can coexist with patents and can independently block generic entry even after all relevant patents have expired or been invalidated.

Why do some generic companies challenge patents on drugs that are not blockbusters?

Secondary patents on smaller-revenue drugs can still be challenged profitably if the at-risk investment is proportionate to the expected return. A drug generating $300 million annually with a formulation patent that is clearly invalid may be a better risk-adjusted opportunity than a drug generating $3 billion annually with 40 overlapping patents. First-filer economics on a smaller drug can generate substantial returns if the legal case is strong and the litigation costs are manageable. Companies that optimize for probability-weighted return rather than total market size can build profitable generic pipelines from non-blockbuster challenges.

How does a biosimilar interchangeability designation affect market penetration speed?

Without interchangeability designation, a biosimilar can be prescribed and dispensed, but pharmacists cannot substitute it for the reference biologic without a prescriber’s explicit authorization. This substantially slows adoption in retail pharmacy channels compared to small-molecule generics, where automatic substitution is standard. Hospital formulary adoption can be faster because formulary committees can make institutional decisions to use biosimilars. Interchangeability designation removes the prescriber authorization requirement and allows biosimilar substitution at the pharmacy level, accelerating market penetration significantly once achieved.

What IPR statistics tell challengers about PTAB success rates for pharma patents?

Pharmaceutical IPR petitions are instituted at rates broadly comparable to other technology areas, typically in the range of 60% to 70% of filed petitions. Among instituted petitions, PTAB cancels at least one challenged claim in a majority of cases, though full claim cancellation of all challenged claims is less common. These aggregate statistics mask significant variation by patent type: formulation and method-of-use patents tend to have higher invalidity rates at PTAB than composition patents covering the active pharmaceutical ingredient. Challengers should not rely on aggregate statistics; patent-specific prior art analysis is the correct basis for assessing IPR viability.