When a buyer writes a $74 billion check for a drugmaker, they are not paying for the molecule. They are paying for the wall of legal protections around it. Bristol-Myers Squibb did not buy Celgene in 2019 for lenalidomide’s chemical structure. It bought the staggered, court-tested set of patents and FDA exclusivities that kept generics on a leash long enough to amortize the deal. That distinction sits at the center of pharma M&A: drugs are commodities, but the exclusivities wrapped around them are not.

The four exclusivity types covered here set the floor and the ceiling of nearly every pharmaceutical valuation. Get them right and a $30 billion deal pencils out. Get them wrong and you watch the cash flow cliff arrive years earlier than the model predicted, which is precisely what happened to Teva when revenues from Copaxone collapsed faster than analysts forecast after the 40mg formulation patents fell.

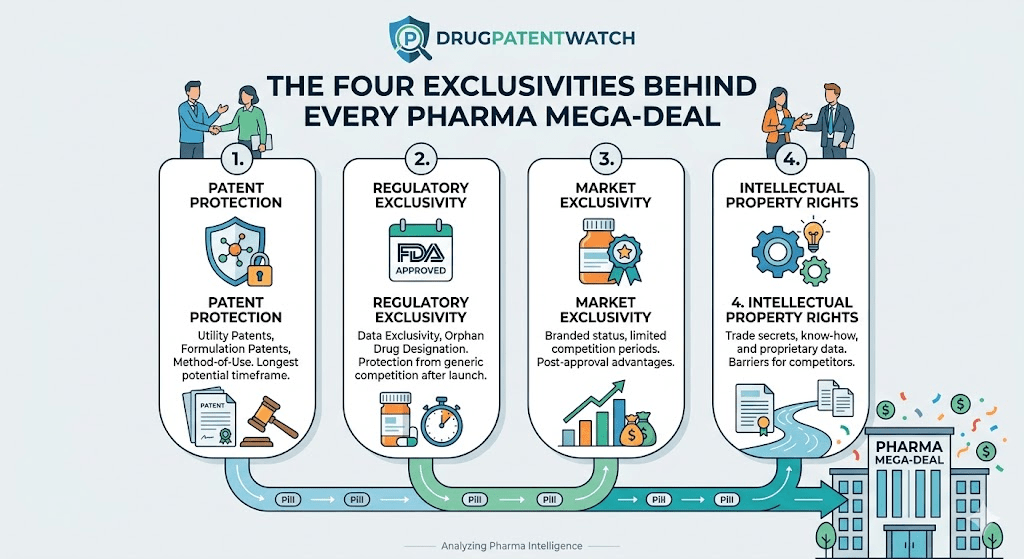

This piece walks through composition-of-matter patents, FDA regulatory exclusivities, biologics data exclusivity under the BPCIA, and patent term extension under Hatch-Waxman. It then unpacks how acquirers stack these protections in deal models, where the litigation discounts come from, and what the recent Inflation Reduction Act changes mean for the math. Real drugs. Real deals. Real numbers.

Why Exclusivity Drives Pharma M&A Valuations

Pharmaceutical assets are unusual among M&A targets because their cash flows are pre-scheduled to collapse. Every other industry models terminal value as a perpetuity or fade. Pharma models terminal value as a cliff, with a generic or biosimilar entrant arriving on a calendar date and revenue dropping 80% to 90% within 24 months for small molecules, and 30% to 70% over three to five years for biologics.

The exclusivity layer is what stands between the model and the cliff. A composition-of-matter patent running to 2033 means the discounted cash flow analysis can recognize 11 more years of brand pricing. Pull that patent and the asset is worth a fraction of what the seller wants. This is why diligence in pharma M&A starts with the Orange Book pull, not the income statement.

The Math Behind Loss-of-Exclusivity Cliffs

Loss of exclusivity (LOE) creates the steepest revenue declines outside of consumer technology fads. For small molecules with multiple generic entrants on day one, IQVIA has tracked first-year revenue erosion of 80% to 90%, with prices falling to 10% of brand within 18 months when four or more ANDA filers receive approval [1]. Atorvastatin, Pfizer’s Lipitor, lost roughly $7 billion of annual U.S. revenue within two years of its November 2011 LOE. Singulair, Merck’s montelukast, dropped from $3.2 billion in 2011 U.S. sales to under $500 million by 2013.

Biologics behave differently. Biosimilars compete on price, but the trajectory is shallower because manufacturing complexity limits the number of competitors and switching frictions slow physician uptake. Humira, AbbVie’s adalimumab, faced nine biosimilars by the end of 2023 and still retained roughly 80% of its U.S. prescription volume into the first quarter of 2024, though rebated net pricing eroded faster than gross numbers suggested.

How Acquirers Discount Cash Flows Past the LOE Date

A standard pharma DCF runs in three segments. The pre-LOE period uses a moderate discount rate (8% to 10%) and full brand pricing. The LOE transition period applies a generic erosion curve based on therapeutic class, number of expected ANDA filers, and channel mix. The post-LOE tail captures residual brand revenue, authorized generics, and any line-extension exclusivities.

Acquirers run sensitivity tables on the LOE date itself. A six-month shift either direction can change an asset’s net present value by 3% to 8%, depending on the size of the franchise. For a $5 billion-a-year drug, that means $150 million to $400 million of valuation hangs on a single calendar question, which is why pediatric exclusivity extensions and patent term adjustment calculations get scrutinized at the partner level in deal teams.

The Risk-Adjusted NPV Model in Pharma Deals

The risk-adjusted NPV (rNPV) approach probability-weights every future cash flow against the chance the exclusivity actually holds. Composition-of-matter patents typically get 85% to 95% probability of surviving challenge, depending on the strength of prior art. Method-of-use patents get 40% to 70%. Formulation patents often get 30% to 50%. Orange Book listings for crystalline forms or salt selections frequently come in below 25% after the Federal Circuit’s pattern of invalidating obvious variants under KSR v. Teleflex.

Deal modelers source these probabilities from a combination of in-house litigators, outside counsel opinions, and patent intelligence platforms. DrugPatentWatch is one of the patent intelligence resources frequently cited in diligence packages, particularly for assembling the full Orange Book picture, ANDA filer history, and exclusivity calendars across multi-product portfolios. The accuracy of the exclusivity calendar feeds directly into the bid.

Exclusivity Type 1: Composition-of-Matter Patents

The composition-of-matter (COM) patent is the strongest form of pharmaceutical exclusivity ever issued. It covers the molecule itself, not how it is made, used, or formulated. If you have a valid COM patent on a drug, no one else can legally sell that molecule for any indication during the term, full stop. This is the patent that anchors every blockbuster valuation.

What Is a Composition-of-Matter Patent in Drug Development?

A COM claim defines the molecule by its chemical structure. For small molecules, that means a Markush-style structural drawing or a specific compound recitation. For biologics, it covers the amino acid sequence, often with claims to specific complementarity-determining regions (CDRs) for antibodies. The U.S. Patent and Trademark Office issues COM patents under 35 U.S.C. § 101 as compositions of matter, subject to the standard requirements of novelty (§ 102), non-obviousness (§ 103), and enablement (§ 112).

COM patents are difficult to invalidate because the prior art rarely discloses the exact structure of a successful drug candidate. The novelty bar is the molecule’s specific arrangement of atoms, and discovery teams usually file the application before any third party could plausibly find the compound. This is why generic challengers attacking COM patents lose more often than they win, and why settlements involving COM patents tend to cluster at or near the patent’s natural expiration date rather than years earlier.

How Long Does Composition-of-Matter Exclusivity Last?

U.S. utility patents run 20 years from the earliest non-provisional filing date under 35 U.S.C. § 154. For pharmaceutical companies, the practical exclusivity period is shorter because the patent clock starts ticking before clinical trials, FDA review, and commercial launch. A drug that spends 10 years in development from patent filing to approval has only 10 years of remaining patent life when it enters the market.

Patent term extension (covered in detail later) restores some of this lost time but caps the post-approval term at 14 years. Patent term adjustment (PTA) under 35 U.S.C. § 154(b) adds days for USPTO delays during prosecution. The combination determines the real-world expiration date that shows up in the Orange Book, which is the date that matters for ANDA filing windows and the M&A model.

The 20-Year Term and the Filing-Date Trap

Companies sometimes file COM patents too early. If a candidate is patented before its therapeutic potential is fully understood, the 20-year clock burns through preclinical work that does not generate revenue. Conversely, filing too late risks public disclosure or independent discovery. Skilled patent groups try to file at the point where the compound’s pharmacology is established but well before formal IND filing.

Acquirers reading a target’s patent estate look closely at the COM filing date relative to the IND date. A long gap between patent filing and IND suggests the compound sat on the shelf, which can mean the COM has fewer commercial years left than the headline expiration date suggests.

Case Study: Keytruda’s Composition-of-Matter Cliff in 2028

Merck’s pembrolizumab, marketed as Keytruda, is the highest-revenue prescription drug in the world, with 2024 sales exceeding $29 billion. The COM patent estate, originally filed by Organon Biosciences (later acquired by Schering-Plough, then Merck), is generally understood to expire in 2028 in the United States. That single date drives Merck’s entire growth strategy, the rationale for the Acceleron acquisition, the Daiichi Sankyo collaboration on ADCs, and the negotiations around subcutaneous Keytruda that could extend franchise life through formulation patents.

Wall Street analysts model a Keytruda revenue decline from $29 billion to $10 billion to $12 billion within three years of biosimilar entry, with the exact slope depending on how many biosimilar developers file Biologics License Applications (BLAs) and how Merck’s subcutaneous formulation fares against the IV biosimilars. The math on Merck’s market capitalization is unforgiving: roughly half of the company’s enterprise value is tied to Keytruda’s post-2028 cash flows, and those cash flows depend on whether secondary patents and formulation strategies can blunt the biosimilar entry.

Why Composition-of-Matter Patents Command the Highest M&A Premium

In M&A models, COM patents get the highest survival probability and therefore the lowest risk adjustment. A buyer paying for a drug protected by a young, well-prosecuted COM patent is effectively buying a calendar with very few question marks on it. Deals where the COM patent has more than 10 years of remaining life routinely price at 4x to 6x peak sales, while deals where the COM is in its final five years price at 1.5x to 3x.

This explains the structure of the Pfizer-Seagen deal in 2023. Pfizer paid $43 billion for Seagen, an antibody-drug conjugate (ADC) specialist whose lead products had COM patents on the linker chemistry running into the mid-2030s. The premium was not for current revenue. It was for a decade-plus of protected cash flows in a therapeutic class where biosimilar entry is particularly difficult because of the manufacturing complexity of ADCs.

Exclusivity Type 2: FDA Regulatory Exclusivity

FDA exclusivity is a separate animal from patent exclusivity, and confusing the two is one of the most common errors in pharmaceutical M&A diligence. The FDA awards exclusivity under 21 U.S.C. § 355 as a statutory market protection independent of any patent. It blocks ANDA approval or follow-on biologic approval for defined periods, regardless of whether the original product’s patents have expired.

The most valuable types are New Chemical Entity (NCE) exclusivity, Orphan Drug exclusivity, Pediatric exclusivity, and the various lesser categories (new clinical investigation, qualified infectious disease product, etc.). Each operates on its own clock and stacks differently with patent protection.

NCE Exclusivity vs. New Use Exclusivity

NCE exclusivity gives a five-year window during which the FDA cannot accept an ANDA referencing the new chemical entity for review. It runs from the date of first approval. The four-year mark matters because Paragraph IV ANDA filers can submit applications one year early if they certify that the patents are invalid, unenforceable, or not infringed by their product. This is why so much patent litigation begins exactly four years after a drug’s approval date.

New use exclusivity (sometimes called new clinical investigation exclusivity) gives three years of protection for new indications, new formulations, or new dosage strengths supported by new clinical data. The protection is narrower because it blocks only ANDA approval for the specific new use, not the underlying compound. Sponsors layer these three-year periods onto existing exclusivity to extend franchise life, particularly through pediatric indication studies and reformulations.

Orphan Drug Exclusivity and Its 7-Year Wall

The Orphan Drug Act of 1983 created a seven-year market exclusivity for drugs treating conditions affecting fewer than 200,000 patients in the United States. The exclusivity, codified at 21 U.S.C. § 360cc, prevents FDA approval of the same drug for the same indication for seven years from the date of orphan approval, even if all patents have expired.

Orphan exclusivity is functionally tighter than patent protection in some ways. While patents can be challenged, designed around, or invalidated, orphan exclusivity is essentially absolute for the indication it covers, with only narrow exceptions for clinically superior competitors. The Amgen acquisition of Horizon Therapeutics in 2023 for $28 billion turned heavily on Tepezza, a teprotumumab product with orphan designation for thyroid eye disease. The seven-year orphan wall, combined with manufacturing complexity, gave Amgen a clear runway despite Tepezza’s relatively modest patent estate.

When Orphan Exclusivity Blocks ANDA Approval

An orphan-designated drug’s seven-year window blocks the FDA from approving any application for the same drug for the same orphan indication. The key tension arises when a drug has multiple indications, some orphan and some not. Generic filers can sometimes carve out the orphan indication from their proposed labeling using a Section viii statement, allowing them to enter the market for non-protected uses while leaving the orphan use to the brand.

This carve-out strategy was central to the Lyrica (pregabalin) litigation, where Pfizer attempted to use a method-of-use patent and orphan-style indication protection to delay generic entry for fibromyalgia and neuropathic pain. The Federal Circuit’s decisions on label carve-outs have been mixed, but the trend has favored generic filers in cases where the carved-out indication can be physically excluded from the label without rendering the product misbranded.

Pediatric Exclusivity: The 6-Month Add-On Worth Billions

Pediatric exclusivity, authorized under 21 U.S.C. § 355a, adds six months to all existing patent and exclusivity periods for a drug if the sponsor completes FDA-requested pediatric studies. Six months sounds modest until you do the math on a $5 billion drug. Pfizer’s pediatric exclusivity on atorvastatin (Lipitor) extended the franchise’s protection by six months and preserved an estimated $2 billion to $3 billion in revenue, depending on the model.

Pediatric exclusivity attaches to the molecule, not to a specific indication or formulation, so it extends the entire patent estate and all FDA exclusivities for the drug. This makes it one of the highest-return investments in pharmaceutical research. Sponsors routinely spend $20 million to $50 million on pediatric trials and reap six-month extensions worth hundreds of millions to billions.

Case Study: Lipitor’s Pediatric Exclusivity and the $1 Billion Add

Pfizer’s atorvastatin franchise generated approximately $12 billion at peak. The drug was originally scheduled to lose exclusivity in mid-2011. Pediatric studies pushed the LOE to November 2011, preserving roughly six months of brand pricing at a time when U.S. monthly Lipitor sales exceeded $700 million. The pediatric exclusivity period, by itself, added more than $4 billion to Pfizer’s franchise economics on an asset that cost less than $50 million to study in adolescents.

The same logic applies to Plavix (clopidogrel) at Bristol-Myers Squibb and to Singulair (montelukast) at Merck. In each case, the six-month pediatric extension represented one of the highest-return R&D investments the company made in the molecule’s lifecycle.

How Regulatory Exclusivity Stacks With Patent Protection

Patent and FDA exclusivities operate independently and stack additively in some cases, with the later expiration controlling. If a drug has a COM patent expiring in 2028 and orphan exclusivity expiring in 2026, the effective LOE is 2028. If the patent expires in 2025 but pediatric exclusivity adds six months, the effective LOE is mid-2025. Acquirers map these calendars for every product in the target’s portfolio before signing.

EvaluatePharma’s 2024 industry outlook estimates that prescription drug sales at risk from patent expiration between 2024 and 2030 total approximately $300 billion globally, with biologics representing more than 60% of the exposure. The figure understates true exposure because it excludes biosimilar and authorized-generic cannibalization within franchise lines.

Exclusivity Type 3: Biologics Data Exclusivity Under BPCIA

The Biologics Price Competition and Innovation Act (BPCIA), enacted as part of the Affordable Care Act in 2010, created the biosimilar pathway in the United States and gave reference product sponsors 12 years of data exclusivity. The BPCIA, codified at 42 U.S.C. § 262, fundamentally changed how biologic drugs are valued in M&A. Before the BPCIA, biologics had no defined generic pathway and were treated almost as perpetual franchises. After the BPCIA, they have calendars.

The 12-Year Data Exclusivity for Biologics

The 12-year period begins on the date of first licensure of the reference biologic product. During the first four years, the FDA cannot even accept a biosimilar application referencing the product. During years five through 12, the FDA can accept applications but cannot grant licensure. The 12-year wall is independent of any patent protection and applies even if the reference product has no enforceable patents.

This 12-year period is materially longer than the equivalent small-molecule NCE exclusivity (5 years) and reflects the regulatory recognition that biologics require larger upfront investments and face different competitive dynamics. The BPCIA’s exclusivity period was negotiated heavily during the ACA debate, with industry pushing for 14 years and generics pushing for 7. The 12-year compromise has held despite repeated FTC and FDA calls for reduction.

How Biosimilar Developers Time Their Entry

Biosimilar developers track the 12-year wall and reference product patent calendars together. The pattern that has emerged: file the biosimilar application around year 9 or 10, complete FDA review during the late portion of the 12-year window, and launch immediately when both the BPCIA wall and the relevant patents have cleared.

The patent dance under 42 U.S.C. § 262(l) governs how biosimilar applicants and reference product sponsors exchange patent information. The Supreme Court’s decision in Amgen v. Sandoz (2017) held that the patent dance is not mandatory, but participation affects what relief either party can obtain in subsequent litigation. Most biosimilar developers now participate in the dance to preserve their litigation options and to surface patent disputes early enough to avoid launch-at-risk scenarios.

Humira’s Patent Thicket and the Delay Premium

AbbVie’s adalimumab, marketed as Humira, is the textbook case of biologic franchise extension through patent layering. The drug was first licensed in 2002, meaning the 12-year BPCIA exclusivity expired in 2014. Generic entry could have begun then. Instead, AbbVie assembled a patent estate of more than 130 issued U.S. patents covering formulation, manufacturing, dosing, and use, with expiration dates running from 2016 to 2034.

This patent thicket forced biosimilar developers into either licensing deals or extended litigation. AbbVie settled with each of the major biosimilar makers (Amgen, Boehringer Ingelheim, Samsung Bioepis, Mylan, and others) on terms that delayed U.S. launches until 2023. The settlements preserved roughly $20 billion of post-2014 Humira revenue that, absent the thicket, would have flowed to biosimilar developers and payers.

AbbVie’s 165-Patent Strategy and the 2023 Biosimilar Wave

The Humira patent strategy attracted Congressional attention and was the subject of FTC studies on patent thickets. AbbVie’s filings disclosed approximately 165 patents and patent applications related to Humira at the peak of the estate, with the Senate Judiciary Committee citing the strategy as a case study in evergreening. Whatever the policy debate, the financial result was clear: Humira generated more than $200 billion of cumulative revenue from 2002 through 2022, with roughly half of that coming after the original 12-year BPCIA exclusivity expired.

The 2023 biosimilar wave began with Amgen’s Amjevita launch in January, followed by eight additional biosimilars by year-end. AbbVie’s Humira revenue dropped from $21.2 billion in 2022 to $14.4 billion in 2023, a 32% decline. The erosion curve has been shallower than small-molecule analogs, with manufacturer rebate dynamics and formulary positioning slowing biosimilar uptake despite list price discounts of 55% to 85%.

Stelara, Enbrel, and the Biosimilar Pipeline

Johnson & Johnson’s ustekinumab, marketed as Stelara, faced biosimilar entry in 2024 after J&J reached settlements similar in structure to AbbVie’s Humira agreements. Stelara generated $10.9 billion in global sales in 2023, with U.S. revenue approximately 70% of that. Biosimilar entry began in January 2025, and J&J has guided to substantial revenue declines through 2026 and 2027.

Amgen’s etanercept, marketed as Enbrel, is the counter-example where patent layering has been even more effective than AbbVie’s Humira strategy. Enbrel was first licensed in 1998, so the BPCIA wall expired more than a decade ago, yet biosimilar entry in the U.S. remains blocked by Roche-Immunex patents licensed to Amgen, with expirations running to 2029. Sandoz and other biosimilar developers have litigated and lost at multiple stages, illustrating that the BPCIA exclusivity is just the floor of biologic protection.

Exclusivity Type 4: Patent Term Extension Under Hatch-Waxman

Patent term extension (PTE) under 35 U.S.C. § 156, enacted as part of the Hatch-Waxman Act of 1984, restores some of the patent life lost to FDA regulatory review. PTE is one patent per drug, capped at five years of extension, with the total post-approval patent term not exceeding 14 years. The selection of which patent to extend is a strategic decision worth hundreds of millions of dollars for high-revenue drugs.

How PTE Restores Patent Life Lost to FDA Review

The PTE calculation under 35 U.S.C. § 156(c) is half the time spent in IND-stage clinical testing plus the full time spent in NDA or BLA review at the FDA. The half-time rule for clinical testing means a drug with eight years of clinical development gets four years of extension credit for that period. The FDA review period adds the entire duration, typically 10 to 14 months for standard review and 6 to 8 months for priority review.

The five-year cap and the 14-year post-approval limit interact in ways that matter for the model. A drug approved 10 years after patent filing has 10 years of post-approval patent life remaining. PTE can add up to four years (capped by the 14-year ceiling). The five-year statutory cap rarely binds because most drugs use less than five years of half-clinical plus FDA review time.

The 14-Year Cap and the Half-Time Rule

The 14-year cap is the more frequent constraint. A drug approved seven years after patent filing has 13 years of post-approval patent life remaining at the time of approval. PTE can add one year (bringing the total to 14), even if the underlying clinical-plus-review time would calculate to four or five years.

Sophisticated patent groups time their COM patent filings to maximize the PTE benefit. Filing the COM patent too early means the 14-year cap binds and most of the PTE credit is wasted. Filing too late risks public disclosure or competitor priority. The optimal filing date is roughly 8 to 12 years before expected approval, depending on the therapeutic area’s typical development timeline.

Case Study: Eliquis and Patent Term Extension Math

Apixaban, marketed as Eliquis by Bristol-Myers Squibb and Pfizer, illustrates PTE’s value at the high end. The COM patent on apixaban was filed in 2001, originally set to expire in 2021 (with patent term adjustment, late 2022). PTE added approximately three years and three months, pushing the effective expiration to early 2026. Eliquis generated roughly $12 billion in 2023 global sales, of which BMS booked the U.S. portion. The three-plus years of PTE-driven extension is worth, conservatively, $25 billion in cumulative revenue and substantially more in net present value.

Eliquis is also currently subject to Inflation Reduction Act price negotiation, which begins to alter the LOE math in ways covered later in this piece. The PTE extension still matters because it controls the date when generic apixaban can enter the market, which is the floor of the IRA negotiation period.

Why a Single PTE Day Can Be Worth $30 Million

For a drug generating $10 billion in annual revenue, each day of additional exclusivity is worth approximately $27 million in revenue, or perhaps $20 million in net cash flow after rebates, manufacturing, and SG&A. This is why companies fight PTE calculation disputes at the USPTO to the bitter end, often litigating in the District of Columbia federal courts over questions of whether interim FDA review periods should count, whether IND stage starts on a specific date, and how to handle delays attributable to the sponsor versus the agency.

The Daiichi Sankyo PTE litigation over Olmesartan and the Photocure ALA-PDT litigation produced the controlling case law on how the FDA’s review period is calculated for PTE purposes. The Federal Circuit has generally read § 156 in favor of sponsors, but the procedural questions still produce expensive disputes.

How These Exclusivities Stack in M&A Valuation

The four exclusivity types do not operate in isolation. They stack, overlap, and interact in patterns specific to each drug. Sophisticated M&A models build a stacked exclusivity calendar showing the controlling protection at every quarter from deal signing to terminal value.

Comparison Table: Four Exclusivity Types Side-by-Side

Exclusivity Type

Statutory Source

Duration

Strength vs. ANDA

Strength vs. Biosimilar

Composition-of-matter patent

35 U.S.C. §§ 101, 154

20 years from filing

Very high (85–95% survival)

Very high (85–95% survival)

NCE exclusivity

21 U.S.C. § 355(j)(5)(F)(ii)

5 years (4 with Para IV)

Absolute during period

Not applicable

Orphan drug exclusivity

21 U.S.C. § 360cc

7 years for orphan indication

Absolute (narrow exceptions)

Absolute (narrow exceptions)

Pediatric exclusivity

21 U.S.C. § 355a

6 months added to all protections

Absolute during period

Absolute during period

BPCIA data exclusivity

42 U.S.C. § 262(k)(7)

12 years from first licensure

Not applicable

Absolute (4 years filing bar, 12 years approval bar)

Patent term extension

35 U.S.C. § 156

Up to 5 years, 14-year cap

Extends underlying patent

Extends underlying patent

Layering Exclusivities to Extend the Cash Flow Tail

The classic layering strategy combines a strong COM patent with method-of-use patents covering specific indications, formulation patents covering specific delivery systems, and pediatric extensions added at the back end. For a drug approved with eight years of clinical development behind it, this stack typically produces 12 to 15 years of effective post-approval exclusivity in the United States.

Biologics layer differently. The BPCIA’s 12-year wall is the floor, but manufacturing process patents, formulation patents, and device patents (for autoinjectors or other delivery systems) extend the practical exclusivity by years. Humira’s patent thicket exemplifies this approach, with formulation and dosing patents pushing biosimilar entry to 2023 even though the 12-year wall expired in 2014.

Paragraph IV Challenges and the Litigation Risk Discount

Paragraph IV certifications are the trigger for most pharmaceutical patent litigation in the United States. Under the Hatch-Waxman Act, a generic ANDA filer can certify that one or more patents listed in the Orange Book are invalid, unenforceable, or not infringed by the generic product. This Paragraph IV certification is treated as an act of patent infringement under 35 U.S.C. § 271(e)(2), giving the brand company standing to sue immediately.

How ANDA Filers Time Their Paragraph IV Notices

The first generic to file a substantially complete ANDA with a Paragraph IV certification is eligible for 180 days of generic exclusivity under 21 U.S.C. § 355(j)(5)(B)(iv). This 180-day window is the prize that drives the entire Paragraph IV strategy, because the first filer can sell its generic without competition from other generics for six months, capturing 30% to 50% of the brand’s revenue at modest discounts to the original price.

The race to file begins exactly four years after the brand’s NDA approval for drugs subject to NCE exclusivity, with multiple generic filers often submitting on the same day to qualify as joint first filers. The Federal Circuit’s decisions on what constitutes substantial completeness and on how joint first-filer status is allocated have produced extensive case law, particularly in the wake of the FDA’s pending ANDA queue management decisions.

The 30-Month Stay and What It Buys Innovators

When a brand company sues a Paragraph IV ANDA filer within 45 days of receiving the certification notice, the FDA automatically stays approval of the ANDA for 30 months under 21 U.S.C. § 355(j)(5)(B)(iii). The 30-month stay is one of the highest-value procedural tools in pharmaceutical IP. It buys the brand company 30 months of additional exclusivity without any merits determination on the underlying patents.

The 30-month stay can be shortened or lifted by court order, but in practice most stays run their full course. For a drug generating $5 billion in U.S. revenue, a 30-month stay is worth approximately $12 billion in preserved revenue at brand pricing, less the manageable costs of patent litigation. This is why brand companies sue every Paragraph IV filer they can, even on patents they expect to lose: the stay alone justifies the litigation.

Settlement vs. Trial: The Reverse-Payment Question After Actavis

Most Paragraph IV cases settle before trial. The settlements typically include an entry date for the generic, sometimes years before patent expiration, in exchange for the generic company dropping its invalidity challenge. The Supreme Court’s decision in FTC v. Actavis, 570 U.S. 136 (2013), held that reverse-payment settlements (where the brand pays the generic) are subject to antitrust scrutiny under a rule-of-reason analysis.

The Actavis decision did not ban reverse-payment settlements, but it raised the cost of structuring them and led to a shift toward licensed entry dates as the primary settlement currency. Settlements involving large reverse payments have decreased in frequency since 2013, but the FTC continues to scrutinize settlement structures, particularly those involving authorized generic agreements or business deals that arguably substitute for cash payments.

PTAB and Inter Partes Review as M&A Risk Factors

The America Invents Act of 2011 created inter partes review (IPR), a Patent Trial and Appeal Board (PTAB) proceeding for challenging patent validity outside of federal court. IPR has become a substantial risk factor for pharmaceutical patents, particularly secondary patents covering formulations, dosing regimens, and crystalline forms.

How IPR Petitions Affect Deal Pricing

IPR institution rates for pharmaceutical patents have run between 60% and 70%, with final invalidation rates of approximately 80% of instituted petitions. The numbers vary substantially by patent type. COM patents face IPR institution rates closer to 30% and invalidation rates of approximately 60% of those instituted. Method-of-use and formulation patents face higher institution and invalidation rates.

For M&A modeling, a pending IPR on a target’s patent reduces the survival probability assigned to that patent in the rNPV calculation. A patent with an instituted IPR but no final written decision typically gets a 30% to 40% survival probability, down from 70% to 85% for an unchallenged patent of the same type. The discount on the asset can run 5% to 15%, depending on which products are protected by the challenged patent.

The Fintiv Doctrine and Its Effect on IPR Discretion

The PTAB’s Fintiv doctrine, named for Apple v. Fintiv, IPR2020-00019, gives the Board discretion to deny IPR institution when parallel district court litigation is sufficiently advanced. The doctrine reduces IPR availability for pharmaceutical patents being litigated in Hatch-Waxman cases, where district court trials often occur on accelerated schedules tied to the 30-month stay.

The 2024 USPTO rulemaking and subsequent litigation have unsettled the Fintiv doctrine’s exact contours, with the Director’s office taking a more case-specific approach to discretionary denial. For deal modelers, the practical effect is that pharmaceutical patents in active Hatch-Waxman litigation get higher survival probabilities than they would absent the Fintiv overlay, because the IPR pathway is less reliably available to challengers.

Real M&A Cases Where Exclusivity Drove the Price

The mechanics of exclusivity stacking are visible in the public valuation language of major pharmaceutical M&A transactions. Four recent deals illustrate how each exclusivity type shows up in the price.

BMS-Celgene: The Revlimid CVR and Volume-Limited Entry

Bristol-Myers Squibb’s $74 billion acquisition of Celgene in 2019 was largely a bet on three Celgene assets: Revlimid (lenalidomide), Pomalyst (pomalidomide), and the in-development bb2121 (idecabtagene vicleucel, now Abecma). The deal included a contingent value right (CVR) tied to FDA approvals of three pipeline products, but the core valuation was Revlimid’s cash flow tail.

Revlimid had a patent estate with expirations running from 2022 to 2027, including the Polymorph patents covering specific crystalline forms. Celgene had settled with the major ANDA filers (Natco, Dr. Reddy’s, Cipla, others) on volume-limited entry agreements that allowed generics to launch with capped market shares in defined percentages each year from 2022 through 2025, with unlimited entry from 2026. The volume-limited entry structure preserved roughly $30 billion to $35 billion of Revlimid revenue compared with a hard generic launch in 2022.

The BMS deal model treated these volume caps as quasi-exclusivities, applying probability adjustments for ANDA filer compliance and FDA enforcement of the agreements. The realized Revlimid revenue from 2022 through 2024 has tracked the model reasonably well, with volume-limited generics taking 20% to 35% of the U.S. market in each year and brand Revlimid retaining the balance.

AbbVie-Allergan: Botox Trade Secrets and Method Patents

AbbVie’s $63 billion acquisition of Allergan in 2020 was driven primarily by Botox (onabotulinumtoxinA). Botox is a biologic, but its manufacturing involves trade secret processes that are extraordinarily difficult to replicate. Allergan’s patent estate covered formulation, dosing regimens, and specific therapeutic uses, but the deeper protection was the manufacturing trade secret around the toxin production and purification process.

Revance Therapeutics has launched a competing botulinum toxin product (DaxibotulinumtoxinA, marketed as Daxxify) with a different formulation, and several biosimilar-style competitors are in development. The Allergan trade secrets have not been litigated in a way that publicly establishes their boundaries, but the empirical evidence is that Botox has maintained near-monopoly aesthetic and therapeutic market share more than 30 years after first FDA approval, which is functionally indistinguishable from continuous exclusivity.

Amgen’s $28 billion acquisition of Horizon Therapeutics, which closed in 2023 after FTC review, was a play on Tepezza (teprotumumab) for thyroid eye disease and Krystexxa (pegloticase) for chronic refractory gout. Both products carried orphan designations, which provided seven-year FDA exclusivity walls and offered relatively clean cash flow forecasts compared with non-orphan biologics of similar revenue size.

The Tepezza orphan exclusivity, combined with the manufacturing complexity of producing a humanized monoclonal antibody for a small patient population, gave Amgen a durable franchise. The FTC’s challenge to the deal focused on potential bundling concerns rather than patent or exclusivity questions, and the deal closed after consent decree negotiations.

Pfizer-Seagen: ADC Linker Patents and Composition Claims

Pfizer’s $43 billion acquisition of Seagen in 2023 was the largest pharmaceutical M&A transaction since BMS-Celgene. Seagen’s value was concentrated in its ADC platform, with marketed products including Adcetris (brentuximab vedotin), Padcev (enfortumab vedotin), Tukysa (tucatinib), and Tivdak (tisotumab vedotin). The platform’s value rested on linker chemistry patents covering the conjugation between the antibody and the cytotoxic payload, with composition claims running into the mid-2030s.

ADCs are particularly difficult biosimilar targets because the complexity of the linker chemistry, the cytotoxic payload, and the conjugation process compound the manufacturing challenges of any biologic. Pfizer’s model assumed substantially shallower erosion curves for the Seagen ADCs than would apply to comparable monoclonal antibodies, which justified the price relative to current revenue. The 2024 results have generally supported the thesis, with Padcev growth particularly strong in metastatic urothelial cancer following the EV-302 readout.

Forecasting LOE: How Analysts Model Generic Entry

Forecasting loss of exclusivity is its own discipline within pharmaceutical analysis. The output is a date and a probability distribution around that date, plus an erosion curve describing how revenue declines after entry begins.

Generic Entry Probability Curves

Generic entry probability is conditional on the strength of the patent estate, the number of expected ANDA filers, the API availability, and the regulatory complexity of the dosage form. For simple solid oral dosage forms with abundant API supply and standard formulations, multiple generic filers typically enter within 12 months of the controlling patent expiration. For complex generics (inhaled products, transdermals, ophthalmic suspensions), the timeline is longer and the number of competitors smaller.

The probability distribution around the LOE date typically has a 6-month standard deviation for clean patent estates and a 12 to 18-month standard deviation for contested estates with active Paragraph IV litigation. The asymmetry usually favors earlier entry, because settlement dates and at-risk launches can compress the timeline, while delays beyond the natural expiration are uncommon.

Erosion Curves: Small Molecule vs. Biologic

Small molecule erosion curves are steeper and more predictable than biologic curves. IQVIA’s data on the 2014 to 2022 period showed average first-year revenue erosion of 78% for small molecules with three or more generic entrants and 91% for those with five or more. By month 24, residual brand revenue averaged 7% to 12% of pre-LOE peak.

Biologic erosion curves are shallower. Humira’s 2023 to 2024 trajectory showed roughly 36% revenue erosion in the first 12 months of biosimilar competition, even with nine biosimilars on the market. Remicade (infliximab) showed similar shallow erosion in its early biosimilar years, with revenue declining 30% to 40% over the first two years of biosimilar competition before accelerating as Pfizer’s Inflectra and Renflexis (Samsung Bioepis) gained payer adoption.

Manufacturing Exclusivity and Trade Secret Protection

Patents and FDA exclusivities are the visible exclusivity types, but manufacturing trade secrets are an underrecognized form of protection that can extend franchise economics well beyond the patent and regulatory calendar.

Process Patents and Why They Matter for Complex Generics

Process patents cover the methods for manufacturing the drug substance and the drug product. For most small molecules, process patents are easy to design around because synthetic chemistry offers multiple routes to the same compound. For complex generics and biologics, process patents can be substantially more difficult to circumvent.

The Glatopa case (Sandoz’s generic glatiramer acetate for Teva’s Copaxone) showed how process complexity can delay generic entry. Glatiramer acetate is a heterogeneous mixture of polypeptides, not a single defined molecule, and Sandoz had to develop and validate its own manufacturing process. The complexity contributed to a generic entry timeline that was years later than would have applied to a typical small molecule of similar revenue size.

Trade Secrets in Biologics Manufacturing

Biologic manufacturing processes are often protected as trade secrets rather than patents. Cell line selection, fermentation conditions, downstream processing, formulation, and fill-finish all involve proprietary knowledge that biosimilar developers must reverse-engineer or develop independently. The reverse-engineering takes years and millions of dollars even when the patent estate is weak, which is one reason why biosimilars have rarely launched at-risk in the United States.

The Defend Trade Secrets Act of 2016 and state trade secret laws provide civil remedies for misappropriation. Trade secret protection is potentially indefinite, as long as the secret is maintained. The practical limit is the difficulty of keeping manufacturing process knowledge secret across a global supply chain and a multi-decade product lifecycle, particularly when key employees move between companies.

Geographic Exclusivity: Why U.S. Patents Drive the Highest Valuations

Global pharmaceutical revenue is geographically concentrated in the United States, which typically represents 40% to 60% of branded drug revenue despite the U.S. population being roughly 4% of the global total. The pricing differential drives the asymmetric weight that U.S. patents and exclusivities receive in valuation models.

SPCs in Europe and Their Comparison to U.S. PTE

Supplementary Protection Certificates (SPCs) under EU Regulation 469/2009 provide patent term extension in Europe that is broadly analogous to U.S. PTE but with different calculation rules. SPC duration is the period between patent filing and first EU marketing authorization, minus five years, capped at five years total. The 14-year post-authorization cap that constrains U.S. PTE does not apply in Europe in the same way.

For dual-jurisdiction analysis, the U.S. PTE typically expires earlier than the European SPC for the same drug, which means biosimilar and generic entry timing differs between the two markets. Acquirers building global revenue forecasts run separate exclusivity calendars for each major market and aggregate the geographic exposures into the rNPV.

Japan, China, and the Patent Linkage Question

Japan introduced patent term extension for pharmaceutical patents under its 1987 amendments to the patent law, with terms similar in structure to U.S. PTE. Japan also operates an informal patent linkage system through PMDA review practices that delay generic approvals during patent litigation, although the linkage is less formal than the U.S. Orange Book system.

China’s 2020 patent law amendments introduced a formal patent linkage system effective in 2021, with limited patent term extension provisions for drugs and a four-year administrative waiting period for generic challenges. The China linkage system is still developing in practice, but the trend toward stronger pharmaceutical IP enforcement in China affects how multinational pharma values its Asian growth exposure in M&A models.

Pricing Pressure After LOE

Loss of exclusivity is one cause of price pressure on pharmaceutical revenue. The other major causes are payer formulary management, manufacturer rebate dynamics, and, increasingly, statutory price negotiation under the Inflation Reduction Act.

IRA Negotiation and the New Exclusivity Math

The Inflation Reduction Act of 2022 authorizes Medicare to negotiate prices for certain high-spend drugs that have been on the market for nine years (small molecules) or 13 years (biologics) without generic or biosimilar competition. The first 10 drugs selected for negotiation, announced in August 2023, included Eliquis, Jardiance, Xarelto, Januvia, Farxiga, Entresto, Enbrel, Imbruvica, Stelara, and Fiasp/NovoLog.

The negotiated prices, which take effect January 1, 2026, will reduce Medicare reimbursement by 38% to 79% depending on the drug, according to CMS announcements. The negotiation effectively shortens the economic exclusivity of a drug by imposing price reductions years before patent or BPCIA expiration. For deal modeling, this means the practical LOE date now has two components: the patent or exclusivity date, and the IRA negotiation date, with the earlier of the two often controlling the revenue trajectory.

How Medicare Price Setting Changes M&A Discounting

Pharmaceutical M&A models built before 2022 assumed that brand pricing held until generic or biosimilar entry. Models built after the IRA must now incorporate price negotiation as a discrete event, typically occurring 9 or 13 years after launch depending on the modality. The result is that long-duration exclusivity is worth less in IRA terms than it was before, because the cash flow tail is truncated by the negotiation date.

Biologics are particularly affected by the 13-year IRA threshold relative to the 12-year BPCIA exclusivity. A biologic that successfully extends franchise life through patent thickets past year 13 now faces IRA negotiation before biosimilar entry, which compresses the value of the patent extension strategy. AbbVie’s post-Humira pipeline (Rinvoq, Skyrizi) is being modeled with this new dynamic in mind, as is Merck’s post-Keytruda transition.

What This Means for Dealmakers

The four exclusivity types covered here are the dominant variables in pharmaceutical M&A valuation, but they do not operate as a checklist. They interact with each other, with FDA designation strategies, with patent litigation outcomes, and with the broader pricing and policy environment.

Diligence Checklist for Pharma Acquirers

Effective diligence on pharmaceutical exclusivity has four core elements. First, build a stacked exclusivity calendar showing the controlling protection for every product in the target’s portfolio at every quarter through year 20. Second, assess the strength of each component patent through independent counsel review, with particular attention to obviousness vulnerabilities under KSR. Third, model multiple generic entry scenarios with probability weights, including settlement-driven entry, at-risk launch, and authorized generic responses. Fourth, overlay the IRA negotiation calendar and Medicare Part D dynamics on the post-LOE revenue tail.

Patent intelligence platforms such as DrugPatentWatch, IPD Analytics, and Cortellis are commonly used to assemble the Orange Book data, Paragraph IV filing history, and exclusivity calendars that feed into these models. The data quality matters because a misread exclusivity date can shift the valuation by hundreds of millions of dollars on a major asset.

When to Walk Away From an Asset

The signs that an asset is worth less than the seller’s ask usually concentrate in a few areas. Heavy reliance on secondary patents (formulation, dosing, crystalline form) with short remaining life and active PTAB challenges suggests a thin exclusivity moat. Concentration of revenue in a single product nearing LOE without a credible follow-on indication or formulation extension implies a steep cash flow cliff. Pending Paragraph IV litigation with weak patent positions and high-quality generic challengers (Teva, Sandoz, Mylan/Viatris, Dr. Reddy’s, Aurobindo) suggests early entry risk.

Walking away is the right answer when the exclusivity stack does not support the seller’s revenue tail assumptions. The pharmaceutical M&A market has examples of acquirers who pressed forward despite weak exclusivity diligence and absorbed multibillion-dollar impairments within three years of closing. The cases are less famous than the successful deals, but they are visible in the goodwill impairment line of large pharma annual reports.

Key Takeaways

Composition-of-matter patents are the strongest form of pharmaceutical exclusivity and command the highest M&A premiums. Their 20-year term, less the development period, defines the floor of a drug’s protected revenue runway.

FDA regulatory exclusivities (NCE, orphan, pediatric, new use) operate independently of patents and provide statutory protection that survives even after patents fall. Pediatric exclusivity’s 6-month extension is one of the highest-return investments in pharmaceutical R&D.

The BPCIA’s 12-year data exclusivity is the floor of biologic protection, but patent thickets covering formulation, dosing, and manufacturing can extend the practical exclusivity by a decade or more, as Humira and Enbrel both illustrate.

Patent term extension under Hatch-Waxman restores some of the patent life lost to FDA review, with the 14-year post-approval cap usually binding more frequently than the five-year statutory limit. A single day of PTE on a $10 billion drug is worth approximately $27 million in revenue.

The IRA’s price negotiation provisions have created a second LOE date for high-spend drugs, effectively truncating the cash flow tail at 9 or 13 years after launch and changing the math on long-duration exclusivity strategies.

Diligence on exclusivity is the central exercise in pharmaceutical M&A valuation. Misreading the exclusivity calendar by 6 to 12 months can shift the valuation of a major asset by $200 million to $500 million.

FAQ

How long does composition-of-matter patent exclusivity last in pharmaceuticals?

U.S. composition-of-matter patents run 20 years from the earliest non-provisional filing date. After accounting for development time, the practical post-approval term is typically 8 to 12 years, with patent term extension adding up to five years subject to a 14-year post-approval cap.

What is the difference between FDA exclusivity and patent exclusivity?

Patent exclusivity is granted by the USPTO and enforced through patent infringement litigation. FDA exclusivity is granted by the FDA under 21 U.S.C. § 355 and operates as an administrative bar on approval of competing applications. The two operate independently, and a drug can have one without the other.

How does the 180-day generic exclusivity work under Hatch-Waxman?

The first generic to file a substantially complete ANDA with a Paragraph IV certification receives 180 days of marketing exclusivity once it launches, during which the FDA cannot approve other generics of the same drug. The exclusivity is the primary economic incentive for generic challenges of pharmaceutical patents.

What does loss of exclusivity (LOE) mean for a drug’s revenue?

LOE means the date when the controlling patent or regulatory exclusivity expires and generic or biosimilar competitors can enter the market. For small molecules, revenue typically declines 70% to 90% within 24 months of LOE. For biologics, declines are shallower (30% to 60% over three to five years) due to manufacturing complexity and slower biosimilar uptake.

Why are biologics protected longer than small molecules under U.S. law?

The BPCIA provides 12 years of data exclusivity for biologics, compared with five years of NCE exclusivity for small molecules. Congress justified the longer period based on biologics’ larger development investments and the additional regulatory complexity of biosimilar review under 42 U.S.C. § 262(k).

What is a patent thicket in pharmaceutical M&A diligence?

A patent thicket is a layered set of patents covering different aspects of a drug (composition, formulation, dosing, manufacturing, methods of use) that force generic or biosimilar challengers to clear multiple patents before launching. Humira’s approximately 165-patent estate is the most-cited example, having delayed U.S. biosimilar entry from 2014 to 2023.

How does the Inflation Reduction Act change pharmaceutical M&A valuation?

The IRA’s Medicare price negotiation provisions create a second LOE date at 9 years (small molecules) or 13 years (biologics) after launch, with negotiated prices reducing revenue by 38% to 79% depending on the drug. The negotiation effectively truncates the long-duration cash flow tail that historically supported high M&A premiums for late-life drugs.

What is a Paragraph IV challenge and how does it affect drug exclusivity?

A Paragraph IV certification is a generic filer’s assertion that one or more patents listed in the Orange Book for a brand drug are invalid, unenforceable, or not infringed. The certification triggers patent infringement litigation under 35 U.S.C. § 271(e)(2) and a 30-month FDA stay on ANDA approval if the brand sues within 45 days.

How do acquirers price the risk of patent litigation in pharma deals?

Acquirers apply probability weights to each patent in the exclusivity stack based on the strength of the patent type, the quality of the prior art, and the status of any pending challenges. Composition-of-matter patents typically receive 85% to 95% survival probability. Method-of-use patents receive 40% to 70%. Formulation patents receive 30% to 50%. The weighted exclusivity calendar feeds directly into the risk-adjusted NPV.

What is the role of orphan drug exclusivity in M&A premiums?

Orphan drug designation under the Orphan Drug Act provides seven years of FDA exclusivity for drugs treating conditions affecting fewer than 200,000 U.S. patients. The exclusivity is functionally absolute for the orphan indication and is independent of patent protection, which makes orphan-designated assets attractive M&A targets even when their patent estates are weak. Amgen’s $28 billion acquisition of Horizon Therapeutics in 2023 was largely driven by Tepezza’s orphan designation for thyroid eye disease.

References

IQVIA Institute for Human Data Science. (2023). The Use of Medicines in the U.S. 2023: Usage and Spending Trends and Outlook to 2027. IQVIA Institute.

FTC v. Actavis, Inc., 570 U.S. 136 (2013).

U.S. Patent and Trademark Office. (n.d.). 35 U.S.C. § 156 – Extension of patent term. United States Code.

U.S. Food and Drug Administration. (n.d.). Approved Drug Products with Therapeutic Equivalence Evaluations (Orange Book). FDA.

Drug Price Competition and Patent Term Restoration Act of 1984 (Hatch-Waxman Act), Pub. L. No. 98-417, 98 Stat. 1585.

Biologics Price Competition and Innovation Act of 2009, 42 U.S.C. § 262 (as part of the Patient Protection and Affordable Care Act, Pub. L. No. 111-148).

Amgen Inc. v. Sandoz Inc., 137 S. Ct. 1664 (2017).

Bristol-Myers Squibb Company. (2019). Form 8-K: Completion of Acquisition of Celgene Corporation. U.S. Securities and Exchange Commission.

AbbVie Inc. (2024). Form 10-K Annual Report for Fiscal Year 2023. U.S. Securities and Exchange Commission.

Pfizer Inc. (2023). Form 8-K: Completion of Acquisition of Seagen Inc. U.S. Securities and Exchange Commission.

Centers for Medicare & Medicaid Services. (2024). Medicare Drug Price Negotiation Program: Negotiated Prices for Initial Price Applicability Year 2026. CMS.

U.S. Senate Committee on the Judiciary, Subcommittee on Antitrust, Competition Policy and Consumer Rights. (2021). Ensuring Affordable & Accessible Medications: Examining Competition in the Prescription Drug Market. Hearing Report.

EvaluatePharma. (2024). World Preview 2024: Outlook to 2030. Evaluate Ltd.

Orphan Drug Act of 1983, Pub. L. No. 97-414, 96 Stat. 2049, codified at 21 U.S.C. §§ 360aa-360ff.

21 U.S.C. § 355a – Pediatric studies of drugs.

America Invents Act, Pub. L. No. 112-29, 125 Stat. 284 (2011).

Apple Inc. v. Fintiv, Inc., IPR2020-00019, Paper 11 (P.T.A.B. Mar. 20, 2020) (precedential).

Amgen Inc. (2023). Form 8-K: Completion of Acquisition of Horizon Therapeutics plc. U.S. Securities and Exchange Commission.

Federal Trade Commission. (2023). Statement Regarding Use of Brand Pharmaceutical Patent Listings in the FDA Orange Book. FTC Policy Statement.

Council Regulation (EC) No. 469/2009 of 6 May 2009 concerning the supplementary protection certificate for medicinal products. Official Journal of the European Union.