How the Hatch-Waxman Act Created the Most Lucrative Six Months in Pharmaceuticals

Before 1984, the United States pharmaceutical market operated without a functional generic drug industry. A manufacturer that wanted to sell a copy of a post-1962 branded drug was required to run its own full clinical trials, duplicating safety and efficacy data the FDA already held. That regulatory cost—prohibitive by design, if not by intent—kept generic drugs at 19% of total prescriptions. Innovators held perpetual market monopoly not primarily because of patents, but because the regulatory wall around the NDA was itself a barrier.

The Drug Price Competition and Patent Term Restoration Act of 1984 (Hatch-Waxman) dismantled that wall on both sides of the ledger. For brand companies, it restored patent time lost to FDA review and codified data exclusivity periods—5 years for new chemical entities, 3 years for new clinical studies supporting supplements. For generic companies, it created the Abbreviated New Drug Application pathway, replacing the requirement for clinical trials with a demonstration of bioequivalence. And then, buried in the statute, it created something neither side had asked for: a mechanism to litigate patent validity before a product is ever sold.

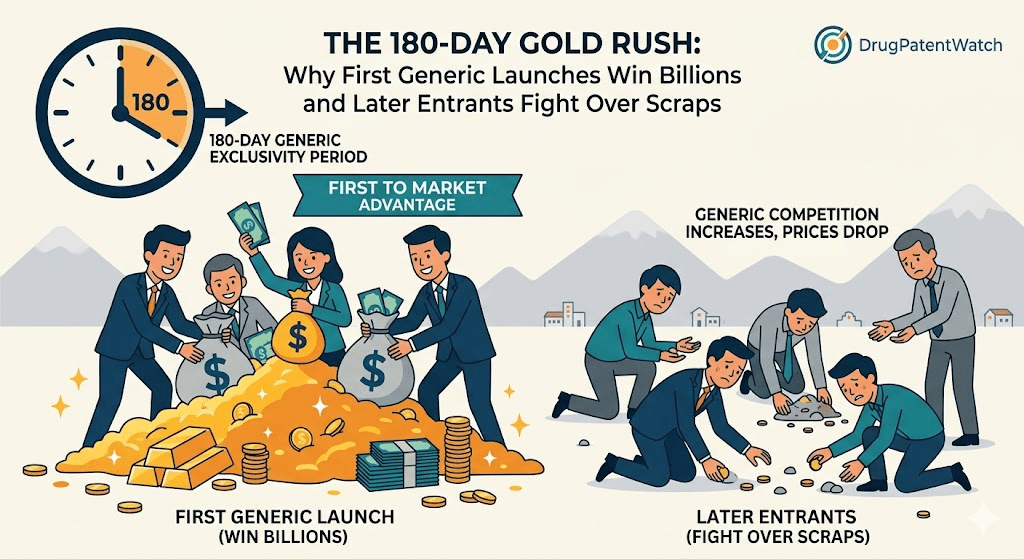

That mechanism—the Paragraph IV certification—and the 180-day exclusivity reward attached to it, produced the most asymmetric prize structure in industrial commerce. The first generic company to successfully challenge a brand-name patent and survive the litigation earns a six-month legal monopoly on the generic market. During that window, generic prices sit 20% to 40% below the brand price rather than the 90%-plus collapse that arrives when the market floods. For a blockbuster molecule, the difference between first and second is not a few percentage points—it is the difference between nine-figure revenue and commodity economics.

What the Paragraph IV Certification Actually Does to a Patent Holder

Why Filing a Paragraph IV Is a Declaration of War, Not a Regulatory Technicality

An ANDA filer must certify the status of every patent listed in the FDA’s Orange Book for the reference listed drug. The four certifications (I through IV) run from “no patent filed” to “the patent will expire before my launch date.” Paragraph IV—the only certification with teeth—states that the listed patent is invalid, unenforceable, or will not be infringed by the generic product.

The certification is, by statutory construction, an artificial act of infringement. It confers federal court jurisdiction over a patent dispute before a single generic unit has been manufactured for commercial sale. The brand holder, upon receiving the mandatory notice letter, has 45 days to sue. If they do, an automatic 30-month stay of FDA final approval for the ANDA attaches—effectively freezing the regulatory clock while litigation proceeds.

The notice letter itself must contain a detailed factual and legal basis for the invalidity or non-infringement position. These letters routinely run 50 to 200 pages. They are litigation documents dressed in regulatory clothing. Experienced IP teams at Teva, Mylan (Viatris), Sun Pharma, and Sandoz treat them as the opening brief in a case that may take four to six years to resolve.

How the 30-Month Stay Works—and When It Expires Without a Decision

The 30-month stay is the brand’s primary defensive instrument. It prevents the FDA from issuing final approval to the generic ANDA for approximately two and a half years, buying time for district court proceedings. If litigation is resolved in the brand’s favor before the stay expires, the ANDA is blocked. If the generic wins, FDA approval can proceed.

The problem arises when the stay expires and no final decision has been issued, or when the district court rules for the generic but the brand appeals. At that point, the generic has FDA approval in hand and a favorable (if not yet final) court ruling. The market sits open. The question is whether to launch.

How the 180-Day Exclusivity Translates Into Actual Revenue Dollars

The Duopoly Premium: Why the First Filer Can Price at 25% Off, Not 90% Off

When a generic company launches under 180-day exclusivity, it competes against one party: the brand. The FDA is legally prohibited from approving any subsequent ANDAs during this period. A pharmacist cannot swap the brand for a competitor generic because no competitor generic exists yet—only the first filer’s product and, potentially, an authorized generic.

This structural duopoly produces pricing dynamics qualitatively different from fully commoditized generic markets. FDA retail sales data documents the price erosion curve:

Competitors in Market

Generic Price as % of Brand

Approximate Price Reduction

1 (first filer only)

60–80%

20–40%

2

50–55%

45–50%

3

33–40%

60–67%

6–9

10–20%

80–90%

10+

Below 5%

Over 95%

The 180-day window captures the left side of this table. Later entrants arrive into the right side. The price difference between being first and being fourth is the difference between a drug that funds a pipeline and one that funds overhead.

Industry studies show generic companies generate 60% to 80% of their total lifetime profit for a given molecule inside this single six-month window. The Association for Accessible Medicines estimated that 180-day exclusivity launches in 2020 alone saved the healthcare system nearly $20 billion—a figure that reflects both the pricing transition and the volume shift away from brands.

Why First-Mover Market Share Persists 10 Years After Launch

Volume compounds the revenue advantage. The first generic establishes supply chain relationships, pharmacy stock positions, and formulary preference before any competitor arrives. Research tracking generic market dynamics finds that the first entrant holds approximately 6 percentage points more market share than subsequent entrants even a decade after launch.

The persistence is not market power in any regulatory sense—it is inertia. Wholesalers and pharmacy chains that source their supply from the first filer have operational relationships, contracts, and reliability data on that supplier. A second or third generic manufacturer arriving six months later needs to offer a compelling price discount to displace an entrenched incumbent. That price competition accelerates the erosion curve for later entrants, further concentrating profits at the front of the queue.

For injectable drugs sold directly to hospital systems—products like vancomycin formulations, oncology injectables, or long-acting antipsychotics—this dynamic is more durable still. Hospital purchasing consortiums negotiate annual or multi-year supply contracts. A manufacturer that wins the first contract for a product like a generic version of Invega Sustenna (paliperidone palmitate) may retain that position for years before a competitor unsettles it.

The Authorized Generic: How Brand Companies Tax the First Filer’s Prize

Why an Authorized Generic Cuts First-Filer Revenue by Up to 52%

The 180-day exclusivity blocks other ANDAs. It does not block the brand. A brand company can launch its own generic version—manufactured on the same line, approved under the existing NDA, packaged with a generic label—on the same day the first-filer launches. This product, the authorized generic, is not subject to the 180-day exclusivity provision because it never filed an ANDA.

FTC analysis of authorized generic economics is unambiguous on the financial impact:

Revenue for the first filer drops by 40% to 52% during the 180-day period when an authorized generic is present.

Wholesale prices are 7% to 14% lower than in markets without authorized generics.

First-filer revenues in the 30 months following exclusivity are 53% to 62% lower when the brand launched an authorized generic alongside them.

Companies with a documented history of authorized generic deployment—Pfizer with Lipitor, Merck with Zocor, AstraZeneca with Prilosec—are effectively known quantities. Any revenue model built on a Paragraph IV challenge against these companies must haircut the exclusivity period value by roughly 50%. Generic strategists who build these projections treat authorized generic probability as a near-binary variable that dominates the financial model.

The ‘No-AG’ Settlement: What Brand Companies Give Up in Exchange for Delay

Authorized generic threat is frequently the negotiating lever in Hatch-Waxman patent settlements. A brand company agrees not to launch an authorized generic during the first filer’s exclusivity period in exchange for the generic company delaying its entry date. The generic gets the full duopoly prize, undiluted. The brand gets a longer exclusivity runway.

The FTC’s position is that these “no-AG” commitments are a form of reverse payment—valuable consideration flowing from brand to generic in exchange for delayed competition—and scrutinizes them under antitrust standards established in FTC v. Actavis (2013). Since Actavis, courts apply a rule-of-reason analysis to reverse payment settlements, meaning neither pure no-AG agreements nor cash payments are per se illegal, but both require demonstrating competitive justification.

The practical implication: no-AG clauses are most commonly offered when the brand’s litigation position is weak or when the authorized generic would generate less revenue than the patent extension’s value. For a generic IP team evaluating a settlement offer, the value of a no-AG clause should be modeled explicitly. A 50% lift on six months of duopoly revenue on a $2 billion molecule is a $200-plus million swing.

How ‘At-Risk’ Generic Launches Work—and When They Destroy Companies

The Risk-Reward Structure of Launching Before Final Patent Resolution

When the 30-month stay expires or when a district court rules for the generic, the ANDA holder faces a decision with a payoff structure unlike almost anything else in corporate finance. Launch at risk means selling the generic product while patent litigation is still live—before a final, non-appealable court ruling has confirmed the right to market.

The upside is real: months or years of revenue on a molecule that may generate $100 million to $500 million monthly at duopoly pricing. On a drug like Plavix or Protonix, even a two-month head start on a settlement-timed entry yields hundreds of millions of dollars.

The downside is catastrophic. If the appellate court reverses and finds the patent valid and infringed, damages are calculated not on the generic’s profits—which are modest given thin gross margins—but on the brand’s lost profits. Brand lost profits account for the price erosion the at-risk launch caused (the brand had to cut price to compete) plus the volume shifted to the generic. Those damages can be trebled for willful infringement. The liability cap, in theory, is the brand’s total lost profit for the infringement period, potentially running to billions of dollars.

The Protonix Case: $2.15 Billion Explains Why Boardrooms Fear At-Risk Launches

Wyeth (acquired by Pfizer) held patents on Protonix (pantoprazole), a proton pump inhibitor with peak sales near $1.9 billion annually. Teva and Sun Pharma both filed Paragraph IV challenges and, after the 30-month stay expired with litigation unresolved, launched generic pantoprazole at risk in late 2007 and early 2008.

The commercial impact was immediate. Protonix brand sales dropped roughly 80% as the generics captured the market. In 2008, brand revenues fell from nearly $1.9 billion to approximately $395 million. Pfizer, which had completed its Wyeth acquisition by then, pursued damages aggressively.

In April 2010, a New Jersey jury upheld patent validity. The generics had been wrong. In June 2013, Teva and Sun settled for a combined $2.15 billion—$1.6 billion from Teva and $550 million from Sun. The settlement remains among the largest in pharmaceutical patent history and stands as the controlling example in any at-risk launch analysis. Teva absorbed a liability that erased years of generic revenue from pantoprazole and depressed earnings for multiple subsequent quarters.

The Apotex-Plavix Channel Flood: How an Injunction Still Costs $442 Million

Bristol-Myers Squibb and Sanofi co-marketed Plavix (clopidogrel bisulfate), which was generating over $6 billion annually at its peak. Apotex challenged the patent, and following a failed settlement agreement—one that state attorneys general and the DOJ rejected on antitrust grounds—Apotex launched generic clopidogrel at risk in August 2006.

BMS and Sanofi obtained a preliminary injunction within weeks, halting further Apotex sales. The court did not, however, order a recall of product already distributed. Apotex had shipped several months of inventory to pharmacy channels in the three-week launch window. That product remained on shelves and continued to erode Plavix sales even after the injunction took effect—a perverse result of the channel-stuffing strategy.

The ultimate patent ruling went against Apotex. A damages judgment later fixed Apotex’s liability at $442 million plus interest. The takeaway for generic counsel: an injunction stops the launch but does not undo the liability clock, and pre-injunction channel inventory creates a damages tail that outlasts the sales.

How the Lipitor Launch Got Everything Right

The November 2011 launch of generic atorvastatin is the canonical success case. Lipitor (atorvastatin calcium) was the highest-grossing pharmaceutical product in history, with peak sales near $13 billion annually. Ranbaxy (now part of Sun Pharma) was the first ANDA filer and had secured a settlement with Pfizer fixing the launch date.

Pfizer simultaneously launched an authorized generic through Watson Pharmaceuticals (now Teva). The dual launch—Ranbaxy generic plus Watson AG—was timed to coincide with settlement-fixed patent expiration, eliminating at-risk liability. The two generics captured over 50% of the market within weeks. Because the transition was orderly and the launch date was known well in advance, PBMs and pharmacy chains had staged their contracting to shift volume immediately. The six-month exclusivity period produced hundreds of millions in revenue for both generic participants while reducing total atorvastatin market prices by approximately 80% within two years. The system functioned as designed.

Key Patent Expiry Dates and Revenue at Risk Through 2030

Which Drug Revenue Cliffs Are Largest for Generic First-Mover Opportunities

The patent expiry timeline from 2025 to 2030 contains several assets where 180-day exclusivity will represent nine-figure prizes for the first successful ANDA filer. The list below reflects confirmed or expected loss of exclusivity dates based on current Orange Book listings and publicly reported settlement terms. Patent expiry timelines shift with litigation outcomes and settlement negotiations; these figures should be verified against current Orange Book data.

Keytruda (pembrolizumab) – Merck: The core composition-of-matter patent expires in 2028. With 2024 revenues exceeding $25 billion, any loss of exclusivity scenario represents the single largest revenue cliff in pharmaceutical history. Pembrolizumab is a large-molecule biologic, so the relevant pathway is the BPCIA biosimilar route, not Hatch-Waxman—but the first biosimilar applicant approved by the FDA will face the same first-mover dynamics that govern small-molecule generics, mediated by formulary access rather than automatic substitution.

Eliquis (apixaban) – Bristol-Myers Squibb/Pfizer: Settlement agreements with generic manufacturers including Teva, Mylan, and Sandoz fixed the loss of exclusivity date at April 2028. Eliquis generated approximately $12 billion in 2024 US revenues. The settlement terms constrain which companies can launch and when, creating a structured entry rather than a pure Paragraph IV race—but the economics of the first entrant period still favor early participants significantly.

Ozempic/Wegovy (semaglutide) – Novo Nordisk: Core composition patents for semaglutide expire in the 2031–2033 window, though this is actively contested. Several Paragraph IV challenges have been filed. The manufacturing complexity of GLP-1 receptor agonists (discussed in detail below) means that even after patent expiration, the number of qualified ANDA filers may be limited, extending the first-mover advantage beyond the standard 180-day window. The combined Ozempic/Wegovy franchise exceeds $20 billion in annual revenue, making this the most contested generic target of the coming decade.

Dupixent (dupilumab) – Sanofi/Regeneron: The patent estate extends into the 2030s, but lifecycle litigation is likely to begin several years before the core composition-of-matter expiry. Dupilumab generated approximately $14 billion in 2024. As a biologic, it travels the BPCIA pathway.

Skyrizi (risankizumab) and Rinvoq (upadacitinib) – AbbVie: These two assets were developed explicitly to replace Humira revenue following biosimilar entry in 2023. Rinvoq (a JAK inhibitor, small molecule) and Skyrizi (an IL-23 inhibitor, biologic) are now AbbVie’s primary growth drivers. Their patent timelines run to the mid-2030s. Given AbbVie’s history of aggressive patent portfolio construction—the Humira patent thicket encompassed over 130 patents—IP teams and generic companies should expect similar lifecycle management strategies here.

Revenue at Risk by Therapeutic Class

Where Generic Entry Will Concentrate Between 2025 and 2030

Oncology small molecules: Lenalidomide (Revlimid) is already in its generic transition, with volume-limited entry by settlement. The next wave includes ibrutinib (Imbruvica, AbbVie/J&J, LOE 2027-2028), which had 2023 revenues near $3.8 billion, and palbociclib (Ibrance, Pfizer, with settlements allowing generic entry beginning 2027). Oral oncology agents tend to have complex dosing schedules and patient adherence programs that slow generic uptake versus simple generics, but the first filer still captures the high-value early period.

GLP-1 receptor agonists: Semaglutide, tirzepatide (Mounjaro/Zepbound, Eli Lilly), and liraglutide (Victoza/Saxenda, Novo Nordisk) represent the most consequential generic targets in the next decade. Tirzepatide’s patents provide protection into the mid-2030s. Liraglutide’s loss of exclusivity is already underway in some dosages, with limited ANDA activity due to manufacturing barriers.

Immunology biologics: Dupilumab, risankizumab, guselkumab (Tremfya, J&J), and ixekizumab (Taltz, Eli Lilly) will face biosimilar competition on a staggered timeline through 2030 and beyond. These are all large-molecule products where the BPCIA pathway governs, and where formulary access strategy matters more than speed alone.

What Investors Are Watching: How Patent Data Moves Generic Stock Valuations

How a Paragraph IV Filing Changes the Financial Profile of Teva, Viatris, and Amneal

For publicly traded generic companies, the Paragraph IV pipeline is a direct proxy for future earnings quality. Analysts covering Teva, Viatris, Amneal, and Hikma maintain explicit models for “first-to-file” positions that contribute non-commodity margin. When a company announces a first ANDA filing against a blockbuster, the equity market typically reacts positively—before the litigation outcome is known—because the filing itself is a call option on 180-day exclusivity.

Teva’s recent performance illustrates the dynamic. The company’s North American generic revenues showed improved quality when volume-limited lenalidomide (generic Revlimid) revenue flowed through in 2022 and 2023. Per-unit margins on lenalidomide were dramatically higher than on base generic products because the settlement structure kept the number of participants small, functioning as a quasi-exclusivity period even beyond the statutory 180 days. Teva management explicitly cited lenalidomide as a revenue stabilizer on quarterly calls, and the stock responded.

Dr. Reddy’s Laboratories crossed $1 billion in North American generic revenue—a milestone the company attributed publicly to lenalidomide and other “new product launches,” the standard term for high-value first-filer positions. The company also received a $72 million settlement payout from Indivior in the Suboxone (buprenorphine/naloxone) litigation, monetizing years of IP challenge work into a direct cash transfer.

Amneal’s Q3 2025 results showed 12% revenue growth driven by complex generics—products where Amneal entered as one of two or three competitors rather than one of ten. The company’s strategy of targeting complex injectables and biosimilars specifically avoids the commodity erosion curve that flattens margins in the oral solid market.

What Hedge Funds and Institutional Investors Look for in First-Filer Catalysts

The standard institutional analysis of a generic company’s Paragraph IV pipeline focuses on three variables: the probability of litigation success, the timing of launch (settlement date vs. trial date vs. at-risk decision), and the authorized generic probability. A sophisticated model discounts each first-filer position by all three factors and sums the risk-adjusted exclusivity revenue across the portfolio.

For large positions in companies like Teva or Viatris, tracking law firm activity—which patent litigators are being retained, which district courts are hearing cases, how similar patent families have been treated in prior rulings—yields leading indicators before earnings. District courts in New Jersey, Delaware, and the Northern District of Illinois handle the bulk of Hatch-Waxman litigation. Win rates by judge, by patent type (composition vs. formulation vs. method-of-use), and by defendant provide a base rate for litigation outcomes that is more precise than headline settlement announcements.

Most Important Ongoing Litigation: What Patent Challenges Are Live Right Now

GLP-1 Patent Wars: Semaglutide Challenges and the Novo Nordisk Defense Strategy

The patent estate covering semaglutide is contested on multiple fronts. Novo Nordisk holds composition-of-matter patents, formulation patents covering the specific buffer systems and excipients used in Ozempic and Wegovy, and device patents covering the FlexPen and autoinjector delivery systems. Several ANDA filers have submitted Paragraph IV challenges targeting different pieces of the estate.

Novo Nordisk’s litigation strategy mirrors the playbook AbbVie used for Humira: file every conceivable patent, assert all of them simultaneously, and use the 30-month stay to extend de facto protection beyond the core composition expiry. The manufacturing barriers around semaglutide add a second defensive layer. Unlike a simple tablet, injectable semaglutide requires peptide synthesis capacity, specific sterile fill-finish manufacturing, and stability data supporting the commercial formulation. The number of manufacturers globally capable of matching Novo Nordisk’s manufacturing specifications is small, which limits the ANDA applicant pool regardless of patent outcome.

Imbruvica Patent Disputes and the AbbVie/J&J Defense Wall

Ibrutinib (Imbruvica), co-marketed by AbbVie and Janssen (Johnson & Johnson), has faced multiple Paragraph IV challenges targeting the compound patent, method-of-use patents, and formulation patents. Settlements have been reached with several ANDA filers fixing launch dates in 2027. The commercial stakes are substantial: Imbruvica generated approximately $3.8 billion in US revenues in 2023, and while that figure is declining with competition from next-generation BTK inhibitors (acalabrutinib, zanubrutinib), it remains a significant generic target.

The more interesting litigation dimension involves the AbbVie-Pharmacyclics IP licensing structure. AbbVie acquired Pharmacyclics in 2015 for $21 billion specifically to control the Imbruvica patent estate. Royalty obligations run in multiple directions depending on the settlement structure. Generic ANDA filers negotiating with AbbVie must account for the royalty-adjusted cost of entry, not just the headline litigation outcome.

Keytruda and the Upcoming Biosimilar Landscape for Pembrolizumab

Merck’s pembrolizumab patent estate has multiple layers. The antibody sequence patents, the manufacturing process patents, and the formulation patents for Keytruda expire on different schedules. Samsung Bioepis, Amgen, and several other companies have initiated biosimilar development programs. The first biosimilar applicant to receive FDA approval—expected to be achievable by 2028—will face the same formulary access barriers that slowed Humira biosimilar adoption.

Pembrolizumab is approved across 40-plus indications. The oncology prescriber community is less price-sensitive than general practitioners prescribing statins or antihypertensives, and payer formulary management in oncology relies more heavily on clinical differentiation arguments. This means the first biosimilar entrant may face slower initial uptake than a standard small-molecule generic, even without automatic substitution barriers.

Merck’s primary biosimilar defense will be formulary contracting—offering deeper rebates on Keytruda to retain preferred status. This strategy is more sustainable for Merck than it was for AbbVie with Humira because pembrolizumab faces no single-indication biosimilar competition (multiple indications spread the risk) and because Merck has pipeline assets (pembrolizumab combinations, coformulations) that can be bundled into payer contracts.

How Patent Thickets Delay Biosimilar Entry—and Why the Strategy Is Under Scrutiny

What a Patent Thicket Actually Looks Like in Practice: The Humira Example

A patent thicket is not a single strong patent but a deliberate accumulation of overlapping patents covering different aspects of a product, designed collectively to make the cost and complexity of challenge prohibitive. AbbVie’s patent estate for Humira (adalimumab) is the defining example: over 130 patents were asserted across six distinct patent families covering the antibody sequence, manufacturing cell lines, formulation, dosing regimens, dosing devices, and method-of-use claims for specific indications.

Challengers did not need to invalidate all 130 patents—they needed to ensure that any one surviving patent did not block their product. The sheer volume of patents, and the litigation cost associated with mounting credible challenges to each, functioned as a financial deterrent. Amgen, Samsung Bioepis, Sandoz, and others ultimately settled with AbbVie on terms that delayed US biosimilar entry until January 2023—years after the core composition patent expired in 2016. By the time the first biosimilar launched, AbbVie had generated an additional $100 billion-plus in Humira revenues protected not by the composition patent but by the thicket.

Despite launching first, Amgen’s Amjevita captured minimal market share in its initial period. Humira retained 96% market share a full year after biosimilar entry. The thicket strategy, combined with aggressive PBM rebate contracting, produced an outcome where “first mover” in the biosimilar context meant first to market but not first to revenue—a fundamental difference from the small-molecule paradigm.

Why the FTC Is Attacking Orange Book Listings for Device and Packaging Patents

The FTC initiated a program in late 2023 targeting improper Orange Book listings—patents that do not describe the drug product itself but instead cover ancillary features like inhaler devices, container closures, or distribution systems. These listings trigger 30-month stays just as compound patents do, delaying generic entry even when the active ingredient patents have expired or been invalidated.

By 2024, the FTC had challenged over 300 individual Orange Book listings. In inhaler litigation involving Teva and Amneal against AstraZeneca (budesonide/formoterol, generic Symbicort) and GSK, courts ordered the delisting of device patents that did not describe the drug formulation. The practical effect accelerates generic timelines: removing a device patent from the Orange Book eliminates the 30-month stay triggered by that patent, allowing the generic to seek approval on the formulation patent timeline alone.

For generic IP teams, this FTC campaign is a net positive in the short term but compresses the window between first and later filers. If improper listings are removed, multiple ANDAs that were otherwise blocked by staggered 30-month stays may clear simultaneously, putting more competitors into the market faster after launch.

Why GLP-1 Manufacturing Complexity Is the Real Barrier for Generic Entrants

What Makes Semaglutide and Tirzepatide Hard to Copy—Even After Patent Expiration

Semaglutide is a 31-amino-acid GLP-1 receptor agonist with a fatty acid side chain attached via a chemical linker to the lysine residue at position 26. That side chain is responsible for the extended half-life (approximately 7 days for injectable formulations) that enables once-weekly dosing. Synthesizing the peptide backbone, attaching the fatty acid chain with the correct stereochemistry, and purifying the product to pharmaceutical grade requires a multi-step solid-phase peptide synthesis process followed by conjugation chemistry that is not standard across generic API manufacturers.

The commercial-scale manufacturing of semaglutide API involves proprietary synthesis routes, specialized purification equipment, and yield optimization that Novo Nordisk has refined over years of production. The FDA’s bioequivalence requirements for injectable peptides are more complex than for oral tablets—generic developers must demonstrate not just pharmacokinetic equivalence but also consistent excipient profiles and sterile fill-finish quality. Even companies with peptide synthesis capacity (Teva API, Bachem, PolyPeptide) face years of process development before they can produce at commercial scale.

Tirzepatide (Eli Lilly’s Mounjaro/Zepbound) introduces additional complexity: it is a dual GIP/GLP-1 receptor agonist with an even larger molecular structure, a different fatty acid conjugation, and proprietary formulation chemistry. The manufacturing barriers are higher still.

This manufacturing moat means the effective patent cliff for GLP-1 agents will arrive later than the legal patent expiration. When semaglutide patents expire in the early 2030s, the number of manufacturers capable of qualifying product for ANDA submission may be three to five globally. The first mover in that constrained field will hold a durable position—similar to the long-acting injectable antipsychotic generics—rather than the rapidly commoditized oral solid market.

Why Long-Acting Injectable Generics Hold Margins for Years After Exclusivity Ends

Long-acting injectable (LAI) antipsychotics—paliperidone palmitate (Invega Sustenna, Invega Trinza), aripiprazole lauroxil (Aristada), and olanzapine pamoate (Zyprexa Relprevv)—are the textbook example of manufacturing-moat-driven first-mover advantage.

The bioequivalence pathway for these products requires clinical pharmacokinetic studies because standard in vitro dissolution testing cannot predict in vivo release from an intramuscular depot formulation. Each such study can cost $5 million to $20 million. The formulation itself—microspheres, nanocrystals, or salt-based suspensions—requires specialized particle engineering. Sterile manufacturing of a suspended solid-in-liquid injection requires Class A fill-finish environments with specific handling protocols.

The result: even after the core patents expire, a generic LAI antipsychotic may face only one or two ANDA competitors for the first three to five years of its market life. The first filer does not enjoy 180 days of statutory exclusivity—it enjoys years of structural exclusivity created by manufacturing scarcity. Pricing in this environment reflects the competitive dynamics: generic LAI antipsychotics frequently hold 40% to 60% of brand price rather than the sub-5% seen in commodity oral solid markets.

How Biosimilar Launch Timing Works Under the BPCIA

The Biosimilar Patent Dance: Why the BPCIA Is More Complex Than Hatch-Waxman

The Biologics Price Competition and Innovation Act (BPCIA), passed as part of the Affordable Care Act in 2010, created the 351(k) regulatory pathway for biosimilars. The patent dispute mechanism under the BPCIA—informally called the “patent dance”—differs fundamentally from Hatch-Waxman’s Paragraph IV process.

Under the patent dance, the biosimilar applicant shares its 351(k) application (including manufacturing details) with the reference product sponsor, triggering a structured exchange of patent lists, counterlists, and then litigation over a subset of patents identified for immediate resolution. A second wave of patent litigation on remaining patents proceeds separately. The 12-year exclusivity period for the reference biologic (versus 5 years for small molecules) delays biosimilar entry significantly, independent of any patent dispute.

The FDA can designate a biosimilar as “interchangeable” if the applicant demonstrates that the product produces the same clinical result as the reference in all indicated conditions and that, for products administered multiple times, switching between the reference and the biosimilar does not present greater safety or effectiveness risks than continued use of the reference. This higher standard requires additional clinical data, typically one or more switching studies.

Semglee, Interchangeability, and What Formulary Access Actually Drives Market Share

Semglee (insulin glargine-yfgn), developed by Viatris and Biocon, received FDA interchangeability designation in July 2021, making it the first interchangeable biosimilar to Sanofi’s Lantus. The designation triggered immediate commercial interest from PBMs, particularly Express Scripts, which placed Semglee on its National Preferred Formulary while removing Lantus.

Research published in Health Affairs in 2025 found that the interchangeability designation’s primary mechanism was enabling formulary preferencing rather than enabling spontaneous pharmacy-level substitution. In states where automatic substitution was permitted and where pharmacists had the legal authority to substitute interchangeable biosimilars, the uptake at the pharmacy counter remained modest. The real driver was payer formulary access: once Express Scripts preferenced Semglee, Lantus faced a rebate war it was unwilling to fully fund.

In employer-sponsored insurance markets, Semglee’s market share rose by over 19 percentage points in early 2022 following the formulary change. The lesson for biosimilar first-mover strategy: securing interchangeability is less valuable as a substitution mechanism and more valuable as a credentialing tool that gives PBMs cover to make formulary switches without physician or patient objection.

What Happens Financially After Loss of Exclusivity: The Brand Perspective

How AbbVie’s Humira Revenue Held Despite 10+ Biosimilars—and What That Means for Future LOE Analysis

Humira (adalimumab) generated $8.9 billion in US revenues in 2023, the year Amjevita and several other adalimumab biosimilars launched. In 2024, US Humira revenues fell to approximately $3.2 billion, reflecting accelerating biosimilar adoption in the second year. But the first-year figure—$8.9 billion against a product losing exclusivity—defied every small-molecule loss-of-exclusivity template.

The mechanism was rebate contracting. AbbVie offered PBMs and health plans rebates large enough to keep Humira on preferred formulary tiers even as biosimilars launched at list prices 80% below Humira’s. The biosimilars responded by adopting a dual-pricing strategy: a high list price with high rebates (to compete for formulary access) and a low list price with minimal rebates (for self-pay and price-sensitive channels). The dual-pricing market structure confused formulary managers and delayed large-scale switching.

By mid-2024, biosimilar market share in the adalimumab space had reached approximately 35% to 40%, concentrated in channels where PBMs had made decisive formulary switches. For investors modeling AbbVie, the takeaway is that a biologic blockbuster with deep PBM relationships can manage its loss-of-exclusivity revenue more favorably than small-molecule brands, but not indefinitely—the erosion accelerates in year two and year three as more payers move.

The Revlimid Volume Cap Structure: A New Template for Managing Generics

Bristol-Myers Squibb negotiated a unique loss-of-exclusivity framework for Revlimid (lenalidomide). Rather than a clean entry date, BMS reached settlements with multiple generic filers—including Teva, Dr. Reddy’s, Natco Pharma, and others—that allow generic entry beginning in 2022 but cap the volume each generic manufacturer can sell. The caps escalate annually, reaching full generic competition only in 2026.

This structure is novel in Hatch-Waxman history. It converts what would have been an immediate full loss of exclusivity into a phased revenue transition. For BMS, each year of partial exclusivity on a $10 billion-peak-revenue product is worth billions. For generic filers, the volume caps guarantee a share of a still-profitable market, without the risk of commodity pricing. For investors, it produced a cleaner, more predictable revenue glide path than the typical patent cliff.

The Revlimid structure is now being studied as a potential template for other blockbuster assets approaching loss of exclusivity. Whether it survives FTC scrutiny as a permissible settlement structure is an open question—the agency has reviewed it and has not taken formal action, but the antitrust analysis could shift if similar structures proliferate.

Competitor Strategies: Which Generic Companies Are Best Positioned for First-Mover Wins

Teva’s Complex Generic Pivot After the Revlimid Windfall

Teva Pharmaceutical Industries, the world’s largest generic company by volume, has spent the past several years deliberately shifting its ANDA portfolio toward complex generics and specialty molecules. Following the Revlimid windfall—which provided substantial revenue to offset the ongoing revenue decline of Copaxone (glatiramer acetate) to competitors—Teva’s North American generic leadership has emphasized building a pipeline of differentiated, high-barrier products.

Their biosimilar portfolio includes Simlandi (adalimumab), launched into the crowded Humira biosimilar market in 2023. Teva’s biosimilar strategy is deliberately selective: they target high-revenue biologics where they can differentiate on launch timing, interchangeability status, or manufacturing reliability rather than entering as the fifth or sixth biosimilar and competing purely on price.

For generic investors, the signal to watch in Teva earnings is the mix shift in North American generic margins. Commodity oral solids generate gross margins in the 30% to 45% range. Complex generics and biosimilars generate 55% to 75% gross margins. If Teva’s new launch cohort in a given quarter is weighted toward complex products, margin expansion follows regardless of volume trends.

Dr. Reddy’s Laboratories: The Litigation-Forward Strategy That Built a Billion-Dollar US Business

Dr. Reddy’s has built its North American generic business on a consistently aggressive Paragraph IV strategy. The company files challenges early, litigates extensively, and accepts settlement terms that preserve first-filer economics even at the cost of delayed launch dates. The Revlimid settlement—which gave Dr. Reddy’s volume-limited entry beginning in 2022—was the product of years of litigation work and produced quarterly revenues that pushed their North American business past the billion-dollar threshold.

The Suboxone (buprenorphine/naloxone film) litigation illustrates a different value pathway: using Paragraph IV challenges not to launch a product but to create legal leverage that resolves as a settlement payment. The $72 million payout from Indivior to Dr. Reddy’s in the Suboxone dispute is essentially IP arbitrage—the value of the challenge right was monetized without a single unit of generic Suboxone being sold.

This approach—filing to create option value, then negotiating the settlement economics—is underappreciated by investors who focus on launch dates and market share figures. For companies with strong IP litigation teams, the Paragraph IV challenge itself is an asset regardless of whether it results in a product launch.

Amneal and the Complex Injectable Thesis

Amneal Pharmaceuticals has built a distinct competitive position by focusing on complex generics—specifically long-acting injectables, inhalation products, and ophthalmics—where the ANDA field is limited by manufacturing barriers rather than just patent position. Their Q3 2025 results, which showed 12% revenue growth and expanded adjusted EBITDA, reflected the strategy’s commercial validation.

The company has filed ANDAs for products like generic Invega Sustenna (paliperidone palmitate LAI) and generic Abilify Maintena (aripiprazole LAI), both of which would represent first-filer economics in a highly constrained competitive field. If successful, these launches would generate multi-year margin contributions that dwarf what Amneal earns from its oral solid generic portfolio.

How FDA Actions Could Affect Generic Launch Timelines

Complete Response Letters, Manufacturing Deficiencies, and Their Impact on First-Filer Status

FDA approval of an ANDA is not automatic upon satisfying bioequivalence requirements. Manufacturing facility inspections (Pre-Approval Inspections, or PAIs) must confirm that the production site meets current Good Manufacturing Practice (cGMP) standards. A PAI failure or the issuance of a Warning Letter to the applicant’s manufacturing site can delay final ANDA approval indefinitely.

For first-filer applicants, a manufacturing delay is particularly damaging because FDA may grant “tentative approval” to subsequent ANDAs—approval that would become final if the first filer’s position is forfeited or if the exclusivity period is triggered and begins to run. A tentatively approved second ANDA filer is positioned to launch the moment the first filer’s 180-day clock expires or is forfeited.

Ranbaxy’s manufacturing problems in the late 2000s and early 2010s illustrate this risk. The company held first-filer positions on numerous high-value ANDAs, including atorvastatin (Lipitor), but its Paonta Sahib and Dewas facilities received FDA Import Alerts that blocked product from entering the US market. Competitors filed motions to have Ranbaxy’s first-filer status forfeited. The FDA’s treatment of these situations—ultimately issuing a consent decree—is a cautionary example of how manufacturing compliance failures can strip years of litigation investment from the books.

How FDA’s Complex Drug Substances Initiative Affects the Bioequivalence Timeline

The FDA’s Product-Specific Guidance (PSG) program provides public guidance on the bioequivalence methodology for specific drugs. For complex products—nasal sprays, inhalation solutions, topical products—these guidances are essential because standard PK studies may be insufficient or unavailable.

When the FDA updates or issues a new PSG, it can significantly shift the competitive timeline. A guidance that requires in vivo clinical endpoint studies (e.g., for complex topicals like acyclovir cream) takes years to conduct, delaying all ANDA submissions and compressing the gap between first and subsequent filers who submit under the same methodology. Conversely, a guidance that permits in vitro equivalence criteria (e.g., for some nasal spray products) opens the ANDA pathway broadly, increasing the number of potential first-filer competitors and potentially intensifying the race to file.

The FDA’s draft guidance on bioequivalence for GLP-1 injectable products—if and when issued—will define the competitive parameters for generic semaglutide and tirzepatide development. The methodology the agency selects will determine whether clinical PK studies, switching studies, or device performance testing is required, materially affecting the cost and timeline of ANDA development for all applicants.

Common Investor Questions About Generic First-Mover Advantage

Does 180-day exclusivity guarantee a six-month monopoly?

No. The FDA is prohibited from approving other ANDAs during the 180-day period, but brand companies can launch authorized generics under their original NDA approval. If an AG launches simultaneously with the first filer, the market is a duopoly from day one. FTC data shows this cuts first-filer revenue by 40% to 52%.

What triggers the 180-day exclusivity clock to start?

The clock begins on the date of the first commercial marketing of the drug by the first ANDA filer, or the date of a final court decision holding the patent invalid or not infringed—whichever occurs first. If the first filer delays launch (common in settlement scenarios), the clock does not run, which can block all subsequent ANDAs indefinitely. This “parking” of exclusivity is why the FTC scrutinizes pay-for-delay settlements.

Can two ANDA filers share first-filer status?

Yes. If two ANDAs with Paragraph IV certifications are submitted on the same day, both qualify as first filers and share the 180-day exclusivity period. Both may launch simultaneously, creating a three-player market from day one of generic entry rather than the pure duopoly a single first filer would hold.

How does the 505(b)(2) pathway interact with first-mover dynamics?

A 505(b)(2) NDA is not an ANDA. It creates a new brand product (with its own 3-year or 5-year exclusivity) that competes directly with the reference listed drug. If a company successfully develops a 505(b)(2) version of an off-patent drug—say, a reformulated extended-release version—it enters the market as a new brand rather than a generic and avoids the commodity pricing erosion entirely. This is a different competitive strategy but can achieve similar economic goals for lifecycle management.

Why does the first biosimilar often not dominate the way the first generic does?

Three reasons. First, automatic pharmacy substitution requires interchangeability designation, which few biosimilars hold. Second, the primary payers in biologic markets (large health plans and specialty PBMs) make formulary decisions annually, meaning even a first-approved biosimilar may not achieve formulary preference immediately. Third, brand companies in biologic markets have deeper rebate capacity and longer PBM contract tenures than brands in the oral solid market, allowing them to defend formulary position even after biosimilar entry.

What determines whether a Paragraph IV challenge succeeds?

Patent validity cases (obviousness, anticipation, written description) are tried in federal district court, with appellate review by the Court of Appeals for the Federal Circuit. The most common invalidity grounds are obviousness under 35 USC 103 and lack of written description under 35 USC 112. Win rates for generic challengers vary by technology type: formulation patents and method-of-use patents are invalidated at higher rates than composition-of-matter patents. Secondary patents added during product lifecycle management (covering specific crystal forms, specific pH ranges, specific excipient combinations) are generally more vulnerable to obviousness challenges.

Investment Strategy: How to Use Patent Data for Portfolio Positioning in Generic Pharma Stocks

What Institutional Analysts Track in the DrugPatentWatch Data Layer

The commercially actionable edge in generic pharma investing is not in knowing when a patent expires—that information is public. The edge is in knowing: which ANDA applicants have filed Paragraph IV certifications, which district courts are handling the litigation, which patent claims are being challenged, and how similar claims have been treated in prior decisions.

Platforms that aggregate Orange Book patent listings, ANDA filing data, litigation status, and settlement terms—like DrugPatentWatch—enable this analysis at a level of granularity that general financial databases do not provide. An investor who knows that four ANDAs have been filed against a specific product, that the district court handling the case has a 70% generic win rate on the relevant patent type, and that the brand company has a history of no-AG agreements has meaningfully better inputs for a price target model than one working from patent expiry dates alone.

The multi-year positioning trade in generic pharma is straightforward in structure: identify companies with large first-filer positions in high-revenue drugs, estimate the revenue contribution under realistic litigation scenarios, compare to market valuation, and adjust for manufacturing risk. The execution requires precise patent data, litigation tracking, and manufacturing quality assessment—inputs that are data-intensive but available.

How Pipeline Replacement Risk Changes the Brand Equation

For brand company investors, the mirror image of the generic first-mover analysis is the pipeline replacement question. When a product like Eliquis (LOE 2028) or Keytruda (core patent 2028) faces loss of exclusivity, the question is not just how fast revenue erodes but whether the company has assets in late-stage development that can absorb the gap.

AbbVie’s Skyrizi and Rinvoq strategy is the most publicized pipeline replacement story in recent history. Those two assets were specifically developed and acquired to replace Humira’s $20-billion-plus revenue peak. By 2024, Skyrizi and Rinvoq combined revenues were approaching $15 billion, partially offsetting the Humira erosion. The investor question for AbbVie today is not whether the company survives Humira’s loss of exclusivity—it clearly does—but whether Skyrizi and Rinvoq face their own LOE cliffs before sufficient replacement assets mature.

Merck faces the same dynamic with Keytruda. The company has invested heavily in combination programs (Keytruda plus Welireg, Keytruda plus co-stimulatory antibodies) and in a subcutaneous formulation of pembrolizumab (approved in 2024) designed to extend the product’s market life beyond IV administration. The subcutaneous formulation carries its own IP life and may be harder for biosimilar developers to match on interchangeability grounds because switching studies between IV and subcutaneous formulations add complexity.

Key Takeaways

The 180-day exclusivity period remains the single most valuable asset class in generic drug development—not because the law gives first filers a monopoly, but because it gives them a duopoly priced at 60% to 80% of brand price rather than the 5% to 10% of brand price that arrives when ten competitors enter simultaneously. That pricing gap, maintained for six months on a multibillion-dollar molecule, funds pipelines, offsets litigation losses, and compounds into the kind of sticky market share lead that persists for a decade.

The Protonix verdict ($2.15 billion), the Plavix injunction, and the Apotex damages award collectively define the downside of at-risk launches. The Lipitor transition defines the upside of a clean, settlement-timed first-filer execution. The Humira biosimilar experience shows that in biologics, being first is necessary but not sufficient—formulary access and payer contracting determine who actually captures the market.

Manufacturing complexity is the next frontier of durable first-mover advantage. Companies that can navigate the bioequivalence requirements for GLP-1 injectables, long-acting antipsychotics, and complex inhalation products will hold positions the commodity generic market cannot replicate. The patent expires; the manufacturing moat does not.

For investors, the data layer matters as much as the headline. The difference between a first-filer position worth $200 million and one worth $20 million often lies in details visible only in the ANDA filing database and the district court docket—not in the Orange Book patent expiry date alone.

Data in this analysis draws on publicly available FDA ANDA filings, Orange Book patent listings, federal court dockets, SEC filings from Teva, Dr. Reddy’s, Amneal, AbbVie, Merck, and BMS, FTC enforcement actions, and peer-reviewed academic literature on generic market dynamics. Patent expiry dates and litigation status should be independently verified against current regulatory filings before making investment decisions.

(2) Pathway")

(2) Beats the Branded Generic Every Time — Unless It Doesn't")