The patent cliff is not a metaphor. It is a measurable revenue event. When a branded drug loses market exclusivity, generic competitors typically capture 80 to 90 percent of unit volume within 12 months, collapsing net realized price along with it. Lyrica (pregabalin) is the standard illustration: its $4 billion-per-year branded franchise hit a monthly average price near $0.13 per unit within two months of generic entry. Xeljanz (tofacitinib) is the current-cycle example, with the first generic tofacitinib approved by the FDA in August 2025 and full generic penetration expected by 2026.

The macro backdrop makes this more urgent than prior cycles. Between 2025 and 2030, the U.S. market alone faces an estimated $230 to $300 billion in annual sales at risk from loss of exclusivity, across roughly 200 drugs including approximately 70 assets each generating over $1 billion annually. The 2016 patent cliff eroded around $100 billion in brand sales. The current wave is three times that scale. By 2026, analysts estimate that eight of the thirteen largest pharmaceutical firms, representing 55 percent of global market capitalization, could see 30 percent or more of their revenue jeopardized, with individual exposure ranging from $6 billion to $38 billion per company.

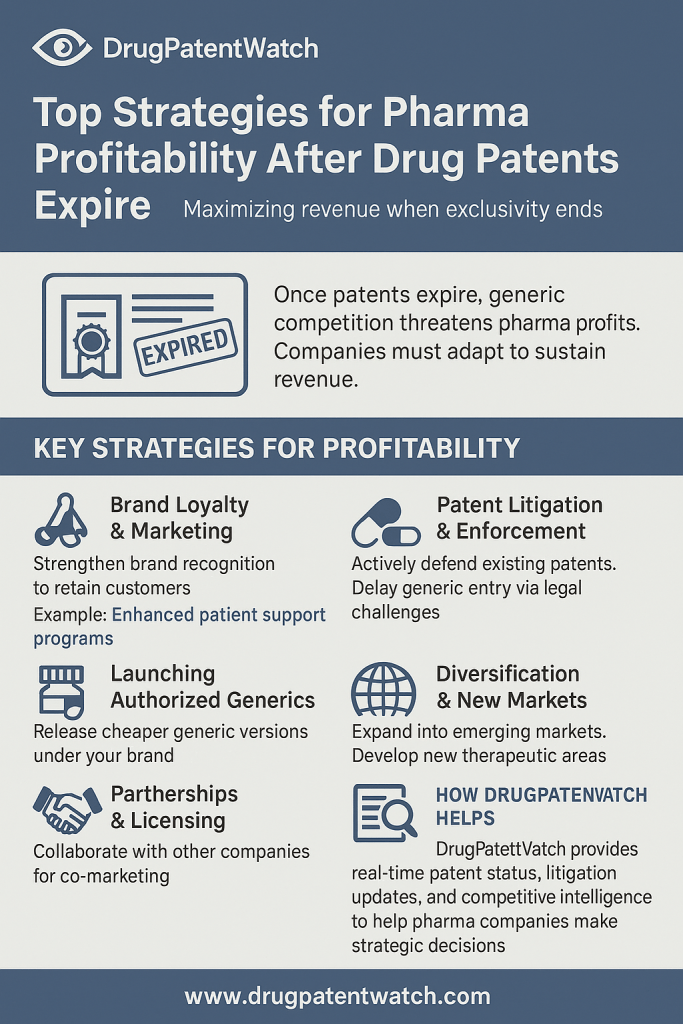

This guide covers every major strategy pharmaceutical companies use to protect and extend revenue through patent expiry: IP portfolio architecture and evergreening, product reformulation roadmaps, authorized generics, indication expansion, biologic-specific tactics, the IRA’s newly activated pricing pressure, competitive M&A, and geographic diversification. Each section includes IP valuation context, relevant case studies with current data, and decision frameworks for analysts modeling loss-of-exclusivity events.

1. Understanding the Patent Clock: Effective Exclusivity vs. Nominal Term

How 20-Year Patents Translate to Shorter Market Windows

A pharmaceutical patent filed under the Patent Cooperation Treaty carries a 20-year nominal term from the filing date. For most drugs, the relevant filing occurs years before FDA approval, which compresses actual market exclusivity to 7 to 12 years on average. A compound entering Phase I clinical trials in year one of its patent term faces, statistically, 10 to 13 years of trials and regulatory review before launch. The result is a market window far shorter than the patent’s face value.

Congress addressed part of this compression with the Hatch-Waxman Act of 1984, which created Patent Term Restoration (PTR) under 35 U.S.C. § 156 to compensate originators for regulatory delay. PTR can restore up to five years of lost exclusivity, capped at 14 years of post-approval protection and 20 years of total patent term. In practice, a typical small-molecule drug with PTR achieves roughly 11.5 years of exclusivity post-approval before its first generic entry.

Separate from the patent term, regulatory data exclusivity provides independent protection. New Chemical Entity (NCE) status under Hatch-Waxman grants five years of FDA data exclusivity during which no Abbreviated New Drug Application (ANDA) can be filed, regardless of patent status. Pediatric exclusivity, granted under the Best Pharmaceuticals for Children Act when a sponsor conducts required pediatric studies, adds six months to any existing exclusivity period, including PTR. New Clinical Investigation (NCI) exclusivity grants three years for newly approved indications supported by new clinical data.

For biologics under the Biologics Price Competition and Innovation Act (BPCIA), the structure is different: 12 years of reference product exclusivity from approval, with a four-year ‘patent dance’ submission window. Biosimilar interchangeability designation, which allows pharmacist-level substitution without prescriber intervention, creates additional market dynamics not present for small molecules.

The Orange Book and Purple Book: Where LOE Intelligence Lives

The FDA’s Approved Drug Products with Therapeutic Equivalence Evaluations, universally called the Orange Book, is the definitive public source for small-molecule patent expiry and exclusivity data. It lists all patents claiming the drug substance, drug product, or method of use for each NDA, along with expiry dates. Any generic filer submitting a Paragraph IV certification must notify the NDA holder, triggering the 30-month stay that gives brands time to litigate without immediate market entry by the generic.

The Purple Book covers licensed biological products and serves an analogous function for biosimilar interchangeability tracking. Unlike the Orange Book, the Purple Book does not list individual patents, making biosimilar competitive intelligence substantially more complex and expensive to develop.

IP teams and portfolio analysts who monitor both databases in real time, cross-referenced against patent prosecution histories at the USPTO, gain 12 to 24 months of actionable lead time before loss of exclusivity events become consensus market knowledge.

Key Takeaways: Section 1

Effective market exclusivity for a small-molecule drug averages 11 to 12 years post-approval, not 20 years. PTR, NCE exclusivity, and pediatric extensions each add distinct, independently trackable time windows. NCE exclusivity blocks ANDA filing for five years; Paragraph IV certification triggers a 30-month litigation stay, extending practical protection further. Biologic exclusivity runs 12 years by statute, but the patent dance and interchangeability hurdles create layered defense opportunities that go well beyond the statutory minimum.

2. Quantifying the 2025-2030 Patent Cliff: Company-by-Company Exposure

The Scale of the Current Cliff

Approximately $300 billion in prescription drug revenue faces patent expiry or loss of exclusivity between 2025 and 2030. Roughly 200 individual drugs fall within this window. The concentration of exposure within a small number of large-cap companies makes this primarily a problem for Big Pharma balance sheets rather than an industry-wide shock distributed evenly across hundreds of sponsors. Six companies account for a disproportionate share of at-risk revenue.

Bristol-Myers Squibb faces the largest growth gap of any large-cap pharma peer, estimated at approximately $38 billion. Eliquis (apixaban), co-marketed with Pfizer, is already subject to Medicare price negotiation with a Maximum Fair Price of $231 per month starting January 2026, down from its $521 list price, representing a 56 percent discount. U.S. patent protection for Eliquis is set to expire in 2028. Opdivo (nivolumab) faces a parallel timeline. Together, these two assets account for roughly half of BMS’s total earnings, creating a concentrated LOE exposure with no single-asset replacement in sight.

Merck & Co. has the industry’s most scrutinized LOE problem in Keytruda (pembrolizumab), which generated more than $29 billion in global sales in 2024, making it the world’s highest-grossing drug. Core patent expiry arrives in 2028. Merck is also preparing for Januvia and Janumet losing exclusivity in 2026, Lynparza (olaparib) in 2027, and Gardasil/Gardasil 9 in 2028. The total at-risk revenue from Merck’s patent cliff exceeds $15 billion in annual sales.

Pfizer’s exposure includes Xeljanz, which already saw its first generic competitor approved in August 2025. The company also co-owns Eliquis with BMS and faces Vyndaqel (tafamidis) and Ibrance (palbociclib) loss of exclusivity within the 2025 to 2028 window.

Johnson & Johnson had Xarelto (rivaroxaban) subject to the IRA’s first negotiation round, with a Medicare Maximum Fair Price set at $197, down from $517. Stelara (ustekinumab) biosimilar competition began in 2023. Both headwinds are concurrent with Darzalex franchise growth, which partially offsets the losses.

Investment Strategy: Mapping LOE Risk to Equity Valuation

For institutional investors, LOE events are not binary. The market typically begins discounting a significant patent expiration 18 to 24 months before the actual date, and the discount is rarely linear. Companies with well-articulated, credible lifecycle extension strategies receive less aggressive discounting than those without. The relevant modeling framework is not ‘will revenue decline’ but rather ‘at what rate, over what time frame, and to what floor.’

Four variables drive the LOE revenue curve: the number of generic entrants and their market entry timeline, the presence or absence of an authorized generic that competes directly at launch, the therapy area’s patient switching behavior (oncology patients switch faster than chronic disease patients), and whether the innovator pursues litigation delay through Paragraph IV challenges.

Companies with high biologic exposure face slower revenue erosion than small-molecule heavy portfolios. Biosimilar penetration in the U.S. averages 30 to 50 percent of unit volume within 24 months of biosimilar approval, compared to 80 to 90 percent for small molecules within 12 months. The gap exists because of biosimilar interchangeability designation requirements, prescriber inertia, and payer contracting complexity.

3. The IP Portfolio as a Financial Asset: Valuation Frameworks

How Patent Portfolios Get Priced in M&A and Licensing Deals

Pharmaceutical intellectual property is the primary driver of company valuation at every stage from preclinical startup to commercial-stage Big Pharma. For a product in late-phase development or early commercialization, the patent estate determines the risk-adjusted net present value (rNPV) of the asset, which then anchors deal pricing in licensing and acquisition transactions.

Standard rNPV modeling for a drug asset under patent protection involves projecting peak sales, applying probability of clinical success and regulatory approval, discounting on a risk-adjusted basis, and defining the revenue tail based on expected exclusivity duration. A two-year extension of effective exclusivity, achieved through a successful Paragraph IV defense or a new formulation patent, can add hundreds of millions to low billions in asset NPV depending on the drug’s peak sales level. Merck’s Keytruda subcutaneous formulation strategy, discussed in detail in Section 5, illustrates how a single reformulation decision can shift a patent expiry from 2028 to potentially 2042, a 14-year NPV delta on the world’s highest-grossing drug.

Royalty rates in biopharmaceutical licensing transactions typically reflect the strength and breadth of the underlying IP. Transactions for drugs in competitive therapy areas with compound patent protection (covering the molecule itself) plus formulation and method-of-use patents command higher royalties than deals involving drugs where only secondary patents remain. A compound patent generates defensible exclusivity. A formulation patent alone generates exclusivity conditional on litigation outcome, which is structurally weaker.

The Patent Thicket as a Specific Asset Class

A patent thicket, the dense cluster of overlapping patents protecting a single drug product, is a distinct IP architecture strategy deployed most aggressively in the biologic segment. AbbVie’s Humira (adalimumab) portfolio became the canonical example: over 160 U.S. patents covering the compound, formulations, dosing regimens, manufacturing processes, and methods of use created an IP fortress that delayed meaningful U.S. biosimilar penetration until 2023, eight years after the European biologics agency approved the first adalimumab biosimilar.

The financial value of the Humira thicket, measured as the incremental revenue generated by biosimilar delay beyond the compound patent expiry, is estimated in the tens of billions of dollars. AbbVie collected $21.2 billion in Humira U.S. revenue in 2022 alone, the final year before biosimilar market entry. That figure represents the economic ceiling of what the thicket strategy protected.

Building a thicket requires IP teams to file continuously throughout a drug’s commercial life, covering every defensible patent class. The relevant categories are the active pharmaceutical ingredient (API) and its salts and crystalline forms, the formulation including excipients and delivery systems, the manufacturing process and quality control methods, specific dosage regimens and titration schedules, methods of treatment for each approved and contemplated indication, and patient selection biomarkers. Each category requires a separate filing strategy and prosecution timeline.

Key Takeaways: Section 3

rNPV models for drug assets must incorporate effective exclusivity duration as a key input, not nominal patent term. Effective exclusivity depends on litigation outcomes, authorized generic decisions, and the existence of secondary patent protection. Patent thicket architecture, particularly for biologics, can extend the economic life of an asset well beyond the compound patent expiry. The Humira portfolio demonstrates that a well-constructed thicket can be worth tens of billions in preserved revenue.

4. Evergreening Strategies: A Technical Roadmap

Evergreening is the practice of securing new patent protection on an existing drug through incremental modifications, replacing expiring primary patent coverage with layered secondary protection. The term carries a regulatory and policy critique that it is worth engaging honestly: not all evergreening creates equivalent clinical value, and the FTC, IQVIA, and a growing body of health policy research have documented cases where the primary purpose of secondary patents is revenue preservation rather than patient benefit. That tension is real. It is also compatible with understanding evergreening as a standard and legally available business strategy.

Polymorph and Salt Form Patents

The same active pharmaceutical ingredient can exist in multiple crystalline arrangements, called polymorphs, or as different salt forms, all of which may have distinct solubility, bioavailability, and stability profiles. A company that holds a composition-of-matter patent on the free-base form of a drug can file separate patents on a monohydrate, anhydrous, or specific polymorph that displays improved properties. AstraZeneca’s esomeprazole (Nexium), the S-enantiomer of omeprazole (Prilosec), is the most frequently cited example of a related tactic, chiral switching.

Chiral switching works when a racemic mixture, containing both R and S optical isomers, is the original drug substance. The patent on the racemate expires, but a new patent on the isolated active enantiomer can provide fresh exclusivity. Nexium’s market exclusivity lasted until 2014, approximately seven years after omeprazole’s generic entry. AstraZeneca generated roughly $4 to 5 billion per year in Nexium U.S. revenue during that window. Generic challengers argued successfully that the enantiomer patent was obvious in light of the racemate; AstraZeneca successfully defended it for years before settlement.

Metabolite Patents

The body converts a parent drug into one or more metabolites during elimination. Where a metabolite is pharmacologically active and distinct from the parent, it is patentable as a separate chemical entity. Fexofenadine (Allegra) is the active metabolite of terfenadine (Seldane), which was withdrawn from the market after safety issues. Hoechst (later Aventis, later Sanofi) launched fexofenadine with new patent protection, effectively extending the antihistamine franchise by more than a decade. The strategy works best when the metabolite has demonstrable clinical advantages and when the metabolite-to-parent conversion is not trivially obvious to a person skilled in the art.

Combination Product Patents

Combining an off-patent or near-patent active ingredient with a second agent in a fixed-dose combination (FDC) product creates a new patentable entity. The FDC can claim both the combination itself and specific dosing ratios, pharmaceutical formulations, and methods of use in populations defined by the second agent’s mechanism. Cardiovascular and diabetes therapy have been particularly active in this space. Merck’s Janumet combined sitagliptin (Januvia) with metformin in a single tablet, generating a separate patent estate with its own Orange Book listings and LOE timeline, even as standalone Januvia approached expiry.

The FDC approach works best when the combination offers a genuine patient adherence benefit, which payers and prescribers are more likely to accept, and when the two agents have complementary mechanisms that reduce off-target effects. FDC products that lack clinical differentiation face accelerated payer pushback on formulary positioning.

Dosage Regimen and Method-of-Use Patents

A new dosing schedule, even for an existing approved drug, can be patentable if non-obvious and clinically meaningful. Twice-weekly dosing of alendronate (Fosamax) was initially patented separately from the daily formulation. The once-weekly dose was patented separately again. Each new regimen carried its own Orange Book listing and LOE timeline, even as the primary compound patent was expiring. Prescribers who had titrated patients to a stable regimen had clinical reasons to continue using the branded product even after generic daily dosing became available.

Method-of-use patents covering specific patient populations, biomarker-selected subgroups, or combination use protocols are increasingly important in oncology and immunology, where companion diagnostics and patient selection algorithms are deeply embedded in prescribing behavior. A biosimilar cannot replicate the method-of-use patent on a companion diagnostic algorithm without separate clinical development, a meaningful barrier.

The Paragraph IV Certification as a Strategic Tool

When a generic filer certifies under Paragraph IV that an Orange Book patent is invalid or not infringed, the brand must decide whether to initiate litigation within 45 days to trigger the 30-month regulatory stay. The decision is not binary. Companies that litigate selectively, choosing only the patent challenges where they have the strongest invalidity defense, preserve both time and litigation resources. Companies that litigate every Paragraph IV challenge, regardless of merit, signal desperation and often lose on secondary patents, accelerating the competitive damage they were trying to delay.

A robust Paragraph IV defense starts with freedom-to-operate analysis during patent prosecution, identifying the weakest claims before a generic filer does. IP teams that invest in this analysis can narrow or abandon vulnerable claims before the Orange Book deadline, removing targets for Paragraph IV challenge without forcing litigation.

Key Takeaways: Section 4

Evergreening through polymorphs, salts, enantiomers, metabolites, and FDCs requires filing during, not after, the primary patent’s commercial period. The earlier secondary patents are filed, the longer their terms. Paragraph IV litigation is selective work, not a blanket reflex. Method-of-use patents in oncology and immunology create durable prescriber inertia that even biosimilar-status products cannot easily displace.

5. Reformulation and Delivery System Innovation

The Reformulation Technology Roadmap

Reformulation is arguably the highest-return LOE strategy available to a commercial-stage pharmaceutical company, provided it happens early enough to shift physician prescribing behavior before generic entry. The core logic: create a patented successor product that offers a genuine patient benefit, transition the prescribing base before the original product goes generic, and let the generic market cannibalize the original rather than the successor.

The delivery system toolkit has expanded substantially in the past decade. Route-of-administration conversions, the IV-to-subcutaneous shift, the oral-to-transdermal patch transition, the tablet-to-oral disintegrating formulation change, each generates new IP claims covering the formulation, the device, and often a companion dosing algorithm. Extended-release and modified-release formulations generate new Orange Book listings independent of the original immediate-release product.

Fentanyl’s commercial lifecycle is a useful technology roadmap in compressed form. The IV formulation was the original approval. Duragesic (transdermal patch) added a second product with its own patent estate and patient population. Actiq (transmucosal lozenge) followed. Fentora (buccal tablet) and Onsolis (buccal film) each carried separate formulation patents covering mucoadhesive polymer systems. Each product served a specific patient subset with distinct clinical needs, and each generated independent Orange Book coverage. The commercial result was a decades-long fentanyl franchise in which generic entry into one formulation category had limited impact on the others.

Merck’s Keytruda Subcutaneous Strategy: A Live Case Study

Keytruda (pembrolizumab) is the clearest current-cycle example of IV-to-SC conversion as a lifecycle extension strategy. The original IV infusion, approved in 2014, requires 30 minutes of clinical administration every three weeks. The subcutaneous formulation approved by the FDA on September 19, 2025 as Keytruda Qlex delivers the same therapeutic effect in a two-minute injection every six weeks, a substantial convenience benefit for patients across 38 solid tumor indications.

Merck developed the SC formulation using berahyaluronidase alfa, a modified human hyaluronidase enzyme licensed from the South Korean company Alteogen, to enable rapid SC delivery of the large-molecule biologic. The SC formulation carries two issued patents from 17 pending applications, covering method-of-treatment and manufacturing process claims. If fully granted and successfully defended, these patents could extend Keytruda exclusivity into 2042, 14 years beyond the original compound patent expiry in 2028.

The IP situation is contested. Halozyme Therapeutics filed suit against Merck in the U.S. District Court in New Jersey in April 2025, alleging that Keytruda SC infringes Halozyme’s MDASE portfolio of patents covering modified human hyaluronidase polypeptides. Halozyme’s MDASE portfolio runs approximately 100 patents with expiry extending to 2034 in the U.S. Merck has filed inter partes review (IPR) petitions with the USPTO challenging seven MDASE patents. The litigation outcome will determine whether Merck can commercialize Keytruda SC freely or must reach a royalty-bearing license agreement. Halozyme has publicly indicated that a reasonable royalty structure on the MDASE portfolio would follow the 3 to 7 percent range it applies to its ENHANZE licensees.

From a financial modeling perspective, the delta between a Keytruda franchise that declines sharply after 2028 and one that migrates successfully to SC with exclusivity extending to 2042 is enormous. Merck CEO Rob Davis has described the SC transition as converting the patent cliff into a ‘hill.’ The company expects the SC formulation to capture 30 to 40 percent of Keytruda’s U.S. patient base by 2027. Even at 30 percent penetration, with SC carrying its own premium pricing and patent protection, the strategy materially alters the revenue trajectory.

Extended-Release and Controlled-Release Formulations

Extended-release (ER) and controlled-release (CR) formulations remain among the most widely deployed and commercially reliable reformulation strategies. The rationale is genuine clinical: once-daily dosing improves adherence, reduces peak-concentration adverse effects, and smooths the pharmacokinetic profile. These benefits support formulary differentiation even when payers pressure prescribers toward generics of the immediate-release form.

Eli Lilly’s Prozac Weekly, a weekly extended-release formulation of fluoxetine launched as daily Prozac’s compound patent neared expiry, provided a bridge strategy that retained a subset of patients who valued the once-weekly convenience despite daily generic fluoxetine being available at a fraction of the cost. The lesson: ER conversion works best when the convenience benefit is clinically meaningful to the patient and when the original twice or three-times-daily dosing carries adherence consequences that prescribers care about. Antidepressant compliance is exactly that kind of case.

Concerta (methylphenidate extended-release) used ALZA’s OROS osmotic delivery technology to create a patent-protected formulation of methylphenidate that outperformed immediate-release Ritalin on duration and tolerability in ADHD. Even after Concerta’s formulation patents expired, the OROS delivery mechanism itself remained a reference point for prescriber preference, illustrating that a delivery system can shape clinical standards even beyond its exclusivity period.

Key Takeaways: Section 5

Reformulation generates new Orange Book listings and new patent terms, but the clinical benefit must be genuine to survive prescriber and payer scrutiny. IV-to-SC conversion is the most active current reformulation category in biologics. Merck’s Keytruda SC represents the most consequential single reformulation bet in the current LOE cycle. ER and CR formulations remain highly reliable for oral small molecules in adherence-sensitive therapy areas. The fentanyl multi-formulation roadmap demonstrates how a single API can sustain a 20-year commercial lifecycle through successive delivery platform patents.

6. Indication Expansion: New Patents from Old Molecules

The Regulatory and IP Mechanics of New Indication Filings

A drug approved for one indication can receive supplemental NDA (sNDA) approval for additional indications, each supported by independent clinical data. Each new indication can generate method-of-use patents, new Orange Book listings, and additional regulatory exclusivities under the NCI three-year provision or orphan drug designation (seven years of exclusivity for drugs treating rare diseases affecting fewer than 200,000 U.S. patients annually). These layers of protection are independent of the original compound patent.

The commercial value of a new indication depends heavily on the therapy area’s reimbursement environment, the unmet medical need in the new patient population, and whether the indication requires the same dosage form or a distinct new formulation, the latter carrying its own IP. Oncology indication expansion has been particularly productive: checkpoint inhibitors like Keytruda and Opdivo (nivolumab) pursued a multi-indication strategy aggressively, accumulating dozens of approved tumor types under an umbrella compound patent estate, with each indication generating separate method-of-use patents and payer coverage decisions.

Repositioning vs. Indication Expansion: A Meaningful Distinction

Repositioning refers to identifying and developing an entirely new therapeutic application for an approved drug, typically one not anticipated at original approval. The distinction matters for IP strategy: a repositioned drug may have a longer development path because the new indication requires Phase II or Phase III evidence from scratch, but it also creates method-of-use patents with no prior art challenge if the new indication was genuinely not anticipated.

Sildenafil’s repositioning from a cardiovascular drug to Viagra for erectile dysfunction, and then to Revatio for pulmonary arterial hypertension, is the frequently cited example. Each indication generated separate dosage-form development, separate regulatory approvals, and separate patent estates. Revatio’s PAH patents allowed Pfizer to maintain an exclusivity period for the compound in one indication even after Viagra’s ED patents expired.

Pediatric Exclusivity as an Indication-Adjacent Strategy

The FDA grants six months of pediatric exclusivity to sponsors who complete required pediatric studies under a Written Request. This extension attaches to all existing patents and exclusivities on the drug, including compound patents, formulation patents, and NCE exclusivity. For a drug with $2 billion in annual U.S. sales, six months of additional exclusivity is worth approximately $1 billion in gross revenue, often dramatically exceeding the cost of the pediatric studies themselves. The strategy works for any drug without prior pediatric approval, giving IP teams a relatively low-complexity path to a meaningful exclusivity extension.

Key Takeaways: Section 6

Every new indication generates independent method-of-use patent opportunities and new Orange Book listings. NCI exclusivity adds three years per new indication with clinical data support. Orphan drug designation adds seven years for qualifying rare disease indications. Pediatric exclusivity adds six months to all existing IP, with typical ROI far exceeding study costs. Multi-indication oncology strategies, as demonstrated by the checkpoint inhibitor class, can accumulate a patent estate that remains relevant long after the underlying compound patent expires.

7. Authorized Generics: Competing Against Yourself

Structure and Strategic Rationale

An authorized generic is a copy of the brand-name drug, identical in formulation, manufactured under the same NDA, and sold by the innovator or a partner at generic prices. It does not require a separate ANDA. The innovator launches it either directly through a subsidiary or via a licensing agreement with an established generic distributor, typically immediately upon patent expiry or in response to a first generic entrant.

The authorized generic creates two revenue streams where the innovator previously had one. The branded product continues selling to price-insensitive patients, payers that require branded dispensing, and markets where formulary positioning remains strong. The authorized generic captures volume from price-sensitive patients and payers who would otherwise switch to independent generics entirely. The net revenue per unit from the authorized generic is lower than the brand price but substantially higher than zero.

Authorized generics are most effective when multiple independent generic competitors are entering simultaneously, which drives generic prices toward commodity levels. In a scenario with six generic entrants, the authorized generic secures one rational market share position in a deeply competitive segment rather than competing ineffectively on branded pricing. The timing matters: an authorized generic launched on day one of generic entry establishes supply chain relationships and formulary contracts that independent generics must displace.

First-Filer Exclusivity and the 180-Day Window

The Hatch-Waxman Act grants 180 days of generic market exclusivity to the first ANDA filer who successfully completes a Paragraph IV challenge. During this window, no other generic can enter the market, and the first filer can price at a meaningful premium above eventual commodity generic levels. An authorized generic launched simultaneously with a Paragraph IV first filer effectively converts 180-day exclusivity from a duopoly to a triopoly, compressing the first filer’s economics. Brands have used this tactic deliberately to weaken the incentive for Paragraph IV challenges, though the FTC has raised market competition concerns about the practice in some contexts.

Key Takeaways: Section 7

Authorized generics preserve a share of volume economics that would otherwise transfer entirely to independent generic entrants. Their impact on total LOE revenue erosion typically reduces the decline rate in the first 12 to 24 months post-expiry. The tactic is particularly valuable when rapid multi-generic entry is anticipated and when the innovator has manufacturing scale advantages over independent generic entrants.

8. Biologic-Specific Strategies and Biosimilar Interchangeability Defense

Why Biologics Require a Different Playbook

Biologic drugs, including monoclonal antibodies, fusion proteins, and protein scaffolds, differ from small molecules in ways that fundamentally change LOE strategy. Their manufacturing complexity, involving cell culture, purification sequences, and formulation conditions that directly affect clinical performance, means that a biosimilar is not a generic equivalent in the same strict chemical sense. Two biologic products with the same reference sequence can have different glycosylation profiles, aggregation behaviors, and immunogenicity risks depending on how they were made.

This manufacturing complexity creates several strategic advantages for originators. First, it raises the barrier for biosimilar developers, who must demonstrate biosimilarity through extensive analytical, preclinical, and clinical data packages that cost $100 million to $200 million or more per product, compared to $2 million to $5 million for a typical small-molecule ANDA. Second, it creates physician hesitancy around automatic substitution, particularly for high-stakes therapy areas like oncology, transplant, and immunology, that small-molecule generics do not face. Third, it provides grounds for patient advocacy around ‘non-medical switching,’ the practice of transitioning a stable patient from originator to biosimilar for cost reasons.

Biosimilar Interchangeability Designation: The Key Competitive Barrier

FDA’s interchangeability designation, established under the BPCIA and finalized in regulatory guidance, allows a pharmacist to substitute a biosimilar for the reference biologic at the point of dispensing without prescriber intervention, exactly as pharmacists can substitute generic drugs. Interchangeability requires the sponsor to demonstrate that switching back and forth between the biosimilar and the reference product does not produce worse outcomes than continuous use of the reference product alone, a ‘switching study’ requirement that adds time and cost to the biosimilar development program.

For originators, delaying a competitor’s interchangeability designation extends the period during which prescriber-level, drug-by-drug substitution decisions are required rather than automatic pharmacy-level substitution. This buys time for patient support programs, hub services, and formulary contracting to entrench the originator product. Even after the first interchangeable biosimilar is approved, the originator typically retains 40 to 60 percent of unit volume for an extended period, compared to the 10 to 20 percent retention typical for small molecules 24 months after generic entry.

The BPCIA Patent Dance: Structure and Strategic Use

The BPCIA establishes a mandatory information exchange between the biosimilar applicant (aBLA sponsor) and the reference product sponsor (RPS) before any litigation can proceed. The aBLA sponsor provides its application and manufacturing information. The RPS identifies patents it believes are infringed. The parties then negotiate a list of patents to litigate in ‘immediate patent resolution,’ and any remaining patents form a ‘stand-by’ list for later litigation.

RPS teams use the patent dance to assess which biosimilar development choices the competitor made, gaining intelligence on the manufacturing process and formulation that is unavailable through public filings. This intelligence can inform both litigation strategy and next-generation product development. It can also reveal whether the biosimilar developer made choices that avoid the most well-defended formulation or manufacturing patents, identifying weaknesses in the RPS’s secondary patent coverage.

AbbVie Humira: The Patent Thicket Standard

AbbVie filed over 160 U.S. patents covering Humira’s compound (adalimumab), formulations, devices (prefilled syringe, autoinjector), manufacturing processes, and methods of use across rheumatoid arthritis, psoriasis, Crohn’s disease, and other indications. The first adalimumab compound patent expired in 2016. The European Medicines Agency approved Amgen’s Amjevita biosimilar in September 2016. But U.S. market entry did not occur until 2023, seven years later, because AbbVie successfully used its secondary patent thicket and litigation strategy to exclude biosimilar entrants until it negotiated a series of licensing agreements with U.S. market entry dates no earlier than January 31, 2023.

The financial impact: AbbVie collected approximately $200 billion in cumulative Humira revenue between 2003 and the start of biosimilar competition. The secondary patent thicket contributed directly to the company’s ability to generate roughly $20 billion per year in Humira U.S. sales through 2022. Biosimilar share of the adalimumab market reached approximately 25 percent by the end of 2023 and expanded through 2024 as interchangeable biosimilars accumulated formulary wins.

Key Takeaways: Section 8

Biologic LOE unfolds over years rather than months, driven by the complexity of biosimilar development and the interchangeability barrier. The BPCIA patent dance provides originators with competitive manufacturing intelligence that small-molecule Hatch-Waxman litigation does not. Patent thicket architecture, deployed systematically from early commercialization, is the most proven strategy for extending effective biologic exclusivity. Interchangeability designation is the single most important biosimilar competitive threat to monitor; originators should track all interchangeability-designated competitors by product and therapy area.

9. IRA Medicare Price Negotiation: A New LOE Accelerant

What the IRA Actually Does to Pharma Pricing

The Inflation Reduction Act of 2022 gave the Secretary of Health and Human Services direct negotiating authority over a selected list of high-spend Medicare Part D drugs, beginning with 10 drugs in 2026, expanding to 15 in 2027, 15 more in 2028, and 20 per year from 2029 onward. The negotiated prices are called Maximum Fair Prices (MFPs) and are statutory ceilings: Part D plans pay no more than the MFP plus a dispensing fee.

To be eligible for negotiation, a small-molecule drug must have been FDA-approved for at least seven years and have no marketed generic competitor. A biologic must have been licensed for at least 11 years without a biosimilar competitor. Orphan drugs designated for a single rare disease and low-spend drugs (below $200 million in annual Medicare expenditure) are excluded. The IRA also requires manufacturers to pay inflation rebates if their list prices rise faster than the general inflation rate, a provision already in effect since 2023.

The MFPs for the first 10 negotiated drugs, effective January 2026, range from a 38 percent discount from 2023 list price for Imbruvica to a 79 percent discount for Januvia. Eliquis is set at $231 per month against a $521 list price. Enbrel drops to a price reflecting more than a 60 percent discount. The CBO estimated the IRA’s drug negotiation provision reduces the federal deficit by $96 billion over 10 years.

How IRA Negotiation Interacts With LOE Strategy

The IRA creates a pre-patent-expiry price compression event that runs parallel to the traditional patent cliff. Before IRA, the revenue curve for a Medicare-dominant drug was roughly flat until LOE, then dropped sharply. Under IRA, the curve begins declining before LOE, as MFPs reduce net realized price while the drug still has patent protection.

For drugs selected for negotiation, this changes the financial calculus of lifecycle extension strategies. If the Medicare price is already compressed by 50 to 79 percent while the patent is still valid, the economic rationale for spending $200 million on a new formulation to extend exclusivity becomes weaker. The reformulation strategy works only if the new product qualifies as a new NDA rather than being tethered to the original negotiated drug’s MFP. FDA’s guidance on what constitutes a sufficiently novel product to escape a prior MFP designation is an active area of regulatory intelligence for pharma legal teams in 2025 and 2026.

The IRA also has a practical impact on the Paragraph IV litigation calculus. A drug whose Medicare price is already heavily negotiated generates less incremental revenue per year of exclusivity extension, reducing the ROI threshold for expensive IP litigation. Companies should model their Paragraph IV defense investment net of the expected IRA-discounted revenue the defense would protect, not against historical pre-IRA net pricing.

Investment Strategy: IRA as a Compounding LOE Risk Factor

For investors analyzing LOE exposure, IRA negotiation adds a second risk layer to selected drugs. The first layer is patent expiry and generic entry. The second is MFP imposition, which can arrive years before patent expiry for drugs that qualify. Eliquis carries both risks concurrently: an MFP effective January 2026 and patent expiry in 2028. The combined effect on BMS’s Eliquis revenue run rate over the 2026 to 2030 period is substantially larger than either factor in isolation.

A useful screen: for any drug with more than $1 billion in annual Medicare Part D spending and no biosimilar or generic competitor, assess whether it meets IRA selection criteria. If it does, build a probability-weighted MFP scenario into the five-year revenue model. Consensus sell-side models frequently underweight this risk for drugs where patent expiry appears distant, because analysts anchor on the patent date rather than the IRA selection timeline.

10. Lifecycle Management Through M&A

Using Acquisitions to Replace Patent-Exposed Revenue

When organic pipeline development cannot fill the revenue gap from an approaching patent cliff within the required timeframe, acquisition is the accelerant of choice. The M&A pace in pharma reflects this directly: the current patent cliff cycle is driving the most intense acquisition activity since the megamerger era of the early 2000s.

The three largest recent deals illustrate the strategic pattern. Johnson & Johnson’s $14.6 billion acquisition of Intra-Cellular Therapies in April 2025 added lumateperone (Caplyta), an approved neurology asset in depression and bipolar disorder, providing commercial revenue to offset J&J’s Stelara and Xarelto headwinds. Merck’s $10 billion purchase of Verona Pharma, completed in October 2024, added ensifentrine (Ohtuvayre), a COPD inhaled therapy approved in June 2024, expanding the company’s respiratory footprint ahead of Keytruda’s 2028 cliff. Sanofi’s up-to-$9.5 billion acquisition of Blueprint Medicines in July 2024 added avapritinib and a pipeline of KIT/PDGFRA oncology assets to Sanofi’s immunology portfolio.

The pattern in all three cases: companies with multi-billion-dollar LOE events approaching within three to five years, acquiring commercial-stage or near-commercial assets in therapy areas where they have existing commercial infrastructure, to convert anticipated revenue declines into portfolio diversification.

Bolt-On Acquisitions for Pipeline Diversification

Below the headline megadeals, smaller bolt-on acquisitions targeting Phase II or Phase III assets in key therapy areas offer a different risk-return profile. The asset price is lower because development risk remains, but the buyer gains years of additional exclusivity from the acquired asset’s own patent term running from filing date, which for a Phase III asset typically means a full commercial period ahead.

For IP teams evaluating target companies, the quality of the acquiree’s patent portfolio is a first-order screen. A Phase III asset with a thin patent estate, covering only the compound patent without secondary protection, carries accelerated LOE risk that will repeat the acquiring company’s current problem 10 to 12 years after the acquisition. Targets with well-constructed secondary patent portfolios, filed during clinical development, are worth a meaningful valuation premium.

Key Takeaways: Section 10

M&A is the fastest mechanism for replacing patent-cliff revenue, but deals signed today address 2030 to 2032 gaps, not immediate cliff events. The strategic value of an acquisition target is inseparable from the quality of its patent estate. Bolt-on Phase III acquisitions with strong secondary patent construction are preferable to commercial-stage assets with thin IP, even at a lower nominal price.

11. Licensing, Collaboration, and Patent Settlements

Royalty Structures and Licensing Economics

Licensing an originator’s technology to generic manufacturers rather than competing head-to-head generates a revenue stream from what would otherwise become zero-margin competition. The structure typically involves an upfront fee, milestone payments triggered by generic approval and launch, and ongoing royalties as a percentage of net sales. Royalty rates in pharma licensing range broadly, from 2 to 3 percent for commodity API technology to 15 to 20 percent for proprietary delivery platforms in high-value therapy areas.

For originator companies, a licensing arrangement converts a competitor into a revenue-sharing partner. The trade-off is accepting a smaller share of a market that generics will eventually dominate anyway, in exchange for certainty, earlier revenue recognition, and reduced litigation cost. Companies that have elected this approach typically do so when they have modeled that litigation is likely to fail, when the generic market is so fragmented that competing on price is economically irrational, or when the licensing revenue can fund higher-return investments in next-generation pipeline assets.

Authorized Generic Licensing vs. Third-Party Collaboration

The choice between launching an authorized generic through a wholly-owned subsidiary and licensing it to an established generic distributor depends on the originator’s manufacturing capacity, its generic market relationships, and its strategic appetite for the generic business long-term. Companies like Pfizer (through Greenstone, now divested) and Novartis (through Sandoz, now a standalone company since October 2023) built generic subsidiaries as permanent infrastructure. Other companies prefer licensing because the generic business requires a fundamentally different commercial model, cost structure, and talent base.

Key Takeaways: Section 11

Licensing to generics is an underutilized strategy for originators that model weak litigation prospects. Authorized generic licensing to established distributors is operationally simpler than building in-house generic infrastructure and is particularly well-suited to companies with single-product LOE events rather than ongoing generic franchises.

12. Strategic Pricing Decisions Around Loss of Exclusivity

The Counterintuitive Logic of Price Increases Before LOE

The standard assumption is that approaching generic competition should trigger brand price reductions to hold volume. The actual behavior in the pharmaceutical market is often the opposite. Many originators raise brand prices in the 12 to 24 months before LOE, because the patients and payers still using the branded product at that stage are systematically less price-sensitive than those who will switch to generics. Price increases at this stage extract maximum value from a shrinking but loyal patient segment.

AstraZeneca’s pricing behavior on Prilosec (omeprazole) in the period before generic entry, and its simultaneous transition to Nexium at a higher price point, illustrates the strategy at scale. Brands that raise prices aggressively before LOE accept lower unit volume in exchange for higher per-unit revenue, optimizing for total revenue rather than market share. The inflection point where further price increases generate net revenue declines rather than gains requires precise price-volume elasticity modeling specific to the drug, payer mix, and therapy area.

Segmented Pricing and Channel Strategy

Payer contracting in the U.S. pharmaceutical market enables price segmentation across channels in ways that are not available in most other industries. A brand near LOE can maintain a high Wholesale Acquisition Cost (WAC) for commercial insurance channels where brand loyalty is strong, while offering deeper rebates to Medicaid managed care organizations where formulary exclusion is the alternative. Medicare Part D contracting introduces a third price point after IRA MFP implementation.

The channel segmentation decision interacts directly with the authorized generic strategy. If the originator launches an authorized generic at 40 to 50 percent below WAC, it anchors the generic market at a specific price level that independent generics must undercut. The branded product, still priced at or above its pre-LOE level for loyal commercial patients, sits in a structurally different market tier.

Key Takeaways: Section 12

Price increases before LOE are rational for brands with loyal patient segments that are immune to generic substitution. Segmented payer contracting allows originators to extract maximum revenue from commercial channels while managing Medicaid and Medicare exposure separately. IRA MFP imposition adds a mandatory floor that cannot be arbitraged through rebate structures for Medicare Part D transactions.

13. Patient Retention Programs and Brand Loyalty

Copay Assistance Programs: Mechanics and ROI

Copay assistance programs, in which the manufacturer covers the patient’s out-of-pocket cost share for a branded drug, directly address the price differential that drives generic switching at the point of dispensing. For a chronic-disease drug where a generic might cost $10 per month and the branded copay without assistance is $60 per month, a copay assistance card that brings the branded out-of-pocket cost to $0 or $5 eliminates the patient-level price signal entirely.

Industry data suggests that well-deployed copay assistance programs, launched three to six months before LOE, can generate two to twenty times return on investment depending on the program structure and the drug’s patient population. The highest ROI scenarios involve chronic-disease drugs with long titration periods, high patient inertia, and therapy areas where prescribers have clinical reasons to prefer brand continuity. Low-complexity chronic diseases with well-established generic safety records generate lower ROI.

The CMS ‘copay accumulator’ rules complicate this strategy for commercially insured patients with high-deductible health plans (HDHPs): under accumulator rules, manufacturer copay assistance does not count toward the patient’s deductible, meaning the patient still faces full cost-sharing once the deductible is met. This reduces the effectiveness of copay assistance for HDHP patients and shifts the focus of retention programs toward non-copay-reduction tactics like patient support services and adherence programs.

Hub Services and Patient Support Infrastructure

Hub services, centralized patient support operations that handle prior authorization assistance, specialty pharmacy coordination, nurse case manager programs, and refill reminder systems, create operational stickiness that generic manufacturers cannot easily replicate. A patient enrolled in a branded hub program who has built a relationship with a nurse case manager and relies on the hub for prior authorization renewal has a higher switching cost than a patient relying only on standard pharmacy dispensing.

Hub investment is particularly high-return for specialty drugs, biologics, and drugs in therapy areas where adherence directly affects clinical outcomes and where treatment discontinuation carries clinical risk. Oncology, immunology, and rare disease are the primary categories.

Key Takeaways: Section 13

Copay assistance programs launched three to six months before LOE represent the highest near-term ROI retention tactic for chronic-disease brands. Hub services create clinical stickiness that is durable beyond the copay assistance mechanism. CMS accumulator rules reduce copay card effectiveness for HDHP patients and should be factored into program design.

14. Geographic Expansion and Emerging Market Tactics

Differential Patent Timelines Across Jurisdictions

Patent expiry dates differ by jurisdiction. A drug may lose exclusivity in the U.S. in 2026 while European patent protection holds until 2028 under Supplementary Protection Certificates (SPCs), which function analogously to U.S. PTR but with separate legal requirements. In Japan, the drug patent term is also 20 years from filing, with a five-year extension available under Japan’s patent term extension system. Emerging markets, particularly in Southeast Asia, Sub-Saharan Africa, and parts of Latin America, have patent systems with varying enforcement capacity and data exclusivity frameworks.

For commercial teams, differential expiry creates geographic revenue management opportunities. Resources pulled from the U.S. market after LOE can shift to markets where exclusivity remains intact. European SPC protection justifies continued marketing investment even after U.S. generic entry. In markets where patent enforcement is weak but health system growth is strong, a company’s brand equity and supply chain relationships can sustain branded market share at premium prices even without patent protection, provided quality differentiation is credible.

Emerging Markets: Growth Headroom and Structural Complexity

Middle-income markets including Brazil, Mexico, Indonesia, India (for branded products), and Turkey offer pharmaceutical market growth rates of 7 to 12 percent annually, compared to 2 to 4 percent in mature Western markets. In many of these markets, generic penetration for even off-patent drugs is lower than in the U.S. or Europe, because generic regulatory capacity is less developed, branded drug preference among prescribers is stronger, and health system infrastructure favors established commercial brands.

The structural complexity is real. Local regulatory requirements, pricing approval processes in markets with reference pricing systems, distribution infrastructure in markets with limited wholesale networks, and political risk around drug pricing regulation all require substantial local capacity and market-specific investment. Companies that treat emerging markets as simple revenue extensions of their developed-market commercial model consistently underperform against companies that invest in genuine local market expertise.

India presents a distinct case for originator companies. India does not grant product patents on pharmaceutical compounds under Section 3(d) of the Indian Patents Act, which requires a showing of significantly enhanced efficacy for patentability of known substances. Originator products compete in the Indian market against domestic generic manufacturers without patent protection, making brand equity, physician relationships, and quality signals the primary commercial levers.

Key Takeaways: Section 14

SPC and patent term extension systems in Europe and Japan allow continued exclusivity after U.S. LOE, justifying continued investment in those markets. Emerging markets offer structurally higher growth rates but require dedicated local infrastructure. India’s Section 3(d) doctrine eliminates originator patent protection for most small molecules, requiring a fundamentally different commercial strategy.

15. Regulatory Intelligence and Policy Monitoring

Tracking the FDA’s Generic Drug Approval Pipeline

Every ANDA filed with the FDA creates a public record in the FDA’s drug approval database. IP teams and competitive intelligence functions that monitor ANDA filings for their pipeline products gain advance warning of generic entry timelines. The FDA’s Generic Drug User Fee Act (GDUFA) performance goals, including a 10-month review target for original ANDAs, provide an approximate timeline from ANDA filing to approval.

Paragraph IV certifications, which require written notification to the NDA holder within 20 days of acceptance by the FDA, provide additional advance warning: a Paragraph IV cert arrives before the generic is approved, not after, giving the brand time to evaluate litigation options before the 45-day clock for filing a patent infringement complaint begins. IP teams that have not invested in ANDA monitoring programs are consistently surprised by Paragraph IV notifications that a systematic monitoring program would have anticipated.

The 505(b)(2) Pathway and Its Competitive Implications

The 505(b)(2) NDA pathway allows an applicant to rely on published literature or existing FDA safety and efficacy findings for some or all of an application, accelerating development of modified-release formulations, new salts, new delivery systems, and combination products. For originator companies pursuing reformulation as an evergreening strategy, the 505(b)(2) pathway is the regulatory mechanism that makes the strategy executable within a commercially relevant timeframe.

Competitors can also use 505(b)(2) to file reformulation-based ANDAs that challenge an originator’s secondary product patents, a tactic particularly common in modified-release drug delivery. An originator that builds a commercial franchise around an ER reformulation should expect 505(b)(2)-based Paragraph IV challenges to that product’s formulation patents, not just the compound patent of the original IR product.

Key Takeaways: Section 15

ANDA monitoring is a non-negotiable function for any commercial-stage pharmaceutical brand. Paragraph IV notification arrives before generic approval and before litigation deadlines, making systematic monitoring a material competitive advantage. 505(b)(2) filers targeting reformulation-based evergreening strategies should expect IP challenges from both ANDA filers and other 505(b)(2) applicants.

16. Investment Strategy: Modeling LOE Events for Institutional Portfolios

Building the LOE Revenue Curve

An LOE event for a branded drug follows a characteristic revenue pattern, but the shape varies substantially based on therapy area, generic competitor count, biosimilar vs. small molecule, payer mix, and originator strategy. The standard modeling approach is to project peak pre-LOE revenue, apply a generic market share curve driven by entrant count and timing, and apply a separate pricing curve for the brand’s residual volume.

For small molecules with full generic availability and no authorized generic, brand volume typically drops to 15 to 25 percent of pre-LOE levels within 12 months and to 5 to 10 percent within 24 months. Net realized price for the brand segment often holds or even increases as remaining volume concentrates among price-insensitive patients. The total brand revenue outcome is lower volume at higher per-unit revenue, partially offsetting the volume loss.

For biologics with biosimilar competition but no interchangeability designation, brand volume retention is substantially better: 50 to 65 percent of unit volume within 12 months is common in immunology and oncology therapy areas. Interchangeable biosimilar approval triggers faster penetration, but the timelines for interchangeable biosimilar development typically add 18 to 36 months beyond initial biosimilar approval.

Key Signals for Portfolio Construction

Several leading indicators should trigger model updates ahead of consensus LOE event pricing in pharma equities. Watch for Paragraph IV notification filings, which trigger Lexis-Nexis and FDA database alerts before any press release. Track ANDA filing activity for drugs with Orange Book patent expiry within 24 to 36 months. Monitor IRA drug selection cycles, which occur annually, for drugs meeting CMS selection criteria. Watch for Phase III biosimilar data releases and FDA aBLA acceptance letters for any reference biologic in the portfolio.

On the lifecycle extension side, track NDA and sNDA filings for reformulated versions of products approaching LOE. A 505(b)(2) or supplemental biologic license application (sBLA) filed two to three years before the primary patent expiry is a strong signal of an originator’s lifecycle management investment and should be factored into extended exclusivity scenarios.

AbbVie’s trajectory from 2019 to 2024, in which the company used Humira’s thicket-protected U.S. revenue to fund the oncology, immunology, and neuroscience acquisitions that built Skyrizi (risankizumab) and Rinvoq (upadacitinib) into multi-billion-dollar franchises, represents the model for how a well-executed LOE management strategy converts a potential cliff into a successful revenue transition. Both Skyrizi and Rinvoq have moved toward peak-sales trajectories that partially offset the Humira biosimilar revenue erosion that accelerated through 2024.

Synthesis: The Strategic Logic Underlying Every Approach

Every strategy in this guide, whether patent prosecution, reformulation, indication expansion, authorized generics, biosimilar interchangeability defense, pricing segmentation, or M&A, reduces to a single operational question: how does the company create and sustain economic distance between its product and the commodity version that generic or biosimilar competition will inevitably produce?

Economic distance can come from genuine clinical differentiation, which payers and prescribers will pay a premium to access. It can come from IP protection, which excludes competitors by law. It can come from operational efficiency, which allows the originator to manufacture and distribute at a cost that makes authorized generic economics viable. It can come from commercial infrastructure, the hub services, patient support programs, and payer contracting relationships that generic manufacturers cannot replicate at launch.

The companies that manage LOE events most successfully are the ones that build all four sources of economic distance simultaneously, starting early enough that each element is mature before the patent cliff arrives. The companies that struggle are the ones that treat LOE planning as a legal problem, delegated to the patent department, rather than a company-wide commercial and scientific challenge that requires coordinated investment years before any single drug’s patent expiry date.