Generic drugs account for nearly 90% of all prescriptions dispensed in the United States yet represent only about 20% of total drug spending [1]. That gap between volume and cost is not an accident of the market. It is the direct product of a legal architecture that took four decades to build, layer by layer, through congressional deals, Supreme Court rulings, regulatory guidance documents, and thousands of hours of federal court litigation. Every generic that reaches a pharmacy shelf does so because someone, somewhere, correctly read a set of patent expiration dates, regulatory exclusivity periods, and litigation risk profiles.

This article is for the people doing that reading. Patent attorneys preparing Paragraph IV certifications. Business development executives modeling generic entry timelines. Institutional investors evaluating pharmaceutical company moats. Regulatory affairs professionals mapping the clearance path for an Abbreviated New Drug Application. If you need a clear-eyed, granular account of how generic pharmaceutical patent and FDA law actually works, including where the system produces predictable outcomes and where it produces chaos, this is it.

We cover the full stack: how pharmaceutical patents are granted and what they cover, how the Orange Book links those patents to FDA approval, how the Hatch-Waxman Act created the litigation ecosystem that now consumes hundreds of millions in legal fees annually, and how modern strategic patenting has stretched brand exclusivity well beyond what Congress envisioned in 1984. We also examine the economics of generic entry, the biosimilar pathway’s distinct legal framework, the liability asymmetry created by PLIVA v. Mensing, and the policy proposals now moving through Washington that could restructure the entire competitive landscape.

Part I: The Patent System and How It Applies to Drugs

What a Pharmaceutical Patent Actually Covers

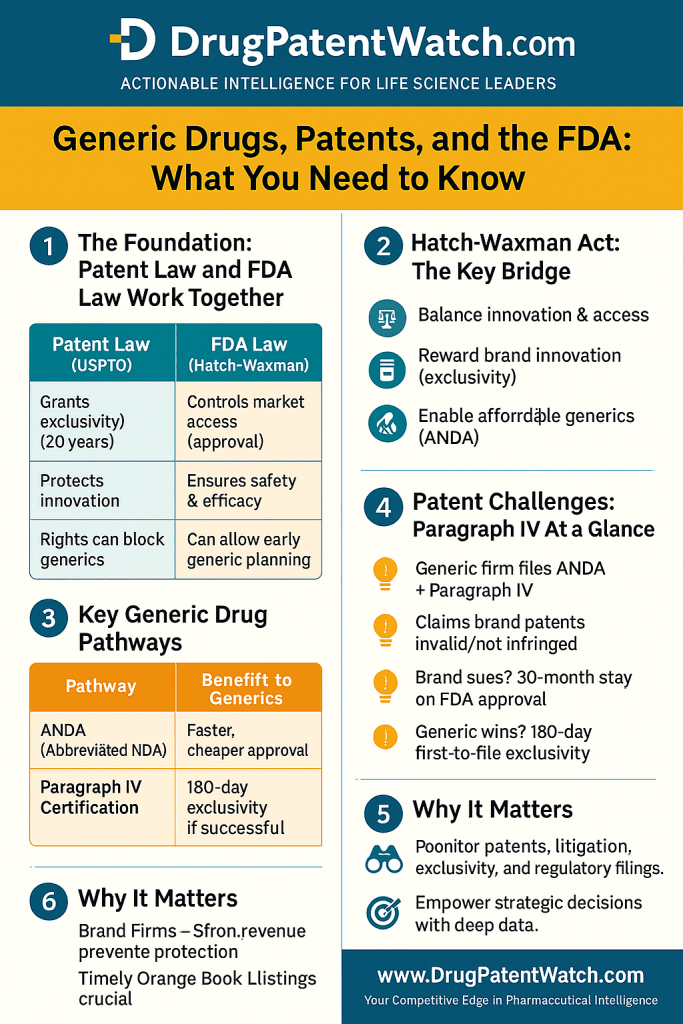

A patent grants its holder the right to exclude others from making, using, selling, or importing the patented invention for 20 years from the filing date [2]. In pharmaceutical development, that broad definition translates into a surprisingly granular set of possible claim types, each with different strategic implications for generic entry.

The most valuable patent type is the compound patent, sometimes called a composition-of-matter patent. This covers the active pharmaceutical ingredient (API) itself. When a company like Pfizer patents a new molecule, that compound patent functions as an absolute bar on generic competition for as long as it remains valid and in force. Any generic manufacturer wanting to sell a drug containing that molecule must either wait for the patent to expire, negotiate a license, or challenge its validity.

Below the compound patent sits a cascade of secondary patents covering formulation, method of use, and manufacturing process. A formulation patent covers how the API is packaged: its salt form, polymorphic crystal structure, extended-release coating, or delivery vehicle. A method-of-use patent covers the clinical application, such as using compound X to treat condition Y. A process patent covers how the molecule is synthesized. These secondary patents can extend meaningful commercial exclusivity long after the original compound patent expires.

This layering is not incidental. It is the central strategy of modern pharmaceutical lifecycle management. The compound patent gives a brand its original monopoly. The secondary patents give it a second act. For a drug like AbbVie’s Humira, the secondary patents gave it a third and fourth act as well.

The 20-Year Clock and Why Effective Patent Life Is Much Shorter

On paper, pharmaceutical patents last 20 years. In practice, effective patent life is typically eight to twelve years from commercial launch [3]. The compression happens because the clock starts at filing, not approval. Drug developers file patents early, often before entering clinical trials, to secure priority dates. The FDA approval process for a new molecular entity then consumes another seven to twelve years. By the time a drug reaches the market, most of its nominal patent term has already burned.

Congress addressed this partially with patent term extension (PTE) under 35 U.S.C. § 156, which allows brands to recover up to five years of patent life lost to FDA review. The total remaining patent life after PTE cannot exceed 14 years from FDA approval. To qualify, the brand must apply for the extension within 60 days of approval and the extension applies to only one patent per drug [4].

Patent term extension matters enormously for blockbuster drugs. When AstraZeneca’s Prilosec (omeprazole) received an extension covering its formulation patent, it bought the company additional years of market exclusivity worth billions. When generic manufacturers challenged that extension’s scope, the litigation ran for years across multiple district courts.

The PTO-FDA Split: Two Agencies, One Bottleneck

The United States Patent and Trademark Office (PTO) grants patents without any involvement from the FDA. The FDA approves drugs without independently assessing patent validity. The two agencies operate on entirely separate legal tracks that only converge in one place: the Orange Book.

This separation creates a structural asymmetry that experienced pharmaceutical litigators exploit routinely. The PTO examines patent applications under a ‘preponderance of the evidence’ standard and typically takes three to five years to complete examination. The FDA evaluates safety and efficacy data and has no authority to look behind a listed patent or assess whether it is valid. That means a brand can list a patent of questionable validity in the Orange Book, triggering a 30-month litigation stay against any generic challenger, even if the patent would fail under careful legal scrutiny.

The FDA has gradually pushed back on this dynamic. Its 2020 and 2021 guidance documents on Orange Book patent listing made clear that only patents claiming the approved drug itself or its approved method of use may be listed [5]. The FTC issued a series of formal challenge letters to brands in 2023 and 2024, targeting Orange Book listings for patents covering devices like inhalers and autoinjectors rather than the drugs themselves. But the agency’s enforcement tools are limited, and the listing abuses continue.

Part II: The Orange Book

How the Orange Book Works and Why It Controls Generic Entry

The FDA’s Approved Drug Products with Therapeutic Equivalence Evaluations, universally called the Orange Book, is the document that connects pharmaceutical patents to the FDA approval process for generics. Every brand drug approved under a New Drug Application (NDA) must disclose its associated patents to the FDA, which lists them in the Orange Book. Generic applicants must then certify, for each listed patent, what their relationship to that patent will be upon launch.

The Orange Book does two things simultaneously. It is a transparency mechanism, making patent data publicly available so generic manufacturers can plan their development programs. It is also a trip wire, because certifying against a listed patent under Paragraph IV automatically exposes the generic applicant to patent infringement litigation before they have sold a single pill.

Data platforms like DrugPatentWatch aggregate and analyze Orange Book listings across thousands of drugs, giving generic manufacturers, investors, and IP teams a structured view of which drugs have patent coverage expiring on what dates, which have active Paragraph IV challenges, and which have already been successfully challenged. That kind of structured intelligence is the starting point for any rational generic pipeline decision.

The Four Paragraph Certifications

When a generic manufacturer files an Abbreviated New Drug Application (ANDA), it must submit one of four certifications for each patent listed in the Orange Book:

Paragraph I: The patent information has not been filed. Rare in practice, since most approved drugs have listed patents.

Paragraph II: The patent has expired. The generic can launch immediately upon FDA approval.

Paragraph III: The patent will expire on a specific date. The generic agrees to wait until expiration. FDA approval is granted but with a deferred effective date tied to patent expiry.

Paragraph IV: The patent is invalid, unenforceable, or will not be infringed by the generic. This is the challenge certification. Filing it is a legal act that functions as a constructive act of infringement under 35 U.S.C. § 271(e)(2), inviting a lawsuit before any product has been sold.

The Paragraph IV pathway is where the money is. It is also where most of the risk is. A generic manufacturer that files a successful Paragraph IV challenge and invalidates a brand patent eliminates a barrier not just for itself but for every subsequent generic applicant. The first filer gets compensated for bearing that risk through 180-day exclusivity. Everyone who files after the first challenge gets a free ride on the litigation outcome.

The 45-Day Trigger and the 30-Month Stay

When a generic files a Paragraph IV certification, federal law requires the generic to notify the brand NDA holder within 20 days [6]. The brand then has 45 days to decide whether to sue for patent infringement. If it does, the FDA cannot approve the ANDA for 30 months, or until a court rules the patent invalid or not infringed, whichever comes first.

The 30-month stay is the mechanism that makes patent listing strategy so commercially important. A brand that lists patents aggressively can extend market exclusivity by 30 months beyond its substantive legal position. Even if the brand ultimately loses the patent case, it has enjoyed 30 months of litigation-protected exclusivity while the case proceeded. On a drug generating $2 billion annually, that is a $5 billion value transfer.

This is not a hypothetical. It is why Sanofi listed device patents covering its EpiPen competitor’s autoinjector in the Orange Book, why AstraZeneca listed inhaler patents for Symbicort, and why AbbVie listed 75 patents covering various aspects of Humira despite the original adalimumab compound patent having long since been the core of its protection. In each case, the listing strategy bought time. Time is money when the product in question generates billions per year.

Part III: The Hatch-Waxman Act

The 1984 Compromise That Created the Modern Generic Industry

Before the Drug Price Competition and Patent Term Restoration Act of 1984, commonly called Hatch-Waxman, the U.S. generic drug industry barely existed. Generic manufacturers had no clear legal pathway to use brand clinical data as the basis for their own approval. They either had to conduct their own expensive clinical trials, which eliminated most of the cost advantage of going generic, or wait until every patent expired, which often meant waiting decades.

Hatch-Waxman solved this by creating the ANDA pathway, which allows a generic to piggyback on the brand’s NDA data by demonstrating pharmaceutical equivalence and bioequivalence rather than re-establishing safety and efficacy from scratch. It simultaneously gave brands something in return: the patent term extension mechanism described above and the 30-month litigation stay that gives brands a meaningful chance to litigate patent challenges before generics reach the market.

The act was a genuine compromise. It gave generic manufacturers a legal right they had not previously enjoyed and gave brands procedural protections to defend their intellectual property. Four decades later, the tradeoffs embedded in that compromise are showing their age. The generic industry has grown into a $139 billion market in the United States alone [7]. The tools brands use to exploit Hatch-Waxman protections have become far more sophisticated than Congress imagined. The patent thicket and pay-for-delay phenomena that now dominate pharmaceutical IP strategy did not exist in 1984.

180-Day Exclusivity: The First-Filer Reward

A generic manufacturer that is the first to file a Paragraph IV certification against a listed patent receives 180 days of market exclusivity upon launch. During that window, the FDA cannot approve any other ANDA for the same drug [8]. This exclusivity is the economic incentive that makes expensive patent litigation rational. Without it, a generic firm would bear the full litigation cost only to have a dozen competitors enter the market simultaneously the day after winning.

The value of 180-day exclusivity depends heavily on the drug’s commercial profile. For a $5 billion-per-year brand with weak patent protection, first-filer status can be worth hundreds of millions. For a $200 million-per-year drug with a complex formulation that limits competition anyway, the value is modest. Generic manufacturers building pipeline strategies use commercial modeling tools alongside patent analysis to prioritize which Paragraph IV challenges justify the litigation investment.

The exclusivity mechanism has one significant complication: it can be forfeited. A first filer loses its exclusivity if it fails to market the drug within 75 days of FDA approval or a court decision. It also faces forfeiture if it withdraws its ANDA or agrees to a settlement that the FTC determines is anticompetitive. The forfeiture provisions exist to prevent first filers from sitting on their exclusivity as a blocking mechanism rather than using it to actually compete.

Authorized Generics: The Brand’s Countermove

When a first-filer generic enters the market during its 180-day exclusivity period, the brand has one countermove that does not require FDA approval: launching its own authorized generic. An authorized generic is simply the brand drug, manufactured by the brand or a contract manufacturer using the brand’s NDA, but sold under a generic label at a lower price. The brand licenses this product to a generic company or launches it through a subsidiary.

Authorized generics are legal. They do not count against the first filer’s 180-day exclusivity because that exclusivity only blocks other ANDAs, not products sold under the brand’s NDA. And they destroy the economics of first-filer exclusivity. When a brand authorized generic enters the market alongside the first-filer generic, price competition intensifies immediately. The first filer’s premium pricing window, which is the mechanism for recouping litigation costs, collapses.

The FTC’s studies on authorized generics found that first-filer revenues dropped by an average of 40-52% when authorized generics competed during the exclusivity period [9]. Some generic firms have negotiated settlements with brands that include provisions restricting authorized generic entry, but these settlements carry antitrust risk of their own.

Part IV: The ANDA Process

Pharmaceutical Equivalence and Bioequivalence: The Technical Baseline

To receive ANDA approval, a generic must demonstrate two things. First, pharmaceutical equivalence: the product must contain the same active ingredient, in the same dosage form and route of administration, at the same strength as the reference listed drug. Second, bioequivalence: the rate and extent of absorption of the active ingredient must not differ significantly from the brand [10].

Bioequivalence studies are conducted in healthy human volunteers. The standard requires that the 90% confidence interval for the ratio of the generic’s pharmacokinetic parameters (typically area under the curve and peak plasma concentration) to the brand’s falls within 80-125% [10]. This is not a symmetric range despite appearances. Products at the edges of the interval perform differently than products near 100%, and for narrow therapeutic index drugs like warfarin or levothyroxine, the FDA applies tighter standards.

The practical result is that most generics are genuinely therapeutically equivalent to their reference products. Studies comparing brand and generic drugs find equivalent clinical outcomes in well over 95% of cases [11]. The persistent public perception that generics are inferior to brands reflects marketing, not pharmacology. Generics can look different, taste different, and have different inactive ingredients, but if they meet bioequivalence standards, they deliver the same therapeutic effect.

The ANDA Review Process and GDUFA

Before 2012, ANDA review times at the FDA were alarmingly slow. The backlog at the Office of Generic Drugs swelled to over 2,700 applications waiting more than three years for a first review. The Generic Drug User Fee Amendments (GDUFA) of 2012 changed that by establishing user fee funding in exchange for performance commitments [12].

Under GDUFA III (the current iteration, covering fiscal years 2023-2027), the FDA committed to reviewing 90% of original ANDAs within ten months of receipt [13]. That target was largely met for the first time in fiscal year 2022. Average ANDA review times for complete, first-cycle approvals now run approximately 11-13 months, down from the multi-year waits of the pre-GDUFA era.

The improvement in review times has material commercial implications. Generic manufacturers can now plan launch timelines with more precision. When a patent expires or a court invalidates a patent, the approval machinery moves quickly enough that generic entry often follows within weeks of the legal clearance date.

The review process has multiple potential outcomes: approval, tentative approval (granted when a drug is approvable but regulatory exclusivity or patents block final approval), or a Complete Response Letter (CRL) identifying deficiencies. CRLs are costly. A first CRL typically adds six to twelve months to the approval timeline. A second CRL can add years, particularly when it involves manufacturing deficiencies requiring facility remediation.

The 30-Month Stay in Practice

When a brand sues on a Paragraph IV certification within 45 days of receiving notice, the FDA automatically stays final ANDA approval for 30 months. The stay runs from the date of the brand’s first receipt of the Paragraph IV notice, not from the filing date of the lawsuit. This matters because brands sometimes receive informal notice before the formal statutory notice period starts.

Multiple patents can produce multiple stays if the brand lists additional patents after the ANDA is filed. Pre-2003 case law allowed brands to list new patents after ANDA submission and trigger fresh 30-month stays. The Medicare Modernization Act of 2003 closed this loophole by limiting the automatic stay to the first Paragraph IV certification against a patent that was listed before the ANDA was filed [14].

Brands can still list new patents after an ANDA is filed, but doing so no longer triggers an automatic stay. The generic applicant must certify against the new patent, and the brand must sue, but there is no automatic 30-month pause. The brand can still obtain a preliminary injunction from the court, but that requires a judicial finding of likelihood of success on the merits, a much higher bar than simply filing a complaint.

Part V: Patent Thickets

How Modern Patent Thickets Are Constructed

A patent thicket is a dense web of overlapping patents covering a single drug product. The strategy exploits a feature of patent law: there is no legal limit on how many patents a brand can list in the Orange Book or how many distinct aspects of a drug they can seek to protect. A brand can patent the compound, its salt form, its polymorph, its formulation, its dosing regimen, its administration device, its manufacturing process, its metabolite, and the method of using it for each indication it receives approval for.

Each additional patent creates another barrier to generic entry. A generic that designs around one patent still faces the others. A generic that challenges one patent through litigation does not clear the others. And each patent listing in the Orange Book can trigger a separate 30-month stay if the brand sues within 45 days of the Paragraph IV notice on that patent. For brands with deep litigation budgets and high-revenue drugs, running parallel litigation tracks on dozens of patents is entirely rational.

The Institute for Medicines, Access and Knowledge (I-MAK) documented this pattern comprehensively in its analysis of the top-selling U.S. drugs. The 12 drugs in its 2020 study had an average of 125 patent applications filed per drug and received an average of 38 patents each [15]. The median time of extended exclusivity beyond the original compound patent, purely from patent strategy, was six years.

Humira: The Case Study That Defines Modern Patent Strategy

AbbVie’s adalimumab, sold as Humira, is the most analyzed drug in pharmaceutical patent history, and for good reason. The drug earned more revenue than any other drug in history before biosimilar competition arrived. AbbVie protected that revenue with a patent portfolio that set a new standard for pharmaceutical IP strategy.

The original adalimumab compound patent expired in 2016. In Europe, biosimilars entered the market almost immediately. In the United States, AbbVie used a combination of patent thickets and litigation settlements to prevent biosimilar entry until 2023. The mechanism was straightforward. AbbVie accumulated patents covering formulation (the citrate-free high-concentration formulation), dosing regimen (the biweekly subcutaneous dose), manufacturing processes, and the autoinjector device. By the early 2020s, it held over 200 patents related to Humira, with expiration dates stretching to 2034 [16].

Rather than fight each of these patents in court, biosimilar manufacturers negotiated settlement agreements with AbbVie that allowed U.S. entry in January 2023 but required license fees and included restrictions on competition. When nine biosimilars did finally launch in 2023-2024, AbbVie’s rebate contracts with pharmacy benefit managers and insurers had pre-positioned Humira on preferred formulary tiers. By mid-2024, biosimilar market share in adalimumab remained below 15% despite meaningful price discounts [17].

The Humira situation illustrates a crucial point: patent expiration is necessary but not sufficient for market competition. Patent strategy, settlement agreements, pricing contracts, and formulary placement all layer on top of the patent clock to determine whether patients actually benefit from generic or biosimilar entry. <blockquote>’Pay-for-delay settlements between brand and generic drug companies cost consumers and taxpayers an estimated $3.5 billion each year.’ — Federal Trade Commission, Pay-for-Delay: How Drug Company Pay-Offs Cost Consumers and Taxpayers [18]</blockquote>

Other Major Thicket Examples

Revlimid (lenalidomide), Bristol Myers Squibb’s blood cancer drug, generated $12 billion in U.S. revenue in 2021. Its compound patent expired in 2019, but BMS had accumulated secondary patents on polymorphs and manufacturing methods extending into the 2020s [19]. Generic manufacturers filed Paragraph IV challenges, and BMS settled with each of them, granting staggered entry dates starting in 2022 with volume caps that limited generic competition to a small fraction of the market for years. By the time volume caps expired in 2026, BMS had extracted the vast majority of Revlimid’s commercial lifetime value under brand pricing.

Enbrel (etanercept), Amgen’s rheumatoid arthritis biologic, faced biosimilar competition approved by the FDA but blocked by a Sandoz settlement that kept biosimilars off the U.S. market until 2029. Amgen’s justification involved manufacturing process patents, but critics noted the settlement came with significant financial compensation flowing from Amgen to Sandoz in a structure analogous to a pay-for-delay arrangement [20].

Lantus (insulin glargine), Sanofi’s long-acting insulin, became the subject of a Congressional investigation in 2021 after its list price increased more than tenfold over 15 years while the company accumulated formulation and device patents to block biosimilar entry. The Mylan biosimilar Semglee received FDA approval and interchangeability designation in 2021, but formulary restrictions slowed adoption significantly in the first two years [21].

Part VI: Paragraph IV Litigation Strategy

How Generic Manufacturers Build a Paragraph IV Case

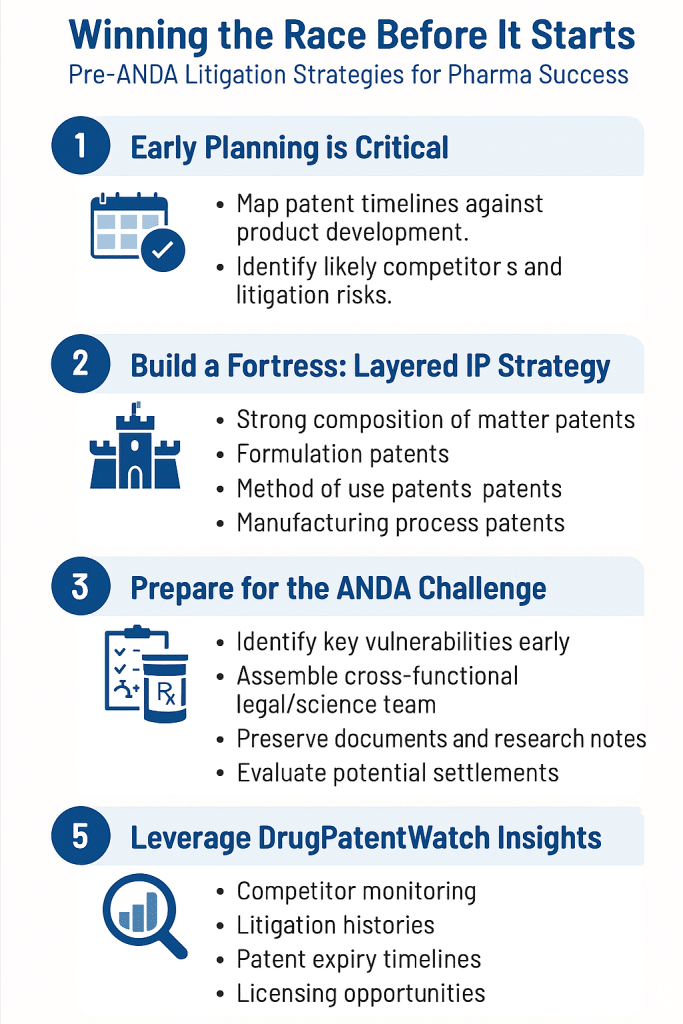

Filing a Paragraph IV certification is a strategic decision, not a reflexive one. Generic manufacturers conduct extensive pre-filing analysis to assess the likelihood of success on both validity and non-infringement grounds before committing to the litigation path. The decision involves patent counsel, scientific experts, regulatory strategists, and commercial modelers working together on a thesis that the listed patent(s) should not block their market entry.

The two primary litigation theories are invalidity and non-infringement. Invalidity challenges attack the patent’s right to exist: arguing that the claimed invention was anticipated by prior art (existed before the patent filing date), obvious to a person of ordinary skill in the art (an obviousness challenge under 35 U.S.C. § 103), or insufficiently disclosed in the patent specification. Non-infringement challenges argue that even if the patent is valid, the generic product or its method of use does not fall within the patent’s claims.

Claim construction is the critical pre-trial step in pharmaceutical patent litigation. The court interprets the meaning and scope of the patent claims, a process called ‘Markman hearing’ after the Supreme Court ruling that established judges, not juries, interpret patent claims. Generic manufacturers win or lose many cases at the Markman stage. If a claim term is construed broadly, it is more likely to cover the generic’s product. If construed narrowly, the generic may design around it or argue non-infringement.

The Economics of Patent Litigation

Patent litigation in the pharmaceutical space is expensive by any measure. A contested Paragraph IV case through trial typically costs $3-10 million per party in attorney’s fees, expert witness fees, and court costs [22]. For multi-patent cases involving five or more patents, total litigation costs can exceed $50 million for each side. These are sunk costs. The generic manufacturer pays them before selling a single unit.

The financial case for bearing these costs depends on the commercial prize. Litigation against a $10 billion-per-year drug like Humira or Revlimid can generate returns that dwarf legal costs by orders of magnitude. Litigation against a $100 million-per-year specialty drug with a complex patent situation may not generate positive expected value even if the generic wins.

This economic filtering is why generic manufacturers focus Paragraph IV challenges on the largest drugs with the most vulnerable patents. DrugPatentWatch provides the patent landscape data that enables that filtering: which patents are listed, when they expire, what types of claims they contain, and whether similar claim types have survived or been invalidated in prior litigation. A generic firm that cannot answer those questions before filing is operating blind.

Notable Paragraph IV Outcomes

Teva’s challenge to Pfizer’s atorvastatin patents (Lipitor) is the canonical success story. Teva filed the first Paragraph IV against Pfizer’s compound patent in 2001, survived years of litigation, and reached a settlement in 2008 that allowed it to enter the U.S. market six months before patent expiry [23]. When Lipitor’s exclusivity ended in November 2011, Teva had 180-day exclusivity and generated approximately $600 million in revenue during that window, among the largest single generic product launches in history.

Apotex’s challenge to Plavix (clopidogrel bisulfate) in 2006 is the cautionary tale. Bristol Myers Squibb and Sanofi sued within 45 days, triggering the 30-month stay. The parties then negotiated a settlement that the state of California and the FTC objected to on antitrust grounds. Under pressure, the brand withdrew from the settlement, Apotex launched at risk, and a court later found the patent valid. Apotex faced approximately $1.2 billion in damages [24]. The case remains the most-cited example of the financial consequences of at-risk generic launch.

Part VII: Pay-for-Delay Settlements

The Mechanics of Reverse Payment Agreements

A pay-for-delay settlement, technically called a ‘reverse payment’ settlement, is an agreement in which a brand patent holder pays a generic challenger to delay market entry. The payment can be cash, but it more often takes the form of a license allowing the generic to market an authorized generic, a co-promotion agreement, a supply deal, or a no-compete agreement in adjacent markets.

The logic from the brand’s perspective is straightforward. If the patent is weak, litigation may invalidate it, destroying the exclusivity position. Paying the generic to settle eliminates that litigation risk. The cost of the payment is always less than the value of extended exclusivity. The generic accepts because it receives certain value without the risk of losing in court and receiving nothing.

The consumer pays the price. Delayed generic entry translates directly into higher drug prices for payers, employers, and patients. The FTC estimated in 2010 that pay-for-delay settlements cost U.S. consumers $3.5 billion annually [18]. Updated academic estimates suggest the figure may be considerably higher when accounting for indirect effects on insurance premiums.

FTC v. Actavis and the Current Legal Standard

For most of the 2000s, courts applied the ‘scope of the patent’ test to pay-for-delay settlements. Under this test, a settlement was presumptively lawful as long as its terms fell within the exclusionary scope of the patent. If the patent covered the drug until 2020 and the settlement allowed generic entry in 2018, the settlement was fine because it still fell within what the patent could have excluded.

The Supreme Court rejected this framework in FTC v. Actavis (2013), holding instead that courts must apply a rule of reason analysis to reverse payment settlements [25]. The Court reasoned that a large reverse payment is a signal of patent weakness, because brand manufacturers do not pay generics large sums to stay out of the market unless they are worried about losing the patent case. Under the rule of reason, courts must weigh the anticompetitive effects of delayed generic entry against any procompetitive justifications.

Actavis did not make pay-for-delay settlements illegal. It made them more legally risky and triggered more careful scrutiny from the FTC. The number of new reverse payment settlements declined after 2013 and then rebounded as brands and generics found structuring approaches that made the ‘payment’ less visible. No-authorized-generic commitments (the brand promises not to launch an authorized generic during the first filer’s 180-day period) have become the dominant currency in these settlements, and their treatment under Actavis remains contested in lower courts.

Part VIII: Inter Partes Review

How IPR Works and Why Pharma Cares

The America Invents Act of 2011 created Inter Partes Review (IPR), a procedure allowing any third party to petition the Patent Trial and Appeal Board (PTAB) to invalidate a patent on grounds of anticipation or obviousness based on patents or printed publications [26]. IPR is faster and cheaper than district court litigation. PTAB proceedings typically conclude within 18 months of institution at a fraction of district court litigation costs.

For generic manufacturers, IPR offers an alternative or parallel challenge pathway. A generic company can file an IPR petition while simultaneously pursuing its Paragraph IV ANDA, attacking the patent at the PTAB while defending its bioequivalence data at the FDA. If the PTAB invalidates the patent before the district court case concludes, the district court proceeding usually becomes moot. PTAB has invalidated approximately 40-45% of pharmaceutical patents it has fully adjudicated since 2012 [27].

The institution rate matters as much as the outcome rate. PTAB must first decide whether to ‘institute’ (accept) the IPR petition. It institutes approximately 60% of petitions in pharmaceutical cases, meaning 40% of petitions are rejected without substantive review. A petition that is not instituted provides no relief and may create estoppel issues in district court litigation.

Pharma’s Defensive Response

Brands responded to the IPR threat with two strategies. First, some brands file their own IPR petitions against competitor patents, creating precedents for narrow claim interpretations that also benefit their own portfolio. This is known as ‘offensive IPR’ strategy, and it has become a standard tool in pharmaceutical IP management.

Second, brands challenged IPR’s constitutional validity. The Supreme Court upheld PTAB’s constitutionality in Oil States Energy Services v. Greene’s Energy Group (2018) [28]. Brands then shifted to arguing that PTAB’s decision not to institute IPRs should be unreviewable on appeal, a position the Federal Circuit has largely accepted under the NHK-Fintiv doctrine, which allows PTAB to deny institution based on parallel district court proceedings. Critics argue NHK-Fintiv has given brands a procedural escape valve, allowing them to advance district court cases rapidly to trigger IPR denials. The Federal Circuit’s en banc ruling in Apple v. Vidal (2022) addressed some of these concerns but did not fully resolve the doctrine’s scope [29].

Part IX: Regulatory Exclusivities

The Non-Patent Barriers That Brands Control Absolutely

Patent protection and regulatory exclusivity are legally distinct. A patent is a right granted by the PTO based on novelty and non-obviousness. Regulatory exclusivity is a period of protection granted by the FDA as a policy incentive, regardless of whether a patent exists. The crucial practical difference: exclusivity cannot be challenged or invalidated. You cannot file an IPR against a period of five-year new chemical entity exclusivity. You cannot bring a Paragraph IV certification against a statutory exclusivity period. You wait.

New Chemical Entity (NCE) Exclusivity: A new molecular entity approved by the FDA receives five years of exclusivity during which no ANDA referencing it can be filed [30]. This five-year period is designed to compensate brands for the cost of developing genuinely new drugs. It runs from the date of NDA approval, not patent expiry. In practice, NCE exclusivity usually runs concurrently with patent protection and is rarely the binding constraint on generic entry for major drugs, because compound patents typically outlast it.

Data Exclusivity (Three-Year Exclusivity): When a brand submits new clinical data to support a new formulation, new indication, or new route of administration, it receives three years of exclusivity covering only that specific approval [31]. A generic can file an ANDA referencing the original drug, but the new indication or formulation is protected for three years from the supplemental NDA approval. Brands use three-year exclusivity aggressively to extend protection for reformulated products.

Orphan Drug Exclusivity: A Policy Tool Being Stretched

Congress created orphan drug exclusivity in 1983 to incentivize development of drugs for rare diseases, defined as conditions affecting fewer than 200,000 Americans [32]. Drugs that receive orphan designation and FDA approval get seven years of exclusivity during which no equivalent product can be approved for the same indication. The FDA cannot approve a generic or biosimilar for that orphan-designated use for seven years.

The orphan drug program has dramatically increased rare disease drug development, which was genuinely underfunded before 1983. The problem is that the program is now being used in ways Congress did not envision. Over 40% of new drug approvals now carry orphan designations, up from approximately 15% in 2000 [33]. Many of these are not true rare diseases in the original sense. They are sub-populations of common diseases, defined narrowly enough to qualify for orphan status. Rare cancers are the most common example: a drug approved for a rare lymphoma subtype gets seven years of exclusivity, then is approved for additional cancer types under supplemental NDAs.

The economic distortions are significant. Orphan drugs have the highest average list prices in the pharmaceutical market. The seven-year exclusivity period, combined with the small patient population and lack of competitive pressure, produces pricing power that bears no relationship to development costs. Congress has introduced multiple bills to reform orphan drug exclusivity by limiting applicability to drugs with genuinely rare disease populations, but none has passed as of early 2026 [34].

Pediatric Exclusivity

Under the Best Pharmaceuticals for Children Act, the FDA grants six months of additional exclusivity to brands that conduct FDA-requested pediatric studies [35]. This six months attaches to all existing patents and exclusivities for the drug. It does not create new exclusivity; it extends existing protection.

The program has funded pediatric research that would otherwise not have been done, which is its stated purpose. It has also been used strategically on drugs where the pediatric indication is commercially negligible but the six-month exclusivity extension on a billion-dollar adult drug is extremely valuable. An antihypertensive earning $3 billion annually in the adult market gets six months of additional market protection worth roughly $1.5 billion in exchange for a pediatric study that might cost $20-50 million.

GAIN Act Exclusivity

The Generating Antibiotic Incentives Now Act of 2012 created five additional years of exclusivity for Qualified Infectious Disease Products, including antibiotics for serious or life-threatening infections [36]. The intent was to reverse the collapse in antibiotic R&D by making the economics more attractive.

The results have been disappointing. From 2012 through 2024, fewer than 20 new antibiotics received GAIN Act designations and actually launched in the U.S. market [37]. The core problem is not the exclusivity period. It is the commercial model: antibiotics work best when used sparingly, which limits sales volume, which limits revenue, which limits the return on development investment regardless of exclusivity length. GAIN Act exclusivity is valuable to the companies that use it, but it has not solved the antibiotic pipeline problem, and most policy analysts now argue that pull incentives like guaranteed purchase contracts or transferable exclusivity vouchers are needed instead.

Part X: Biosimilars

The BPCIA Pathway: Hatch-Waxman’s More Complex Sibling

The Biologics Price Competition and Innovation Act (BPCIA) of 2009 created a regulatory pathway for biosimilars that parallels Hatch-Waxman but differs in almost every material respect [38]. Biological drugs are large, complex molecules produced by living cells. They cannot be generically reproduced in the way a small-molecule drug can. A biosimilar is not identical to its reference biologic; it is highly similar with no clinically meaningful differences in safety, purity, or potency.

Because of this complexity, BPCIA requires biosimilar applicants to conduct clinical trials demonstrating biosimilarity, unlike ANDA applicants who only need bioequivalence studies. These trials are expensive: a biosimilar development program typically costs $100-300 million, compared to $1-5 million for a small-molecule generic [39]. The regulatory pathway also takes longer. From biosimilar program initiation to FDA approval typically runs eight to twelve years, compared to three to five for a generic drug.

The Patent Dance

BPCIA includes a patent dispute resolution mechanism officially called the ‘patent dance,’ a sequential information-sharing and litigation-triggering process that has become one of the most complex procedural frameworks in pharmaceutical law. The biosimilar applicant must share its application with the brand within 20 days of FDA acceptance. The brand must respond with a list of patents it believes would be infringed. The parties then exchange positions and ultimately identify which patents will be litigated [40].

The patent dance is voluntary, in the sense that biosimilar applicants can opt out of the information-sharing steps, but opting out exposes them to immediate litigation. Courts have held that a biosimilar applicant that skips the patent dance can be sued immediately by the brand for declaratory judgment, eliminating the applicant’s ability to control the litigation timeline.

Critics of the patent dance argue it serves primarily to help brands identify which manufacturing processes the biosimilar uses, information they can then use to construct infringement claims around previously unasserted patents. Biosimilar manufacturers argue they should be able to design around brand manufacturing patents without disclosing their proprietary processes in detail before litigation begins.

Interchangeability and the Automatic Substitution Question

A biosimilar can be approved as ‘biosimilar’ without being designated ‘interchangeable.’ Interchangeability requires additional evidence that the biosimilar can be substituted for the reference biologic without increased risk compared to using the reference product alone, and without involvement of the prescribing physician [41].

Interchangeability matters at the pharmacy level because state pharmacy substitution laws generally allow pharmacists to substitute interchangeable products automatically, as they do with small-molecule generics, without calling the prescribing physician. Without interchangeability, the physician must specifically prescribe the biosimilar or authorize the substitution. This is a material commercial barrier in practice because physicians tend not to actively switch stable patients from a working biologic to a biosimilar unless they or their health system has a strong incentive to do so.

Semglee (insulin glargine biosimilar from Biocon/Viatris) received the first FDA interchangeability designation in 2021 [42]. Since then, several other biosimilars have received interchangeability status. The Humira biosimilars Hyrimoz, Hadlima, and Cyltezo all received interchangeability designations in 2023-2024, but commercial uptake remained constrained by formulary position and rebate contracting.

The Rebate Trap

The persistence of brand biologics in the face of biosimilar competition cannot be explained entirely by patents, exclusivities, or interchangeability status. The rebate structure of the U.S. pharmaceutical market is equally important.

Pharmacy benefit managers (PBMs) negotiate rebates with drug manufacturers in exchange for preferred formulary placement. The brand biologic, which has been generating rebates for years and has a well-established rebate relationship with major PBMs, can offer a rebate on a base price that reflects its pricing history. The biosimilar, which has a lower list price, can offer a rebate only on its lower price. In absolute dollar terms, the brand’s rebate may be larger, even though its net price after rebate may be higher than the biosimilar’s net price.

Health plans and PBMs that optimize for rebate revenue may prefer the higher-list-price brand to the lower-price biosimilar because the gross-to-net differential is larger. This perverse incentive has been documented extensively and forms the basis for ongoing FTC investigations into PBM rebate practices [43]. The Inflation Reduction Act’s drug pricing provisions have begun to address this indirectly, but the rebate trap remains a significant barrier to biosimilar uptake as of 2026.

Part XI: PLIVA v. Mensing and Generic Drug Liability

What the Court Decided and Why It Matters

In 2011, the Supreme Court ruled in PLIVA, Inc. v. Mensing that federal law preempts state tort claims against generic drug manufacturers for failure to warn [44]. The plaintiffs argued that generic metoclopramide manufacturers should have updated their labels to warn about the risk of tardive dyskinesia, a serious neurological side effect, even before the FDA required the brand to do so. The Court held that because generic manufacturers are required by federal law to maintain labels identical to the brand’s, they could not have independently strengthened their warnings without violating federal law. State tort law cannot impose a duty that conflicts with federal law.

The practical effect was immediate and sweeping. Patients injured by generic drugs lost their primary legal remedy against generic manufacturers in most circumstances. Under Mensing and its 2013 sequel Mutual Pharmaceutical Co. v. Bartlett, generic manufacturers cannot be held liable under state tort law for design defect claims or failure-to-warn claims as long as their products match the brand’s approved labeling.

This creates a stark liability asymmetry. A patient injured by a brand drug can sue the brand under failure-to-warn theories even when the FDA has not yet required a label change, because brands have the legal authority to unilaterally update their labels through the Changes Being Effected (CBE) regulation. A patient injured by the generic version of the same drug, taking the same medication, experiencing the same injury, may have no remedy against the generic manufacturer.

Who Is Affected

The patients most exposed by the Mensing doctrine are those who take generic drugs, which is approximately 90% of prescription drug users in the United States. They are disproportionately lower-income, elderly, and uninsured or underinsured patients who are directed to generics by their insurance plans or cannot afford brand drugs. The doctrine thus concentrates the liability gap precisely in the populations least positioned to bear it.

Patricia Zlaket of CaseyGerry LLP, one of the plaintiff firms that litigated extensively in this space, summarized the practical effect: generic manufacturers enjoy market protection from competition through Hatch-Waxman while simultaneously enjoying liability protection from patient claims through Mensing. The brand bears both competitive risk and legal risk; the generic bears neither fully [45].

Legislative Proposals

Multiple bills have been introduced to restore liability parity by amending the Federal Food, Drug, and Cosmetic Act to allow generic manufacturers to update their labels unilaterally, the same right that brands have under the CBE process [46]. If generic manufacturers could update labels, the federal preemption defense that Mensing relies on would dissolve, and state tort claims could proceed normally.

Industry opponents argue this would create labeling divergence between brands and generics, confusing physicians and patients. The counterargument is that the FDA could establish a process for reviewing and harmonizing label changes, and that the current system, in which injured patients have no remedy, is worse than the proposed alternative. As of early 2026, no legislation has passed, and the Mensing doctrine remains intact.

Part XII: The Economics of Generic Entry

Price Erosion Curves

The price dynamics after generic entry follow a reasonably predictable pattern across therapeutic categories. On the first day of generic competition, prices do not collapse. The first-filer generic typically prices 10-30% below the brand and captures significant volume through pharmacy substitution, while the brand maintains close to its original price for patients with insurance that favors the brand.

As additional generics enter after the 180-day exclusivity period ends, price competition accelerates sharply. With two generics, prices fall approximately 30-50% below brand. With five or more generics, prices typically fall 70-90% below brand [47]. This erosion pattern is why generic manufacturers compete intensely for first-filer status: being first in a market with one competitor is fundamentally different from being fifth in a market with ten.

The time frame for reaching maximum price competition varies. For oral solid dosage forms (tablets and capsules), multiple generic competitors typically enter within six to twelve months of the first generic launch. For complex dosage forms like injectables, extended-release formulations, or transdermal patches, the technical barriers to manufacturing keep the generic field smaller, and price erosion is less severe. Injectables and complex generics often sustain two or three competitors for years, producing prices 30-50% below brand rather than 85-90%.

Market Concentration in the Generic Industry

The U.S. generic drug industry has consolidated substantially since 2000. The top ten generic manufacturers now control approximately 65% of generic drug sales by volume, up from 45% in 2010 [7]. The largest players include Teva, Viatris (formed from the merger of Mylan and Upjohn), Sandoz (now publicly traded separately from Novartis), Hikma, and Sun Pharmaceutical. Indian manufacturers including Dr. Reddy’s and Cipla hold significant U.S. market positions as well.

This consolidation has reduced competition in some product categories. When Teva, Mylan, and Sandoz all make the same generic product, they may have less incentive to compete aggressively on price than when there are 15 independent generic manufacturers fighting for market share. The FTC and DOJ have examined this concern repeatedly. The generic drug price-fixing scandal that produced over $1 billion in settlements with Teva, Heritage Pharmaceuticals, and other companies between 2016 and 2024 demonstrated that reduced competition creates opportunities for coordination [48].

The consolidation dynamic has also affected product availability. When a product is manufactured by only one or two firms, a manufacturing problem, recall, or regulatory action at a single facility can produce shortages. The FDA’s drug shortage database shows hundreds of drugs in shortage at any given time, with sterile injectables and older generic drugs disproportionately represented [49].

First-to-File vs. Later-Entrant Economics

The economic gap between being first and being third in a generic market is enormous. Academic research published in the Journal of Health Economics estimated that the average first-filer generic earns approximately $97 million during its 180-day exclusivity period, compared to approximately $22 million for the typical generic entrant that enters the market after exclusivity ends [50].

The gap varies by drug. For large-market drugs like statins, proton pump inhibitors, and antidepressants, first-filer value can reach hundreds of millions. For smaller drugs, it may not cover litigation costs. Generic manufacturers building rational pipelines weight their Paragraph IV challenge decisions by: (a) the size of the branded market, (b) the strength of the patent position, (c) the number of other companies likely to file first, (d) the expected litigation cost, and (e) the probability of authorized generic competition during exclusivity.

Part XIII: Using Competitive Intelligence Tools

Reading an Orange Book Entry as a Competitive Signal

An Orange Book entry is not just a regulatory disclosure. It is a competitive intelligence document. A sophisticated reader looking at an Orange Book listing for a high-revenue drug sees not just patent expiration dates but the brand’s strategic intentions.

A drug with a compound patent expiring in 2026, a formulation patent expiring in 2029, and a device patent expiring in 2032 is telling you something specific: the brand is planning a lifecycle extension strategy built on a reformulated product and a proprietary delivery device. The generic opportunity at 2026 exists, but it is contested. The opportunity at 2032 is uncertain because it depends on whether the device patents hold. A manufacturer entering now should plan for the 2026 entry on the original formulation while watching the 2029 formulation patent closely.

A drug with only a compound patent expiring in 2025 and no other listed patents tells a different story: this is a clean entry opportunity with limited secondary patent risk. Generic manufacturers racing to that drug face competition from other early filers but face lower litigation complexity than drugs with layered patent portfolios.

DrugPatentWatch as a Competitive Intelligence Layer

DrugPatentWatch aggregates Orange Book data, ANDA filing records, PTAB proceedings, district court case data, and patent expiration timelines into a structured, searchable platform that enables the kind of analysis described above at scale. For a business development team evaluating 50 potential generic targets simultaneously, manually tracking each drug’s Orange Book listings, active litigation, Paragraph IV challenges, and first-filer status in real time is operationally impossible.

The platform’s value is in answering specific commercial questions quickly: Which drugs in therapeutic area X have compound patents expiring in the next three years with no formulation patents behind them? Which of those drugs have existing Paragraph IV challenges filed, and by whom? Which are already in district court litigation, and what stage are those cases at?

These questions translate directly into pipeline prioritization decisions. A company that can identify a drug with expiring patent protection, no active first-filer challenge, and favorable manufacturing characteristics has found a market entry opportunity that its competitors may have missed. Getting to that insight three months before a competitor files is worth millions.

Mapping Patent Cliffs with Data

‘Patent cliff’ is the term used to describe the period when a major drug’s patent protection expires and generic competition begins. From a brand perspective, the cliff represents catastrophic revenue loss. From a generic perspective, it is a launch opportunity. From an investor perspective, it is either a buying opportunity (for generic manufacturers positioned to capitalize) or a selling signal (for brand manufacturer shareholders who understand the revenue implications).

Patent cliff mapping has become a standard analytical exercise for pharmaceutical sector investors and business development teams. The exercise involves identifying drugs with significant patent expirations in a defined forward window, assessing the complexity of their patent situations (compound-only patents are cleaner than patent thickets), estimating the timing and extent of generic price erosion, and modeling the commercial opportunity for generic entrants.

Several major drugs face significant patent expirations in the 2025-2028 window. Eliquis (apixaban), Bristol Myers Squibb and Pfizer’s blood thinner, has base patent protection expiring in 2026-2028 depending on jurisdiction, with secondary patents that will be contested [51]. Keytruda (pembrolizumab), Merck’s blockbuster cancer immunotherapy, faces patent expirations beginning in 2028 that will trigger one of the largest biosimilar development races in pharmaceutical history [52]. Ozempic and Wegovy (semaglutide), Novo Nordisk’s GLP-1 receptor agonists, have compound patents with various expiration dates and a complex secondary patent landscape that will produce years of litigation before generic entry is commercially available [53].

Part XIV: Policy Reforms on the Horizon

Orange Book Reform

The FTC issued a policy statement in 2023 asserting that Orange Book listings for device patents (covering autoinjectors, inhalers, and similar delivery mechanisms rather than the drug itself) violate FDA regulations [54]. The FTC then sent formal challenge letters to dozens of brand manufacturers demanding withdrawal of these listings, citing products like AstraZeneca’s Symbicort and Teva’s ProAir as examples.

The legal status of these challenges remains unsettled. FDA regulations require that only patents that claim the approved drug or its approved method of use may be listed. The FTC argues that a patent covering an inhaler device does not claim the approved drug. Brand manufacturers argue that because the device is integral to drug delivery, patents on the device are covered by the listing requirement.

Congressional proposals would clarify the statute by explicitly limiting Orange Book listings to compound and formulation patents, excluding manufacturing process patents and device patents. Such a change would materially reduce the number of triggerable 30-month stays and limit brands’ ability to stack litigation delays through device patent listings.

The CREATES Act and REMS Abuse

The CREATES Act (Creating and Restoring Equal Access to Equivalent Samples), passed in 2019, addressed a specific abuse: brand manufacturers withholding drug samples from generic manufacturers who need them to conduct bioequivalence studies [55]. Without access to the brand product, a generic cannot run the comparative absorption studies required for ANDA approval.

Brands used Risk Evaluation and Mitigation Strategy (REMS) programs, which are FDA-mandated safety protocols for dangerous drugs, to refuse sample sales to generic manufacturers, arguing that REMS safety protocols prevented sample distribution. The CREATES Act gave generic manufacturers a private right of action to sue brands that withhold samples without good cause, and established that brand companies must provide samples on commercially reasonable market terms.

The act has had a measurable effect. Several cases settled promptly after passage when generic manufacturers threatened CREATES Act litigation, and samples that had been withheld for years became available. But REMS abuse continues in more subtle forms, including brands designing REMS programs specifically to create distribution barriers [56].

Drug Pricing Reform and Antitrust Enforcement

The Inflation Reduction Act of 2022 authorized the government to negotiate prices for certain high-cost Medicare drugs and capped Medicare drug price increases at the rate of inflation [57]. The first round of IRA price negotiations covered ten drugs, including Eliquis, Jardiance, Xarelto, and seven others, with negotiated prices taking effect in 2026. The second round covered fifteen additional drugs.

The IRA provisions interact with patent strategy in complex ways. When the government negotiates a lower price for a patented drug, it reduces the commercial incentive for that drug’s brand to file continuation patent applications extending protection. If the government price is already at a discount, adding six months of pediatric exclusivity or a new formulation patent adds less marginal value. Whether this dynamic will reduce secondary patent filings over time is an empirical question that will take years to answer.

FTC antitrust enforcement has intensified in the pharmaceutical sector, targeting both pay-for-delay settlements and market allocation agreements among generic manufacturers. The DOJ’s ongoing prosecution of generic executives and companies for per se antitrust violations in the generic drug price-fixing case represents the most aggressive criminal antitrust action in the pharmaceutical sector in decades [48].

The current administration has maintained the Biden administration’s antitrust posture toward pharmaceuticals, continuing FTC and DOJ enforcement actions while adding new scrutiny to PBM rebate practices. Whether Congress will pass any structural reform remains uncertain. Pharmaceutical lobbying remains among the most intensive in Washington, and the industry’s campaign contributions span both parties.

Part XV: Building a Generic Drug Intelligence System

The Data Inputs That Matter

A generic manufacturer, investor, or payer navigating this landscape needs to track multiple data streams simultaneously. Patent data from the Orange Book and PTO tells you what IP barriers exist. ANDA filing data from the FDA’s generic drug database tells you who else is planning to enter. PTAB proceeding data tells you whether existing patents are under challenge. District court docket data tells you whether active litigation is delaying approval. Commercial data tells you how large the market opportunity is and what price erosion looks like in comparable therapeutic categories.

None of these data streams is comprehensive on its own. The Orange Book lists patents but not their claim scope or likelihood of survival in litigation. ANDA filing data shows who has filed but not their development stage or manufacturing readiness. PTAB data shows petitions filed but not their probability of institution. Integrating these streams into a coherent view of a drug’s competitive landscape requires either significant internal analytical resources or access to a platform that has already done the integration work.

The Timeline Management Problem

Generic drug development timelines are long and uncertain. From the decision to develop a generic product to commercial launch typically runs three to seven years. Within that window, patent expiration dates, litigation outcomes, and competitor actions can all shift the commercial landscape materially. A drug that looked like a clean entry opportunity when you began development may face unexpected secondary patents, a new competitor who filed first, or a brand that launched an authorized generic.

Timeline management requires monitoring the landscape continuously rather than conducting an entry assessment once and moving on. A competitive filing that enters the patent landscape eighteen months into your development program changes your economics entirely. An IPR decision that invalidates a key patent three years into your program eliminates a litigation risk and may accelerate your timeline. These events require real-time data, not annual reviews.

Making Decisions Under Uncertainty

The fundamental intellectual challenge in generic pharmaceutical strategy is making decisions years in advance with incomplete information. You cannot know whether a patent will be invalidated before you commit to a development program. You cannot know whether a competitor will file first. You cannot know whether the FDA will issue a Complete Response Letter that delays your approval by eighteen months. You can only estimate probabilities and make expected-value calculations.

The expected-value framework is the right tool here, but it requires honest inputs. Optimistic litigation probability assessments and inflated revenue projections compound each other to produce business cases that cannot survive contact with reality. The most disciplined generic pharmaceutical organizations combine rigorous patent risk assessment (which requires honest analysis of prior art and claim scope) with conservative commercial modeling (which requires realistic price erosion assumptions) and explicit timeline risk assessment (which requires honest mapping of regulatory and manufacturing risks).

Key Takeaways

Patents and exclusivities are different weapons. Patents can be challenged, invalidated, and designed around. Regulatory exclusivities like NCE, orphan, and pediatric exclusivity cannot. A generic manufacturer whose market entry strategy depends on patent expiration alone may still be blocked by an exclusivity period that runs years past that date.

The Orange Book is a strategic document. Brands list patents aggressively to multiply 30-month stays. The FTC and FDA are actively contesting device and manufacturing process listings, but the landscape has not yet fully changed. Reading Orange Book entries skeptically, and tracking which listings are being contested, is a core competitive intelligence discipline.

180-day exclusivity is valuable but fragile. Authorized generic competition can halve first-filer revenue during the exclusivity window. Pay-for-delay settlements can extend brand exclusivity at consumer expense. The FTC’s Actavis standard has added legal risk to reverse payment settlements but has not eliminated them.

Biosimilars operate under different rules. The BPCIA pathway is more expensive, more complex, and slower than Hatch-Waxman. Patent thickets, interchangeability requirements, and rebate structures create barriers that persist long after FDA approval. Investors and manufacturers treating biosimilars as simple analogs to small-molecule generics misunderstand the competitive dynamics.

The PLIVA v. Mensing liability gap is unresolved. Generic manufacturers that account for 90% of prescriptions face essentially no state tort liability for labeling defects. This asymmetry creates a consumer protection problem that Congress has not addressed. Any significant legislative movement on this issue would materially affect generic manufacturer risk profiles.

Data quality determines competitive positioning. The difference between a generic manufacturer that finds patent cliff opportunities before competitors and one that finds them at the same time as competitors is an intelligence advantage. Platforms like DrugPatentWatch that integrate patent, regulatory, and litigation data are not a luxury for generic pharmaceutical companies; they are a structural requirement for operating profitably in this market.

FAQ

Q1: How does a brand manufacturer decide which patents to list in the Orange Book, and what happens if it lists one that does not qualify?

The brand is legally required to list any patent that claims the approved drug or its approved method of use and that would be infringed by an ANDA applicant. In practice, brands have interpreted this requirement broadly and listed patents covering delivery devices, metabolites, and manufacturing processes that the FDA argues do not qualify. If the FDA determines a patent should not have been listed, it can demand withdrawal. The FTC has sent formal challenge letters to brands over improper listings since 2023 [54]. A generic manufacturer can also petition the FDA to remove an improper listing, and several such petitions have succeeded. The consequence for the brand of an improper listing is primarily loss of the triggered 30-month stay, not a financial penalty, which means the deterrence has historically been limited.

Q2: What is the difference between a product patent, a use patent, and a formulation patent from a litigation strategy perspective?

A product (compound) patent is the hardest to design around because the generic must contain the same API as the brand. Invalidity arguments (prior art, obviousness) are the primary challenge path. A use patent is more amenable to non-infringement arguments: the generic manufacturer can seek FDA approval only for the non-patented uses and rely on label carve-outs, removing the patented indication from the generic label. The risk is that physicians prescribe the generic for the patented use anyway (so-called ‘skinny labeling’ risk, which the Federal Circuit examined in GlaxoSmithKline v. Teva [58]). A formulation patent is typically challenged on both invalidity and non-infringement grounds; generics often design formulations that achieve bioequivalence while avoiding the specific excipient combinations or release mechanisms claimed in the formulation patent.

Q3: When does it make sense to pursue an IPR petition against a pharma patent rather than litigating in district court?

IPR makes sense when the primary invalidity theory rests on prior art (patents or printed publications) rather than experimental evidence, since PTAB only considers those two categories of prior art. It also makes sense when the patent faces weak prior art that district court review would catch anyway but that PTAB can address faster and more cheaply. IPR is less useful when non-infringement is the primary argument, since PTAB does not adjudicate infringement. The procedural risk is estoppel: a party that files an IPR and loses at PTAB may be estopped from raising the same invalidity arguments in district court. Generic manufacturers frequently run parallel tracks (district court litigation and IPR), which allows them to maintain maximum optionality while pursuing the fastest path to patent invalidation.

Q4: How do payers and PBMs use patent and exclusivity data in formulary decision-making?

Sophisticated payers and PBMs track patent expiration dates actively to plan formulary transitions. When a major drug is expected to face generic competition, the payer may negotiate deeper rebates from the brand in exchange for maintaining formulary position for one or two more years, then plan a formulary switch to the generic when it launches. This pre-expiration negotiating leverage is real but requires accurate patent expiration data. Payers that rely on generic entry dates provided by the brand itself may get strategically optimistic forecasts. Independent patent analysis, using resources like DrugPatentWatch to verify which patents are actually blocking entry and on what timeline, gives payers the negotiating leverage that comes from knowing the brand’s position as well as the brand does.

Q5: What effect does the Inflation Reduction Act’s price negotiation authority have on pharmaceutical patent strategy going forward?

The IRA’s impact on patent strategy is still developing, but several effects are visible. First, for drugs subject to IRA price negotiation, the government negotiated price is set at a discount to market regardless of remaining patent term. This reduces the marginal value of patent extensions beyond the negotiation trigger date, since you cannot charge the negotiated price plus the value of an additional five years of exclusivity; you can only charge the negotiated price. Second, the IRA’s inflation rebate penalties (which require brands to pay rebates when drug prices increase faster than inflation) create an incentive to launch new products at higher initial prices, which may accelerate the already-present trend of high-launch-price specialty drugs. Third, the IRA’s small molecule vs. biologic disparity, which gives small molecules nine years before negotiation eligibility and biologics thirteen years, has already affected R&D investment allocation decisions, with some companies explicitly shifting pipeline investment toward biologics to maximize the IRA exclusivity window [59].

References

[1] Association for Accessible Medicines. (2025). The U.S. Generic & Biosimilar Medicines Savings Report. Washington, DC: AAM.

[2] 35 U.S.C. § 154(a)(2). Patent Term.

[3] DiMasi, J. A., Grabowski, H. G., & Hansen, R. W. (2016). Innovation in the pharmaceutical industry: New estimates of R&D costs. Journal of Health Economics, 47, 20-33. https://doi.org/10.1016/j.jhealeco.2016.01.012

[4] 35 U.S.C. § 156. Extension of Patent Term.

[5] U.S. Food and Drug Administration. (2020). Listed Drugs, 30-Month Stays, and Approval of ANDAs and 505(b)(2) Applications Under Hatch-Waxman, as Amended by the Medicare Prescription Drug, Improvement, and Modernization Act of 2003: Questions and Answers. FDA Guidance Document.

[6] 21 U.S.C. § 355(j)(5)(B)(iii). Abbreviated New Drug Applications.

[9] Federal Trade Commission. (2011). Authorized Generic Drugs: Short-Term Effects and Long-Term Impact. Washington, DC: FTC.

[10] U.S. Food and Drug Administration. (2024). Bioequivalence Studies With Pharmacokinetic Endpoints for Drugs Submitted Under an ANDA: Guidance for Industry. FDA Guidance Document.

[11] Kesselheim, A. S., Misono, A. S., Lee, J. L., Stedman, M. R., Brookhart, M. A., Choudhry, N. K., & Shrank, W. H. (2008). Clinical equivalence of generic and brand-name drugs used in cardiovascular disease. JAMA, 300(21), 2514-2526. https://doi.org/10.1001/jama.2008.758

[12] Generic Drug User Fee Amendments of 2012, Pub. L. No. 112-144, Title III, 126 Stat. 1099.

[13] U.S. Food and Drug Administration. (2023). GDUFA III Performance Goals and Program Enhancement Commitments. Silver Spring, MD: FDA.

[14] Medicare Prescription Drug, Improvement, and Modernization Act of 2003, Pub. L. No. 108-173, § 1101, 117 Stat. 2066.

[15] Initiative for Medicines, Access & Knowledge (I-MAK). (2020). Overpatented, Overpriced: How Excessive Pharmaceutical Patenting Is Extending Monopolies and Driving Up Drug Prices. New York: I-MAK.

[16] Feldman, R. (2018). May your drug price be ever green. Journal of Law and the Biosciences, 5(3), 590-647. https://doi.org/10.1093/jlb/lsy022

[17] IQVIA Institute for Human Data Science. (2024). The Use of Medicines in the U.S. 2024. Parsippany, NJ: IQVIA.

[18] Federal Trade Commission. (2010). Pay-for-Delay: How Drug Company Pay-Offs Cost Consumers and Taxpayers. Washington, DC: FTC.

[19] I-MAK. (2021). Revlimid Patent Analysis. New York: I-MAK.

[20] Sarpatwari, A., Avorn, J., & Kesselheim, A. S. (2015). Using a drug-specific regulatory exclusivity period to understand pharmaceutical patenting. Drug Safety, 38(9), 797-807.

[21] U.S. Food and Drug Administration. (2021). FDA Approves First Interchangeable Biosimilar Insulin Product [Press release]. Silver Spring, MD: FDA.

[22] American Intellectual Property Law Association. (2023). Report of the Economic Survey 2023. Arlington, VA: AIPLA.

[23] Rosen, J. (2012). The Lipitor litigation: A chronological case study. Journal of Generic Medicines, 9(1), 3-12.

[24] In re Plavix Litigation. (2007). Bristol-Myers Squibb Co. v. Apotex Inc., Case No. 04-cv-945 (D.N.J.).

[25] FTC v. Actavis, Inc., 570 U.S. 136 (2013).

[26] Leahy-Smith America Invents Act, Pub. L. No. 112-29, § 6, 125 Stat. 284 (2011).

[27] Sterne, R. E., & Nearhood, J. C. (2023). Patent Trial and Appeal Board statistics. IPWatchdog Annual Patent Report 2023.

[28] Oil States Energy Services, LLC v. Greene’s Energy Group, LLC, 584 U.S. 325 (2018).

[29] Apple Inc. v. Vidal, 63 F.4th 1 (Fed. Cir. 2023).

[30] 21 U.S.C. § 355(c)(3)(E)(ii). New Chemical Entity Exclusivity.

[32] Orphan Drug Act, Pub. L. No. 97-414, 96 Stat. 2049 (1983).

[33] U.S. Food and Drug Administration. (2024). Novel Drug Approvals for 2023. Silver Spring, MD: FDA.

[34] Congressional Research Service. (2024). Orphan Drug Act: Background and Issues (Report No. R45671). Washington, DC: CRS.

[35] Best Pharmaceuticals for Children Act, Pub. L. No. 107-109, 115 Stat. 1408 (2002).

[36] Generating Antibiotic Incentives Now Act, Pub. L. No. 112-144, § 801, 126 Stat. 1099 (2012).

[37] Pew Charitable Trusts. (2024). Tracking the Global Pipeline of Antibiotics in Development. Philadelphia: Pew.

[38] Biologics Price Competition and Innovation Act of 2009, Pub. L. No. 111-148, § 7001, 124 Stat. 804.

[39] Mulcahy, A. W., Hlavka, J. P., & Case, S. R. (2018). Biosimilar cost savings in the United States: Initial experience and future potential. RAND Health Quarterly, 7(4), 3.

[41] U.S. Food and Drug Administration. (2019). Considerations in Demonstrating Interchangeability With a Reference Product: Guidance for Industry. FDA Guidance Document.

[42] U.S. Food and Drug Administration. (2021). Semglee Product Information. Silver Spring, MD: FDA.

[43] Federal Trade Commission. (2024). Pharmacy Benefit Managers: The Powerful Middlemen Inflating Drug Costs and Squeezing Main Street Pharmacies. Washington, DC: FTC.

[44] PLIVA, Inc. v. Mensing, 564 U.S. 604 (2011).

[45] CaseyGerry LLP. (2025). Generic drugs and the new normal in pharma litigation. San Diego: CaseyGerry.

[46] Patient Access to Drugs Act of 2021, S. 3097, 117th Cong. (2021).

[47] Reiffen, D., & Ward, M. R. (2005). Generic drug industry dynamics. Review of Economics and Statistics, 87(1), 37-49.

[48] U.S. Department of Justice. (2024). Generic Drug Price-Fixing Investigation Update [Press release]. Washington, DC: DOJ.

[49] U.S. Food and Drug Administration. (2024). Drug Shortages: Root Causes and Potential Solutions. Silver Spring, MD: FDA.

[50] Berndt, E. R., Mortimer, R., Bhattacharjya, A., Parece, A., & Tuttle, E. (2007). Authorized generic drugs, price competition, and consumers’ welfare. Health Affairs, 26(3), 790-799.

[53] Novo Nordisk A/S. (2024). Semaglutide Patent Portfolio Disclosure. Bagsvaerd: Novo Nordisk.

[54] Federal Trade Commission. (2023). FTC Challenges Improper Orange Book Patent Listings [Press release]. Washington, DC: FTC.

[55] CREATES Act of 2019, Pub. L. No. 116-94, § 610, 133 Stat. 2534.

[56] Sarpatwari, A., Barber, M. J., & Kesselheim, A. S. (2020). The CREATES Act and barriers to generic drug access. New England Journal of Medicine, 382(21), 1967-1969.

[57] Inflation Reduction Act of 2022, Pub. L. No. 117-169, 136 Stat. 1818.

[58] GlaxoSmithKline LLC v. Teva Pharmaceuticals USA, Inc., 7 F.4th 1320 (Fed. Cir. 2021).

[59] Congressional Budget Office. (2023). Effects of Drug Price Negotiation Stemming from the Inflation Reduction Act on Pharmaceutical Revenues and Research and Development (Report No. 59580). Washington, DC: CBO.

")