Every brand team runs the same model. The compound patent expires on a known date. You build a 24-month revenue bridge, pencil in an authorized generic, brief the board, and hand the asset to the lifecycle management group. Then, eighteen months before the cliff, the litigation stay gets extended. The IRA selects your drug for price negotiation at year seven. A secondary patent triggers another 30-month automatic stay. Your authorized generic runs into an FDA manufacturing hold. The PBM drops you from formulary six months early. Three years after your supposed LOE date, you’re still in court, but you’re also generating 40 percent less revenue than your model predicted.

That gap between model and reality is what this article is about.

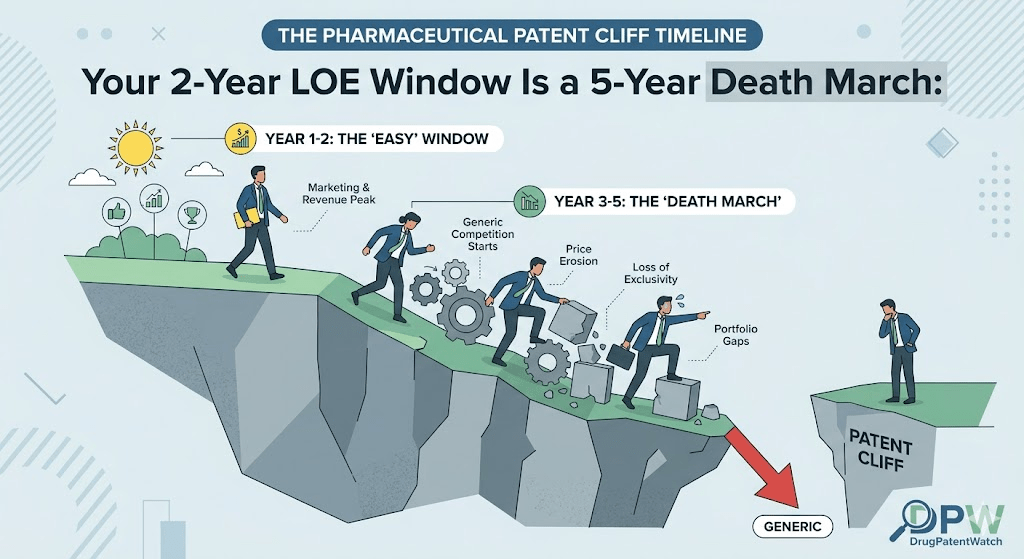

The standard pharmaceutical loss-of-exclusivity framework treats LOE as a discrete event with a predictable revenue half-life. It isn’t. It’s a five-year process that begins, at minimum, 36 months before the primary patent expiration date and ends only when the last secondary patent is litigated away, the last biosimilar achieves interchangeability status, and the last PBM formulary cycle completes. For drugs caught inside the Inflation Reduction Act’s negotiation perimeter, that timeline extends further.

Between 2025 and 2030, the global pharmaceutical industry faces a Loss of Exclusivity wave that puts an estimated $200 billion to $400 billion in branded drug revenue at direct risk. That range reflects genuine uncertainty about litigation outcomes, biosimilar entry timelines, and IRA price negotiation schedules. The uncertainty itself is part of the problem. Companies that plan for the low end of that range and live through the high end don’t survive intact.

What follows is a granular, stage-by-stage analysis of exactly how that death march unfolds — the legal mechanics, the commercial triggers, the regulatory timelines, and the financial structure of the erosion that brand teams routinely underestimate.

What Loss of Exclusivity Actually Means: A Precise Definition

Loss of exclusivity is not synonymous with patent expiration. The two terms are often used interchangeably in earnings calls and investor presentations, and that imprecision costs money.

Patent expiration refers specifically to the end of a granted patent’s 20-year term, measured from the earliest filing date, subject to patent term extensions under the Hatch-Waxman Act (35 U.S.C. § 156) and any applicable pediatric exclusivity extensions. A drug typically has multiple active patents at any given point — compound patents, formulation patents, method-of-use patents, polymorph patents, and, for drug-device combinations, device-mechanism patents. Each of these has a separate expiration date. Referring to “the patent expiration” for a blockbuster biologic that lists 80 patents in the Orange Book tells you almost nothing about when generic or biosimilar competition will actually arrive.

Loss of exclusivity, in the commercially meaningful sense, is the date on which a generic or biosimilar product enters the market and begins competing for prescription volume. That date depends on the compound patent expiration, minus or plus:

Active patent term extensions (PTEs) under Hatch-Waxman, which can add up to five years of patent term to compensate for regulatory review time

Pediatric exclusivity grants, which add six months to the expiration date of any patent or regulatory exclusivity period

The 30-month automatic litigation stay triggered by a Paragraph IV ANDA certification, which delays FDA approval of the generic application while litigation proceeds

The 180-day marketing exclusivity period granted to the first Paragraph IV filer

Regulatory exclusivity periods independent of patents, including five-year NCE exclusivity, three-year clinical investigation exclusivity, and seven-year orphan drug exclusivity

For biologics, the 12-year biologics exclusivity period is meaningfully longer than the five-year new chemical entity exclusivity for small molecules. A biologic approved in 2015 cannot have a biosimilar approved on the basis of reference product data until 2027, even if every patent on the product expires in 2024. A patent-free biologic from 2024 to 2027 is not generic-equivalent — it’s simply three years of reduced-competition branded marketing before biosimilar entry becomes legally possible.

This distinction matters operationally. A brand’s revenue model must account for all of these layers simultaneously, not sequentially.

The Five-Year LOE Arc: Stage-by-Stage Breakdown

The actual LOE timeline for a blockbuster drug runs roughly as follows. The specific dates shift by product, but the structural sequence is consistent enough to treat as a template.

Stage 1: The IRA Trigger Window (Years Minus 7 to Minus 5 Before LOE)

Before you reach the patent cliff, the Inflation Reduction Act may cut your revenue first.

To be eligible for IRA negotiation, drugs must be among the top of the list in terms of Medicare expenditure, lack any generic or biosimilar equivalents, and have already been on the market for a set number of years — seven for small molecules and eleven for biologics. The negotiated Maximum Fair Price takes effect two years after selection.

The Inflation Reduction Act introduces a regulatory mechanism that allows the Centers for Medicare and Medicaid Services to set prices for top-selling drugs that lack generic or biosimilar competition. This shift effectively moves the revenue cliff forward, often by several years, fundamentally altering the return on investment for research and development.

For the first ten drugs selected in the IRA’s inaugural negotiation round, the negotiated prices represented discounts between 38 percent and 79 percent from the list price. Novo Nordisk’s Ozempic is projected to drop from a list price of $959 to a Medicare price of $274 per month.

The IRA creates a pre-LOE revenue hit that most brand models built before 2022 never accounted for. Merck, whose pembrolizumab (Keytruda) faces this exposure, was explicit about the sequence. In its 2024 annual report, Merck expected U.S. sales to begin declining in January 2028 with government pricing under the Inflation Reduction Act, then to ‘further decline’ after loss of exclusivity tied to the expiration of the U.S. compound patent in December 2028. Two separate revenue cliff events, 12 months apart, both driven by policy mechanisms that did not exist when Keytruda was approved.

The IRA “pill penalty” creates an additional structural perversity. Small molecule drugs are eligible for selection to the Medicare Drug Price Negotiation Program seven years after Food and Drug Administration approval, and the price control goes into effect at year nine. Biologics face the same mechanism at years eleven and thirteen, respectively. The disparity — shorter windows for small molecules — has begun to reshape early-stage pipeline decisions at several major companies. Novartis, AstraZeneca, and others have publicly acknowledged shifts away from certain small-molecule development programs as a direct result.

Stage 2: The Paragraph IV Filing Surge (Years Minus 4 to Minus 3)

Between three and four years before a drug’s primary compound patent expiration, the Paragraph IV filings begin. This is when the five-year death march officially starts on the litigation calendar.

Under the Hatch-Waxman framework, a generic manufacturer that files an ANDA with a Paragraph IV certification is asserting that the listed Orange Book patents are invalid or will not be infringed by the generic product. Filing an Abbreviated New Drug Application with a Paragraph IV certification is the legal equivalent of suing the patent holder before a single tablet is manufactured. The 180-day marketing exclusivity granted to the first successful Paragraph IV filer can be worth hundreds of millions of dollars and transforms generic development into an information race as much as a scientific one.

Once the brand manufacturer receives notice of a Paragraph IV filing and initiates patent infringement litigation within 45 days, an automatic 30-month stay kicks in. The FDA cannot approve the ANDA for 30 months from the date of notice, even if the generic application is otherwise approvable. This 30-month stay is the single most powerful revenue-protection tool available to brand manufacturers and is routinely used as a matter of course regardless of the underlying patent strength.

The litigation stay alone buys 2.5 years. When the primary compound patent expires, it is not unusual to find that 3 to 6 additional formulation or method-of-use patents still carry active 30-month stays, each requiring its own litigation to resolve. The cumulative effect on the actual competitive entry date can be substantial — measured in years, not months.

Stage 3: The Patent Thicket and Secondary Patent Defense (Years Minus 3 to LOE Date)

A drug protected by a primary compound patent with an approaching expiration date typically has layers of secondary patents filed well after initial approval. For the 12 best-selling drugs in the U.S., innovator companies have sought an average of 38 years of patent protection — nearly twice the statutory 20-year term. For drugs that undergo evergreening, the average delay in the arrival of meaningful generic competition can be several years, each year representing billions in lost sales opportunities for generics and billions in excess costs for the healthcare system.

AbbVie’s construction of the Humira patent fortress is the most studied example. A full 89 percent of Humira’s secondary patents were filed after the drug was already approved and on the market, with nearly half filed more than a decade after its launch. These were not patents on the core invention; they were secondary patents covering everything from manufacturing processes and formulations to specific methods of use for various autoimmune conditions. The result was that biosimilar makers largely settled with AbbVie, agreeing to delayed U.S. market entry in 2023 with ongoing royalty payments, while some gained earlier access to European markets starting in 2018.

The FTC has begun dismantling the most aggressive version of this strategy. In 2024 and 2025, the FTC launched a coordinated enforcement campaign against improper Orange Book listings. The Commission sent warning letters to major pharmaceutical companies, including Teva, GSK, and AstraZeneca, challenging over 300 patent listings it deemed improper.

In a June 2024 ruling, five device patents were removed from Teva’s Orange Book entry after Amneal and the FTC challenged them. The judge noted that listing device patents was improper, emphasizing that generics should not be blocked by peripheral claims. Teva appealed, and in December 2024, the Federal Circuit affirmed the district court’s decision, ruling that the Listing Statute requires a patent to both claim the drug and cover the NDA product itself — and Teva’s patents did not claim the active ingredient, only components of the inhaler.

In December 2025, following sustained pressure from the FTC, Teva Pharmaceuticals requested the removal of more than 200 patent listings from the Orange Book. These patents covered asthma, diabetes, and COPD treatments. Each of those listings had been capable of triggering a 30-month stay. Each removal means competitive entry is now earlier than it would have been.

Stage 4: The Serial Litigation Strategy (LOE Date Through Year Plus 2)

Even after the primary compound patent expires and the initial round of Hatch-Waxman litigation concludes, brand manufacturers can extend the competitive delay through serial litigation — filing new infringement suits on patents obtained after the original settlement.

In the case of Astellas’s overactive bladder drug mirabegron (Myrbetriq), after an initial Hatch-Waxman case settled in 2020 with generic entry expected in 2024, Astellas pursued four additional lawsuits, each built on new but substantively indistinguishable patents. These tactics delayed broad competition, leaving only two firms to launch in 2024 under the threat of massive damages.

The pattern is not limited to Myrbetriq. Similar serial litigation has been documented for bimatoprost (Latisse), aflibercept (Eylea), and tasimelteon (Hetlioz). The mechanism works because Hatch-Waxman does not prohibit subsequent litigation on subsequently granted patents. A brand company that files a new patent application during an ongoing ANDA suit, obtains grant six months later, and then sends a second Paragraph IV notice letter can restart the litigation clock on the same generic product.

For brand revenue models, serial litigation is a wild card. It can extend effective exclusivity by 18 to 36 months beyond the nominal LOE date. For generic manufacturers, it creates a discounting problem: the NPV of a generic opportunity shrinks materially if the expected launch date shifts three years to the right under litigation pressure.

Stage 5: The Post-LOE Formulary and PBM Erosion Phase (LOE Date Through Year Plus 3)

The compound patent expires. The litigation settles or expires. The first generic launches. The death march enters its final phase, which is also the one most underestimated in brand revenue models: the PBM formulary cycle.

Erosion occurred in steps coinciding with PBM formulary contracting cycles, typically January 1st and July 1st. By 2025, biosimilars had captured approximately 20 to 30 percent of the volume — a far cry from the 90 percent seen in small molecules. This indicates that biologic LOE models must account for a two- to three-year ramp to peak erosion, rather than the six-month crash of small molecules.

For small molecules, the formulary cycle is less forgiving. Small molecule erosion is driven by automatic substitution laws at the state level. Once a generic is rated ‘AB’ (therapeutically equivalent) in the Orange Book, pharmacists must substitute it for the brand unless the prescriber explicitly writes ‘Dispense as Written.’ PBMs reinforce this by placing the brand on a non-preferred tier or excluding it entirely, creating a hard stop for patient access.

The average brand-name drug loses between 80 percent and 90 percent of its volume to generics within six months of LOE, with price erosion in that window averaging 80 to 85 percent below the pre-generic brand price. For drugs with annual revenues above $1 billion, the projected revenue loss over 24 months post-LOE often exceeds the combined R&D spend on the next two pipeline candidates.

The Lipitor case remains the definitive data point. Multiple generic manufacturers entered simultaneously in November 2011. Market pricing collapsed from approximately $5 per tablet for branded Lipitor to under $0.10 per tablet for generic atorvastatin within 18 months. By the end of 2012, generic atorvastatin had captured approximately 80 percent of total atorvastatin prescriptions. Pfizer’s revenues fell from over $9 billion in 2010 to under $2 billion by 2013.

Why the Standard 2-Year LOE Model Is Structurally Wrong

The two-year LOE model emerged from a simpler era of pharmaceutical finance. In that era, a drug with a single compound patent, minimal secondary coverage, and a straightforward ANDA filing process could reasonably be modeled with a pre-LOE revenue maximization phase and a post-LOE 24-month erosion curve. That drug still exists, but it is no longer the dominant case among blockbusters.

The modern blockbuster has four structural characteristics that break the two-year model:

Characteristic 1: Multiple Revenue Compression Mechanisms Now Operate Simultaneously

In the pre-IRA world, a brand faced one primary revenue threat: patent expiration followed by generic entry. Today, it faces three: patent expiration-driven generic entry, IRA price negotiation, and biosimilar or generic formulary substitution operating across PBM contracting cycles. These mechanisms are not sequential. They overlap, and their combined effect on revenue is not additive — it compounds.

A drug selected for IRA negotiation at year seven post-approval will see Medicare pricing take effect at year nine. If the compound patent expires at year twelve, the IRA price is already embedded in the brand’s revenue base for three years before generic entry. The post-LOE revenue collapse then starts from a lower base. The brand’s effective peak revenue never materializes in the way the original franchise model assumed.

Characteristic 2: Biosimilar LOE Is a Slope, Not a Cliff

For biologics, the six-month collapse model does not apply. Biosimilar market uptake in the United States has been materially slower than small-molecule generic uptake for multiple structural reasons: the absence of automatic substitution for non-interchangeable biosimilars, PBM rebate agreements that favor the originator biologic, physician prescribing inertia, and patient assistance programs that reduce out-of-pocket costs for the brand.

The Humira biosimilar launch in 2023 is the most recent data point. Since the U.S. launch of Humira biosimilars in 2023, discounts have ranged from 5 to 85 percent off the drug’s list price, and market share losses of 30 to 70 percent are expected in the first year due to the growing presence of biosimilars in the U.S. and Europe. The range — 30 to 70 percent — is enormous and reflects the structural variability in biosimilar uptake speed. A brand that models a 60 percent first-year volume loss and experiences 30 percent instead has over-provisioned its transition costs and under-delivered on investor expectations in the opposite direction.

The practical implication: biologic LOE models need a minimum three-year post-LOE window to capture peak erosion, not a two-year window. The death march for biologics is slower, but it runs longer.

A brand that exits litigation with its primary compound patent intact but faces four outstanding secondary patent suits involving formulation, polymorph, and method-of-use claims cannot produce a reliable LOE revenue model. The actual competitive entry date is a distribution, not a point estimate. That distribution may span two to four years. The brand’s revenue planning operates on a point estimate because accounting standards require it, but the commercial reality operates on a distribution.

Teams that build revenue bridges around the midpoint of that distribution will be wrong half the time by construction. Teams that build to the earliest plausible entry scenario and then manage upside — by maintaining optionality in lifecycle management investments and authorized generic timing — are more resilient to the actual outcome.

Characteristic 4: Authorized Generic Launch Timing Is Itself a Multi-Year Decision

An authorized generic is a branded manufacturer’s own generic version of its drug, launched either directly or through a partner. It competes with the first-filer generic during the 180-day exclusivity period and preserves some gross margin for the brand company relative to losing all volume to third-party generics. But the authorized generic launch decision is neither simple nor riskless.

If the brand launches an authorized generic too early relative to the 180-day exclusivity period, it reduces the first-filer’s incentive to win the litigation — which can inadvertently benefit the brand company if losing the litigation keeps generics out longer. If it launches too late, it leaves the 180-day period entirely to the first-filer and surrenders volume and margin without compensation. The decision tree involves litigation timing, first-filer financial condition, probability of multiple entrants after the 180-day period, and PBM formulary cycle alignment. All of those variables are in motion simultaneously for the 36 months around the LOE date.

Keytruda’s LOE Timeline: What a $29 Billion Cliff Actually Looks Like

Keytruda (pembrolizumab, Merck) is the world’s best-selling drug, at $29.5 billion in 2024 revenue, about 56 percent of Merck’s entire business. When the IV formulation’s key patents expire in 2028, Merck faces losing more than half its revenue from a single event. Biosimilar manufacturers including Amgen, Samsung Bioepis, and Bio-Thera Solutions are already preparing their entries.

The sequence is already playing out in Merck’s public disclosures. IRA pricing takes effect in January 2028. Compound patent expiration follows in December 2028 in the U.S. and not until 2031 in Europe. Biosimilar development programs are in clinical trials at multiple manufacturers. The 36-month biosimilar interchangeability ramp begins, under the best-case scenario, in 2029.

The five-year death march for Keytruda runs from 2026 to 2031. Year 2026 is when strategic planning for the post-LOE world should already be complete. Year 2028 is the IRA price reset. Late 2028 or 2029 is the first biosimilar entry. 2030 to 2031 is peak erosion in the U.S. 2031 marks EU patent expiry. Between those endpoints, Merck’s revenue base transitions from a biologic monopoly to a competitive biosimilar market, with IRA pricing embedded throughout.

No two-year model captures that arc.

Eliquis LOE Timeline: How BMS and Pfizer Extended a $13 Billion Revenue Runway

Eliquis (apixaban, Bristol-Myers Squibb/Pfizer) generated about $13 billion in 2024 revenue. Generic entry is expected April 1, 2028, following court rulings that delayed initial 2026 expectations.

The Eliquis timeline illustrates the litigation extension mechanism in practice. The original Paragraph IV litigation established a settlement framework with expected generic entry in 2026. Subsequent litigation on secondary patents extended that to April 2028. BMS and its partner Pfizer secured a critical court win in August 2020 that would let them keep the market to themselves until 2026. Further litigation pushed competitive entry to 2028. The revenue runway extended by two years through secondary patent defense — two years on a $13 billion annual revenue base.

The commercial implication: the litigation investment was worth several hundred million dollars in legal fees to protect an estimated $26 billion in incremental revenue. That return-on-litigation calculus is straightforward, and it explains why brand manufacturers continue to pursue secondary patent defense even when the underlying patent quality is questionable.

Entresto LOE: Novartis, Pediatric Exclusivity, and the Softening Maneuver

Entresto (sacubitril/valsartan) had annual 2024 revenue of approximately $7.8 billion with loss of exclusivity in mid-2025.

In Novartis’s fourth-quarter and full-year 2024 earnings call, company executives expressed confidence that Novartis would be able to smoothly weather Entresto’s loss of exclusivity in mid-2025. The company expects to ‘secure pediatric exclusivity’ for Entresto, which could potentially help soften the blow of generics.

The pediatric exclusivity extension, worth six months added to any existing patent or regulatory exclusivity, is one of the most consistently used LOE delay mechanisms. It costs relatively little to obtain — a company must run a pediatric study, which may or may not have commercial value, but the study itself typically costs far less than six months of blockbuster drug revenue. Entresto’s pediatric study investment was, by any reasonable calculation, one of the highest-return R&D dollars Novartis spent.

The IRA ‘Negotiation Cliff’ vs. the Patent Cliff: Which Hits First?

For drugs approved between 2014 and 2018 with projected blockbuster revenues, the answer to this question now determines financial planning priorities for the next decade.

A small molecule approved in 2015 and still on market without generic competition becomes IRA-eligible for negotiation in 2022 (seven years post-approval). CMS selects drugs for negotiation annually. If selected in 2024, the Maximum Fair Price takes effect in 2026. If the compound patent expires in 2028, the IRA price is in market for two full years before generic competition begins. The brand’s effective peak revenue in 2025 and 2026 is structurally lower than it would have been without the IRA, regardless of what happens in the patent litigation.

For biologics, the timing gap is wider. An eleven-year eligibility threshold for IRA selection, combined with a 13-year biologics exclusivity floor on biosimilar approval, means that a biologic approved in 2012 faces IRA pricing in 2023 and biosimilar competition no earlier than 2025. In that case, the IRA price arrives two years before the earliest possible biosimilar entry. The commercial team managing that product is operating at a negotiated government price while simultaneously trying to defend against biosimilar clinical development programs that are already in Phase III trials.

“The next patent cliff, between 2025 and 2030, is set to be one of the biggest since 2010 from a loss of revenue perspective, with blockbuster drugs including Merck’s Keytruda, BMS’s Eliquis, and Johnson & Johnson’s Darzalex all losing market exclusivity.” — ResearchAndMarkets.com, as cited in DrugPatentWatch’s LOE analysis, 2025.

The interaction between IRA timelines and patent expiration schedules is now a primary variable in pharmaceutical asset valuation. The IRA effectively moves the revenue cliff forward, often by several years, fundamentally altering the return on investment for research and development. Analysts valuing pipeline assets must now model a four-variable system: patent expiration timing, litigation stay probability distribution, IRA selection likelihood, and biosimilar or generic entry speed. The two-year LOE model addresses only one of those four variables.

The ‘Pill Penalty’ and How It Distorts Small-Molecule Pipeline Investment

The IRA’s differential treatment of small molecules and biologics — seven-year eligibility versus eleven-year eligibility — has been widely criticized under the label “pill penalty.” The practical effect is that small-molecule drugs face earlier price controls relative to their effective patent life than biologics do.

In the same previously mentioned PhRMA study, 78 percent of companies reported that they expect to cancel early-stage small-molecule pipeline projects, preventing these drugs from even reaching the end of their research stages, as they are no longer economically viable.

The directive for the Secretary to work with Congress to end the pill penalty comes from a differential in the IRA’s price-fixing model: small molecule drugs are eligible for selection to the MDPNP seven years after FDA approval, and the price control goes into effect at year nine. The Trump administration’s April 2025 executive order acknowledged this asymmetry and directed HHS to develop reforms, though the structural mechanics of the IRA require legislative action to change.

For LOE planning purposes, the pill penalty means that the effective revenue window for a novel small molecule — from approval to the combination of IRA pricing plus eventual generic entry — is now shorter by design. A drug approved today with projected exclusivity to year 20 of its patent life should be modeled for IRA pricing at year nine, regardless of the patent picture. That is not a contingency; it is the base case under current law.

How Generic Manufacturers Actually Model Entry Timing: The NPV Calculation

Understanding how generic companies value LOE opportunities is critical for brand teams trying to anticipate the timing and intensity of generic competition. The generic NPV model for a Paragraph IV challenge is essentially a real-options framework.

The core inputs to a generic opportunity NPV model are: pre-LOE brand revenue (typically the three-year average trailing the LOE date, adjusted for market growth), from which a total addressable market is derived. Against that market, the generic firm models its expected market share as a function of the number of anticipated entrants, the FDA approval timeline (driven by ANDA complexity), and the probability and duration of litigation.

The first-filer advantage is enormous. The 180-day marketing exclusivity period granted to the first successful Paragraph IV challenger creates a duopoly for six months: the brand and one generic. In that window, the first-filer generic can price at a meaningful discount to the brand while maintaining margins far above what will exist once multiple generics enter. The 180-day marketing exclusivity granted to the first successful Paragraph IV filer can be worth hundreds of millions of dollars.

For a drug generating $5 billion annually in U.S. revenue, first-filer exclusivity during the 180-day window — assuming 40 percent volume capture at 40 percent discount — represents roughly $400 million in gross margin in six months. After the 180-day period expires and multiple generics enter, the market price collapses. The first-filer’s economics collapse with it. The entire value of the Paragraph IV challenge concentrates in that exclusivity window, which is why generic companies spend tens of millions of dollars in litigation costs to win it.

What the Number of ANDA Filers Tells You About Post-LOE Price Erosion

For traditional generics, price erosion is a function of the number of competitors. FDA and HHS data demonstrate a consistent, mathematically predictable pattern. The relationship is approximately as follows: with one generic entrant (first-filer exclusivity), prices fall to 60 to 80 percent of brand price. With two to three entrants, prices fall to 30 to 50 percent. With four or more entrants, prices fall below 20 percent of brand price. With ten or more entrants, prices in mature high-volume markets can fall to 5 percent or less of original brand price.

The Lipitor case is the benchmark. Market pricing collapsed from approximately $5 per tablet for branded Lipitor to under $0.10 per tablet for generic atorvastatin within 18 months. That 98 percent price decline reflects the dynamics of a very high-volume market with no significant technical barriers to generic manufacturing. Not every small molecule follows that trajectory, but the directional trend — rapid price collapse with multiple entrants — is consistent enough to treat as a planning baseline.

For brand teams, the number of active ANDA filers for their drug is therefore one of the most commercially useful data points available. DrugPatentWatch tracks ANDA filings, Paragraph IV certifications, and first-filer status for virtually every Orange Book-listed drug. If a brand drug has 12 ANDA filers with Paragraph IV certifications and an ongoing litigation stay that expires in 18 months, the analyst can model a reasonable range of generic entry dates and price erosion scenarios. That data is available years before LOE and changes the planning calculus materially.

The Biosimilar Interchangeability Problem: Why Biologic LOE Takes Longer

For biologics approaching LOE, the single most consequential regulatory distinction is between biosimilar approval and biosimilar interchangeability designation.

A biosimilar approved under the BPCIA (Biologics Price Competition and Innovation Act) can be prescribed by physicians as an alternative to the reference product, but it cannot be automatically substituted at the pharmacy level without the prescriber’s consent in most U.S. states. This is the fundamental difference from a small-molecule generic with an AB rating, which pharmacies must substitute automatically. The interchangeability designation changes that: an interchangeable biosimilar can be substituted at the pharmacy level, subject to state substitution laws, without prescriber involvement.

Achieving interchangeability designation requires additional switching studies demonstrating that alternating between the biosimilar and the reference product does not produce greater safety risks than using the reference product alone. Those studies add time and cost to the biosimilar development program. The result is that even after a biosimilar launches, its market penetration is limited by the absence of automatic substitution. Physicians must actively switch patients, or PBMs must use formulary exclusion as the mechanism.

PBM formulary exclusion is increasingly the driver of biosimilar adoption, but it operates on the annual formulary cycle. A PBM decision to exclude an originator biologic and prefer its biosimilar takes effect on January 1st or July 1st of a contract year. If the biosimilar launches in March, it waits until the next formulary cycle to achieve broad formulary advantage — which may be nine months away. The originator biologic maintains formulary access during that window.

The combined effect of interchangeability delays, formulary cycle timing, and physician prescribing inertia explains why biosimilar market penetration typically ramps over two to three years rather than compressing into six months.

The BPCIA ‘Patent Dance’ and How It Extends Biologic LOE

The BPCIA established a specific patent dispute resolution pathway called the “patent dance” — a structured information exchange between biosimilar applicants and reference product sponsors that determines which patents are litigated and in what sequence. The dance is optional for biosimilar applicants but has strategic implications regardless.

If a biosimilar applicant participates in the patent dance, it provides the reference product sponsor with its manufacturing process information and receives in return the sponsor’s list of patents it believes would be infringed. The parties then negotiate which patents to litigate immediately and which to defer. This structured process concentrates litigation on high-value patents and can shorten the total litigation timeline. It can also extend it, depending on how many patents the sponsor lists and how strategically it sequences its assertions.

Biosimilar applicants that opt out of the patent dance cannot be sued for patent infringement until they give 180-day commercial marketing notice, at which point the full patent assertion process begins. The opt-out strategy can delay litigation, but it also extends the uncertainty about which patents will ultimately be asserted and litigated.

For brand teams tracking competitive biosimilar timelines, the patent dance status is an observable indicator. A biosimilar applicant that has completed the patent dance negotiation and entered the litigation phase has a materially more defined entry timeline than one that has not yet given marketing notice.

Lifecycle Management: What Actually Works and What Doesn’t

Lifecycle management — the set of strategies brand manufacturers use to extend revenue beyond the primary patent expiration — is as old as the Hatch-Waxman Act itself. The effectiveness of individual strategies varies significantly, and the regulatory environment of 2025 and 2026 has changed the calculus on several of them.

New Formulation and Delivery System Patents: The Evergreening Trade-Off

Filing for a new extended-release formulation, a new delivery mechanism (auto-injector, transdermal patch, inhalation device), or a new salt form is the most common secondary patent strategy. If the new formulation offers genuine clinical benefit — improved patient adherence, reduced side effects, more convenient dosing — it may also generate its own prescriber demand and allow product hopping before generic entry on the original form.

Product hopping describes the practice of transitioning the patient base from an original branded formulation to a new formulation before the original formulation faces generic competition. The new formulation carries its own secondary patents. Physicians prescribing the new formulation write scripts that generics cannot automatically fill if the new formulation is not yet generically available. The revenue base migrates with the patients.

The legal risk to product hopping has increased. While the practice is generally legal under U.S. antitrust law unless undertaken with anticompetitive intent and no offsetting clinical rationale, the FTC under both the Biden and Trump administrations has signaled increased willingness to scrutinize transitions that lack demonstrable clinical benefit.

In 2023, 2024, and 2025, the FTC asserted that hundreds of patents were improperly listed in the Orange Book, meaning the agency disputed the accuracy or relevance of the patent listings, which it said resulted in higher costs and disincentives that delayed generic competition. The FTC’s enforcement campaign has not directly targeted product hopping as a standalone practice, but its aggressive approach to Orange Book listings suggests that secondary patents listed in connection with product hopping transitions will receive heightened scrutiny going forward.

Authorized Generics: The Brand’s Defensive Countermove

The authorized generic strategy deploys the brand’s own generic version of the drug through a partner or subsidiary to compete for generic volume during and after the 180-day exclusivity period. It reduces the revenue value of a Paragraph IV win for the first-filer generic, which in turn reduces the number of generic companies willing to invest in Paragraph IV litigation. Over time, this can paradoxically extend brand exclusivity by making generic challenges less financially attractive.

Pfizer pursued multiple lifecycle strategies simultaneously for Lipitor: launching an authorized generic through Watson Pharmaceuticals, negotiating retail pharmacy partnerships to maintain branded market share through discount programs, and investing in post-LOE marketing to retain brand loyalty. The authorized generic through Watson allowed Pfizer to capture a share of the generic revenue pool rather than surrendering it entirely.

The authorized generic decision requires careful timing relative to the litigation calendar. Launching the authorized generic before the first-filer’s 180-day exclusivity period ends destroys the first-filer’s exclusivity value and creates litigation risk. Launching simultaneously with or immediately after the 180-day period ends is the standard playbook.

New Indication Expansion: The Only True Revenue Extension

Every other lifecycle management strategy defends existing revenue. New indication expansion generates genuinely new revenue by creating new patient populations, new prescribing physicians, and new commercial infrastructure around the same molecule.

A successful new indication approval does not necessarily extend the primary compound patent — the compound patent covers the active ingredient regardless of indication — but it extends the product’s commercial life through clinical differentiation, physician engagement, and formulary access in new therapy areas. It may also generate new method-of-use patents that provide litigation leverage against generics seeking to carve in to those indications.

Merck has been pushing lifecycle moves designed to make switching less straightforward for Keytruda, including new formulations and routes of administration, which is part of how originators try to hold share when a biologic approaches loss of exclusivity. Keytruda’s subcutaneous formulation, approved in the U.S. in 2024, creates a separate Orange Book entry with its own patent protection timeline.

OTC Switch: The Post-LOE Revenue Pivot

Some drug manufacturers may choose to create an OTC version of their branded product to maintain and/or grow volume post-LOE. An OTC formulation strategy may help a company decelerate value erosion post-LOE, maintain current customers and acquire new ones, and protect the branded product’s long-term revenue stream.

The OTC switch strategy works best for drugs where the clinical risk of unsupervised patient use is low, the indication is patient self-diagnosable, and the brand has sufficient consumer equity to command a price premium over the generic prescription product. Claritin (loratadine), Prilosec (omeprazole), and Zyrtec (cetirizine) are canonical examples. Each preserved meaningful branded revenue through OTC conversion after generic erosion in the prescription channel.

The OTC pathway requires FDA approval of a new labeling framework and often additional safety studies. It also requires a different commercial infrastructure — consumer marketing, retail distribution, and OTC pricing economics — that most prescription pharmaceutical companies do not maintain internally. The lead time for a successful OTC switch is typically three to five years from conception to launch.

The Supply Chain Dimension: Why Generic Entry Risk Goes Beyond Patent Law

The pharmaceutical industry’s supply chain concentration in China and India has added a new layer of LOE timing risk that patent analysts rarely model. For a generic or biosimilar manufacturer, FDA approval of the ANDA or BLA is only one gating factor. Manufacturing readiness and supply chain reliability are gating factors of equal or greater practical importance.

External forces beyond the patent system are increasingly influencing the reliability and cost of generic entry. The pharmaceutical supply chain’s dependence on China has transformed from a logistical detail into a primary geopolitical risk factor.

A generic firm with FDA approval but a manufacturing site on import alert cannot launch. A biosimilar developer with a biosimilar application accepted for review but an API supplier facing export restrictions cannot complete its application. These scenarios have played out in practice — not just as theoretical risks — and they create a form of de facto exclusivity extension that benefits brand manufacturers without requiring any litigation.

For brand teams tracking competitive biosimilar programs, manufacturing site registrations, API supplier relationships, and FDA inspection histories at key biosimilar manufacturers are observable intelligence that can sharpen entry timing models. This data is available through FDA inspection databases, import alert records, and drug shortage monitoring systems.

FDA Manufacturing Holds and Their Effect on Generic Launch Timelines

A generic manufacturer that receives a Complete Response Letter citing manufacturing deficiencies faces a remediation and resubmission cycle that can add 12 to 24 months to its launch timeline. During that window, the brand retains its market exclusivity for practical purposes even if the patent landscape has otherwise cleared.

FDA’s current Good Manufacturing Practice (cGMP) enforcement has become more stringent for overseas manufacturing facilities since 2020, with India-based generic manufacturers in particular facing more frequent warning letters and import alerts. In a market with limited first-filer competitors, a cGMP hold on the first-filer’s primary facility can delay competitive entry by a year or more — time during which the brand can regain formulary position and rebuild its commercial infrastructure.

The commercial intelligence implication: brand teams monitoring the manufacturing compliance histories of their Paragraph IV filer competitors have an early warning system for potential launch delays that is independent of the litigation calendar.

What Does the 5-Year LOE Timeline Mean for Payer and Formulary Strategy?

Payers — health plans, PBMs, and integrated delivery networks — face a different version of the five-year LOE timeline than brand manufacturers do. Their challenge is forecasting formulary savings opportunities accurately enough to build them into benefit design before the savings materialize.

A health plan that builds a 2026 benefit design around expected generic entry for a major drug in that year, only to see the generic delayed until 2028 by secondary patent litigation, faces two years of unexpected branded drug costs at full price. The difference between the modeled generic price and the actual branded price across an entire covered population can represent tens of millions of dollars in unplanned pharmaceutical spend.

PBMs address this through formulary contingency provisions — clauses in pharmacy benefit contracts that allow formulary changes when generic entry timelines shift. But those provisions require accurate intelligence on the litigation calendar, which most payer organizations do not maintain internally. The gap between patent database data and formulary planning calendars represents a genuine commercial inefficiency that affects plan design and cost modeling.

How PBMs Use the LOE Calendar to Negotiate Rebates Pre-Emptively

A sophisticated PBM that knows a drug faces LOE in 18 months has leverage in the current-year rebate negotiation cycle. The brand manufacturer knows that the PBM can switch formulary placement to a biosimilar or generic as soon as one is available. That knowledge shifts negotiating power toward the PBM even before competition exists. The result is that rebate rates on drugs with approaching LOE dates tend to increase as the LOE date approaches — the brand surrenders margin in rebates to maintain formulary position in the pre-LOE window.

This pre-LOE rebate escalation is a predictable commercial consequence of transparent patent expiration timelines. It is part of the five-year revenue erosion arc, not a post-LOE phenomenon. A brand that forecasts revenue on the basis of current gross-to-net ratios will overestimate net revenue if it fails to model the pre-LOE rebate trajectory.

The Financial Impact of Getting LOE Timing Wrong: Earnings Volatility and Analyst Credibility

The financial consequences of LOE timing miscalculation are asymmetric. When generic entry arrives earlier than modeled, the revenue shortfall is immediate and material. When generic entry is delayed by litigation, the upside is real but rarely credited to management competence — it is attributed to patent defense, which is expected.

For drugs above $1 billion annual revenue, the projected revenue loss over 24 months post-LOE often exceeds the combined R&D spend on the next two pipeline candidates. The projected LOE impact is material enough to move company-level earnings per share by 10 to 40 percent in the LOE year.

The analyst community’s reaction to LOE surprises is well-documented. A company that guides to a 2026 LOE date in its 2024 annual report, then faces litigation settlement in early 2025 that moves generic entry to 2025, will face a stock price reaction that reflects not just the year of accelerated revenue loss but also a reassessment of management’s ability to forecast and defend its IP position. The credibility penalty compounds the financial penalty.

Conversely, companies that proactively disclose the full distribution of LOE timing scenarios — acknowledging secondary patent litigation risk, IRA selection probability, and biosimilar development timelines at multiple competitor programs — tend to receive more stable analyst coverage because they are managing expectations across the full five-year arc rather than anchoring to a single point estimate.

Merck’s Forecast Architecture as a Template for LOE Disclosure

Merck’s disclosure approach for Keytruda deserves attention as a practical template. Rather than citing a single LOE date, Merck disclosed the sequential pressure points: IRA pricing in January 2028, followed by compound patent expiration in December 2028, with European exclusivity running to 2031. This multi-event disclosure allows analysts to build their own revenue bridge models rather than receiving a single-point LOE estimate that is certain to be wrong in at least one dimension.

The disclosure also implicitly acknowledges that biosimilar competition will ramp over multiple years after the compound patent expires — it does not suggest a single-event revenue cliff. That framing is commercially accurate and financially more informative than the traditional cliff language.

LOE Risk by Therapeutic Class: Which Categories Face the Steepest Erosion Curves?

The speed and depth of post-LOE revenue erosion varies significantly by therapeutic class. The key variables are patient population size (which determines the number of potential generic entrants and the intensity of first-filer competition), clinical switching risk (which determines how quickly physicians transition patients), and manufacturing complexity (which determines how many generic manufacturers can realistically enter the market).

Oncology: High Revenue, Slow Biosimilar Uptake, Multiple Litigation Layers

Oncology is where the LOE problem is most acute in the current cycle. Keytruda, Eliquis, and Opdivo are concentrated in a narrow 2026-2028 window, with individually enormous revenue bases. Oncology biologics face slower biosimilar uptake than non-oncology biologics because physician prescribing decisions in oncology are more conservative — oncologists are slower to switch therapies for patients with life-threatening disease. That conservatism benefits brand manufacturers but also means the biosimilar market ramp is genuinely slower, not just a modeling convenience.

Oncology also concentrates the highest density of secondary patent litigation. Manufacturers of cancer treatments are acutely aware that a single additional year of exclusivity on a $5 billion drug is worth $5 billion. The litigation investment per year of extended exclusivity is therefore rational to a degree that other therapeutic classes do not support.

Immunology: The Humira Aftermath and What It Means for Dupixent

In its 2024 full-year results, Sanofi reported €13.1 billion ($15.5 billion) in Dupixent sales, about 30 percent of the total sales of the company that year. Dupixent’s revenue is diversified across multiple chronic type-2 inflammatory diseases, atopic dermatitis, asthma, chronic rhinosinusitis with nasal polyps, and eosinophilic esophagitis, which means exposure is not concentrated in a single indication.

In November 2025, Formycon announced progress with FYB208, a dupilumab biosimilar candidate, including completed preclinical development and preparation for clinical studies. The biosimilar development clock for Dupixent has started. Given Dupixent’s diversified indication base, biosimilar uptake dynamics will be more complex than for Humira — different indications have different prescriber conservatism levels, and the rebate economics of the PBM formulary decisions will need to account for the full indication breadth.

The Humira precedent is instructive. Despite its patent protection expiring in the U.S. in 2023 with multiple biosimilar competitors, AbbVie has maintained meaningful revenue through a combination of patient assistance programs, direct hospital contracting, and international exclusivity that extends longer than U.S. protection. The total revenue decline has been real but slower than initial models predicted.

Cardiovascular and Metabolic: The Semaglutide Wildcard

Ozempic and Wegovy (semaglutide, Novo Nordisk) generated a combined $26 billion in 2024. While the main U.S. patent does not expire until December 2031, international patents expire in Canada, India, Brazil, and China in 2026.

The semaglutide international LOE creates a bifurcated global revenue model. Novo Nordisk maintains U.S. exclusivity through 2031, but generics in India and Brazil launch in 2026. The U.S. compounding market, which has been producing semaglutide compounded copies under an FDA drug shortage designation, is a separate competitive dynamic that does not strictly respect patent boundaries in the traditional sense — though FDA enforcement actions through 2025 have progressively restricted compounded semaglutide as the official shortage designation expired.

Orange Book Reform and Its Effect on the 5-Year LOE Calendar

The Orange Book is the FDA’s official list of approved drug products with therapeutic equivalence evaluations. It is also the mechanism through which patent listings trigger the 30-month automatic stay. Reforms to Orange Book listing rules directly affect the length and structure of the five-year LOE death march.

Legislative efforts to address patent thickets and evergreening have multiplied since 2022, and several have now moved past committee consideration into active debate. The most significant are the Protecting Biosimilar Competition Act (targeting BPCIA patent assertion limits), the PATENT Act (reforming Orange Book listing rules to require affirmative demonstration of relevance), and various versions of the Stop STALLING Act (imposing financial penalties on sham citizen petitions).

If the PATENT Act passes in a form that requires affirmative demonstration of relevance for Orange Book listings, secondary patents currently listed without clear connection to the active ingredient will lose their stay-triggering capability. That would compress the litigation runway available to brand manufacturers, advancing competitive entry dates across a broad swath of products. The commercial impact would be felt most acutely by brands with the largest secondary patent portfolios.

The Federal Circuit’s Teva Ruling and Its Downstream Effect on Device-Drug Patents

The Federal Circuit ruled in December 2024 that the Listing Statute requires a patent to both claim the drug and cover the NDA product itself — and Teva’s patents did not claim the active ingredient, only components of the inhaler. Five patents. Each one had been creating litigation leverage and triggering stay periods that blocked generic approval. With those five gone, the competitive clock for generic albuterol inhalers moved forward by years.

The ruling’s downstream effect extends beyond albuterol inhalers. Any drug-device combination product where the listed patents cover device components rather than the active ingredient is now vulnerable to similar challenges. The logical extensions include insulin delivery devices, autoinjectors for biologics, and metered-dose inhalers for respiratory drugs. Generic and biosimilar manufacturers are now conducting systematic reviews of Orange Book listings for all combination products, identifying patents that fail the Federal Circuit’s standard, and preparing challenge strategies accordingly.

How to Build a Defensible 5-Year LOE Revenue Model

Building a revenue model that accurately captures the five-year LOE arc requires a different analytical architecture than the standard two-year cliff model. The model must account for four categories of events, each with its own probability distribution and timing uncertainty.

Step 1: Map the Full Patent Landscape, Not Just the Compound Patent

The compound patent expiration date is the anchor, not the endpoint. A complete patent landscape map includes every Orange Book-listed patent, its expiration date, its subject matter (compound, formulation, method-of-use, device), and its current litigation status. For biologics, the BPCIA patent list adds a parallel track. Tools like DrugPatentWatch provide this landscape mapping in structured form, including Paragraph IV filing histories, first-filer status, and litigation outcome data.

The model should treat the furthest-dated secondary patent with active litigation as the worst-case LOE date and the compound patent expiration as the best-case LOE date, then assign probability weights to intermediate scenarios based on litigation precedent in the relevant patent category and court.

Step 2: Model IRA Selection Probability as a Revenue Scenario, Not a Footnote

For any drug generating more than $2 billion in annual Medicare Part D or Part B spend without generic or biosimilar competition, IRA selection probability in the next three negotiation cycles should be treated as a base-case scenario, not a tail risk. The negotiated price range — based on the first round’s 38 to 79 percent discounts from list — should be modeled as a revenue reduction in the Medicare channel with an effective date two years from selection.

Step 3: Separate Small-Molecule and Biologic Erosion Curves

Small-molecule drugs follow the six-month volume collapse curve after the first multi-source generic entry. Biologics follow a two-to-three-year ramp curve. The model must use different erosion curves for each, and the biologic curve must account for the interchangeability designation gap between initial biosimilar approval and pharmacy-level substitution capability.

Step 4: Build in the Pre-LOE Rebate Escalation

Gross-to-net ratios for blockbuster drugs approaching LOE typically deteriorate in the 18 to 24 months before competitive entry as PBMs use formulary leverage to extract higher rebates. A revenue model that holds the current gross-to-net constant through the LOE date will overstate net revenue in the pre-LOE window. The pre-LOE rebate escalation should be modeled as a discrete revenue reduction, typically 3 to 8 percentage points of gross-to-net increase in the 24 months before competitive entry.

Step 5: Assign Probability-Weighted Launch Dates to Each Known Competitor Program

For biosimilars specifically, the competitive timeline is observable in real time through FDA biosimilar application submissions, clinical trial registrations, manufacturing site approvals, and patent dance status disclosures. A brand team that tracks the development status of every known biosimilar program for its product can build a probability-weighted launch timeline that is meaningfully more accurate than using the compound patent expiration date as a proxy for biosimilar entry.

The Strategic Reframe: From LOE Defense to LOE Transition

The most common strategic failure in LOE planning is framing the problem as defense. Companies that define their LOE strategy as “delaying generic entry” and “protecting brand revenue” are, by construction, playing a game they cannot win. The patent eventually expires. The generic eventually enters. The brand revenue eventually erodes. Defense is a time-buying exercise, not a value-creation strategy.

Companies that reframe the LOE problem as a revenue transition — from a declining branded asset to a portfolio of next-generation assets, franchise extensions, and market participation in the generic or biosimilar space itself — are better positioned to extract value across the full five-year arc.

Strategic planning for LOE typically begins three to five years before patent expiration, involving cross-functional teams assessing options for maximizing remaining exclusivity period revenue, preparing for generic competition, and transitioning resources to growth products. The three-to-five-year lead time is the minimum. Companies that begin planning at two years are already in triage mode, executing strategies that should have been decided years earlier.

LOE strategy can and should evolve over time. For companies already within that two-year window, all is not lost — although the urgency to act now and accelerate planning efforts is definitely greater.

The commercial reality is that some revenue preservation strategies require lead times longer than the two-year window allows. A successful OTC switch takes three to five years. A new indication that generates meaningful prescriber volume takes two to four years from approval. An authorized generic partnership requires six to twelve months to negotiate and structure. All of these must be decided and resourced well before the LOE date to be executable at the right time.

What the 2025-2030 Patent Cliff Tells Us About Industry-Wide Strategic Preparedness

Between 2025 and 2030, patents for nearly 200 drugs are set to expire, including approximately 70 blockbuster drugs — each generating over $1 billion in annual sales. Potential losses exceed $300 billion.

This concentration of LOE events creates an industry-wide competition for the same strategic resources: M&A targets that can replace revenue, licensing deals that can accelerate pipeline, and talent capable of managing complex LOE transitions. All of those resources are finite. Companies that have already secured their post-LOE revenue bridge — through acquisitions, partnerships, or pipeline advancement — are in a structurally better position than companies still searching for it with 24 months to LOE.

Bristol-Myers Squibb’s position illustrates the challenge at scale. Bristol-Myers Squibb faces the steepest proportional cliff. With Eliquis at $13 billion facing 2028 generic entry and Opdivo facing LOE in 2028, BMS must replace an enormous revenue base while simultaneously managing the transition. Its acquisition of Karuna Therapeutics and Mirati Therapeutics in 2023 and 2024, respectively, were explicitly framed as pipeline investments to offset the LOE exposure. Whether those pipeline assets mature on the right timeline is the $25 billion question.

Competitive Intelligence Tools for Tracking the 5-Year LOE Window in Real Time

Accurate LOE planning requires access to real-time patent, litigation, and regulatory data that is not available from standard corporate intelligence sources. The pharmaceutical IP data infrastructure has matured significantly over the past decade, and several platforms now provide the granular tracking that the five-year LOE model requires.

DrugPatentWatch is the primary resource for tracking Orange Book patent listings, Paragraph IV certification histories, first-filer status, ANDA approval timelines, and biosimilar development program status. The platform aggregates FDA Orange Book data, ANDA filing records, patent litigation records, and biosimilar application data into a single searchable database. For brand teams building LOE models, the ability to see how many ANDAs have been filed against a specific drug, which have Paragraph IV certifications, and which are in active litigation materially improves the accuracy of competitive entry timing estimates.

The FDA’s Drugs@FDA database and Purple Book provide primary data on approval histories, exclusivity periods, and biosimilar reference product relationships. PACER, the federal court filing system, provides real-time access to patent litigation pleadings, court opinions, and settlement filings. For active litigation monitoring, the combination of PACER filings and legal database access provides the most current picture of litigation status.

For biologic LOE specifically, the FDA’s biosimilar development program tracking, combined with ClinicalTrials.gov registrations for switching and comparability studies, provides observable leading indicators of biosimilar development program progress that can sharpen entry timing models by 12 to 18 months relative to using patent expiration dates as a proxy.

Key Takeaways

The two-year LOE model is structurally inadequate for any drug with secondary patent coverage, IRA exposure, or biosimilar competition. The actual revenue erosion arc for blockbusters spans five years or more, beginning at the IRA selection trigger and ending only at peak biosimilar or generic penetration.

The IRA creates a pre-LOE revenue cliff for high-Medicare-spend drugs that operates independently of and in advance of patent expiration. For small molecules, the trigger is seven years post-approval; for biologics, eleven years. Revenue models built before 2022 do not include this mechanism.

The Paragraph IV litigation calendar starts 30 to 48 months before the compound patent expiration and generates a probability distribution of competitive entry dates, not a single point estimate. Serial litigation tactics can extend that uncertainty window by 18 to 36 months beyond the nominal LOE date.

Biosimilar LOE is a slope, not a cliff. The two-to-three-year biosimilar market penetration ramp reflects interchangeability designation gaps, PBM formulary cycle timing, and physician prescribing inertia. Biologic LOE models need a minimum three-year post-entry window to capture peak erosion.

The FTC’s 2024-2025 Orange Book enforcement campaign, culminating in Teva’s removal of over 200 device patent listings, has structurally shortened the secondary patent runway for drug-device combination products. LOE timelines for inhalers and autoinjectors are advancing as a direct result.

Pre-LOE rebate escalation — driven by PBM leverage in the 18 to 24 months before competitive entry — is a predictable gross-to-net deterioration that standard LOE models omit. It reduces net revenue in the window before the cliff, compressing the revenue bridge further.

The five-year death march requires a five-year planning horizon. LOE strategies that require three or more years to execute — OTC switches, new indication approvals, authorized generic partnerships — must be decided and resourced well before the 24-month window that most brand teams treat as their planning horizon.

Real-time intelligence on ANDA filing status, litigation calendar, biosimilar development program progress, and FDA manufacturing compliance histories at competitor facilities materially improves the accuracy of LOE timing models. Platforms like DrugPatentWatch aggregate this data in trackable form.

FAQ

Q1: What is the difference between patent expiration and loss of exclusivity in pharma?

Patent expiration is the legal end of a specific patent’s 20-year term. Loss of exclusivity (LOE) is the date on which a generic or biosimilar competitor actually enters the market and begins eroding brand revenue. The two dates can differ by several years due to patent term extensions, pediatric exclusivity add-ons, the 30-month litigation stay under Hatch-Waxman, first-filer 180-day marketing exclusivity, and FDA regulatory exclusivity periods that operate independently of patents.

Q2: How does the IRA affect a drug’s LOE timeline?

The Inflation Reduction Act allows CMS to negotiate drug prices for high-Medicare-spend branded drugs without generic or biosimilar competition. Small molecules become eligible at year seven post-approval; biologics at year eleven. The negotiated Maximum Fair Price takes effect two years after selection. For drugs with approaching LOE dates, this creates a pre-competitive price reduction that arrives before generic or biosimilar entry — effectively moving the revenue cliff earlier without changing the patent expiration date.

Q3: What is the 30-month stay and how does it extend effective exclusivity?

Under Hatch-Waxman, when a generic manufacturer files an ANDA with a Paragraph IV certification and the brand manufacturer sues within 45 days, an automatic 30-month stay prevents the FDA from approving the generic application while the patent litigation proceeds. For each separately listed Orange Book patent challenged by the generic, a separate 30-month stay can be triggered. Brand manufacturers with multiple listed patents can stack stays, though courts have placed limits on abusive stay use.

Q4: What is product hopping and is it legal?

Product hopping is the practice of transitioning the patient base from an original branded formulation to a reformulated version before the original faces generic competition. The new formulation carries its own secondary patents and may not have generic equivalents yet. It is generally legal under U.S. antitrust law unless a court finds it was undertaken specifically to exclude competition with no offsetting clinical benefit — a high bar that is rarely met. The FTC has signaled increased scrutiny but has not established product hopping as per se unlawful.

Q5: How does biosimilar interchangeability status affect LOE modeling?

An interchangeable biosimilar can be substituted at the pharmacy level without prescriber involvement, subject to state laws. A non-interchangeable biosimilar requires active prescriber decisions to switch patients. The absence of interchangeability substantially slows biosimilar market penetration, extending the brand’s effective revenue duration. LOE models for biologics must account for the timing gap between initial biosimilar approval and interchangeability designation — which can add 12 to 24 months to peak erosion timelines.

Q6: What is serial patent litigation and how does it delay generic entry beyond the nominal LOE date?

Serial patent litigation involves a brand manufacturer filing new infringement suits on patents obtained after an initial Hatch-Waxman settlement. Because Hatch-Waxman does not bar subsequent litigation on subsequently granted patents, a brand that obtains a new patent during ongoing ANDA litigation can restart the litigation clock on the same generic product. The Myrbetriq case documented four additional lawsuits filed after the initial 2020 settlement, delaying broad competition into 2024 despite the original settlement contemplating 2024 generic entry in any case.

Q7: What is the 180-day first-filer exclusivity and why does it matter for LOE timing?

The first generic company to file an ANDA with a Paragraph IV certification for a given drug receives 180 days of marketing exclusivity after it first commercially markets the product. During this window, no other generic can receive FDA approval. This exclusivity period concentrates enormous financial value in the first six months of generic competition — the first-filer can price at a meaningful discount to the brand while maintaining margins far above the eventual multi-entrant equilibrium. It also means that brand revenue in the first six months post-LOE declines less sharply than the subsequent 12 to 18 months when multiple generics enter.

Q8: How should pre-LOE authorized generic strategy be timed?

An authorized generic launched during the first-filer’s 180-day exclusivity period competes directly with the first-filer, reducing the value of that exclusivity and potentially deterring future Paragraph IV challenges for the brand’s other products. It also allows the brand company to capture some generic revenue during the exclusivity window. The optimal timing depends on the first-filer’s financial condition, the probability of additional generic entrants, and the brand company’s pricing strategy. Standard practice is to launch the authorized generic simultaneously with or immediately after the first-filer’s launch, not before it.

Q9: How do Orange Book listing reforms affect existing LOE timelines?

Reforms that require affirmative demonstration of patent relevance for Orange Book listings remove stay-triggering capability from patents that do not directly cover the drug’s active ingredient. The Federal Circuit’s December 2024 ruling on Teva’s inhaler device patents established that device-component patents cannot be listed in the Orange Book for drugs that include those devices. For any drug-device combination with device patents currently listed, that ruling opens those listings to challenge and potential removal, advancing competitive entry timelines.

Q10: What data sources give the most accurate picture of competitive LOE timing in real time?

The most actionable LOE intelligence comes from four primary sources: the FDA Orange Book (patent listings and expiration dates, regulatory exclusivity periods, AB-rating status for generic equivalents), DrugPatentWatch (ANDA filing histories, Paragraph IV certification status, first-filer identification, litigation outcome tracking, biosimilar development program status), PACER federal court filings (real-time litigation proceedings, settlement filings, court opinions), and ClinicalTrials.gov (biosimilar switching and comparability studies, which provide observable indicators of biosimilar development program progress). Together, these sources support a probability-weighted competitive entry model that is materially more accurate than compound patent expiration date analysis alone.

Citations

DrugPatentWatch. (2026, March 22). Drug patent expiration: The complete strategic guide to loss of exclusivity, lifecycle management, and the $400 billion cliff. https://www.drugpatentwatch.com/blog/the-impact-of-drug-patent-expiration-financial-implications-lifecycle-strategies-and-market-transformations/

DrugPatentWatch. (2026, March 10). The patent cliff playbook: Pharmaceutical IP valuation, generic entry timing, and biosimilar strategy. https://www.drugpatentwatch.com/blog/patent-expirations-seizing-opportunities-in-the-generic-drug-market/

DrugPatentWatch. (2026, March 4). Predict the patent cliff: The patent cliff is coming. Here’s how to see it first. https://www.drugpatentwatch.com/blog/predict-the-patent-cliff/

Alcimed. (2025, October 27). Patent cliff: What strategies can help biopharma stay competitive? https://www.alcimed.com/en/insights/patent-cliff/

BioSpace. (2025, February 19). 5 pharma powerhouses facing massive patent cliffs — and what they’re doing about it. https://www.biospace.com/business/5-pharma-powerhouses-facing-massive-patent-cliffs-and-what-theyre-doing-about-it

Labiotech. (2026, March 23). The next pharma patent cliff: how 2026-2032 will reshape revenue. https://www.labiotech.eu/best-biotech/pharma-patent-cliff/

DrugPatentWatch. (2025, December 16). The patent cliff playbook: A strategic guide to tracking and capitalizing on pharmaceutical loss of exclusivity. https://www.drugpatentwatch.com/blog/the-patent-cliff-playbook-a-strategic-guide-to-tracking-and-capitalizing-on-pharmaceutical-loss-of-exclusivity/

DeepCeutix. (2026, February 2). $300 billion in pharma revenue loses patent protection by 2030. https://deepceutix.com/insights/patent-cliff-reformulation

Global Pricing Innovations. (2025, November 4). Patent cliff in pharma: Navigating disruption and creating opportunity. https://globalpricing.com/patent-cliff-in-pharma-navigating-disruption-and-creating-opportunity/

DrugPatentWatch. (2026, February 27). The LOE sales playbook: 100 revenue triggers for pharmaceutical supply vendors. https://www.drugpatentwatch.com/blog/the-loe-sales-playbook-100-revenue-triggers-for-pharmaceutical-supply-vendors/

DrugPatentWatch. (2026, April 5). Lipitor’s patent cliff playbook: How Pfizer kept 40% market share after generic entry. https://www.drugpatentwatch.com/blog/how-can-pharmaceutical-marketing-evolve-with-generic-entry-the-example-of-lipitor/

DrugPatentWatch. (2026, January 22). The patent cliff and beyond: A definitive guide to generic and biosimilar market entry. https://www.drugpatentwatch.com/blog/generic-drug-entry-timeline-predicting-market-dynamics-after-patent-loss/

DrugPatentWatch. (2026, March 13). Follow the patent, find the generic: The complete lifecycle of how cheap drugs win. https://www.drugpatentwatch.com/blog/understanding-the-lifecycle-of-generic-drugs-from-development-to-market-impact/

Pharmaceutical Executive. (2025). Loss of exclusivity: Strategies to maximize product value. https://www.pharmexec.com/view/loss-exclusivity-strategies-maximize-product-value

Flevy. (n.d.). What does LOE mean in pharmaceuticals? (Loss of exclusivity explained). https://flevy.com/topic/life-sciences/question/decoding-loe-pharmaceuticals-meaning-implications-explained

DrugPatentWatch. (2026, February 2). The data-driven guide to winning the 2026 patent cliff. https://www.drugpatentwatch.com/blog/the-data-driven-guide-to-winning-the-2026-patent-cliff/

DrugPatentWatch. (2026, March 11). The IRA price reset: What it actually does to pharma pricing, and what comes next. https://www.drugpatentwatch.com/blog/the-ira-price-reset-what-it-actually-does-to-pharma-pricing-and-what-comes-next/

Boston Consulting Group. (2023, June 28). Navigating the Inflation Reduction Act’s impact on drug pricing and innovation. https://www.bcg.com/publications/2023/navigating-inflation-reduction-act-impact-on-drug-pricing-innovation

Epstein Becker Green. (2025, May 2). Medicare drug price negotiation program: The IRA ‘pill penalty’ and other IRA reforms on the horizon for 2026. https://www.healthlawadvisor.com/medicare-drug-price-negotiation-program-the-inflation-reduction-act-pill-penalty-and-other-ira-reforms-on-the-horizon-for-2026

ITIF. (2025, February 25). The Inflation Reduction Act is negotiating the United States out of drug innovation. https://itif.org/publications/2025/02/25/the-inflation-reduction-act-is-negotiating-the-united-states-out-of-drug-innovation/

Congressional Research Service / Congress.gov. (n.d.). Medicare drug price negotiation under the Inflation Reduction Act: Industry responses and potential effects. https://www.congress.gov/crs-product/R47872

PMC / National Library of Medicine. (2025). Negotiating Medicare drug prices: A new attempt to control purchase prices. https://pmc.ncbi.nlm.nih.gov/articles/PMC12179530/

Pharmaphorum. (2025, June 16). US drug pricing overhaul: The IRA and the executive order on most-favored-nation drug pricing. https://pharmaphorum.com/sales-marketing/us-drug-pricing-overhaul-inflation-reduction-act-ira-and-executive-order-eo-most

Commonwealth Fund. (2025, November 13). How drugmakers use the patent process to keep prices high. https://www.commonwealthfund.org/publications/explainer/2025/nov/how-drugmakers-use-patent-process-keep-prices-high

DrugPatentWatch. (2026, January 16). Evergreening by lawsuit: Strategic patent actions and generic entry stagnation. https://www.drugpatentwatch.com/blog/evergreening-by-lawsuit-strategic-patent-actions-and-generic-entry-stagnation/

DrugPatentWatch. (2026, March 8). When the patent wall crumbles: Secondary abandonment and the death of drug evergreening. https://www.drugpatentwatch.com/blog/when-the-patent-wall-crumbles-secondary-abandonment-and-the-death-of-drug-evergreening/

Gaffney, A., et al. (2025). Serial patent litigation: An emerging strategy to delay entry of generic competition. PMC / National Library of Medicine. https://www.ncbi.nlm.nih.gov/pmc/articles/PMC12757684/

DrugPatentWatch. (2026, March 22). Drug patent evergreening works, until it doesn’t. https://www.drugpatentwatch.com/blog/does-drug-patent-evergreening-prevent-generic-entry/

DrugPatentWatch. (2026, February 3). The evergreening gambit: A strategic guide to pharmaceutical patent lifecycle management. https://www.drugpatentwatch.com/blog/the-evergreening-gambit-a-strategic-guide-to-pharmaceutical-patent-lifecycle-management/

DrugPatentWatch. (2025, December 2). Mastering LOE: Expert strategies to predict drug patent expiry and seize generic market share. https://www.drugpatentwatch.com/blog/mastering-loe-expert-strategies-to-predict-drug-patent-expiry-and-seize-generic-market-share/

DrugPatentWatch. (2026, March 24). Win the generic drug market: Patents, ANDAs, IP valuation, and the tactics that separate first-movers from also-rans. https://www.drugpatentwatch.com/blog/how-to-succeed-in-generic-drug-market-entry/

")