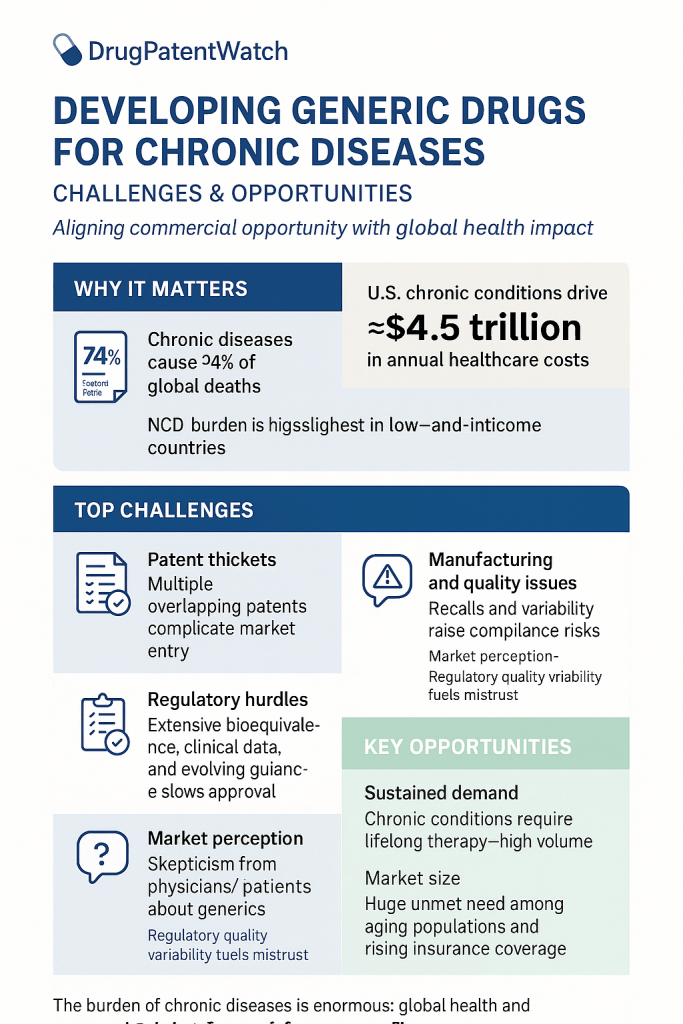

Chronic diseases kill 74% of all humans who die each year. That is not a warm-up statistic—it is the entire commercial premise of the generic pharmaceutical industry. Noncommunicable diseases (NCDs) including cardiovascular disease, type 2 diabetes, chronic obstructive pulmonary disease (COPD), and cancer require decades of continuous medication management. That sustained, high-volume demand is precisely what makes the generic drug market a $500+ billion global business and, for companies that execute correctly, one of the most predictable revenue engines in all of healthcare.

But predictable does not mean easy. The distance between a brand-name drug’s patent expiration and a generic manufacturer’s first commercial shipment is littered with regulatory tripwires, patent thickets, supply chain failures, and PBM opacity. This guide maps that distance in full. It covers the molecular science of bioequivalence, the IP valuation mechanics that determine whether a molecule is actually worth chasing, the exact technology roadmaps innovator companies use to delay your entry, and the commercialization tactics that separate generic launches that capture 70% market share from ones that stall at 12%.

The target audience is pharma and biotech IP teams, portfolio managers, R&D leads, and institutional investors who need more than a regulatory overview. You will find patent-specific analysis, IP asset valuations for named drugs, manufacturing technology comparisons, and investment strategy notes throughout.

1. The Market Case: Why Chronic Diseases Drive Generic Demand

The Disease Burden as a Revenue Map

NCDs account for $4.5 trillion in annual U.S. healthcare expenditures. Over three-quarters of all NCD-related deaths occur in low- and middle-income countries, where healthcare systems cannot sustain brand-name drug pricing. This geography matters commercially: generic manufacturers with quality systems capable of serving both FDA and WHO Prequalification standards can address global demand simultaneously, multiplying addressable market size without proportional increases in development cost.

The math on medication volume is straightforward. A patient diagnosed with hypertension at age 45 takes antihypertensives for the next 30 to 40 years. Multiply that duration by the 1.28 billion adults worldwide with hypertension, and the continuous prescription volume becomes self-evident. The same logic applies to metformin use in type 2 diabetes, inhaled corticosteroids in asthma, and statins in hyperlipidemia. These are not acute-use markets with episodic demand spikes. They are annuity-like revenue streams for whichever manufacturer holds formulary position.

Generic drugs represent 89% of all U.S. prescriptions filled but only 26% of total drug expenditure. That asymmetry—vast volume at compressed margins—defines the competitive structure of the entire industry and explains why timing, patent intelligence, and manufacturing scale are the primary determinants of profitability.

The Adherence Multiplier

Cost is the number-one driver of medication non-adherence in chronic disease. Patients report skipping or rationing prescriptions for diabetes, hypertension, and asthma at rates that consistently track with out-of-pocket cost thresholds. Non-adherence carries a $300 billion annual price tag in avoidable hospitalizations, emergency visits, and disease progression costs in the U.S. alone.

Generic drugs reduce that friction. Studies show patients started on generic medications are more likely to maintain their regimen over 12 months than patients started on equivalent brand-name drugs. For chronic disease categories where adherence directly prevents expensive acute events—myocardial infarction in hypertension, ketoacidosis in diabetes, exacerbations in COPD—the public health value of generic availability translates directly into health system cost savings that payers recognize and reward through formulary preference.

Key Takeaways: Market Context

The NCD burden creates structural, recurring demand for long-term generic medications. The 89%/26% volume-to-spend ratio confirms that generic strategy is fundamentally a volume game requiring operational scale. Adherence data links generic affordability to measurable health outcomes, which gives generic manufacturers a value-based argument for formulary preference beyond price alone. For portfolio managers: therapeutic areas with high chronic disease prevalence and imminent patent expirations are the most defensible targets for ANDA investment.

2. Taxonomy of Follow-On Drugs: Small Molecules, Biosimilars, and Complex Generics

Understanding what category of follow-on drug you are developing is not a semantic exercise. It determines development cost, timeline, regulatory pathway, competitive density, pricing power, and IP strategy. Conflating these categories is a common and expensive mistake in portfolio planning.

Small Molecule Generics: High Volume, Compressed Margins

Small molecule generics are chemically synthesized compounds with well-defined molecular structures. The active pharmaceutical ingredient (API) is identical to the reference listed drug (RLD). Atorvastatin calcium (generic Lipitor), amlodipine besylate (generic Norvasc), metformin hydrochloride (generic Glucophage), and lisinopril are canonical examples—all among the highest-prescription-volume drugs in the U.S. and all now generic.

Development follows the Abbreviated New Drug Application (ANDA) pathway. No new clinical trials for efficacy or safety are required; the manufacturer demonstrates bioequivalence through pharmacokinetic studies in healthy volunteers. Development cost typically ranges from $1 million to $4 million. That low barrier produces intense competition: once six or more generics enter a market, prices collapse to 5-10% of original brand pricing.

The IP asset value of a target small molecule generic is almost entirely determined by patent expiration timing and the number of likely ANDA filers. A molecule with a single compound patent expiring in 18 months and no active Paragraph IV challenges pending from competitors is a high-value opportunity. The same molecule with four tentative approvals already issued and a contested patent litigation dragging through district court has fundamentally different economics.

IP Valuation: Small Molecule Generics

For ANDA targets in chronic disease categories, IP valuation requires mapping four data layers:

Orange Book patent listings (compound, formulation, method of use, polymorph patents with their expiration dates and associated exclusivities)

Active Paragraph IV certification filings and their litigation status

Authorized generic agreements (brand companies frequently launch their own authorized generic the same day as the first generic, neutralizing the 180-day exclusivity advantage)

Post-patent regulatory exclusivity protections still running (pediatric exclusivity, NCE exclusivity)

A concrete example: atorvastatin calcium (Lipitor) lost its primary compound patent in November 2011. Ranbaxy had secured first-filer status via Paragraph IV certification years earlier, but complications from an FDA import alert on Ranbaxy’s Paonta Sahib facility, combined with Pfizer launching an authorized generic on day one, significantly compressed the financial upside of that exclusivity window. The lesson for IP teams is that patent expiration date is a necessary but insufficient input for valuing a generic opportunity. The full IP stack, authorized generic risk, and manufacturing qualification status all feed into the net present value calculation.

Biosimilars: Higher Margins, Higher Science Bar

Biosimilars are follow-on versions of reference biological products—large, complex molecules manufactured in living cell systems (Chinese hamster ovary cells, Escherichia coli, Saccharomyces cerevisiae). They cannot be called “identical” to the reference product because biological manufacturing processes introduce inherent micro-heterogeneity in glycosylation patterns, folding conformations, and post-translational modifications. The regulatory standard is “highly similar,” with no clinically meaningful differences in safety, purity, or potency.

The distinction matters practically: biosimilar development costs exceed $100 million and take 7 to 8 years. A biosimilar program requires extensive analytical characterization (mass spectrometry, circular dichroism, surface plasmon resonance), animal pharmacology and toxicology studies, comparative pharmacokinetic/pharmacodynamic (PK/PD) clinical studies, and immunogenicity assessments. The 351(k) pathway under the Biologics Price Competition and Innovation Act (BPCIA) governs U.S. approval.

Biosimilar price erosion is structurally shallower than small molecule generic erosion. Reference biologics typically see 15-30% price reductions when biosimilars enter, compared to 80%+ for small molecules. Fewer competitors enter (the capital requirements screen out smaller players), and physicians and patients exhibit greater inertia around switching biologic therapies. That combination produces more durable pricing power for biosimilar developers.

IP Valuation: Biosimilars

Biosimilar IP valuation is more complex than small molecule analysis because the relevant protections extend beyond Orange Book patents. Key inputs include:

12-year reference product exclusivity under the BPCIA (10 years in the EU), which blocks 351(k) approval regardless of patent status

Patent dance procedures: the BPCIA mandates a staged exchange of patent lists between the biosimilar applicant and the reference product sponsor, potentially triggering litigation on dozens of patents simultaneously

Market-specific interchangeability status (discussed in Section 3), which dramatically affects capture of pharmacy-level substitution volume

Reference product sales at risk: the higher the reference biologic’s revenue, the more the originator will spend on patent enforcement and physician retention programs

A high-profile example is adalimumab (Humira, AbbVie). Humira generated over $20 billion in annual global revenue at its peak. AbbVie constructed a patent portfolio exceeding 250 patents in the U.S. alone—compound patents, formulation patents, manufacturing process patents, and device patents on the autoinjector—while simultaneously executing a global settlement strategy that licensed biosimilar entry in Europe starting 2018 but delayed U.S. entry until January 2023. IP teams modeling the Humira biosimilar opportunity in 2020 needed to value not just the U.S. market opportunity but the cost and timeline risk from AbbVie’s layered IP enforcement strategy. Several biosimilar developers spent $300-500 million on development and litigation before reaching the U.S. market.

Complex Generics: The Blue Ocean, With Hazards

Complex generics occupy a category the FDA defines by complexity of active ingredient, formulation, dosage form, route of administration, or drug-device combination status. The category includes transdermal drug delivery systems (patches), liposomal formulations (e.g., liposomal doxorubicin), inhaled products (dry powder inhalers, metered-dose inhalers), long-acting injectables (LAIs) using microsphere or implant technology, and topical products with local site of action.

Development cost sits between small molecule generics and biosimilars—typically $10 million to $50 million depending on the required studies. The key challenges are that standard pharmacokinetic bioequivalence methods often cannot demonstrate equivalence for locally-acting products (e.g., inhaled corticosteroids where lung deposition is the relevant endpoint, not blood concentration), and that FDA product-specific guidance is absent or ambiguous for many complex products.

Less competition enters these markets because fewer generic manufacturers have the formulation science capabilities, device engineering expertise, or regulatory experience required. That limited competition sustains pricing at 40-60% of reference product levels even after multiple generics enter, compared to the near-zero margins in crowded small molecule markets.

IP Valuation: Complex Generics

IP valuation for complex generics requires layering patent analysis with regulatory pathway risk scoring. A target that has clear FDA product-specific guidance, a defined bioequivalence methodology, and a single compound patent expiring within two years is far more valuable than an equivalent-revenue target where FDA guidance is ambiguous and three competing ANDA filers are already in review. Companies such as Amneal, Hikma, Perrigo, and Par Pharmaceutical have built significant franchise value in complex generics precisely by targeting markets where regulatory ambiguity is solvable with scientific investment but deters less sophisticated competitors.

Feature

Small Molecule Generics

Biosimilars

Complex Generics

Active ingredient nature

Chemically synthesized, identical to RLD

Derived from living cell systems, highly similar

Chemically synthesized; complexity in formulation or delivery

Molecular structure

Small, fully characterizable

Large, inherently variable

Variable; delivery system adds complexity

Bioequivalence standard

Standard PK BE (AUC/Cmax within 80-125% CI)

‘Highly similar’; totality of evidence

Product-specific; may require in vitro/in vivo correlation or clinical endpoints

U.S. regulatory pathway

ANDA (Hatch-Waxman)

351(k) (BPCIA)

ANDA, sometimes 505(b)(2); product-specific FDA guidance

Typical development cost

$1-4 million

>$100 million

$10-50 million

Development timeline

2-4 years pre-filing

7-8 years

3-6 years

Post-entry price erosion

Up to 95% with 6+ competitors

15-30%

30-55%

Competitive density

High

Moderate

Low to moderate

Table 1: Follow-On Drug Categories Compared

Key Takeaways: Taxonomy

Each category of follow-on drug demands a distinct IP strategy, capital budget, and time horizon. Small molecule generics compete on speed to market and manufacturing cost efficiency. Biosimilars compete on analytical science depth, litigation tolerance, and physician/payer relationships. Complex generics compete on formulation expertise and regulatory navigation capability. Portfolio managers allocating R&D capital should treat these as distinct asset classes with non-correlated risk and return profiles.

3. Regulatory Pathways: ANDA, 505(b)(2), and the 351(k) Biosimilar Track

The ANDA Pathway: Mechanics and Strategic Implications

The Abbreviated New Drug Application, established by the Drug Price Competition and Patent Term Restoration Act of 1984 (Hatch-Waxman Act), is the foundation of the U.S. generic industry. The “abbreviated” designation reflects its core value: the applicant relies on FDA’s prior finding of safety and efficacy for the reference listed drug. No animal studies and no human efficacy trials are required. The generic manufacturer must demonstrate pharmaceutical equivalence (same active ingredient, strength, dosage form, route of administration) and bioequivalence.

Bioequivalence is defined as equivalent rate and extent of absorption, tested through pharmacokinetic studies in healthy adult volunteers under fasting and fed conditions for oral products. The FDA accepts bioequivalence when the 90% confidence interval for the geometric mean ratio of AUC (total exposure) and Cmax (peak concentration) falls within 80.00% to 125.00% of the reference drug values. This interval is not a measure of how closely the generic performs to the brand—it is a statistical range within which the FDA considers performance equivalent given normal biological variability.

For a small number of drugs with narrow therapeutic indices (NTI drugs)—warfarin, levothyroxine, phenytoin, cyclosporine, digoxin, lithium—the FDA applies tighter bioequivalence acceptance criteria, typically requiring the 90% confidence interval to fall within 90.00% to 111.11%. NTI drugs require particular attention during post-approval monitoring because even modest variability in blood concentrations can produce serious adverse events, and this is the pharmacological basis for some of the most persistent physician reluctance to authorize generic substitution.

Bioequivalence Studies: Design and Cost

A standard single-dose, two-period, two-sequence crossover bioequivalence study in 24 to 36 healthy volunteers costs approximately $300,000 to $600,000 for the clinical component alone. For fed and fasting conditions combined, two studies are typically required. For products with complex PK profiles, replicate design studies are sometimes necessary. Analytical method development and validation, statistical analysis, and regulatory preparation add to the total.

The FDA’s Model Integrated Summary of Bioavailability (MISAB) and the use of population PK methods are expanding for specific product types, reducing the number of subjects required in some cases. However, for most standard oral solid dose forms, the conventional two-period crossover remains the gold standard.

Labeling and the Skinny-Label Strategy

Generic applicants must use labeling identical to the reference listed drug for all approved indications, unless a specific indication remains under patent or exclusivity protection. The “skinny-label” mechanism (formally, section viii carve-out under 21 CFR 314.94) allows a generic to seek approval for the subset of indications not covered by listed method-of-use patents, omitting protected indications from the proposed label.

Skinny labeling enables earlier market entry but creates patent infringement exposure. The GSK v. Teva case, decided by the Federal Circuit in 2021, held that Teva’s skinny label for carvedilol (Coreg) could still induce infringement of GSK’s method-of-use patents covering heart failure treatment—even though Teva’s label only listed the non-patented indication of hypertension. The court found that other elements of Teva’s label and marketing implicitly directed use for heart failure. That decision sent a significant chilling signal through the generic industry, and IP counsel at generic companies now routinely model active inducement risk as a component of skinny-label strategy.

The Hatch-Waxman Act: Patent Certifications and Their Commercial Significance

Every ANDA contains a certification for each patent listed in the FDA Orange Book for the reference drug. The four paragraph certifications are:

Paragraph I: No patent information filed in the Orange Book.

Paragraph II: The patent has expired.

Paragraph III: The applicant will not seek approval before the patent expires.

Paragraph IV: The patent is invalid, unenforceable, or will not be infringed by the proposed generic.

Only Paragraph IV certifications trigger the dynamic commercial opportunities—and legal risks—that define generic pharmaceutical strategy. Filing a Paragraph IV certification constitutes an act of patent infringement and requires notifying both the patent owner and the NDA holder. If the brand company files suit within 45 days, the FDA is automatically prohibited from approving the ANDA for 30 months (the ’30-month stay’) while litigation proceeds. The generic company bears litigation costs throughout this period while receiving no revenue.

The first applicant to file a substantially complete ANDA with a Paragraph IV certification is eligible for 180 days of generic market exclusivity if it successfully prevails in the litigation or the patent is otherwise resolved. During this period, no other ANDA can be approved for the same drug. That 180-day exclusivity window is the primary financial incentive for aggressive patent challenges.

The 505(b)(2) Pathway: Differentiation Through Hybrid Development

The 505(b)(2) New Drug Application permits reliance on published literature and FDA’s prior approval of a related drug without conducting a full original clinical program. Unlike an ANDA, a 505(b)(2) application can propose a new indication, a new dosage form, a new route of administration, a new strength, or a new formulation of an approved active ingredient. The applicant conducts only the studies necessary to bridge from the known active ingredient to the proposed new product.

This pathway is strategically important for generic companies seeking to escape commodity pricing. A 505(b)(2) product can qualify for 3 years of New Clinical Study Exclusivity (if new clinical investigations were essential to approval), 7 years of Orphan Drug Exclusivity, or 5-year NCE exclusivity if the active moiety has never been approved. That exclusivity converts what would otherwise be a generic ANDA exercise into a branded or semi-branded product with temporary protection from generic competition.

Examples include extended-release reformulations that received 505(b)(2) approval after the immediate-release compound patent expired, new combinations of two established generics, and ophthalmic formulations of drugs already approved orally. The pathway is extensively used in specialty CNS, ophthalmology, and dermatology segments. For IP teams, 505(b)(2) products in the portfolio represent distinct IP assets with their own exclusivity timelines and must be tracked separately from ANDA assets.

The 351(k) Biosimilar Pathway: Science, Litigation, and the Patent Dance

The Biologics Price Competition and Innovation Act (BPCIA), enacted in 2010, established the 351(k) pathway for biosimilar approval. The pathway requires a “totality of evidence” demonstration of biosimilarity: structural and functional analytical characterization, animal PK and toxicology data, and at least one comparative clinical trial addressing PK, PD, safety, and immunogenicity.

The BPCIA’s patent resolution mechanism—the “patent dance”—is more complex than the Hatch-Waxman certification system. After the biosimilar applicant provides its 351(k) application to the reference product sponsor, a staged exchange of patent lists and positions occurs over 60-180 days. The parties negotiate which patents will be litigated in a first wave and which will be reserved for later. If no agreement is reached, the reference product sponsor can bring suit on patents from a negotiated list. The process is designed to resolve patent disputes before the biosimilar reaches the market, but in practice it generates multiyear, multi-patent litigation campaigns that can cost both parties tens of millions of dollars.

Interchangeability Designation: The Pharmacy-Level Substitution Prize

An interchangeable biosimilar—one that FDA has determined can be substituted for the reference product at the pharmacy without prescriber intervention, mirroring the automatic substitution of small molecule generics—requires additional switching study data demonstrating no increased safety risk or decreased efficacy from alternating between the biosimilar and the reference product.

Interchangeability is commercially significant. Most U.S. state pharmacy substitution laws require interchangeability status before a pharmacist can substitute a biosimilar without prescriber authorization. Without it, market penetration depends on prescriber-driven switches, which are slower and more expensive to achieve.

The first interchangeable biosimilar approved in the U.S. was Semglee (insulin glargine-yfgn, Viatris/Biocon) in July 2021 for the reference product Lantus. The second was Cyltezo (adalimumab-adbm, Boehringer Ingelheim) in October 2021 against Humira. Both cases required specific switching study designs demonstrating stable safety and efficacy across multiple transitions between the biosimilar and the reference product.

Immunogenicity Assessment: The Technical Floor

Immunogenicity assessment is mandatory for all biosimilars and is among the most technically challenging components of the development program. Anti-drug antibody (ADA) formation can neutralize the therapeutic protein’s activity, alter its PK profile, or produce hypersensitivity reactions. Assessment requires:

Screening assays (electrochemiluminescence, ELISA, or bridging assay formats)

Confirmatory assays to eliminate false positives

Characterization assays to distinguish neutralizing from non-neutralizing ADAs

Clinical sampling plans spanning at least 12 months for chronically administered products

The critical regulatory expectation is that the immunogenicity risk profile of the biosimilar is no greater than that of the reference product. Comparability must be demonstrated statistically, and sample sizes in clinical studies must be powered to detect clinically meaningful differences in ADA incidence and neutralizing antibody rates.

Indication Extrapolation: Expanding Approval Without Redundant Trials

Indication extrapolation allows biosimilar approval for indications in which no direct clinical data was generated with the biosimilar, provided there is adequate scientific justification. The justification requires shared mechanism of action across indications, similar PK/PD profiles, comparable immunogenicity risk, and similar toxicity profiles.

Extrapolation is widely accepted by both FDA and EMA and is scientifically well-supported for many biologic drug classes. It is controversial in specific cases—for example, the extrapolation of biosimilar infliximab data from rheumatoid arthritis to inflammatory bowel disease raised questions from some gastroenterology societies about whether the mechanism of action is sufficiently similar across tissue compartments to justify extrapolation without IBD-specific clinical data. These controversies are worth tracking because payer and prescriber acceptance of extrapolated indications varies by therapeutic area and directly affects real-world market penetration.

FDA vs. EMA: Divergent Requirements and the Cost of Regulatory Fragmentation

FDA designates; state laws govern pharmacy substitution

EMA/HMA state scientific interchangeability; national bodies decide pharmacy substitution

Decision authority

FDA makes final approval decision

EMA recommends to European Commission for binding decision

Collaborative mechanism

FDA/EMA Parallel Scientific Advice (PSA) pilot (launched September 2021)

Same

For biosimilar developers targeting both markets, divergent clinical study requirements can mean separate patient population designs, distinct reference products (a U.S.-licensed reference biologic and an EU-authorized reference biologic may differ), and separate regulatory submissions with different data packages. The FDA/EMA Parallel Scientific Advice program allows simultaneous scientific dialogue with both agencies during development to reduce this divergence, but it remains a pilot program with limited uptake.

Key Takeaways: Regulatory Pathways

The ANDA pathway is efficient for standard bioequivalent products but creates high-stakes, high-cost litigation risk through the Paragraph IV certification system. Skinny-label carve-outs require rigorous active inducement risk analysis post-GSK v. Teva. The 505(b)(2) pathway enables differentiation and temporary exclusivity that simple ANDAs cannot generate. The biosimilar 351(k) pathway demands scientific investment well beyond standard BE studies, and interchangeability designation is the single most commercially impactful regulatory milestone a biosimilar developer can achieve. FDA/EMA regulatory fragmentation adds 15-25% to global biosimilar development budgets on average.

Investment Strategy: Regulatory Pathway Analysis

For portfolio managers: rank ANDA targets by probability-adjusted approval timeline, not just patent expiration date. Include FDA complete response letter (CRL) rate for the active ingredient category and the median approval cycle time for that formulation type. For biosimilar investments, model interchangeability approval as a separate value-creating event that justifies the additional switching study investment. 505(b)(2) assets should be valued using a brand-analog DCF framework, not a generics margin model, given their exclusivity protection.

4. Intellectual Property Valuation: The Asset Behind Every Patent Expiration

The Orange Book as a Financial Statement

The FDA Orange Book (Approved Drug Products with Therapeutic Equivalence Evaluations) lists every patent and exclusivity protecting a brand-name drug. For generic developers, it is the primary IP intelligence document—but it is incomplete and requires supplementation.

Orange Book listings are self-reported by NDA holders. Companies have both incentivized and debated what belongs in the Orange Book, and over-listing of patents (listing patents that may not actually claim the drug product itself) is a documented practice that forces generic companies into unnecessary Paragraph IV certifications and associated litigation costs. The FDA does not independently verify the validity of Orange Book listings against patent claims.

A comprehensive IP valuation for a generic target therefore requires: Orange Book data cross-referenced against the full text of each listed patent claim, analysis of prosecution history for claim scope limitations, a freedom-to-operate search for unlisted patents that may nonetheless cover the proposed generic formulation, and a review of inter partes review (IPR) petitions already filed against the listed patents.

Types of Pharmaceutical Patents and Their Strategic Weight

Pharmaceutical companies layer patents in a deliberate sequence designed to extend exclusivity from the initial compound discovery forward through the product lifecycle. Each layer has distinct IP valuation weight:

Compound patents cover the active pharmaceutical ingredient itself. They are filed earliest in the development cycle, typically 8-10 years before commercial launch, which means by the time a drug generates meaningful revenue, the effective commercial patent life on the compound is often only 10-12 years. Compound patents are the broadest and most valuable in the portfolio but are also the most contested by generic challengers.

Formulation patents cover specific pharmaceutical compositions—excipient combinations, release-modifying technologies, crystalline forms used in manufacturing. AstraZeneca’s quetiapine extended-release formulation (Seroquel XR) carries formulation patents that ran several years beyond the compound patent on quetiapine itself. These patents are narrower than compound patents and therefore more susceptible to design-around strategies by generic developers, but they require significant analytical investment to challenge.

Method-of-use patents cover approved therapeutic indications. They are the direct target of skinny-label carve-out strategies. Their commercial value to a brand-name company depends on whether the protected indication represents a dominant share of prescribing volume. If the patented indication accounts for 80% of actual use, a generic’s skinny label may capture only a fraction of the market and will still face active inducement risk if prescribers substitute the generic for the patented indication.

Polymorph patents cover specific crystalline forms of the active compound. The same chemical entity can exist in multiple solid-state structures—polymorphs, solvates, hydrates, amorphous forms—with different solubility, stability, and manufacturing characteristics. Patenting a polymorph that offers superior manufacturability or bioavailability extends exclusivity beyond the compound patent without any therapeutic innovation. Generic developers must either design around by selecting a different polymorph (if bioequivalence can be demonstrated) or challenge the validity of the polymorph patent. Roflumilast (Daliresp, AstraZeneca) and arformoterol (Brovana) both carry polymorph patents that generic developers were required to navigate.

Process patents cover manufacturing methods for the API or drug product. These are the least commercially significant for blocking generic entry because generic manufacturers are generally free to use alternative synthetic routes. However, process patents can matter if only one viable synthesis route exists for a complex molecule or if the patented process is essential to achieving required purity specifications.

IP Valuation Framework: Scoring a Generic Target

A systematic IP valuation for a chronic disease generic target should score the following factors:

Revenue at risk: Current brand-name annual net sales, adjusted for growth trends in the indication and any pending new competitive threats to the brand.

Patent complexity score: Number of listed patents, diversity of patent types (compound only versus compound plus formulation plus method-of-use plus polymorph), remaining patent lives, and assessed validity based on prior art searches and IPR history.

Paragraph IV challenge status: Number of generic filers already in the queue, litigation outcomes in analogous cases, and estimated time to resolution.

Authorized generic risk: History of the brand-name company executing authorized generic agreements with large generic manufacturers on the day of first generic entry.

Exclusivity overhang: Any running statutory exclusivity periods (pediatric exclusivity, NCE exclusivity, Orphan Drug exclusivity) that extend beyond patent expiration and block ANDA approval regardless of patent status.

Regulatory complexity: FDA review cycle time for the specific dosage form, known bioequivalence study challenges, and the presence or absence of product-specific guidance.

This multi-factor scoring produces a net opportunity value per generic target that is more useful than a simple “patent expires in 18 months” shorthand.

Key Takeaways: IP Valuation

The Orange Book provides the starting point for IP analysis, not the conclusion. Compound, formulation, method-of-use, polymorph, and process patents each require distinct challenge strategies and carry different litigation risk profiles. Authorized generic agreements and running exclusivity periods can negate the commercial value of a first-filer patent win. Systematic IP valuation scoring allows portfolio managers to prioritize ANDA investments by risk-adjusted NPV rather than surface-level patent expiration timing.

5. Evergreening Technology Roadmap: How Innovators Delay Your Entry

Evergreening is not a single tactic. It is a layered program that brand-name companies execute in parallel, with each element designed to reinforce the others. Understanding the full roadmap is essential for generic IP teams evaluating a target.

Layer 1: The Formulation Switch (Product Hopping)

Product hopping refers to a brand company transitioning market focus from an existing formulation to a new one—typically from immediate-release to extended-release, or from capsule to tablet—before the primary compound patent expires. The new formulation carries its own patent protection and, if the brand successfully migrates prescriber habits to the new version before the original formulation goes generic, the original formulation becomes commercially irrelevant even after generic entry.

Namenda (memantine, Allergan/Forest) is the textbook example. Forest Laboratories converted the market from immediate-release Namenda to once-daily Namenda XR before the IR compound patent expired, then announced it would discontinue IR Namenda. When a court rejected the discontinuation strategy as anticompetitive (NY v. Actavis), Forest settled and allowed continued IR availability. Still, the XR conversion extended meaningful branded revenue by several years.

Copaxone (glatiramer acetate, Teva) underwent a similar switch from a 20 mg/mL daily injection to a 40 mg/mL three-times-weekly formulation before multiple generic manufacturers could capture the original formulation market. Teva invested heavily in promoting the 40 mg/mL version to neurologists and patients, and by the time generics for the 20 mg/mL version launched, Teva had already migrated a significant proportion of its patient base to the protected formulation.

Layer 2: Patent Thickets

A patent thicket is a dense, overlapping cluster of patents covering multiple aspects of a single drug product simultaneously. The commercial objective is to ensure that no generic company can enter the market by challenging only one or two patents; the generic must defeat the entire thicket before receiving final approval.

The Humira (adalimumab, AbbVie) patent thicket reached 250+ U.S. patents by 2020. The patents covered the antibody sequence itself, formulation components (high-concentration aqueous solutions, citrate-free formulations to reduce injection site pain), manufacturing processes (cell culture conditions, purification methods), dosing regimens (specific clinical protocols), and the autoinjector device design. Biosimilar developers entering the U.S. market needed to analyze and either design around or litigate each relevant cluster, with the result that AbbVie was able to negotiate global patent settlements with multiple biosimilar manufacturers, delaying U.S. entry entirely until January 2023—more than five years after European biosimilar entry.

The thicket strategy works because litigation is expensive and time-consuming for the challenger. Each additional patent added to the thicket increases the cost and timeline of generic entry, even if individual patents have low probability of being sustained on validity challenge. The goal is not to win every patent case; it is to make the total cost of entry high enough to deter or delay competition.

Layer 3: Pediatric Exclusivity Gaming

The Best Pharmaceuticals for Children Act (BPCA) grants six additional months of exclusivity on all existing patents and exclusivities when a brand company conducts pediatric clinical studies in response to an FDA written request. The six-month extension applies to all forms and formulations of the active moiety in the Orange Book.

While pediatric studies represent legitimate scientific value for drug safety data in children, the extension has been used strategically for drugs with minimal pediatric use but large adult markets. For a drug generating $2 billion annually, six additional months of exclusivity is worth approximately $1 billion in retained revenue. The cost of the pediatric clinical program is rarely above $30-50 million. The return on investment for pediatric exclusivity obtained at the right point in the drug’s lifecycle is among the highest in pharmaceutical strategy.

Reverse payment settlements, colloquially called “pay-for-delay” agreements, involve the brand-name company paying the first-filing generic manufacturer to drop its Paragraph IV patent challenge and delay market entry until a negotiated future date. These settlements can take the form of cash payments or other value transfers such as authorized generic agreements, supply agreements, or co-promotion deals.

The Supreme Court addressed pay-for-delay in FTC v. Actavis (2013), holding that such settlements can be subject to antitrust scrutiny under a “rule of reason” standard. Post-Actavis, the FTC has continued to monitor and challenge settlements it views as anticompetitive, and several have been unwound or restructured. The legal exposure has reduced the frequency of large cash payments but not eliminated the practice.

For generic developers, a competitor’s settlement is both an opportunity and a warning. It signals that the settling generic considers the patent stronger than its challenge suggests, and it narrows the competitive field by removing a first-filer from the day-one launch window. Monitoring settlement filings via DOJ and FTC databases is a standard component of competitive intelligence for generic strategy.

Layer 5: Citizen Petition Tactics

Brand-name companies file citizen petitions with the FDA requesting that the agency impose additional requirements on generic applicants—new study designs, additional safety data, or revised bioequivalence criteria. While many citizen petitions raise legitimate scientific issues, others are filed close to generic approval timelines with the evident purpose of delaying approval.

The FDA Reauthorization Act of 2017 (FDARA) gave FDA authority to summarily deny a citizen petition filed with “the primary purpose of delaying the approval of an application.” The agency has invoked this authority on several occasions, but citizen petitions remain a routine element of the brand defense playbook and introduce procedural delay risk that generic developers must account for in their launch planning.

Evergreening Technology Roadmap: Summary Timeline

The following describes how a brand company typically sequences these tactics across a drug’s lifecycle:

Year 0-3 post-launch: Build primary compound patent protection; begin formulation optimization R&D to generate patentable line extensions.

Year 4-8: File formulation, polymorph, and method-of-use patents. Begin pediatric clinical program if a written request is obtainable.

Year 8-12: Execute product hop to new formulation if commercially viable; invest in patient and prescriber migration to new version. Begin preliminary authorized generic negotiations with large generic partners.

Year 12-15: Patent expiry window. File citizen petitions on incoming ANDA applications. Manage Paragraph IV litigation strategy; assess reverse payment settlement economics for first-filer. If settled, control the authorized generic launch timing.

Year 15+: Compound patent fully expired; manage formulation and method-of-use patent litigation for later-expiring protection layers.

Key Takeaways: Evergreening

Generic IP teams should map all five layers for any target exceeding $500 million in annual brand revenue. Product hopping can make the targeted formulation commercially irrelevant even after legal market entry; assess prescribing migration data before committing ANDA development resources. Patent thickets require a coordinated IPR + design-around strategy, not sequential single-patent challenges. Pediatric exclusivity can add six months to any timeline and must be factored into launch date projections. Post-Actavis, reverse payment settlements require monitoring but remain a competitive intelligence input.

6. The Patent Cliff: Identifying and Capturing High-Value Windows

What a Patent Cliff Actually Is

The pharmaceutical industry uses “patent cliff” to describe periods when multiple high-revenue branded drugs lose exclusivity within a compressed timeframe, creating a concentrated wave of generic opportunities. The 2010-2015 cliff—during which Lipitor (atorvastatin), Plavix (clopidogrel), Seroquel (quetiapine), Lexapro (escitalopram), and others lost protection—accelerated tens of billions of dollars from brand to generic revenue.

For generic manufacturers, a patent cliff is predictable years in advance. The core data—patent expiration dates, running exclusivity periods, number of ANDA filers—is publicly available and aggregable. The competitive challenge is not identifying the cliff; it is executing faster and better than every other generic company that identified the same opportunity.

Lipitor: The Benchmark Patent Cliff Case

Atorvastatin calcium (Lipitor, Pfizer) lost its U.S. compound patent protection in November 2011 after generating peak annual revenues of $13 billion. The patent cliff analysis several years prior identified atorvastatin as the single most valuable generic opportunity in history at that time.

Ranbaxy (now Sun Pharma) had secured first-filer status through a Paragraph IV certification and successfully prevailed in the patent litigation, entitling it to 180 days of generic exclusivity. However, several complications compressed the financial benefit:

The FDA issued Ranbaxy a consent decree in 2012 related to manufacturing violations at Indian facilities, forcing Ranbaxy to source the product from a compliant site and delaying full commercial launch.

Pfizer launched an authorized generic through Greenstone (its own subsidiary) on day one of generic availability, effectively splitting the 180-day exclusivity period with Ranbaxy and preventing Ranbaxy from capturing the full 180-day premium.

Within 10 months of generic entry, atorvastatin prices had fallen more than 90% as Watson, Mylan, Teva, and a dozen other generics received approvals.

The atorvastatin case illustrates that being the first-filer is necessary but not sufficient for realizing the full financial value of a patent cliff opportunity. Manufacturing qualification, authorized generic risk, and the speed of subsequent ANDA approvals all determine actual realized revenue.

The 180-Day Exclusivity Mechanics

The 180-day exclusivity period for the first ANDA Paragraph IV filer does not run automatically from approval. It is triggered by the earlier of: (1) the date of the first commercial marketing of the generic drug by the first applicant, or (2) a court decision holding the patent invalid, unenforceable, or not infringed (if the first applicant is the successful litigant).

Forfeiture provisions complicate the exclusivity. The first applicant forfeits 180-day exclusivity if it fails to market within 75 days of a final court decision or FDA approval (whichever is later), among other triggers. Patent-related forfeiture provisions were added by the Medicare Prescription Drug, Improvement, and Modernization Act (MMA) of 2003 after it became clear that some first-filers were sitting on their exclusivity rights without marketing, effectively blocking all other generics from entering.

Upcoming Patent Cliff Opportunities in Chronic Disease

The 2024-2030 period includes several high-value patent expirations in chronic disease categories. Without providing specific current data (recommend verifying with DrugPatentWatch for real-time expiration dates and ANDA filing counts), the categories with the highest volume of expiring protection include:

Diabetes: Several GLP-1 receptor agonists and SGLT-2 inhibitors have entered or are entering their patent exclusivity windows, though the biosimilar and complex generic development required for some formulations extends effective competition timelines significantly.

Cardiovascular: Anticoagulants, antiplatelets, and newer lipid-lowering agents have active patent expiration timelines through 2030.

Respiratory/Immunology: Several biologic agents used in asthma, COPD, and associated comorbidities have biosimilar development programs underway.

CNS: Several branded CNS drugs for depression, anxiety, and neurodegenerative disorders have ANDA pipelines building ahead of patent expirations.

Key Takeaways: Patent Cliff Strategy

First-filer status requires a combination of precise patent expiration timing intelligence, early ANDA filing capability, and litigation readiness. Manufacturing qualification at the time of approval is a non-negotiable requirement for capturing the financial value of exclusivity. Authorized generic risk must be priced into any 180-day exclusivity NPV model. DrugPatentWatch and comparable patent intelligence platforms are the operational tools for building and maintaining this pipeline across all major therapeutic areas.

Investment Strategy: Patent Cliff Positioning

For institutional investors: generic companies with disclosed first-filer positions in chronic disease categories approaching patent expiration represent a predictable, near-term catalyst that can be modeled with reasonable precision from public ANDA filing data and Orange Book patent records. Monitor FDA tentative approval announcements, which confirm that manufacturing and regulatory requirements are substantially met and that only patent/exclusivity barriers remain to commercial launch.

7. Manufacturing Excellence and Supply Chain Resilience

cGMP as Competitive Differentiator, Not Just Compliance Requirement

Current Good Manufacturing Practices (cGMP) requirements apply equally to brand-name and generic manufacturers—but in the generic market, where products are chemically identical, manufacturing quality is among the few remaining competitive differentiators. A generic manufacturer with a pristine compliance record, no outstanding Form 483 observations, and no Warning Letters attracts formulary preference from large payers and health systems that have been burned by quality-related shortages.

The FDA inspects manufacturing facilities on a risk-based schedule. Import alerts and consent decrees—formal enforcement actions requiring specific remediation before the FDA will approve new drug applications from a facility—are among the most commercially damaging events a generic company can experience. Ranbaxy’s consent decree in 2012 and subsequent criminal settlement, along with similar enforcement actions against Wockhardt (2013) and other Indian manufacturers, demonstrated that quality failures carry existential financial consequences, not merely regulatory inconvenience.

The generic industry’s global manufacturing concentration in India and China creates persistent quality monitoring obligations. FDA’s Office of Pharmaceutical Quality publishes inspection databases and compliance action histories that serve as practical screening tools for supply chain risk management.

Continuous Manufacturing: The Quality and Cost Efficiency Paradigm Shift

Traditional batch manufacturing in pharmaceuticals requires sequential, discrete unit operations—blending, granulation, drying, compression, coating—each performed in separate equipment with manual transfers and intermediate testing. Batch sizes are fixed, and deviations require the entire batch to be held pending investigation.

Continuous manufacturing integrates these unit operations into an uninterrupted process flow with real-time monitoring via Process Analytical Technology (PAT) sensors—Raman spectroscopy, near-infrared spectroscopy, particle size analyzers—that provide immediate feedback on process parameters and product quality attributes. The result is real-time release testing capability, reduced cycle times (from 30+ days to as few as 5 days for some products), smaller physical footprint, lower direct labor costs, and improved batch-to-batch consistency.

FDA has actively promoted continuous manufacturing adoption as a supply chain resilience tool, recognizing that the technology’s real-time quality monitoring and flexible production capacity make it better suited to responding to demand surges or supply disruptions. Janssen (Johnson & Johnson) received the first FDA approval for a product manufactured via continuous manufacturing—darunavir—in 2016. Since then, approvals for continuous manufacturing processes have accelerated across multiple companies including Vertex, Eli Lilly, and several generic manufacturers.

For generic manufacturers, the capital investment in continuous manufacturing ($10-30 million per production line) is justified by the lifecycle savings in batch failures, cycle time reduction, and the competitive differentiation of a documented quality advantage. Companies like Amneal and Sandoz have invested in continuous manufacturing capabilities specifically to address the high-volume, quality-sensitive segments of the generic market.

Drug Shortages: The Market Failure Hidden in the Pricing Model

The U.S. experienced 270 active drug shortages in 2025. The FDA received 731 supply chain issue reports from manufacturers between 2017 and 2021, with 113 producing meaningful shortages. The majority involved generic drugs. The median shortage duration for essential generic medicines—those on the FDA’s Essential Medicines List or equivalents—is 4.0 years. That is not a supply chain disruption; it is a structural failure.

The root cause is well-understood: intense price competition drives generic drug margins to levels that cannot support investment in redundant manufacturing capacity, buffer inventory, or facility modernization. When a single manufacturer experiences a quality event, the concentrated supply base has no capacity slack to absorb the shortfall.

The valsartan contamination crisis of 2018 illustrates the cascade. N-nitrosodimethylamine (NDMA) contamination was discovered in valsartan API produced at Zhejiang Huahai Pharmaceuticals in China. Multiple finished-dose manufacturers used this API supplier. The FDA recall covered over 30 different valsartan products from multiple manufacturers simultaneously. Even though alternative antihypertensives existed, they were not therapeutically identical for all patients—particularly those with heart failure or post-MI protocols where valsartan is a guideline-directed therapy. The shortage lasted years and had documented adverse health effects.

The strategic and policy response has multiple components: the Civica Rx and CivicaScript models (nonprofit generic manufacturing cooperatives owned by health systems and philanthropic investors), state-level generic drug reserve stockpile programs, BARDA’s Essential Medicines initiatives targeting domestic manufacturing for critical products, and FDA fee waivers and expedited review for applicants willing to establish U.S. manufacturing for shortage drugs.

Domestic Manufacturing: Economic Case and Limitations

The economic case for domestic generic drug manufacturing is improving but not yet fully competitive with Indian and Chinese APIs on a pure cost basis. Labor and facility costs in the U.S. remain higher than in South and Southeast Asia. The offset comes from reduced regulatory risk (FDA facility proximity reduces inspection cycle time), lower supply chain lead times (weeks versus months), and insurance value against geopolitical supply disruption—a concern that became concrete during COVID-19 PPE and active ingredient shortages in 2020.

BARDA’s domestic manufacturing investment programs, the Drug Security Innovation Act proposals, and the Bipartisan Safer Medicines Partnership are policy instruments designed to close the economic gap through procurement preferences, grants, and tax credits for domestic manufacturing. For generic companies evaluating manufacturing footprint decisions, modeling domestic versus offshore with the full risk-adjusted cost—including shortage probability, quality enforcement risk, and lead-time-related inventory carrying cost—often produces a closer comparison than a simple unit cost analysis.

Key Takeaways: Manufacturing and Supply Chain

cGMP compliance and continuous manufacturing adoption are increasingly differentiating strategic assets, not commodity cost centers. Drug shortages in generic markets are a structural consequence of pricing dynamics, not random disruptions. IP teams and portfolio managers evaluating generic targets should include manufacturing supply concentration risk in their opportunity assessments—a product with 90% of API sourced from a single country with documented quality enforcement history carries real commercial risk that must be discounted in valuation models. Domestic manufacturing is becoming economically viable with policy support and full risk-adjusted cost accounting.

8. Market Dynamics: PBMs, Price Erosion, and the IRA Wildcard

Price Erosion Curves: The Quantitative Reality

Generic price erosion follows a predictable curve, driven by the number of approved competitors:

Generic Competitors

Average Price vs. Brand

1 (first generic, 180-day exclusivity)

60-80% of brand price

2

46% of brand price

5

21% of brand price

6+

5-10% of brand price

This curve has profound implications for investment timing. The first generic captures the majority of the available margin premium. By the time six competitors are approved—often within 12-24 months of first generic entry for a large-volume product—the market has largely become a manufacturing cost and logistics efficiency competition.

For chronic disease medications that generate $1 billion or more in brand revenue, even the commodity pricing phase represents hundreds of millions in annual revenue across all generic participants. But individual company economics at that phase depend entirely on manufacturing efficiency and volume scale.

Pharmacy Benefit Managers: The Layer That Obscures Generic Savings

PBMs manage prescription drug benefits for approximately 270 million Americans through three dominant companies: CVS Caremark, Express Scripts (Cigna), and OptumRx (UnitedHealth). Their formulary placement decisions—which drugs are covered, at what tier, with what cost-sharing—determine whether patients fill generic prescriptions at all.

The theoretical value proposition of generic drugs is straightforward: cheaper than brand, same therapeutic effect, better adherence. The PBM layer complicates that value proposition in several documented ways.

Spread pricing occurs when a PBM reimburses a pharmacy a defined amount for a dispensed generic but charges the insurer a higher amount, retaining the difference as revenue. A 2019 Ohio Medicaid audit found that PBMs charged the state $224.8 million more than they reimbursed pharmacies for prescription drugs over a two-year period, a significant portion of which involved generic drugs. Multiple states have since enacted spread pricing prohibitions for Medicaid managed care.

Formulary management creates variable patient cost-sharing for generics based on tier placement. Even though a generic drug may cost the PBM or health plan $2 per fill, the patient may face a $20-50 copayment if the drug is placed on a non-preferred generic tier. In 2022, 54% of Medicare Part D enrollees paid more than $2 for at least one generic prescription fill, and over 12% paid more than $20. That variability undermines the adherence benefit that generic drugs exist to deliver.

Generic “clawbacks”—where PBMs recover reimbursements from pharmacies via “direct and indirect remuneration” (DIR) fees—further complicate the economics of generic dispensing for pharmacies, sometimes resulting in pharmacy reimbursement below acquisition cost. When pharmacies cannot profitably dispense a generic, they have reduced incentive to substitute generics and may steer patients toward more profitable brand drugs.

The Inflation Reduction Act: Unintended Consequences for Generic Economics

The Inflation Reduction Act (IRA) of 2022 introduced Medicare drug price negotiation—the federal government’s ability to directly negotiate Maximum Fair Prices (MFPs) for a defined list of high-expenditure brand drugs. The policy objective is reducing brand drug costs for Medicare beneficiaries.

The mechanism creates an indirect risk for generic manufacturers. When MFPs are set significantly below current brand list prices, they narrow the price differential between brand and generic drugs. If a brand drug’s negotiated MFP approaches generic market pricing, the financial incentive for manufacturers to develop and maintain generic products in that category erodes. Payers may also prefer the price-negotiated brand over generics if the cost difference becomes minimal, undermining generic formulary preference that drives volume.

The Congressional Budget Office and several independent analyses have modeled the generic market impact as modest in the near term, given that IRA negotiation initially targets drugs without generic competition (a qualification requirement under the statute). However, as the negotiated drug list expands over time, the potential for downstream effects on generic pipeline investment is real and requires active monitoring by generic industry stakeholders.

Policy reforms targeting PBM transparency—requiring pass-through rebate models, prohibiting spread pricing in government programs, and mandating DIR fee reporting—are advancing at both federal and state levels. These reforms, if implemented broadly, would increase the patient-level cost savings delivered by generic drugs and improve adherence rates, strengthening the public health and commercial case for generic development.

Key Takeaways: Market Dynamics

Price erosion timelines are largely determined by ANDA filing counts and can be modeled from public FDA databases. PBM opacity reduces the realized patient-level value of generic drugs and creates adherence barriers that cost the system more than the generic savings deliver. The IRA’s MFP mechanism requires ongoing analysis for each generic pipeline target in relevant therapeutic areas. PBM transparency reform is the most structurally significant policy development for improving generic drug value delivery.

Investment Strategy: Pricing and Policy

For portfolio managers: model generic drug NPV with explicit price erosion scenario analysis (optimistic: 2 competitors at launch; base: 4 competitors within 12 months; conservative: 6+ competitors within 18 months). Flag any IRA drug list overlap in the pipeline and assess the MFP negotiation risk to the category’s long-term generic economics. Monitor PBM reform legislation quarterly for implications on formulary structure.

9. Patient and Physician Perceptions: The Last-Mile Problem

The Credibility Gap Between Scientific Equivalence and Clinical Practice

FDA’s official position is that all approved generic drugs are as safe and effective as their brand-name counterparts. The scientific basis for that position—rigorous bioequivalence standards, cGMP manufacturing requirements, Orange Book therapeutic equivalence ratings—is sound. Yet patient and physician reluctance toward generic substitution persists in specific contexts.

The reluctance concentrates in predictable areas. Narrow therapeutic index drugs—warfarin, levothyroxine, antiepileptics, immunosuppressants, lithium—generate the most clinically meaningful concern. For these drugs, even modest AUC or Cmax variability within the 80-125% bioequivalence window can produce clinical events. A patient stabilized on warfarin at a specific international normalized ratio (INR) may need dose adjustment when switching to a new generic formulation, not because the generic is inferior, but because normal PK variability means individual patient response can shift with any formulation change.

For most drugs, this concern is not clinically justified. Bioequivalence at the population level is robust, and any specific patient’s experience of “feeling different” after a generic switch is more likely to reflect differences in tablet appearance, taste, or pill burden than actual pharmacological differences. Placebo-nocebo effects are well-documented in generic switching contexts.

The practical commercial challenge is that physician prescribing inertia and patient preference both cost generic companies prescriptions. A neurologist who has seen one patient require dose adjustment after a generic antiepileptic switch may develop a durable habit of writing “brand medically necessary” for all antiepileptic prescriptions.

Demographic Concentration of Negative Perceptions

Research consistently finds generic drug skepticism concentrated among elderly patients, racial and ethnic minorities, and individuals with lower health literacy. The CDC has documented that Black patients in rural Alabama showed significantly higher skepticism about generic drug safety than white patients in the same population, controlling for socioeconomic status. Elderly patients are more likely to notice and report symptoms associated with pill appearance changes (different color, different size) and attribute them to efficacy differences.

These are not trivial commercial challenges. Generic companies targeting cardiovascular and diabetes medications—the highest-volume chronic disease categories—are marketing to populations with disproportionate representation of elderly and minority patients.

Communication Strategies That Work

The most effective interventions in the literature for improving generic acceptance combine prescriber education with pharmacist counseling at the point of dispensing. Pharmacists who proactively explain to patients why the pill looks different and reassure them that the active ingredient is identical achieve measurably higher acceptance rates and lower callback rates than pharmacies that simply dispense without explanation.

For generic manufacturers, digital marketing directed at prescribers and patients can accelerate adoption. SEO-optimized educational content targeting terms physicians and patients search around specific drug substitutions, combined with clinical detailing that presents bioequivalence data alongside adherence outcome data, builds the confidence that drives sustained prescribing. The atorvastatin generic launches demonstrated that targeted cardiologist outreach with outcome data achieved faster market penetration than pure price messaging.

Key Takeaways: Perceptions

Perception management is a commercial priority, not a secondary concern. Narrow therapeutic index drugs require active physician communication strategies to prevent systematic “brand medically necessary” notation. Pharmacist-level counseling is the most cost-effective last-mile intervention for generic acceptance. Demographic-targeted educational programs are both ethically appropriate and commercially sensible for high-prevalence chronic disease markets.

10. Strategic Opportunities: Super Generics, Biosimilars, and AI-Driven Development

Super Generics and Value-Added Formulations

The generic industry is bifurcating. One segment competes on manufacturing cost efficiency and speed-to-market for commoditized small molecule ANDAs, operating on sub-5% net margins. The other segment—sometimes called “value-added generics” or “super generics”—develops differentiated follow-on products that offer genuine improvements in patient experience or clinical outcomes and command pricing power that standard generics cannot achieve.

Value-added generics typically use one of several platform technologies:

Extended-release systems (matrix tablets, osmotic pump delivery, multi-particulate systems) that reduce dosing frequency from twice-daily or three-times-daily to once-daily. Patient adherence data consistently shows that once-daily regimens achieve meaningfully higher compliance rates than more frequent dosing schedules, which is a clinically relevant benefit, not just a convenience feature.

Long-acting injectable (LAI) formulations using microsphere technology (PLGA polymer-based), implantable rods, or nanocrystal suspensions that extend drug release from days to weeks or months. LAIs in psychiatry—for antipsychotics like risperidone and paliperidone—address one of the most expensive adherence failures in all of medicine: patients with schizophrenia who do not take oral medications consistently have dramatically higher hospitalization rates. Developing generic LAI formulations for established antipsychotics is technically challenging but commercially compelling.

Transdermal delivery systems that bypass hepatic first-pass metabolism, allow for dose titration, and improve tolerability for compounds with GI side effects. Generic transdermal patches require not only PK bioequivalence but also skin adhesion performance data and dermal safety studies—a higher development bar that limits competition.

Liposomal formulations that alter a drug’s distribution, toxicity profile, or site-specific delivery. Liposomal doxorubicin (Doxil) in oncology is the reference example of how a liposomal formulation produces a meaningfully different clinical profile from free drug. Generic liposomal formulations require complex manufacturing characterized by particle size distribution, lamellarity, encapsulation efficiency, and drug release kinetics—all parameters with no simple bioequivalence analog.

Biosimilar Pipeline Priorities in Chronic Disease

The biologics with the highest biosimilar development priority in chronic disease categories are those combining large reference product revenue with expiring or recently expired exclusivity:

Adalimumab biosimilars for rheumatoid arthritis, psoriasis, and inflammatory bowel disease are now commercially launched in the U.S. with multiple biosimilars approved. Penetration is building but slower than European markets due to formulary management and prescriber inertia.

Ustekinumab (Stelara, Johnson & Johnson) biosimilars are advancing through development programs with U.S. exclusivity expiration occurring in 2023. Several companies have 351(k) applications in FDA review. Stelara generated approximately $10 billion in global annual revenue at peak, making it among the most commercially significant biosimilar targets.

GLP-1 receptor agonists (semaglutide, liraglutide) are complex polypeptides that occupy a transitional category between small molecules and large biologics. Their patent landscapes and regulatory pathways are under active development, and the commercial opportunity given the obesity and diabetes epidemic is enormous.

Insulin analogues (glargine, lispro, aspart) have established biosimilar markets in the U.S. and EU, but market penetration has been slower than expected due to PBM formulary management favoring brand insulins supported by large rebate agreements.

AI and Machine Learning: Where the Technology Actually Delivers

Artificial intelligence applications in generic development fall into two categories: those with demonstrated value and those that remain aspirational.

Demonstrated value: Computational prediction of polymorphic forms, solubility enhancement strategies, and excipient compatibility for oral solid dose formulations. Machine learning models trained on physicochemical data can reduce the number of failed formulation iterations in early development, cutting 3-6 months from development timelines. Predictive ADME modeling can flag potential bioequivalence challenges before costly clinical studies are initiated.

AI-driven market analysis: Predictive models for generic market entry timing, pricing trajectories, and prescriber switching likelihood based on historical launch data. McKinsey analysis attributed 20% higher six-month market penetration to companies using predictive launch analytics versus those relying on conventional market research.

Supply chain optimization: Machine learning applied to demand forecasting for generic drugs reduces inventory carrying costs and improves production scheduling efficiency in continuous manufacturing environments.

Still aspirational: End-to-end in silico bioequivalence prediction that would replace clinical PK studies. The FDA’s current position requires pharmacokinetic data in humans for ANDA bioequivalence; computational models, however sophisticated, do not yet meet this evidentiary bar. Companies marketing AI-powered ANDA development shortcuts that claim to eliminate clinical studies are overstating current regulatory acceptability.

Key Takeaways: Strategic Opportunities

The highest-value generic portfolio segments are value-added generics (LAIs, liposomal formulations, complex transdermal systems) and biosimilars (particularly high-revenue biologics with expiring BPCIA exclusivity). AI delivers measurable ROI in formulation development, market analytics, and supply chain optimization but does not eliminate the clinical study requirements that define regulatory pathways. Companies building capabilities in continuous manufacturing, analytical characterization for complex products, and AI-driven launch analytics are building durable competitive advantages beyond price.

Investment Strategy: Biosimilar Positioning

For institutional investors evaluating biosimilar developers: assess the company’s analytical characterization platform depth, not just its clinical pipeline. The ability to generate high-resolution comparability data (glycan profiling, higher-order structure characterization via hydrogen-deuterium exchange mass spectrometry) is a leading indicator of regulatory dossier quality that precedes FDA approval by 3-4 years. Companies with this depth are more likely to achieve interchangeability designation, the highest-value biosimilar regulatory milestone.

11. Generic Launch Playbook: Case Studies and Best Practices

Teva’s Sildenafil Launch (2017): The Market Capture Blueprint

Pfizer’s Viagra (sildenafil citrate 100mg) lost its compound patent in December 2017. Teva Pharmaceuticals, having secured first-filer status, launched generic sildenafil at approximately $35 per pill against the brand price of $65—an aggressive but not deep discount designed to capture prescriber and patient switching without triggering immediate brand price matching.

Teva’s launch strategy concentrated physician-directed promotion on urologists and primary care physicians with the highest sildenafil prescribing volume, using script-level prescribing analytics to identify and tier targets. The campaign centered on data demonstrating bioequivalence and cost savings, not general awareness. Within 12 months, Teva had captured approximately 70% of the combined brand-plus-generic sildenafil prescription volume. That market share position deteriorated as additional generics received approval and prices fell toward commodity levels, but the first-year revenue generation from the exclusivity period justified the launch investment many times over.

The lesson: first-filer generic launches require a commercial infrastructure that looks more like a brand launch than a typical ANDA rollout. Physician segmentation, detail force deployment, and data-driven prescriber targeting are not optional overhead; they are the mechanism for converting regulatory exclusivity into revenue capture before the exclusivity window closes.

Zarxio (Filgrastim-sndz): Building the Biosimilar Playbook

Sandoz launched Zarxio (filgrastim-sndz) as the first FDA-approved biosimilar in the U.S. in September 2015 against Amgen’s Neupogen. The launch encountered several structural headwinds that subsequent biosimilar developers have learned from:

Formulary barriers were significant. Many oncology practices and health systems had existing supply agreements with Amgen that created friction for Zarxio adoption. Sandoz invested heavily in payer contracting to achieve formulary parity.

Physician education was the primary commercial challenge. Oncologists treating cancer patients undergoing chemotherapy-induced neutropenia are cautious about therapeutic substitution. Sandoz deployed medical affairs resources alongside its sales force to present the clinical data package supporting biosimilarity and to build physician confidence.

Pricing was set at approximately 15% below Neupogen at launch—shallower than small molecule generic pricing reflects, consistent with the lower competitive intensity and higher development cost structure of biosimilars.

Zarxio achieved meaningful market penetration but the pace was slower than initially projected. The case validated that biosimilar launches require sustained commercial investment over multiple quarters, not the single-quarter market capture that characterizes small molecule generic launches.

Truxima (Rituximab-abbs): Distribution Partnership as Launch Accelerant

Celltrion’s Truxima (rituximab-abbs) became the first Rituxan (rituximab) biosimilar approved in the U.S. in November 2019. Celltrion partnered with Teva Pharmaceuticals for U.S. commercialization, leveraging Teva’s established oncology distribution network and payer relationships.

The partnership model allowed Truxima to reach payer formularies and hospital pharmacy supply agreements faster than Celltrion could have accomplished independently as a biosimilar-only developer without a scaled U.S. commercial infrastructure. The rituximab biosimilar market subsequently attracted additional entrants (Ruxience from Pfizer, Riabni from Genentech’s own program), and the competitive landscape evolved toward the price-step-down dynamic that eventually brings biosimilar pricing to 30-40% below reference product levels.

The Truxima case is the template for biosimilar developers without U.S. commercial scale: identify a commercialization partner with established oncology or specialty pharmacy infrastructure, structure the partnership with economics that reflect the partner’s commercial value, and invest in payer access activities before launch rather than after.

Key Takeaways: Launch Strategy

First-filer generic launches require commercial investment proportional to the exclusivity window’s financial opportunity—under-investing is the most common failure mode. Biosimilar launches require sustained commercial effort over 6-12 months, not a single quarter push. Distribution partnerships can accelerate biosimilar market access when the developer lacks U.S. commercial infrastructure. Market data platforms that segment prescribers by script volume and switching propensity are the operational tools that translate launch investment into revenue capture.

12. Master Key Takeaways and Investment Strategy

The Integrated Strategic Picture

The generic pharmaceutical market for chronic disease medications is not a monolithic industry. It is a spectrum of asset types—commodity small molecule ANDAs, high-value first-filer exclusivity plays, complex generic formulation programs, and biosimilar development campaigns—each with distinct economics, risk profiles, and competitive dynamics.

Chronic disease demand fundamentals are structurally favorable: NCD prevalence is increasing globally, healthcare budgets are under cost pressure in every developed market, and payer policies that drive generic substitution will intensify rather than moderate. The secular tailwind is real.

The tactical challenges are equally real. Patent thickets and evergreening tactics require sophisticated IP monitoring and litigation capability. Biosimilar development demands $100M+ capital and 7-8 years of scientific execution. Complex generic development requires formulation science expertise and regulatory navigation skills that most manufacturers do not have. Supply chain fragility is a structural market failure that creates both risk and opportunity.

Companies that are building capabilities in IP intelligence, complex formulation science, continuous manufacturing, analytical characterization for biologics, and AI-driven commercial analytics are positioning for the next decade’s competitive dynamics. Companies that remain in commodity small molecule production are facing sustained margin compression.

Key Strategic Decisions for Each Stakeholder