The most consequential commercial event in biopharma over the next decade is not a drug approval or a clinical trial readout. It is the convergence of two slow-moving structural forces: the patent expiration of the world’s highest-revenue biologics and the accelerating healthcare demand driven by aging populations across East and Southeast Asia.

Between 2025 and 2032, biologics generating a combined estimated $200 billion in annual global revenue face patent cliffs. The list includes Humira (adalimumab), Stelara (ustekinumab), Keytruda (pembrolizumab), Opdivo (nivolumab), Eylea (aflibercept), and the entire oncology immunotherapy stack that reshaped medicine over the past fifteen years. Each of these molecules is protected not by a single patent but by layered intellectual property portfolios, and the precise shape of each cliff — when it starts, how steep it is, and in which jurisdiction it occurs first — differs materially by country.

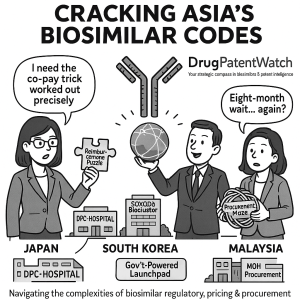

Japan, South Korea, and Malaysia occupy distinct positions in this commercial landscape. Japan, the world’s third-largest pharmaceutical market at roughly $90 billion in annual drug spend, offers the highest realized revenue per approved product but runs one of the most counterintuitive reimbursement systems in the world. South Korea, with an estimated $22 billion biopharma market, has transformed itself through deliberate state capitalism into the second-most prolific source of FDA-approved biosimilars globally, behind only the United States itself. Malaysia, a $900 million combined generic-and-biosimilar market growing at a steady 4% CAGR, is at a structural inflection point: regulation is mature, procurement is broken, and the gap between those two facts is both the central challenge and the central opportunity.

This guide provides the granular technical, regulatory, IP, and commercial intelligence needed to build a winning strategy in each arena.

Part I — The Biosimilar Blueprint: Science, Manufacturing, and IP Creation

What a Biosimilar Is (and Isn’t)

The ‘Similar, Not Identical’ Standard and Why It Matters for IP

A biosimilar is a biological medicine approved on the basis that it is highly similar to an already-approved reference biologic, with no clinically meaningful differences in safety, purity, or potency. The FDA, EMA, PMDA, MFDS, and NPRA are aligned on this definition, even as their specific evidentiary requirements diverge in the details.

The word ‘similar’ is not a regulatory hedge. It reflects a hard scientific reality. Biologics are produced in living cell systems — most commonly Chinese Hamster Ovary (CHO) cells for mammalian-expressed proteins, or Escherichia coli and Saccharomyces cerevisiae for simpler structures. No two cell lines, even those expressing the same coding sequence, produce an identical glycoprotein profile. Post-translational modifications, principally N-linked and O-linked glycosylation, are a function of the host cell’s metabolic state, the bioreactor feeding strategy, dissolved oxygen tension, and dozens of other process variables. The originator’s glycan profile is itself a moving target across manufacturing batches, within approved specification limits.

This fact has a direct and underappreciated IP consequence. Because the originator cannot patent a molecule per se — only specific compositions, formulations, methods of manufacture, and methods of use — the biosimilar developer’s task is to reverse-engineer a process that reliably produces a glycoprotein population sufficiently similar to the reference product’s approved specification range, without infringing any active patent claims covering the originator’s specific process. The process is the product, and the process is also the IP asset.

Why the Generic Drug Analogy Fails Strategically

The generic drug development model is instructive mainly for understanding what biosimilar development is not. A generic developer synthesizes an identical small-molecule active pharmaceutical ingredient (API), runs a single-dose crossover pharmacokinetic study in 24 to 36 healthy volunteers to demonstrate bioequivalence, and files an Abbreviated New Drug Application (ANDA) at a total development cost typically between $1 million and $4 million over roughly 24 months.

Biosimilar development runs $100 million to $250 million over seven to nine years. The capital requirement for a state-of-the-art commercial-scale biomanufacturing facility — typically requiring 10,000 to 20,000 liters of bioreactor capacity for a high-volume monoclonal antibody — exceeds $500 million. The supply chain requires an unbroken cold chain at 2-8 degrees Celsius from fill-finish to patient administration, adding logistical costs that have no analog in the oral solid dosage world. Protein degradation pathways — aggregation, deamidation, oxidation, fragmentation — require rigorous stability programs across multiple climatic zones, each with distinct temperature and humidity stress profiles.

These cost and complexity differences produce a structurally different competitive market. Generics attract dozens of filers once a molecule goes off-patent, driving rapid price erosion to near-commodity levels. Biosimilars attract a handful of well-capitalized developers per molecule, creating an oligopolistic structure where even a 20-30% price discount over the originator can yield enormous revenue. The market for a leading biosimilar position against a $6 billion annual revenue reference product can be worth $500 million to $1 billion in net revenue, even after accounting for price erosion. That math explains why Pfizer, Amgen, Sandoz, Celltrion, and Samsung Bioepis compete at the same level.

The Manufacturing Stack: Where IP Is Born

Cell Line Development and the Proprietary Master Cell Bank

The starting point of any biomanufacturing program is cell line development. The developer must generate a new, proprietary cell line — the originator’s cell line is a trade secret and a core competitive asset, never disclosed in regulatory filings or published literature. This requires transfecting the coding sequence for the desired protein into a CHO host cell, selecting high-producing clones through a multi-round screening process, and banking the final clone as a Master Cell Bank (MCB) and Working Cell Bank (WCB).

Cell line selection criteria include volumetric productivity (grams of protein per liter of culture per day), product quality attributes (specifically the glycosylation profile), genetic stability over the cell passages that correspond to a commercial manufacturing campaign, and absence of adventitious agents. The MCB is a regulated starting material, and its characterization package — full genomic sequencing, adventitious agent testing, expression level documentation — is submitted as part of the biosimilar’s quality dossier to every regulatory authority.

The cell line itself is potentially patentable. CHO expression systems developed for specific proteins can be covered by patents on the cell line’s genetic modifications, the selection marker systems used, or the fed-batch media compositions that drive productivity. A freedom-to-operate analysis for any biosimilar program must include a sweep of cell line patents, not just product and process patents.

Upstream Bioprocess: Fed-Batch, Perfusion, and the Scale-Up Challenge

Commercial biomanufacturing uses either fed-batch or perfusion culture modes. Fed-batch, the dominant paradigm for monoclonal antibody production, involves inoculating a bioreactor with cells from the working cell bank, growing the culture to peak cell density over 10 to 14 days with sequential nutrient additions, then harvesting the culture fluid. Titers for commercial-scale mAb production routinely reach 5 to 10 grams per liter in leading operations, a ten-fold improvement over early 2000s benchmarks driven primarily by media and feeding strategy optimization.

Perfusion culture, increasingly adopted for products requiring shorter culture durations or for intensified processes that increase annual facility output, involves continuous cell retention and fresh media addition. Perfusion creates a different glycoprotein environment — lower ammonia accumulation, more consistent pH and dissolved oxygen — which can shift glycosylation profiles relative to fed-batch production of the same protein. A biosimilar developer switching from fed-batch to perfusion must demonstrate that the resulting product quality attributes remain within the analytical similarity range established against the reference product.

Scale-up from bench (2-liter bioreactor) to clinical manufacturing (200 to 500 liters) to commercial scale (10,000 to 20,000 liters) is not linear. Mixing efficiency, dissolved oxygen gradients, shear stress on cells, and heat transfer all change non-linearly with vessel volume. Each scale change can alter glycosylation patterns, aggregation propensity, and charge heterogeneity. The manufacturing process validation package submitted to regulators must demonstrate consistency across at least three full-scale commercial batches.

Downstream Purification: Chromatography Trains and the Purity Imperative

Downstream processing purifies the target protein from host cell proteins (HCPs), host cell DNA, product-related impurities (aggregates, fragments, charge variants), and process-related impurities (Protein A leachate, viral particles). A standard mAb purification train includes a Protein A affinity capture step, two orthogonal polishing chromatography steps (typically ion exchange and hydrophobic interaction or mixed-mode), and viral clearance steps including low-pH hold and nanofiltration.

Each chromatography resin, membrane, and buffer system is potentially covered by vendor patents. More critically, the specific configuration of steps, the operating conditions (pH, conductivity, gradient slopes), and the pooling criteria that define a ‘good’ fraction are proprietary process knowledge. A biosimilar developer cannot access the originator’s purification train specifications. The developer must build a process that consistently achieves purity specifications — typically less than 100 ppm HCP, undetectable host cell DNA, and aggregation below 1-2% by size exclusion chromatography — that match the reference product’s profile, using methods that do not infringe active process patents.

The Glycosylation Similarity Standard: What Regulators Require

Glycosylation is the most scrutinized post-translational modification in biosimilar comparability exercises. For IgG1 monoclonal antibodies, the Fc glycan at Asn297 directly regulates antibody-dependent cellular cytotoxicity (ADCC) activity through its interaction with Fc gamma receptors on natural killer cells and macrophages. Afucosylated glycoforms enhance ADCC; high-mannose glycoforms accelerate clearance.

Regulators require a complete N-glycan profiling comparison between biosimilar and reference product using methods including normal-phase HPLC with fluorescence detection, capillary electrophoresis with laser-induced fluorescence (CE-LIF), and high-resolution mass spectrometry (LC-MS/MS). The specification ranges for major glycoforms (G0F, G1F, G2F, and their afucosylated counterparts) must be defined and shown to overlap with the reference product’s distribution. If a biosimilar’s fucosylation level differs materially from the reference product, the developer must present functional ADCC data to demonstrate no clinically meaningful difference.

The Global Regulatory Comparability Exercise

The Totality-of-Evidence Pyramid

The regulatory approval of a biosimilar rests on a stepwise comparability exercise governed by the ‘totality of the evidence’ principle. The logical architecture is a three-tier pyramid: a broad, deep base of analytical chemistry data, a middle tier of non-clinical functional data, and a narrow peak of targeted clinical confirmation. The strength of the lower tiers reduces the data requirements at the upper tiers — a principle that, properly executed, saves hundreds of millions in development cost and years of development time.

The base tier covers primary structure (amino acid sequence by peptide mapping with MS confirmation), higher-order structure (secondary structure by circular dichroism and FTIR, tertiary structure by near-UV CD and intrinsic fluorescence, quaternary interactions by analytical ultracentrifugation), post-translational modifications (N- and O-glycan profiling, disulfide bond mapping, methionine oxidation, asparagine deamidation), biological activity (receptor binding affinity by SPR and ELISA, Fc effector function assays, cell-based potency), and impurity profile (aggregates, fragments, HCPs, DNA).

The middle tier uses in vitro cell-based assays and, where required by specific product risk profiles, comparative in vivo pharmacology and toxicology studies in relevant animal species. The value of in vivo non-clinical studies for mAbs is limited, since most rodent models do not express the human antigen target. Regulators, including the PMDA and MFDS, are increasingly willing to waive repeated-dose toxicology studies when the quality data is analytically compelling and no new safety signals are anticipated.

The peak tier is clinical confirmation: a comparative pharmacokinetic study, typically a single-dose crossover design in healthy volunteers, using both intravenous and subcutaneous routes if both are commercially relevant, followed by a comparative pharmacodynamic endpoint study if a validated PD biomarker exists. A large-scale equivalence trial in patients — the most expensive element — is required only when residual uncertainty about clinical comparability cannot be resolved through the analytical and PK/PD evidence alone.

Extrapolation: The Commercial Multiplier

Extrapolation is the regulatory principle that allows a biosimilar approved in one indication to receive approval in all other indications of the reference product, without requiring separate clinical trials for each one. It is not automatic and requires scientific justification, but when granted, it multiplies the commercial value of a single clinical development program by the number of approved indications.

The standard justification for extrapolation includes: the mechanism of action is the same across all extrapolated indications; the safety and efficacy profile is adequately characterized in the tested population; and there are no specific patient or disease factors in the extrapolated indications that would create meaningful uncertainty about the comparable performance of the biosimilar.

For rituximab, which has approved indications in non-Hodgkin’s lymphoma, chronic lymphocytic leukemia, rheumatoid arthritis, granulomatosis with polyangiitis, microscopic polyangiitis, and pemphigus vulgaris, a biosimilar developer that runs a single comparative PK study and an efficacy confirmation trial in one oncology indication can potentially receive approval across all six. The development cost savings from extrapolation for a multi-indication product can reach $200 million or more.

Biosimilar Interchangeability: A Critical Commercial Distinction

Interchangeability designations differ materially across the jurisdictions covered in this guide, and the commercial implications of those differences are substantial.

In the United States, the FDA grants ‘interchangeable’ status as a specific, higher designation under the Biologics Price Competition and Innovation Act (BPCIA). An interchangeable biosimilar has demonstrated, typically through a switching study alternating patients between biosimilar and reference product, that it produces the same clinical result and that switching does not carry an increased risk of adverse events or diminished efficacy. This designation permits pharmacy-level automatic substitution without prescriber consultation, the pharmacist behavior that drives rapid generic substitution rates of 80-90% in the small-molecule world. As of early 2026, the FDA has granted interchangeable designation to a small but growing number of biosimilars, including several insulins and an adalimumab biosimilar.

In the European Union, the EMA’s official scientific position, shared by the Heads of Medicines Agencies (HMA), is that all EMA-approved biosimilars are interchangeable, meaning a prescriber can switch a patient from reference product to biosimilar with confidence. The decision on automatic pharmacy substitution is delegated to individual member states, producing a patchwork of national policies. Germany, France, and several Nordic countries permit or encourage substitution under defined conditions; others do not.

Japan and South Korea have no formal interchangeability designation. Switching is a physician decision, and pharmacist-level substitution is not permitted in either country. Malaysia’s NPRA states that registered biosimilars are interchangeable for prescribing purposes — meaning a physician can choose either product — but explicitly prohibits automatic substitution, and requires all biologics to be prescribed by brand name to ensure traceability.

The practical commercial implication for any biosimilar developer entering these Asian markets: market share gains depend on changing physician prescribing behavior, not on pharmacy channel dynamics. That requires a medical affairs strategy, real-world evidence generation, and direct engagement with hospital formulary committees, not a pharmacy-focused sales model.

IP Valuation Framework: Reference Product Patents and Their Commercial Weight

How to Value a Biosimilar Entry Opportunity

The risk-adjusted commercial value of a biosimilar program is a function of five variables: reference product revenue in the target market, the expected biosimilar price discount relative to the originator, the achievable market share given the competitive and reimbursement environment, the net present value of development costs discounted for probability of technical and regulatory success, and the probability-weighted legal cost and delay risk from patent litigation.

Each of these inputs varies substantially by molecule and by country. A trastuzumab biosimilar in Japan generates very different economics than the same product in South Korea, because the reimbursement mechanics, competitive intensity, and patent landscape differ materially. The framework presented below applies to each major molecule discussed in this guide.

Trastuzumab (Herceptin): The Anchor Oncology Asset

Herceptin, Genentech/Roche’s HER2-targeted monoclonal antibody, generated peak global revenues exceeding $6.5 billion annually before biosimilar competition began in earnest. In Japan, trastuzumab biosimilars have been the primary driver of oncology biosimilar adoption, accelerated by the government’s targeted prescribing incentive of roughly 1,500 yen per prescription during the initial post-launch period.

The trastuzumab patent estate illustrates the full complexity of originator IP strategy. Roche’s primary composition-of-matter patent on the humanized anti-HER2 antibody expired in the early 2010s. However, the company filed and prosecuted downstream patents covering specific formulations (the L-histidine buffered, polysorbate 20-containing lyophilized product), the subcutaneous formulation co-administered with recombinant human hyaluronidase (Herceptin Hylecta), manufacturing process improvements, and device patents covering the single-use injection device for the subcutaneous presentation.

The subcutaneous formulation represents classic evergreening: a genuinely improved product that extends the commercial life of the franchise by offering patient and nurse convenience, simultaneously creating new IP that the biosimilar developer must design around or wait to expire. Any biosimilar developer filing for the intravenous formulation must still independently develop a subcutaneous variant if they want to capture that growing market segment, and must navigate the device patents separately. This is not unique to trastuzumab — it is a template that originator companies apply systematically to their entire biologic portfolios.

For IP valuation purposes, the remaining value in the trastuzumab franchise by market is modest, since competitive biosimilar markets are already established in all three Asian markets. The more important analytical exercise is to use trastuzumab as a proof-of-concept for understanding how evergreening will extend the franchise value of next-generation assets like pembrolizumab and aflibercept, which are still years from their primary patent cliffs.

Bevacizumab (Avastin): The Oncology Workhorse

Avastin, Genentech/Roche’s anti-VEGF antibody for colorectal, lung, and cervical cancers, among others, generated peak revenues of roughly $7 billion globally. Bevacizumab biosimilars have penetrated major markets aggressively following the expiration of core composition-of-matter patents. In Japan, bevacizumab biosimilars are among the most actively prescribed, largely because their use is concentrated in the DPC inpatient hospital setting, where the fixed per-diem reimbursement creates a direct financial incentive for hospitals to substitute cheaper alternatives.

The bevacizumab estate is relatively thin compared to trastuzumab. Roche did not develop a subcutaneous formulation or a combination product that would anchor new IP claims. The primary formulation patent covering the specific buffer and concentration used in Avastin is the main ongoing litigation target. Freedom-to-operate analysis for bevacizumab biosimilar developers centers on demonstrating a different excipient system or buffer composition that achieves equivalent stability and delivers equivalent PK without infringing the specific formulation claims.

Bevacizumab also has an important ophthalmology use, specifically the off-label treatment of neovascular age-related macular degeneration, a practice that has created a separate market dynamic with its own IP considerations (including Genentech’s separately commercialized Lucentis/ranibizumab and the newer Eylea/aflibercept, both still under active patent protection in most Asian markets).

Adalimumab (Humira): The Global Evergreening Masterclass

Humira, AbbVie’s anti-TNF-alpha antibody, is the best-documented case study in biological product life cycle management. At peak, it generated more than $20 billion in annual global revenue. AbbVie built a patent portfolio of over 250 patents covering the adalimumab molecule and product, a strategy that delayed biosimilar entry in the United States until 2023, nearly a decade after European biosimilar entry began.

The AbbVie IP strategy for Humira used every available tool. The core composition-of-matter patents on the fully human anti-TNF antibody and its antigen-binding sequences were filed in the 1990s. AbbVie then filed patents covering: the high-concentration subcutaneous formulation (100 mg/mL, which produces less injection site pain than the original 50 mg/mL formulation); citrate-free formulations; specific methods of treating rheumatoid arthritis, psoriasis, and Crohn’s disease; combination uses with methotrexate; manufacturing process improvements including specific purification steps; and the auto-injector device design.

The high-concentration, citrate-free formulation is particularly instructive for the Asian market context. AbbVie launched this improved formulation across major markets, including Japan, as the standard of care product while the original 50 mg/mL formulation was the reference used in biosimilar comparability exercises. Biosimilar developers must show similarity to the approved reference product, but if the market has shifted to the improved formulation, commercial success requires matching that formulation’s performance regardless of whether it is the official regulatory reference product. This creates a significant additional development burden.

In Japan, the adalimumab biosimilar market is active, with products from multiple developers including Daiichi Sankyo, Mitsubishi Tanabe, and several international entrants. The DPC system drives inpatient use, while the co-pay cap dynamics are less disadvantageous for adalimumab than for higher-cost biologics, given that its per-course cost is less likely to systematically push patients into the monthly cap reduction trigger.

Part II — Japan: Cracking the Co-Pay Paradox

Market Size, Growth Trajectory, and Competitive Structure

Japan’s biosimilar market, valued at approximately $502 million in 2024, is underperforming relative to its fundamental opportunity. The broader biologics market in Japan generates roughly $15 to $18 billion annually. With the government targeting 80% biosimilar usage volume for applicable molecules by 2029 — a target it is unlikely to hit on schedule — the theoretical addressable market is enormous.

Growth forecasts range from a conservative 9.3% CAGR to an aggressive 22% depending on whether the government’s reimbursement interventions succeed in resolving the co-pay paradox described below. The 22% scenario requires a meaningful policy correction; the 9.3% scenario reflects trend continuation without structural change.

Therapeutic concentration is high. Oncology — trastuzumab, bevacizumab, rituximab, cetuximab — and autoimmune disorders — infliximab, etanercept, adalimumab — account for more than 70% of biosimilar spend. The filgrastim (G-CSF) segment, a first-generation biosimilar category, remains a significant volume contributor in the inpatient oncology setting due to its DPC dynamics. Ophthalmology biosimilars represent the next significant growth category as ranibizumab and aflibercept approach their Japanese patent cliffs.

The competitive structure is a mix of global originators running biosame strategies, foreign biosimilar specialists partnering with domestic distributors, and a limited number of Japanese manufacturers with in-house biologic manufacturing capability. The barriers to independent commercial launch for foreign entrants without a domestic partner are high, given the complexity of hospital contracting and the importance of established relationships with the PMDA and the Central Social Insurance Medical Council (Chuikyo), the body that sets reimbursement prices.

PMDA Pathway: Full Technical Breakdown

Definition Scope and Reference Product Requirements

The PMDA defines a biosimilar as a biological product that demonstrates comparability to an already-approved originator biological in Japan with respect to quality, safety, and efficacy. The agency’s guidelines, first issued in 2009 and updated with Q&A supplements through 2024, cover recombinant proteins expressed in microbial, yeast, insect, or mammalian cells, including mAbs, Fc-fusion proteins, enzymes, hormones, and cytokines. Cell therapy products, blood-derived products, and allergen extracts fall outside the standard biosimilar framework.

The reference product must be an originator approved in Japan based on a full data dossier. Products approved in Japan on the basis of a foreign reference product (i.e., products imported and approved under a Japanese New Drug Application relying on overseas data) are not eligible as comparators under standard rules. This requirement creates a complexity: if a product was approved in the EU five years before it was approved in Japan, the EU product has been the reference for European biosimilar programs, but Japanese biosimilar applicants must use the Japan-approved version as their primary comparator, which may have different batch history, formulation minor variations, or manufacturing site history.

Analytical Similarity: Orthogonal Methods and the PMDA’s Emphasis on Quality

The PMDA places greater relative weight on the analytical similarity package than most other major regulators. This is consistent with Japan’s broader pharmaceutical culture, where quality assurance has historically been a primary professional and regulatory concern, and where the ‘totality of the evidence’ principle is interpreted to mean that outstanding analytical data can substantially reduce the clinical development burden.

Required analytical methods include peptide mapping with LC-MS/MS for primary sequence confirmation, intact mass analysis for gross molecular weight, N-glycan profiling by HPLC or CE-LIF with mass spectrometry confirmation, charge heterogeneity profiling by isoelectric focusing and cation exchange chromatography, size exclusion chromatography for aggregate quantification, subunit analysis under reducing and non-reducing conditions, and a panel of biological activity assays covering all known mechanisms of action. The PMDA expects method validation for all analytical procedures, with acceptance criteria justified in the context of reference product variability data.

For clinical PK studies, the PMDA accepts data from non-Japanese subjects, provided the applicant submits a justified analysis of relevant ethnic pharmacogenomic factors. CYP450-mediated metabolism is not relevant for mAbs, but target receptor polymorphisms that affect drug-target binding kinetics can, in principle, create ethnic differences in PK. For most mAbs, the scientific justification is straightforward, and the PMDA’s 2023 guidance updates made the ethnic-factor waiver a more predictable part of the submission pathway.

Post-Marketing Requirements: RMP and Safety Database Obligations

The PMDA’s Risk Management Plan requirement for biosimilars is detailed and closely monitored. The RMP must specify safety concerns — identified risks, potential risks, and missing information — and define pharmacovigilance activities and risk minimization measures for each. For biosimilars, the PMDA specifically requires routine and enhanced pharmacovigilance systems capable of distinguishing adverse events attributable to the biosimilar from those attributable to the reference product, an important traceability requirement given that both products may be in concurrent use in Japan.

Post-marketing studies evaluating long-term immunogenicity are a standard PMDA expectation. Anti-drug antibody (ADA) development is the primary immunogenicity concern for protein therapeutics, and the PMDA requires prospective detection, characterization (neutralizing vs. non-neutralizing), and clinical impact assessment of ADAs in the post-marketing setting. This data feeds into periodic benefit-risk evaluation reports submitted on a schedule determined by the initial RMP.

The Reimbursement Labyrinth: DPC, Co-Pay Caps, and Financial Incentives

The Structural Architecture of Japanese Drug Reimbursement

Japan operates a universal health insurance system where the government sets reimbursement prices for all approved drugs through a biennial revision process. The NHI drug price list (yakka) assigns a specific yen price to every approved drug. When a biosimilar is approved, it receives its own NHI price, typically set at 70% of the reference product’s price in the first pricing cycle, with further reductions in subsequent cycles if the product does not achieve market penetration targets.

This pricing architecture creates a transparent and predictable revenue model: a biosimilar developer knows the maximum reimbursable price from the day of approval. The commercial uncertainty lies in the volume capture, which is where the co-pay paradox and DPC dynamics become decisive.

The Co-Pay Cap Mechanism: The Paradox Explained Precisely

The co-pay structure operates as follows. Patients under 70 years old generally pay 30% of drug costs up to a monthly maximum, which varies by income tier. Once a patient’s total monthly healthcare out-of-pocket expenditure (across all services and drugs) reaches this maximum, the government absorbs all additional costs. After this maximum has been reached three times within a 12-month window, the maximum is reduced — permanently lowered for that patient during that coverage year.

For patients on high-cost biologic therapies, the monthly drug cost alone is often sufficient to trigger the cap. An infliximab infusion at the originator’s NHI price might generate a monthly co-pay of 80,000 to 100,000 yen for a standard 5 mg/kg dose before the cap kicks in. Once the patient reliably hits the cap, their marginal monthly cost for every subsequent infusion is zero. The biosimilar, priced at 70% of the originator, reduces the monthly drug cost to a level that may no longer trigger the cap as quickly or as reliably — meaning the patient’s out-of-pocket cost paradoxically increases when they switch to the cheaper product.

This is not a theoretical edge case. McKinsey’s analysis of the infliximab biosimilar launch in Japan identified this mechanism as the principal factor explaining why infliximab biosimilar penetration in Japan was significantly below that seen in Germany, the Netherlands, and the Nordic countries, where flat co-pay structures or reference pricing systems create direct patient cost incentives to use biosimilars.

The paradox does not apply uniformly. For biologics with monthly drug costs that fall below the cap threshold, such as etanercept at standard doses, the co-pay is a fixed percentage with no cap triggering, and biosimilar price reductions translate directly into patient savings. This explains why etanercept biosimilars achieved much higher penetration rates in Japan than infliximab biosimilars in comparable time periods post-launch.

DPC: The Inpatient Incentive That Works

The Diagnostic Procedure Combination (DPC) system covers approximately 55% of all general hospital beds in Japan, applying a fixed per-diem payment rate to each hospitalized patient based on their diagnosis code and associated treatment category. The hospital receives the same payment regardless of whether it administers the originator biologic or the biosimilar. Every yen saved on drug acquisition translates directly to the hospital’s operating margin.

This mechanism drove filgrastim biosimilar penetration to over 70% in the inpatient oncology setting within a few years of approval, and is the primary force accelerating trastuzumab and bevacizumab biosimilar uptake in hospitals with high DPC coverage. The commercial implication for biosimilar developers is clear: market access strategy in Japan must be segmented by care setting. The inpatient oncology and rheumatology teams at major academic medical centers and DPC-covered hospitals are the primary commercial targets, because the financial incentive to switch is structural, durable, and independent of physician education about biosimilar science.

The 1,500-Yen Prescriber Incentive and Its Documented Effectiveness

Japan’s Ministry of Health, Labour and Welfare (MHLW) has experimented with direct financial incentives to accelerate biosimilar uptake. A premium of approximately 1,500 yen per biosimilar prescription, available to prescribing physicians for a defined initial period, generated a measurable and statistically significant increase in trastuzumab biosimilar prescription rates in a 2024 study published in a peer-reviewed pharmacoeconomics journal. The effect was concentrated in outpatient settings where the DPC incentive does not apply and where the co-pay paradox is most acute.

The mechanism is analogous to the pay-for-performance bonuses used in the UK’s NHS Quality and Outcomes Framework and in US Medicare’s Merit-Based Incentive Payment System (MIPS), though at a much smaller absolute scale. The documented effectiveness of even modest financial nudges suggests that expanding the incentive program — broadening the molecule list, increasing the premium amount, or extending the eligibility period — could meaningfully accelerate Japan’s progress toward its biosimilar penetration targets.

IP Valuation: Trastuzumab, Bevacizumab, and the Evergreening Playbook in Japan

The Japan-Specific Patent Landscape

Japan’s patent term is 20 years from filing, with a patent term extension (PTE) available for up to five additional years to compensate for the time lost to regulatory review. PTE applications for biologics are common and are evaluated by the Japan Patent Office (JPO) using the same first-marketing approval date reference used in the US and EU systems. For a biologic first approved in Japan in 2002 with a 2019 patent expiration, a five-year PTE could extend protection to 2024, significantly affecting the biosimilar market entry timeline.

The critical strategic insight for biosimilar developers is that the Japanese patent register is a distinct landscape from the US or European registers. A patent that has expired in the US may still be active in Japan if it was filed later, has a different prosecution history, or received a PTE based on the Japanese approval date. Developers who assume that the European biosimilar launch timeline applies directly to Japan make a systematic error with real cost consequences.

Evergreening Tactics and the Japan-Specific Counter-Strategies

Originator companies use several standard evergreening tactics in Japan:

Formulation patents on pH, concentration, buffer system, and excipient composition are filed routinely and can extend effective market exclusivity by three to seven years beyond composition-of-matter patent expiry. The Japanese courts have been willing to enforce formulation patents with relatively narrow scope — meaning a biosimilar developer can often design around a formulation patent by adopting a different buffer system that achieves the same stability goals, provided they can demonstrate equivalent quality attributes.

Process patents covering specific chromatography resins, viral inactivation parameters, or filtration configurations are increasingly common. These are difficult to detect through public patent records alone because the manufacturing process is not disclosed in regulatory submissions or published literature. Biosimilar developers must identify these patents through patent landscaping and then design processes that achieve equivalent purity profiles through different means.

Device patents on auto-injectors, safety syringes, and combination products represent the newest and most commercially impactful form of evergreening. The commercial success of the NIPRO/Owen Mumford UniSafe syringe biosimilar launch in Japan illustrates that device differentiation cuts both ways: originators use it to defend share by migrating patients to device-locked branded combinations, but biosimilar developers who invest in superior device engineering can use device quality as a positive commercial differentiator rather than simply trying to replicate the originator’s device.

Competitive Dynamics: ‘Biosames,’ Device Differentiation, and Key Players

The Biosame Phenomenon: Originator Self-Cannibalization as Defense

The ‘biosame’ strategy represents one of the most sophisticated competitive tactics in the Japanese market. When Kyowa Kirin launched a biosame version of its own Nesp (darbepoetin alfa) in 2019 at a price point equivalent to incoming biosimilar competition, it used three simultaneous advantages that no independent biosimilar entrant could match: an already-established physician relationship with the product, an existing manufacturing line with known regulatory history, and brand recognition built over years of clinical use.

The biosame strategy effectively collapses the price gap that would otherwise accrue to biosimilar entrants while retaining the originator’s commercial infrastructure advantage. From a market structure perspective, it is equivalent to a fast follower launching a ‘premium generic’ — product identical in molecule, price-competitive with biosimilars, but carrying the brand equity of the originator.

Biosame strategies are most viable for originators with substantial domestic manufacturing capability in Japan. Companies that rely entirely on overseas production may find the Japan-specific NHI pricing and post-marketing obligations for a biosame too costly relative to the benefit of share defense. The strategy is therefore particularly relevant for Japanese domestic originators like Kyowa Kirin, Chugai, and Takeda, rather than for US or European multinationals manufacturing in Ireland or Singapore.

Key Commercial Players

The Japan biosimilar market has a distinct competitive map. Global biosimilar specialists including Sandoz (Novartis), Pfizer, and Amgen compete with specialized Japanese distributors who hold the commercial rights for Korean biosimilars. Celltrion’s products reach the Japanese market through licensing and distribution arrangements rather than direct commercialization. Samsung Bioepis products have entered through partnerships with Organon and local distributors.

Domestic Japanese companies active in biosimilar development include Daiichi Sankyo, which has developed its own adalimumab biosimilar, and Kyowa Kirin, which manages its biosame program independently. The Japanese generics-to-biosimilar conversion companies — Sawai, Towa, and Nichi-Iko — have not developed significant biosimilar positions, as the manufacturing complexity is beyond their current capabilities.

Key Takeaways — Japan

Japan’s biosimilar market offers the highest revenue per product of the three markets covered here, but the path to realizing that revenue requires resolving the co-pay paradox through careful pricing strategy and a segmented market access approach. The DPC inpatient system creates a durable structural incentive that should be the primary commercial focus at launch, with outpatient penetration following as physician education and government incentives build confidence and change prescribing habits over time. Formulation, device, and process patent evergreening is active and creates a meaningfully different launch timeline in Japan versus Europe or the US for several key molecules. Regulatory acceptance of foreign clinical data reduces the incremental development cost for Japan market entry, making a Japan market entry viable as an extension of a global program rather than a standalone investment.

Investment Strategy — Japan

Portfolio managers evaluating biosimilar-focused companies with Japan exposure should weight several factors specifically. Revenue recognition timing is affected by the NHI biennial price revision cycle — a product launched in year one of a cycle receives full pricing for two years before its first downward revision, while a product launched in year two faces an early price cut. Market penetration rates for the inpatient segment are more predictable and faster than outpatient, so near-term revenue forecasts for any new Japanese biosimilar launch should be modeled with higher confidence in the DPC segment than in the outpatient rheumatology or dermatology segment. Companies with strong hospital relationships and existing DPC-covered hospital contracting infrastructure have a durable commercial advantage that is difficult to replicate on a short timeline. The device differentiation opportunity is underappreciated: the NIPRO/UniSafe case demonstrates that a superior delivery device can produce disproportionate market share gains in a market that typically selects on price alone.

Part III — South Korea: How a Government Builds a Global Powerhouse

Market Size, CAGR, and Export Architecture

South Korea’s biosimilar market reached approximately $531 million in 2023 and is projected to exceed $1.6 billion by 2027 at a CAGR of 22.5%. The domestic market, while significant, is not the strategic focus of the Korean national biosimilar program. The real objective is export revenue: Korean companies have built their entire commercial infrastructure around capturing share in the US, European, and Japanese markets, with the domestic market serving primarily as a regulatory credentialing platform.

The South Korean biopharma market as a whole is approximately $22 billion, making it the 13th largest pharmaceutical market globally. As of 2024, companies headquartered in South Korea had developed the second-highest number of FDA-approved biosimilars of any country, behind the United States itself. By early 2026, that position was reinforced by ongoing FDA approvals from Celltrion’s and Samsung Bioepis’s expanding pipelines.

The geographic concentration of biomanufacturing capacity in Songdo, Incheon — a purpose-built biotechnology city — is strategically significant. Songdo now has the single largest concentration of biopharmaceutical manufacturing capacity at a single location in the world, combining Samsung Biologics’ four production facilities, Celltrion’s dedicated manufacturing complex, and contract development manufacturing (CDMO) operations that serve both domestic companies and global clients. This geographic concentration enables shared infrastructure, labor pool depth, and supply chain efficiency that generates durable cost advantages.

The Third Five-Year Plan: Targets, Funding, and Industrial Logic

National Target Architecture: 2023-2027

The South Korean government’s Third Five-Year Comprehensive Plan for the Development and Support of the Bio-Pharmaceutical Industry (2023-2027), jointly managed by the Ministry of Health and Welfare (MOHW), the Ministry of Science and ICT (MSIT), and the Ministry of Trade, Industry and Energy (MOTIE), sets the following national targets for 2027:

Development of two new blockbuster drug products each generating more than $700 million in annual revenue. Elevation of at least three Korean domestic companies into the global top-50 pharmaceutical companies by revenue. Growth of pharmaceutical export revenue to $16 billion, representing a doubling of the pre-Plan baseline. Achievement of third-place global ranking in clinical trial site volume, measured by the number of active investigational new drug studies conducted in Korean facilities.

These are not advisory targets. They are backed by specific funding mechanisms, regulatory commitments, and infrastructure investments that create concrete institutional accountability for outcomes.

The K-Bio Vaccine Fund and Capital Deployment

The Plan allocates a KRW 1 trillion (approximately $720 million at 2024 exchange rates) K-Bio Vaccine Fund specifically for R&D and commercialization of vaccines and biologics, including biosimilars. A second, larger mega-fund focused on late-stage clinical development and global market entry was in development as of early 2026. These funds operate as government-backed investment vehicles, co-investing with private capital rather than providing grants, which aligns government and private investor risk more closely than traditional subsidy programs.

Public-private co-investment in AI-driven drug discovery, digital manufacturing twins for bioprocess optimization, and real-world evidence platforms were explicitly funded in the Plan. The AI component is not decorative: Samsung Biologics has deployed machine learning models for fed-batch optimization that have improved titer consistency and glycoform reproducibility at commercial scale, a direct competitive advantage in the CDMO business where process reliability is the primary selection criterion for clients.

Bio-Cluster Infrastructure and Regulatory Streamlining

The Songdo International Business District serves as the anchor bio-cluster, with satellite clusters established in Osong (North Chungcheong Province), Daejeon (the national research and development hub), and Pangyo (adjacent to Seoul). Each cluster combines wet laboratory infrastructure, GMP manufacturing space, regulatory affairs support from co-located government agencies, and access to academic institution partnerships. Companies establishing operations within designated cluster boundaries receive corporate tax reductions, accelerated equipment depreciation, and priority access to government-sponsored clinical trial networks.

Regulatory streamlining is operationally concrete. The MFDS announced a dedicated fast-track review program for biosimilars beginning in 2026, targeting reduction of total review time from the current median of approximately 18 months to under 12 months for applications meeting pre-specified completeness criteria. This acceleration is achievable in part because Korean biosimilar developers filing with the MFDS typically also hold EMA or FDA approval, providing the MFDS with a high-quality precedent data package that reduces the MFDS’s independent analytical burden.

MFDS Pathway: Harmonization as Competitive Strategy

The Strategic Design of Korean Regulatory Alignment

When the MFDS issued its first biosimilar guidelines in 2009, harmonizing with the WHO, EMA, and PMDA frameworks was not merely a scientific choice — it was an export strategy. A Korean biosimilar meeting MFDS requirements was designed, from inception, to also meet EMA and (with incremental additional data) FDA requirements. This integration of regulatory compliance with commercial market access is the operational core of the Korean biosimilar model.

The reference product framework in Korea requires the comparator to be an originator approved in Korea via a full data dossier. Foreign-sourced reference products — for example, using the EU-approved originator as the primary comparator in a development program — are acceptable with a bridging study demonstrating analytical equivalence between the EU-sourced and Korea-approved reference. This flexibility is commercially important: Korean companies running global development programs can use the same reference product lots across their entire regulatory filing strategy, reducing the total volume of reference material needed and streamlining the analytical comparability database.

Extrapolation is permitted by the MFDS with the same scientific standards as the EMA: mechanism-of-action consistency across extrapolated indications, no population-specific safety concerns, and adequate overall characterization of the biosimilar in the studied indication. The MFDS has a track record of granting broad extrapolation for well-characterized mAbs, supporting the commercial viability of single-indication clinical programs.

IP Valuation: Celltrion’s Remsima Portfolio and the Paragraph IV Equivalent

Remsima (Infliximab): A First-Mover IP Asset Worth Analyzing Precisely

Celltrion’s Remsima was the world’s first approved monoclonal antibody biosimilar, receiving Korean approval in 2012 and EMA approval in 2013. The IP value of Remsima is no longer in the product itself — infliximab’s global market has been heavily penetrated by biosimilar competition — but in what Remsima demonstrated: that a Korean company could develop, manufacture, and gain regulatory approval for a complex mAb biosimilar at world-class quality standards, then commercialize it globally.

The ‘first approved mAb biosimilar’ status created durable brand equity that translates into physician trust and formulary positioning in markets where biosimilar adoption is still building. Remsima has also been the platform for Remsima SC, Celltrion’s subcutaneous reformulation of infliximab. This product exemplifies the biobetter strategy: by developing a subcutaneous formulation co-administered with hyaluronidase, Celltrion created a genuinely improved product with new IP, different MFDS and EMA approval dates, and a distinct commercial position that is difficult for pure biosimilar competitors to replicate without independent subcutaneous formulation development programs.

For IP valuation, Remsima SC’s value lies in the new patent estate covering the subcutaneous formulation and the proprietary co-administration technology. Unlike a standard biosimilar, which can only compete on price and quality, Remsima SC competes on delivery convenience and a distinct clinical positioning, making it more defensible against subsequent competition and capable of maintaining a premium price relative to the IV formulation.

The Korean ‘Paragraph IV Equivalent’ Dynamic

Korea’s pharmaceutical patent challenge system, while structured differently from the US Hatch-Waxman Paragraph IV framework, produces analogous commercial dynamics. When a Korean biosimilar developer files with the MFDS and there are active Korean patents covering the reference product, the originator company receives notification, triggering a period for patent dispute resolution. The commercial implications — first-filer advantages, at-risk launch decisions, settlement agreements that may include market entry date provisions — parallel the US experience, though the specific legal procedures differ.

For international developers, understanding the specific Korean patent challenge precedents for infliximab, trastuzumab, and adalimumab is essential before filing the MFDS application for any molecule in these classes. The Korean Intellectual Property Office (KIPO) maintains an accessible patent register, and MFDS notification procedures are documented in the agency’s pharmaceutical affairs regulations. These records, combined with litigation databases maintained by Korean IP law firms, constitute the primary intelligence source for Korean launch timing analysis.

Celltrion: Pioneer Strategy, US Manufacturing, and 2030 Pipeline

The 22-Product Portfolio Commitment

Celltrion’s stated goal of commercializing a portfolio of 22 biosimilar products by 2030 is not aspirational window dressing. As of early 2026, the company had approximately 11 biosimilars approved across major markets, with a further seven to eleven products in various stages of late clinical development or regulatory review. The 2030 portfolio includes products in ophthalmology (ranibizumab biosimilar), oncology immunotherapy (pembrolizumab biosimilar, where Keytruda’s key patents are expected to expire around 2028 in most major markets), and dermatology (ustekinumab biosimilar, competing against Johnson & Johnson’s Stelara).

Each of these pipeline additions represents a distinct IP landscape challenge, a separate clinical development program, and a separate market access investment. The total investment required to execute the 22-product strategy across development, manufacturing, and commercialization exceeds $5 billion over the period, suggesting that Celltrion’s capital allocation strategy — including the decision to maintain its own direct commercialization infrastructure in the EU and US rather than relying on partners — requires continued access to debt and equity capital at favorable terms. Any investor modeling Celltrion should stress-test the capital structure against scenarios where launch timing delays or pricing pressure in one or more key markets reduce expected cash flow.

US Manufacturing Acquisition: Tariff Mitigation and Strategic Signaling

Celltrion’s announced acquisition of a large-scale US biologics manufacturing facility in 2025, detailed in a letter to shareholders, is a multi-objective strategic move. The stated primary objective is tariff mitigation. The possibility of US pharmaceutical import tariffs — discussed seriously in the US executive branch and Congress through 2024 and 2025 — creates specific commercial risk for a company with all existing manufacturing in South Korea and Ireland. A US-sited drug substance manufacturing facility converts the risk profile from a currency and trade policy exposure to a domestic production story with ‘Made in USA’ marketing value.

The secondary objective is supply chain diversification. A single-country manufacturing model, even with Korea’s world-class facilities, concentrates geopolitical and natural disaster risk. The US facility provides a second manufacturing node that can backstop Korean production during disruptions, supporting FDA and EMA supply commitments under Product Shortage Prevention frameworks.

The tertiary objective is regulatory relationship building. A company manufacturing in the US employs a US workforce, pays US corporate taxes, and has standing to engage directly with FDA manufacturing quality and biosimilar policy teams in a way that foreign manufacturers do not. This matters for the ongoing relationship with the FDA on manufacturing supplements, post-approval changes, and the agency’s evolving interchangeability designation framework.

Direct EU and US Commercialization: The P&L Implications

Celltrion’s decision to build direct sales and marketing infrastructure in Europe (beginning 2019) and the US (beginning 2023) rather than continuing to rely on commercial partners produces significantly higher gross margins per unit sold at the cost of higher fixed operating expenses. The margin benefit of eliminating a commercial partner’s 25-35% take on net sales is substantial over the long term, but the fixed cost structure creates operating leverage risk: if biosimilar pricing deteriorates faster than expected due to competitive dynamics, the direct commercial model’s fixed costs magnify the downside versus a partnership model where cost of sales is variable.

Samsung Bioepis: Partnership Architecture and the Spinoff Rationale

The Partnership-First Commercial Model

Samsung Bioepis has chosen a fundamentally different commercial architecture than Celltrion. The company focuses its resources on R&D, process development, and manufacturing, delegating commercialization to global partners with existing market access infrastructure. Biogen has been the primary US commercialization partner for Samsung Bioepis products, including its adalimumab biosimilar (Hadlima), its etanercept biosimilar (Benepali), and its ranibizumab biosimilar (Byooviz). Organon acquired commercialization rights to Samsung Bioepis’s US and European biosimilar portfolio from Merck in 2021, taking on several additional products.

The partnership model’s advantage is capital efficiency. Samsung Bioepis does not maintain a global salesforce or country-by-country market access team, which allows it to deploy its capital more intensively toward pipeline expansion and manufacturing excellence. The disadvantage is revenue share dilution and strategic dependence on partners whose priorities and market execution capabilities may not align perfectly with Samsung Bioepis’s own commercial goals. Biogen’s 2025 decision to exit the ophthalmology biosimilar space — transferring Samsung Bioepis’s ranibizumab commercialization rights to Harrow — illustrates this risk: Samsung Bioepis had no control over Biogen’s strategic exit and had to manage the transition to a new partner without disrupting supply and market access in the middle of a commercial launch.

The Samsung Biologics Spinoff: Strategic Logic and IP Separation

Samsung Biologics’ announced intention to spin off Samsung Bioepis into an independent publicly traded entity addresses a structural conflict of interest that has increasingly complicated the CDMO business. Samsung Biologics competes directly with Lonza, WuXi Biologics, Boehringer Ingelheim, and Catalent for CDMO manufacturing contracts. Potential CDMO clients who are originator biologic companies face a conflict in contracting manufacturing to Samsung Biologics while Samsung Bioepis develops biosimilars targeting those very same originators’ products.

The spinoff separates the two businesses’ IP estates, competitive positions, and governance structures. Samsung Biologics post-spinoff becomes a pure CDMO without any biosimilar development assets, eliminating the conflict of interest for originator CDMO clients. Samsung Bioepis post-spinoff becomes a fully independent biosimilar and novel drug development company with its own capital markets strategy, a cleaner IP ownership structure, and the ability to make acquisition and partnership decisions without Samsung Biologics board-level conflict-of-interest considerations.

For analysts, the post-spinoff Samsung Bioepis is a more comparable entity to Celltrion — a pure-play biosimilar developer with a specific pipeline, known cost structure, and defined commercial strategy. Valuation multiples applicable to biosimilar-focused companies apply cleanly, rather than the mixed CDMO/biosimilar conglomerate discount that applied to the pre-spinoff structure.

Technology Roadmap: Korean Biomanufacturing Scale and CHO Cell Advancement

Samsung Biologics’ Four-Facility Capacity Stack

Samsung Biologics has built commercial-scale biomanufacturing capacity in four sequential tranches in Songdo. The first three facilities, operational between 2011 and 2020, provide a combined installed capacity of approximately 180,000 liters of fed-batch bioreactor volume, making Samsung Biologics the largest single-site CDMO globally by volume. The fourth facility, completed in 2023, added an incremental 240,000 liters and introduced both additional fed-batch trains and an intensified perfusion manufacturing suite designed to serve the next generation of biologic products, including cell and gene therapies, which require different process modalities than conventional mAbs.

The fifth facility, announced in 2023 and under construction as of early 2026, targets an additional 180,000 liters, bringing total installed Songdo capacity above 600,000 liters by 2025-2026. At current commercial mAb titers of 5 to 8 grams per liter over a 14-day cycle, this capacity can theoretically produce 300 to 400 metric tons of mAb drug substance per year, dwarfing any individual originator’s in-house biomanufacturing footprint.

Process Intensification and the Next Generation of Efficiency

Korean CDMO and biosimilar companies are actively investing in process intensification technologies that reduce the cost of goods for biosimilar production. Continuous manufacturing approaches that replace batch upstream and downstream processing with continuous bioprocessing trains — cell retention devices, continuous capture chromatography, inline virus inactivation — can reduce facility footprint by 40-60%, cut manufacturing cycle time from weeks to days, and improve batch-to-batch consistency by minimizing process variable accumulation over long culture durations.

Samsung Biologics and Celltrion have both published process development results indicating pilot-scale implementation of continuous bioprocessing for selected mAb products. Full commercial-scale validation of continuous manufacturing for a biosimilar product is expected by 2027, at which point the regulatory pathway for continuous manufacturing supplements will be better defined by the FDA and EMA. This investment has direct IP implications: continuous manufacturing processes generate new patentable process innovations distinct from the batch processes of the reference product, potentially providing additional IP protection for the Korean manufacturers’ biosimilar products.

Key Takeaways — South Korea

South Korea’s biosimilar success is structural, not accidental. State capital, regulatory alignment with export markets, and purpose-built manufacturing infrastructure created an ecosystem where Celltrion and Samsung Bioepis could reach global scale faster than any private-sector-only model would have permitted. For non-Korean companies, competing head-on in mainstream mAb categories against these national champions in their home market is a losing strategy. The viable alternatives are licensing or distribution partnerships that access the Korean manufacturing cost base, niche therapeutic area focus in categories where Korean pipeline coverage is thin, or biobetter/next-generation product strategies that compete on differentiation rather than price.

Investment Strategy — South Korea

Institutional investors evaluating Korean biosimilar companies should build their models around three distinct revenue streams: domestic Korean market sales (lower margins, driven by government price controls), export royalties and milestone payments from commercial partnerships in the US and EU (high margin, lumpy timing), and direct commercialization revenue from Celltrion’s own EU and US salesforce (high top-line, high fixed cost structure with operating leverage). The Celltrion US manufacturing acquisition changes the tariff risk profile materially. Analysts who modeled 15-20% tariff sensitivity on Korean-manufactured product shipped to the US should revise those models to reflect the partial mitigation of domestic US production. Samsung Bioepis post-spinoff warrants re-rating as a pure-play biosimilar compounder: revenue visibility is higher, margin structure is cleaner, and the CDMO conflict-of-interest discount disappears.

Part IV — Malaysia: The Procurement Bottleneck and the NPRA’s Precision Framework

Market Size and the 800-Day Drug Lag

Malaysia’s combined generic and biosimilar pharmaceutical market was valued at approximately $898.7 million in 2022 and is forecast to reach $1.24 billion by 2030, representing a CAGR of roughly 4%. The biosimilar component is a subset of this figure and is not separately disclosed in government statistics with granularity, but industry estimates place biosimilar-specific spend at $60 to $80 million annually, a fraction of Japan’s or South Korea’s scale.

The structural drag on market development is the 800-day median approval lag documented in a 2023 retrospective study published in the Journal of Applied Pharmaceutical Science. This metric measures the median time between a biosimilar’s first approval in a major reference jurisdiction (typically the EU) and its subsequent NPRA approval. An 800-day lag means that by the time a biosimilar reaches the Malaysian market, it is already three to five years into its commercial life in Europe. The competitive dynamics, clinical adoption data, and physician confidence built in the EU market are valuable but do not automatically transfer to Malaysia’s procurement and prescribing environment, requiring a largely independent market access investment.

The drivers of the lag are multiple. Applicant submission timing is often the primary factor — companies prioritize major market submissions and file Malaysia as a secondary or tertiary market. NPRA review timelines, while not globally the slowest, are affected by resource constraints and queue management. Reference product bridging requirements add analytical work for products that were not originally developed with Malaysia as a primary market. The 2023 NPRA guideline update addressed some procedural clarity issues, and the NPRA has publicly committed to accelerated review timelines for products with existing EMA or FDA approval, but the 800-day lag figure reflects years of accumulated backlog that will take time to resolve.

NPRA Pathway: December 2023 Updates and Interchangeability Rules

The NPRA’s December 2023 second edition of its Guidance Document and Guidelines for Registration of Biosimilars in Malaysia incorporated updates from the WHO’s 2022 biosimilar guideline revision. The key technical changes include expanded guidance on analytical similarity assessment, specifically the application of quality range approaches for setting specification limits that reflect reference product variability; updated pharmacovigilance requirements aligned with the ICH E2E guideline structure; and a new section on biosimilar naming conventions for traceability, requiring non-proprietary name plus suffix identification on all prescriptions and dispensing records.

The interchangeability and substitution clarifications in the second edition formalized a policy that had been operationally in place but previously under-documented. The NPRA’s position is that once a biosimilar is registered, a prescriber may choose it or the reference product with confidence that both will produce the same therapeutic effect — clinical interchangeability for prescribing choice. Automatic pharmacy-level substitution is explicitly and unambiguously prohibited. All biologics, including biosimilars, must be prescribed by brand name, not by international non-proprietary name (INN) alone. This brand-name prescribing requirement is the enforcement mechanism for traceability: it ensures that if an adverse event occurs, the specific product and batch number can be identified in the pharmacovigilance database.

Reference Product and Bridging Data Requirements

The NPRA requires the comparator to be an innovator biologic registered in Malaysia on the basis of a full data dossier. This is a meaningful constraint. Not all reference products registered in Malaysia were submitted with a full dossier — some older products received approval under different regulatory frameworks. In those cases, the biosimilar applicant must conduct additional analytical characterization work to establish that the Malaysia-registered reference product is itself comparable to the well-characterized version used in the primary biosimilar development program.

Foreign clinical data from EU or US biosimilar programs is acceptable provided the applicant includes a justification that Malaysian patient population pharmacokinetics are not expected to differ materially from the study population, and that the reference product used in the foreign study is analytically equivalent to the Malaysia-registered comparator. This double-bridging requirement — foreign program to Malaysian reference product, and foreign clinical population to Malaysian patient population — adds analytical and regulatory work that requires local regulatory expertise to execute efficiently.

The Procurement Puzzle: Tenders, Price Paradoxes, and Policy Contradictions

The Three-Channel Public Procurement Architecture

Malaysia’s Ministry of Health procures pharmaceuticals through three channels. The first is the APPL (Approved Pharmacy Products List), a direct procurement contract mechanism for a defined list of products, historically managed through a government-linked company concession structure. The second is centralized national tender management for high-volume, high-spend products. The third is direct hospital or clinic purchase for lower-value items below specified threshold procurement values.

For biosimilars, the national tender is the primary access route. Tender cycles for major biologic categories occur every two to three years, with contract durations of one to two years. Winning a national tender provides access to the entire public sector network, which is the dominant channel for expensive biologic therapies given that most patients in Malaysia are treated in government facilities where drugs are provided free or at nominal cost.

The Price Paradox: Policy Contradiction in Public View

Reports from Malaysian industry associations and academic healthcare economists, published through 2024 and 2025, document a specific pattern: the MOH’s tender evaluation process has awarded contracts to locally manufactured generics and biosimilars at prices substantially above those offered by imported alternatives. The reported price premium range is 100 to 200% above the imported competitor price for the same molecule.

The mechanism behind this outcome is the “Local Partner Advantage” (LPA) policy embedded in public procurement regulations, which gives preference and scoring advantages to products manufactured in Malaysia or supplied by Malaysian-registered companies under defined local content thresholds. When the LPA scoring weight is high enough, a locally produced product at double the price of an import can still achieve a higher total tender evaluation score.

This creates a direct policy contradiction. The government’s official position, expressed in the MOH Position Statements on the Use of Biosimilars and in public health policy documents, states that biosimilars are endorsed as cost-effective tools to expand patient access. The procurement mechanism simultaneously generates above-market drug costs in the public sector, partially offsetting the cost savings that were the justification for adopting biosimilars in the first place.

For foreign biosimilar developers, the LPA policy means that a competitive clinical and quality dossier is insufficient for tender success. The commercial strategy must include either a manufacturing presence in Malaysia, a partnership with a Malaysian-registered company with local content qualification, or a pricing strategy aggressive enough to overcome the LPA scoring premium of a local competitor.

Transparency and Speed Challenges

Independent of the LPA issue, Malaysia’s pharmaceutical tender process has documented operational problems. End-to-end tender duration from publication to contract award averages six to nine months, with some tenders taking longer due to evaluation appeals or procedural challenges. Historically, competing bid values were published post-award, providing market transparency; more recent reports from industry sources indicate that this transparency has diminished, making it harder for companies to assess whether their bids were competitively priced or whether evaluation criteria were applied consistently.

Supply gap periods — the interval between the end of one tender contract and the start of the next, during which hospitals revert to spot purchases or experience shortages — are a documented problem for several biologic categories. These gaps create patient access interruptions and undermine the prescribing confidence that biosimilar market development depends on.

IP Valuation: What Biologics Approvals in Malaysia Are Actually Worth

A Market Access Value Framework for Southeast Asia Entry

Valuing an NPRA approval for a biosimilar requires a different framework than valuing an EMA or FDA approval. The absolute revenue opportunity — $60 to $80 million total addressable biosimilar market in Malaysia — is small relative to the development and regulatory submission costs. The strategic value of a Malaysian approval is therefore not primarily in Malaysia-specific revenue; it is in the following:

Regional platform credibility: NPRA approval signals regulatory rigor sufficient to satisfy neighboring ASEAN markets, including Thailand (FDA Thailand), Vietnam (DAV), Indonesia (BPOM), and the Philippines (FDA Philippines), each of which applies its own framework but often treats NPRA approval as a favorable precedent.

Investor signaling for Southeast Asia market development: for companies whose investment thesis includes building an ASEAN biosimilar presence, Malaysian approval is a credible proof point that the regulatory and commercial groundwork for regional expansion is in place.

Government tender leverage: NPRA approval is a necessary but not sufficient condition for public procurement. Companies with NPRA approval and a local distribution or manufacturing partner are in a materially better position to win MOH tenders than companies with approval alone.

The IP dimension in Malaysia is relatively limited for most biosimilar categories. Most reference biologic patents are already expired or near expiration in Malaysia, given the country’s historical pharmaceutical patent framework and the 800-day approval lag that means most biosimilars are filed in Malaysia well after originator patent expiry. The primary IP concern in Malaysia for biosimilar developers is less about litigation risk and more about ensuring that the local partner’s activities comply with Malaysian pharmaceutical and IP regulations, particularly regarding product labeling, brand name use, and pharmacovigilance responsibilities.

Key Takeaways — Malaysia

Malaysia has a mature, globally respected regulatory framework for biosimilars. The NPRA’s December 2023 guideline update aligns the country with WHO 2022 standards and provides clear procedural expectations for applicants. The commercial barrier to success is the public procurement system, not the regulatory pathway. Market entry strategies that do not explicitly address the tender process, local content requirements, and the structural price paradox will underperform regardless of the quality of the regulatory dossier. The 800-day approval lag is a structural challenge but one that companies can partially mitigate by filing in Malaysia earlier in the global rollout sequence, using the NPRA’s acceptance of EU clinical data to reduce the incremental submission burden.

Investment Strategy — Malaysia

Malaysia is not a standalone investment thesis for most biosimilar developers. It functions most effectively as part of a broader ASEAN market entry platform. Companies building an ASEAN biosimilar business should model Malaysian procurement revenue with high uncertainty bands given tender cycle timing variability and pricing unpredictability, and weight the strategic value of NPRA approval primarily in terms of its contribution to regional regulatory credibility rather than standalone revenue. Manufacturing joint ventures with Malaysian partners — particularly in the context of the Malaysian Investment Development Authority (MIDA) biotechnology incentive programs — can convert the local content challenge into a genuine cost and market access advantage. MIDA offers pioneer status tax exemptions and infrastructure subsidies for qualifying biopharmaceutical manufacturing investments, providing a financial rationale for local production investment that goes beyond procurement scoring alone.

Part V — Patent Intelligence: Navigating the Thicket

The BPCIA ‘Patent Dance’ and Its Asian Equivalents

The US Biologics Price Competition and Innovation Act (BPCIA) created a formal, multi-step process for pre-launch patent dispute resolution between biosimilar applicants and originators. The process — colloquially known as the ‘patent dance’ — involves mandatory exchange of the biosimilar’s regulatory application (the aBLA) with the originator, a defined period for the originator to identify patents it intends to assert, a further exchange period for the biosimilar developer to respond, and a litigation phase focused on a subset of the most commercially significant patents before launch.

None of Japan, South Korea, or Malaysia has a procedure identical to the BPCIA patent dance. However, each has patent notification mechanisms for pharmaceutical products that trigger when a drug application references a registered originator product. In Japan, the PMDA requires a patent status declaration as part of the new drug application process, and the JPO provides an inter partes opposition process that can be used to challenge originator patents pre-launch. In Korea, the MFDS notification framework triggers a defined dispute resolution period when an originator’s registered patents are implicated by a biosimilar application. In Malaysia, the patent linkage system is less developed, but the Patents Act provides standard infringement and invalidity procedures before the Malaysian courts.