Last updated: June 20, 2026

Executive summary: Mesalamine has shifted from protected branded sales to a largely generic, price-competitive market across ulcerative colitis (UC) and Crohn’s disease (CD). U.S. revenue growth is constrained by widespread generic availability, frequent dosage-form substitution, and payor-driven rebate pressure. Near-term financial trajectory is shaped less by blockbuster-like patent exclusivity and more by: (1) erosion of remaining brand premiums, (2) channel mix between oral delayed-release versus rectal/extended-release products, (3) tenders and biosimilar-style “equivalent” switching dynamics for generics, and (4) regulatory and labeling fragmentation across different mesalamine delivery systems.

What drives the mesalamine market today: pricing, switching, and channel mix

Mesalamine’s market structure is dominated by generic competition. The therapeutic class is chronic, adherence-dependent, and requires ongoing maintenance. That supports volume durability, but not premium pricing. Revenue is therefore mostly a function of: (a) patient persistence, (b) prescriber and formulary behavior by dosage form, and (c) gross-to-net dynamics via rebates and discounts.

How do delivery systems affect product-level demand

Mesalamine’s commercial split tracks delivery mechanism and site of action:

- Oral delayed-release (DR) for UC colitis segment coverage

- Oral extended-release (ER) for specific release profiles and adherence

- Rectal formulations (suppositories, enemas) for distal disease

- Combination regimens (oral plus rectal) that raise total therapy cost but stabilize treatment frequency

This creates a structural pattern: even when the active ingredient is “the same,” payors and patients can distinguish products by release profile, dosing schedule, and tolerability. Generic entrants that are not perfectly substitutable at formulary decision time can face slower share capture, especially for rectal disease states.

What is the revenue impact of payer formulary management

Commercial outcomes are strongly influenced by:

- “Preferred generic” contracting for high-volume oral products

- Step edits for rectals in some formularies

- Ongoing rebate pressure that compresses net pricing even when list prices look stable

Net revenue is usually most sensitive when multiple equivalent generics compete simultaneously in the same NDC set.

What keeps mesalamine volumes stable despite generic erosion

Key demand stabilizers:

- Long-duration treatment of UC maintenance

- High clinical need for rescue-to-maintenance transition after flares

- Formularies that keep at least one low-cost option accessible for chronic therapy

The market typically stays resilient on units but loses value per unit.

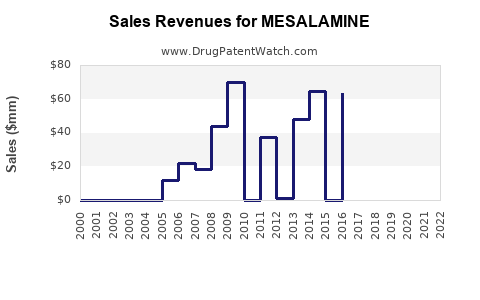

How has mesalamine financial performance evolved: U.S. revenue, share shifts, and price compression

Mesalamine is a mature category where financial trajectory is best described by unit stability plus net price decline. In this setup, the “winners” tend to be large generic platforms with manufacturing scale, efficient distribution, and strong contracting leverage.

U.S. market dynamics that typically govern mesalamine P&L

For a typical mesalamine manufacturer or label-holder, financial performance is driven by:

- Net price per script and per DDD (drug-daily-dose) after rebates

- Volume share in the preferred tier

- Litigation or exclusivity disruptions that temporarily protect segments

- Contracting cycles with PBMs and large integrated payors

Where the strongest financial pressure usually comes from

- Oral delayed/extended-release products are usually the most attacked by generic substitution.

- Rectal products can be more fragmented, creating pockets of share retention for specific dosage forms, but they still face pricing pressure as generics expand.

What patents protect mesalamine products and how does that affect revenue

Mesalamine is an active ingredient rather than a single, unified product. Patent estates differ by formulation, delivery system, dosing, and method-of-use.

Which IP categories most often matter commercially for mesalamine

- Formulation and delivery patents

Protect specific release profiles (DR vs ER), matrix designs, or coating approaches.

- Method-of-use patents

Cover dosing regimens, maintenance schedules, or specific patient subgroup claims.

- Manufacturing process patents

Less visible in market-facing narratives, but they can delay entry for certain process designs.

How exclusivity timing translates to financial outcomes

When exclusivity or brand-protecting patents lapse, generic entry usually produces:

- rapid share shift in oral products

- margin compression for remaining manufacturers

- higher marketing efficiency requirements and stronger rebate intensity

For mesalamine, exclusivity tends to be “segment-specific.” This means category revenue may hold up, while specific brands or specific dosage strengths lose share.

What is the Orange Book status of mesalamine: which drugs have listed patents

The Orange Book listing structure matters because it defines where Paragraph IV challenges, “skinny label” opportunities, and generic timelines appear. Mesalamine’s Orange Book status is also product-specific (by strength, dosage form, and application). Category-level analysis must translate to specific branded or NDA-held products.

How Orange Book listings influence generic launch calendars

- Orange Book-listed patents can delay generic approval until expiration or settlement.

- If patents are challenged via Paragraph IV, launch timing hinges on litigation outcomes or settlements.

- If no Orange Book patents are listed for a given dosage strength, entry timelines are driven by generic application readiness and exclusivity attached to the reference NDA.

What generic entry risks exist for mesalamine: Paragraph IV, settlements, and launch calendars

In mature small-molecule markets, entry risk is less about “whether” generics will come and more about “when” and “how quickly” they capture share.

Why litigation matters financially

Even when exclusivity is limited, litigation can:

- delay generic launches by months to years

- create “design-around” constraints for certain formulation variants

- shift market perception and contracting behavior for payors and distributors

What settlement-driven market behavior looks like

After settlements:

- generic launch volumes can ramp quickly if the settlement includes broad timing relief

- payors may accelerate switching once a low-cost preferred generic is confirmed as in-market

In practice, financial trajectory follows settlement calendars closely because net pricing responds to competitive entry.

How do payors treat oral vs rectal mesalamine: competitive pressure by segment

Mesalamine’s commercial story diverges by disease distribution and product segment.

Oral segments

- High script counts, strong formulary influence.

- Faster generic substitution typical.

- Net price compression is usually steep.

Rectal segments

- Smaller base but often more tolerability- and site-specific decisions.

- Switching can be slower due to adherence, administration technique, and disease positioning.

- Net price compression still occurs but can show more variation across NDCs.

How does mesalamine compare with competing IBD therapies: revenue resilience and risk

Mesalamine competes with multiple IBD maintenance approaches:

- aminosalicylates other than mesalamine

- corticosteroid regimens for flares (not maintenance)

- immunomodulators

- biologics and small-molecule anti-inflammatories for more severe disease

Mesalamine’s distinct advantage is safety profile and broad maintenance use in mild-to-moderate UC, which supports volume. Its financial risk is substitution by higher-efficacy therapies in patients who step up, plus ongoing generic pricing pressure.

Where mesalamine tends to outperform

- lower-risk patients on standard maintenance pathways

- settings where cost containment prioritizes aminosalicylates

Where mesalamine tends to lose

- escalation to biologics/small molecules

- patients with refractory disease who cycle through immunotherapy lines

What does the financial trajectory imply for investors: margin trends and growth levers

Mesalamine category economics typically favor scale and low-cost supply. Growth comes from:

- unit growth through new patient starts and persistence

- share gains in specific dosage strengths where contracting supports switches

- reduced cost of goods via manufacturing optimization

The constraint is that pricing is capped by generic parity and rebate intensity. Any “brand premium” tends to be temporary.

Which companies are likely to capture share: generic platforms and contract winners

In mesalamine, the competitive field often concentrates among major generic manufacturers that can:

- supply multiple strengths and dosage forms

- manage parallel distribution channels

- sustain rebate competitiveness in PBM-driven contracting

Share outcomes depend on which companies are “preferred” for key NDCs and whether any manufacturing disruptions or quality issues create supply gaps.

What manufacturing and IP barriers affect mesalamine market entry

Barriers that can slow generic erosion in specific NDCs:

- specialized coating or release technology for ER/DR products

- process validation requirements

- stability and bioequivalence requirements that limit rapid scale

- supply chain readiness across strengths

These factors can cause delayed penetration into particular segments even when generic approval is available.

Key takeaways

- Mesalamine’s financial trajectory is dominated by generic competition, which drives unit stability but suppresses net pricing.

- Segment-specific factors (oral ER/DR vs rectal) influence how fast substitution occurs and how much net revenue compresses.

- Patent and Orange Book dynamics are product- and strength-specific. When exclusivity or listed patents expire, category value typically shifts quickly toward the lowest net-cost suppliers.

- The market’s near-term outlook favors low-cost manufacturing scale and preferred-tier formulary status rather than premium product differentiation.

- Growth levers remain persistence and unit demand, while margin performance depends on rebate management and contracting outcomes.

FAQs

- Which mesalamine dosage forms usually experience the fastest generic price erosion?

- How do PBM formulary changes typically impact mesalamine net revenue versus list price?

- What factors determine whether a rectal mesalamine generic can displace the incumbent?

- How do patent settlements in mesalamine usually affect generic launch timing and share ramp?

- What role does escalation to biologics and small molecules play in long-term mesalamine demand?

References

- U.S. Food and Drug Administration. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. (Accessed 2026-06-21).