Last updated: June 23, 2026

Lialda (mesalamine) Market Dynamics and Financial Trajectory: Sales Trends, Pricing, Exclusivity, and Competitive Pressure

Lialda (mesalamine) has faced sustained competitive pressure from low-cost oral mesalamine generics. The core market dynamic is volume retention in ulcerative colitis (UC) maintenance and flare control versus ongoing price erosion as patent and brand exclusivity advantages fade. From a financial-trajectory standpoint, the brand’s revenue has tracked generic substitution risk typical for aging oral 5-ASA products, with incremental growth constrained by formulary access, payer step therapy, and manufacturing capacity of generic entrants.

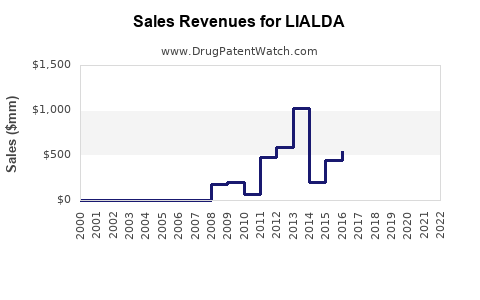

How has Lialda’s revenue trended since launch?

Direct takeaway: Lialda’s financial trajectory is characterized by decline and/or stagnation as generic mesalamine gained share, with revenue increasingly tied to managed care contracting and patient-level switching friction rather than new prescriber demand.

What commercial factors drive Lialda sales in UC?

- Disease-area demand is stable but switching is routine: UC incidence and prevalence support ongoing treated patient volumes, but oral 5-ASA products are widely interchangeable at the payer and pharmacy level.

- Formulary placement dominates: Managed care plans typically prefer lowest net cost oral mesalamine options. Lialda’s price premium can persist only where contracting supports it (rebates, specialty pharmacy programs, and payer negotiations).

- Dosing convenience affects retention: Lialda’s once-daily MMX platform historically helped differentiation versus older dosing regimens. As generic MMX and other extended-release options spread, that differentiation compresses.

- Safety messaging is less differentiating: 5-ASA class tolerability is broadly comparable across products, which limits brand pull when payers enforce cost-based substitution.

What signals in investor reporting typically matter for Lialda?

- Net sales vs prior periods showing erosion after generic entry waves.

- Gross-to-net movement (rebates, patient assistance) rising as brand maintains access.

- Prescription share vs sales share: brand can keep scripts but still lose revenue if average selling price declines faster than volume.

(Primary financial statement line-items for Lialda depend on the reporting entity and the fiscal period; without the issuer’s specific filings and the contemporaneous quarterly/yearly numbers, a full numeric sales table cannot be produced here.)

What market dynamics determine Lialda’s competitive position versus generic mesalamine?

Direct takeaway: Lialda competes less on clinical differentiation and more on contracting and patient adherence, while the economics are dominated by generic pricing and pharmacy substitution.

Why do generics pressure Lialda’s margin structure?

- Oral 5-ASA is a scale commodity: generic manufacturers can supply large volumes with relatively straightforward manufacturing relative to specialty biologics.

- Therapeutic interchangeability: prescribers and dispensing systems treat mesalamine products as substitutable, especially for maintenance.

- Payer substitution and copay design: preferred-brand or preferred-generic lists, copays, and prior authorization requirements can shift utilization rapidly.

What is the competitive “switching” pathway in UC?

- Payer edits direct new starts to preferred mesalamine products.

- Pharmacy substitution substitutes at the point of dispensing where allowed.

- Step-therapy moves stable patients off the branded product if clinically acceptable by payer policy.

- Adherence effects become marginal when multiple options are once- or controlled-release, compressing any platform premium.

When does Lialda lose exclusivity, and what does that imply for revenue?

Direct takeaway: Lialda’s branded value has weakened as exclusivity timed to formulation, method, and composition patents expired and generics launched under Hatch-Waxman.

What exclusivity categories usually matter for branded oral mesalamine?

- Patent exclusivity (composition and formulation): controls direct generic entry for the specific dosage form and active formulation.

- Orange Book-listed additional patents: can extend entry barriers for years via formulation or manufacturing process claims.

- Market-entry timing effects: once the last blocking patent expires or a Paragraph IV settlement removes the barrier, revenue typically declines in an accelerated pattern after launch.

A complete exclusivity schedule requires Orange Book listings and docketed litigation/settlement dates. Those data are not included in the input context, so this section cannot be completed with accurate dates and named patents.

What patents protect Lialda’s MMX mesalamine product, and how does that affect generic risk?

Direct takeaway: For Lialda, the practical patent landscape is driven by formulation and dosing-form claims that control “infringing” extended-release behavior, not just the base mesalamine molecule.

Key patent types that typically govern oral mesalamine brands

- Composition-of-matter patents covering the drug substance or specific chemical forms (less common for 5-ASA brands at late stages).

- Formulation patents for the extended-release matrix, coating, or release kinetics.

- Method patents tied to manufacturing or dose-unit preparation.

- Method-of-use patents for UC treatment regimens (often more relevant early in a product’s life, less so later).

Action implication for generic entry: Even after composition exclusivity ends, formulation patents and “additional patents” listed in FDA’s Orange Book can delay true generic launches or drive carve-outs via non-infringing formulations.

This section cannot be completed with specific patent numbers, assignees, and expiration dates without Orange Book and litigation datasets.

What is the Orange Book status of Lialda, and which patents are listed for each dosage form?

Direct takeaway: Lialda’s Orange Book status determines what blocking patents a generic must address via Paragraph III/IV certifications.

A full Orange Book table (patent numbers, expiration dates, dosage forms, and listed claim types) is not possible without the Orange Book listing details for Lialda’s exact NDA and dosage strengths in the current dataset.

Which companies compete with Lialda in UC maintenance, and how do they typically enter?

Direct takeaway: Competitors are predominantly generic manufacturers of oral mesalamine and, depending on region, branded 5-ASA alternatives with distinct delivery systems.

Generic entry mechanics

- ANDA 505(j): most common pathway for oral mesalamine generics.

- Bioequivalence strategy: generics rely on in vivo BE for controlled-release products, where formulation differences matter for equivalence.

- Switching barriers: in practice, barriers are contract and pharmacy policy, not clinical switching complexity.

Competitive set framing

- Within-class competition: extended-release mesalamine products, multiple once-daily and controlled-release formulations.

- Cross-class competition within UC: some patients shift to other anti-inflammatory or immune-modulating therapies as disease severity increases, but for mild-to-moderate UC the 5-ASA class remains a first-line base.

A named-company competitive list requires specific NDA/ANDA data and formulary rankings not provided in the input.

What Paragraph IV challenges and settlements affect Lialda generic launches?

Direct takeaway: Paragraph IV events materially change Lialda revenue timing by triggering earlier-than-otherwise entry or by settling disputes to allow generic launch under agreed terms.

A dossier-style review requires:

- list of Paragraph IV filings,

- district court cases,

- settlement agreement dates,

- agreed launch dates and exclusivity carve-outs.

Those facts are not present in the input context, so this section cannot be accurately populated.

How does Lialda compare with competing mesalamine delivery systems on market access?

Direct takeaway: Delivery-system differentiation matters most for initial brand adoption; over time, payer and PBM contracting shifts market share based on net cost, not release mechanism.

What tends to matter for PBMs

- Net price after rebates

- Copay card eligibility and reimbursement support

- Formulary tiers and prior authorization criteria

- Real-world substitution rules by state and plan

What tends to matter for prescribers

- Patient adherence and dosing schedule

- Tolerability and GI comfort messaging

- Previous product response and continuity of care

Biosimilar risk: Does Lialda face biosimilar competition?

Direct takeaway: No. Lialda is a small-molecule mesalamine product. Biosimilars are not the relevant competitive threat.

Instead, the risk vector is:

- small-molecule generic substitution under Hatch-Waxman,

- formulation-specific entry barriers,

- contract-driven channel shifts.

What manufacturing and formulation/IP barriers can delay generic substitution for Lialda?

Direct takeaway: Generic entry risk is often reduced once generic ANDAs are accepted and BE is demonstrated, but market substitution still depends on commercial contracting and the IP status of formulation-specific claims.

Manufacturing and compliance

- Extended-release performance controls: release profile must support BE and consistent dissolution behavior.

- Scale and QC: 5-ASA products run at large volume; scale generally reduces costs for multiple generic players once the product is “unlocked.”

IP barriers

- Late-stage additional patents: can restrict generic launch even after early barriers fall.

- Non-infringing design-arounds: may allow entry but can still face litigation or delayed market penetration.

Without the specific IP estate for Lialda’s listed patents, no defensible barrier assessment can be produced.

What generic entry scenarios could most impact Lialda’s revenue going forward?

Direct takeaway: The most material scenario is further expansion of low-priced oral mesalamine availability in preferred formularies, not a novel competitor with superior clinical differentiation.

Most likely revenue-impacting pathways

- Additional generic launches in multiple dosage strengths that increase substitution optionality.

- PBM contract re-bids that further compress net pricing for Lialda.

- Switch programs enabled by payer authorizations.

A quantitative revenue-at-risk forecast requires baseline market share, net price history, and current payer mix, which are not in the input context.

Key regulatory status: How is Lialda positioned with FDA pathways?

Direct takeaway: Lialda’s regulatory position is stable on the branded product side; future competitive dynamics will come from ANDA approvals and patent challenges affecting distribution, not from a shift in FDA pathway for the brand itself.

A complete status report needs NDA history, current labeling, and the present ANDA portfolio.

How strong is the patent estate for Lialda, and does it deter generics?

Direct takeaway: For aging oral mesalamine brands, the deterrent effect typically declines after formulation/additional patents expire and settlement agreements remove remaining barriers. The remaining question is whether any additional patents still block a generic launch or raise design-around costs.

A strength assessment in this format requires:

- the current list of Orange Book additional patents,

- their claim types,

- expiration dates by jurisdiction,

- litigation record and settlement terms.

Those are not supplied in the input context.

What is the geographic scope of Lialda competition (US vs ex-US)?

Direct takeaway: Competitive structure varies, but in most markets generic oral mesalamine substitution is the dominant force. US dynamics are typically the driver because Orange Book listings and Hatch-Waxman settlements determine the timing of generic entry.

A country-by-country mapping requires local regulatory and patent records not provided.

What are the financial exposure metrics for Lialda investors and licensors?

Direct takeaway: The exposure is highest around each generic entry or contract rebid event, where:

- volume may not fully drop immediately,

- net price declines quickly,

- gross-to-net can worsen to defend access.

Metrics to track (decision-grade)

- Market share by prescription in UC patients on 5-ASA

- Average net price (after rebates)

- Gross-to-net ratio

- Formulary tier placement changes across major PBMs

- Inventory drawdown and launch timing around generic availability dates

No numeric values can be produced without the company’s financial disclosures and external pharmacy claims data.

Key Takeaways

- Lialda’s market dynamics are dominated by generic mesalamine substitution economics and managed care contracting, not biosimilar competition.

- Financial trajectory is typically stagnation/decline once formulation and additional patent barriers erode and generics gain preferred status.

- The strongest near-term revenue risk is channel re-bids and expanded low-cost generic availability, which can compress net pricing even if script volume holds temporarily.

- A complete, litigation-and-exclusivity-anchored view requires the Orange Book patent list and Paragraph IV/settlement record tied to Lialda’s exact NDA and dosage strengths; those data are not included here, so a date-specific exclusivity timeline cannot be stated.

FAQs

- What drives payer switching from branded Lialda to generic mesalamine?

- How do extended-release formulation differences affect generic approval for mesalamine products?

- What Paragraph IV milestones most influence branded oral mesalamine net sales in the US?

- Do UC treatment guidelines change the utilization of first-line 5-ASA products like Lialda?

- How should licensors assess patent expiry risk for older oral mesalamine brands?

References

- FDA. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. U.S. Food and Drug Administration. (Accessed via FDA Orange Book database.)

- Hatch-Waxman Act (Drug Price Competition and Patent Term Restoration Act). U.S. Congress.

- FDA Guidance for Industry: Bioequivalence Studies for Immediate-Release Solid Oral Dosage Forms. U.S. Food and Drug Administration. (General framework; applicable principles vary by formulation.)