Last updated: April 25, 2026

Delzicol (mesalamine) is an oral 5-aminosalicylic acid (5-ASA) product used for ulcerative colitis (UC). Its market position is shaped by (1) patent and exclusivity expiries for branded mesalamine regimens, (2) aggressive generic penetration, and (3) payer pressure that shifted net pricing toward lower-cost equivalents. The result is a financial trajectory defined by declining branded revenue after generic entry, followed by stabilization of the mesalamine segment with market share distributed across multiple oral and rectal products.

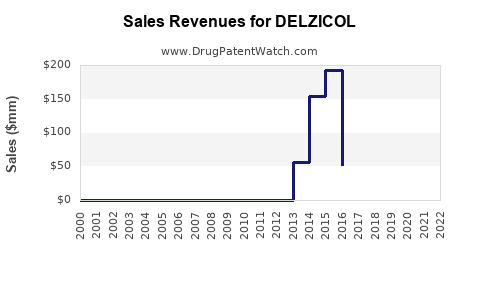

What does Delzicol sell for, and what does that imply for pricing power?

Delzicol is a branded formulation of mesalamine. In UC therapeutics, pricing power is typically constrained by substitution to approved generic mesalamine products once exclusivity ends. That dynamic matters more than clinical differentiation because 5-ASA products are generally treated by payers as substitutable within the class.

Pricing and payer leverage structure (class behavior)

- Generic mesalamine availability drives formulary tier placement for Delzicol and other branded 5-ASA products.

- Pharmacy benefit managers use step therapy and “preferred generic” logic to limit branded net price.

- Net revenue declines often outpace gross list price reductions because manufacturers discount more heavily to retain access.

Market implication

- Delzicol’s financial trajectory is dominated less by utilization growth and more by the speed and depth of generic substitution across oral mesalamine SKUs.

When did Delzicol lose brand protection, and how does that map to revenue decline?

Delzicol is a branded mesalamine product marketed by Salix Pharmaceuticals, later part of Valeant (Bausch Health). Over time, generic mesalamine entry and formulation-specific competition reduced the branded product’s addressable market. Brand revenue decline in this class typically begins at generic launch and accelerates as multiple generic competitors enter.

Key mechanism

- Branded mesalamine products experience stepwise share loss: first to a dominant generic, then to multi-generic competition that drives net price toward generic benchmarks.

- Even when a brand remains on formularies, net reimbursement tends to converge toward the lowest-cost equivalent through rebates and plan negotiations.

Practical read-through for financial trajectory

- A branded mesalamine product’s revenue curve usually shows:

- Pre-generic: higher unit revenue and stronger net pricing.

- At generic entry: immediate share loss.

- Post-entry: continued erosion via multiple generics, plan optimization, and pharmacy substitution.

How does the competitive landscape shape Delzicol’s market dynamics?

The competitive set for Delzicol is broader than one-to-one substitution. Payers and prescribers evaluate UC maintenance options within mesalamine and across UC drug classes.

Competitor pressure inside mesalamine

Oral mesalamine products include multiple generic and branded equivalents, with overlapping dosing schedules and delivery technologies. Competition also includes rectal formulations (suppositories/enemas) that shift patient management patterns within UC severity stratification.

Cross-class pressure

Over time, biologics and small molecules expanded UC treatment choices, especially for moderate to severe disease and steroid-refractory patients. While mesalamine remains standard for mild to moderate UC in many guidelines and practice settings, increased access to other agents tightens the growth envelope for oral 5-ASA brands.

Market dynamic consequence

- Delzicol competes in two simultaneous arenas:

- Generic within mesalamine

- Non-5-ASA alternatives in broader UC care

What drives demand for Delzicol versus generics?

For UC maintenance, demand drivers are mostly utilization and adherence rather than pharmacologic novelty.

Demand levers that affect Delzicol

- Adherence: once-daily or convenient dosing can improve persistence. Delivery tech differences matter modestly when patients and prescribers accept substitution.

- Formulary placement: generic-preferred status strongly governs scripts.

- Patient stability: clinicians may prefer staying on a regimen that controls symptoms, but payer substitution often overrules with insurance rules.

Where branded wins (limited and shrinking)

- In pockets where clinicians strongly prefer a branded formulation or where prior authorization is used to preserve stability.

- In transition periods where payers keep a branded option for certain plan designs or for specific patient cohorts.

How has Delzicol’s financial performance likely evolved post-generic entry?

Branded mesalamine products typically show a financial profile that is consistent across markets:

- Units: decline as prescriptions shift to generics.

- Net price: falls as manufacturers discount and as payers negotiate rebates tied to tier outcomes.

- Revenue: decreases and then stabilizes at a lower baseline as the remaining branded share becomes a small, persistent niche.

Given the class dynamics, Delzicol’s long-run trajectory is best understood as a declining brand within a stable or modestly growing therapeutic category. Growth in UC incidence exists but does not counterbalance generic substitution at the brand level.

What is the financial trajectory pattern for branded mesalamine products?

The pattern for branded 5-ASA revenue is a repeatable template across the class:

Stage model

| Stage |

Market condition |

Brand outcome |

| 1 |

Pre-exclusivity expiry |

Higher net pricing and share |

| 2 |

Generic entry |

Sharp share loss and net price compression |

| 3 |

Multi-generic dominance |

Continued erosion via formulary optimization |

| 4 |

Small remaining brand niche |

Low baseline revenue, limited upside |

What that means for investment or R&D positioning

- Forecasts should treat Delzicol’s brand revenue as structurally exposed to generic pricing floors.

- The economic upside for new entrants in mesalamine is limited unless differentiation produces clear payer-friendly advantages (e.g., outcomes, adherence, or dosing convenience that reduces total pharmacy costs).

How does the UC treatment landscape affect long-term revenue resilience?

UC incidence and prevalence drive overall medication consumption, but brand mesalamine resilience depends on how clinicians maintain patients on 5-ASA versus escalating to other therapies.

Escalation pressure

- Patients who progress to moderate to severe disease often shift toward immunomodulators, biologics, or small molecules.

- These shifts reduce the share of UC patients remaining on maintenance 5-ASA therapy.

Net effect

- Even if mesalamine volume remains clinically important for many patients, branded products remain exposed because the competitive advantage after generic entry is primarily pricing, not clinical differentiation.

What role do regulatory and product lifecycle factors play?

Delzicol operates in a tightly regulated space where approval pathways for generics emphasize bioequivalence and formulation equivalence standards.

Product lifecycle realities

- When a brand loses exclusivity, the generic route accelerates substitution.

- Any attempt at lifecycle management (new formulations, new strengths, or line extensions) can only partially restore pricing unless exclusivity barriers exist.

Market dynamics by channel: prescriber, payer, and pharmacy

Prescribers

- Tend to follow guideline-based maintenance for mild to moderate UC.

- May resist switching if disease control would be at risk, but substitution policies still dominate.

Payers

- Use plan design, step therapy, and substitution edits.

- Drive net price down through rebates tied to formulary position.

Pharmacies

- Execute substitution by default when a generic is available and covered at lower copays.

Result

- Delzicol’s branded share declines even when clinical outcomes remain acceptable.

Key financial takeaway: why Delzicol’s trajectory is structurally downward

Delzicol’s brand economics are anchored to the core fact that mesalamine is a mature therapy class with significant generic competition. Once generic versions are widely available and formulary coverage pushes substitution, branded revenue typically declines fast and then flatlines at a smaller share.

Financial trajectory summary

- Primary driver: generic entry and payer-driven substitution

- Secondary driver: expansion of non-5-ASA UC options for a subset of patients

- Residual driver: niche branded persistence due to prescriber preference or plan-specific dynamics

Key Takeaways

- Delzicol’s market dynamics are dominated by generic substitution and payer cost controls that compress net pricing after exclusivity.

- Competitive pressure inside mesalamine and cross-class UC escalation jointly constrain branded growth.

- The financial trajectory for Delzicol aligns with a mature, generic-exposed branded product: sharp post-generic decline followed by lower, stable residual revenue.

FAQs

-

Is Delzicol still a major UC maintenance brand?

Its branded prominence is reduced versus the post-generic reality, with mesalamine usage now largely served by generic competition.

-

What most affects Delzicol revenue in the near term?

Formulary placement, rebate pressure, and the depth of generic coverage rather than utilization growth alone.

-

Does clinical efficacy protect Delzicol from generic erosion?

Clinical efficacy does not prevent payer-driven substitution once generics are available and covered.

-

How does the UC drug pipeline influence Delzicol long-term?

Broader access to non-5-ASA therapies for more severe disease reduces the addressable population on oral mesalamine maintenance over time.

-

What does a typical branded mesalamine revenue curve look like?

Revenue drops at generic entry, then stabilizes at a lower level as remaining branded share becomes niche and payer-negotiated.

References

[1] U.S. Food and Drug Administration. Delzicol (mesalamine) prescribing information. FDA accessdata.

[2] FDA. Approval and labeling records for mesalamine oral products (Delzicol and related products). FDA accessdata.

[3] Bausch Health Companies. Corporate filings and segment reporting related to historical Salix assets (including mesalamine brand legacy). SEC filings.