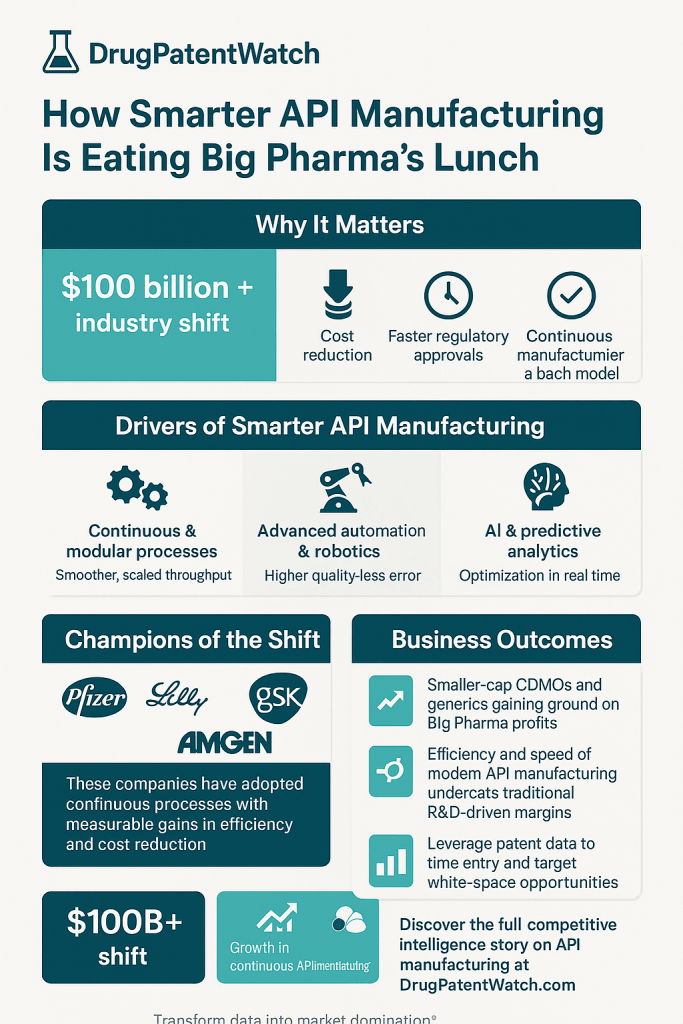

The pharmaceutical industry’s API manufacturing layer is undergoing a structural break, not an upgrade cycle. The convergence of continuous manufacturing (CM), Industry 4.0 process control, and AI-driven synthesis optimization is eroding the cost and quality advantages that large, vertically integrated manufacturers spent decades building through scale. What is emerging in their place is a new competitive model in which speed to market, process IP, and manufacturing data assets matter as much as molecular IP.

The numbers tell a direct story. FDA data shows that new drug applications built on continuous manufacturing processes earned approval an average of nine months faster and reached commercial supply twelve months sooner than comparable batch-based applications. McKinsey estimates that advanced analytics in pharmaceutical production can deliver 10-20% reductions in conversion costs and 10-15% reductions in cost-of-quality metrics. The Novartis-MIT Center for Continuous Manufacturing demonstrated that end-to-end integrated continuous manufacturing (ICM) can compress raw-material-to-tablet cycle times from 200 days to 2 days.

Those are not incremental efficiency claims. They represent a fundamental shift in where value accrues in the drug supply chain, and which companies capture it.

The competitive implications extend beyond operations. Continuous manufacturing generates dense process data that can itself become proprietary IP, layering process patents atop composition-of-matter claims and creating defensive patent estates that complicate generic Paragraph IV challenges. At the same time, the approaching 2030 patent cliff — roughly 200 molecules losing exclusivity — gives generic and CDMO players a finite, high-stakes window in which CM-based cost structures can deliver decisive first-to-file ANDA advantages.

This pillar page synthesizes the technical architecture of smart API manufacturing, the IP strategy it enables, the market data driving adoption, and the specific company-level case studies that separate genuine capability from marketing claims.

2. The API Market in 2025: Size, Patent Cliff, and Supply Chain Exposure

2.1 Global API Market Scale and Growth Trajectory

The global API market stands at approximately $238.4 billion in 2025, on a trajectory toward $405.1 billion by 2034 — a compound annual growth rate of roughly 6%. Technavio’s parallel projection puts incremental growth at $97.6 billion between 2025 and 2029, implying a slightly higher CAGR of 7.1%, driven by demand acceleration in oncology, biologics, and specialty generics.

North America held the largest regional share in 2024 at 38.36% of global market value, or approximately $86.7 billion. Asia-Pacific is the fastest-growing region, at a 6.37% CAGR, anchored by India’s generics manufacturing base and China’s dominance in KSM (key starting material) and advanced intermediates production.

China’s API market alone is estimated at $14.5 billion in 2025. That figure matters for a specific reason: over 80% of APIs used in U.S.-marketed medicines are currently sourced from China and India. That single-source concentration is not a theoretical risk. The COVID-19 pandemic produced documented shortages of finished drug products traceable directly to API supply disruptions originating from a handful of Chinese manufacturing provinces. The geopolitical exposure inherent in that structure — and the bipartisan political pressure to reduce it — is one of the cleaner tailwinds in pharma manufacturing today.

2.2 IP Valuation: The API Patent Landscape as a Core Asset

API-related patents are stratified into several distinct but overlapping categories, each with different IP valuations and vulnerability profiles. Composition-of-matter (CoM) patents protect the chemical entity itself and typically carry the highest valuation — patent term restoration under the Hatch-Waxman Act can extend CoM protection by up to five years (capped at 14 years of post-approval protection), and supplementary protection certificates (SPCs) in EU jurisdictions can add another five years on top of the standard 20-year patent term.

Below CoM patents sit formulation patents, method-of-use patents, and process patents. Process patents — covering the specific synthetic route, crystalline polymorph, or manufacturing conditions used to produce an API — are where the smart manufacturing revolution intersects most directly with IP strategy. A company that patents a continuous manufacturing process for an established API can, under the right circumstances, generate a defensible patent estate even after the underlying CoM patent expires. The Orange Book listing eligibility of manufacturing-process patents is limited (NDA holders typically list CoM and formulation patents, not process patents), but process patents retain full enforceability in litigation and can form the basis for preliminary injunctions against generic entrants who copy the method.

The market value of process patent portfolios has historically been underestimated relative to CoM portfolios, largely because process patents are harder to detect through standard competitive intelligence tools. Platforms like DrugPatentWatch provide structured access to this layer of the IP estate, enabling generic manufacturers, CDMOs, and IP counsel to identify which API processes carry active patent protection, when key manufacturing process patents expire, and where freedom-to-operate gaps exist for alternative synthesis routes.

2.3 The 2030 Patent Cliff: Scope and Strategic Implications

Approximately 200 small-molecule drugs are projected to lose exclusivity by 2030. Several of these are high-revenue products whose API manufacturing complexity has historically served as a practical entry barrier alongside formal IP protection. As CoM and formulation patents expire on drugs like Keytruda (pembrolizumab, though that is a biologic — the small-molecule cliff includes drugs like Entresto, Jardiance, Farxiga, Eliquis, and Xarelto), the manufacturing cost structure of generic API production becomes the primary competitive differentiator.

Eliquis (apixaban), with U.S. sales exceeding $12 billion annually, is among the most watched. Its CoM patent expired in 2019, but a thicket of formulation and use patents maintained exclusivity longer. Generic ANDA filers who can produce apixaban API via a CM process at lower COGS than their Indian and Chinese-based batch competitors will be positioned to sustain margin even under aggressive price competition post-launch.

Key Takeaways — Section 2

The API market is growing at 6-7% CAGR toward $405 billion by 2034, with North America holding the largest share but Asia-Pacific growing fastest. The 80%+ U.S. API dependency on China and India is a documented supply-chain vulnerability that domestic manufacturing initiatives are targeting directly. Process patents represent an undervalued but strategically important layer of the pharmaceutical IP estate, particularly as the 2030 patent cliff creates high-stakes generic entry opportunities in which manufacturing cost structure becomes the decisive competitive variable.

Investment Strategy — Section 2

Institutional investors should model the 2030 patent cliff not just as a revenue erosion event for branded manufacturers, but as a manufacturing-capability arbitrage opportunity. Companies with domestic CM-based API production for high-volume small molecules (apixaban, rivaroxaban, dapagliflozin, sacubitril/valsartan) are positioned to capture disproportionate generic market share at better margins than Asian batch producers, particularly as U.S. trade policy pressure on API sourcing accelerates. Long positions in CDMOs with verified CM infrastructure — Continuus Pharmaceuticals, Patheon (Thermo Fisher), and Samsung Biologics for the biologic tier — carry a different risk profile than positions in traditional batch-only generics manufacturers.

3. From Batch to Continuous: The Technical Architecture of Modern API Production

3.1 The Batch Processing Legacy: Operational Mechanics and Cost Structure

Traditional batch pharmaceutical manufacturing operates on a sequential, discrete-step model. Each unit operation — reaction, extraction, crystallization, filtration, drying — runs to completion before the intermediate product advances to the next step. Between steps, in-process testing consumes time, often days, and finished-batch release testing consumes additional weeks. The total cycle time from raw material intake to released API can run 100-200 days for complex molecules.

The Quality-by-Testing (QbT) paradigm that governs batch production is structurally reactive. Quality decisions are made post-hoc, after the batch has already been produced. If a batch fails in-process testing or final release testing, the entire batch is rejected — or, more commonly, placed on hold pending investigation, which involves root-cause analysis, regulatory notification, and potential batch disposition decisions that can take months.

Batch manufacturing also carries a substantial capital footprint. Large-scale batch API facilities require dedicated multi-purpose reactor suites, separate buildings for each major unit operation, extensive material handling infrastructure, and large intermediate storage capacity. A commercial-scale batch API plant for a high-volume small molecule can represent a capital investment of $200-500 million, with fixed costs that are largely independent of production volume.

The hidden cost in this model is variability. Batch-to-batch variability in API quality characteristics — particle size distribution, polymorphic form, residual solvent levels, impurity profiles — is an inherent feature of batch production, not a correctable defect. Each batch is a unique experiment. Regulatory submissions for batch-manufactured APIs must include statistical characterizations of acceptable variability ranges, and any excursion outside those ranges triggers regulatory reporting obligations.

3.2 Continuous Manufacturing: Integrated Process Architecture

Continuous manufacturing eliminates the batch paradigm by integrating all unit operations into a single, uninterrupted process stream. Raw materials enter one end of the system; finished API (or finished dosage form, in end-to-end implementations) exits the other, continuously and at a controlled rate. There are no intermediate batches, no inter-step hold periods, and no batch-release testing in the traditional sense.

The core technical components of a CM system for small-molecule API production include:

Continuous flow reactors (CFRs) handle the synthetic chemistry steps. Plug-flow reactors, microreactors, and continuous stirred-tank reactor (CSTR) arrays replace the large-scale batch reactors of traditional API plants. CFRs offer precise control over residence time, temperature, and mixing, enabling reaction conditions — particularly for highly exothermic or cryogenic reactions — that are impractical or hazardous at batch scale. Grignard reactions, nitrations, and lithiation steps that require strict temperature control at -78°C to -100°C can be run continuously in microreactor systems at a fraction of the capital cost of batch cryogenic reactors.

Continuous downstream processing covers extraction, washing, separation, and crystallization steps. Liquid-liquid extraction, for instance, can run in continuous counter-current extraction columns rather than batch separatory funnels. Continuous crystallization is technically the most challenging step — controlling crystal nucleation, growth kinetics, and particle size distribution in a continuous system requires sophisticated feedback control from in-line Process Analytical Technology (PAT) sensors.

Integrated real-time quality control runs continuously via PAT instruments including near-infrared (NIR) spectroscopy, Raman spectroscopy, UV-Vis inline photometers, and particle size analyzers. These instruments generate continuous quality attribute data that feeds directly into automated control systems. Under an FDA-approved Real-Time Release Testing (RTRT) framework, the system can release product quality determinations in real time, eliminating the separate laboratory testing step entirely.

3.3 Quality by Design vs. Quality by Testing: The Regulatory Calculus

The Quality by Design (QbD) framework, codified in ICH Q8, Q9, Q10, and now reinforced for continuous processes in ICH Q13, treats product quality as an outcome of process design rather than an outcome of testing. Under QbD, a manufacturer defines a Design Space — the multidimensional combination of input variables and process parameters that reliably produce API meeting all critical quality attributes (CQAs). Any operation within the Design Space is, by definition, compliant, without requiring regulatory approval for every process adjustment.

This matters enormously for continuous manufacturing because CM processes inherently operate across a range of conditions rather than at fixed set points. ICH Q13 provides specific guidance on how to define and justify Design Spaces for CM systems, including provisions for material attribute variability (managing API and excipient variability), control strategy documentation (specifying how PAT data triggers automated corrective actions), and batch definition (particularly important because CM systems do not produce discrete batches in the traditional sense — the batch can be defined by time, by mass of input, or by mass of output).

The FDA published its guidance on continuous manufacturing in 2019 and has been actively reviewing CM applications since then. Critically, FDA stated explicitly in a 2022 self-audit that NDA and ANDA applicants using CM received approval approximately nine months faster on average than batch applicants, and that CM products entered commercial manufacturing approximately twelve months sooner after approval. That is a twelve-month head start on revenue generation — a figure that compounds substantially for high-revenue products.

3.4 ICH Q13 and Global Regulatory Harmonization

ICH Q13, finalized in 2022 and adopted by FDA, EMA, PMDA (Japan), and Health Canada, is the first globally harmonized guideline specifically addressing continuous manufacturing of drug substances and drug products. Its adoption eliminates a significant source of regulatory uncertainty that previously deterred companies from investing in CM for products with global commercial ambitions.

ICH Q13 defines two types of CM operations: integrated continuous manufacturing, where API synthesis and drug product manufacturing run as a single connected process (the Novartis-MIT ICM model), and non-integrated CM, where the API synthesis and drug product manufacturing steps are continuous but conducted at different sites or times. The guideline provides detailed expectations for process control strategy, PAT method validation, batch definition, startup and shutdown procedures, and the management of process disturbances.

For IP counsel, ICH Q13 is relevant because it defines the technical vocabulary and process architecture that underpins process patent claims for CM-based API production. Patent applications claiming CM-based synthesis routes should be drafted to align with ICH Q13 terminology — citing specific PAT methods, control strategy elements, and Design Space parameters — to ensure claim scope is both defensible and clearly distinguishable from batch-based prior art.

Key Takeaways — Section 3

Batch API manufacturing is a structurally reactive, capital-intensive model with inherent quality variability and cycle times of 100-200 days. Continuous manufacturing compresses those cycle times to hours or days, shifts quality control to real-time in-process monitoring under an RTRT framework, and enables process intensification through flow chemistry that is technically impractical in batch equipment. ICH Q13 provides the global regulatory framework for CM adoption. FDA data shows a 9-12 month approval-to-market acceleration for CM-based applications.

4. The Enabling Technology Stack: IIoT, AI/ML, Digital Twins, and PAT

4.1 IIoT Sensor Infrastructure and Real-Time Process Data

Industrial Internet of Things (IIoT) deployments in pharmaceutical manufacturing begin at the sensor layer. Modern API production facilities instrument every critical process parameter point — reactor temperature and pressure, flow rates through continuous reactors, pH at extraction steps, crystallizer temperature profiles, particle size distributions in continuous crystallizers — with sensors connected to a centralized data acquisition system. The data density generated by a fully instrumented CM line is orders of magnitude greater than that produced by batch operations monitored only at discrete time points.

IIoT sensors in pharmaceutical CM systems serve four distinct functions. First, they feed real-time process data to automated control systems that maintain process parameters within defined Design Space boundaries. Second, they provide the data streams required for PAT-based quality determinations under RTRT frameworks. Third, they generate the historical process data that feeds predictive maintenance models — tracking vibration signatures, thermal profiles, and pressure differentials across pumps, heat exchangers, and compressors to predict component failures before they interrupt production. Fourth, they create audit-trail-compliant process records that satisfy FDA 21 CFR Part 11 data integrity requirements.

The market for IIoT-enabled pharmaceutical facilities held the largest technology segment share in 2024, precisely because sensor infrastructure is the prerequisite layer on which all other smart manufacturing capabilities depend. Companies that have not yet built robust IIoT data collection infrastructure face a compounding disadvantage: they cannot build predictive models without historical data, and they cannot generate historical data without instrumentation.

4.2 AI and Machine Learning in API Synthesis Optimization

AI and ML applications in API production span the entire process lifecycle, from initial synthetic route selection through commercial manufacturing optimization.

At the R&D stage, generative AI tools trained on chemical reaction databases can propose novel synthetic routes for target API molecules, predict reaction yields and selectivity under specified conditions, and flag potential impurity formation pathways before synthesis begins. Insilico Medicine’s experience — identifying a novel target and advancing to preclinical candidate in 18 months at a cost of $2.6 million — is frequently cited as a benchmark. The key claim for API manufacturing specifically is that AI-assisted route scouting reduces the number of experimental iterations required to identify an optimal continuous synthesis process, compressing the process development timeline before clinical-stage scale-up.

At the manufacturing scale, ML models trained on historical process data learn the multivariate relationships between process inputs (raw material attributes, reactor conditions, solvent properties) and process outputs (yield, purity, particle size distribution, polymorphic form). These models can predict, in real time, how a drift in one input variable will propagate through the process and affect downstream quality attributes — enabling pre-emptive automated corrections rather than post-hoc investigations.

Bosch’s pharmaceutical equipment division has deployed ML-based process optimization across tablet compression and coating operations, reporting measurable reductions in production downtime and material waste. Eli Lilly, a more directly relevant example, has integrated digital twin models with real-time analytics across multiple manufacturing sites, reporting reductions in unplanned downtime and improved API yield consistency.

AI-powered visual inspection systems represent a specific, well-documented application. In one reference case, a Landing AI system reviewed 50,000 quality inspection decisions and disagreed with human inspectors five times — and was correct in four of the five disagreements. That performance profile (lower error rate, no fatigue effects, continuous operation) is directly applicable to API crystallization monitoring and particle inspection in downstream processing.

4.3 Digital Twins: Virtual Process Replication and Predictive Control

A digital twin is a dynamic computational model of a physical process system, updated in real time from sensor data and capable of running predictive simulations faster than the real process runs. In pharmaceutical CM, digital twins at the unit-operation level model individual reactors, crystallizers, and separators. At the process level, they model the entire connected manufacturing line. At the enterprise level, they integrate manufacturing performance data with supply chain, inventory, and commercial demand data.

The practical value of digital twins in CM process development lies in their ability to compress experimental timelines. Rather than running multiple physical process experiments to characterize how the process responds to input variability or equipment changes, engineers run the experiments on the digital twin first. The physical experiments confirm the twin’s predictions and generate validation data, rather than serving as the primary discovery mechanism.

Eighty-six percent of industry respondents in a 2024 pharmaceutical manufacturing survey cited digital twin applicability in production operations as significant — a notably high consensus figure for a technology that was considered experimental as recently as 2018. Eli Lilly’s CM implementation is among the most cited examples of digital twin deployment at commercial scale.

For regulatory purposes, digital twin models that have been validated against physical process data can support Design Space justifications in regulatory submissions. FDA’s Emerging Technology Program, which reviews novel manufacturing technologies before formal NDA or ANDA filing, has engaged with digital twin-supported CM submissions, providing pre-approval feedback that reduces regulatory review risk.

4.4 Process Analytical Technology as the Quality Backbone

Process Analytical Technology (PAT) is the instrument layer that makes RTRT scientifically defensible. PAT instruments generate continuous in-process measurements of critical quality attributes without removing samples from the process stream. The primary PAT technologies deployed in API CM include:

Near-infrared (NIR) spectroscopy measures API concentration, polymorphic form, moisture content, and key impurity levels in real time via fiber-optic probes inserted directly into the process stream. NIR is particularly well-established for solid-state pharmaceutical applications and is routinely accepted by FDA as the primary measurement method for RTRT in continuous dosage form manufacturing.

Raman spectroscopy provides complementary CQA data, particularly for polymorphic form identification and crystallization endpoint determination, and performs better than NIR in aqueous systems, making it useful for API synthesis monitoring in flow reactor systems.

Focused Beam Reflectance Measurement (FBRM) provides real-time particle size and count data in crystallization systems, enabling closed-loop control of crystal growth kinetics — one of the most technically challenging aspects of continuous crystallization.

Mass spectrometry coupled to continuous flow reactors provides real-time impurity profiling, detecting formation of process-related impurities in the parts-per-million range as they form, rather than after batch completion.

The combination of these PAT instruments, integrated into a centralized process control system with validated chemometric models linking spectral data to CQA values, creates the evidentiary basis for an RTRT regulatory submission. ICH Q13 provides specific guidance on PAT method validation requirements for CM applications.

Key Takeaways — Section 4

The enabling technology stack for smart API manufacturing is hierarchical: IIoT sensor infrastructure at the foundation, PAT instruments for real-time quality measurement, AI/ML models for predictive process optimization, and digital twins for process simulation and Design Space validation. Each layer depends on the one below it. Companies that have invested sequentially in all four layers have created a manufacturing data asset that is genuinely difficult to replicate quickly, because the ML models and digital twins improve with accumulated process history — a compounding advantage.

Investment Strategy — Section 4

Companies with deep PAT-validated CM infrastructure are better positioned to support RTRT regulatory strategies, which in turn reduce post-approval manufacturing change notification burdens. That operational flexibility has direct revenue implications: a manufacturer who can adjust process parameters within an approved Design Space without a prior approval supplement can respond to demand signals faster than competitors constrained by traditional change control processes. For investors, PAT-validated RTRT capability is a leading indicator of regulatory agility, not just a manufacturing quality story.

5. The Competitive Arithmetic: Quantifying Cost, Quality, and Speed Advantages

5.1 Cycle Time and Throughput

The cycle time compression achievable through CM is the most dramatic quantitative claim in this space and also the best documented. The Novartis-MIT ICM platform reduced raw-material-to-tablet cycle time from 200 days (batch) to 2 days. That 99% reduction was achieved by eliminating inter-step hold times, integrating in-process quality testing into the process stream, and removing the batch release testing step through RTRT. Even partial implementations of CM — where only downstream drug product steps are continuous while the API synthesis remains batch-based — typically compress cycle times by 30-60%.

Pfizer reported a 50% reduction in production cycle time following its deployment of automation, connected worker tools, and smart manufacturing platforms across its network. That figure is broadly consistent with industry data showing that CM implementations at the drug product level (tableting, coating) can halve the time from API receipt to finished drug product release.

Syntegon’s Xelum platform for continuous oral solid dosage manufacturing is a well-documented commercial case. Xelum uses identical equipment modules at R&D scale and commercial scale, enabling direct transfer of process parameters without the traditional scale-up step. Scale-out — adding parallel process units to increase throughput rather than increasing the size of individual units — replaces scale-up entirely. This means process characterization and optimization work performed in development transfers directly to commercial manufacturing, eliminating the 12-24 month traditional scale-up phase.

5.2 Cost of Goods Reduction: The Data

McKinsey’s pharmaceutical manufacturing analytics benchmarking data identifies three quantifiable cost levers: 5-10% procurement savings from AI-optimized raw material purchasing and supplier management, 10-20% reductions in conversion costs (energy, labor, yield loss, rework) from advanced process control, and 10-15% reductions in cost of quality (testing, rejection, regulatory investigations) from real-time quality monitoring. Stacked, these represent a potential 25-45% reduction in total API manufacturing cost per kilogram for a company that fully implements the technology stack.

Equipment footprint reduction is another direct cost lever. CM requires physical plant that is more than ten times smaller than equivalent batch capacity for many solid-state small-molecule APIs. A CM facility producing the same annual API output as a traditional batch plant can occupy a single-story building rather than a multi-building campus. Capital costs for greenfield CM facilities are correspondingly lower. WSP estimates that CM facilities can cut energy consumption by up to 20% relative to batch facilities of equivalent output, driven primarily by the elimination of large batch reactors (which require substantial heating and cooling energy per cycle) in favor of continuously operating, thermally efficient flow systems.

Inventory holding costs fall substantially in CM operations because the process runs continuously from raw material to API, with minimal in-process inventory. For highly potent APIs (HPAPIs) — where material handling requirements are stringent and storage costs are high — the reduced inventory footprint has direct financial value. CM lines for HPAPIs can be designed as fully closed systems, reducing containment engineering requirements and associated capital costs.

5.3 Speed to Market: The FDA Continuous Manufacturing Approval Data

FDA’s 2022 self-audit of its continuous manufacturing review experience is the most authoritative public data point on regulatory timing. Applications built on CM processes achieved approval approximately nine months faster than comparable batch applications. After approval, CM-based products reached commercial supply approximately twelve months faster than batch-based products.

The mechanistic explanation for the post-approval speed advantage is straightforward: CM operations that run under RTRT do not require the separate batch release testing period that batch operations require. A batch-manufactured drug product spends weeks in the quality control laboratory after manufacturing is complete, waiting for finished-product test results before being released for distribution. A CM product operating under RTRT releases product continuously as it is manufactured, with quality determinations made in real time. The distribution supply inventory is available for patient use earlier.

For a product generating $1 billion in annual revenue, a twelve-month earlier entry to market has a net present value that easily justifies a substantial CM infrastructure investment.

5.4 Supply Chain Resilience: Quantifying the China/India Concentration Risk

The API supply chain’s geographic concentration is not a theoretical risk. The FDA’s Drug Shortage Staff database documents recurring API-driven shortages traceable to single points of failure in Chinese or Indian manufacturing. Sterile injectable APIs — including many oncology, anti-infective, and critical care products — are disproportionately affected because their manufacturing is concentrated in a smaller number of qualified facilities.

The U.S. Economic Development Administration’s Advanced Pharmaceutical Manufacturing (APM) Tech Hub initiative, funded at $500 million under the CHIPS and Science Act implementation framework, explicitly targets domestic API production capacity as a national security goal. The initiative’s overarching narrative projects that reshoring 350 medicines to domestic CM-based production would generate $17.85 billion in cumulative economic activity and reduce the frequency of critical drug shortages. The APM Consortium, anchored by universities, CDMOs, and technology vendors, aims to deliver API production outcomes two to three times faster than the current rate of domestic capacity build-out.

The EDA’s support for domestic CM-based API production means that companies investing in U.S.-based CM infrastructure have access to federal cost-sharing that partially offsets capital expenditure. That changes the investment calculus for domestic vs. offshore API sourcing decisions, particularly for products on the strategic medicines list.

Key Takeaways — Section 5

CM compresses API-to-market cycle times by up to 99% in end-to-end implementations, with more typical partial-CM deployments delivering 30-60% cycle time reductions. McKinsey data supports a 25-45% stacked COGS reduction for fully deployed smart manufacturing. FDA data shows a nine-month approval acceleration and twelve-month earlier commercial supply for CM-based applications. The $17.85 billion APM Tech Hub initiative creates federal cost-sharing for domestic CM capacity investment.

Investment Strategy — Section 5

The twelve-month earlier commercial supply advantage translates to a readily quantifiable NPV uplift for any product with annual revenues above $300 million, making the CM capital investment case straightforward. More strategically, domestic CM capacity positions companies favorably under evolving U.S. drug pricing and trade policy. The combination of EDA cost-sharing, IRA pricing negotiation exemptions for products in shortage, and competitive moats from CM-based COGS advantages creates a favorable policy and competitive environment for domestic API manufacturing investment through at least 2030.

6. IP Valuation and Patent Strategy in the Continuous Manufacturing Era

6.1 How Continuous Manufacturing Reshapes the Patent Thicket

The pharmaceutical patent thicket — the dense network of overlapping patents that branded manufacturers use to extend effective market exclusivity beyond the initial CoM patent expiration — traditionally involves a predictable set of patent types: new formulations, new salt forms, new polymorphic forms, new dosage regimens, and metabolite patents. Each layer is challenged through Paragraph IV ANDA certification, typically requiring generic filers to mount invalidity or non-infringement arguments against each listed Orange Book patent.

Continuous manufacturing introduces a new and underappreciated layer: process patents. A CM-based synthesis process for an established API — even one whose CoM patent has expired — can generate patentable claims covering the specific flow chemistry route, the PAT-based process control strategy, the continuous crystallization parameters, and the Real-Time Release Testing methodology. These process patents do not appear in Orange Book listings (FDA lists patents covering the finished drug product, not the API manufacturing process), so they are not subject to automatic Paragraph IV challenge in the ANDA process.

This creates a strategic asymmetry. A branded manufacturer who transitions to CM production of an established drug’s API obtains process patent protection that a generic competitor filing a Paragraph IV ANDA will not automatically address. The generic must independently develop its own API synthesis process — if it copies the CM process, it faces process patent infringement claims outside the ANDA framework, including potential preliminary injunction exposure.

6.2 Process Patents vs. Composition-of-Matter Patents: Valuation Framework

CoM patents for blockbuster drugs carry enormous IP valuations. Keytruda’s pembrolizumab patent estate, for instance, has been analyzed at valuations ranging from $40-80 billion based on discounted cash flow models applied to remaining patent exclusivity. Process patents for API manufacturing carry a different and generally lower valuation, but their strategic value lies in their interaction with generic competitive dynamics rather than in direct revenue protection.

A process patent covering a CM-based API synthesis route has three primary sources of IP value. First, it prevents generic manufacturers from adopting the same efficient CM process, potentially preserving a COGS advantage for the branded manufacturer’s authorized generic or its own generic subsidiary. Second, it creates licensing revenue potential if the CM process is genuinely more efficient than alternatives and generic manufacturers are willing to pay for access rather than developing their own route. Third, it can be used defensively to raise the cost and time of generic entry by forcing competitors to develop and validate alternative API synthesis processes, which requires substantial R&D investment and regulatory documentation.

Quantifying process patent value requires a different model than CoM patent valuation. The relevant metric is the manufacturing cost differential between the patented CM process and the best available alternative batch process, multiplied by the expected commercial production volume over the patent term. For a high-volume API produced at multi-ton scale annually, a $10/kg COGS advantage over a 15-year process patent term represents substantial cumulative value even before licensing premium is considered.

6.3 Evergreening Tactics and Continuous Manufacturing

Evergreening — the practice of filing secondary patents to extend effective market exclusivity beyond the primary CoM patent — is a well-documented pharmaceutical IP strategy, and continuous manufacturing creates new evergreening opportunities that complement traditional tactics.

Traditional evergreening routes (new formulations, new polymorphs, new dosage forms) are well understood by generic challengers and have been repeatedly litigated. The Inter Partes Review (IPR) process at the USPTO has made traditional evergreening patents increasingly vulnerable to post-grant invalidity challenges. As of 2025, the IPR institution rate for pharmaceutical formulation patents is approximately 60-70%, and invalidation rates for instituted patents run at roughly 65%.

CM-based process patents present a different IPR risk profile. Process chemistry claims rooted in novel flow chemistry approaches, specific PAT instrument configurations, or continuous crystallization control algorithms are likely to find less prior art than formulation or polymorph claims, making them harder to invalidate on novelty or obviousness grounds. The technical specificity of well-drafted CM process claims — describing specific reactor residence time windows, solvent system parameters, and PAT measurement protocols — makes the obviousness case harder to make in IPR.

For a company managing a patent cliff on a high-revenue product, layering CM process patents atop expiring CoM and formulation patents can extend the window of practical market exclusivity by the time required for a generic competitor to independently develop, validate, and obtain regulatory approval for an alternative API synthesis process. That window is typically 24-36 months.

6.4 Paragraph IV Filing Strategy and CM Process Patent Intersection

Generic ANDA filers must certify, for each patent listed in the Orange Book for the reference listed drug (RLD), that either the patent has expired (Paragraph II), the generic will not launch before expiration (Paragraph III), or the patent is invalid or will not be infringed by the generic product (Paragraph IV). CM-based API manufacturing process patents are not Orange Book-listed, so Paragraph IV certification does not apply to them.

This creates a specific strategic scenario: a generic manufacturer can successfully challenge all Orange Book-listed formulation and CoM patents via Paragraph IV, obtain tentative ANDA approval, and then face a separate process patent infringement suit brought by the branded manufacturer after the ANDA is approved — an action brought under 35 U.S.C. § 271(a) rather than the Hatch-Waxman automatic 30-month stay framework. The generic’s launch would not be automatically stayed by a § 271(a) suit, but the preliminary injunction standard (likelihood of success on the merits plus irreparable harm) could block commercial launch if the process patent claims are strong.

IP counsel advising ANDA filers should conduct freedom-to-operate (FTO) analyses covering not just Orange Book-listed patents but the full API process patent landscape, including patents assigned to the NDA holder’s API supplier or CM technology partner. Tools like DrugPatentWatch allow systematic identification of manufacturing process patents associated with specific drugs, providing the starting point for FTO analysis.

Key Takeaways — Section 6

Continuous manufacturing generates a new category of patentable IP — CM process patents covering flow chemistry routes, PAT-based control strategies, and RTRT methodologies — that is not subject to Orange Book listing and therefore does not face automatic Paragraph IV challenge. These patents carry lower absolute valuations than CoM patents but serve strategic functions in evergreening and in complicating generic entry. IPR vulnerability for well-drafted CM process patents is likely lower than for traditional formulation patents. FTO analysis for ANDA filers must cover API process patents, not just Orange Book listings.

Investment Strategy — Section 6

For branded pharmaceutical companies, the strategic value of CM process patent portfolios lies in their ability to raise the cost and complexity of generic entry in the post-CoM-expiry period. Companies that have built CM production for their highest-revenue products should be assessed not just on operational efficiency gains but on the strength of their process patent estates — specifically whether those patents cover novel flow chemistry steps, validated PAT methods, and continuous crystallization control algorithms that would be genuinely difficult for generic manufacturers to design around. For IP-focused investors, a CM process patent portfolio represents a lower-valuation but potentially higher-defensibility layer of the IP estate.

7. Case Studies: Who Is Winning and Why

7.1 Vertex Pharmaceuticals: Orkambi, Symdeko, and the CM IP Stack

Vertex’s cystic fibrosis franchise — Orkambi (lumacaftor/ivacaftor), Symdeko/Symkevi (tezacaftor/ivacaftor), Trikafta/Kaftrio (elexacaftor/tezacaftor/ivacaftor) — provides the clearest case study of CM adoption at a branded pharmaceutical company. Both Orkambi and Symdeko received FDA approval using continuous manufacturing processes for the drug product manufacturing step, making them among the first approved products to carry the CM designation in FDA’s product approval database.

The IP valuation context matters here. Vertex’s CF portfolio generated approximately $9.9 billion in 2024 net product revenues. The CM manufacturing processes for these products are patented alongside the CoM and formulation patents, creating a multi-layered IP estate. Critically, the CF portfolio faces a biosimilar/generic threat horizon that is longer than most small-molecule products due to the complexity of the modulator combinations, but the CM process patents provide an additional layer of protection for the manufacturing approach even after CoM exclusivity expires.

For IP analysts, the Vertex case demonstrates that CM adoption in drug product manufacturing (not API synthesis) can still generate protectable process IP, particularly when the CM process is integrated with the product’s specific formulation characteristics in ways that would not apply to a generic’s different formulation.

7.2 Novartis-MIT Center: The $85M Bet That Became Continuus Pharmaceuticals

The Novartis-MIT Center for Continuous Manufacturing, an $85 million collaborative research program initiated in 2007, produced the first demonstrated end-to-end integrated continuous manufacturing line for a pharmaceutical product. The platform reduced raw-material-to-tablet cycle time from 200 days (conventional batch) to 2 days — a 99% reduction — by running API synthesis, workup, formulation, tableting, and coating as a single, uninterrupted process.

The commercial spinout, Continuus Pharmaceuticals, is currently scaling this ICM platform to produce both API and finished tablets for a marketed generic drug, with a total end-to-end process residence time under 30 hours. The ICM platform’s commercial viability depends on several technical advances over the original MIT demonstration: robust continuous crystallization control, integrated PAT covering both API and drug product quality attributes, and automated process control that can maintain steady state through the startup and shutdown transients that are inherent in any continuous process.

From an IP perspective, Continuus holds a portfolio of patents covering specific aspects of ICM implementation, including control algorithms for managing the API-to-drug-product interface within a continuous process. These represent genuine process IP with defensible claims, not just operational improvements.

7.3 Pfizer’s 50% Cycle Time Reduction: Operational Details

Pfizer’s reported 50% production cycle time reduction reflects its systematic deployment of connected worker technology, automated workflow management, and smart manufacturing infrastructure across its global manufacturing network. Pfizer’s Kalamazoo, Michigan and Freiburg, Germany sites are the most often cited in its public disclosures as CM-enabled facilities.

Daurismo (glasdegib), approved by FDA in 2018 for acute myeloid leukemia, was manufactured using a continuous manufacturing process — one of the first Pfizer products to carry this designation. The manufacturing process for glasdegib was developed using QbD principles with an extensive PAT-based control strategy, and the NDA included a Design Space justification that allowed post-approval process adjustments without prior approval supplements within defined parameter ranges.

For investors, Pfizer’s CM investment is part of its broader “Global Supply Network” optimization program, which targeted $1.5 billion in manufacturing cost reductions over the 2020-2025 period. CM is one component of that program alongside site rationalization, external manufacturing optimization, and digitalization of quality systems.

7.4 Eli Lilly’s Verzenio and Digital Twin Deployment

Verzenio (abemaciclib), Lilly’s CDK4/6 inhibitor approved in 2017, is manufactured using a continuous manufacturing process for at least the drug product step. Verzenio generated approximately $4.1 billion in 2024 net revenues, making it one of the highest-revenue products currently manufactured under a CM designation.

Lilly’s broader manufacturing investment in digital twins and real-time analytics is documented in its corporate sustainability reporting. The company has deployed digital twin models across multiple manufacturing sites, targeting pre-emptive identification of potential quality or equipment issues before they affect production output. The specific claim — reducing unplanned downtime and improving API yield consistency — is consistent with the general ML model for predictive maintenance, though Lilly has not published quantitative performance data for public analysis.

7.5 Lupin Limited: Continuous Flow Reactor at Ankleshwar

Lupin, the Indian generic pharmaceutical manufacturer with approximately $3.3 billion in annual revenues, has deployed a continuous flow reactor (CFR) at its Ankleshwar API manufacturing facility in Gujarat. This is a meaningful data point because it demonstrates that CM adoption is not limited to large Western branded manufacturers — generic API producers with cost-competitive Indian manufacturing bases are also investing in flow chemistry.

Lupin’s CFR deployment targets specific synthetic steps in generic API production where flow chemistry offers yield, safety, or selectivity advantages over batch methods, rather than full end-to-end CM. This incremental approach is the most common model of CM adoption in the generic API sector: selectively applying flow chemistry to the steps where it offers the largest efficiency gain, while retaining batch methods for steps where they are already optimized.

From a competitive intelligence perspective, Lupin’s CFR investment signals that the competitive floor for API manufacturing capability in the Indian generic sector is rising. Companies that rely on pure batch API production for complex small molecules may find their COGS disadvantage relative to CFR-equipped competitors widening over the next five years.

Key Takeaways — Section 7

CM adoption among branded manufacturers is concentrated in drug product manufacturing steps, with Vertex, Pfizer, and Eli Lilly as the most documented cases. The Novartis-MIT / Continuus Pharmaceuticals platform represents the most advanced end-to-end ICM implementation, covering API synthesis through finished dosage form. Generic manufacturers including Lupin are adopting flow chemistry selectively for API synthesis, beginning a CM adoption cycle in the generics sector that will intensify as the 2030 patent cliff creates competitive pressure on API COGS.

8. The Biologics Challenge: Continuous Manufacturing for Large Molecules

8.1 Upstream vs. Downstream: The Asymmetric State of Biologic CM

Biologic API manufacturing — covering monoclonal antibodies (mAbs), antibody-drug conjugates (ADCs), fusion proteins, and recombinant enzymes — operates on a fundamentally different technical basis than small-molecule API manufacturing. Where small-molecule CM in flow chemistry is well-advanced, biologic CM faces a structural asymmetry: upstream continuous processing (perfusion cell culture, continuous clarification) is more technically mature than downstream continuous processing (continuous chromatography, continuous viral inactivation, continuous ultrafiltration/diafiltration).

Upstream bioreactor perfusion technology has been commercially deployed for over two decades. Genzyme (now Sanofi Genzyme) used perfusion bioreactors for imiglucerase (Cerezyme) production in the 1990s, and perfusion bioreactors are now the standard production mode for several high-value biologics where volumetric productivity advantages or product stability requirements favor continuous culture over fed-batch. Perfusion maintains cell viability at steady state by continuously removing spent media and adding fresh nutrients, achieving cell densities 5-10 times higher than fed-batch and enabling continuous product harvest.

Downstream continuous processing is where the technical gaps are most significant. Continuous chromatography platforms — including simulated moving bed (SMB) chromatography, periodic counter-current (PCC) chromatography, and continuous multi-column chromatography (CMCC) — have been demonstrated at pilot scale for mAb purification but face challenges in achieving the residence time consistency, viral safety demonstration, and regulatory acceptance required for commercial biologic manufacturing. FDA and EMA have received submissions incorporating downstream CM elements, but the regulatory precedent base is smaller than for small-molecule CM.

8.2 Biosimilar Interchangeability and Manufacturing Process Considerations

Biosimilar interchangeability — the FDA designation that allows pharmacists to substitute a biosimilar for the reference biologic without prescriber intervention — requires a demonstration that the biosimilar can be expected to produce the same clinical result in any given patient and, for products administered multiple times, that switching between the reference and biosimilar carries no additional safety or efficacy risk.

The manufacturing process is central to biosimilar interchangeability because the biological characteristics of a mAb or fusion protein (glycosylation profile, charge variant distribution, aggregation tendency) are process-dependent. A biosimilar applicant who adopts a continuous upstream process that produces a different glycosylation pattern from the reference product’s fed-batch process must demonstrate analytical and clinical comparability — a substantial evidentiary burden.

For CM adoption in biologic manufacturing, this creates a specific challenge: process changes that shift the product’s quality attribute profile require re-bridging studies and potentially new regulatory submissions. A biosimilar manufacturer who commits to CM must either demonstrate that their CM process produces an identical analytical fingerprint to the reference product’s batch process, or accept that they are not pursuing the interchangeability designation.

This is not a barrier to CM adoption in biologics — it is a framing for the additional regulatory work required. Wuxi Biologics and Samsung Biologics, two of the largest CDMOs in the biologic manufacturing space, have invested in continuous upstream processing infrastructure and have the analytical capability to conduct the comparability studies required for CM-based biologic submissions.

8.3 IP Valuation: Biologic API Manufacturing and the CMC Patent Estate

The Chemistry, Manufacturing, and Controls (CMC) patent estate for biologic drugs is more complex than for small molecules, reflecting the larger number of variables that influence biologic product quality. CMC patents for biologics can cover cell line engineering, expression vector design, cell culture media composition, upstream process parameters (feed strategy, pH control, dissolved oxygen setpoints), downstream purification protocols (resin chemistries, column loading conditions, elution gradients), and formulation compositions.

For a commercially approved mAb, the CMC patent estate is often as extensive as the CoM patent estate. AbbVie’s protection of Humira (adalimumab) is the most frequently cited example: the Humira patent estate included over 130 patents, a substantial fraction of which covered manufacturing and formulation aspects of the product, not just the antibody sequence or target binding claims. That patent estate successfully delayed biosimilar entry in the U.S. until 2023, despite EU biosimilar entry in 2018.

Continuous manufacturing for biologic APIs adds new CMC patentable subject matter: perfusion process parameters, integrated continuous downstream processing configurations, PAT methods for real-time glycosylation monitoring, and process control algorithms for managing the cell culture steady state. These represent genuinely novel IP relative to the conventional fed-batch CMC estate.

Key Takeaways — Section 8

Biologic CM is technically asymmetric: upstream perfusion technology is commercially mature, while downstream continuous processing remains largely at pilot scale. Biosimilar interchangeability requirements create additional analytical and regulatory burdens for biologic CM adoption that do not apply to small-molecule CM. Biologic CMC patent estates are large and complex, and CM adoption adds new patentable subject matter covering continuous process parameters and PAT-based quality control strategies.

Investment Strategy — Section 8

CDMOs with demonstrated continuous upstream bioprocessing capability (Wuxi Biologics, Samsung Biologics, Lonza) are better positioned to win biologics manufacturing contracts as biosimilar developers seek production efficiency advantages. For biosimilar developers specifically, the interchangeability designation requires analytical comparability to the reference product — which means CM adoption must be designed from the start to produce a product with an identical quality attribute fingerprint to the fed-batch reference. Companies that make this work gain a production cost advantage while retaining the interchangeability designation’s commercial premium in pharmacy-substitution markets.

9. The 2030 Patent Cliff: API Manufacturing as a Generic Drug Weapon

9.1 The Scope of the Cliff and a Target List Framework

The 2030 patent cliff is the largest wave of small-molecule drug patent expirations in pharmaceutical history. The products losing exclusivity include several with annual global revenues exceeding $5 billion: Keytruda (pembrolizumab — biologic, but illustrative of scale), Eliquis (apixaban, ~$12B globally), Jardiance (empagliflozin, ~$8B), Farxiga/Forxiga (dapagliflozin, ~$6B), Entresto (sacubitril/valsartan, ~$6B), and Xarelto (rivaroxaban, ~$5B in remaining markets with U.S. generics already launched).

Each of these represents a specific API manufacturing challenge for generic entrants. Apixaban synthesis involves a complex multi-step synthetic route with a key asymmetric induction step that requires either chiral auxiliary chemistry or asymmetric catalysis. Empagliflozin synthesis requires stereoselective C-glycosylation, a notoriously challenging reaction in batch chemistry that can be more effectively controlled in continuous flow systems. Sacubitril involves a convergent synthesis with a stereoselective reduction step.

For a generic developer prioritizing CM investment, the target selection framework should rank molecules by three variables: annual revenue (determining the revenue pool available for market share capture), synthetic complexity (determining where CM offers the largest process advantage over batch competitors), and CMC patent landscape density (determining whether the branded manufacturer has erected CM process patent barriers that would require alternative route development).

9.2 First-to-File ANDA and CM as a Cost Moat

The first-to-file ANDA advantage under Hatch-Waxman grants the first generic applicant a 180-day market exclusivity period, during which no other generic may be approved for commercial sale. This exclusivity period is commercially valuable — for a $5 billion drug, 180 days of shared generic duopoly with the branded manufacturer can generate $300-500 million in generic revenues for the first filer, depending on price erosion dynamics.

A generic manufacturer who has developed a CM-based API synthesis process before filing the ANDA is in a stronger competitive position than a batch-only competitor for several reasons. The CM process can produce API more rapidly once ANDA approval is granted, enabling faster commercial launch. The lower COGS from CM production allows more aggressive pricing during the exclusivity period while maintaining higher margins. The validated CM process, documented with extensive PAT data and process characterization, may support a more technically robust ANDA submission, reducing FDA review time and back-and-forth questions.

The 180-day exclusivity period also matters for CM investment justification. A company that invests $20-30 million in a CM-based API process for a drug approaching patent expiry can, if it achieves first-to-file status and successfully launches, recover that investment within the 180-day exclusivity window for any product with peak generic revenues above $200 million annually.

Key Takeaways — Section 9

The 2030 patent cliff involves approximately 200 small-molecule drugs with aggregate global revenues of hundreds of billions of dollars. CM-based API manufacturing creates a COGS moat for generic entrants who invest ahead of the cliff. Target selection for CM investment should prioritize high-revenue molecules with synthetically complex API routes where flow chemistry offers a demonstrable process advantage. First-to-file ANDA status combined with CM-based COGS advantages can deliver 180-day exclusivity period returns that justify the upfront CM development investment.

Investment Strategy — Section 9

Generic pharmaceutical companies with active CM development programs targeting 2030 patent-cliff molecules represent a specific investment thesis: they are pre-investing in manufacturing capability that will deliver returns when CoM and formulation patents expire. The key due diligence question is whether the CM process has been sufficiently de-risked through process characterization and PAT validation before the ANDA filing deadline — underdeveloped CM processes that are still in optimization at ANDA filing carry regulatory review risk. Companies with FDA Emerging Technology Program engagement for their CM-based ANDAs have demonstrated the highest level of regulatory de-risking.

10. Future Technology Roadmap: 2025 to 2035

10.1 Near Term (2025-2027): PAT Expansion, RTRT Adoption, and AI-Assisted Process Development

The near-term technology roadmap for smart API manufacturing centers on three areas of rapid deployment. PAT adoption is expanding from leading-edge innovators to the broader pharmaceutical manufacturing base, driven by ICH Q13’s regulatory clarity and FDA’s expressed preference for RTRT-capable CM applications. The key technical development in this window is the integration of mass spectrometry and ion mobility spectrometry as real-time process analytical tools, extending in-process quality monitoring to complex impurity profiles and genotoxic impurity surveillance.

AI-assisted synthetic route development is transitioning from research tool to standard workflow component. By 2027, AI route-prediction platforms (including Scinai, Chemify, and academic platforms like ASKCOS from MIT) will be integrated into process chemistry workflows at most top-20 pharmaceutical companies. The practical impact on API manufacturing is that CM-compatible synthetic routes will be identified earlier in process development, reducing the timeline for CM process design.

RTRT regulatory submissions will become standard for new CM applications. By 2027, FDA expects to have reviewed and approved at least 25-30 CM-based applications with full RTRT designations, creating a substantial body of regulatory precedent. That precedent will reduce the time required for FDA to review subsequent RTRT submissions, compressing approval timelines further.

10.2 Mid Term (2028-2031): AI-Native Synthesis and Smart Factory Rollout

The mid-term roadmap is defined by the deployment of AI-native synthesis platforms — systems where AI models control the flow chemistry process in real time, adjusting reaction conditions based on in-line analytical data without human intervention. This is technically more ambitious than current ML-based process monitoring, which operates primarily in a supervisory mode. True closed-loop AI control of synthetic chemistry requires process models of sufficient accuracy to predict the effect of real-time condition adjustments on downstream quality attributes, validated across the full Design Space.

Companies like Pfizer, Eli Lilly, and Novartis have published research programs targeting AI-native synthesis for specific reaction classes (particularly catalytic asymmetric reactions and photochemical reactions) in the 2028-2030 timeframe. The commercial deployment timeline depends on successful validation and regulatory acceptance of AI-controlled process parameters within ICH Q13 Design Space frameworks.

Smart factory rollout — the integration of robotics, automated material handling, and AI-based process orchestration into complete API manufacturing facilities — will expand from pilot implementations to multi-site deployment among top-tier manufacturers. The reference case is Syntegon’s Xelum platform for solid dosage, which has been commercially deployed at multiple sites. The equivalent for API synthesis, integrating continuous flow chemistry, automated workup, and continuous crystallization into fully connected, robotically assisted production systems, will reach commercial scale at leading CDMOs and captive manufacturer sites.

10.3 Long Term (2032-2035): Decentralized and Point-of-Care Manufacturing

The long-term manufacturing vision involves distributed, small-footprint API production closer to the patient population. This concept — variously called distributed manufacturing, point-of-care manufacturing, or on-demand pharmaceutical production — is technically enabled by the small plant footprint of CM systems and by 3D printing of drug products.

3D-printed pharmaceuticals, currently approved only for Aprecia’s Spritam (levetiracetam) in the U.S., allow production of individual, customized doses with specific release profiles that cannot be achieved with conventional tableting. The API manufacturing implication is that personalized dosage forms require small-batch or continuous-micro-scale API supply to the formulation step — a requirement that CM micro-reactor systems can meet more efficiently than batch chemistry.

Blockchain-based API traceability, integrated into distributed manufacturing networks, will address the supply chain provenance concerns that currently complicate regulatory acceptance of distributed drug manufacturing. Pharmaceutical-grade blockchain implementations will track API and excipient provenance from raw material source through each manufacturing step to finished product distribution, creating immutable compliance records.

10.4 Green Chemistry and Sustainable API Production

The environmental regulatory pressure on pharmaceutical manufacturing is growing across multiple jurisdictions. The European Chemicals Agency’s REACH regulations, the EPA’s pharmaceutical effluent guidelines in the U.S., and ESG reporting requirements under the EU Corporate Sustainability Reporting Directive (CSRD) are converging to make solvent waste, energy consumption, and carbon emissions material compliance considerations for API manufacturers.

CM processes have measurable sustainability advantages relative to batch manufacturing: a 20% reduction in energy consumption (WSP data), substantially reduced solvent volumes per unit of API produced (because flow chemistry enables more efficient reactions in smaller reactor volumes), and reduced aqueous waste from workup steps when continuous extraction systems replace batch separations.

Green chemistry principles — solvent selection guides, atom economy optimization, catalytic vs. stoichiometric reagent substitution — are increasingly integrated into CM process design from the outset, not retrofitted after route selection. Biocatalysis, using engineered enzymes for stereoselective transformations, is advancing rapidly as an alternative to traditional chemical asymmetric synthesis for chiral API production. Enzymatic processes run in aqueous media at mild temperatures, dramatically reducing organic solvent consumption and enabling integration into continuous aqueous process streams.

Key Takeaways — Section 10

The near-term roadmap (2025-2027) centers on PAT expansion, RTRT adoption, and AI-assisted process development entering standard workflows. The mid-term period (2028-2031) will deliver AI-native synthesis for specific reaction classes and broad smart factory rollout. The long-term horizon (2032-2035) targets distributed and point-of-care manufacturing enabled by small-footprint CM and 3D printing. Green chemistry integration with CM processes offers both environmental compliance advantages and process efficiency benefits through reduced solvent consumption and biocatalytic route adoption.

11. Challenges and Risk Factors

11.1 Capital Expenditure and ROI Timeline

The upfront capital cost of CM infrastructure is the most frequently cited barrier to adoption, particularly for mid-size manufacturers who cannot amortize the investment across a large product portfolio. A fully instrumented CM line for a small-molecule API — including flow chemistry reactors, PAT instruments, automated control systems, and a validated RTRT framework — requires a capital investment in the range of $15-50 million depending on throughput requirements and chemical complexity.

For large-molecule biologics, the capital cost of transitioning from fed-batch to continuous upstream processing is higher, because perfusion bioreactors, continuous clarification systems, and downstream continuous chromatography platforms require capital investment of $50-150 million for a multi-product clinical and commercial scale facility.

ROI timelines depend on product revenue and the size of the COGS advantage. For high-volume generic APIs approaching patent expiry, the ROI calculation is relatively straightforward. For low-volume specialty APIs with limited commercial shelf life, the COGS advantage may not justify the capital investment without additional value creation through process patent licensing or API supply partnerships with multiple customers.

The EDA APM Tech Hub cost-sharing and available contract manufacturing development grants from BARDA and DTRA reduce the effective capital cost for domestic U.S. CM investments, improving ROI timelines for manufacturers targeting strategic medicines categories.

11.2 Cybersecurity in Connected Manufacturing Environments

A fully instrumented CM facility — with IIoT sensors, networked PAT instruments, AI-based process control systems, digital twin infrastructure, and enterprise integration to ERP and quality management systems — presents a substantially larger cybersecurity attack surface than a traditional batch manufacturing facility. The pharmaceutical industry has experienced several high-profile cyberattacks, including the NotPetya attack in 2017 that cost Merck approximately $870 million in production losses and remediation expenses.

For CM facilities, the cybersecurity risk is qualitatively different from traditional manufacturing cyberattacks because a successful attack on a CM process control system could corrupt real-time quality decisions under an RTRT framework — potentially releasing substandard product before the compromise is detected. This is not a hypothetical risk; it is a recognized regulatory concern. FDA’s data integrity guidance explicitly addresses electronic records in automated manufacturing systems, and the NIST Cybersecurity Framework’s pharmaceutical sector implementation guidelines address RTRT-specific data integrity requirements.

Manufacturers implementing CM with RTRT should build cybersecurity architecture into the process control design from the outset, including network segmentation between the operational technology (OT) layer (PAT instruments, PLCs, SCADA systems) and the information technology (IT) layer (ERP, LIMS, quality management systems), intrusion detection systems on the OT network, and offline backup validation capabilities.

11.3 Ecosystem Maturity Requirements

Continuous manufacturing cannot be implemented in isolation. The transition requires simultaneous maturation of multiple supporting functions. Raw material specification and qualification must be tightened because CM processes are more sensitive to input variability than batch processes that can accommodate wide material attribute ranges through in-process adjustments. Suppliers of KSMs and advanced intermediates must be qualified to deliver tighter attribute specifications.

Equipment vendors must supply components designed for continuous operation rather than batch cycles. Tablet compression tooling, for instance, is typically designed for intermittent use; continuous tableting operations require tooling materials and designs validated for the fatigue loads of continuous operation. The supplier base for CM-compatible pharmaceutical equipment is smaller and more specialized than the conventional batch equipment supplier base.

Quality management systems and SOPs must be redesigned for continuous manufacturing principles. Batch record systems, deviation investigation procedures, product release criteria, and change control processes all require revision to reflect the absence of discrete batches and the presence of RTRT-based release decisions. This organizational change management component is consistently underestimated in CM implementation timelines.

11.4 Workforce and Knowledge Transfer

CM operations require a workforce with different skill profiles than batch manufacturing. Process chemists must understand flow chemistry principles and reactor design, beyond traditional synthetic chemistry training. Quality engineers must understand PAT method development and chemometric model building, beyond conventional analytical chemistry. Process control engineers must understand pharmaceutical-specific control system design, including the regulatory requirements for Part 11-compliant automated quality decisions.

Building this workforce requires either retraining existing personnel or recruiting from a limited pool of people with combined pharmaceutical and CM expertise. Universities with CM-focused pharmaceutical engineering programs — MIT, University of Strathclyde, TU Wien — are producing graduates with the relevant technical skill set, but the pipeline is not yet large enough to fully meet industry demand.

Augmented reality (AR) and virtual reality (VR) training platforms represent a practical near-term solution for knowledge transfer in CM facilities, enabling operators to train on virtual representations of CM equipment before working with physical systems. Several pharmaceutical CM operators have implemented VR-based training programs, reporting faster operator qualification timelines and reduced training-related process disruptions.

Key Takeaways — Section 11

The principal barriers to CM adoption are capital expenditure and ROI timeline uncertainty (particularly for mid-size manufacturers), cybersecurity risk in connected manufacturing environments, the need for simultaneous ecosystem maturation across raw material suppliers and equipment vendors, and workforce skill gaps. Each of these is solvable with sufficient investment and time. The companies that solve them fastest will accumulate the CM process expertise, validated manufacturing data, and process patent portfolios that create the most durable competitive advantages.

12. Analyst and Investor Framework: What to Watch

12.1 Metrics That Signal Genuine CM Maturity

Not all CM capability claims in pharmaceutical company disclosures reflect equivalent levels of process maturity. Analysts evaluating a company’s CM investments should distinguish between four maturity levels.

At the lowest level, a company has deployed CM equipment for drug product manufacturing (tableting, coating) but retains conventional batch API synthesis. This is the most common current state for large branded manufacturers and represents a meaningful efficiency improvement but not a fundamental shift in API supply chain strategy.

At the second level, the company has implemented continuous flow chemistry for specific API synthetic steps, with batch workup and downstream processing. Lupin’s Ankleshwar CFR deployment fits this model. This level delivers targeted efficiency and safety improvements but does not achieve the full cycle time or COGS advantages of integrated CM.

At the third level, the company runs a fully continuous API synthesis and workup process, with PAT-based in-process quality monitoring and a documented process control strategy meeting ICH Q13 requirements. This level enables RTRT applications and process patent filing for the CM route.

At the fourth and highest level, the company operates an end-to-end ICM platform integrating API synthesis through finished dosage form production, with RTRT designation, a validated digital twin, and a CM process patent estate. Continuus Pharmaceuticals’ ICM platform approaches this level for small-molecule generics; no commercial biologic manufacturer has fully achieved it for large-molecule production.

Specific metrics that indicate genuine CM maturity include: RTRT designation in FDA approval letters, Emerging Technology Program engagement before ANDA or NDA submission, process patents filed covering CM-specific synthesis routes and PAT control strategies, and publicly disclosed CM-related capital expenditure that is proportionate to the company’s product revenue base.

12.2 Red Flags in CM Adoption Claims

Several patterns in corporate CM disclosures should prompt skepticism.

Vague “digitalization” language without specific CM platform identification is a common red flag. “We are investing in smart manufacturing” without specification of which unit operations are continuous, which PAT instruments are deployed, and whether RTRT has been submitted to FDA describes an aspiration, not a capability.

CM adoption claims focused exclusively on drug product manufacturing (tableting, coating) while API synthesis remains entirely batch-based overstate the supply chain resilience and COGS improvement relative to companies with continuous API synthesis. The largest cost reduction opportunities in small-molecule manufacturing lie in the API synthesis and crystallization steps, not in downstream drug product manufacturing.

Large capital expenditure announcements for CM infrastructure without corresponding FDA Emerging Technology Program engagement or published process characterization data suggest either early-stage development (where the commercial timeline is uncertain) or investment in CM infrastructure that is not yet production-validated.

For CDMO-focused investors specifically, watch for the distinction between CM capability for a company’s own products versus CM service capability available to CDMO customers. A CDMO with CM infrastructure that has been validated only on its own internal development compounds has not yet demonstrated the platform portability and regulatory flexibility required to deliver CM services commercially to external clients.

Key Takeaways — Section 12

CM maturity exists on a four-level spectrum from drug-product-only CM through full end-to-end ICM with RTRT and process patent protection. Genuine maturity signals include RTRT designations in FDA approval letters, Emerging Technology Program engagement, and process patents covering CM-specific routes. Red flags include vague digitalization language, CM claims limited to downstream drug product steps while API synthesis remains batch, and capital investment announcements without regulatory engagement evidence.

13. Conclusion

The competitive shift in API manufacturing is real, measurable, and accelerating, but it is not evenly distributed. A small number of companies have built genuine CM capability across the full spectrum from process development through commercial production, regulatory approval, and process patent protection. A larger number are somewhere on the maturity spectrum. The majority of pharmaceutical manufacturers have not yet made the infrastructure investments required to compete at the highest CM capability level.

The strategic implications differ by company type. For branded pharmaceutical manufacturers, CM adoption serves three distinct purposes: operational cost reduction across the manufacturing network, process patent generation that extends effective exclusivity in the post-CoM-expiry period, and supply chain resilience in the face of geopolitical pressure on Asian API sourcing. All three are material to long-term revenue and margin sustainability.

For generic manufacturers and CDMOs, CM is primarily a competitive cost and speed weapon in the context of the 2030 patent cliff. Companies that have CM-based API manufacturing capability in place before the wave of CoM patent expirations hit will enter a period of sustained competitive advantage over batch-only competitors, with lower COGS, faster ANDA approval timelines, and more robust regulatory submissions.