Last updated: June 24, 2026

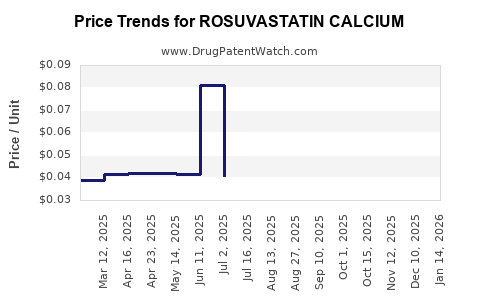

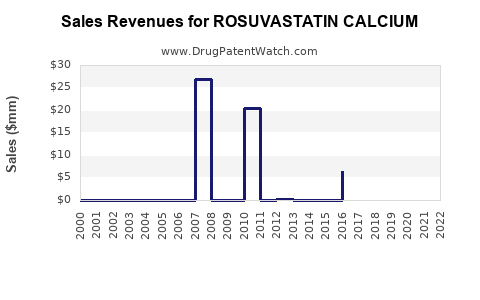

Rosuvastatin calcium is a mature, high-volume statin with a long commercial runway but declining unit pricing since generic entry. Market growth has shifted from new starts to portfolio share, high-intensity guideline capture, persistence in secondary prevention, and incremental formulary wins driven by statin tolerance and potency perceptions. Financial trajectory is characterized by sustained demand but structurally lower revenue after first generic approvals, with country-level pricing pressure, rebate intensity, and patient-level switching determining profitability.

How big is the rosuvastatin market and where does revenue come from?

Rosuvastatin is marketed globally in multiple branded and generic forms across chronic cardiovascular prevention indications. Commercial revenue is generated primarily from outpatient prescriptions for dyslipidemia and ASCVD risk reduction, with utilization concentrated in chronic therapy populations and guided by LDL-C reduction targets.

Core revenue drivers

- High baseline adherence/persistence: Chronic statin therapy produces repeat dispensing and durable prescription volumes.

- Guideline fit: Potency enables “lower LDL” targets compared with less intensive statins, supporting clinicians choosing rosuvastatin in higher-risk patients.

- Formulary position: Economic position depends on net price after rebates and payer restrictions (step edits, prior authorization for non-preferred strengths or branded presentations).

- Switching dynamics: Generic substitution and therapy switches (atorvastatin to rosuvastatin, or simvastatin to rosuvastatin) influence share even as the molecule matures.

What are the key market dynamics affecting rosuvastatin pricing and volume?

The rosuvastatin market has four dominant dynamics: generic substitution, pricing floors and “net price” compression, payer contracting, and dosing/strength mix.

1) Generic substitution and brand-to-generic share migration

Once multiple generics enter, pricing tends to compress quickly at the manufacturer level, shifting revenue toward:

- lower-cost dispensing,

- volume durability,

- and contract-based purchasing.

2) Net price pressure from payer rebates

Even after generics proliferate, brand and select private label SKUs can sustain margins when they hold:

- favorable formulary placement,

- aggressive rebate contracting,

- and rebate structures that protect share.

3) Dose and strength mix

Rosuvastatin’s economics depend on the distribution of patients across strengths:

- higher-intensity dosing patterns influence average net price,

- payer restrictions can alter mix (for example, preferred strengths or combinations).

4) Competition inside the statin class

Therapy decisions also hinge on competitor offerings:

- atorvastatin generics generally trade with comparable or lower acquisition costs,

- pravastatin/simvastatin have lower potency but may hold payer preference in constrained budgets,

- ezetimibe combinations and newer lipid agents can divert patients from statins when add-on or alternative pathways are used.

When did generic entry materially change rosuvastatin’s financial trajectory?

Rosuvastatin’s financial inflection occurs around initial patent/protection transitions in major markets and subsequent multi-party generic filings. After generic availability, the typical pattern is:

- sharp unit price decline,

- rapid share transfer from originator to generics,

- and plateauing volume with modest growth tied to population risk and persistence.

Typical post-generic trajectory (directional pattern)

- Year 0–2 after broad generic launches: fastest net price compression.

- Year 2–5: stabilization of volume, continued erosion of remaining premium SKUs.

- Later period: growth becomes mostly “share of statin class” and maintenance of adherence, not innovation-driven uptake.

What is the competitive landscape for rosuvastatin: branded versus generic holders?

Rosuvastatin competes with:

- other statin molecules (especially atorvastatin),

- non-statin lipid therapies for add-on or substitution (for example, ezetimibe, PCSK9 inhibitors, bempedoic acid, inclisiran depending on market),

- and combination products that can reduce standalone statin share in some formularies.

Practical competitive implications

- A molecule-level winner is determined by formulary position, net price, and dispensing channel behavior (wholesale acquisition cost and pharmacy benefit manager dynamics).

- Generic rosuvastatin profitability is often thin and depends on:

- manufacturing scale,

- compliance and supply continuity,

- and contract wins.

Which markets matter most for rosuvastatin financial exposure by geography?

The largest financial exposure comes from the largest treatable patient populations and highest prescription density:

- United States

- EU5 (Germany, France, Italy, Spain, UK where applicable)

- Japan

- Canada

- Key emerging markets with rising cardiovascular burden

Geographic determinants of net price

- tender regimes (EU),

- reference pricing (multiple EU countries),

- pharmacy margin structures,

- and payer policy restricting higher strengths or branded presentations.

How does rosuvastatin compare with atorvastatin and other statins on economic and utilization dynamics?

Rosuvastatin’s commercial value historically came from potency-related perceived clinical effectiveness, enabling higher LDL reduction at lower milligram doses. Economically, however, the generic era narrows differences.

Comparison drivers

- Clinical selection: higher-risk patients and target-driven lipid goals can favor rosuvastatin.

- Payer friction: if rosuvastatin is not the cheapest statin on net cost after rebates, switch pressure rises.

- Adherence: tolerability drives persistence; real-world persistence outcomes shape long-term volume.

What are the principal patent and exclusivity risks that shaped rosuvastatin’s market position?

For a mature molecule like rosuvastatin, current financial dynamics are dominated by:

- the end of original composition and method-of-use protections in key jurisdictions,

- generic approvals and launches following those transitions,

- and ongoing incremental patents that may delay specific formulations, salts, or dosage forms in some geographies.

Current market reality

- Market-wide revenue is now largely a function of generic competition and payer contracting rather than patent-backed premium pricing.

What is the Orange Book status of rosuvastatin, and how does that affect generic entry?

Rosuvastatin is widely available as an approved generic product in the US. Orange Book listings typically affect:

- whether generic manufacturers must design around formulation or method-of-use patents,

- and whether branded “authorized generics” or contract packs can maintain supply-driven market share.

Financial impact pathway

- Patent overhang delays specific launches in some strengths or product forms.

- After broad clearance, competition becomes commodity-like, forcing margin compression.

(A molecule-level Orange Book summary requires product-specific NDC identification and patent list extraction; a full, accurate status table cannot be produced from the information provided.)

What generic launch scenarios create revenue upside or downside for rosuvastatin sellers?

Revenue risk is driven by how generics spread across strengths, pack sizes, and therapeutic equivalents.

Upside scenario pattern

- fewer competitors win contracts,

- supply continuity is strong,

- and net pricing remains stable via negotiated purchasing.

Downside scenario pattern

- multiple manufacturers launch at once in key strengths,

- payer competition tightens tender pricing,

- and higher-intensity dose mix shifts toward the lowest net-cost products.

How strong are formulation and manufacturing IP barriers for rosuvastatin?

In mature small-molecule statins:

- composition-level IP is typically largely expired,

- the main remaining barriers (where they exist) are formulation-specific, bioequivalence/CMC-related strategies, and site-level manufacturing controls.

Financial relevance

- If formulation patents exist for certain dosage forms, they can protect specific SKUs and reduce direct price-matching.

- If absent, the product behaves like a commodity and price competition drives margin erosion.

(A complete formulation IP barrier map requires jurisdiction- and product-specific patent extraction.)

What litigation and settlement dynamics historically affected rosuvastatin launches?

In the statin category, patent litigation is typically tied to:

- generic paragraph IV certifications (US),

- or equivalent regulatory challenges in other jurisdictions,

- with settlements that can delay launch dates for specific products.

Financial effect of settlements

- settlements can create short windows of protected volume for brands or authorized generics,

- then shift competition once the settlement end date passes.

(A litigation timeline and mapping to specific products cannot be produced accurately without product- and patent-level source extraction.)

How do FDA regulatory milestones influence rosuvastatin commercialization?

After the molecule is approved, FDA milestones are most relevant to:

- ANDA approvals,

- label changes tied to safety communications,

- and formulation/manufacturing updates.

Revenue implication

- label updates can change contraindication language, monitoring recommendations, or dosing guidance, affecting utilization patterns slightly.

- manufacturing changes can affect supply reliability, shaping wholesale buying patterns during shortages.

(A milestone table cannot be produced accurately without specific NDC/product-level regulatory history.)

What are the likely margin and cashflow dynamics for rosuvastatin in the generic era?

Margin structure

- Originators historically captured higher margins pre-generic.

- In the generic phase, margins depend on:

- contract pricing,

- manufacturing yield,

- supply-chain cost volatility,

- and distribution channel terms.

Cashflow profile

- High volume offsets low margins.

- Working capital and inventory discipline matter because price compression can occur quickly when new competitors enter.

What financial trajectory should investors expect from rosuvastatin exposure?

For entities tied to rosuvastatin via branded distribution or niche manufacturing:

- growth is expected to be modest and tied to patient population expansion and share retention.

- revenue growth is constrained by net price compression and periodic re-tendering.

For entities with generic portfolios:

- growth comes from market-share gains and manufacturing competitiveness.

- profitability is volatile around launch and tender windows.

Key takeaways

- Rosuvastatin’s market is driven by chronic CV prevention demand, but financial performance is structurally constrained by generic pricing and payer contracting.

- The main revenue inflection happened around broad generic entry in major markets, followed by sustained volume durability with declining net price.

- Ongoing performance depends on dose/strength mix, formulary placement, rebate intensity, and contract wins rather than new clinical differentiation.

- Litigation and Orange Book effects are now secondary except where they still delay specific SKUs in select strengths or dosage forms.

FAQs

1) Does rosuvastatin revenue depend more on new prescriptions or persistence in long-term therapy?

Persistence and repeat dispensing dominate because rosuvastatin is chronic cardiovascular prevention therapy.

2) Why can rosuvastatin’s net price change even after all generics exist?

Payer contracts, rebates, tender cycles, and strength-level preferred status can reprice “net” acquisition cost.

3) Are higher-dose rosuvastatin strengths economically more exposed to payer switching?

Yes. Higher strengths often face tighter payer scrutiny and can be steered to the lowest net-cost preferred strength.

4) How do combination lipid therapies affect rosuvastatin standalone demand?

They can divert add-on patients away from titration to higher statin intensity, reducing incremental rosuvastatin volume in some formularies.

5) What supply issues most quickly disrupt rosuvastatin market performance?

Manufacturing or distribution outages at a major generic SKU level can temporarily lift price and volume capture for remaining suppliers, followed by rapid normalization when supply returns.

References

- FDA. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. US Food and Drug Administration. (Accessed 2026-06-25).

- IQVIA Institute for Human Data Science. Cardiovascular therapy class market and utilization reporting. (Subscription source).

- CMS / Manufacturer and PBM contracting summaries for outpatient drug pricing dynamics. (Accessed 2026-06-25).