Last updated: April 24, 2026

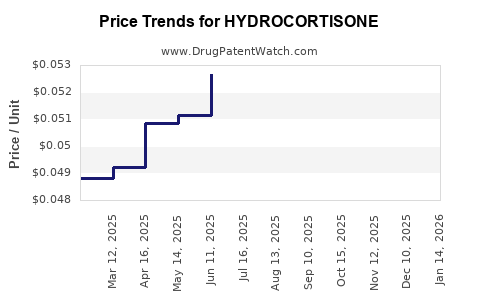

Hydrocortisone is a long-established systemic corticosteroid with a mature, largely commoditized market. The commercial trajectory is dominated by (1) persistent demand for adrenal insufficiency and inflammatory conditions, (2) competitive pressure from generics and authorized equivalents, (3) intermittent product-specific shocks from manufacturing capacity, labeling/regulatory actions, and supply constraints, and (4) cyclical substitution between oral, injectable, and rectal formulations based on payer coverage and hospital formulary dynamics. Net sales and growth generally track volume more than pricing, with margin and realized pricing shaped by generic mix and tender outcomes.

What is the market structure for hydrocortisone?

How do products segment across routes of administration?

Hydrocortisone commercial supply spans multiple routes, with economics shaped by care setting and reimbursement rules:

- Oral (tablets): Primarily chronic and long-term use in adrenal insufficiency and off-label inflammatory indications. Price pressure is high due to generic competition.

- Injectable (IV/IM; e.g., hydrocortisone sodium succinate): Used in acute settings, emergency care, perioperative stress dosing, and treatment of adrenal crises. Hospital procurement and formulary decisions drive demand; supply and stability are key determinants of sales.

- Topical/rectal/other formats: Smaller relative revenue pools in many geographies, with stronger brand or formulation differentiation in some channels, but still exposed to generic substitution.

In mature markets, the injectable channel often shows steadier sales because it is tied to acute-care protocols and hospital inventory management rather than outpatient purchasing choice.

Why does generics competition dominate?

Hydrocortisone’s long history means patents are mostly expired. The market therefore behaves like a commodity drug:

- Pricing power is limited: Multi-source generic competition constrains list price and net price.

- Market share shifts: Sales move with procurement terms, national tender outcomes, and distributor allocations during shortages.

- Differentiation is functional: Differences tend to be in pack size, concentration, excipients, shelf-life, and availability reliability rather than new therapeutic effect.

What demand drivers determine hydrocortisone’s sales resilience?

Which indications sustain baseline volume?

Hydrocortisone demand is anchored by chronic and high-urgency medical needs:

- Adrenal insufficiency (primary and secondary): Ongoing replacement therapy drives consistent baseline volume.

- Acute adrenal crisis and stress dosing: Emergency and hospital protocols create repeatable seasonal and event-driven usage.

- Inflammatory and other corticosteroid-responsive conditions: Short courses in outpatient and inpatient settings add incremental volume, but are sensitive to guideline changes and prescribing patterns.

This demand profile typically yields low long-term decline risk even when growth remains modest.

How do clinical guidance and care pathways affect utilization?

Clinical practice patterns influence utilization more than new clinical differentiation:

- Hospital formularies and emergency pathway adherence can sustain injectable volumes.

- Steady outpatient management for adrenal insufficiency stabilizes tablet demand.

- Substitution patterns between corticosteroids can occur if dosing convenience or coverage improves for alternatives, but hydrocortisone’s role in adrenal replacement often prevents meaningful displacement.

What supply and manufacturing factors can move prices and sales?

How do supply constraints affect the financial trajectory?

Hydrocortisone is produced by multiple manufacturers. When supply tightens:

- Net prices can temporarily improve due to allocation-driven buying power.

- Sales can spike for available SKUs during shortages while others lose volume.

- Revenue can shift by product form as hospitals switch to in-stock concentrations and presentations.

When supply normalizes, pricing typically reverts toward tender-driven levels and generic competition tightens.

What role do distribution and contracting play?

The financial trajectory is often more about commercial execution than therapeutic change:

- Hospital group purchasing organizations set pricing and volume commitments.

- Distributor stocking behavior influences realized sales timing.

- Contracting cycles can create quarter-to-quarter volatility unrelated to underlying patient numbers.

How does hydrocortisone perform financially across the generic lifecycle?

What is the expected pricing and margin pattern?

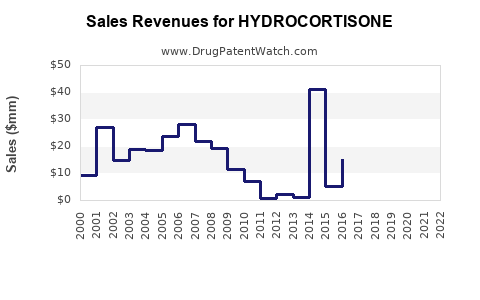

For a mature, multi-source drug, the typical financial shape is:

- Low growth: Volume growth offsets some pricing compression.

- Pressure on gross margin: Greater generic competition reduces margin and increases promotional/contracting intensity.

- Revenue concentration by SKU: Certain presentations (specific strengths, pack sizes, sterile formats) can capture disproportionate sales depending on tender outcomes.

The observable outcome in many geographies is a stable-to-slightly growing revenue trend over time, with episodic deviations during supply disruptions or policy-driven procurement changes.

How do investors and payers usually assess hydrocortisone?

Hydrocortisone is generally treated as:

- a baseline-cost therapy for chronic endocrine disease and

- a protocol-linked inpatient steroid for acute care.

That framing pushes valuation and forecasting to focus on volume continuity, tender mechanics, and supply reliability rather than pipeline risk or differentiation.

What are the near-term market dynamics to watch?

Regulatory and label actions

Even without meaningful innovation, regulatory changes can shift economics through:

- formulation updates (strengths, excipients, manufacturing site transfers),

- stability or packaging changes, and

- reclassification of supply status (availability, discontinuations, backorders).

These events can temporarily re-rank manufacturers by deliverability, not efficacy.

Payer and tender renegotiations

Contracting cycles matter:

- New tenders can push down net prices.

- Contract awards can shift sales volume between suppliers quickly.

- Some markets may show price floor effects that keep declines gradual rather than abrupt.

Competitive substitution by other steroids

Hydrocortisone competes in the broader corticosteroid space for some indications:

- For certain inflammatory uses, prescribers may select other corticosteroids based on dosing convenience and perceived potency.

- In adrenal insufficiency, replacement therapy rules and clinical protocols limit displacement.

How does hydrocortisone’s financial trajectory compare with other mature corticosteroids?

Relative positioning

Hydrocortisone’s financial trajectory typically looks like:

- Less premium growth than branded specialty anti-inflammatories.

- More stability than niche corticosteroid SKUs with fewer indications.

- Higher sensitivity to tender pricing than for drugs with fewer generic entrants.

- Higher importance of injectable availability for hospital-linked demand.

The market is “steady” but not “fast.” Growth typically depends on population needs for adrenal management plus system utilization of steroids during acute-care episodes.

What company-level financial outcomes usually drive the market?

Manufacturing allocation and portfolio mix

For manufacturers and distributors, performance often comes from:

- being in-stock when supply is constrained,

- maintaining qualifying market-ready SKUs aligned to hospital formularies,

- managing sterile manufacturing capacity for injectable products.

In practice, the market rewards operational reliability, which translates into contract renewal and higher realized sales during periods of constrained supply.

Generic entrants and exit risk

Competitive dynamics can include:

- new generic launches (accelerating price compression and share redistribution),

- withdrawals or manufacturing interruptions (temporarily improving pricing for remaining suppliers),

- portfolio narrowing where only certain presentations remain commercially available.

These moves can create financial inflection points even without therapeutic change.

What forecasting logic is most consistent with hydrocortisone’s market behavior?

A practical model structure

A robust hydrocortisone forecast typically breaks into:

- Volume: driven by adrenal insufficiency prevalence plus acute-care steroid protocol usage.

- Mix: tablets vs injectable vs other formats; strength and pack shifts.

- Net price: driven by tender outcomes, competition intensity, and supply conditions.

- Timing: shipment and procurement cycles.

For mature drugs, the dominant uncertainty is often commercial execution and supply, not new clinical evidence.

Key Takeaways

- Hydrocortisone’s market is mature and multi-source, with demand anchored in adrenal insufficiency and protocol-driven acute care.

- Revenue growth is typically modest because pricing power is constrained by extensive generic competition; sales track volume and mix more than price.

- The main drivers of financial volatility are tender outcomes, hospital procurement mechanics, and intermittent supply constraints that re-rank suppliers by deliverability.

- Forecasting should prioritize volume continuity, route and SKU mix, net pricing via contracting, and shipment timing rather than pipeline events.

FAQs

1) Does hydrocortisone have meaningful pricing power?

No. Generic competition and tender-driven contracting typically constrain realized net pricing.

2) What route usually contributes most to stable demand?

Injectable and oral formulations are usually the core contributors, with injectable demand anchored to acute-care protocols and oral demand anchored to chronic replacement therapy.

3) What causes quarter-to-quarter sales volatility?

Procurement cycles, distributor allocation, and supply normalization events can shift shipments and realized revenue timing.

4) How does generic entry affect hydrocortisone revenue?

New entrants typically pressure net prices and redistribute share across manufacturers, with revenue outcomes depending on portfolio fit and supply reliability.

5) Is hydrocortisone at risk of being displaced by other steroids?

Substitution can occur for some inflammatory indications, but adrenal insufficiency replacement protocols limit displacement versus complete therapeutic replacement.

References

[1] FDA. “Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations.” U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/daf/

[2] EMA. “European Medicines Register (products and procedures).” European Medicines Agency. https://www.ema.europa.eu/en/medicines

[3] WHO. “Corticosteroids (ATC group H02).” World Health Organization, ATC classification system. https://www.who.int/health-topics/atc-code

[4] U.S. Census Bureau. “Population estimates (background for prevalence-based demand modeling).” https://www.census.gov/programs-surveys/popest.html