Last updated: June 24, 2026

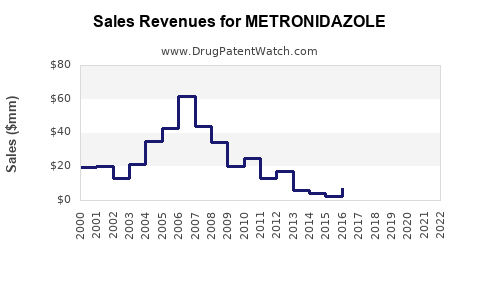

Metronidazole is an off-patent, widely genericized antibiotic and antiprotozoal with mature demand across oral, topical, and injectable segments. The financial trajectory is defined by (1) high generic penetration and substitution, (2) periodic supply and pricing cycles for sterile and dosage-specific presentations, (3) branded-to-generic conversion dynamics in women’s health and GI indications, and (4) limited incremental value from new formulations because core active ingredient IP is largely expired.

What is the current market size and revenue trend for metronidazole (US and global)?

Featured snippet answer: Metronidazole revenue trends track broader antibiotic category volumes and pricing cycles, with mid-single-digit to low-single-digit annual declines in value in many mature markets due to price erosion from generics, partially offset by stable usage for anaerobic infections, bacterial vaginosis, and amebiasis.

US market structure: which dosage forms monetize best?

Metronidazole monetization is typically concentrated in:

- Oral immediate-release tablets/capsules (systemic and common GI/gynecologic indications)

- Oral extended-release and prodrug/derivative variants only where present (historically smaller scale)

- Vaginal gels/creams and vaginal tablets (women’s health, recurrent demand)

- IV metronidazole (hospital-acquired anaerobic infection use and perioperative prophylaxis in some protocols)

Revenue is most sensitive to:

- Net price per unit (generic competition drives declines)

- Mix (IV share rises with inpatient utilization; oral dominates outpatient)

- Formulation availability (sterile fill-finish and supply disruptions can temporarily lift pricing)

Global revenue pattern

Globally, metronidazole behaves like a large-volume off-patent commodity:

- Higher growth in emerging markets usually comes from population growth and broader access to essential antimicrobials.

- Value growth in developed markets is constrained by aggressive price competition and formulary substitutions.

Financial trajectory expectation: steady volume, pressured price, episodic inflation from supply constraints.

What market dynamics drive metronidazole pricing and demand (antibiotic stewardship, substitution, formularies)?

Featured snippet answer: Demand is relatively stable because indications are entrenched in clinical pathways, but net revenue is continuously compressed by therapeutic substitution to low-cost generics and by stewardship rules that restrict broad-spectrum prescribing.

Demand stability levers

- Anaerobic infection protocols: metronidazole remains a standard component when anaerobes are implicated (often as part of combination regimens).

- Bacterial vaginosis (BV) and gynecologic use: metronidazole products have recurring utilization, including treatment and recurrence management.

- GI and parasitic indications: persistent use in amebiasis and related infections in endemic geographies.

Price pressure levers

- Multiple approved ANDAs and pharmacy substitution: rapid conversion after reference listing.

- Tender-based procurement in hospitals: strongest downward pressure on IV and institutional oral supply contracts.

- Stewardship-driven narrowing of use: may reduce “unnecessary” utilization but rarely eliminates core indications.

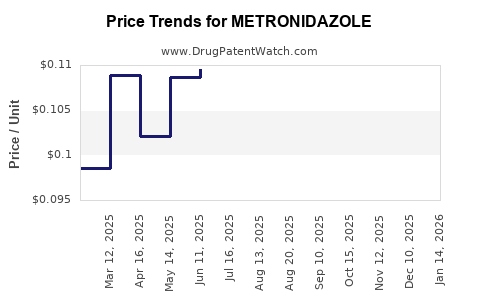

Supply and manufacturing bottlenecks

Metronidazole’s manufacturing footprint can concentrate key steps in fewer plants, so:

- Sterile product shortages can produce temporary price spikes.

- Excipient/formulation-specific constraints affect the availability of vaginal and IV SKUs disproportionately versus tablets.

How does the generic landscape for metronidazole shape the financial trajectory?

Featured snippet answer: Metronidazole’s financial profile is dominated by generic price competition, where the market leader depends on supply reliability and contracted hospital/tender performance more than on innovation.

Generic entry and substitution economics

- Once multiple ANDAs compete, the incumbent’s share declines quickly through:

- Wholesale and pharmacy substitution

- PBM formulary placement

- Institutional preference for contracted lowest cost

What determines which generic wins

- NDC-level availability and backorders

- Unit cost and shipping lead time

- Quality history and inspection outcomes

- Tender relationships with group purchasing organizations (GPOs)

Revenue concentration risk

For manufacturers, revenue is vulnerable to:

- Loss of contracted slots

- Temporary plant outages

- Compliance-driven discontinuations

What is the patent and exclusivity situation for metronidazole, and when does exclusivity end?

Featured snippet answer: The active ingredient metronidazole is off-patent. Most remaining IP and exclusivity are formulation- and use-specific, with long ago-expired primary composition coverage driving today’s generic dominance.

Composition and core process IP

- Active ingredient protection for metronidazole dates back to earlier decades and is not a practical barrier to generic manufacturing in most major markets today.

- Modern competitive differentiation is largely formulation, stability, and manufacturing compliance, not composition patents.

Formulation and method-of-use remnants

Even with core off-patent status:

- Some products may still have secondary patents around specific salt forms, release characteristics, packaging, or administration regimens.

- In practice, these remnants tend to affect niche SKUs rather than the entire molecule market.

How many patents protect metronidazole formulations and what types matter commercially?

Featured snippet answer: The economically relevant patent estate for metronidazole is concentrated in secondary patents and life-cycle around particular dosage forms and clinical claims, not the base active ingredient.

Patent types that affect product-level risk

- Composition of matter for a specific formulation

- Dosage form patents (vaginal gels/creams, IV stability, controlled release concepts)

- Method-of-use patents (specific regimens, specific patient subpopulations, or combination therapies)

- Manufacturing/process patents (crystallization, impurity controls, sterile fill methods)

Commercial relevance

The largest financial impact occurs when:

- A secondary patent covers a commercially dominant dosage form in a high-volume indication.

- A manufacturer’s product uses a protected formulation approach that prevents ANDA carve-outs.

In most cases for metronidazole, the active ingredient’s off-patent status limits overall monopoly value.

What Orange Book status applies to metronidazole products (and how does it influence generic entry)?

Featured snippet answer: Orange Book coverage for metronidazole products is typically limited to residual exclusivities and secondary patents per specific NDA/NDCs, while generic entry has largely already occurred for most major SKUs.

How Orange Book listings affect market shares

- Orange Book barriers matter most at the NDC level.

- Once the listing is inactive or expired, ANDA approvals and automatic substitution accelerate.

Practical result

For investors and licensors, the metronidazole market is best treated as:

- A commodity-like IP environment where company differentiation is execution-driven.

What Paragraph IV patent challenges or metronidazole litigation has historically affected entry?

Featured snippet answer: Patent challenges for metronidazole have occurred at the formulation or product level, but they rarely change the overall market structure because multiple generics already supply most segments.

What to watch if litigations occur

When challenges surface, they usually aim to:

- Carve out around a specific patent listed on a particular NDA

- Attack validity or non-infringement of a formulation/method patent

Financial impact pattern

Even when litigation delays entry:

- The delay is typically measured in months to a limited time window.

- Market revenue recovers when additional supply enters quickly due to widespread generic capacity.

How does metronidazole compare with alternative therapies for anaerobic infections and BV?

Featured snippet answer: Metronidazole faces substitution from other antibiotics for some indications, but it retains a durable role because anaerobic coverage and BV efficacy are well-established, and generics keep it cost-advantaged.

Anaerobic infection comparators

- Beta-lactam/beta-lactamase inhibitor combinations that cover anaerobes can substitute in some settings.

- Carbapenems cover anaerobes broadly but are typically reserved due to stewardship and cost.

BV comparators

- Clindamycin products and other BV-specific regimens compete for share.

- Switching patterns depend on:

- Tolerability profiles

- Recurrence patterns

- Local guideline adoption and payer preference

Financial implication

Metronidazole’s cost base helps it keep share, but recurrence and antibiotic guideline shifts can re-balance mix across classes.

What are the main growth opportunities for metronidazole revenue (and where is upside limited)?

Featured snippet answer: Growth upside is mostly in volume expansion and mix into settings that use higher-cost sterile and women’s health presentations, with limited value from IP-driven premium pricing.

Realistic upside sources

- Emerging market tender growth for essential antimicrobials

- Institutional inventory turns if supply disruption reduces availability of competitors

- Formulation-specific reliability improvements that win contracts

Where upside is limited

- Premium pricing is structurally constrained by generic competition.

- Broad new indications would need clinical differentiation and sustained premium pricing, which is difficult for an off-patent commodity.

How does metronidazole IV vs oral vs topical revenue typically differ?

Featured snippet answer: IV and sterile topical SKUs can have higher revenue per unit and more pricing volatility, while oral tablets usually anchor volume at lower net price.

IV (hospital-driven)

- Revenue sensitivity to:

- Inpatient utilization

- Procurement contracts

- Sterility and supply continuity

Oral (outpatient-driven)

- Revenue stability is higher, but net price declines faster once additional generics enter.

Vaginal products (women’s health)

- Smaller total volumes than oral, but often higher persistence from guideline-based regimens.

- Demand can be impacted by recurrence and adherence.

What generic entry risks exist for branded or legacy metronidazole products?

Featured snippet answer: The primary risk is not re-entry from a single future challenge but ongoing price erosion from additional approved generics, plus SKU-level discontinuations that can temporarily cede share.

Risks by category

- Brand-like remnants: limited as metronidazole is already generic-dominated.

- Residual exclusivity SKUs: risk when the last listed patent expires or when litigation ends.

- Supply discontinuations: risk when a manufacturer exits due to compliance or manufacturing economics.

What commercial outcomes have settlement agreements and licensing deals historically produced in this category?

Featured snippet answer: Settlements in off-patent antibiotic markets tend to govern launch timing of specific generic SKUs rather than restore long-term pricing power for the active ingredient.

How settlements translate into revenue

- If an agreement delays a competitor’s entry:

- The incumbent may keep share at higher net price for a limited period

- If non-exclusive licensing is involved:

- Pricing normalization occurs quickly after launch

Practical market effect

Expect most revenue outcomes to be:

- Short-term share protection

- Temporary pricing lift until additional supply enters

What is the regulatory status landscape for metronidazole (FDA pathways, inspections, and post-market requirements)?

Featured snippet answer: Metronidazole is regulated through a mature generic portfolio with ANDAs for oral and topical products and approvals for sterile IV products, subject to ongoing GMP and post-market reporting.

Key regulatory drivers for competitors

- GMP compliance and sterile manufacturing validation

- Stability and shelf-life control

- Bioequivalence requirements for generics

- Supply chain continuity

Regulatory risk for producers

- Facility issues can lead to:

- Holds

- Warning letters or consent decrees

- Product discontinuations that create market pricing volatility

Key company and competitive landscape dynamics for metronidazole

Featured snippet answer: The market is supplied by multiple generic manufacturers, with leadership determined by contract execution, product availability, and cost structure.

Competitive factors that move unit share

- Contract placement with wholesalers and GPOs

- Portfolio breadth across dosage forms (oral, vaginal, IV)

- Ability to maintain consistent NDC supply

Investor lens

- Profitability tends to be constrained by price competition.

- Cash flows track operational reliability and the ability to maintain market share through procurement cycles.

Timeline: how metronidazole economics typically evolve across a life cycle

Featured snippet answer: Revenue follows a pattern: initial branded pricing, then step-down after generic introductions, then commodity-level price compression with episodic rebounds tied to supply.

Generic-driven life cycle (typical pattern)

- Pre-generic: higher margins, limited entrants

- Early generics: share splits among multiple ANDAs, rapid net price declines

- Mature generics: near-commodity pricing, profitability depends on scale and supply continuity

- Supply disruptions: temporary pricing/volume boosts for available SKUs

Key Takeaways

- Metronidazole’s financial trajectory is shaped primarily by generic price erosion and SKU-level supply continuity, not active-ingredient exclusivity.

- Demand is comparatively stable due to entrenched indications (anaerobic infections and BV), but net revenue is constrained by therapeutic substitution and formularies.

- IV and sterile-related presentations show more pricing volatility because contract procurement and supply disruptions move unit economics faster than oral tablets.

- IP effects are usually secondary and product-specific; the overall market behaves like an off-patent commodity where execution drives outcomes.

FAQs

1) Why does metronidazole price sometimes spike even with heavy generic competition?

Spikes usually tie to sterile manufacturing constraints, short supply of specific NDCs, and procurement-driven scarcity that temporarily lifts net pricing before additional supply normalizes.

2) Which metronidazole dosage form is most exposed to hospital tender pressure?

IV and institutional SKUs are most exposed because hospital purchasing is contract-centric and rapidly reallocates volume to lowest-cost, reliably supplied NDCs.

3) How do stewardship guidelines affect metronidazole market demand?

They can reduce low-acuity or non-indicated use, but core guideline-based roles in anaerobic infection regimens and BV treatment typically preserve baseline demand.

4) What drives switching between metronidazole and alternative BV therapies?

Payer preference, formulary tiering, tolerability, recurrence patterns, and product availability drive switching more than clinical novelty in a mature category.

5) Is there meaningful upside from new metronidazole formulations?

Upside is usually limited unless a new formulation wins a measurable advantage that changes payer behavior or creates a differentiated, protected niche at the NDC level.

References

- US Food and Drug Administration. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. https://www.accessdata.fda.gov/scripts/cder/daf/

- US Food and Drug Administration. Drug Shortages. https://www.accessdata.fda.gov/scripts/drugshortages/

- FDA. ANDA regulations and bioequivalence framework. https://www.fda.gov/drugs/abbreviated-new-drug-application-anda