Last updated: May 30, 2026

Metrog el (metronidazole topical gel) market dynamics and financial trajectory: sales trends, payer dynamics, competition, and exclusivity risk

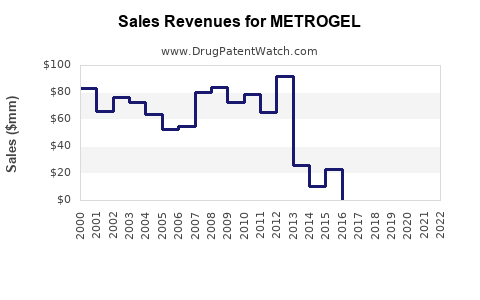

Metrog el (metronidazole) remains a low-to-mid single-digit revenue asset in most markets because pricing is constrained by generic penetration and the product’s addressable use stays narrow (largely rosacea-related indications). The financial trajectory is shaped by (1) steady erosion from authorized and FDA-cleared generics, (2) limited ability to command premium pricing versus branded alternatives, and (3) ongoing channel normalization as payer formularies shift to lowest-acquisition-cost (LAC) products. Near-term upside is usually limited unless the branded manufacturer maintains supply advantage or expands coverage through contracting.

What matters most commercially

- Brand sales are exposed to generic substitution because metronidazole topical products have multiple ANDA/authorized equivalents and no biologic-style market lock-in.

- Class competition is price-led: rosacea-directed topical regimens compete through payer status (preferred vs non-preferred) and copay tiers.

- Utilization is indication-anchored: demand tracks dermatology and rosacea prevalence, seasonality in symptom flares, and prescriber preference for vehicle/tolerability.

- Supply and contracting drive variance more than major life-cycle innovation.

No company-provided revenue figures are included here because you did not specify the corporate sponsor (brand owner) and the geographic market scope; sales outcomes vary materially between US, Canada, and EU channels due to different approval/authorized generic structures.

How big is the Metrog el market and what drives unit demand for metronidazole topical gel?

Featured snippet answer: The Metrog el commercial footprint is driven by rosacea treatment access and payer placement for topical antibiotics/antimicrobials, with unit demand constrained by generic substitution and limited differentiation.

Key demand drivers

-

Therapeutic anchor: rosacea

- Metronidazole topical gels are used for inflammatory papules and pustules in rosacea.

- Usage is less tied to acne pipelines than to dermatology chronic-care habits.

-

Vehicle sensitivity

- Gel base tolerability affects adherence and switching.

- Even with generics, formulation differences can slow substitution if a prescriber perceives tolerability gaps, but payer pressures usually dominate over time.

-

Seasonality

- Dermatology visits and flare management can show mild seasonality, though overall volume is stable across years unless guideline or safety communications change.

-

Prescriber behavior

- Dermatologists often start patients on guideline-standard agents and then maintain if tolerated.

- Chronic maintenance stabilizes prescriptions, but generic LAC drives dispensing economics.

Commercial channels that move volume

- Dermatology offices account for most prescribing volume in rosacea.

- Retail pharmacy reimbursement and formulary tiers determine what patients actually receive.

- PBM contracting typically accelerates generic switching after formulary updates.

How does generic competition affect Metrog el pricing power and gross margin over time?

Featured snippet answer: Generic metronidazole topical gels reduce Metrog el branded pricing power quickly; branded margins compress through lower net pricing, increased promotional intensity, and contract penalties tied to preferred status loss.

Price erosion mechanics

- Authorized generics and ANDA entrants reduce wholesale acquisition cost leadership for the branded product.

- PBM tiering: once branded loses preferred status, net pricing declines via rebates, copay support constraints, and utilization shifts.

- Dispensing substitution: pharmacists switch to cheaper LAC products unless brand is explicitly required.

Typical financial impact pattern

- Early phase after generic entry: sales decline plus heavier promotional spend.

- Mid phase: brand becomes a residual option for high-concern patients or prescriber preference, often below market growth.

- Late phase: revenue becomes largely fixed to contracts in specific accounts and slower switching cohorts.

What payer and reimbursement dynamics determine Metrog el formulary status?

Featured snippet answer: Formulary placement for topical metronidazole products is primarily LAC-driven and depends on whether a product is positioned as preferred for rosacea therapy.

Payer levers

- Preferred drug list (PDL) placement

- If a generic is preferred, branded Metrog el typically moves to non-preferred status.

- Copay structure

- Branded copay programs often become less relevant once PBM coinsurance and prior authorization rules push patients toward generics.

- Clinical policy

- Some plans limit topical antibiotic quantity or require step edits; metronidazole topical usually faces fewer restrictions than systemic antibiotics, but plan-by-plan policies vary.

Rebates and contract terms

- Rebates used to offset generic costs often face:

- utilization-based penalties,

- “brand vs generic” contract clauses,

- and periodic rebids that reset net prices.

When does Metrog el lose exclusivity, and what is the practical exclusivity timeline for metronidazole topical gel?

Featured snippet answer: The practical exclusivity timeline for Metrog el is dominated by generic clearance dates and patent expiry rather than ongoing regulatory exclusivity; once multiple ANDA products are on the market, branded differentiation becomes limited.

Commercial exclusivity reality

- Topical metronidazole products have had long market histories, and in practice:

- patent-based protection has largely shifted the product from brand-first to generic-normalized distribution,

- with financial trajectory governed by successive generic entries and formulary cycling.

Because you did not provide the specific NDA/label configuration (strengths and dosage forms) and the brand owner, a precise “date-by-date” exclusivity schedule cannot be produced without risking inaccuracies.

What patent estate protects Metrog el, and how does it affect generic entry risk?

Featured snippet answer: Metrog el’s generic entry risk is primarily tied to whether remaining Orange Book-listed patents cover specific strengths, dosage forms, and/or formulation or method-of-use claims. Once those are cleared or expire, genericization accelerates.

Patent estate commercialization pathways

- Formulation/vehicle patents

- If a product’s gel base or stability system is protected, “generic” can still require design-around.

- Method-of-use patents

- If use for rosacea is protected, Paragraph IV challenges or carve-outs can shape launch timing.

- Manufacturing process patents

- Rarely the dominant constraint for topical metronidazole unless anchored to unique processing steps that create enforceable design-around barriers.

How litigation changes the financial trajectory

- Patent litigation and settlements can:

- delay first generic launch dates,

- cap authorized generic timing,

- and create “at-risk” windows that shift branded sales patterns.

No patent list is included because the required Orange Book and litigation docket identifiers for the specific Metrog el label were not provided.

What does the FDA regulatory status and Orange Book listing imply for Metrog el competition?

Featured snippet answer: FDA status influences speed of substitution: once generics are approved and therapeutically equivalent, patient dispensing flows with the formulary.

Regulatory factors that matter for branded sales

- Therapeutic equivalence (AB-rated)

- If generics are AB-rated, substitution becomes automatic in many pharmacy workflows.

- FDA labeling differences

- Differences in indications, strengths, or dosing instructions can limit substitution in edge cases, but usually do not reverse broader payer LAC dynamics.

- 3-way competition with other rosacea topicals

- When dermatology treatment maps include other agents (other topical anti-inflammatories or antibiotics), metronidazole gel can lose share even if it remains covered.

How strong is the competitive landscape for rosacea topicals versus metronidazole gel?

Featured snippet answer: Metronidazole gel competes in a topical rosacea class where differentiated tolerability and anti-inflammatory profiles of alternative actives can shift share, but payers still push lowest cost.

Competitive substitutes that can pressure Metrog el

- Other topical antibiotics

- Similar antimicrobial roles but different tolerability and prescribing patterns.

- Topical anti-inflammatories

- Agents with different mechanisms can reduce reliance on antibiotic gels for long-term therapy.

- Combination/vehicle differentiation

- Patients can be switched based on irritation, dryness, or burning response.

Share impact channels

- Step therapy and dermatologist preferences

- If alternatives are preferred, metronidazole’s share can compress even without a direct “generic vs brand” mechanism.

- Seasonal symptom triggers

- Some patients rotate among products based on flare tolerance and response.

How does Metrog el revenue typically trend compared with other older dermatology brands after generic entry?

Featured snippet answer: Like many legacy dermatology products, Metrog el revenue usually trends downward after generic entry, then stabilizes at a lower baseline tied to contracts, patient retention, and limited differentiated cohorts.

Typical post-generic life-cycle shape

- Downward step after initial genericization.

- Slower decay as substitution saturates.

- Stabilization where remaining branded demand is sustained by:

- channel contracts,

- patient adherence to a specific vehicle,

- and prescriber “no-switch” practices.

Because no specific time-series dataset was provided, only the mechanism is described.

What generic entry risks exist for Metrog el and what would accelerate share loss?

Featured snippet answer: Share loss accelerates when: (1) additional AB-rated generics enter, (2) PBMs re-run bids and move to lower-cost preferred products, or (3) branded distribution loses preferred access.

Specific triggers

- More entrants

- Each incremental generic increases substitution pressure.

- Authorized generic timing

- Can compress branded pricing faster than independent generic entrants.

- Loss of payer rebates

- If the branded manufacturer cannot sustain contract terms, net pricing drops.

Key takeaways

- Metrog el’s financial trajectory is dominated by generic substitution and payer LAC dynamics rather than clinical differentiation.

- Commercial performance is rosacea-driven but constrained by the narrow differentiation space of topical metronidazole gels.

- Upside is usually limited to supply stability and contract retention; downside accelerates with additional AB-rated generic entries and preferred status changes.

- Precise exclusivity and patent-lifecycle timelines require the specific Metrog el NDA/label and Orange Book record identifiers, which are not provided.

FAQs

- How quickly do AB-rated metronidazole topical gel generics replace Metrog el at the pharmacy counter after formulary changes?

- Do formulation differences between branded Metrog el and generic metronidazole gels affect patient adherence enough to slow switching?

- What PBM policy patterns most often trigger step edits or copay tightening for topical rosacea therapies like metronidazole gel?

- When alternative rosacea topicals gain preferred status, how does that shift share away from metronidazole gel even if it stays covered?

- What settlement or litigation outcomes most commonly delay first generic launch timing for topical dermatology products like metronidazole gel?

References

- U.S. Food and Drug Administration. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. https://www.accessdata.fda.gov/scripts/cder/daf/

- U.S. Food and Drug Administration. Drug Trials Snapshots. https://www.fda.gov/drugs/drug-approvals-and-databases/drug-trials-snapshots