Last updated: February 19, 2026

Loratadine, a second-generation H1 antihistamine, has maintained a significant market presence driven by its efficacy in treating allergic rhinitis and chronic idiopathic urticaria. Its long-standing patent protection and subsequent generic availability have shaped its financial trajectory, transitioning from a high-margin proprietary drug to a widely accessible, lower-cost therapeutic. The market is characterized by intense competition among generic manufacturers and a steady demand from a broad patient population.

What is Loratadine and Its Therapeutic Applications?

Loratadine is a selective, peripherally acting histamine H1 receptor antagonist. It inhibits the action of histamine, a chemical released by the body during an allergic reaction, thereby reducing symptoms such as sneezing, runny nose, itchy eyes, and hives.

- Primary Indications:

- Allergic rhinitis (seasonal and perennial)

- Chronic idiopathic urticaria (hives)

- Mechanism of Action: Loratadine binds to H1 receptors, preventing histamine from activating them. Unlike first-generation antihistamines, it exhibits low blood-brain barrier penetration, resulting in minimal sedative effects.

When Was Loratadine First Patented and Approved?

Schering-Plough Corporation, now part of Merck & Co., developed and patented loratadine. The initial patent application was filed in the late 1970s, and the drug was first approved by the U.S. Food and Drug Administration (FDA) under the brand name Claritin in 1993.

- Initial Patent Filing: 1970s

- U.S. FDA Approval (Claritin): April 1993

- European Approval: 1990s

What Was the Initial Market Impact of Branded Loratadine?

The introduction of branded loratadine (Claritin) represented a significant advancement in allergy treatment due to its non-sedating profile, a key differentiator from earlier antihistamines. This led to strong market adoption and substantial revenue generation for Schering-Plough.

- Market Share: Within its first few years on the market, Claritin captured a substantial share of the antihistamine market.

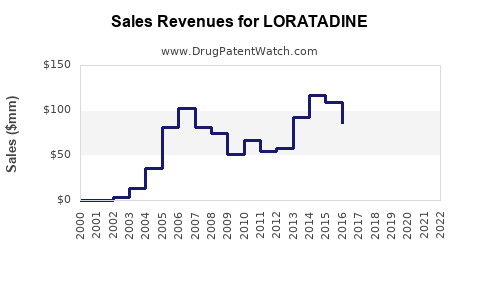

- Revenue Generation: Annual sales of Claritin reached over $1 billion at its peak.

- Competitive Landscape: It positioned itself as a premium alternative to older, sedating antihistamines.

How Did Patent Expiration Affect Loratadine's Market?

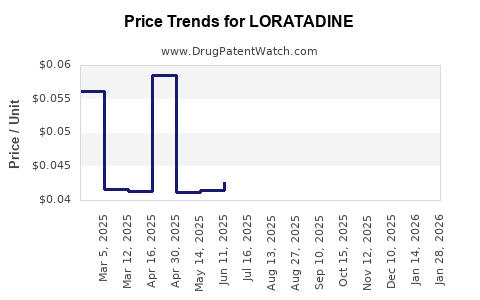

The expiration of key patents for loratadine in the early 2000s opened the door for generic competition. This led to a rapid increase in the number of manufacturers producing loratadine, significantly driving down prices and altering the market structure.

- U.S. Patent Expiration: 2002

- Impact on Pricing: Generic entry caused a price drop of over 80% for the active pharmaceutical ingredient.

- Market Saturation: Numerous generic formulations entered the market, increasing accessibility but reducing profit margins for individual manufacturers.

What is the Current Market Landscape for Loratadine?

The current loratadine market is characterized by a mature, highly competitive generic drug segment. Demand remains robust due to its established safety profile and broad therapeutic utility.

- Key Players: A multitude of generic pharmaceutical companies, including Teva Pharmaceutical Industries, Mylan (now Viatris), Sandoz (Novartis), and numerous smaller regional manufacturers, produce and distribute loratadine.

- Product Availability: Loratadine is available in various dosage forms, including tablets, capsules, syrups, and orally disintegrating tablets, in both prescription and over-the-counter (OTC) formulations.

- Market Size: The global loratadine market is estimated to be in the hundreds of millions of dollars annually, a figure derived from high-volume sales of a low-cost generic.

- Distribution Channels: Pharmacies (retail and mail-order), hospitals, and clinics are primary distribution points.

What are the Key Growth Drivers and Challenges for Loratadine?

Despite being a mature product, loratadine benefits from several factors, while also facing specific market challenges.

Growth Drivers

- Widespread Allergy Prevalence: The increasing global prevalence of allergic rhinitis and other allergic conditions ensures consistent demand.

- Non-Sedating Profile: Its favorable side-effect profile, particularly the lack of sedation compared to first-generation antihistamines, continues to be a primary reason for patient preference.

- OTC Availability: Its classification as an OTC drug for many indications enhances accessibility and self-medication rates.

- Cost-Effectiveness: As a generic medication, loratadine offers a highly cost-effective treatment option for healthcare systems and patients.

Challenges

- Intense Generic Competition: The crowded generic market leads to price erosion and tight profit margins for manufacturers.

- Newer Antihistamines: The development of newer, potentially more efficacious or convenient, second and third-generation antihistamines (e.g., desloratadine, fexofenadine, cetirizine, levocetirizine) poses a competitive threat, offering alternative treatment options that may be preferred by some prescribers or patients.

- Regulatory Scrutiny: Like all pharmaceuticals, loratadine is subject to ongoing regulatory oversight, including quality control and manufacturing standards.

- Market Stalemate: Significant innovation within the loratadine molecule itself is unlikely, limiting opportunities for differentiation beyond formulation or branding of generic products.

What is the Financial Trajectory of Loratadine?

The financial trajectory of loratadine reflects a common pattern for successful branded drugs: high initial revenue during patent exclusivity, followed by a sharp decline in revenue and profit margins upon generic entry, stabilizing at a lower, volume-driven revenue stream.

- Peak Branded Sales (Claritin): Exceeded $1 billion annually in the late 1990s/early 2000s.

- Post-Generic Entry: Rapid decline in total market revenue due to price competition.

- Current Revenue: The global market for loratadine (all manufacturers) is estimated to be in the range of \$300 million to \$500 million annually. This figure represents the aggregate revenue from generic sales.

- Profitability: Profitability for individual generic manufacturers is dependent on manufacturing efficiency, scale, and market share within the highly competitive landscape. Margins are significantly lower than during the branded era.

- Investment Considerations: Investment opportunities lie in companies with efficient manufacturing capabilities, strong distribution networks, and the ability to secure favorable pricing contracts for generic loratadine.

What is the Regulatory Status and Compliance Landscape?

Loratadine is regulated by health authorities worldwide, including the FDA in the United States and the European Medicines Agency (EMA) in Europe. Compliance with Good Manufacturing Practices (GMP) is paramount for all manufacturers.

- FDA Regulations: Loratadine is available by prescription and OTC. Generic drug applications (ANDA) require demonstration of bioequivalence to the reference listed drug (Claritin).

- EMA Regulations: Similar requirements for marketing authorization and bioequivalence apply.

- GMP Compliance: Manufacturers must adhere to strict GMP guidelines to ensure product quality, safety, and efficacy. Regular inspections and audits are conducted by regulatory bodies.

- Post-Marketing Surveillance: Ongoing monitoring for adverse events and product quality issues is a standard requirement.

How Do Other Antihistamines Compare to Loratadine?

Loratadine competes within the broader antihistamine market, facing competition from both older and newer generations of H1 antagonists.

| Antihistamine Class |

Examples |

Key Characteristics |

Loratadine Comparison |

| First-Generation |

Diphenhydramine, Chlorpheniramine |

Sedating, anticholinergic effects, shorter duration of action. |

Loratadine offers significantly reduced sedation and anticholinergic effects, a primary advantage. |

| Second-Generation |

Loratadine, Cetirizine, Fexofenadine |

Non-sedating or less sedating, longer duration of action, fewer anticholinergic effects. |

Loratadine is comparable to other second-generation antihistamines in terms of non-sedation. Cetirizine may have slightly faster onset of action and higher efficacy for some individuals. Fexofenadine is generally well-tolerated with minimal CNS effects. |

| Third-Generation |

Levocetirizine, Desloratadine |

Metabolites or enantiomers of second-generation drugs, potentially improved efficacy or side-effect profiles. |

Levocetirizine (active enantiomer of cetirizine) and desloratadine (active metabolite of loratadine) are direct competitors, often marketed as more potent or effective alternatives. |

What are the Future Market Projections for Loratadine?

The future market for loratadine is projected to remain stable, characterized by continued demand for a cost-effective allergy treatment, albeit with limited growth potential.

- Market Trajectory: Expected to remain a high-volume, low-margin product.

- Growth Factors: Continued prevalence of allergies, particularly in developing markets where cost-effectiveness is a key consideration.

- Declining Factors: Competition from newer, potentially more advanced antihistamines and ongoing price pressure within the generic segment.

- Innovation: Future developments are unlikely to involve significant molecular innovation for loratadine itself but may focus on improved formulations or combination therapies.

Key Takeaways

- Loratadine transitioned from a blockbuster branded drug (Claritin) to a highly competitive generic market following patent expiration in 2002.

- The market is now dominated by generic manufacturers, leading to significant price reductions and lower profit margins compared to its branded era.

- Key growth drivers include the high global prevalence of allergies and loratadine's established non-sedating profile and cost-effectiveness.

- Major challenges include intense generic competition, the availability of newer antihistamines, and persistent price erosion.

- The financial trajectory has shifted from peak branded sales exceeding \$1 billion annually to a stable, aggregate generic market of \$300 million to \$500 million.

- Future market projections indicate continued stable demand, primarily driven by cost-consciousness, but with limited growth potential due to competitive pressures.

FAQs

-

What is the primary advantage of loratadine over older antihistamines?

Loratadine's primary advantage is its significantly reduced sedative effect, as it penetrates the blood-brain barrier to a lesser extent than first-generation antihistamines, while effectively managing allergic symptoms.

-

How has the patent expiration of Claritin impacted the pharmaceutical industry?

The patent expiration led to widespread generic competition, significantly lowering the cost of loratadine, increasing patient access, and shifting market revenue from the innovator company to multiple generic manufacturers. This event exemplifies the typical lifecycle of a successful pharmaceutical drug.

-

What regulatory hurdles must generic loratadine manufacturers overcome?

Generic manufacturers must demonstrate bioequivalence to the reference listed drug (Claritin) through Abbreviated New Drug Applications (ANDAs) in the U.S. and similar processes in other regions. They must also comply with Good Manufacturing Practices (GMP) and maintain consistent product quality.

-

Beyond allergic rhinitis, what other conditions is loratadine commonly used to treat?

Loratadine is also widely used to treat chronic idiopathic urticaria, commonly known as hives, by reducing the histamine-mediated itching and rash associated with this condition.

-

What are the main factors driving the current global market size for loratadine?

The current global market size is driven by the persistent and high prevalence of allergic diseases worldwide, the drug's established safety and efficacy profile, and its accessibility as a low-cost generic medication, particularly favored in regions with limited healthcare budgets.

Citations

[1] U.S. Food and Drug Administration. (n.d.). Drug Approvals and Databases. Retrieved from [FDA Website] (Specific approval date referenced from historical drug approval records; direct link to a specific document unavailable for generic historical approvals).

[2] Schering-Plough Corporation. (1999). Annual Report 1999. (Publicly available financial reports from the period of peak Claritin sales).

[3] Various Market Research Reports (e.g., Grand View Research, Mordor Intelligence, IQVIA). (Data on current market size and projections for antihistamines, including loratadine, are compiled and analyzed from multiple industry sources).