The $1.6 trillion global pharmaceutical industry runs on a single underlying premise: time-limited exclusivity justifies the cost of discovery. Strip out that premise, and the math of drug development collapses. A new molecular entity typically costs $2.6 billion and 10 to 15 years to develop, with a clinical success rate of roughly 12% from Phase I. The patent system is the mechanism that makes those odds commercially tolerable.

This guide covers that system in full, from the initial filing of a composition-of-matter claim through the multi-jurisdictional lifecycle management programs that can extend a drug’s protected commercial window by a decade or more. It is written for practitioners who need more than a survey, IP teams building or auditing a portfolio, R&D leads weighing pipeline decisions against exclusivity timelines, and institutional investors who model loss-of-exclusivity events into net present value calculations.

The source material draws on FDA Orange Book records, PTAB databases, European Patent Office (EPO) prosecution history, published litigation outcomes from the District of Delaware and the District of New Jersey, recent BPCIA patent dance disclosures, and publicly filed ANDA data through Q1 2026.

II. The Economic Architecture of Pharmaceutical Patents

Why the Patent Monopoly Exists and What It Actually Buys

A pharmaceutical patent is a statutory bargain. The government grants a 20-year exclusivity period from filing date in exchange for public disclosure of the invention. In practice, the pharmaceutical company uses the period of patent-protected sales to recover R&D costs and generate a return on capital before generic or biosimilar competition drives prices down by 38-85%, depending on the therapeutic class and number of market entrants.

The economics are stark. Keytruda (pembrolizumab), Merck’s PD-1 checkpoint inhibitor, generated $25 billion in 2023 sales. Its core composition-of-matter patents expire in 2028. Without ongoing lifecycle management, Merck is looking at the largest single-drug revenue cliff in pharma history. Compare that to AbbVie’s management of adalimumab (Humira), which accumulated over $200 billion in lifetime sales by building a 132-patent thicket that delayed US biosimilar competition until 2023, nearly two full decades after the first biosimilar approval in Europe.

The financial leverage of strong patent coverage is measurable. Studies of patent expiration events across 2010-2022 show that drugs entering first-generic competition lose a median 68% of branded revenue within 12 months. Drugs with secondary patent clusters around new formulations or delivery devices show a slower erosion curve, losing roughly 35-40% in year one, because initial generic competition targets only the base composition while the supplementary coverage keeps newer dosage forms protected.

Patents as Balance Sheet Assets

For institutional investors, drug patents are not abstract legal protections. They are balance sheet assets with quantifiable present values. The IP-to-enterprise-value ratio has become a standard screening metric for biotech analysts at firms like Cowen, SVB Securities, and Leerink. A single composition-of-matter patent on a blockbuster can represent $8-15 billion in risk-adjusted net present value, depending on remaining patent life, probability of successful Paragraph IV defense, and market penetration assumptions.

When Pfizer acquired Seagen in 2023 for $43 billion, a significant portion of that premium reflected Seagen’s antibody-drug conjugate (ADC) patent estate, particularly the IP around linker chemistry and conjugation methods. Similarly, AstraZeneca’s $39 billion acquisition of Alexion in 2021 was built on Alexion’s complement inhibitor patent portfolio, with Soliris’ eculizumab composition-of-matter patent and its associated method-of-use patents for rare complement-mediated diseases providing the exclusivity runway that justified the price.

Key Takeaways: Section II

Patents in pharma are financial instruments with computable values, not just defensive legal tools. The difference between a well-managed and poorly managed patent estate can amount to five or more years of additional protected revenue, often worth billions in NPV terms. Analysts should model patent coverage as a probabilistic cash flow duration, not a binary on/off event.

Investment Strategy Note

When screening pharma equities, map each revenue-generating drug to its Orange Book-listed patents and calculate the probability-weighted loss-of-exclusivity date. A drug with a single composition-of-matter patent expiring in three years trades differently than one with overlapping formulation, method-of-use, and device patents extending effective exclusivity by six-plus years. The delta between those two scenarios frequently explains valuation gaps that screen as cheap on conventional multiples.

III. Patent Taxonomy: A Technical Breakdown of Every Protection Layer

Composition-of-Matter (Base/Product) Patents

The composition-of-matter patent, often called the base or product patent, covers the active pharmaceutical ingredient (API) itself: its chemical structure, molecular formula, or, for biologics, its amino acid sequence or nucleotide sequence. This is the most commercially valuable patent class because it bars all competitors from making, using, or selling the molecule regardless of indication, formulation, or manufacturing process.

A composition-of-matter patent on a first-in-class molecule commands the highest IP valuation because it captures the entire downstream commercial value of the molecule across all its potential uses. When Pfizer filed the composition-of-matter patent on sertraline (later Zoloft) in 1981, the patent covered the molecule comprehensively. The litigation that followed its 2006 expiration was effectively a single-front battle. Contrast that with the multi-front patent defense that AbbVie ran for adalimumab, which required generic challengers to defeat over 100 separately prosecuted patents before gaining market access.

For biologics, composition-of-matter protection is technically and legally more complex. The sequence patent covers the primary amino acid structure, but the therapeutic protein as manufactured includes glycosylation patterns, higher-order folding, and post-translational modifications that differ between manufacturers. This structural complexity creates additional patentable space that does not exist in small-molecule chemistry. Amgen’s patents on etanercept (Enbrel) and filgrastim (Neupogen) occupied this space extensively, covering not just the sequence but also specific glycoforms, pegylation sites, and purification methods.

Secondary Patents: The Evergreening Architecture

Secondary patents are the primary mechanism of lifecycle extension. They do not protect the core molecule but rather improvements to it, and the strength of any individual secondary patent varies widely depending on the nature of the claimed improvement, the prior art landscape, and the examining jurisdiction. The categories are worth treating in technical depth.

Polymorph and Pseudopolymorph Patents

Polymorphism refers to the ability of a solid material to exist in more than one crystalline form. For APIs, different polymorphic forms can have dramatically different solubility profiles, dissolution rates, and physical stability characteristics. Paroxetine hydrochloride (Paxil) had its core patent expire, but SmithKline Beecham successfully prosecuted patents on the hemihydrate form, which triggered years of litigation before courts ultimately invalidated those claims. The lesson for IP teams: polymorph patents are prosecutable and commercially valuable but face elevated invalidity risk because polymorph generation is often viewed as routine experimentation. The non-obviousness argument requires specific data demonstrating unexpected properties in the claimed form, such as a 3x improvement in dissolution rate or significantly enhanced thermal stability.

Enantiomer Patents

Many pharmaceutical compounds are racemates, mixtures of two mirror-image stereoisomers. If one enantiomer carries the therapeutic activity and the other contributes side effects or is therapeutically inert, the pure enantiomer represents a patentable improvement. The classic example: AstraZeneca converted omeprazole (Prilosec) into esomeprazole (Nexium) by patenting the S-enantiomer, which has a longer half-life and higher bioavailability. Nexium’s launch preceded Prilosec’s patent expiration and generated over $5 billion in peak annual sales, funded in part by heavily marketed physician switching. Critics called it textbook evergreening; defenders note that esomeprazole does show measurably superior pharmacokinetics in CYP2C19 poor metabolizers.

Formulation and Drug Delivery Patents

Extended-release formulations represent one of the most commercially durable categories of secondary patents. The mechanism of protection is genuine improvement in clinical utility: a once-daily formulation reduces pill burden, improves adherence, and often reduces peak plasma concentration-related adverse effects. Shire’s Adderall XR patents covering the spheroidal oral drug absorption system (SODAS) bead technology kept competition at bay for years after the immediate-release salt formulation lost protection.

Newer drug delivery platforms, including lipid nanoparticle (LNP) formulations, polymer-drug conjugates, and device-drug combinations, create significant secondary patent opportunities. Moderna and BioNTech’s LNP delivery patents for mRNA vaccines illustrate how delivery platform IP can be as commercially important as the API itself. The LNP composition and manufacturing process patents, including those licensed from Acuitas Therapeutics, were among the most contested IP assets in the COVID-19 vaccine landscape.

Method-of-Use and New Indication Patents

A method-of-use patent covers the application of a known compound to a specific therapeutic context. Under 35 U.S.C. Section 101, methods of treatment are patentable in the US, provided they meet novelty and non-obviousness standards. These patents typically expire later than the core composition-of-matter patent if they were filed after a new indication is discovered, providing a downstream exclusivity layer. Sildenafil’s path from cardiovascular drug candidate to Viagra and then to Revatio (for pulmonary arterial hypertension) is a compressed illustration: the PAH indication generated a separate exclusivity runway under both method-of-use patents and orphan drug designation.

Process Patents

Process patents cover the manufacturing method rather than the product. They are particularly significant for biologics, where the process is inseparable from the product. FDA’s longstanding “the process is the product” principle for biologics means that changes in cell line, fermentation conditions, purification protocol, or formulation process can result in a product with different safety and immunogenicity profiles. Amgen’s manufacturing process patents for etanercept covered specific CHO cell culture conditions and downstream purification sequences, creating barriers for biosimilar developers that were independent of the product composition patents.

For small molecules, process patents protect synthetic routes that offer cost advantages or purity improvements. They are less common as standalone commercial barriers because generic manufacturers can typically design around a process patent by developing alternative synthetic routes, but they add cost and complexity to the ANDA preparation process.

Tertiary Patents: Device-Drug Combinations

Tertiary patents cover medical devices used in conjunction with an active ingredient that may itself be off-patent. The GlaxoSmithKline Diskus inhaler device patents for fluticasone-salmeterol (Advair) are a frequently cited example. The device’s multi-dose dry powder delivery mechanism was covered by a separate set of device patents that outlasted the API patents, creating a barrier not to the drug itself but to the preferred delivery format. Device-drug combination patents are increasingly relevant in biologics, where autoinjectors, prefilled syringes, and wearable injectors carry independent IP coverage.

Key Takeaways: Section III

Patent protection in pharma is a layered architecture, not a single document. IP teams should systematically pursue composition-of-matter, polymorph, formulation, method-of-use, process, and device patents as discrete coverage layers, each with its own prosecution strategy, expiration timeline, and litigation profile. The commercial durability of a franchise depends on how many of those layers can be successfully defended simultaneously.

IV. IP Valuation Frameworks: Quantifying the Asset Behind the Molecule

Standard Valuation Methods Applied to Pharmaceutical Patents

Pharmaceutical patent valuation sits at the intersection of IP law, pharmacoeconomics, and capital markets. Three established frameworks are in use: income-based valuation, market-based valuation, and cost-based valuation.

Income-Based Valuation (rNPV)

The risk-adjusted net present value (rNPV) method is the industry standard for pipeline assets. It discounts projected future cash flows from patent-protected sales by a weighted cost of capital, typically 8-12% for late-stage pharma assets, and adjusts those cash flows by the probability of regulatory success at each development stage. The rNPV of a patent is therefore a function of remaining patent life, projected peak sales, probability of successful Paragraph IV defense (if ANDA challenges are anticipated), and the probability that superior competitors enter the market before patent expiry.

For a marketed drug, the calculation simplifies to the present value of projected patent-protected revenue minus the projected generic entry revenue, discounted to today. If Drug X generates $3 billion per year in US sales, faces a composition-of-matter expiration in 2028, and has secondary patents extending effective exclusivity to 2031, the incremental patent value of those secondary patents at a 10% discount rate is roughly $5-6 billion in gross NPV terms, before probability-adjusting for litigation risk.

Market-Based Comparables

Licensing transactions provide market-based data points. The royalty rate in a typical pharma licensing deal ranges from 8-20% of net sales for a marketed product, compared to 2-6% for an early-stage compound. Applying these observed royalty rates to projected revenues via the relief-from-royalty method generates a market-benchmarked IP valuation. The limitation of this approach is that transaction data is often confidential, complicating comparable selection.

Cost-Based Approaches

Cost-based valuation, which calculates the cost to recreate the IP through parallel research, is rarely the primary method in pharma because the cost of re-running clinical trials for a molecule that has already proven efficacy tells you very little about the market value of that proven efficacy. It is used as a floor valuation in accounting contexts and for transfer pricing in multinational IP structures.

IP Valuation Case Studies

Humira (adalimumab) – AbbVie

Adalimumab’s patent estate is the most exhaustively studied case in pharmaceutical IP valuation. AbbVie listed over 100 patents in the FDA’s Purple Book, covering the antibody sequence, formulation (citrate-free high-concentration formulation), manufacturing process, methods of use across nine approved indications, and the prefilled autoinjector device. At peak sales of $21 billion globally in 2022, the total IP asset value of the adalimumab portfolio was estimated by several sell-side desks at $60-80 billion in cumulative remaining NPV, ahead of the 2023 US biosimilar entry.

The citrate-free formulation patent, challenged but ultimately not defeated before US biosimilar entry, is a textbook example of a secondary patent carrying disproportionate commercial value: the reformulation reduced injection-site pain and supported patient preference for the branded product even after biosimilar availability.

Enbrel (etanercept) – Amgen

Amgen built an estimated 100+ patents around etanercept using a strategy that Biopharma Dive described as an “interlocking wall of intellectual property protection.” The original composition-of-matter patent expired in 2012 in the US, yet biosimilar competition did not arrive until 2029 due to manufacturing process patents and method-of-use patents that were either enforced through litigation or resolved via settlement. Cumulative Enbrel revenues exceeded $70 billion globally before biosimilar entry. The incremental IP valuation of the post-2012 secondary patent estate, which blocked biosimilar entry for 17 additional years in the US, represents one of the highest measured returns on a secondary patent prosecution program in pharma history.

Keytruda (pembrolizumab) – Merck

Pembrolizumab’s core composition patents expire around 2028 in the US, with patent term extension (PTE) potentially adding one to two years. At $25 billion in 2023 sales, and with biosimilar entry expected in the 2030-2033 timeframe depending on PTE and BPCIA litigation outcomes, the rNPV exposure from the LOE event is significant. Merck’s IP team has been prosecuting secondary patents on pembrolizumab combination regimens (with chemotherapy and other checkpoint inhibitors), specific formulation improvements, and manufacturing bioprocess parameters. The commercial question is whether combination regimens protected by method-of-use patents on specific chemotherapy backbone combinations will retain a price premium after the core composition-of-matter patent expires.

Investment Strategy Note

For buy-side analysts, Merck’s post-2028 revenue trajectory is the single most important modeling assumption in any Merck equity position above a one-year holding period. The probability that secondary patents on pembrolizumab combination regimens survive PTAB review and district court challenge should be assigned a range, not a point estimate. Base case: effective exclusivity extends to 2031 through formulation and combination patents. Bull case: BPCIA patent dance litigation delays US biosimilar launch to 2033 or later. Bear case: PTAB invalidates key secondary patents, biosimilar entry in late 2028.

Key Takeaways: Section IV

Pharmaceutical IP valuation requires modeling patent coverage as a probability distribution over time, not a single expiration date. rNPV is the appropriate primary method for marketed-drug IP assets. Secondary patent estates can represent multiples of the core composition-of-matter patent value when successfully defended, as the Amgen/etanercept case demonstrates.

V. The Drug Patent Lifecycle: Filing, Prosecution, and Effective Market Life

The Clock Problem: Why 20 Years Is Not 20 Years

A utility patent in the US has a statutory term of 20 years from the earliest claimed non-provisional filing date. For most industries, that 20-year window is the operating period. For pharmaceuticals, it is dramatically compressed by the regulatory approval process.

Consider the typical timeline. A company identifies a lead compound and files a patent application during late lead optimization, often two to four years into the discovery program. The FDA approval process for a New Chemical Entity (NCE) requires Phase I, II, and III trials plus an NDA review period: collectively, that process consumes eight to twelve years. An NCE filed in 2010 approved in 2021 has consumed 11 years of its patent term before generating a single dollar of sales. If the composition-of-matter patent expires in 2030, effective patent-protected market life is nine years, not twenty.

This compression drives everything else in pharmaceutical patent strategy. The Hatch-Waxman Act created patent term extension specifically to address this problem, but PTE is limited to five years and capped at 14 years of post-approval exclusivity. The gap between the 20-year statutory term and the actual effective market life is the financial wound that evergreening, regulatory exclusivities, and secondary patent strategies exist to close.

Filing Strategy: Provisional vs. Non-Provisional Applications

A provisional patent application establishes a priority date without beginning the 20-year term. This buys 12 months for additional R&D before the non-provisional filing. For pharmaceutical companies, timing the transition from provisional to non-provisional is a calculated trade-off: filing the non-provisional too early wastes patent term before the drug reaches market; filing too late risks losing priority to a competitor filing on a similar compound.

Continuation-in-part (CIP) applications allow a company to add new matter to a patent family while claiming priority to the original filing for the original matter. This is a common prosecution tool for pharmaceutical secondary patents: the original filing covers the composition; subsequent CIPs claim specific crystalline forms, formulations, or metabolites, each with its own 20-year term from its own filing date. A well-managed patent family can therefore have several members with staggered expiration dates, creating overlapping protection layers.

Prosecution Strategy and the Record That Follows You

The prosecution history, called the file wrapper, is the complete record of communications between the applicant and the USPTO during patent examination. Every argument made during prosecution to distinguish prior art becomes part of the claim scope through prosecution history estoppel. Overly narrow arguments made to overcome prior art rejections can limit the claim’s scope in subsequent infringement litigation, even against competitors whose products do not literally infringe but would infringe under the doctrine of equivalents.

Pharmaceutical IP teams should treat each prosecution decision as a litigation preview. Claim language choices that appear pragmatic during prosecution, such as accepting an examiner’s narrowing amendment to secure allowance, can create infringement loopholes that a well-resourced generic competitor will exploit during ANDA litigation. Coordinating prosecution strategy with litigation counsel, particularly in a patent family with known commercial importance, is standard practice at major pharmaceutical companies.

Key Takeaways: Section V

The 20-year patent term is a ceiling, not a floor, for pharmaceutical exclusivity. Effective market life is determined by the sum of regulatory approval time subtracted from the patent term, which typically yields 8-12 years of protected sales for an NCE before statutory extensions. Filing strategy and prosecution history management are the upstream decisions that determine downstream litigation vulnerability.

VI. Patent Term Extension, Patent Term Adjustment, and the Clock Math

Patent Term Extension (PTE) Under Hatch-Waxman

Patent Term Extension under 35 U.S.C. Section 156 restores patent term lost during the FDA regulatory review period. The calculation has three inputs: the regulatory review period (time from IND filing to NDA approval), a 5-year cap on the total extension granted, and a maximum effective patent life of 14 years from the date of first commercial marketing approval.

The formula: PTE = (0.5 x testing phase) + (regulatory review phase) – (any applicant-caused delays). The testing phase includes Phase I, II, and III clinical work. Only one PTE is available per drug product, and it can be applied to only one patent per product. That single-patent constraint matters strategically: the patentee must select the patent receiving the PTE, generally the composition-of-matter patent, even if secondary patents might benefit more from the extension in certain circumstances.

For biologics, PTE applies to the same statutory framework but interacts with the BPCIA’s 12-year exclusivity period for reference biological products. The interplay between PTE, the 12-year exclusivity, and Purple Book listing creates a distinctly more complex exclusivity calculation than the small-molecule Orange Book framework.

Patent Term Adjustment (PTA) Under the AIPA

Patent Term Adjustment under 35 U.S.C. Section 154(b) compensates patent holders for delays caused by the USPTO during prosecution. PTA accumulates when the USPTO fails to meet specific statutory deadlines, for example, failing to issue a first office action within 14 months of filing or failing to respond to an applicant’s response within four months. Unlike PTE, PTA can be applied to every patent in a family, making it particularly valuable for secondary patent programs where the aggregate prosecution delays across a dozen patents can add six to eighteen months of PTA to each.

The critical cases shaping PTA calculation include the Federal Circuit’s decisions in Supernus Pharmaceuticals v. Iancu and the Novartis series. These cases refined how applicant-caused delays are calculated and subtracted from USPTO-caused delays, with significant financial consequences for large patent families. The Supernus decision specifically held that certain applicant delays that occur before any USPTO delay cannot be subtracted from the PTA, a holding that increased PTA awards for pharmaceutical patent holders.

Supplementary Protection Certificates (SPCs) in the EU

The EU equivalent of PTE is the Supplementary Protection Certificate (SPC), governed by EU Regulation 469/2009. An SPC can extend patent protection for a medicinal product by up to five years from patent expiration, provided the first marketing authorization in the EU was obtained during the patent term. A pediatric extension of six months is available if the required pediatric investigation plan is completed.

The EU SPC system is being harmonized through the Unitary SPC regulation, which entered into force in 2023. The Unitary SPC, once fully operational, provides protection across all EU member states through a single certificate issued by the EPO, eliminating the current country-by-country application process. For multinational pharmaceutical companies maintaining SPCs in 15-20 EU member states, the cost savings from Unitary SPCs are material.

Obviousness-Type Double Patenting (ODP) and Terminal Disclaimers

Obviousness-type double patenting (ODP) is an evolving doctrine with significant consequences for pharmaceutical patent term. ODP prohibits a patent owner from obtaining a second patent that is not patentably distinct from a first patent, preventing artificial term extension by filing continuation applications claiming obvious variants of an already-patented invention. Courts invalidate patents found to be barred by ODP unless the patentee has filed a terminal disclaimer, which ties the expiration of the later patent to that of the earlier patent.

The Federal Circuit’s 2024 decision in In re Cellect significantly tightened ODP doctrine, holding that PTA-adjusted patents can be subject to ODP invalidation if the PTA-extended term runs beyond a parent patent to which the continuation is connected. For pharmaceutical companies with large patent families where individual patents received different PTA awards, the Cellect ruling created a portfolio review imperative: patents that received significant PTA may now carry ODP vulnerability if they share specification matter with earlier-filed family members.

Key Takeaways: Section VI

PTE and PTA are complementary tools with distinct mechanics, limits, and strategic applications. PTE restores one patent’s term against regulatory delay; PTA restores each patent’s term against USPTO delay. The Cellect ODP decision introduced new complexity for large patent families with PTA-extended members. IP teams managing large continuation families should perform ODP exposure analysis against the Cellect framework.

Investment Strategy Note

When an expiring drug has a PTE pending or filed, the resolution date and PTE quantum matter for LOE modeling. A six-month PTE extension on a drug with $5 billion in annual US sales represents $2.5 billion in incremental protected revenue, easily worth the USPTO filing and prosecution cost. Check the Orange Book PTE column and the FDA’s public database of PTE applications for pending extensions on drugs approaching expiration.

VII. Evergreening: Technology Roadmaps, Litigation Exposure, and Quantified Impact

Defining the Evergreening Spectrum

The term “evergreening” covers a wide spectrum of practices, from genuine incremental innovation with real clinical benefit to patent filings on trivial modifications that offer no therapeutic improvement. IP teams, analysts, and regulators should distinguish between these categories because they carry different litigation risk profiles, different regulatory exclusivity implications, and different reputational consequences.

At one end: a sustained-release reformulation that enables once-daily dosing for a drug previously requiring three-times-daily administration genuinely reduces pill burden and improves adherence, with measurable clinical outcomes data. Patents on this formulation reflect real innovation and are generally more defensible under validity challenge.

At the other end: a polymorph patent on a crystalline form with no demonstrated clinical superiority over the original polymorph, filed to block generic entrants from using the most commercially convenient crystalline form, sits closer to the problematic end of the spectrum. Courts in several jurisdictions, particularly in India and Canada, have invalidated such patents under heightened novelty or utility standards.

The financial stakes make the spectrum worth mapping precisely. A study published by the Initiative for Medicines, Access, and Knowledge found that secondary patents on 12 top-selling drugs added an estimated $52.6 billion in extra consumer costs. That figure is a regulatory and antitrust liability figure as much as it is a revenue protection figure: it attracts FTC scrutiny, state AG investigations, and the kind of congressional attention that generates proposals like the PREVAIL Act and the Patent Eligibility Restoration Act.

Technology Roadmap: Evergreening for Small Molecules

A systematic small-molecule evergreening program typically proceeds through the following stages:

Phase 1 (Years 0-5 post-NDA): The composition-of-matter patent and any immediate-release formulation patents are in force. The focus is on completing the Crystal Form Screen (identifying all accessible polymorphs and selecting the most commercially stable form for the NDA product) and filing patents on the selected form and its manufacturing process. Simultaneously, the team screens for active metabolites, since a pharmacologically active metabolite can represent an independent patentable compound with its own composition-of-matter protection.

Phase 2 (Years 3-8 post-NDA): Formulation development programs targeting extended-release, modified-release, or novel delivery technologies begin. These programs should be clinically grounded: dose reduction, reduced side effects, or adherence improvement data support both the regulatory filing for a supplemental NDA and the non-obviousness argument in subsequent patent prosecution. Combination patents with other approved agents in the same therapeutic category are pursued where pharmacological rationale exists.

Phase 3 (Years 6-12 post-NDA): New indication development, either through investigator-initiated studies or a company-funded Phase II program, identifies patentable method-of-use claims for previously unrecognized therapeutic applications. Pediatric study completion triggers the six-month pediatric exclusivity extension in both the US and EU. If the drug qualifies for orphan designation in a rare disease sub-population, the orphan NDA generates seven years of US orphan drug exclusivity independent of the patent estate.

Phase 4 (Years 10+): Device combination patents on autoinjectors, drug-device combination products, or co-packaged regimens maintain premium pricing and formulary differentiation after the core composition-of-matter patent has expired.

Technology Roadmap: Evergreening for Biologics

Biologic evergreening operates through a distinct set of tools because the nature of the molecule, a protein with complex higher-order structure, creates different patentable space.

Phase 1 (Years 0-5 post-BLA): The sequence patent and any initial formulation patents are in force. The focus is on characterizing the molecule’s critical quality attributes (CQAs): glycosylation patterns, charge variants, aggregation propensity, and oxidation sites. CQA-specific patents, covering purified preparations with defined glycoform distributions, have been successfully prosecuted for several biologics and create a barrier for biosimilar developers who cannot exactly replicate the reference product’s CQA profile.

Phase 2 (Years 3-8 post-BLA): High-concentration formulation patents for subcutaneous administration, enabling needle-length reduction and improved patient self-injection experience, are particularly valuable if the original biologic was administered intravenously. AbbVie’s citrate-free adalimumab formulation patent is the textbook example. The transition from IV to SC administration or from low-concentration to high-concentration subcutaneous formulation typically involves years of pharmaceutical development work that the patent reflects genuinely.

Phase 3 (Years 5-15 post-BLA): Next-generation molecule development: a PEGylated version, a half-life extended variant using Fc engineering (e.g., YTE mutations extending FcRn binding), or a bispecific derivative of the original monoclonal antibody. Each of these represents an independently patentable compound with its own 20-year patent term from filing, while sharing the brand equity and clinical track record of the originator molecule.

Phase 4 (Years 10+): Fixed-dose combination biologics, co-formulated with a second biologic in the same injection, represent the frontier of biologic lifecycle extension. No commercially successful co-formulated biologic combination has yet completed this pathway, but several are in development, with patent protection on the combination formulation representing a potentially long-lived commercial strategy.

Quantified Impact of Secondary Patents

The academic and regulatory literature provides several anchoring data points:

A study by Feldman and colleagues found that 78% of drugs associated with new patents from 2005 to 2015 were existing drugs, not new molecular entities. The same study found that the 100 best-selling drugs had an average of 4.5 patents each, with secondary patents providing an average of 6.3 years of additional exclusivity beyond the original composition-of-matter protection.

I-MAK’s analysis of the 12 top-selling US drugs found that each had 38 to 132 patent applications associated with it. The average cost to patients attributed to this secondary patent activity, measured as the price premium above the estimated competitive market price, was $4.4 billion per drug over the study period.

AbbVie’s adalimumab secondary patents generated estimated additional US exclusivity of 8-10 years beyond the composition-of-matter expiration. Amgen’s etanercept secondary patents extended effective US exclusivity by approximately 17 years. These are outliers, but they establish the ceiling of what a systematically executed secondary patent program can achieve.

Key Takeaways: Section VII

A well-structured secondary patent program adds 3-10+ years of effective exclusivity beyond the core composition-of-matter patent, with the upper range achievable only through a multi-layer program that covers formulation, manufacturing process, device, and method-of-use claims simultaneously. The litigation vulnerability of each layer differs: active-ingredient patents are hard to invalidate but eventually expire; formulation and polymorph patents are more susceptible to prior art and obviousness challenges. Balance the portfolio accordingly.

Investment Strategy Note

When a competitor files an ANDA, the Orange Book tells you which patents the generic is challenging. If the ANDA Paragraph IV certification targets only the composition-of-matter patent and not the secondary patents, the brand company may lose the composition-of-matter case but retain effective market exclusivity through the unchallenged secondary coverage. Read the Paragraph IV certification letters, not just the patent expiration dates.

VIII. Regulatory Exclusivity Stacking in the US and EU

US Regulatory Exclusivity: The Complete Toolkit

Patents and regulatory exclusivities are legally distinct instruments governed by separate statutes. Regulatory exclusivities block generic or biosimilar approval regardless of patent status; they can provide protection even after all relevant patents have expired or been invalidated.

New Chemical Entity Exclusivity (NCE)

Five years from NDA approval for a drug containing a new active moiety not previously approved. During the NCE period, the FDA cannot accept for filing any ANDA or 505(b)(2) application referencing the approved drug, except that an ANDA with a Paragraph IV certification can be filed after four years. NCE exclusivity runs concurrently with the patent term, not sequentially, so its independent value to a company depends on whether the NCE period extends beyond the relevant patent’s expiration.

New Clinical Investigation Exclusivity (3-Year)

Three years from NDA or supplemental NDA approval for changes that require new clinical studies (not necessarily new Phase III trials): new indications, new formulations, new dosage forms, or new routes of administration. This exclusivity prevents full ANDA approval, though it does not block ANDA filing. For a secondary patent program, this exclusivity is synergistic: a new extended-release formulation generates both a secondary formulation patent and a three-year NCE exclusivity from its sNDA approval.

Orphan Drug Exclusivity (ODE)

Seven years for drugs designated to treat a rare disease affecting fewer than 200,000 US patients. ODE blocks FDA approval of a “same drug” for the same orphan indication, but it does not block approval for a different indication. The orphan route is particularly strategic for precision oncology, rare genetic diseases, and pediatric conditions. Combined with the seven-year ODE, qualified infectious disease products can receive an additional five-year exclusivity extension under the GAIN Act.

Pediatric Exclusivity

Six months added to all existing patents and regulatory exclusivities in exchange for completion of a Pediatric Research Equity Act (PREA) required study or a voluntary FDA-requested pediatric study under the Best Pharmaceuticals for Children Act (BPCA). Unlike other exclusivities, pediatric exclusivity attaches to existing protection rather than starting a new clock. For a drug with $5 billion in annual US sales, six additional months of exclusivity is worth roughly $2.5 billion in gross revenue before probability adjustment.

Biologic Exclusivity Under the BPCIA

Reference biological products receive 12 years of exclusivity from the date of first licensure, during which the FDA cannot approve a biosimilar referencing that product. An additional four-year period blocks even the filing of a biosimilar BLA. The 12-year period is the longest regulatory exclusivity in the US drug approval system and is independent of patent status. A biologic whose composition-of-matter patent has been invalidated retains the 12-year exclusivity against biosimilar approval.

EU Regulatory Exclusivity: The 8+2+1 System and Its Proposed Replacement

Current Framework

The current EU system grants eight years of regulatory data protection (RDP), during which no biosimilar or generic manufacturer can use the innovator’s preclinical and clinical data in support of their own marketing authorization application. Following the eight-year RDP, a two-year period of market exclusivity prevents the competitor product from being placed on the market, even if the marketing authorization has been issued. An additional one-year extension applies if a new therapeutic indication with significant clinical benefit is approved during the first eight years.

The 8+2+1 structure results in a maximum of 11 years of combined regulatory protection, often running concurrently with the patent term. For drugs with late patent expirations, the regulatory exclusivity may expire before the patent; for drugs that lost patent protection early (e.g., through IPR proceedings or litigation defeat), the regulatory exclusivity provides a floor of generic-free market time.

Proposed EU Pharma Package Reforms (2024-2026)

The European Commission’s pharmaceutical package, under negotiation through 2024 and 2025, proposes restructuring the EU exclusivity framework significantly. The baseline RDP would decrease from eight years to six years for most drugs, with conditional extensions of six months for demonstrating unmet medical need, six months for conducting comparative clinical trials, one year for a significant new therapeutic indication approved within the data protection period, and two years for launching in all EU member states within two years of initial approval.

The European Parliament proposed capping total RDP at 8.5 years. For orphan medicines, the baseline Orphan Market Exclusivity (OME) would decrease from 10 years to 9 years, with a one-year extension for each additional orphan indication approved (maximum twice), and a two-year extension for approval in all EU member states. The practical result: companies that run a pan-EU launch and invest in comparative clinical data could approach or exceed the current 10-year OME. Companies that take a staggered EU launch approach or skip comparative trials will face earlier generic entry.

Stacking Strategy: How the Layers Interact

The interaction between patent coverage and regulatory exclusivities determines the effective exclusivity duration. Consider a drug approved in the US as an NCE in 2023:

From NDA approval in 2023, the five-year NCE exclusivity runs to 2028. The composition-of-matter patent filed in 2010 expires in 2030. PTE of 3.5 years extends the patent to 2033. A pediatric study completed in 2026 adds six months to both the NCE exclusivity (to 2028.5) and the composition-of-matter patent’s PTE (to 2033.5). A secondary extended-release formulation sNDA approved in 2025 generates three-year NCE exclusivity on the ER formulation (to 2028) and a secondary formulation patent filed in 2022 expiring in 2042.

In this scenario, the drug has base patent-protected sales through 2033.5 (PTE + pediatric extension on composition-of-matter), while the ER formulation has patent coverage through 2042. Generic competition against the immediate-release formulation begins in 2033.5, but the ER formulation remains protected through 2042 if the ER formulation patent survives challenge. Effective commercial exclusivity in a market where the ER formulation captures the majority of prescription volume extends to approximately 2042.

Key Takeaways: Section VIII

Regulatory exclusivities and patents are parallel protection systems that should be managed together, not sequentially. The combination of NCE exclusivity, pediatric extensions, ODE, and secondary formulation patent coverage can generate an effective market life that significantly exceeds what the composition-of-matter patent alone would provide.

Investment Strategy Note

When modeling LOE events, check both the Orange Book patent expiration AND the FDA exclusivity database. A drug losing its last Orange Book patent may retain years of NCE or orphan exclusivity, delaying generic entry. The two databases are separate and must be reviewed independently. The FDA’s Drugs@FDA database shows all approval dates and exclusivity grants; the Orange Book shows listed patents.

IX. The Hatch-Waxman Litigation Machine: Paragraph IV, 30-Month Stays, and 180-Day Exclusivity

How Hatch-Waxman Created the Modern Patent Battlefield

The Drug Price Competition and Patent Term Restoration Act of 1984, commonly called the Hatch-Waxman Act, restructured the competitive dynamics of the US drug market. Before 1984, generic drug manufacturers had to run their own clinical trials to prove safety and efficacy, creating a practical barrier to generic entry that had nothing to do with patent protection. Hatch-Waxman solved this by allowing generic manufacturers to reference the innovator’s NDA through an Abbreviated New Drug Application (ANDA), relying on the brand’s existing safety and efficacy data.

The trade-off: generic manufacturers must certify with respect to each Orange Book-listed patent. Certifications range from Paragraph I (the patent is expired) to Paragraph IV (the patent is invalid, unenforceable, or not infringed by the generic). The Paragraph IV certification is the trigger for Hatch-Waxman litigation.

Paragraph IV Filing Mechanics

When a generic files an ANDA with a Paragraph IV certification, it must notify each patent owner and the NDA holder within 20 days of the FDA’s acknowledgment letter. The patent owner then has 45 days to file suit for patent infringement in federal district court. If suit is filed within 45 days, an automatic 30-month stay of ANDA approval takes effect, blocking final FDA approval for up to 30 months regardless of the merits of the case.

The 30-month stay is the centerpiece of brand-name companies’ patent defense strategy. It gives the innovator time to litigate the case without the immediate competitive pressure of a generic launch. During the stay period, the brand-name company files its Markman brief (claim construction), conducts fact and expert discovery, and typically reaches a ruling or settlement before the stay expires.

The automatic nature of the 30-month stay has been criticized as creating perverse incentives: brand companies can obtain the stay by filing on any listed Orange Book patent, including secondary patents of questionable validity, without any preliminary showing of likelihood of success. This dynamic contributed to the 2003 Medicare Modernization Act amendments that limited brand companies to one 30-month stay per ANDA, preventing the strategy of listing new secondary patents during ANDA prosecution to trigger successive stays.

The 180-Day First-Filer Exclusivity

The first company to file an ANDA with a Paragraph IV certification for a given drug earns 180 days of market exclusivity if it successfully challenges the patent (through litigation or settlement with a negotiated entry date). During those 180 days, the FDA cannot grant final approval to any subsequent generic filer.

The commercial value of the 180-day period is substantial. For a drug with $3 billion in annual sales, generic erosion from 100% branded to approximately 50-60% of remaining branded sales during the 180-day period, combined with the generic’s initial pricing at 20-30% of brand price, yields a typical 180-day exclusivity value of $150-300 million for the first-filer. This value has historically been sufficient to justify multi-year litigation campaigns against brand patents with genuine invalidity arguments.

The Medicare Modernization Act introduced forfeiture provisions to prevent first-filers from sitting on 180-day exclusivity without actually launching, a “parking” strategy that blocked subsequent generics from entering while the first filer remained in settlement negotiations with the brand. Forfeiture triggers include failure to market within 75 days of a court decision finding the challenged patent invalid or not infringed, or failure to market within 75 days of a court decision on appeal.

Authorized Generics and the 180-Day Calculation

A brand company can launch an “authorized generic,” a generic version sold under the innovator’s NDA but priced at generic levels, during the first filer’s 180-day exclusivity period. The authorized generic erodes the first filer’s revenue during the exclusivity period by creating a competitor product at the same price point, without actually being a new ANDA approval that would violate the exclusivity. Courts have held that authorized generic competition is not barred by the 180-day exclusivity.

The practical effect: the financial value of the 180-day period is reduced when the brand launches an authorized generic simultaneously. First-filers now price their generic settlement negotiations with authorized generic competition as a base case, not a bear case. For brand companies, the authorized generic strategy generates revenue from generic patients who migrate away from the brand regardless of the first-filer’s status, while limiting the first-filer’s profit incentive to challenge in the first place.

Key Litigation Venues and Their Characteristics

The District of Delaware handles the majority of Hatch-Waxman litigation due to the Delaware corporate formation concentration among pharmaceutical companies. Delaware courts have developed substantial expertise in pharmaceutical patent cases, with established local rules for patent cases, predictable scheduling, and a judicial bench familiar with the Markman process. The District of New Jersey handles a significant volume of pharma cases as well, given the New Jersey headquarters concentration.

Venue strategies have shifted since the Supreme Court’s TC Heartland decision in 2017, which held that patent cases can only be brought in a district where the defendant is incorporated or has a regular and established place of business. For foreign generic manufacturers, venue analysis now turns on the location of US distribution facilities, registered agents, and domestic subsidiaries.

Key Takeaways: Section IX

Hatch-Waxman created a litigation system where patent challenges are not an aberration but a designed feature of generic market entry. Every major pharmaceutical patent should be prosecuted, managed, and audited with the assumption that a well-funded generic challenger will mount a Paragraph IV campaign before the patent expires. The 30-month stay and 180-day exclusivity are the two most commercially consequential provisions in US drug patent law and drive the settlement economics of virtually every significant generic entry negotiation.

X. Biosimilar Patent Strategy: The BPCIA Patent Dance in Detail

What the Patent Dance Actually Requires

The Biologics Price Competition and Innovation Act (BPCIA), enacted in 2010, created an FDA pathway for biosimilar and interchangeable biosimilar approvals. The BPCIA also created a patent resolution mechanism that practitioners call the “patent dance,” a multi-step information exchange and litigation sequencing protocol that governs how biosimilar manufacturers and reference product sponsors resolve patent disputes.

Step 1: Within 20 days of the FDA accepting a biosimilar BLA for review, the biosimilar applicant provides the reference product sponsor with a copy of the BLA and manufacturing information sufficient to assess the biosimilar’s compliance with the sponsor’s listed patents.

Step 2: Within 60 days of receiving that information, the reference product sponsor provides the applicant with a list of patents the sponsor believes would be infringed by the biosimilar product.

Step 3: The biosimilar applicant responds within 60 days, providing its positions on validity, enforceability, and infringement for each listed patent, plus a list of patents it believes the sponsor will assert and that should be litigated.

Step 4: The parties exchange revised lists and negotiate which patents will be litigated in an immediate Phase I litigation, with the remaining patents reserved for Phase II litigation that begins 30 days before the biosimilar’s commercial launch.

Phase I litigation proceeds as a conventional patent infringement and invalidity action. The biosimilar applicant must give 180 days’ notice before commercial launch, enabling the reference product sponsor to seek a preliminary injunction on any Phase II patents not yet litigated.

The complexity of the patent dance creates significant strategic options and risks for both parties. Reference product sponsors with broad patent portfolios can use the dance to delay commercial launch while cycling through Phase I and Phase II litigation on different patent groups. Biosimilar applicants can choose to skip portions of the dance, accepting certain legal consequences while accelerating their commercial timeline.

The Amgen v. Sandoz Decision and Its Consequences

The Supreme Court’s 2017 decision in Amgen v. Sandoz resolved two critical patent dance disputes: whether participation in the patent dance is mandatory and whether the 180-day commercial notice can be given before BLA approval. The Court held that the information exchange provisions of the patent dance are optional, not mandatory, and that the biosimilar applicant can give the 180-day notice before or after FDA approval.

This ruling weakened the reference product sponsor’s position by confirming that biosimilar manufacturers can bypass parts of the patent dance, triggering Phase II litigation without the prior information exchange. Biosimilar manufacturers can provide 180-day notice upon BLA acceptance, enabling a commercial launch approximately 180 days after FDA approval without waiting for patent dispute resolution.

The practical consequence for reference product sponsors: the patent dance is now a tool for organizing and sequencing litigation rather than a mandatory process for identifying the complete patent landscape. Sponsors must be prepared to pursue preliminary injunction proceedings in Phase II litigation on short notice, requiring real-time patent preparedness across their full biologic portfolio.

Biosimilar Interchangeability and Its Patent Implications

An interchangeable biosimilar meets a higher FDA standard than a standard biosimilar: it demonstrates that the product can be expected to produce the same clinical result in any given patient, and for products administered multiple times, the risk of switching and alternating between the reference product and the biosimilar is not greater than the risk of using the reference product alone.

The commercial significance: an interchangeable biosimilar can be substituted by a pharmacist for the reference product without physician intervention in most US states, enabling the same automatic substitution mechanism that drives small-molecule generic uptake. The first biosimilar to achieve interchangeability for a given reference product earns one year of exclusivity against other interchangeable biosimilars.

From a patent strategy perspective, the interchangeability designation creates both risk and opportunity. For reference product sponsors, a competitor achieving interchangeability status accelerates market share loss because the commercial friction of non-interchangeable substitution is removed. For biosimilar manufacturers, interchangeability designation is a significant competitive moat against other biosimilar entrants and justifies the additional investment in the switching studies required.

Key Takeaways: Section X

The BPCIA patent dance is a litigation sequencing mechanism, not a comprehensive patent clearance process. Reference product sponsors should prepare for Phase II injunction proceedings on short timelines following FDA approval of biosimilar BLAs. Biosimilar manufacturers should evaluate the costs and benefits of full patent dance participation versus early launch risk with patent litigation reserves.

XI. The Patent Cliff: Revenue Exposure, Case-Specific Modeling, and Mitigation Roadmaps

Scale of the 2024-2030 Cliff

The pharmaceutical industry faces an unprecedented concentration of patent expirations through 2030. Over 190 drugs, including 69 blockbusters, are projected to lose exclusivity between 2024 and 2030, with approximately $300 billion in cumulative annual revenues at risk. The top of this list includes pembrolizumab ($25B, Merck, expiration ~2028-2031 with secondary patent dependencies), ustekinumab ($10B, Johnson & Johnson, US biosimilar entry began 2023), apixaban ($12B, Bristol-Myers Squibb/Pfizer, US patent expiration 2026), and ibrutinib ($10B, AbbVie/Johnson & Johnson, US LOE ~2027).

Revenue Erosion Mechanics

The pattern of revenue erosion following patent expiration follows a predictable but variable curve depending on drug class, number of generic entrants, payer formulary behavior, and the brand’s own commercial response. Oral solid dosage forms with multiple generic entrants see the steepest initial erosion: branded revenue can fall 70-80% within the first six months as payers mandate substitution and pharmacies automatically fill prescriptions with the lowest-priced generic.

Physician-administered drugs, including infused biologics and oncology agents, show slower erosion because the clinical administration channel creates substitution friction. Biosimilar uptake in the US has been substantially slower than small-molecule generic uptake: adalimumab biosimilars launched in 2023 captured roughly 25-30% of the adalimumab market by Q4 2023, far below the 70-80% first-year erosion typical for oral small molecules. European biosimilar uptake is faster, driven by mandatory tendering processes in hospital formularies.

Quantitative Modeling: The Eli Lilly Prozac Precedent

When fluoxetine (Prozac) lost its composition-of-matter patent in 2001, Eli Lilly’s US fluoxetine revenues dropped from $2.4 billion annually to approximately $300 million within two years. The erosion rate exceeded 87% over 24 months. This case established the speed of small-molecule generic displacement as the base case: rapid, deep, and substantially irreversible once the first generic achieves significant distribution.

For Merck’s pembrolizumab approaching its 2028-2031 exclusivity window, the relevant modeling inputs include: annual US Keytruda revenue of $14 billion (US fraction of global $25B); estimated US biosimilar uptake rate given the PD-1 checkpoint inhibitor category’s physician-administered IV and SC administration route; probability-weighted patent life based on PTE filing and secondary patent defense outcomes; and competitive dynamics from Opdivo (nivolumab) biosimilars, which will enter the market contemporaneously.

Under a base case where effective US exclusivity extends to 2031 and biosimilar uptake follows the adalimumab trajectory, Merck’s US pembrolizumab revenue model looks something like this:

2028-2031: Full protected revenue, approximately $14-16B/year (with modest growth). 2032: First biosimilar year, approximately $9-10B branded remaining, heavy market share loss beginning in hospital systems. 2034: Mature generic market, branded revenue approximately $2-3B (physician administration loyalty segment).

This cliff, $14B in annual revenue dropping to $2B over five years, is the central financial risk in any multi-year Merck equity investment thesis.

Mitigation Strategies: The Comprehensive Playbook

Next-Generation Compound Development

The most durable mitigation: developing a next-generation compound that supersedes the current product before it goes off-patent. Lilly’s replacement of Prozac with Cymbalta (duloxetine), a dual serotonin-norepinephrine reuptake inhibitor with a distinct mechanism, partially offset Prozac’s LOE. The timing challenge is enormous: a next-generation compound needs to be in Phase III when the current product’s LOE occurs, requiring 8-12 years of pipeline investment that must be initiated when the current product is at or near peak sales.

R&D Diversification into Orphan and Precision Medicine

The orphan drug and precision medicine sectors offer higher NPV per program due to compressed development timelines, premium pricing, and seven-year US ODE. Many precision oncology companies generate strong returns from a portfolio of focused programs, each with a defined patient population identified by a companion diagnostic, rather than from a single blockbuster. This reduces the single-drug revenue concentration that makes a patent cliff catastrophic.

AstraZeneca’s strategic shift toward oncology, rare diseases, and cardiovascular/metabolic diseases (CVM) over the 2013-2020 period, executed through a combination of internal R&D restructuring and targeted acquisitions (Alexion, Rare Disease; Pearl Therapeutics, respiratory), reduced the company’s exposure to any single product’s LOE event.

Authorized Generics as a Revenue Defense

When secondary patent defense fails and LOE is imminent, an authorized generic allows the branded company to capture revenue from the generic price segment. The authorized generic is sold under the innovator’s ANDA, at generic-competitive prices, allowing the brand to retain some volume even as branded prescription share collapses. Pfizer launched an authorized generic of atorvastatin (Lipitor) simultaneously with the first generic entry in 2011, capturing a significant share of the generic market. The authorized generic strategy reduces the revenue cliff’s steepness by ensuring the brand company participates in the generic market rather than simply losing all non-loyal-prescriber volume.

Case Study: Amgen’s Enbrel Patent Thicket

Amgen’s management of the etanercept franchise represents the most extensively documented example of secondary patent protection enabling long-term commercial dominance. The original etanercept composition-of-matter patent, based on Immunex’s TNF receptor fusion protein work, expired in the US in 2012. Sandoz received FDA biosimilar approval for Erelzi (etanercept-szzs) in 2016. Yet Sandoz did not launch commercially until late 2016 in the EU (where no US patents applied) and faced a US market blocked by Amgen’s manufacturing process and method-of-use patents until 2029.

The key patents blocking US biosimilar entry included manufacturing process patents on specific CHO cell culture conditions, purification methods, and formulation parameters, as well as method-of-use patents on the subcutaneous dosing regimen and specific DMARD-combination treatment protocols. Sandoz and Momenta challenged these patents in PTAB IPR proceedings and district court; Amgen successfully defended the most commercially critical claims. The result: $70+ billion in cumulative Enbrel revenues across the full commercial life, with the secondary patent estate generating an estimated $40+ billion in revenue that would not have been generated without the post-2012 IP protection.

Key Takeaways: Section XI

The 2024-2030 patent cliff is the most concentrated LOE event in pharmaceutical history by revenue at risk. Companies facing blockbuster LOEs need a multi-pronged response: secondary patent defense to slow generic entry, authorized generic programs to participate in the post-LOE market, next-generation compound development to replace revenue, and portfolio diversification to reduce single-product revenue concentration.

Investment Strategy Note

For analysts, the patent cliff creates concrete short opportunities (sell before LOE, cover after generic erosion is priced in) and long opportunities (buy companies that have over-earned on a blockbuster and are now trading below the value of the remaining pipeline, post-cliff). The timing is critical: markets frequently misjudge both the speed of generic erosion and the speed of pipeline value realization. The most common error is underestimating how quickly oral solid dose biosimilars erode branded revenue and overestimating how quickly next-generation pipeline drugs reach market.

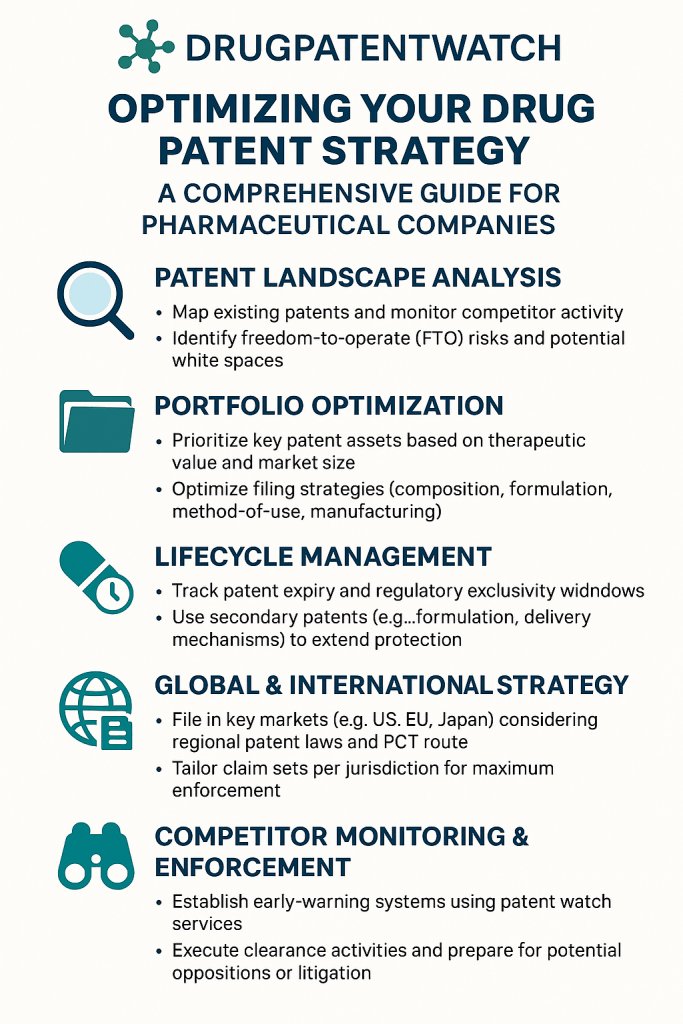

XII. Patent Portfolio Optimization: Audit Frameworks, Pruning Criteria, and Monetization

Portfolio Architecture Principles

An optimized pharmaceutical patent portfolio is not the largest possible portfolio. It is the portfolio that delivers maximum commercial protection per dollar of prosecution and maintenance cost, with coverage concentrated in patents that either protect revenue-generating products, support commercial freedom to operate, or generate licensing income. The pharmaceutical company’s IP team faces the same capital allocation problem as any portfolio manager: too many positions dilute returns, while too few create concentration risk.

Pharmaceutical maintenance fees add up rapidly. US maintenance fees for a granted patent run from $1,800 at 3.5 years to $7,700 at 11.5 years (large entity rates). A company maintaining 2,000 active US patents spends roughly $10-15 million annually in maintenance fees alone, before prosecution attorney fees. For a portfolio of 500 patents in the US plus corresponding foreign filings, annuity costs in Europe, Japan, China, and key emerging markets easily reach $30-50 million per year.

Audit Methodology

A rigorous patent portfolio audit evaluates each patent on four dimensions: commercial relevance (does the patent protect a marketed product, a pipeline product in clinical development, or a technology platform currently in active R&D?), claim scope (is the patent’s claim set broad enough to block competitor products, or have prosecution amendments narrowed it to the point where design-arounds are straightforward?), validity risk (has the patent survived PTAB scrutiny? does it have prior art exposure identified during a freedom-to-operate analysis?), and remaining term (what is the patent’s remaining life considering PTA, PTE, and any terminal disclaimers?).

Patents scoring low on commercial relevance and claim scope, combined with high validity risk and short remaining term, are abandonment candidates. The maintenance fee savings from abandoning a patent that has no commercial value exceed zero, which is the return from maintaining it.

Pruning Criteria: When to Abandon

Abandonment decisions follow a decision tree. First: is the patent listed in the Orange Book or Purple Book as covering an approved product? If yes, do not abandon without a detailed analysis of what ANDA or biosimilar market entry it blocks. Second: does the patent cover active pipeline programs in Phase II or Phase III? If yes, maintain it regardless of current commercial value. Third: has the patent been the subject of a Paragraph IV challenge or PTAB IPR? If it has survived challenge, its demonstrated validity is an asset; if it was invalidated, it has zero commercial value.

Patents covering technologies abandoned by R&D, compounds that failed in development, or approaches superseded by newer platform technologies are the cleanest abandonment candidates. These patents consume maintenance budget without contributing commercial protection.

Monetization: Out-Licensing Non-Core IP

Non-core patents covering technology platforms or compounds outside the company’s current therapeutic focus can be out-licensed or sold rather than simply abandoned. The market for pharmaceutical patent transactions has grown significantly: IP marketplace platforms, patent brokers, and NPE (non-practicing entity) licensing operations actively purchase pharmaceutical IP. A patent covering a validated mechanism or a lead compound in a therapeutic area the original developer has exited can have significant value to a competitor or emerging company pursuing that target.

PLIVA’s Azithromycin licensing to Pfizer is the canonical example of an early-stage pharmaceutical company monetizing core IP through a major pharma licensing deal. PLIVA discovered and globally patented Azithromycin but lacked Pfizer’s commercial infrastructure for global launch. The licensing deal, which led to Zithromax’s commercial success under Pfizer, generated royalties that funded PLIVA’s expansion into the US and European markets. The deal structure illustrates that IP valuation is not solely a function of the patent holder’s own commercial capabilities but also of what the IP enables for a licensee with superior distribution.

Key Takeaways: Section XII

Patent portfolio optimization is a continuous cost-benefit exercise, not a one-time event. Annual audits aligned with pipeline updates ensure that maintenance costs track commercial priorities. Abandonment of non-commercial patents and out-licensing of non-core IP are active value-generating decisions, not admissions of failure.

XIII. Licensing Architecture: In-Licensing, Out-Licensing, Cross-Licensing, and Valuation

In-Licensing: Accessing External Innovation

In-licensing is the acquisition of rights to an external technology, compound, or patent estate. For large pharmaceutical companies, in-licensing is the primary mechanism for accessing breakthrough innovations generated by smaller biotechs or academic institutions that lack clinical development or commercial infrastructure. The in-licensor retains the underlying IP; the licensee acquires the right to develop and commercialize.

Licensing deal terms vary by stage, therapeutic category, and competitive dynamics. A Phase I-stage compound in oncology might carry an upfront payment of $20-50 million, milestones totaling $300-600 million tied to clinical and regulatory events, and a royalty rate of 10-15% on net sales. A Phase III-ready compound with clinical proof-of-concept in a high-value indication might carry $200-500 million upfront, milestones exceeding $1 billion, and royalties in the 15-20% range.

The key licensing agreement provisions are: exclusivity scope (geographic, indication-specific, or compound-class exclusivity define the value boundary), sublicensing rights (whether the licensee can further sublicense to third parties, critical for global licensing deals where regional partners may be needed), improvement patents (who owns IP generated by the licensee during development, and does it feed back to the licensor?), and milestone definitions (ambiguous milestone triggers are the leading source of licensing litigation).

Cross-Licensing: IP Exchange Without Royalty Cash Flow

Cross-licensing agreements grant each party rights to use the other party’s patents, often without monetary royalties changing hands. The exchange of patent rights in lieu of payment reflects the mutual value recognition that each party’s IP creates for the other. Cross-licensing is common in areas with dense patent thickets, including biologic manufacturing processes, where multiple companies hold overlapping IP covering different aspects of the same technical process.

The strategic value of cross-licensing: freedom to operate without litigation exposure, cost reduction by avoiding duplicative R&D to design around a competitor’s patents, and access to platform technologies that would otherwise require licensing fees. The risk: a poorly negotiated cross-license can inadvertently grant a competitor access to core IP at below-market value, or fail to include improvement patents, allowing the competitor to leverage the licensed technology into innovations that later compete with the licensor’s products.

Key Takeaways: Section XIII

Licensing strategy should be integrated with portfolio strategy: out-licensing non-core IP generates revenue while reducing maintenance costs; in-licensing fills pipeline gaps at a cost reflective of the licensee’s risk-adjusted return; cross-licensing eliminates litigation risk in areas with overlapping IP. Each transaction should be evaluated against a clearly defined build/buy/partner analysis that quantifies the cost of independent IP development against the licensing economics.

XIV. AI in Drug Discovery and Patent Strategy: Inventorship Rules, Claim Architecture, and Portfolio Tools

How AI Accelerates Discovery and Changes What Gets Patented

AI-driven drug discovery platforms, including structure-based design tools like Schrodinger’s physics-based modeling stack, generative chemistry platforms like Insilico Medicine’s Chemistry42, and protein structure prediction integrated into lead optimization (AlphaFold derivatives), are compressing the timeline from target identification to clinical candidate. The claimed reduction is from five to six years using conventional medicinal chemistry to two to three years using AI-accelerated workflows.

What changes: AI platforms generate far more candidate molecules than conventional programs, which means more potential patent filings, broader claim scaffolds supported by more species data, and a higher volume of invention disclosure forms requiring triage. What also changes: the standard for non-obviousness shifts. When an AI trained on millions of known structure-activity relationships generates a lead compound, the question of whether a human medicinal chemist of ordinary skill would have been led to that compound becomes more complex. The AI’s output might look obvious in retrospect, since it drew on public training data, but the specific compound prediction required computational methods not available to a skilled artisan using conventional approaches.

Inventorship Under the Thaler Standard

Under current US patent law, only natural persons can be named as inventors. The Federal Circuit’s 2022 decision in Thaler v. Vidal rejected applications listing DABUS, an AI system, as the sole inventor of two inventions. The court held that Section 100(f) of the Patent Act limits inventorship to natural persons, and that Congress would have to act to extend inventorship rights to AI systems.

The consequence for pharmaceutical AI discovery programs: human contribution to the conception of the claimed invention must be documented and must be substantive. “Significant contribution to the conception of the claimed invention” is the legal standard from Pannu v. Iolab. For AI-assisted discovery, this means documenting the human decisions that shaped the AI output: selecting training datasets, defining objective functions, making expert judgment calls on which AI-generated candidate to advance based on ADMET properties, and applying medicinal chemistry intuition to modify the AI’s initial output.

Companies using AI in discovery should implement structured invention disclosure processes that capture: which AI tool was used, what human instructions were given to the AI, what human expert decisions modified the AI’s output, and why those human decisions were scientifically non-obvious. This documentation trail is the foundation of an inventorship argument if the patent is challenged on conception grounds.

Claim Architecture for AI-Discovered Drugs

AI-generated drug discovery programs often produce a large number of active compounds across a chemotype series, sometimes thousands of compounds. This breadth of data supports broader Markush group claims in the patent application, since the claim scope must be commensurate with the enablement disclosure. A conventional medicinal chemistry program might generate 50-100 tested compounds supporting a relatively narrow Markush group; an AI platform generating 10,000 compounds with confirmed activity supports broader claims.

The strategic implication: AI-assisted discovery programs should file patent applications that capture the full scope of the AI-defined chemical space, not just the specific lead compound. A composition-of-matter claim covering a broad Markush group, supported by AI-generated activity data across the group, provides generic competitors far less room to design around into unclaimed but active chemical space.

AI Tools for Portfolio Management

Beyond discovery, AI tools are reshaping how companies manage existing patent portfolios. Natural language processing (NLP) tools now scan patent databases, opposition proceedings, and litigation outcomes in near real-time, flagging competitor filings in specific technology areas, identifying patents that might be used to block commercial programs, and prioritizing IPR petitions based on the strength of available prior art.

Machine learning-based patent valuation models now incorporate citation frequency, forward citation velocity, legal status, prosecution history, and claims language to produce automated patent strength scores. These scores, while imprecise as standalone metrics, are useful for prioritizing audit resources and identifying high-priority patents for defensive litigation preparation.

Key Takeaways: Section XIV

AI is changing both the volume and the character of pharmaceutical patent filings. IP teams must adapt processes for invention capture, inventorship documentation, and claim drafting to accommodate AI-assisted discovery workflows. The legal framework governing AI inventorship is settled for now: humans must be the inventors. The practical question is how to document human contribution with sufficient specificity to survive conception challenges.

XV. Global Patent Harmonization: PCT, TRIPS, PPH, and the Persistent Friction Points

The PCT System: What It Provides and What It Does Not

The Patent Cooperation Treaty (PCT), administered by WIPO, provides a single international filing mechanism that establishes a priority date recognized in all 157 contracting states. Filing a PCT application gives an applicant up to 30 months from the priority date (31 months in some jurisdictions) to decide which national or regional patent offices to enter for substantive examination. The PCT also provides an international search report and written opinion, which serves as a preliminary patentability assessment.

What the PCT does not provide: a granted international patent. Patent grant remains a national and regional decision; the PCT only streamlines the process of entering national phases. A PCT application that receives a positive international search report still requires separate examination and prosecution in each national office where grant is sought. For pharmaceutical companies seeking protection in 40 or more jurisdictions, the PCT is a timing tool, not a cost reduction tool; the aggregate examination, translation, and annuity costs across multiple jurisdictions remain substantial.

The Patent Prosecution Highway (PPH)

The PPH enables an applicant who has received a positive examination outcome in one patent office to request accelerated examination in another participating office, leveraging the first office’s examination results. Participating offices in the PPH include the USPTO, EPO, JPO, CNIPA (China), and over 30 others. For pharmaceutical companies prosecuting the same patent family in multiple jurisdictions simultaneously, the PPH can reduce prosecution pendency and cost by enabling one jurisdiction’s allowance to accelerate examination elsewhere.

Persistent Friction: Local Clinical Trial Requirements