Last updated: February 19, 2026

PRILOSEC (omeprazole) is a proton pump inhibitor (PPI) that effectively reduces gastric acid production. Its market trajectory is characterized by significant patent challenges, generic competition, and sustained demand driven by its therapeutic efficacy.

What is PRILOSEC and its Mechanism of Action?

PRILOSEC is the brand name for omeprazole, a medication belonging to the class of proton pump inhibitors (PPIs). It functions by irreversibly inhibiting the H+/K+-ATPase enzyme system, commonly known as the proton pump, which is located in the gastric parietal cells. This inhibition blocks the final step in gastric acid secretion, leading to a profound and long-lasting reduction in intragastric acidity.

The primary indications for PRILOSEC include the treatment of:

- Gastroesophageal Reflux Disease (GERD): This involves the management of symptoms such as heartburn and regurgitation, as well as the healing of erosive esophagitis.

- Peptic Ulcer Disease: This includes the treatment of duodenal ulcers and gastric ulcers.

- Zollinger-Ellison Syndrome: A rare condition characterized by excessive gastric acid production.

- Helicobacter pylori (H. pylori) Eradication: When used in combination with antibiotics, PRILOSEC helps eradicate H. pylori infection, a common cause of peptic ulcers.

What are the Key Patent Milestones for PRILOSEC?

The patent history of omeprazole is critical to understanding its market dynamics. The original patent for omeprazole was filed by Astra AB (now AstraZeneca) in the United States in 1979 and granted in 1982 [1]. This patent provided initial market exclusivity for the drug.

Key patent milestones include:

- Original U.S. Patent: U.S. Patent No. 4,255,431, granted March 10, 1981 [1].

- Exclusivity Periods: Following patent grants, regulatory bodies provide periods of market exclusivity. For PRILOSEC, this initially allowed AstraZeneca to maintain a monopoly.

- Patent Expirations: The primary U.S. patent for omeprazole expired in the early 2000s, paving the way for generic competition. For instance, it was widely reported that generic versions became available around 2001-2002 [2].

- Subsequent Patents and Litigation: AstraZeneca pursued secondary patents, such as those related to formulations (e.g., delayed-release capsules) and manufacturing processes. These patents were often subject to legal challenges from generic manufacturers seeking to enter the market. Litigation surrounding these secondary patents frequently involved debates over patent validity, infringement, and inventorship. For example, a significant legal battle involved disputes over the enantiomer of omeprazole, esomeprazole (Nexium), and its relationship to the original omeprazole patent [3].

How Has Patent Expiration Impacted PRILOSEC's Market Share and Revenue?

The expiration of PRILOSEC's core patents triggered a significant shift in its market dynamics, characterized by rapid erosion of market share and substantial revenue decline for the innovator drug.

Market Share Dynamics:

- Pre-Expiration: Before patent expiry, AstraZeneca held a near-monopoly on omeprazole, with PRILOSEC as the dominant branded product.

- Post-Expiration: Upon the entry of generic omeprazole, the market share for branded PRILOSEC began to decline sharply. Generic manufacturers, able to produce omeprazole at a lower cost, offered their products at significantly reduced prices.

- Generic Dominance: Within a few years of generic availability, generic omeprazole products collectively captured the vast majority of the market share for the active pharmaceutical ingredient (API). This is a typical pattern observed for blockbuster drugs following patent expiry.

Revenue Trajectory:

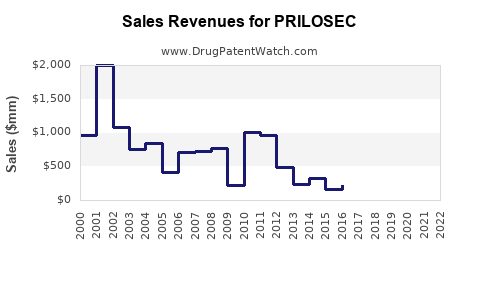

- Peak Sales: PRILOSEC achieved peak annual sales for AstraZeneca in the late 1990s and early 2000s, with figures often cited in the range of \$5 billion to \$6 billion globally before generic entry [4].

- Revenue Decline: Following the introduction of generics, PRILOSEC's sales experienced a steep decline. For example, in 2002, shortly after generic entry, AstraZeneca reported a significant drop in PRILOSEC sales, reflecting the immediate impact of competition.

- Sustained Demand for Omeprazole: While branded PRILOSEC sales diminished, the overall market for omeprazole continued to be substantial due to its proven efficacy and widespread prescribing. Generic omeprazole manufacturers benefited from this sustained demand, collectively achieving high sales volumes.

Comparison with Esomeprazole (Nexium):

AstraZeneca sought to mitigate the impact of generic omeprazole by developing and marketing esomeprazole (Nexium), a more potent enantiomer of omeprazole. Nexium was introduced with its own patent protection, allowing AstraZeneca to recapture market share and revenue.

- Nexium's Rise: Nexium became a significant revenue driver for AstraZeneca, often exceeding \$5 billion annually during its patent-protected period.

- Cannibalization and Lifecycle Management: While Nexium was marketed as a superior product, it also effectively cannibalized some of the market for branded PRILOSEC. The strategy aimed to extend the overall lifecycle of the omeprazole molecule's market presence under different brand names and patent protections.

- Nexium's Generic Entry: Similar to PRILOSEC, Nexium eventually faced its own patent expiries, leading to the introduction of generic esomeprazole and a subsequent decline in branded Nexium sales.

The experience of PRILOSEC exemplifies the predictable market dynamics following the loss of patent exclusivity, highlighting the critical role of generic competition in driving down drug prices and shifting market share.

What is the Current Market Status of PRILOSEC and its Generic Equivalents?

The market for PRILOSEC (omeprazole) is now dominated by generic manufacturers. Branded PRILOSEC sales have become a small fraction of their former peak.

Generic Market Dominance:

- API Production: Numerous pharmaceutical companies worldwide manufacture and market generic omeprazole. The active pharmaceutical ingredient (API) is widely available.

- Pricing: Generic omeprazole is available at a fraction of the cost of branded PRILOSEC. This price disparity drives significant prescription volume towards generic options.

- Market Share: Generic omeprazole collectively holds over 95% of the market share for this therapeutic agent.

- Over-the-Counter (OTC) Availability: In many regions, lower-dose omeprazole formulations are also available over-the-counter, further increasing accessibility and market penetration outside of prescription channels.

Branded PRILOSEC:

- Niche Market: Branded PRILOSEC continues to exist but primarily serves a niche market of patients who specifically request or are prescribed the original brand for personal preference or by physician direction.

- Limited Sales: Sales figures for branded PRILOSEC are now minimal compared to its historical performance. AstraZeneca may have divested or significantly reduced its marketing efforts for the original brand.

Therapeutic Class Performance:

- PPI Market: Omeprazole remains a foundational therapy within the broader proton pump inhibitor class. However, newer PPIs and H2 receptor antagonists also compete for market share.

- Competition: While omeprazole is a widely used and cost-effective option, other PPIs like lansoprazole, pantoprazole, rabeprazole, and esomeprazole (Nexium, which is also now largely genericized) continue to be prescribed. The choice often depends on physician preference, patient response, and formulary considerations.

Regulatory Landscape:

- FDA Approvals: The U.S. Food and Drug Administration (FDA) has approved numerous generic omeprazole applications over the past two decades. Each approval signifies a successful demonstration of bioequivalence to the reference listed drug.

- Global Availability: Generic omeprazole is available in virtually all major pharmaceutical markets globally, contributing to its widespread use.

The current market status reflects a mature drug lifecycle where the primary value is captured by cost-effective generic alternatives, while the innovator brand plays a minimal role in overall market volume and revenue.

What are the Financial Implications for Companies Involved with PRILOSEC?

The financial implications for companies involved with PRILOSEC have evolved dramatically since its introduction and subsequent patent expiry.

For AstraZeneca (Innovator):

- Early Revenue Generation: AstraZeneca experienced immense financial success during PRILOSEC's patent-protected period. Billions of dollars in revenue were generated, funding further R&D and acquisitions.

- R&D Investment: Profits from PRILOSEC fueled significant investments in developing new drugs, including esomeprazole (Nexium), which served as a crucial lifecycle management strategy.

- Post-Patent Decline: Following patent expiry, sales of branded PRILOSEC plummeted. This loss of revenue necessitated strategic shifts and a focus on newer, patent-protected products.

- Divestment and Licensing: Over time, AstraZeneca may have divested rights or licensed older products like PRILOSEC to other entities or focused its resources on next-generation therapies.

For Generic Manufacturers:

- Significant Revenue Opportunity: The expiration of PRILOSEC patents presented a substantial revenue opportunity for generic drug manufacturers. The large market volume and the ability to produce at lower costs allowed for profitable operations.

- Market Entry Strategy: Companies like Teva Pharmaceutical Industries, Mylan (now Viatris), and numerous others successfully launched generic omeprazole, capturing significant market share.

- Volume-Based Business: The financial model for generic omeprazole is largely volume-driven. While profit margins per unit are lower than for branded drugs, the high prescription volume ensures substantial overall revenue.

- Competition and Price Erosion: The market for generic omeprazole is highly competitive, leading to continuous price erosion. Companies must maintain efficient manufacturing and supply chains to remain competitive.

- Portfolio Diversification: Generic companies typically market a broad portfolio of generic drugs. Omeprazole, while significant, is usually one of many products contributing to their revenue.

For Healthcare Payers and Patients:

- Cost Savings: The availability of generic omeprazole has resulted in massive cost savings for healthcare systems, insurers, and patients. The price differential between branded and generic forms is typically 80-90% or more.

- Increased Accessibility: Lower prices have increased patient access to effective acid suppression therapy, improving treatment rates for conditions like GERD and peptic ulcers.

- Formulary Decisions: Payers (insurance companies, PBMs) heavily favor generic omeprazole on their formularies due to its cost-effectiveness, further driving down branded sales.

The financial trajectory of PRILOSEC illustrates a common theme in the pharmaceutical industry: immense profitability during the innovator period, followed by a significant shift in financial gains towards generic manufacturers after patent expiry, ultimately benefiting payers and patients through reduced costs.

What are the Future Market Projections for PRILOSEC?

The future market for PRILOSEC is projected to remain stable, driven by its established efficacy and cost-effectiveness as a generic medication.

Continued Generic Dominance:

- Stable Demand: The underlying demand for omeprazole as a treatment for acid-related gastrointestinal disorders is expected to remain robust. The aging global population and the prevalence of conditions like GERD contribute to this sustained need.

- Price Sensitivity: The market will continue to be highly price-sensitive. Generic omeprazole will remain the preferred choice for most prescribers and payers.

- Competition Among Generics: The generic market will remain competitive, with ongoing efforts by manufacturers to optimize production costs and maintain market share. This competitive landscape will likely prevent significant price increases for generic omeprazole.

Limited Growth for Branded PRILOSEC:

- Negligible Market Share: Branded PRILOSEC is unlikely to regain significant market share. Its role will continue to be marginal, serving a very small segment of the market.

- Potential for Withdrawal: In some markets, AstraZeneca or its licensees might eventually withdraw the branded product if sales become economically unviable, though this is a slow process.

Evolution of PPI Market:

- Therapeutic Substitution: While omeprazole remains a primary choice, the broader PPI market is subject to ongoing evolution. New formulations or combination therapies could emerge, but are unlikely to displace the established generic omeprazole market given its cost advantage.

- Other Acid Suppressants: The market for other acid suppressants (e.g., H2 blockers, potassium-competitive acid blockers) will continue to influence the overall landscape, but omeprazole's established position is secure.

Potential Factors Influencing the Market:

- Regulatory Changes: Any significant changes in regulatory approval pathways or post-market surveillance requirements could indirectly affect the generic market, but are unlikely to disrupt the fundamental dynamics.

- Reimbursement Policies: Evolving healthcare reimbursement policies by payers could slightly shift prescribing patterns, but generic omeprazole is typically favored.

- New Clinical Guidelines: Updates to clinical guidelines for managing acid-related disorders might influence treatment algorithms, but are unlikely to diminish the role of cost-effective omeprazole.

In summary, the future market for PRILOSEC is characterized by its entrenched position as a widely accessible and affordable generic medication. Significant growth or shifts in its market share are not anticipated.

Key Takeaways

- PRILOSEC (omeprazole) is a proton pump inhibitor that significantly reduced gastric acid production.

- The drug's patent expired in the early 2000s, leading to the widespread introduction of generic omeprazole.

- Patent expiration resulted in a dramatic decline in branded PRILOSEC sales and market share, a common outcome for blockbuster drugs.

- Generic omeprazole now dominates the market, offering significant cost savings to healthcare systems and patients.

- AstraZeneca mitigated some of the revenue loss through the development of esomeprazole (Nexium), another PPI with its own patent protection.

- The financial trajectory of PRILOSEC shows immense early profitability for the innovator, followed by substantial revenue generation for generic manufacturers.

- The future market for omeprazole is projected to remain stable, with continued generic dominance driven by its established efficacy and cost-effectiveness.

Frequently Asked Questions

-

Has AstraZeneca continued to market branded PRILOSEC?

AstraZeneca has largely transitioned its focus to newer therapies. While the branded PRILOSEC might still be available in some markets, its market presence and sales are minimal compared to its peak. Its market role is primarily that of a legacy product.

-

What is the difference between omeprazole and esomeprazole (Nexium)?

Esomeprazole is the S-enantiomer of omeprazole. It is marketed as being more potent and having a more consistent effect on acid reduction compared to racemic omeprazole (the mixture of enantiomers found in generic omeprazole). However, both are highly effective PPIs.

-

Are there any significant safety concerns associated with long-term omeprazole use that might impact its market?

Long-term use of PPIs, including omeprazole, has been associated with potential risks such as vitamin B12 deficiency, hypomagnesemia, increased risk of fractures, and an increased susceptibility to certain infections like Clostridium difficile. These concerns are managed through appropriate prescribing guidelines and periodic reassessment of treatment necessity.

-

How do regulatory approvals for generic omeprazole impact market competition?

Each FDA approval for a generic omeprazole product signifies a new competitor entering the market. This increases competition, driving down prices further and ensuring a robust supply chain for affordable omeprazole.

-

What was the approximate peak annual revenue generated by branded PRILOSEC before generic competition?

Branded PRILOSEC achieved peak annual sales estimated to be between \$5 billion and \$6 billion globally for AstraZeneca. This figure highlights the drug's significant commercial success during its period of market exclusivity.

Citations

[1] U.S. Patent No. 4,255,431. (1981, March 10). Method of preparing 2-mercaptobenzimidazole derivatives. Astra AB.

[2] Generic drug entry for omeprazole. (2001-2002). Various pharmaceutical industry reports and news archives.

[3] In re Omeprazole Patent Litigation, 227 F.3d 1352 (Fed. Cir. 2000).

[4] AstraZeneca PLC Annual Reports. (1998-2002). Publicly available financial statements.