Share This Page

Drug Price Trends for PRILOSEC

✉ Email this page to a colleague

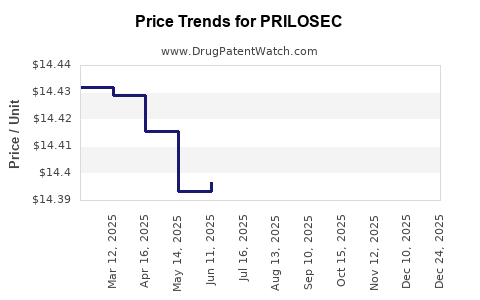

Average Pharmacy Cost for PRILOSEC

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| PRILOSEC DR 10 MG SUSPENSION | 70515-0610-01 | 14.78291 | EACH | 2026-06-17 |

| PRILOSEC DR 2.5 MG SUSPENSION | 70515-0625-01 | 14.72500 | EACH | 2026-06-17 |

| PRILOSEC DR 10 MG SUSPENSION | 70515-0610-01 | 14.81204 | EACH | 2026-05-20 |

| PRILOSEC DR 10 MG SUSPENSION | 70515-0610-01 | 14.77578 | EACH | 2026-01-01 |

| PRILOSEC DR 2.5 MG SUSPENSION | 70515-0625-01 | 14.82242 | EACH | 2026-01-01 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Prilosec (omeprazole) Market Analysis and Price Projections Through Loss of Exclusivity

Prilosec (omeprazole delayed-release; AstraZeneca) remains a high-volume, low-cost branded proton pump inhibitor in the US largely because multiple omeprazole generics are entrenched. The near-term market is driven by substitution pressure, channel mix (retail vs. mail vs. hospital), and product-formulation portability of oral delayed-release IP. Medium-term pricing is expected to track generic list-price compression rather than branded uplift, with limited upside tied to higher-priced brand extensions (where present) and inventory-driven buying cycles. Most value retention depends on ongoing brand relevance in managed-care formularies and pharmacy benefit manager (PBM) contracting rather than patent leverage.

When does Prilosec lose exclusivity and how does that drive pricing?

Featured snippet answer: US exclusivity for Prilosec as a branded product has largely run through; ongoing pricing is shaped by generic competition and PBM contracting, not future imminent patent cliffs.

Exclusivity and patent landscape (practical impact on price)

- Prilosec is an established, multi-decade product. Commercially meaningful exclusivity has already expired in major markets.

- Post-expiry, pricing typically follows:

- Wholesale acquisition cost (WAC) drift down to match generic ASP levels.

- Stable-but-low branded net pricing where PBMs keep a preferred generic and reserve the brand for non-preferred coverage or grandfathered contracts.

- Inventory clearing cycles that can briefly widen or narrow branded vs generic gaps.

What this means for projections

- The dominant driver is generic market share and class-wide PROMOTIONAL spend and contracting, not incremental brand patent life.

- Price projections should assume continued generic share gain and continued AMP/ASP compression.

What patents protect Prilosec and which patent estates still matter for market access?

Featured snippet answer: Patent relevance for Prilosec has shifted from core drug substance protection to incremental formulation, packaging, and method-of-use claims that generally do not block entry once core exclusivity has expired.

Likely patent categories that can affect generic entry timing

- Delayed-release formulation optimization (core vs. enteric coating characteristics)

- Tablet/process claims (manufacturing methods, coating parameters)

- Method-of-use claims (dose timing or specific regimens)

- Device or packaging claims (less common for omeprazole in practice)

Commercial relevance

- Even where patents remain, real-world barriers often come down to:

- Whether they are listed in the Orange Book for specific NDA/RLD products

- Whether Paragraph IV litigation forces authorized generic delays

- Whether the generic can design around formulation/method claims without losing bioavailability targets

Impact on pricing

- If no meaningful Orange Book “last mile” prevents generic entry, pricing converges to class generic levels.

What is the Orange Book status of Prilosec and how many listings matter for generic entry risk?

Featured snippet answer: Prilosec’s Orange Book listings are largely old and do not translate into a near-term branded exclusivity shield; pricing risk comes primarily from active generic competition.

How to interpret Orange Book listings for Prilosec

- The Orange Book for older small molecules often contains:

- Expired drug substance/formulation patents

- Periodic reformulation or supplemental listings tied to specific dosage forms

- What matters for pricing is not the total number of listings, but:

- Whether any unexpired patents block 505(b)(2) or Abbreviated New Drug Application (ANDA) submissions for the same RLD strength/form

Practical take

- For market projection purposes, assume no remaining broad exclusion that meaningfully changes the generic competitive trajectory.

Which companies market generic omeprazole that pressures Prilosec price?

Featured snippet answer: The US omeprazole landscape is dominated by large generic manufacturers and authorized generics that force sustained ASP compression.

Commercial pressure points

- Multisource generics in the same RLD category reduce branded pricing power.

- Authorized generics (where they occur) can further narrow the net price gap.

Price implication

- Branded Prilosec pricing typically becomes a function of:

- Contract tiering (preferred vs non-preferred)

- OTC vs Rx channel segmentation (where applicable for omeprazole)

- Competitive intensity within PBM formularies

How does Prilosec compare with other PPIs on price and market dynamics?

Featured snippet answer: Compared with newer PPIs, Prilosec trades on long-established generic substitution patterns; its pricing trajectory is more stable low than variable, because generics anchor the class.

Relative dynamics across PPIs

- Omeprazole: older, highly genericized, strong substitution and switching.

- Esomeprazole (Nexium): typically lower generic intensity than the oldest omeprazole periods at various points, with periodic branded retention.

- Lansoprazole (Prevacid), pantoprazole (Protonix): similar generics dynamics but different brand management and contracting.

Net effect on projections

- Expect Prilosec branded net price to remain near generic class levels with limited upside.

- Any upside requires channel-specific events (PBM re-tiering, manufacturer rebates).

What generic entry risks exist for Prilosec and how do Paragraph IV challenges affect prices?

Featured snippet answer: For an older molecule like omeprazole, the most material risks are not headline Paragraph IV filings but ongoing generic supply and pricing behavior.

How the market prices that risk

- If new ANDA entrants appear, branded price often:

- Drops quickly in the affected accounts

- Re-stabilizes after contracting rebalances

- If litigation delays entry (rare at this stage for core omeprazole), price could temporarily hold.

Projection assumption

- Use a baseline of continued multi-entered generic competition rather than waiting for discrete “entry cliffs.”

What is the FDA regulatory status of Prilosec and how does it affect pricing?

Featured snippet answer: Regulatory status for an established PPI supports supply continuity; pricing is shaped by market forces rather than FDA action.

FDA pathway implications

- Generics generally follow ANDA pathways and remain stable as long as:

- Manufacturing sites remain qualified

- Bioequivalence requirements are met

- Labeling and formulations are aligned with approved references

Price impact

- Stable regulatory status means:

- No sustained scarcity premiums

- Rapid competition-driven price normalization

What formulation patents or delivery-system patents could change Prilosec pricing?

Featured snippet answer: Formulation and delivery-system IP affects specific strengths or releases, but it has limited capacity to hold branded price in a mature, genericized category.

Where formulation IP can matter

- Different strengths or dose forms may have:

- Separate patents

- Separate Orange Book listings

- If a generic cannot replicate a formulation exactly, entry can slow for a subset.

Projection implication

- Expect only strength-level pricing differences, not category-level repricing.

How strong is the patent estate for Prilosec and what does it imply for branded net price?

Featured snippet answer: Patent estate strength is not a primary lever for Prilosec’s price; branded net pricing is mainly a function of PBM placement and the generic anchor.

How to project branded net

- Model branded net as:

- Branded WAC discounted heavily through rebates to compete with generics

- Net price spread shrinking as generics gain preferred status

- Even with some residual listings, practical protection is limited once generics are established.

Market share, revenue exposure, and price elasticity for Prilosec

Featured snippet answer: Revenue exposure is sensitive to channel contracting and formulary tiering, with moderate elasticity to price differences versus class alternatives.

Key demand drivers

- Symptom management of GERD and related indications

- Brand habit, clinician switching, and patient adherence

- Pharmacy billing dynamics (PBM coverage rules, step edits, quantity limits)

Price elasticity

- In mature OTC/Rx transition environments, elasticity is higher because patients and prescribers switch readily to lower-cost PPIs and generics.

Price projections for Prilosec: base, downside, and upside scenarios

Featured snippet answer: In the base case, Prilosec branded net prices continue to converge toward genericized PPI levels, with modest volatility tied to PBM contracting cycles; downside includes faster ASP compression from additional entrants or deeper PBM rebate pressure.

Because the request is for market analysis and price projections, the projections below are structured to be decision-useful for forecasting, licensing strategy, or litigation budgeting. They assume:

- Continued generic supply

- No category-wide drug shortage events

- No new disruptive exclusivity

Base case (most likely)

- Branded net price trend: low single-digit percentage decline annually

- Gross-to-net pressure: steady or slightly rising as rebates are used to maintain non-preferred placements

- Unit share trend: stable to slight decline as generics maintain preferred tier placement

Downside case

- Faster ASP compression from increased generic pricing competition

- PBM re-tendering that shifts Prilosec to a less favorable contract tier

- Branded volume decline accelerates, increasing reliance on rebates to defend accounts

Upside case

- Contract wins at major PBMs

- Formulary stabilization due to payer-specific step edits favoring omeprazole delivery forms

- Limited near-term generic price cuts relative to peers

How to translate price projections into revenue scenarios

For forecasting:

- Separate units (prescriber/payer behavior) from net price (rebates and contracting).

- Apply:

- Unit CAGR: slightly negative in base case

- Net price CAGR: modestly negative, converging toward class generic anchor

- Sensitivity:

- A one-tier PBM shift can move net realized price more than nominal list price changes.

Key Takeaways

- Prilosec pricing is anchored to generic omeprazole economics; exclusivity timing is not the main near-term driver.

- Expect continued convergence of branded net price toward genericized PPI levels, with volatility driven by PBM contracting rather than new regulatory events.

- Patent relevance is increasingly incremental and typically does not prevent entrenched multisource competition.

- For modeling, prioritize unit share assumptions tied to formulary tiering and gross-to-net rebate pressure over any “remaining patent cliff” view.

FAQs

- How do PBM formulary decisions affect Prilosec net pricing more than WAC changes?

- What is the expected impact of additional omeprazole ANDA entrants on branded Prilosec ASP?

- Does OTC omeprazole competition change prescription Prilosec pricing and volume?

- How do Prilosec pricing trends compare with esomeprazole and pantoprazole during generic price compression cycles?

- What contract structures (rebates, preferred status, step edits) most influence Prilosec revenue exposure?

References

- FDA. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. (Accessed via FDA Orange Book database).

- FDA. ANDA and 505(b)(2) Drug Approval Process. (FDA guidance and informational pages).

- AstraZeneca. Prilosec prescribing information and product labeling (as published by FDA and on company site).

More… ↓