Last updated: April 24, 2026

What is the market structure for famotidine?

Famotidine is an oral histamine H2-receptor antagonist with a long commercial history and broad availability. The market dynamics are dominated by loss of exclusivity, low manufacturing differentiation, and high substitution among functionally similar acid-suppressing therapies.

Market characteristics

- Generic-led category: Famotidine is widely marketed as a generic product across multiple strengths (most commonly 20 mg and 40 mg).

- Low brand stickiness: Switching to other generic famotidine SKUs is common when pricing and distribution are favorable.

- Therapeutic substitution pressure: Proton pump inhibitors (PPIs) and antacids compete at the use-case level (dyspepsia, GERD symptom control, ulcer-related indications).

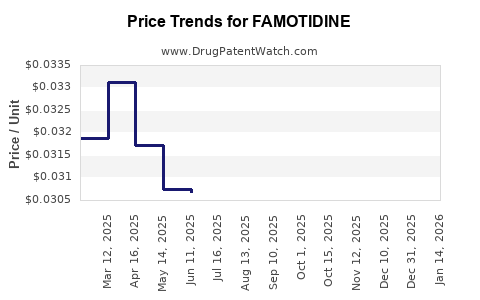

- Price-driven procurement: Hospital and pharmacy formularies tend to optimize acquisition cost, which compresses net pricing for widely stocked generics.

Implication for revenue

- Volume matters more than price. Revenue growth, when it occurs, tends to track distribution scale, contracted pricing, and inventory cycles rather than premiumization.

- Pricing floors exist but are fragile. Once multiple suppliers ramp into the same channels, net price can drift toward sustainable generic margins.

How does the drug’s legal and supply landscape affect pricing?

Famotidine’s financial trajectory is tightly linked to:

- Generic competition intensity

- Regulatory and manufacturing continuity

- Channel contracting behavior (wholesale and institutional)

Pricing pressure mechanics

- Entry of additional generic manufacturers tends to lower average net price across the category.

- Manufacturing disruptions can temporarily lift pricing when supply tightens, but the benefit typically fades as supply normalizes.

- Parallel substitution across acid-suppressing drugs limits downside protection: if famotidine pricing weakens, some demand migrates to alternatives.

What are the key demand drivers for famotidine?

Demand is concentrated in common gastrointestinal (GI) symptom and acid-related use cases where H2 blockers remain a cost-effective option.

Primary demand drivers

- GERD and dyspepsia: Use remains steady because symptom-driven therapy is frequent and dosing is simple.

- Over-the-counter (OTC) availability: Where OTC positioning is permitted, it reduces reliance on prescription economics.

- Institutional protocols: Hospitals often stock famotidine for specific prophylaxis and treatment pathways where clinicians prefer H2 blockade versus alternatives.

Secondary demand drivers

- Guideline and formulary fit: Formularies can shift seasonally or protocol-driven.

- Insurance coverage and copay management: These influence patient choice when multiple generics or classes are available.

How did supply shocks reshape financial outcomes in the category?

The famotidine market is historically exposed to supply constraints because:

- many products are produced by limited manufacturing networks for active pharmaceutical ingredient (API) and solid oral forms,

- and multiple generic players rely on similar sourcing structures.

Supply shock pattern

- Tight supply triggers wholesale and retail price increases.

- Higher price enables margin recovery for producers that remain online.

- New supply and normalized production pulls prices back down.

Net effect on financial trajectory

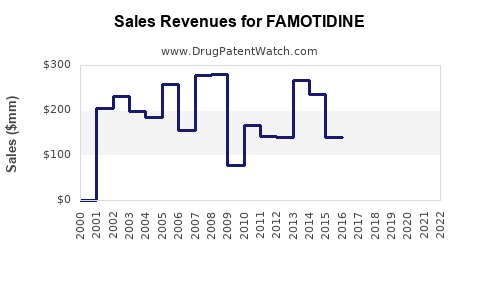

- Revenue can spike during constrained periods due to price lift and constrained demand allocation.

- Profitability can follow supply availability more than demand growth.

- Over longer horizons, sustained revenue growth is limited by generic price compression.

What is the financial trajectory of famotidine in revenue terms?

Famotidine’s long-run financial profile is typically:

- High baseline revenue from volume, but

- Low-to-moderate net pricing once multiple generics compete,

- Intermittent profitability peaks during supply tightness.

Trajectory by horizon

- Short term (months to 1 year): Revenue and operating profit track procurement pricing, wholesaler inventories, and manufacturing continuity.

- Medium term (1 to 3 years): Price normalization dominates. Winners keep share through distribution contracts and consistent supply, while laggards lose share as formulary switching occurs.

- Long term (3+ years): With ongoing generic entry and replacement by alternative classes, category growth tends to be modest and mostly volume-driven.

How do competitor classes influence famotidine’s pricing power?

Famotidine faces two layers of competition:

Within H2 blockers

- Same-class agents compete directly. Market share rotates through small price differences and distribution access.

Cross-class: PPIs and other acid suppression

- PPIs often carry preference in chronic GERD management due to stronger acid suppression.

- In intermittent symptom settings, H2 blockers retain relevance because of lower acquisition cost.

Financial implication

- Famotidine’s ability to hold net price is constrained by therapeutic substitution, especially when payers and formularies steer to lower cost alternatives.

What are the principal levers for market share and financial performance?

For generics, the operational levers matter more than product differentiation.

Key levers

- Contracted distribution and formulary placement (access to institutional buyers)

- API and intermediate sourcing security (continuity reduces fulfillment failures)

- Manufacturing scale and yield (reduces unit cost and stabilizes supply)

- Batch release performance and compliance record (limits volume loss from recalls or delays)

- SKU breadth (20 mg, 40 mg strengths and packaging sizes that match buyer demand)

Expected outcomes

- Firms that maintain consistent supply and price competitiveness usually show steadier revenue.

- Firms that miss manufacturing windows often see revenue drops that do not fully recover because buyers reassign contracted volume.

What do historical financial patterns imply for future profitability?

With generic maturity:

- baseline margins depend on cost position and supply reliability,

- upside is episodic and driven by market tightness,

- downside risk is persistent due to price erosion and alternative class substitution.

Profitability pattern

- Margin expansion during supply constraints and procurement restocking cycles.

- Margin compression as additional generic supply enters or procurement pressure increases.

Strategic constraint

- Long-term profitability is limited by the category’s low differentiation and the regularity of price undercutting among generics.

Key market and financial indicators to track for famotidine

A business-focused investor or R&D operator should watch indicators that directly map to procurement and supply economics.

Category indicators

- Wholesale pricing trends (generic net price movement)

- Inventory levels at wholesalers and large retail chains

- Manufacturing and recall events affecting supply continuity

- Institutional formulary updates (hospital protocol changes)

- Competitive entry timing (new generic launches or expansions)

Operational indicators (company level)

- Fill rate and backorder frequency (supply credibility)

- Unit cost movement (API and conversion costs)

- Batch failure rates and regulatory quality metrics

- Contract renewal outcomes with pharmacy benefit managers and distributors

Market outlook: how will dynamics likely evolve?

The most likely evolution is continuation of the mature generic pattern:

- stable demand for acid suppression in intermittent and cost-sensitive segments,

- persistent downward pressure on net pricing as generic supply stays abundant,

- episodic profitability from supply tightness or contract-driven resets.

Likely directional trends

- Net pricing: broadly downward with occasional spikes during supply constraints.

- Revenue: stable to modestly growing if supply and distribution scale improve.

- Profitability: volatile around supply events; structural margin compression remains the base case.

Key Takeaways

- Famotidine is a mature, generic-led acid-suppression market where pricing power is structurally limited by substitution and procurement behavior.

- Financial trajectory is dominated by supply continuity, contracted pricing, and episodic spikes during market tightness rather than sustained premium revenue growth.

- Long-run performance depends on unit cost position, manufacturing reliability, and distribution access, not formulation innovation.

- Institutional and therapeutic substitution pressures cap durable margin expansion and keep category growth modest.

FAQs

-

Is famotidine’s growth driven by prescription expansion?

No. The market is mature and demand typically tracks volume and procurement allocations more than new patient acquisition.

-

What most affects famotidine pricing in the generic market?

Supply availability and wholesale procurement pricing, with additional downward pressure from ongoing generic competition.

-

Do hospitals prefer famotidine over other acid suppressants?

Usage depends on protocol and formulary decisions. PPIs often dominate chronic GERD management, while H2 blockers persist in specific institutional pathways and cost-sensitive settings.

-

What determines which generic manufacturers win share?

Reliable supply, batch release performance, and contract placement with distributors and institutional buyers.

-

What does the future likely look like for margins?

Margins tend to compress structurally due to price competition, with temporary expansion during supply constraints.

References

[1] U.S. Food and Drug Administration. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. https://www.accessdata.fda.gov/scripts/cder/daf/ (accessed 2026-04-24)

[2] World Health Organization. ATC/DDD Index. https://www.whocc.no/atc_ddd_index/ (accessed 2026-04-24)

[3] National Library of Medicine. PubChem Compound Summary for Famotidine. https://pubchem.ncbi.nlm.nih.gov/ (accessed 2026-04-24)