Last updated: April 24, 2026

How does niacin’s market structure shape pricing, demand, and margins?

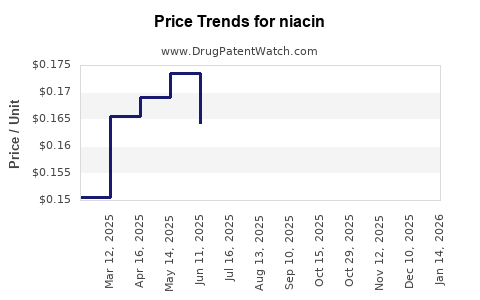

Niacin is a long-established vitamin ingredient and drug compound used across two broad demand streams: (1) lipid modification in cardiometabolic therapy and (2) nutrition and supplement use. Commercial dynamics differ by segment because niacin’s key products are largely commodity-like, with pricing and margin behavior driven by sourcing costs, regulatory posture, and formulation differentiation.

Segment split by market role

- Prescription / lipid-modifying use

- Demand hinges on guideline positioning, tolerability, and clinician preference versus alternative lipid therapies (especially statins and newer lipid agents).

- Niacin’s clinical use has narrowed from broad historic adoption to a more constrained role due to safety and efficacy perceptions versus competing therapies.

- Nutraceutical / nutrition use

- Demand is tied to supplement adoption, ingredient availability, and consumer purchasing cycles.

- Price behavior resembles ingredient markets more than branded pharma, with margin variability linked to supply chain costs and compliance-driven manufacturing capacity.

Competitive and supply dynamics

Niacin is produced and sold as an active ingredient (API) and in multiple dosage forms, which drives a market structure where:

- The API supply base is extensive, lowering switching costs for formulators.

- Formulation differentiation matters more than molecule differentiation (extended-release vs immediate-release, purity specs, and excipient systems).

- Buyer power is high: large formulators and distributors can source multiple qualifying suppliers.

Implication for financial trajectory

Because niacin’s molecule is mature and supply is deep, long-run pricing pressure tends to dominate unless a company holds a differentiated manufacturing position (high-purity, compliant scale, or proprietary controlled-release/combination formulations) or sells through a sustained branded channel with contractual reimbursement dynamics.

What drives demand growth or decline for niacin across geographies and therapy settings?

Prescription demand drivers (lipid modification)

Key demand factors are:

- Guideline and payer posture: reimbursement and guideline inclusion affect utilization rates.

- Safety/tolerability profile: flushing and tolerability determine persistence on therapy and willingness to prescribe.

- Therapeutic competition: statins and other lipid-lowering drug classes have become the default standard of care, limiting niacin’s addressable patient pool.

Net effect: prescription volume is structurally constrained relative to earlier decades, with periodic rebounds tied to specific formulational choices and payer decisions rather than broad adoption.

Nutrition and supplement demand drivers

Key demand factors are:

- Ingredient availability and price: commodity API pricing transmits quickly to finished goods.

- Regulatory and quality standards: GMP manufacturing and supplier qualification matter for downstream brand owners.

- Consumer health trends: cardiometabolic self-care and vitamin consumption patterns influence purchasing.

Net effect: supplement demand can be more resilient than prescription demand during periods when lipid therapy adoption shifts, but it still tracks ingredient pricing and consumer demand elasticity.

How has the regulatory environment influenced niacin’s market participation and product mix?

Drug labeling and use constraints

Niacin has long been used as a lipid-modifying agent. Over time, regulatory scrutiny and updated risk-benefit expectations narrowed preferred use cases. The result is a market where:

- Use is more selective than it used to be.

- Formulation strategy becomes important: companies prioritize extended-release or specific dosing regimens to manage tolerability (where allowed and clinically supported).

GMP and quality standards as a market gate

Even where niacin demand remains, the competitive bar for supply is compliance:

- Finished dose manufacturers and ingredient buyers require validated manufacturing and consistent impurity profiles.

- This tends to concentrate business among producers with proven quality systems, even when commodity pricing remains competitive.

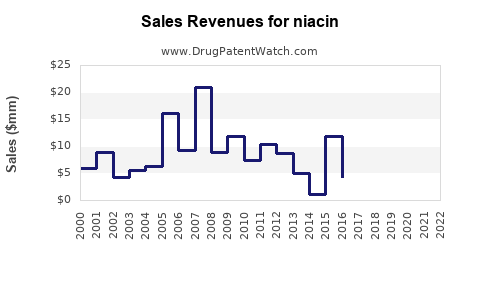

What is the historical financial trajectory implied by niacin’s maturity and typical market behavior?

Niacin’s financial trajectory is best understood as a mix of:

- Stable baseline revenue from broad vitamin/supplement penetration and legacy prescription manufacturing,

- Lower growth ceilings due to limited molecule differentiation and therapy competition,

- Margin compression risks because commodity-grade supply and generic competition are strong.

Typical revenue pattern in mature API vitamin/drug markets

- Revenue growth generally tracks population and supplement market size rather than innovation cycles.

- Price per unit trends toward equilibrium with supply-demand balances.

- Operating margins often depend on:

- Scale and yield (manufacturing efficiency),

- Quality and compliance overhead,

- Formulation complexity (extended-release is costlier than immediate release),

- Contract structure (spot vs long-term supply).

Stage-gate view of the financial curve

- Early / expansion phases: higher pricing power and prescription adoption drove revenue.

- Maturity phases: adoption plateaus; pricing and margin pressure rise from competitors and generics.

- Constrained growth phase: further utilization declines in lipid modification as alternative therapies dominate; growth returns primarily through supplement channels or specialized formulations.

How do product formats affect unit economics for niacin businesses?

Niacin’s economics vary by format, because manufacturing complexity, excipient selection, and dissolution profile controls drive cost and buyer preference.

Common commercial format categories

| Format category |

Primary demand channel |

Margin drivers |

Key risks |

| Immediate-release niacin |

Generic lipid and supplement |

Low manufacturing complexity; supply flexibility |

Higher flushing-related tolerability issues can reduce prescription persistence |

| Extended-release niacin |

Targeted lipid use where appropriate |

Higher formulation value; better tolerance management |

Regulatory and guideline restrictions can still cap uptake |

| Niacin as supplement ingredient |

Nutrition |

Volume scale; formula flexibility |

Commodity pricing pressure; quality and compliance requirements |

Unit economics pattern

- Extended-release can support better pricing versus immediate-release, but market size is smaller and adoption is constrained by clinical preference shifts.

- Supplement-grade niacin is more volume-driven; margin tends to be thin and volatile around commodity pricing.

What role does generic competition and patent status typically play for niacin revenue?

Niacin’s molecule is not in an innovation cycle. For business planning, the practical reality is:

- Generic and contract manufacturing are the dominant routes for supply.

- Revenue growth depends less on patent-protected exclusivity and more on:

- supplier qualification,

- pricing terms,

- and continued presence in downstream branded or store-brand formulations.

That structure limits long-duration high-margin trajectories at the molecule level.

How do payer and clinician dynamics translate into a financial trajectory for niacin-lipid use?

For prescription niacin, financial trajectory is shaped by:

- Share of lipid therapy: as statin and other therapies expand, niacin’s share compresses.

- Switching behavior: clinicians are more likely to stop or avoid niacin when tolerability concerns outweigh perceived incremental benefits.

- Formulary placement: if payers restrict niacin tiers or require prior authorization, volume growth slows and absorbs margin through lower net prices.

Net effect is a prescription revenue base that is typically:

- steady but not expanding fast,

- more sensitive to policy changes than to breakthrough adoption.

What financial performance benchmarks are most relevant to niacin-facing businesses?

For R&D and investment decisions, the metrics that map to niacin’s market reality are:

- Net pricing (per kg API or per unit dose) relative to commodity cycles

- Gross margin spread vs input costs (niacin raw material, conversion yields, QA costs)

- Capacity utilization and batch success rate

- Regulatory compliance costs (batch release, impurity control, ongoing validation)

- Customer concentration and contract terms (long-term supply reduces price volatility exposure)

In mature niacin markets, these metrics generally explain the majority of financial outcomes.

How should businesses model forward financial scenarios for niacin?

A practical scenario model for niacin assumes:

- Prescription segment stays flat-to-declining in utilization with occasional stabilization when formulational positioning and payer coverage align.

- Supplement segment grows with consumer category demand but faces margin pressure when API pricing softens or supply expands.

Forward-looking model structure (directional)

- Base case: stable revenue with modest declines in blended unit margins unless differentiated extended-release volumes scale.

- Downside: commodity oversupply or policy tightening reduces net prices; margin erodes faster than volume can offset.

- Upside: sustained supplier qualification gains and contract-based pricing reduce volatility; extended-release share rises in specific channels.

What actionable takeaways follow for R&D and commercial strategy?

For ingredient/API suppliers

- Win on quality consistency and supply reliability. In commodity-like markets, buyer qualification and batch predictability often decide share.

- Convert pricing risk into stable margins through long-term contracts with volume commitments.

For formulation and dose developers

- Focus differentiation on tolerability engineering (where clinically accepted) and manufacturing robustness rather than molecule-level novelty.

- Target channels where niacin demand still exists with payer and clinician alignment.

For investors

- Treat niacin as a mature, policy- and commodity-driven business profile.

- Upside requires either scale-based cost advantage or a defensible position in formulation/channel mix, not a patent-led growth thesis.

Key Takeaways

- Niacin’s market is split between constrained lipid-modifying prescription demand and broader, more volume-driven supplement/ingredient demand.

- Financial outcomes track commodity pricing, compliance/QA cost control, and contract terms more than innovation cycles.

- Extended-release can improve unit economics, but adoption is still capped by therapy competition and prescribing patterns.

- Long-run growth ceilings are low at the molecule level; durable performance depends on differentiated manufacturing execution and stable customer relationships.

- The most investable angle is often cost-and-quality leadership rather than exclusivity-driven pricing power.

FAQs

-

Is niacin’s prescription market likely to expand materially?

Typically no; lipid therapy competition and tolerability/policy constraints cap growth, leading to flat-to-declining utilization in many settings.

-

Where can niacin companies find the most resilient demand?

The nutrition and supplement channels tend to offer more resilience due to broader consumer adoption and ingredient use.

-

Does extended-release niacin improve economics?

It can support higher pricing than immediate-release, but market size and payer/clinician acceptance still constrain volume upside.

-

What drives volatility in niacin margins?

Input/commodity pricing swings, capacity utilization, and QA release costs are the main margin variables in mature niacin markets.

-

What is the key strategic focus for suppliers?

Sustained GMP compliance, impurity control, yield performance, and contract structures that stabilize net pricing.

References

[1] FDA. (n.d.). Dietary Supplements. U.S. Food & Drug Administration. https://www.fda.gov/food/dietary-supplements

[2] NIH Office of Dietary Supplements. (n.d.). Niacin (Vitamin B3). National Institutes of Health. https://ods.od.nih.gov/factsheets/Niacin-HealthProfessional/

[3] Drugs.com. (n.d.). Niacin Information. https://www.drugs.com/niacin.html