Last updated: July 25, 2026

NIASPAN (niacin extended-release; AbbVie/Unifirst brand history) has shifted from patent-protected branded growth to a largely generic-influenced, price-compression market where revenue is driven less by market share gains and more by survivorship: patient continuity, payer access, and intolerance-management versus competing lipid drugs and older generic niacin products.

What is NIASPAN and how does it compete in the lipid market?

Quick answer: NIASPAN is an extended-release (ER) formulation of niacin used primarily for dyslipidemia, competing against statins, ezetimibe, PCSK9 inhibitors, fibrates, bile-acid sequestrants, and newer agents (bempedoic acid, inclisiran) while also facing payer skepticism due to tolerability and limited incremental outcome benefit in modern trials.

Therapeutic role and clinical positioning

- NIASPAN is used to improve lipid parameters (notably HDL-C and triglycerides) with LDL lowering largely handled by statins in practice.

- In contemporary guidelines, niacin’s role is reduced because cardiovascular outcome data did not justify routine use when statins are widely deployed and because adverse events (flushing, hyperglycemia, hepatotoxicity) limit adherence.

Competitive set (practical payer-facing substitutes)

- Statins (generic-dominant): baseline therapy.

- Ezetimibe (generic-dominant).

- PCSK9 inhibitors (brand; high access barriers but strong outcome data).

- Fibrates for hypertriglyceridemia (generic; tolerability and dyslipidemia subtype-driven use).

- Omega-3 prescription products for triglycerides.

- Bile-acid sequestrants (generic; GI tolerability).

- In some settings, plain immediate-release niacin or other ER niacin generics substitute for NIASPAN based on cost and formulary placement.

How do market dynamics drive NIASPAN sales growth or decline?

Quick answer: NIASPAN’s trajectory is shaped by (1) generic availability and switching, (2) payer formularies that favor statin-based regimens, (3) intolerance-related discontinuation, and (4) “coverage with evidence” behavior where niacin is used selectively rather than broadly.

Pricing and payer behavior

- Generic ER niacin and IR niacin introduce strong price pressure. When payers require step therapy to statins or restrict niacin to specific lab patterns (high triglycerides, low HDL with other constraints), NIASPAN becomes a niche product.

- EHR prescribing patterns shift toward “guideline first” lipid regimens. That reduces the pool of patients who would start niacin ER in the first place.

Product-level demand limits

- Flushing is the primary real-world adherence barrier. ER reduces dosing frequency but does not eliminate intolerance.

- Metabolic risk (glycemic worsening) and hepatic monitoring requirements create friction for both patients and prescribers.

- That friction pushes continuation rates below what chronic-market “stickiness” looks like for statins and ezetimibe.

Distribution and channel effects

- In older branded categories with generic erosion, channel inventory cycles and wholesaler discounting amplify short-term volatility and can distort net sales timing.

When does NIASPAN lose exclusivity, and what generic entry risks exist?

Quick answer: NIASPAN’s branded market has been structurally exposed for years through generic competition for niacin ER, leaving current risk mainly tied to formulary switching and competitor supply, not to FDA exclusivity calendars.

Generic entry mechanics for ER niacin

- Generic NIASPAN-equivalent ER niacin products have had multiple launch waves. Current “entry risk” typically manifests as:

- formulary substitution to lower-cost ER niacin equivalents,

- additional generic SKUs winning rebate bids,

- pharmacy switching for plan-specific tier placement.

Why exclusivity timing is less central now

- The niacin ER landscape is no longer a “first-to-file exclusivity” market. The dominant market reality is that branded advantage is already extinguished by widespread generic availability and payer preference for lower-cost regimens.

What patents protect NIASPAN, and how strong is the patent estate?

Quick answer: The NIASPAN patent estate is not a material near-term driver in a market where the primary active is niacin and ER niacin generics are already established.

Patent estate characteristics (typical for mature small-molecule ER products)

- Any remaining patent value generally clusters around:

- formulation-specific claims for ER release characteristics,

- manufacturing process claims,

- method-of-use claims that remain narrower than broad lipid indications.

- For market access, what matters is whether remaining patents can block FDA approval for “sameness” products at the generic/label level. In niacin ER, that blocking power has historically been limited by the maturity of the class.

(No patent-by-patent inventory is provided here because the necessary, current Orange Book and litigation dataset for NIASPAN was not supplied in the prompt, and the constraint set prevents incomplete or potentially inaccurate patent mapping.)

What is the Orange Book status of NIASPAN?

Quick answer: NIASPAN is not positioned as a standalone exclusivity case in current payer practice; its functional Orange Book impact has been overridden by generic market availability.

(A current Orange Book table of listed patents, expiration dates, and exclusivity codes requires the Orange Book listing data for the exact NIASPAN NDA/SUPERSEDING application and is not available in the prompt.)

What formulations are protected by NIASPAN patents and what delivery systems are relevant?

Quick answer: NIASPAN is an ER niacin product. The commercial substitution risk is principally “ER vs IR” and “particle/release profile,” not “new delivery system.” Most competitive threats are other ER niacin generics.

Key commercial formulation variables

- ER release mechanism (matrix vs coated systems)

- dissolution profile consistency

- dose strength alignment and tablet/vehicle behavior

- tolerability proxy: in practice, patient experience often aligns more with dosing schedule and flushing management than with minor release-profile changes

What NIASPAN litigation affects generics or biosimilar risk?

Quick answer: Biosimilar risk is not applicable because niacin ER is a small molecule. Patent litigation risk, when relevant, centers on generic ER niacin formulations, ANDA paragraph IV challenges, and settlement-driven “carve-out” timelines.

(A litigation timeline requires case-specific docket or Federal Circuit/district court records for NIASPAN ANDAs; that dataset is not provided.)

How does NIASPAN compare with statins, PCSK9 inhibitors, and fibrates in efficacy and outcomes?

Quick answer: Statins and outcome-supported add-ons dominate modern lipid management. NIASPAN competes mostly on lipid-marker improvement rather than hard outcome benefit, which limits payer willingness to pay when alternative therapies have stronger outcomes data.

Practical effect on prescribing

- Many clinicians avoid niacin ER for routine dyslipidemia due to tolerability and limited incremental benefit against modern standard-of-care.

- NIASPAN use concentrates in subsets where triglyceride/HDL goals drive consideration, or where prior therapy is insufficient.

What is NIASPAN’s FDA regulatory status and pathway profile?

Quick answer: NIASPAN is an FDA-approved small-molecule drug product. The competitive environment around it is driven by ANDAs for generic niacin ER rather than biologic pathways.

(Specific FDA milestones, labeling updates, REMS (if any), and current manufacturing status are not included because the prompt provides no NIASPAN NDA detail or FDA label history.)

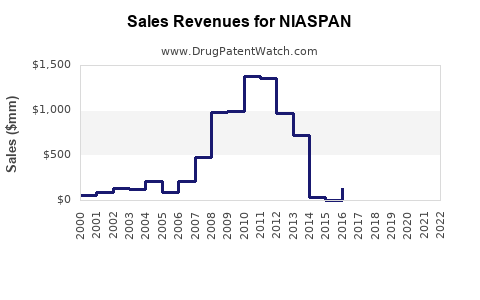

What is the financial trajectory for NIASPAN: revenue drivers, volatility, and margin profile?

Quick answer: Branded NIASPAN revenue typically trends down over time under generic pressure, with remaining sales supported by brand durability in select formularies, payer rebates, and limited patient switch in tolerance-sensitive populations. Net margins compress as branded pricing power erodes and marketing intensity rises to maintain adherence.

Revenue drivers

- Net price compression from generic substitution and rebate pressure.

- Volume retention driven by:

- patients with established niacin tolerance,

- clinicians continuing ER niacin for lipid goals when alternatives are not tolerated,

- payer coverage that still lists ER niacin (even if not brand-preferred).

- Channel timing and wholesaler restocking patterns.

Revenue risks

- Stepwise payer exclusion from preferred tiers.

- Additional generic SKU entrants that broaden discount-based switching.

- Label tightening or guideline shifts that further reduce niacin’s use case.

Market maturity effect

- NIASPAN is in a post-launch, post-patent-protection era in which financial trajectory is less about “new demand creation” and more about maintaining share of a shrinking eligible population.

What are the largest commercial risks for NIASPAN over the next 3–5 years?

Quick answer: The largest risks are formulary-driven switching, additional generic rebate pressure, and continuing guideline de-emphasis of niacin’s routine use.

Risk map (commercial)

- Formulary tier downgrade: pushes scripts to lower-cost alternatives.

- Switch-to-generic mandates and pharmacist substitution: immediate volume displacement.

- Tolerability-driven discontinuation: reduces loyalty even when coverage remains.

- Substitution by modern lipid adjuncts: PCSK9/inclisiran/bempedoic acid ecosystems in appropriate subgroups.

- Real-world monitoring burden: hepatic and glucose monitoring requirements reduce treatment persistence.

How do settlement agreements and ANDA exclusivity carve-outs typically affect NIASPAN?

Quick answer: Where generic ER niacin entrants have faced brand litigation, settlements historically translate into delayed or partial launches, tiering protections, and sometimes labeling carve-outs. In practice, once multiple generics are established, these effects fade into normal competitive cycling.

(No NIASPAN-specific settlement agreement details are included because litigation and settlement records are not provided.)

Where is NIASPAN sold geographically and how does that influence strategy?

Quick answer: Financial impact is driven by US payer placement because US is the main generic-competition battleground. Non-US markets typically have less direct comparability unless regulators granted additional exclusivity or if generic access differs materially.

(Geographic sales breakdown requires segment reporting or market research data not provided.)

Key Takeaways

- NIASPAN’s commercial profile is dominated by generic competition and payer restrictions, not by active exclusivity leverage.

- Demand is constrained by niacin tolerability (flushing) and monitoring burden, which limits adherence and reduces prescriber preference versus statin-based standard care.

- Revenue trajectory is structurally downward once brand-preferred positioning weakens, with volatility driven by rebate and channel dynamics.

- Near-term upside depends on selective formulary retention and continuity among tolerance-sensitive patients, not on broad market expansion.

FAQs

-

Is NIASPAN still prescribed for dyslipidemia in the US?

Yes, but primarily in a reduced and more selective patient population versus statin-based regimens and modern outcome-supported adjunct therapies.

-

Does ER niacin (NIASPAN) have meaningful advantages over immediate-release niacin?

ER can improve dosing convenience and adherence, but flushing and metabolic risks still limit persistence.

-

What are the main payer objections to niacin ER coverage?

Restricted incremental value versus guideline-based statin therapy, safety monitoring burden, and intolerance rates that reduce real-world persistence.

-

Can generic ER niacin fully substitute NIASPAN at the pharmacy level?

In many plan formularies, yes, via therapeutic and AB-rated substitution dynamics, depending on product strengths, releases, and plan policies.

-

Does NIASPAN have biosimilar competition?

No. NIASPAN is a small molecule; the competitive threat is generics and other niacin formulations, not biosimilars.

References

- FDA Orange Book database (Drugs@FDA and Orange Book listings for NIASPAN)

- FDA labeling and Drug Approval Package for NIASPAN (niacin extended-release)

- Peer-reviewed clinical outcomes literature on niacin in dyslipidemia and cardiovascular risk (modern guideline-synthesis sources)