Daptomycin - Generic Drug Details

✉ Email this page to a colleague

What are the generic sources for daptomycin and what is the scope of patent protection?

Daptomycin

is the generic ingredient in five branded drugs marketed by Cubist Pharms Llc, Accord Hlthcare, Aspiro, Be Pharms, Biocon Pharma, Dr Reddys, Eugia Pharma, Fresenius Kabi Usa, Hainan Poly Pharm, Hangzhou Zhongmei, Hengrui Pharma, Hikma, Hisun Pharm Hangzhou, Hospira, Maia Pharms Inc, Meitheal, Mylan, Mylan Labs Ltd, Qilu Pharm Hainan, Sagent Pharms Inc, Teva Pharms Usa, Xellia Pharms Aps, and Baxter Hlthcare Corp, and is included in thirty-two NDAs. There are seven patents protecting this compound and one Paragraph IV challenge. Additional information is available in the individual branded drug profile pages.Daptomycin has ninety-seven patent family members in thirty-eight countries.

There are ten drug master file entries for daptomycin. Twenty-six suppliers are listed for this compound. There is one tentative approval for this compound.

Summary for daptomycin

| International Patents: | 97 |

| US Patents: | 7 |

| Tradenames: | 5 |

| Applicants: | 23 |

| NDAs: | 32 |

| Drug Master File Entries: | 10 |

| Finished Product Suppliers / Packagers: | 26 |

| Raw Ingredient (Bulk) Api Vendors: | 48 |

| Clinical Trials: | 94 |

| Patent Applications: | 4,355 |

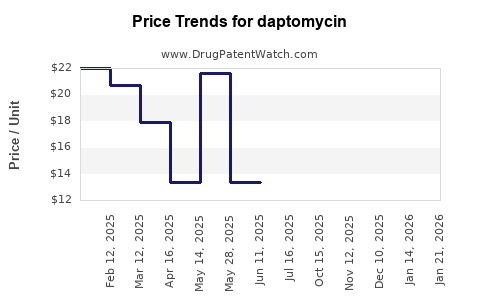

| Drug Prices: | Drug price trends for daptomycin |

| Patent Litigation and PTAB cases: | See patent lawsuits and PTAB cases for daptomycin |

| What excipients (inactive ingredients) are in daptomycin? | daptomycin excipients list |

| DailyMed Link: | daptomycin at DailyMed |

Recent Clinical Trials for daptomycin

Identify potential brand extensions & 505(b)(2) entrants

| Sponsor | Phase |

|---|---|

| University Clinical Hospital na V.V.Vinogradov (branch of RUDN university na Patrice Lumumba) | PHASE3 |

| The Peter Doherty Institute for Infection and Immunity | PHASE4 |

| Todd C. Lee MD MPH FIDSA | PHASE4 |

Generic filers with tentative approvals for DAPTOMYCIN

| Applicant | Application No. | Strength | Dosage Form |

| ⤷ Start Trial | ⤷ Start Trial | 350MG/VIAL | POWDER;INTRAVENOUS |

The 'tentative' approval signifies that the product meets all FDA standards for marketing, and, but for the patents / regulatory protections, it would approved.

Pharmacology for daptomycin

| Drug Class | Lipopeptide Antibacterial |

Medical Subject Heading (MeSH) Categories for daptomycin

Anatomical Therapeutic Chemical (ATC) Classes for daptomycin

Paragraph IV (Patent) Challenges for DAPTOMYCIN

| Tradename | Dosage | Ingredient | Strength | NDA | ANDAs Submitted | Submissiondate |

|---|---|---|---|---|---|---|

| CUBICIN RF | For Injection | daptomycin | 500 mg/vial | 021572 | 1 | 2008-11-19 |

US Patents and Regulatory Information for daptomycin

| Applicant | Tradename | Generic Name | Dosage | NDA | Approval Date | TE | Type | RLD | RS | Patent No. | Patent Expiration | Product | Substance | Delist Req. | Exclusivity Expiration |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Cubist Pharms Llc | CUBICIN | daptomycin | POWDER;INTRAVENOUS | 021572-002 | Sep 12, 2003 | DISCN | Yes | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | ||||

| Mylan | DAPTOMYCIN | daptomycin | POWDER;INTRAVENOUS | 213966-001 | Aug 7, 2023 | AP | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| Xellia Pharms Aps | DAPTOMYCIN | daptomycin | POWDER;INTRAVENOUS | 206005-001 | Jun 15, 2016 | AP | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| Hisun Pharm Hangzhou | DAPTOMYCIN | daptomycin | POWDER;INTRAVENOUS | 212250-001 | Apr 21, 2021 | AP | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| Dr Reddys | DAPTOMYCIN | daptomycin | POWDER;INTRAVENOUS | 208375-001 | May 1, 2019 | AP | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| >Applicant | >Tradename | >Generic Name | >Dosage | >NDA | >Approval Date | >TE | >Type | >RLD | >RS | >Patent No. | >Patent Expiration | >Product | >Substance | >Delist Req. | >Exclusivity Expiration |

Expired US Patents for daptomycin

| Applicant | Tradename | Generic Name | Dosage | NDA | Approval Date | Patent No. | Patent Expiration |

|---|---|---|---|---|---|---|---|

| Cubist Pharms Llc | CUBICIN | daptomycin | POWDER;INTRAVENOUS | 021572-001 | Sep 12, 2003 | ⤷ Start Trial | ⤷ Start Trial |

| Cubist Pharms Llc | CUBICIN | daptomycin | POWDER;INTRAVENOUS | 021572-002 | Sep 12, 2003 | ⤷ Start Trial | ⤷ Start Trial |

| Cubist Pharms Llc | CUBICIN | daptomycin | POWDER;INTRAVENOUS | 021572-002 | Sep 12, 2003 | ⤷ Start Trial | ⤷ Start Trial |

| Cubist Pharms Llc | CUBICIN | daptomycin | POWDER;INTRAVENOUS | 021572-001 | Sep 12, 2003 | ⤷ Start Trial | ⤷ Start Trial |

| Cubist Pharms Llc | CUBICIN | daptomycin | POWDER;INTRAVENOUS | 021572-001 | Sep 12, 2003 | ⤷ Start Trial | ⤷ Start Trial |

| >Applicant | >Tradename | >Generic Name | >Dosage | >NDA | >Approval Date | >Patent No. | >Patent Expiration |

EU/EMA Drug Approvals for daptomycin

| Company | Drugname | Inn | Product Number / Indication | Status | Generic | Biosimilar | Orphan | Marketing Authorisation | Marketing Refusal |

|---|---|---|---|---|---|---|---|---|---|

| Pfizer Europe MA EEIG | Daptomycin Hospira | daptomycin | EMEA/H/C/004310Daptomycin is indicated for the treatment of the following infections.Adult and paediatric (1 to 17 years of age) patients with complicated skin and soft-tissue infections (cSSTI).Adult patients with right-sided infective endocarditis (RIE) due to Staphylococcus aureus. It isrecommended that the decision to use daptomycin should take into account the antibacterial susceptibility of the organism and should be based on expert advice.Adult and paediatric (1 to 17 years of age) patients with Staphylococcus aureus bacteraemia (SAB).In adults, use in bacteraemia should be associated with RIE or with cSSTI, while in paediatric patients, use in bacteraemia should be associated with cSSTI.Daptomycin is active against Gram positive bacteria only. In mixed infections where Gram negative and/or certain types of anaerobic bacteria are suspected, daptomycin should be co-administered with appropriate antibacterial agent(s).Consideration should be given to official guidance on the appropriate use of antibacterial agents. | Authorised | yes | no | no | 2017-03-22 | |

| Merck Sharp & Dohme B.V. | Cubicin | daptomycin | EMEA/H/C/000637Cubicin is indicated for the treatment of the following infections.Adult and paediatric (1 to 17 years of age) patients with complicated skin and soft-tissue infections (cSSTI).Adult patients with right-sided infective endocarditis (RIE) due to Staphylococcus aureus.It is recommended that the decision to use daptomycin should take into account the antibacterial susceptibility of the organism and should be based on expert advice.Adult and paediatric (1 to 17 years of age) patients with Staphylococcus aureus bacteraemia (SAB). In adults, use in bacteraemia should be associated with RIE or with cSSTI, while in paediatric patients, use in bacteraemia should be associated with cSSTI.Daptomycin is active against Gram positive bacteria only. In mixed infections where Gram negative and/or certain types of anaerobic bacteria are suspected, Cubicin should be co-administered with appropriate antibacterial agent(s). Consideration should be given to official guidance on the appropriate use of antibacterial agents. | Authorised | no | no | no | 2006-01-19 | |

| >Company | >Drugname | >Inn | >Product Number / Indication | >Status | >Generic | >Biosimilar | >Orphan | >Marketing Authorisation | >Marketing Refusal |

International Patents for daptomycin

| Country | Patent Number | Title | Estimated Expiration |

|---|---|---|---|

| Australia | 2013316779 | ⤷ Start Trial | |

| Australia | 2018217322 | ⤷ Start Trial | |

| Brazil | 112015005400 | ⤷ Start Trial | |

| Canada | 2884484 | ⤷ Start Trial | |

| Chile | 2015000608 | ⤷ Start Trial | |

| >Country | >Patent Number | >Title | >Estimated Expiration |

Supplementary Protection Certificates for daptomycin

| Patent Number | Supplementary Protection Certificate | SPC Country | SPC Expiration | SPC Description |

|---|---|---|---|---|

| 1115417 | 06C0022 | France | ⤷ Start Trial | PRODUCT NAME: DAPTOMYCINE; REGISTRATION NO/DATE: EU/1/05/328/001-002 20060119 |

| 1115417 | 22/2006 | Austria | ⤷ Start Trial | PRODUCT NAME: DAPTOMYCIN; REGISTRATION NO/DATE: EU/1/05/328/001 UND 002 20060119 |

| 1115417 | CA 2006 00018 | Denmark | ⤷ Start Trial | PRODUCT NAME: DAPTOMYCIN |

| 1115417 | SZ 22/2006 | Austria | ⤷ Start Trial | PRODUCT NAME: DAPTOMYCIN |

| 1115417 | SPC/GB06/024 | United Kingdom | ⤷ Start Trial | SUPPLEMENTARY PROTECTION CERTIFICATE NO SPC/GB06/024 GRANTED TO CUBIST PHARMACEUTICALS, INC IN RESPECT OF THE PRODUCT DAPTOMYCIN, THE GRANT OF WHICH WAS ADVERTISED IN JOURNAL NO 6162 DATED 27 JUNE 2007 HAS HAD ITS MAXIMUM PERIOD OF DURATION CORRECTED, SUBJECT TO THE PAYMENT OF THE PRESCRIBED FEES IT WILL EXPIRE ON 22 JANUARY 2021. |

| >Patent Number | >Supplementary Protection Certificate | >SPC Country | >SPC Expiration | >SPC Description |

More… ↓

Make Better Decisions: Try a trial or see plans & pricing

Drugs may be covered by multiple patents or regulatory protections. All trademarks and applicant names are the property of their respective owners or licensors. Although great care is taken in the proper and correct provision of this service, thinkBiotech LLC does not accept any responsibility for possible consequences of errors or omissions in the provided data. The data presented herein is for information purposes only. There is no warranty that the data contained herein is error free. We do not provide individual investment advice. This service is not registered with any financial regulatory agency. The information we publish is educational only and based on our opinions plus our models. By using DrugPatentWatch you acknowledge that we do not provide personalized recommendations or advice. thinkBiotech performs no independent verification of facts as provided by public sources nor are attempts made to provide legal or investing advice. Any reliance on data provided herein is done solely at the discretion of the user. Users of this service are advised to seek professional advice and independent confirmation before considering acting on any of the provided information. thinkBiotech LLC reserves the right to amend, extend or withdraw any part or all of the offered service without notice.

ISSN: 2162-2639

Privacy and Cookies

Terms & Conditions

Site Map

DrugPatentWatch Alternatives

LOE / Major Patent Expirations 2026 - 2027

NCE-1 Patent Challenge Dates 2026 - 2027

Friedman, Yali. "DrugPatentWatch" DrugPatentWatch, thinkBiotech, 2026, www.DrugPatentWatch.com.

See Primary Research Papers Citing DrugPatentWatch